Passive Investing Shapes Market Flows

In a market dominated by passive strategies, investment decisions are often detached from traditional valuation metrics, which blurs the distinctions between classic styles such as value and growth.

Passive investors are commonly associated with broad market index funds tracking benchmarks like the S&P 500 or the Nasdaq. Yet passive capital also flows into sector- or factor-focused ETFs, including funds targeting areas such as consumer staples or large-cap growth.

While “passive” refers to not selecting individual stocks, it does not necessarily mean the investment behavior itself is passive. Increasingly, investors in passive vehicles actively trade themes and narratives, shifting capital between popular sectors and strategies.

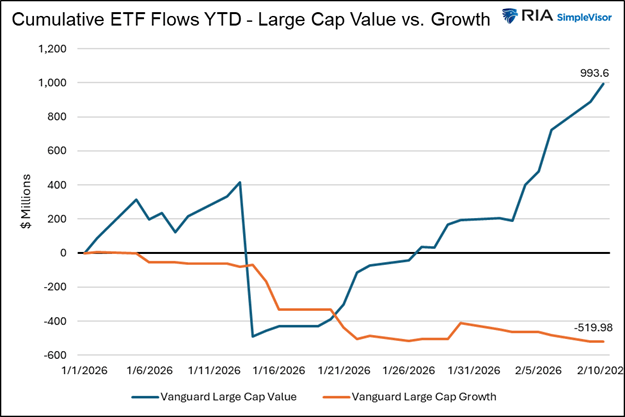

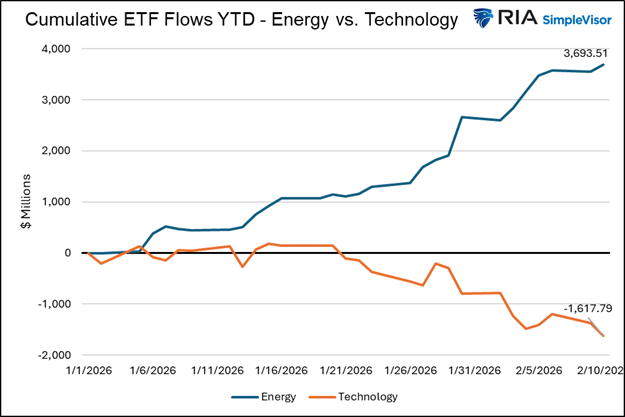

For example, in recent months, stocks within large-value ETFs have gained popularity, while the once-favored mega-cap technology names have lost momentum. This rotation is clearly visible in the diverging performance of value and growth ETFs and sectors, as well as in the inflows and outflows among the largest exchange-traded funds.

The first chart below highlights the sharp contrast in capital flows between the Vanguard Value ETF and the iShares Russell 1000 Growth ETF.

The second chart illustrates an even wider divergence in flows between the Energy Select Sector SPDR Fund and the Technology Select Sector SPDR Fund.

All flow data presented in the charts is sourced from ETF.com.

The Value Rotation Narrative

Financial media has been heavily focused on the apparent shift from “expensive” growth stocks into supposedly “cheaper” value stocks. However, as discussed in Part One, investors are largely responding to a narrative. In many cases, market participants believe they are buying value when they are actually selling it.

The value-rotation story generally goes like this: high-beta, mega-cap growth stocks have already enjoyed strong gains and now appear overvalued and risky. As a result, investors assume the logical move is to rotate into the opposite segment of the market—smaller-cap, lower-priced, and traditionally “value” sectors.

Whether or not this reasoning is accurate, the narrative itself is influencing markets, sectors, and factor performance. Even if many so-called value ETFs do not truly represent value, capital flows continue to follow the story until investor sentiment eventually shifts.

When narratives diverge from underlying fundamentals, however, distortions can emerge. For that reason, active investors must recognize the influence of prevailing narratives while also identifying genuine value opportunities—because eventually the market tends to reward them.

Why Traditional Screens Often Miss True Value

Most value investors start their search with quantitative screens that filter for metrics such as low price-to-earnings ratios, high dividend yields, or low price-to-book multiples. While these indicators are helpful starting points, they should not be treated as definitive conclusions. Frequently, they only highlight companies that appear inexpensive on the surface.

In reality, “cheap” valuation metrics can sometimes reflect underlying problems rather than attractive opportunities. For example:

- Earnings could be cyclical and currently near their peak.

- The company’s business model may be weakening.

- Management execution might be inconsistent.

- Emerging legal, political, or structural challenges could be affecting the outlook.

Many screening models—particularly those that rely on historical data rather than forward-looking estimates—struggle to differentiate between companies that are truly undervalued and those that are simply in decline. As a result, investors often mistake statistical cheapness for genuine value.

A Forward-Looking Framework

To properly assess value, investors should evaluate companies through several valuation perspectives. Each perspective addresses a different aspect of a company’s fundamentals, and when all three point in the same direction, the likelihood of identifying genuine value opportunities increases.

These perspectives focus on the past, present, and future. Investors should ask: Does the company have a strong earnings history? Is it currently performing well? And does it have solid prospects for future growth? Just as important as earnings themselves is how the current share price compares with past results, current performance, and expected future earnings.

