Inflation measurement sits at the core of modern macroeconomics. Interest-rate policy, asset valuations, fiscal planning, and central-bank credibility all hinge on how price pressures evolve. Yet the benchmark most policymakers rely on — the Consumer Price Index (CPI) — is a monthly government report designed for a far less digitized and fast-moving economy.

Increasingly, market participants are supplementing that traditional gauge with real-time alternatives. Among them, Truflation has emerged as the most widely cited live inflation index. Built from millions of observed prices and updated continuously, it offers a near real-time snapshot of price dynamics. In early 2026, its signal diverges meaningfully from official CPI data.

Methodology and Structural Differences

Truflation was launched in December 2021 amid frustration over the lag in official inflation reporting. While CPI is released monthly and relies heavily on surveys, sampling, and statistical smoothing, Truflation applies a bottom-up, digitally native methodology.

The index aggregates data from more than 30 million items across 30+ licensed providers — including online retailers, housing platforms, and consumer-data firms. Prices update daily and are secured through decentralized oracle infrastructure on the Chainlink network, increasing transparency and reducing the risk of retrospective revisions.

Like CPI, Truflation tracks twelve broad consumption categories. However, its category weights are recalibrated annually using observed spending patterns rather than fixed survey-based assumptions. This allows the index to adjust more quickly to shifts in consumer behavior and pricing trends.

Historically, that responsiveness has mattered. Empirical comparisons suggest Truflation has often led CPI turning points by roughly 40 to 75 days, flagging inflection points in inflation momentum well before they appear in official releases.

Institutional Validation

Skepticism toward alternative measures is natural. Still, Truflation has begun clearing some of the credibility hurdles required for broader institutional adoption.

Throughout 2024 and 2025, its short-term forecasting accuracy was notable. In many instances, its readings anticipated CPI outcomes within approximately ±0.1 percentage points. That degree of precision has encouraged growing usage among macro hedge funds and systematic trading strategies.

Institutional validation advanced further in early 2026 when Truflation was integrated into the Bloomberg L.P. terminal ecosystem — a quiet but meaningful step that elevated it from a crypto-native experiment into a recognized macro data input.

Transparency also strengthens its appeal. Daily updates, publicly documented methodology, and auditability offer advantages in markets that reprice continuously, where a 30-day lag can materially affect positioning.

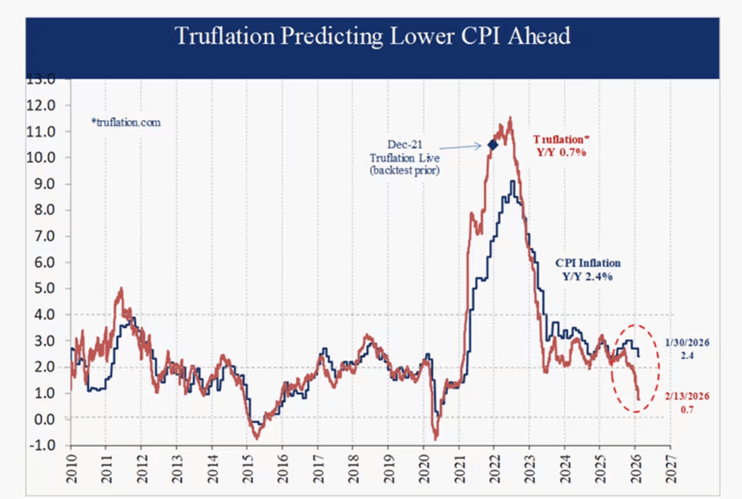

The 2026 Divergence

By mid-February 2026, the spread between Truflation and official CPI readings had widened to one of the largest gaps since the index was created:

- Official CPI (January 2026): 2.4% year-over-year

- Truflation (Feb 1–18, 2026): ~0.7%

- Core CPI: ~2.5%

- Truflation core proxy: ~1.3%

Such a divergence presents a challenge: either real-time data are signaling a rapid disinflationary shift not yet captured by government statistics, or the high-frequency approach is temporarily underestimating sticky components embedded in CPI.

If historical lead times hold, markets may need to reassess the inflation trajectory sooner rather than later.

The widening gap between the two measures points to fundamentally different interpretations of current inflation momentum. The central source of divergence is housing.

Truflation incorporates real-time asking rents pulled from active market platforms, capturing the recent cooling in rental prices as it happens. By contrast, official CPI relies heavily on “Owner’s Equivalent Rent,” a survey-based estimate that typically lags actual rental-market conditions by six to twelve months.

In effect, the two gauges are measuring different time horizons. Truflation reflects present housing dynamics, while CPI still embeds rental trends from prior quarters.

The macro implications are significant. If the real-time signal is more accurate, the U.S. economy could be moving closer to disinflation — or even deflationary — conditions, historically associated with rising recession risk. Meanwhile, official data continue to portray a controlled soft landing, with inflation appearing comfortably near target.

Explaining the Reluctance

Despite its growing track record, many economists remain hesitant to incorporate Truflation into formal macro frameworks. The resistance tends to rest on three main arguments.

1. Institutional inertia.

CPI has decades of embedded usage. Forecasting models, policy rules, asset-allocation frameworks, and academic research are all synchronized to its monthly release cycle. Integrating a daily inflation measure would require reworking not only projections, but established institutional workflows.

2. Volatility bias.

Because Truflation updates continuously, it can display sharp short-term swings. A rapid daily decline may be dismissed as noise, even when it reflects genuine pricing shifts. By comparison, CPI’s smoothed profile feels more stable — even if that stability comes at the expense of timeliness.

3. Composition differences.

Truflation assigns slightly less weight to housing than CPI. Critics argue this could understate inflation during periods of accelerating rents. Yet the reverse also holds true: when rental markets cool quickly, CPI may overstate underlying price pressure — which appears to be the present dynamic.

Ultimately, the hesitation is less about data availability and more about comfort. A measure that moves faster and smooths less inevitably challenges established interpretive habits.

Conclusion: Why the Signal Matters

If Truflation’s current reading is directionally correct, monetary-policy expectations could be misaligned with underlying inflation trends. The Federal Reserve may have greater scope to ease than prevailing consensus assumes, even as headline data suggest economic resilience.

This does not mean Truflation should replace CPI as the official benchmark. But when divergences persist and widen, dismissing the alternative becomes increasingly difficult.

More broadly, the debate underscores a structural issue: inflation cannot be treated solely as a once-a-month statistic in an economy where prices adjust continuously. Measurement tools must evolve alongside market speed.

Truflation’s importance does not rest on perfection. Its value lies in timeliness, transparency, and the growing challenge of ignoring what it is signaling.

Sources: Charles-Henry Monchau

Leave a comment