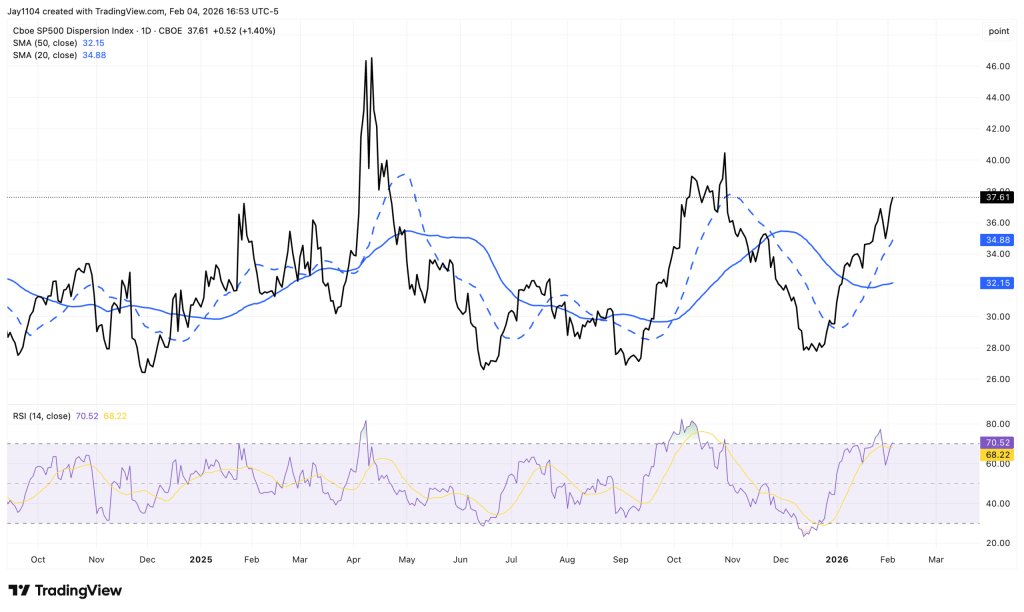

Stocks ended lower on Wednesday, though the S&P 500 slipped just 50 basis points. In contrast, the equal-weight S&P 500 ETF (RSP) gained nearly 90 basis points, highlighting a notable degree of dispersion beneath the surface. This divergence was reflected in the Dispersion Index, which climbed to 37.6 and is once again approaching the upper end of its historical range. As earnings season draws to a close, dispersion is likely to ease, with correlations gradually moving higher.

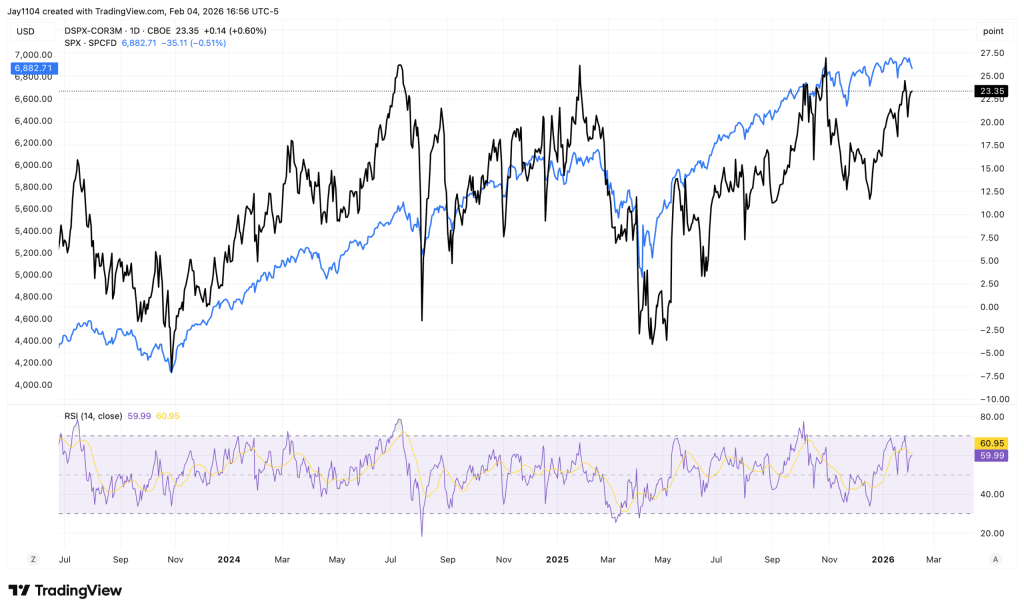

The spread between the Dispersion Index and the three-month implied correlation index widened on Wednesday. As earnings season comes to an end, this gap is likely to narrow in the coming weeks as dispersion trades begin to unwind and correlations normalize.

