Key Takeaways

U.S. large-cap stocks slipped to multi-month lows this week as oil prices surged, although dip buyers quickly stepped in. A modest rotation across sectors is giving bulls some optimism ahead of upcoming earnings releases and key economic data. Meanwhile, potential distribution in SPY and consolidation in the U.S. dollar could serve as important signals for market direction.

As the week progresses, traders may finally shift their attention away from geopolitical tensions. Following the release of the Beige Book on Wednesday afternoon, Broadcom reported earnings. The semiconductor firm—less highlighted than the “Magnificent Seven”—has been under pressure like many peers, currently about 25% below its December record high of $413. After four consecutive declining sessions, a rebound would provide some relief for the VanEck Semiconductor ETF, which tracks the chip sector.

Chip and Consumer Earnings Shift Focus

Upcoming earnings from Marvell Technology and Costco Wholesale will further influence market sentiment. Marvell’s results could add to volatility in semiconductor stocks, while Costco’s report may offer new insight into the strength of the consumer.

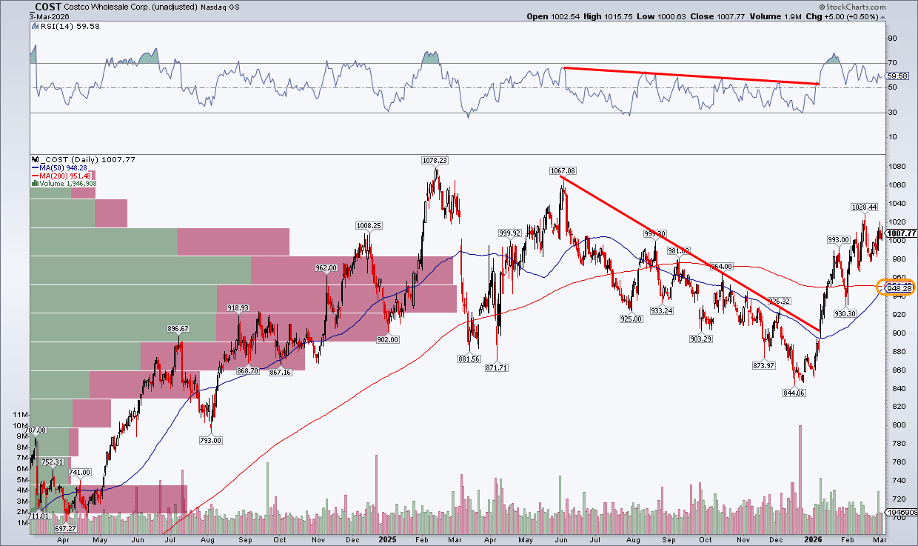

Looking more closely at Costco, bullish signals are beginning to emerge after a difficult second half of 2025. The consumer-staples retailer fell sharply from $1,067 last June to a 16-month low in December, marking its first series of 52-week lows since March 2009.

Currently, however, the stock has recovered above its long-term 200-day moving average as well as its rising 50-day average. A bullish “golden cross” could soon form just as the company releases its fiscal Q2 results. A positive reaction to the earnings report would likely be viewed as an encouraging sign for the broader economy. While consumer staples are typically considered defensive, Costco’s performance is closely tied to middle- and upper-income consumer spending and it has historically been a major leader during long-term bull markets.

It’s the Market Reaction That Matters, Not the Data

At the moment, a pullback in that group would be unwelcome, especially as stocks such as American Express (NYSE: AXP) are already showing potential warning signals. What matters most won’t simply be the revenue and earnings figures released on Thursday evening, but how the stock responds when trading resumes on Friday. In the end, investors’ reactions to fundamental data often carry more weight than the data itself.

Economic Data Takes Center Stage

With that in mind, Friday morning’s focus will shift toward domestic economic indicators rather than the ongoing concerns surrounding the Middle East conflict, including tensions near the Strait of Hormuz, drone and missile strikes, and the possibility of crude oil prices climbing above $100 per barrel for WTI and Brent.

In fact, something unusual is set to occur: the February Employment Situation report and the January Retail Sales report are scheduled to be released at the same time. Key questions remain—how strong will the headline job gains be? Will consumer spending confirm a solid start to the year? For now, it’s uncertain.

