Key Market Highlights

- Japanese equities tumbled sharply, with the Nikkei 225 dropping as much as 6.9% and the TOPIX falling up to 5.7%, as investors reacted to surging oil prices, escalating Middle East tensions, and weak U.S. employment data.

- Asian markets traded cautiously while oil prices remained volatile amid uncertainty over shipping through the Strait of Hormuz. Investors are also watching a series of upcoming central bank meetings for signals on inflation. On Wall Street, attention is turning to Jensen Huang’s AI conference at Nvidia, while the U.S. dollar eased slightly from recent highs but stayed near key technical levels.

- Oil prices fluctuated, with Brent crude trading around $105 per barrel and West Texas Intermediate near $99, after surging more than 40% over the past two weeks. The rally followed a U.S. strike on Iran’s Kharg Island, the country’s main oil export hub, and retaliatory Iranian attacks on Israel and several Arab states.

- The International Energy Agency indicated that strategic oil reserves could soon be released to markets. Meanwhile, Donald Trump rejected ceasefire negotiations and called on nations to help reopen the Strait of Hormuz to global shipping.

- Bond investors are debating the inflation outlook, weighing whether the Iran-war-driven oil shock will sustain inflation pressures or eventually lead to slower growth. Some strategists warn that markets may be underestimating that risk, favoring bullish bond strategies such as long positions in short-term rates that anticipate deeper Federal Reserve rate cuts than currently priced in.

- U.S. stock futures edged higher on Sunday night, with Dow Jones Industrial Average, S&P 500, and Nasdaq Composite futures all posting modest gains. U.S. crude briefly climbed above $100 per barrel before retreating, while economic data from China came in stronger than expected.

- U.S. equities declined for a third consecutive week as the Iran conflict entered its second full week. All three major indexes lost more than 1% again and hovered near their 2026 lows amid volatile markets and sharply rising oil prices.

U.S. Economic Data and Earnings Calendar

Investors will look for clearer signals next week on how the Middle East conflict may be altering expectations for interest-rate cuts this year, as policymakers at the Federal Reserve meet for the first time since U.S. and Israeli airstrikes on Iran roughly two weeks ago. The escalation pushed oil prices sharply higher and triggered volatility across global markets.

Comments from Fed Chair Jerome Powell following the policy decision will be closely monitored, as they could highlight divisions within the Federal Open Market Committee. Some officials support deeper rate cuts amid signs of labor-market weakness, while others remain concerned about persistent inflation. The press conference may also be Powell’s second-to-last before his term concludes in May.

Also on Wednesday, the February Producer Price Index will provide insight into wholesale inflation after January’s stronger-than-expected increase. Meanwhile, upcoming reports on new and pending home sales will be examined for indications of recovery in the U.S. housing market.

Economic Calendar

Monday, March 16

- February Industrial Production and Capacity Utilization data

- March Empire State Manufacturing Survey

- March Homebuilder Confidence

Tuesday, March 17

- February Pending Home Sales

Wednesday, March 18

- Federal Open Market Committee interest-rate decision

- Press conference by Jerome Powell, chair of the Federal Reserve

- February Producer Price Index

- January Factory Orders

Thursday, March 19

- January New Home Sales

- Weekly Initial Jobless Claims (week ending Mar. 14)

- March Philadelphia Fed Manufacturing Index

- January Wholesale Inventories

Friday, March 20

Xpeng (NYSE:XPEV)

Micron Technology (NASDAQ: MU) is set to report earnings after its stock surged more than fourfold over the past year amid the AI boom. The memory-chip maker posted a 60% year-over-year jump in revenue last quarter and exceeded profit expectations.

FedEx (NYSE: FDX) will release quarterly results on Thursday. Its shares have climbed nearly 25% this year, and investors will look for signals on global shipping trends and the health of the broader economy.

Results from Dollar Tree (NASDAQ: DLTR) are expected to provide further insight into U.S. consumer spending after the retailer previously noted that customers were feeling financially “stretched.” Earnings from General Mills, Lululemon Athletica, and Macy’s will also offer a clearer view of consumer demand.

Nuclear-energy startup Oklo is scheduled to report earnings as well, after announcing earlier this year a deal to supply power for data centers operated by Meta Platforms.

Meanwhile, Alibaba Group, China’s largest technology company, will post earnings as it accelerates investment in artificial intelligence. Chinese EV maker XPeng, a global competitor to Tesla, is also due to report.

Alibaba is reportedly preparing to launch an enterprise-focused agentic AI service built on its Qwen model by the DingTalk team, potentially as soon as this week. The company plans to gradually integrate the service with platforms such as Taobao and Alipay, aiming to capitalize on growing demand for AI assistants capable of performing complex tasks.

