AUD/USD is trading lower below the key 0.7000 psychological level during Thursday’s Asian session, pressured by mixed Australian trade data. The pair is also weighed down by a firm U.S. dollar, which is hovering near a two-week high. With limited domestic catalysts, traders are now turning their attention to the upcoming U.S. JOLTS job openings data for fresh direction.

AUD/USD Technical Outlook

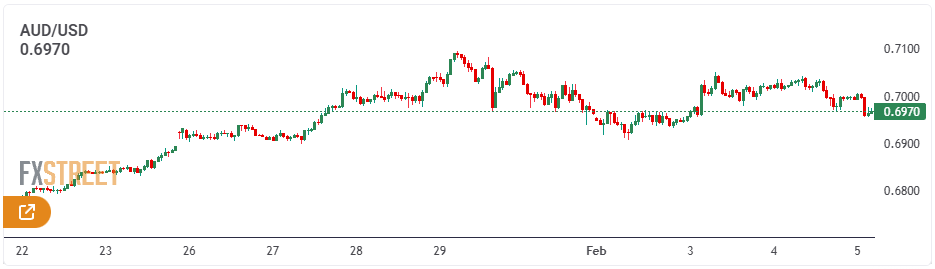

Should bullish momentum intensify, AUD/USD is likely to encounter its next resistance at the 2026 peak of 0.7093 (Jan 29), followed by the 2023 high at 0.7157 (Feb 2).

On the downside, a break below the February low at 0.6908 (Feb 2) may trigger a deeper pullback toward the interim 55-day SMA at 0.6693, ahead of the 2026 trough at 0.6663 (Jan 9). Additional downside support is seen at the 100-day SMA at 0.6628, with stronger support at the 200-day SMA at 0.6563 and the November low at 0.6421 (Nov 21).

Momentum indicators remain constructive and point to further upside potential, although the pair’s overbought readings suggest the risk of a near-term correction. The RSI hovers near 72, while the ADX around 50 continues to signal a strong underlying trend.

Bottom line

AUD/USD continues to be heavily influenced by global risk appetite and developments in China’s economy. A sustained move above the 0.7000 handle would reinforce a more credible bullish outlook.

For the time being, a weaker U.S. dollar, stable—though not particularly strong—domestic data, a still-hawkish tilt from the RBA, and modest backing from China leave the balance of risks skewed toward further upside rather than a pronounced pullback.

Fundamental Analysis

AUD/USD remains entrenched in its broader uptrend despite renewed selling pressure emerging on Wednesday. Any near-term pullbacks are expected to attract buying interest, as the Reserve Bank of Australia continues to project a clearly hawkish stance following its latest rate decision.

The Australian Dollar is struggling to extend Tuesday’s advance, easing back and once again testing the psychologically significant 0.7000 mark.

The retreat comes as the U.S. Dollar regains some traction, with markets having largely absorbed the RBA’s hawkish hike and refocusing attention on U.S. economic and monetary policy developments.

Australia: Growth Is Cooling, Not Collapsing

Recent Australian data have been underwhelming rather than alarming, reinforcing a well-established narrative. Economic activity is slowing, but in a controlled manner, with momentum easing rather than breaking down—supporting the soft-landing view.

January PMI surveys align with this assessment, as both Manufacturing and Services strengthened and remained firmly in expansion territory, at 52.3 and 56.3 respectively. Retail sales continue to show resilience, and although the trade surplus narrowed to A$2.936 billion in November, it remains solidly positive.

Growth is moderating only gradually, following a 0.4% quarter-on-quarter rise in GDP in Q3. On an annual basis, output expanded by 2.1%, matching the RBA’s projections.

The labour market remains a standout performer. Employment jumped by 65.2K in December, while the unemployment rate unexpectedly edged down to 4.1% from 4.3%.

Inflation, however, continues to be the key challenge. December CPI surprised to the upside, with headline inflation accelerating to 3.8% year-on-year from 3.4%. The trimmed mean rose to 3.3%, in line with market expectations but slightly above the RBA’s 3.2% forecast. On a quarterly basis, trimmed mean inflation increased to 3.4% in the year to Q4, marking the highest level since Q3 2024.

China: A Backdrop of Support, Not a Catalyst

China continues to offer a generally supportive backdrop for the Australian dollar, though without the momentum needed to drive a sustained upswing.

Economic growth ran at an annualised 4.5% in the October–December quarter, with quarter-on-quarter expansion at 1.2%. Retail sales rose 0.9% year-on-year in December—respectable, but not particularly compelling.

More recent indicators point to a renewed loss of momentum. Both the NBS Manufacturing PMI and the Non-Manufacturing PMI slipped back into contraction territory in January, at 49.3 and 49.4 respectively.

By contrast, the Caixin surveys painted a slightly brighter picture, with the Manufacturing PMI edging up to 50.3 to remain in expansion, while the Services PMI increased to 52.3.

Trade stood out as a relative bright spot, as the surplus widened sharply to $114.1 billion in December, supported by nearly 7% growth in exports and a solid 5.7% rise in imports.

Inflation signals remain mixed. Consumer prices were unchanged at 0.8% year-on-year in December, while producer prices stayed firmly negative at -1.9%, underscoring that deflationary pressures have yet to fully fade.

For now, the People’s Bank of China is maintaining a cautious stance. Loan Prime Rates were left unchanged in January at 3.00% for the one-year and 3.50% for the five-year, reinforcing expectations that policy support will remain gradual rather than aggressive.

RBA: Leaning Hawkish, In No Hurry to Ease

The RBA raised the cash rate to 3.85% in a decisively hawkish move that largely met expectations. Upward revisions to both growth and inflation forecasts signal firmer economic momentum and increasingly broad-based price pressures. Core inflation is now projected to remain above the 2–3% target band for much of the forecast horizon, reinforcing the case for a restrictive policy stance.

The central message is that inflation is becoming more demand-driven. The RBA cited stronger-than-expected private demand as a key justification for tighter policy, even as productivity growth remains subdued. While Governor Bullock described the move as an “adjustment” rather than the beginning of a renewed hiking cycle, the signal was clear: policymakers are uneasy with the upward drift in inflation.

For markets, this implies interest rates are likely to stay higher for longer, limiting the scope for near-term easing. From an FX perspective, this provides marginal support for the Australian dollar—particularly against low-yielding peers—even as the RBA’s emphasis on full employment tempers the likelihood of an aggressive tightening phase.

In the wake of the decision, markets are now pricing in nearly 40 basis points of additional tightening by year-end.

Positioning: Shifting Sentiment Toward the AUD

The latest positioning data suggest the worst of the bearish sentiment toward the Australian dollar may have passed. CFTC figures show that non-commercial traders have returned to a net long stance for the first time since early December 2024, although the position remains modest at just over 7.1K contracts in the week ending January 27.

Open interest has also climbed to its highest level in several weeks, exceeding 252K contracts, indicating that traders are beginning to re-engage with the market. That said, the move appears tentative rather than a strong conviction call on a sustained appreciation in the AUD, at least for now.

Key Drivers Ahead

Near term: Market attention is shifting back toward the United States. Incoming economic data, tariff-related developments, and ongoing geopolitical headlines are likely to drive movements in the U.S. dollar. For the Australian dollar, the key swing factors remain domestic labour market and inflation data, and how these shape expectations for the RBA’s next policy decision.

Risks: The AUD remains highly sensitive to global risk sentiment. A sharp deterioration in risk appetite, renewed concerns over China’s outlook, or an unexpected resurgence in the U.S. dollar could quickly unwind recent gains.

Sources: Fxstreet

Leave a comment