Friday Risk Sentiment and Sector Trends

What should become clearer, however, is traders’ appetite for risk as the weekend approaches. Market behavior at the close of the first week of the month—especially with the VIX nearing the 30 level—may provide clues about how the remainder of the first quarter could unfold. Will markets experience heightened volatility, or will conditions calm after March’s turbulent start? Instead of speculating, the charts may offer the answers.

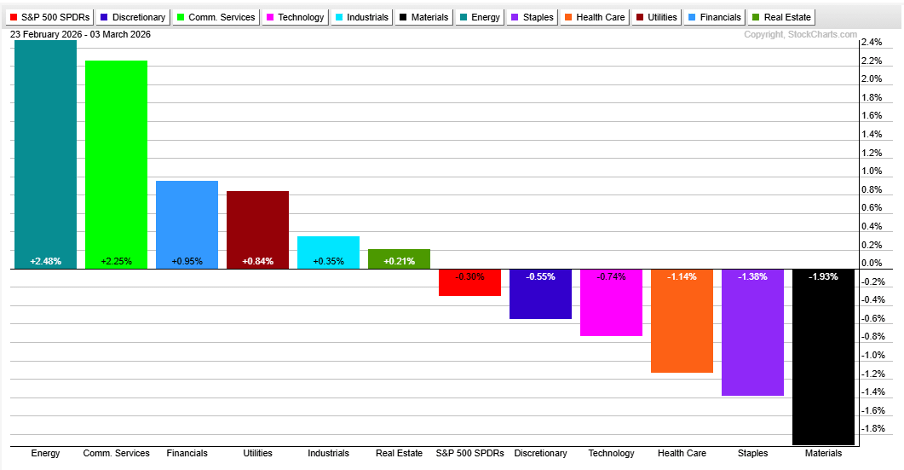

Sector movements have stood out this week. Despite sharp volatility in Energy and other cyclical industries, the Financials (XLF) sector has still managed to generate modest outperformance. That’s an encouraging sign for bullish investors, considering banks and related stocks have been among the market’s leaders since October 2022. At the same time, Energy (XLE) and Utilities (XLU) have continued to rank among the top performers over the past six trading sessions.

However, two sectors trailing behind are Health Care (XLV) and Consumer Staples (XLP). This suggests there hasn’t been a complete shift into defensive assets even as the VIX has climbed. It’s worth noting that the S&P 500 (SPY) has only slipped slightly since February 23, which may hint at a somewhat healthier sector backdrop. By the market close on Friday, we should have a clearer picture of the trend.

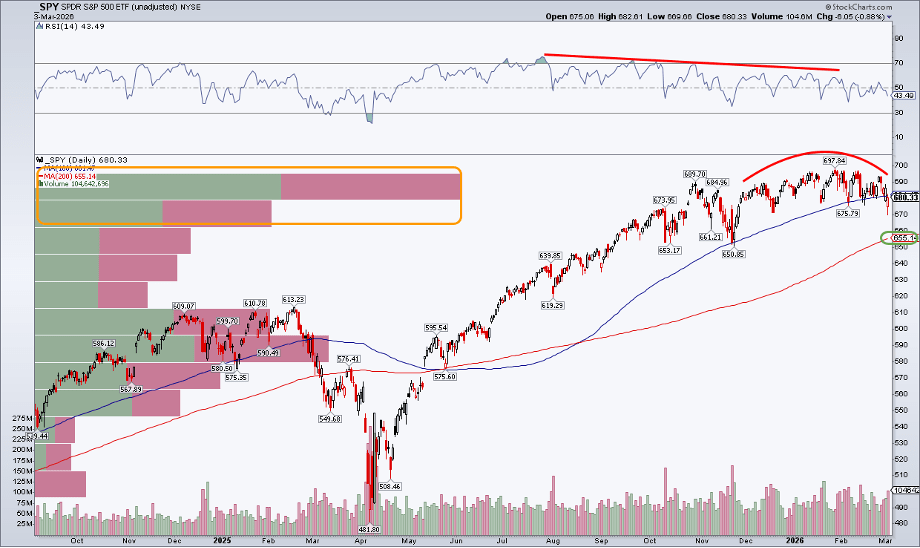

SPY: Bulls and Bears Still Battling

Looking at the bigger picture, the SPY still appears somewhat fragile. A bearish rounded-top pattern seems to be forming, and the price has slipped below the 100-day moving average. While this moving average isn’t always a primary indicator, it has acted as a fairly reliable support and resistance level over the past two years.

