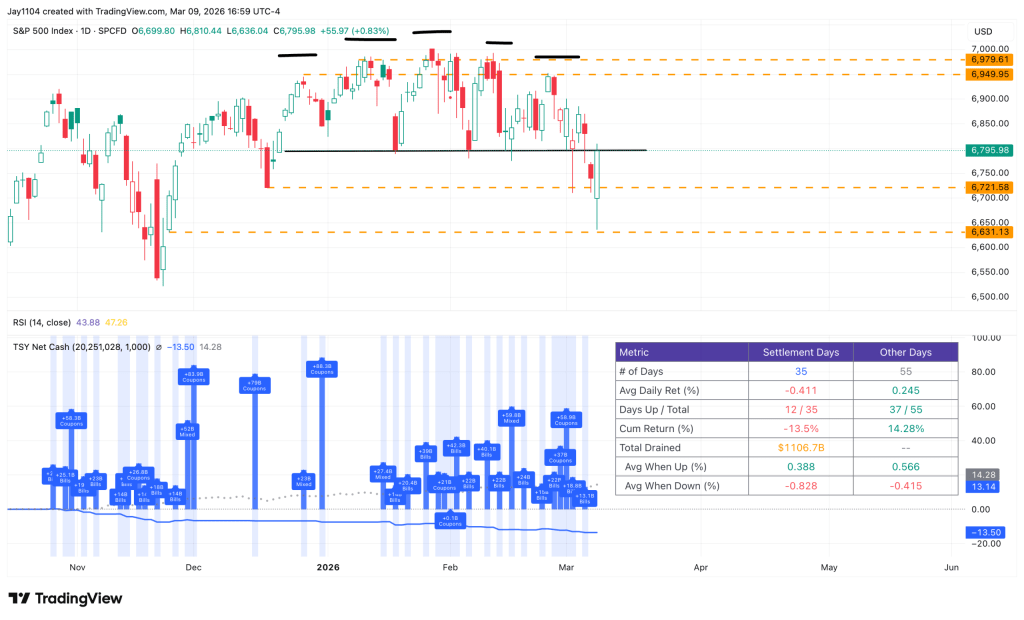

Stocks dropped sharply at Monday’s open but, as anticipated, recovered steadily throughout the session as volatility began to fade. Sentiment improved further later in the day after headlines suggested the war could end soon.

From a bullish perspective, however, one key challenge remains. Today marks the settlement of roughly $15 billion in Treasury bills. Historical data indicates that markets rise only about one-third of the time on settlement days, while in roughly two-thirds of cases equities tend to decline.

It is still possible that elevated volatility overrides the typical settlement pattern, allowing the market to post a modest gain of around 40 to 50 basis points. Even so, the historical analysis has generally proven reliable.

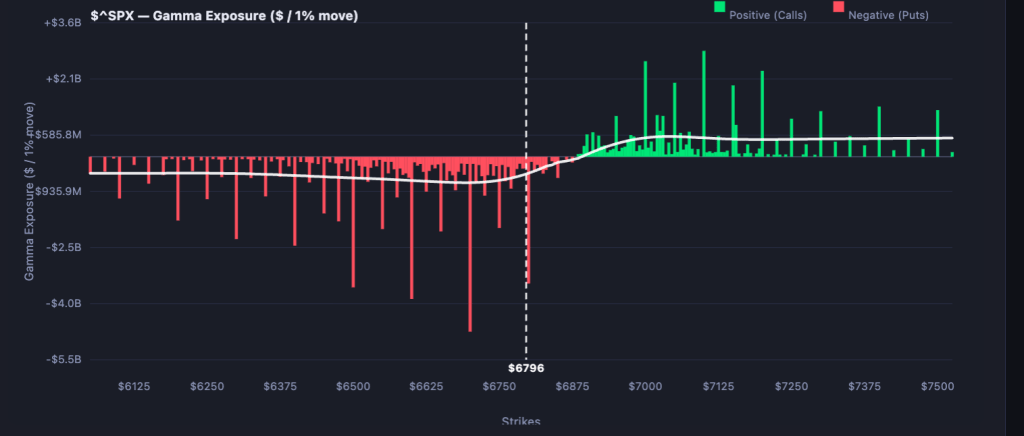

From both an options-market and technical-analysis standpoint, 6,800 is a key level. If the SPX moves above it, the index could quickly advance toward 6,900, which corresponds to the zero gamma level.

Another concern is that the USD/JPY cross-currency basis has been turning more negative, pointing to tighter dollar liquidity. This comes on top of signals from the Treasury settlement data. Overall, the liquidity situation hasn’t improved much so far and may even be slightly worse.

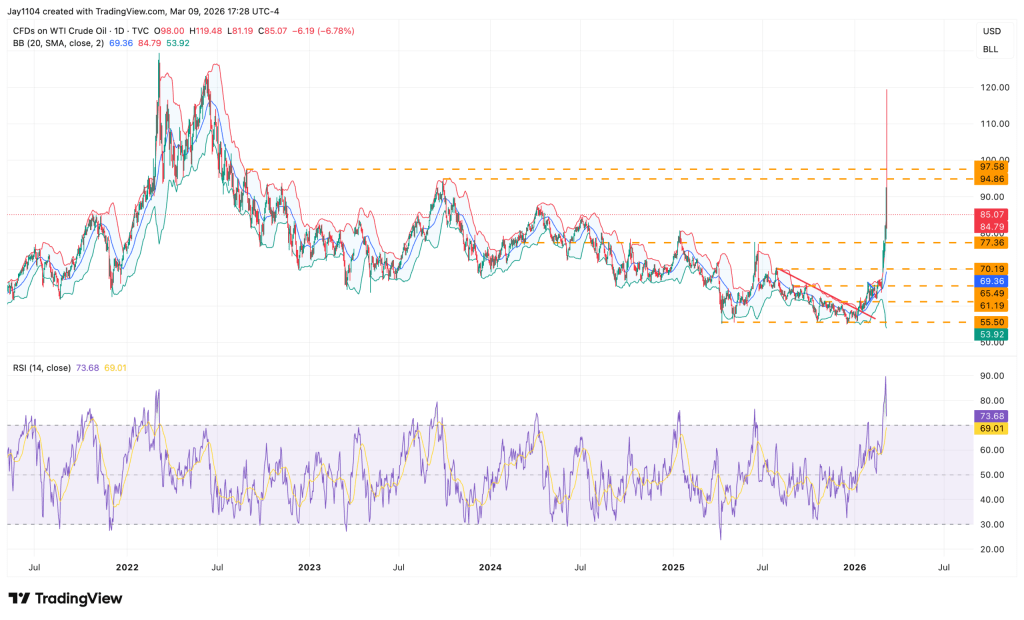

That said, the cross-currency basis could widen if markets begin to believe oil prices will stabilize or decline. For now, however, the outlook remains uncertain and difficult to call.

Oil had clearly become overbought, trading above its upper Bollinger Band while the RSI was above 70. There also appears to be solid support near the $80 level. While prices could decline further, a return to the $60 range in the near term seems unlikely.

Oil at $80 is certainly preferable to $100, but it is still significantly higher than $60. A $20 jump in prices represents more than a 33% increase, which is unlikely to be favorable for the upcoming CPI report or for consumers paying at the gas pump.

Sources: Michael Kramer

Leave a comment