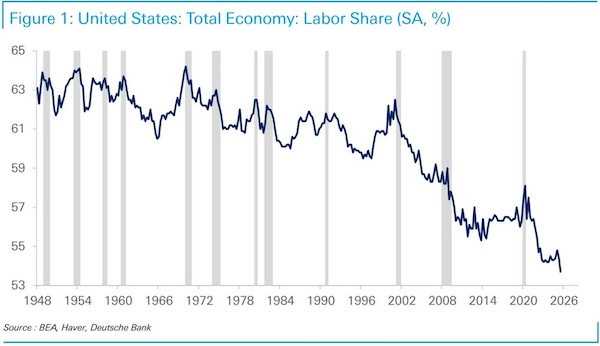

One of the most significant macroeconomic trends of recent decades has been the sharp decline in labor’s share of income. As David Hay notes, the rise of populism in the US mirrors the long expansion in corporate profit margins — essentially the flip side of a prolonged downturn in labor’s share.

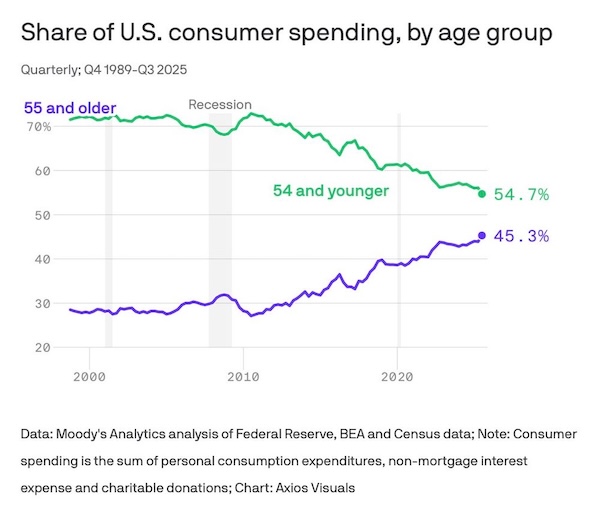

This shift was largely driven by favorable demographics and accelerating globalization. However, both forces now appear to be reversing. On the demographic front, Axios recently highlighted that older Americans are increasingly powering economic growth — a “gray-shaped” dynamic rather than the previously discussed K-shaped recovery.

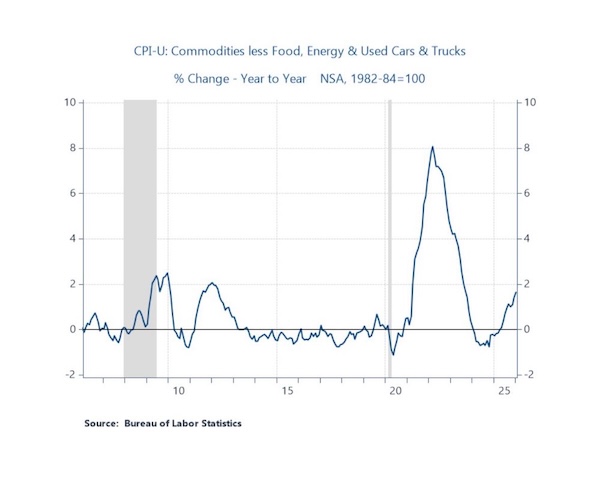

Meanwhile, the inflationary cost of deglobalization may only be beginning to surface. According to Brean Capital, core CPI excluding used vehicles and shelter has ticked higher, with the three-month annualized rate climbing to 2.9% from 1.1% in December. This suggests tariff-related pressures may still be lingering, complicating hopes for a smooth return to the Fed’s 2% inflation target.

Financial markets are already reacting to these evolving macro conditions. As Callum Thomas observes, gold has been the best-performing asset class of the 2020s so far, while bonds have lagged significantly — raising questions about how the rest of the decade will unfold.

Leadership within equities is also shifting. Research from Daily Chartbook indicates that the “Magnificent Seven” peaked relative to the energy sector in December 2025, matching the same relative level seen in October 2020 — just before the Energy Select Sector SPDR Fund embarked on a 250% rally over the following two years.

So far this year, energy stands out as the stock market’s top-performing sector. According to Rob Thummel, the sector delivers what investors increasingly value: strong free cash flow, rising dividends, significant share buybacks, inflation hedging characteristics, and tangible asset exposure.

Echoing this thematic rotation, Goldman Sachs suggests the market may be entering what one seasoned client calls the “revenge of the dinosaurs” phase — a resurgence of traditional, capital-intensive industries in an era marked by structural inflation pressures and shifting global dynamics.

Sources: Jesse Felder

Leave a comment