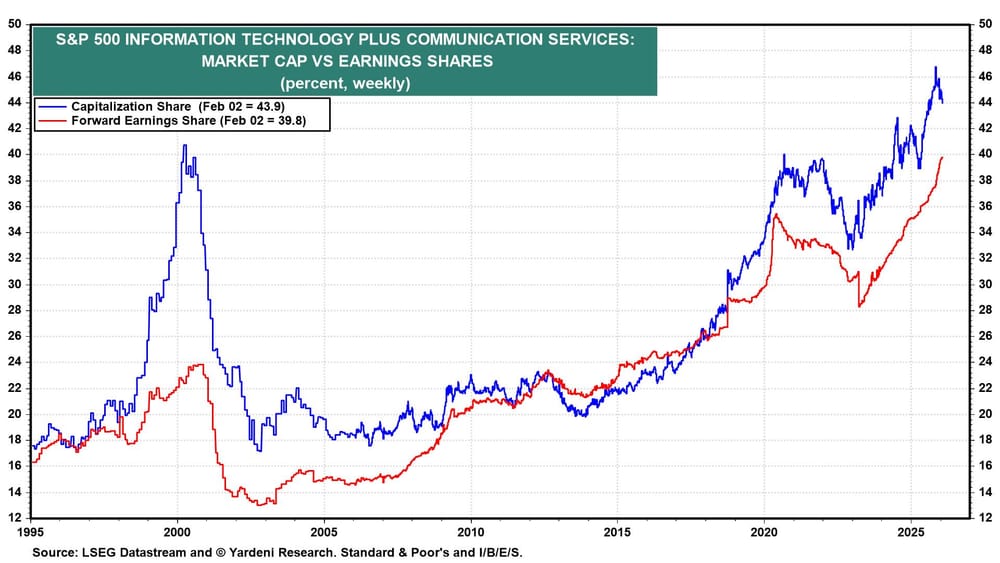

On December 7, 2025, we advised maintaining a market-weight stance rather than an overweight position in the S&P 500’s Information Technology and Communication Services sectors. Since then, their combined share of the index’s market capitalization has fallen from a record 46.7% on November 5, 2025, to 43.9% as of Monday (see chart). This decline has occurred even as their combined contribution to S&P 500 earnings continued to climb, reaching a new high of 39.8% by Monday.

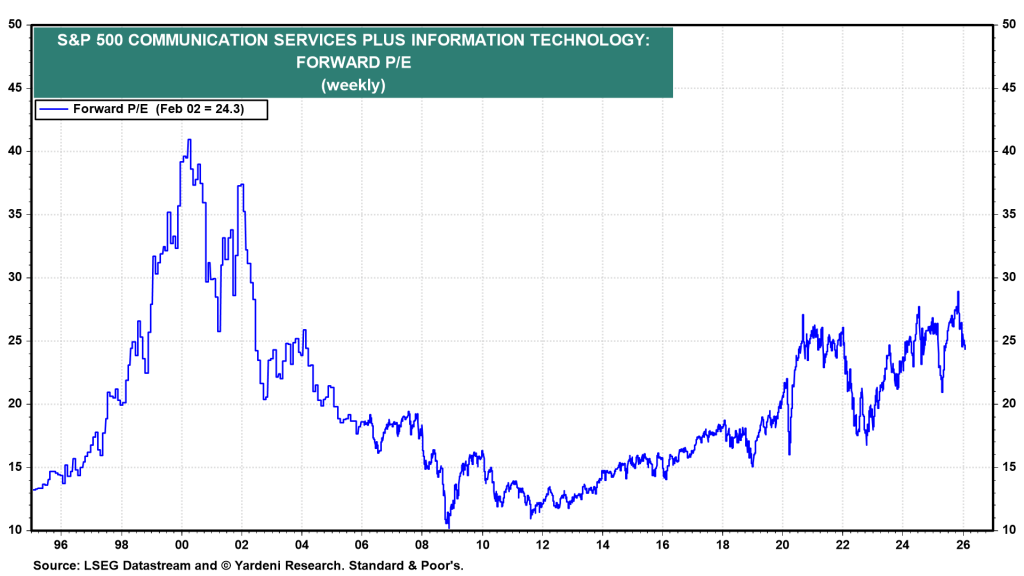

Despite strong growth in the two sectors’ combined forward earnings, their aggregate forward P/E multiple has compressed from 28.9 on November 5, 2025, to 24.3 currently (see chart).

On December 7 last year, we argued that AI was intensifying competition among the Magnificent Seven, compelling them to sharply ramp up investment in AI infrastructure. On that basis, we recommended an underweight position. We expect the primary beneficiaries of this dynamic to be the broader S&P 500—often referred to as the “Impressive 493”—which are leveraging AI tools to boost productivity rather than competing on infrastructure scale.