Technical Analysis

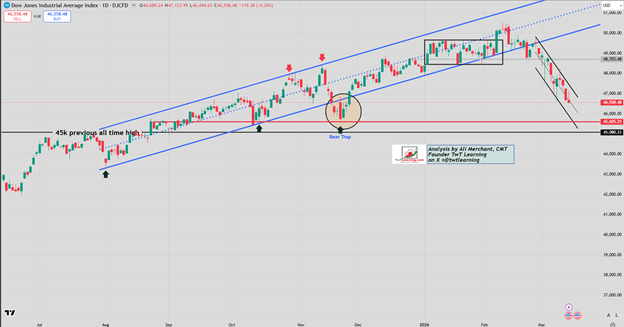

Dow Jones Industrial Average (DJIA) Index

The DJIA has broken below its long-term uptrend that began in August 2025 and is now trading within a downward-sloping channel, signaling a potential shift in short-term momentum.

- Key support: 46,430

- Next downside target: Around 45,770 if the index breaks decisively below support.

- Short-term rebound level: A corrective bounce toward 47,000 remains possible as long as 46,430 holds.

In technical terms, the market is currently testing a critical support zone. Holding above it could trigger a temporary recovery, while a breakdown would likely accelerate downside pressure within the bearish channel.

DJIA Daily Candlestick Chart

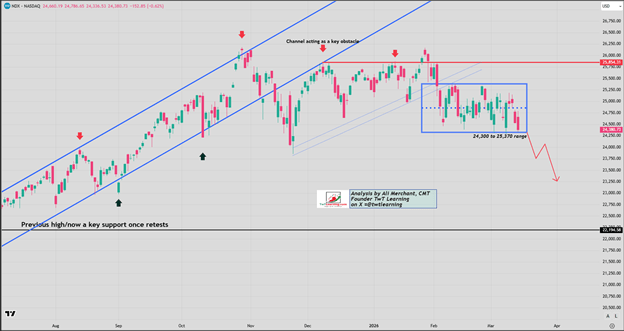

Nasdaq‑100

The Nasdaq-100 is currently moving within a rectangular trading range between 24,300 and 25,370, with 24,860 acting as the midpoint pivot that helps define near-term direction.

- Key support: 24,300

- Midpoint resistance/pivot: 24,860

- Upper range resistance: 25,370

A Monday 9:30 a.m. ET open below 24,300 would signal a bearish breakout from the range.

Downside targets if the breakdown occurs:

- 23,800

- 23,250

If support holds, the index is likely to continue consolidating within the lower portion of the range, trading roughly between 24,300 and 24,860 in the near term.

NDX Daily Candlestick Chart

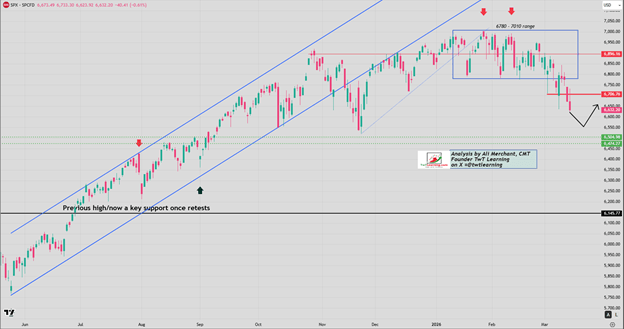

SPX (S&P500) Index

The S&P 500 has broken below a rectangular consolidation pattern, signaling the start of a bearish move in the near term.

- Primary support zone: 6,550 – 6,520

- Key resistance: 6,670 – 6,680

A temporary corrective rebound toward 6,660–6,680 remains possible. However, this resistance area needs to hold firmly to maintain the bearish outlook.

If the index fails to reclaim this resistance zone, downside momentum could continue toward the 6,550–6,520 support range.

SPX Daily Candlestick Chart

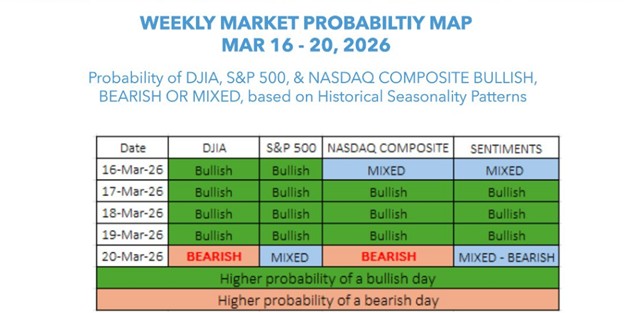

Weekly Probability Outlook for Major U.S. Stock Indices

The U.S. weekly market probability map for March 16–20, 2026 indicates that historically, major U.S. indices tend to begin the week with mixed performance, followed by a three-day rally, before shifting to a mixed-to-bearish tone toward the end of the week.

This outlook applies broadly to benchmarks such as the S&P 500, Nasdaq-100, and Dow Jones Industrial Average.

The probability maps are constructed from historical seasonality trends, analyzing how markets have typically behaved during the same calendar period in past years. Sentiment readings in the model are generated through a seasonality-based scoring framework, which evaluates historical performance patterns to estimate the likely directional bias for the week.

Sources: Ali Merchant

Leave a comment