Past Earnings

The first step is determining whether the stock appears expensive based on its recent financial performance. Measures such as trailing price-to-earnings ratios, free cash flow yield, and profit margins help investors evaluate valuation relative to earnings and cash flow generated over the past year or two.

One-Year Forward Earnings

Forward-looking estimates are often more informative than historical metrics—but only when those projections are credible. As the legendary investor Benjamin Graham once advised, investors should limit forecasts to what can reasonably be anticipated.

Businesses with stable financial trends, durable competitive advantages, and consistent management execution generally deserve greater confidence than companies reliant on optimistic projections, uncertain economic scenarios, or speculative growth stories.

Growth-Adjusted Valuations

As discussed earlier, both trailing and forward P/E ratios can appear elevated if earnings growth is expected to accelerate. For that reason, investors often incorporate the PEG ratio, which compares valuation multiples with anticipated growth rates.

This third layer is frequently absent from many screening approaches. It is also the most challenging to evaluate, since small adjustments to growth expectations can significantly influence whether a stock qualifies as a genuine value opportunity.

Applying the Framework

In Part One, we highlighted that companies such as Walmart and Costco—often perceived as classic value names—are not necessarily inexpensive.

Applying the three-tier framework shows that Walmart, for example, trades at a P/E ratio of 46, a forward P/E of 43, and a PEG ratio of 4.50, indicating a relatively high valuation across all three measures.

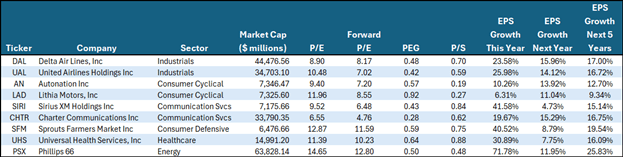

To help investors identify companies that may represent genuine value rather than merely appearing inexpensive, we developed a screening process. The companies that emerge from this screen combine relatively low valuations with solid earnings prospects and growth expectations that justify their current prices. While these stocks may better resemble true value opportunities in today’s market, they still carry risks.

The screen included the following criteria:

- Market capitalization above $5 billion

- U.S.-listed companies

- P/E ratio

- Forward P/E ratio

- PEG ratio

- Price-to-sales ratio

- Quick ratio

Beyond the three primary valuation lenses, we also incorporated the price-to-sales ratio to reinforce the valuation assessment and the quick ratio to gauge a company’s short-term liquidity. Financial companies were excluded from the analysis because their earnings structures differ significantly from those of most other industries, making direct comparisons less meaningful.

Why True Value Often Gets Overlooked

Market outcomes are shaped not only by fundamentals but also by investor psychology and industry incentives. Many professional portfolio managers prefer to hold widely owned stocks because straying too far from benchmark indices can create career risk. Meanwhile, passive investment vehicles allocate capital according to index weightings that loosely align with their mandates, which naturally directs more money toward the largest and most established companies. Financial media narratives can further reinforce this dynamic by highlighting popular themes that attract even more capital to the same group of stocks.

These forces often create a self-reinforcing cycle: popular companies draw new inflows, rising prices follow, and the higher prices then attract additional investment. Companies that fall outside the spotlight frequently face the opposite pattern—even when their earnings and financial positions remain solid. As a result, the valuation gap between favored companies and overlooked ones can widen significantly.

For example, the companies identified in our screen generally represent only small positions in widely held ETFs. Phillips 66, the largest firm in the screen, represents just 3.78% of the Energy Select Sector SPDR Fund. Delta Air Lines and United Airlines—the next-largest companies—account for only 0.86% and 0.67% of the Industrial Select Sector SPDR Fund respectively. Their weights are even smaller in the large-cap value ETF Vanguard Value ETF.

The Value Trap

A common misconception in investing is that a stock that looks “cheap” automatically qualifies as a value investment. In reality, one of the riskiest situations is when a stock appears inexpensive but lacks the earnings strength, growth potential, or stability needed to justify its low valuation.

Take the airline sector as an example. Both Delta Air Lines and United Airlines appear in our screen as potential value candidates. However, their revenue prospects are highly sensitive to economic conditions and jet fuel prices. In addition, a meaningful share of their profits comes from airline credit card reward partnerships. If the economy slows, forecasts for strong double-digit earnings growth may prove unrealistic.

Rising jet fuel costs also pose an important question: can airlines pass those higher costs on to consumers? Another uncertainty is whether increasing competition from newer financial service providers could pull customers away from airline rewards cards tied to networks such as Visa and Mastercard.

Ultimately, genuine value investing requires both a reasonable price and credible earnings prospects. The stronger the investor’s confidence in a company’s future earnings growth, the higher the likelihood that a value investment will succeed.

Summary

Identifying true value has always been challenging, but the rise of passive investing has made the task even more difficult. Many investors today purchase “value” in name only, often through ETFs labeled with the term. These funds attract capital from investors seeking value exposure, yet fewer participants are actively searching for genuinely undervalued companies.

This dynamic can lead to a wide divergence between stocks perceived as value and those that truly offer value. Over time, such market distortions can create compelling opportunities—though investors must remain patient while waiting for those valuation gaps to eventually close.

Sources: Michael Lebowitz

Leave a comment