Technology has always been a highly competitive industry, and AI is intensifying that dynamic even further. In my 2018 book Predicting the Markets, I described the tech sector as a textbook case of “creative destruction,” where new innovations relentlessly displace older technologies.

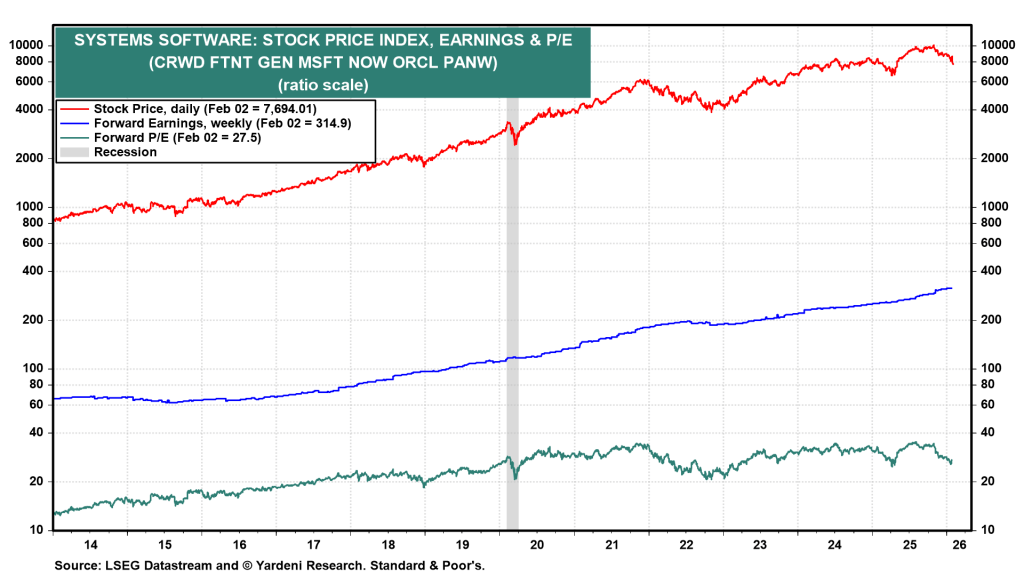

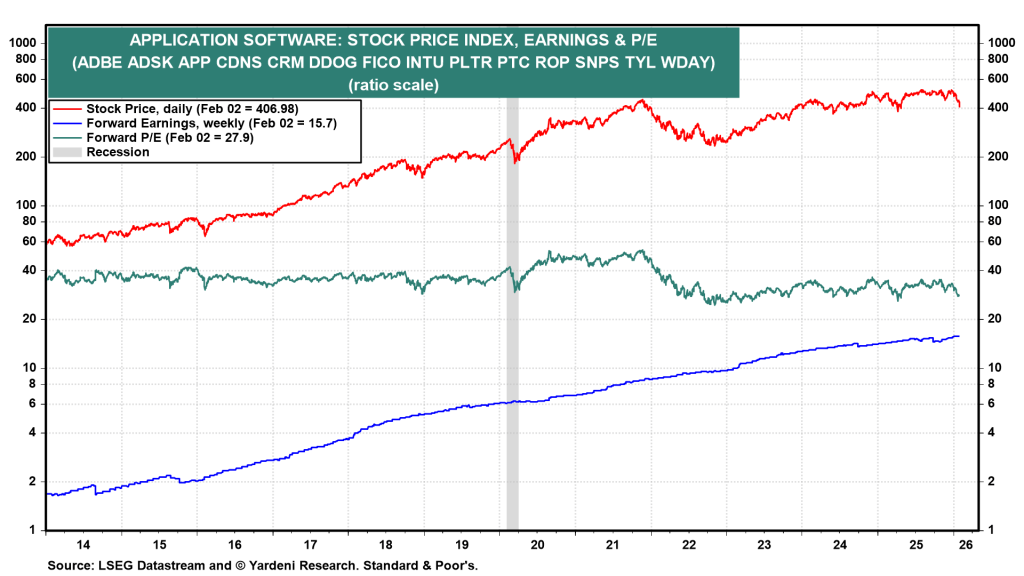

More recently, software stocks have come under pressure as AI tools become increasingly proficient at writing code (see charts). While forward earnings for the sector have climbed to record levels, investors have compressed valuation multiples in response to the growing competitive threat posed by AI.

On Tuesday, software stocks were hit particularly hard after Anthropic unveiled new tools for its Cowork product. While it remains too early to assess their practical impact, investors responded by marking down valuation multiples across the software sector.