That said, the bulls have shown resilience this week. U.S. large-cap stocks rebounded significantly from their lows on both Monday and Tuesday. However, the sharp volatility and heavy trading volumes mean a large amount of shares have changed hands between roughly $670 (Tuesday’s low) and the record high just under $700 set on January 28. For technical analysts, that kind of activity often signals distribution.

Typically, bullish investors prefer to see tight consolidation rather than price structures that stretch out over several months. The concern is that major market participants could be gradually selling shares after a long rally. In other words, traders should remain cautious—especially with potential distribution patterns emerging as March unfolds.

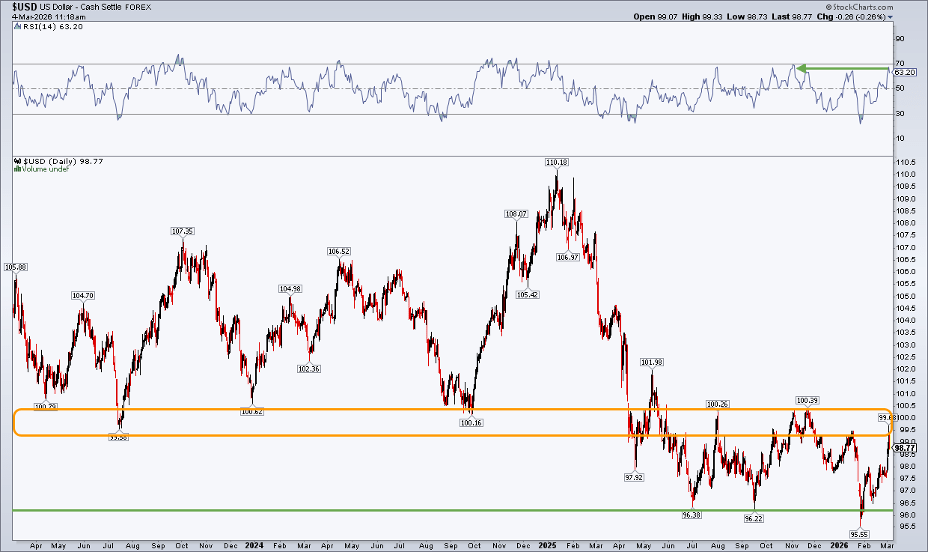

The Dollar’s Rally: Why It Matters

From an intermarket standpoint, the US Dollar Index ($USD) should remain a key indicator to watch for the rest of the quarter. Earlier this week, it moved into the important 99.50–100.50 range but was initially pushed back. Now trading below 99 ahead of major economic releases, a move toward 10-month highs above 100.39 would likely signal a broader risk-off environment in financial markets.

The latest rebound followed what appears to have been a bullish false breakdown, occurring when market sentiment toward the dollar had become excessively negative. To put things into perspective, it’s quite rare for the dollar to remain trapped in such a tight trading range for an extended period.

Once the index eventually breaks out or breaks down, the move could carry significant consequences across global asset markets—from equities to commodities and currencies. For the moment, however, the situation remains a wait-and-see one as traders watch for a decisive shift.

The Bottom Line

March volatility has arrived as expected. Geopolitical tensions have intensified, yet the S&P 500 continues to show resilience. With several key earnings reports and important economic data releases approaching, the market’s reaction heading into the weekend will likely provide the clearest signal for traders.

At the very least, attention may briefly shift away from geopolitical developments. For now, the key areas to monitor include evolving sector trends, the months-long consolidation in the S&P 500, and the range-bound movement of the US Dollar Index. Together, these factors could offer important clues about the market’s next direction.

Sources: Mike Zaccardi

Leave a comment