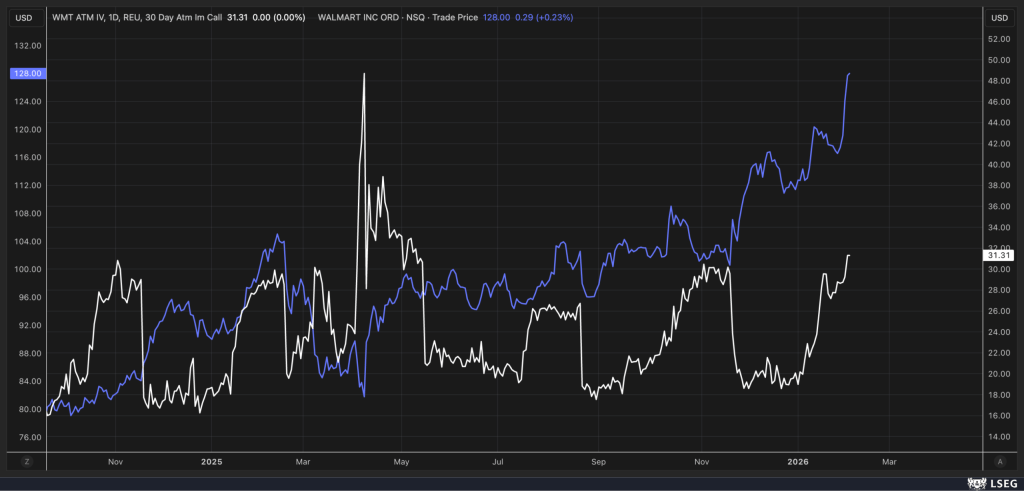

One explanation for the notable strength in Walmart (NASDAQ: WMT) and the broader consumer staples sector may be the rise in implied volatility. While IV typically increases ahead of earnings season, this year it appears to be climbing to levels well above those seen in prior quarters. With Walmart not scheduled to report until February 19 and most retailers releasing earnings later in the cycle, the recent strength in XLP may not reflect a true sector rotation. Instead, it could be driven by the same dispersion dynamics observed ahead of the major technology earnings releases.

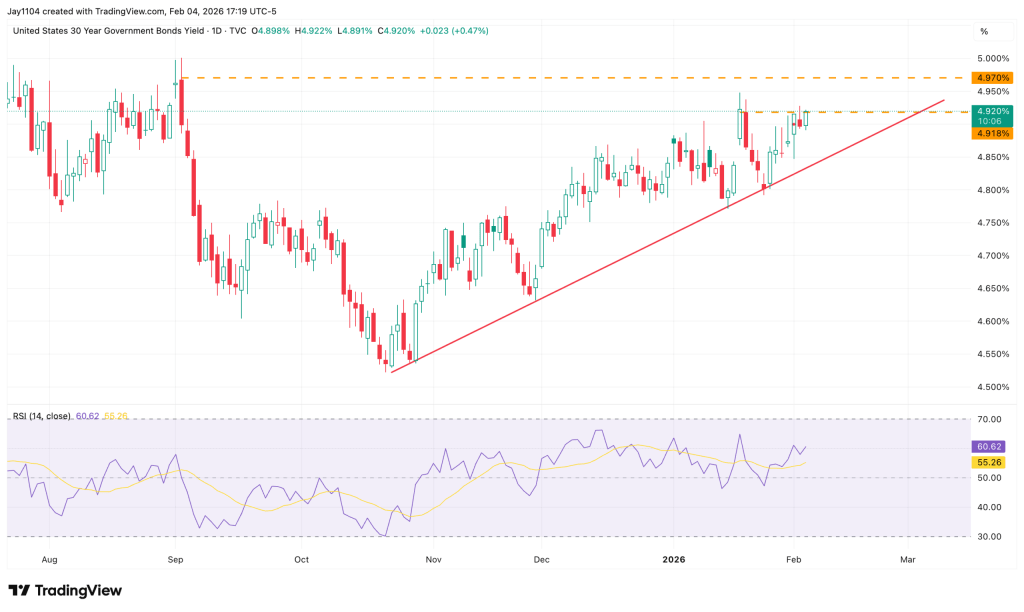

Long-term rates edged higher on Wednesday, with the 30-year yield rising about 2 basis points to 4.92%, once again testing the upper end of its resistance range. Whether it ultimately breaks higher remains uncertain. Fundamentally, yields have had ample justification to move higher for weeks, yet they remain stubbornly range-bound. The 30-year could arguably already be above 5%, but the market continues to wait.

The latest QRA released Wednesday continues to point to mounting stress at the long end of the curve, though those pressures have yet to fully materialize. The report noted that the Treasury General Account (TGA) is expected to exceed $1 trillion around tax season—roughly $150 billion above current levels. That represents a significant liquidity drain from the system, and based on rough estimates, the Fed’s bill purchases would dilute, rather than offset, that impact.

Looking ahead, Kevin Warsh’s arrival in May adds another layer of uncertainty around balance-sheet policy. As a result, liquidity conditions are likely to remain tight for some time.

Sources: Michael Kramer

Leave a comment