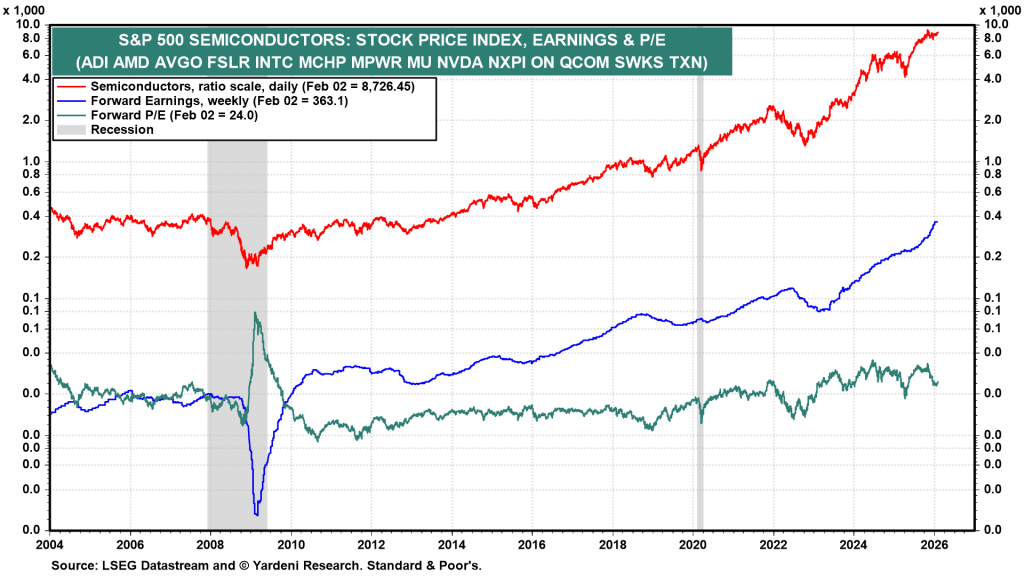

By contrast, semiconductor stocks have proven relatively resilient, even as the industry’s forward P/E multiple has declined amid a sharp surge in forward earnings (see chart). Competitive pressures are intensifying, particularly among chips designed to rival Nvidia’s (NASDAQ: NVDA) GPUs. At the same time, tight memory supply has driven prices sharply higher, though history suggests that once capacity expands to meet demand, those prices are likely to retreat.

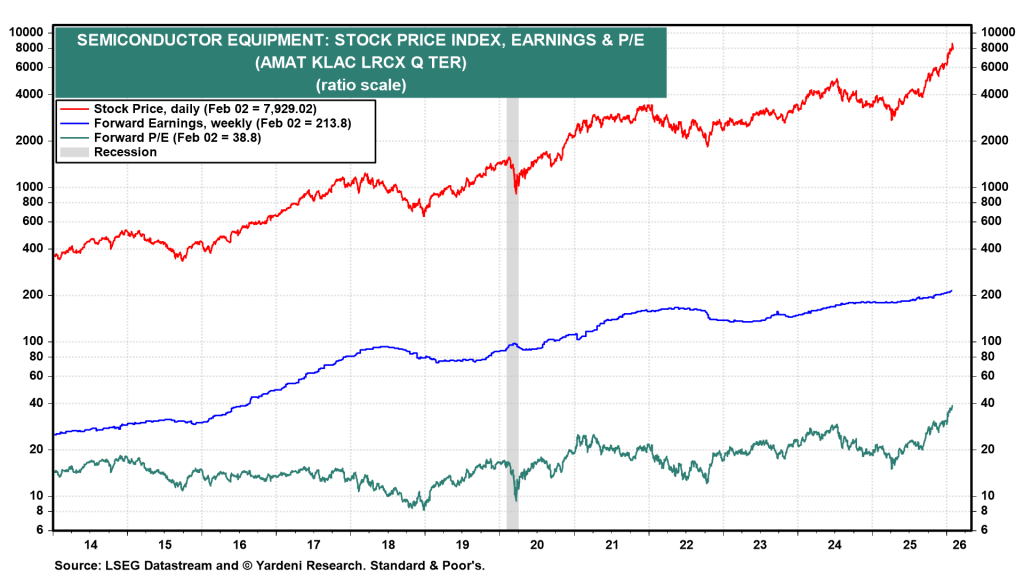

Shares of semiconductor equipment makers have continued to climb, alongside rising earnings and expanding valuation multiples (see chart). This strength reflects the industry’s relative insulation from competitive pressures, as these companies benefit whenever demand is strong for equipment that enables chipmakers to expand production capacity.

Sources: Ed Yardeni

Leave a comment