During and in the aftermath of 9/11, Nassim Taleb—a Lebanese-born former options trader and quantitative analyst—published Fooled by Randomness. He later refined and formalized the idea in his 2007 book The Black Swan, drawing on the metaphor of the rare black swan, an anomaly among typically white birds.

Taleb defined a Black Swan as an event that meets three criteria: first, it is an extreme outlier, often without historical precedent; second, it carries an immediate and profound impact; and third, it becomes explainable only in hindsight, after the event has occurred.

Forty years ago tomorrow, on the morning of Tuesday, January 28, 1986, tens of millions of Americans watched live as the Space Shuttle Challenger lifted off—only to explode 73 seconds into flight, killing all seven crew members, including the widely admired teacher-astronaut Christa McAuliffe.

The tragedy met all of Nassim Taleb’s criteria for a Black Swan event. First, it was unprecedented, marking the first fatal in-flight disaster involving a US spacecraft. Second, its impact was immediate: President Ronald Reagan postponed his State of the Union address scheduled for that evening. Third, the cause was only fully understood after the fact, when physicist Richard Feynman explained during televised hearings that the disaster resulted from O-ring failure in unusually cold conditions.

One response that did not occur—then or in most Black Swan events—was a meaningful stock market selloff. Markets were largely indifferent. The S&P 500 rose on the day of the explosion and continued higher, gaining 2.6% for the week and 16.8% over the remainder of 1986. The Dow Jones Industrial Average also advanced, rising 1.2% on the day, 2.7% for the week, and 22.6% for the year.

Another Black Swan touched Great Britain exactly fifty years earlier, when global stock markets closed on January 28, 1936, to mark the funeral of King George V. He was succeeded by Edward VIII, whose relationship with an American divorcée triggered a constitutional crisis that lasted much of the year. The turmoil ended with Edward’s abdication in favor of his younger brother, who became King George VI and later passed the crown to his daughter, Elizabeth II—the longest-reigning and arguably most popular British monarch—suggesting the succession ultimately resolved smoothly.

Despite the political uncertainty, 1936 proved to be a strong year for markets during an otherwise bleak Depression-era decade, with the Dow Jones Industrial Average rising 25%.

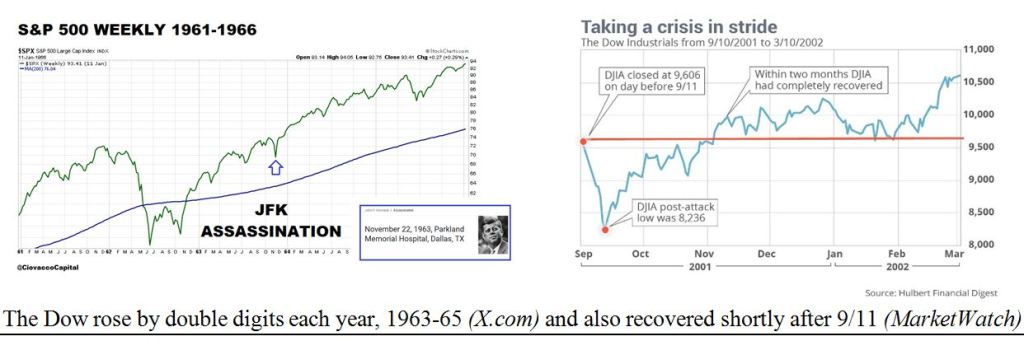

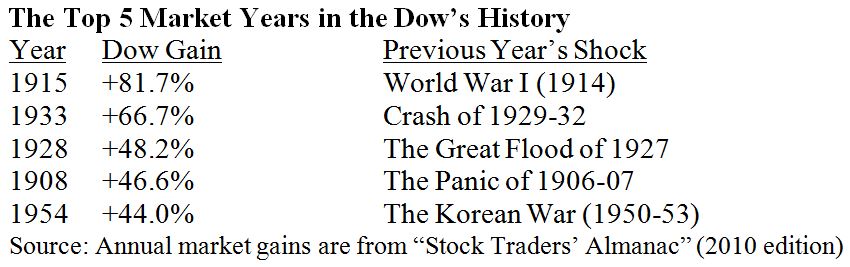

Across the past century, several other major Black Swan events have reshaped history, including the outbreak of World War I following the assassination in Sarajevo on June 28, 1914; Japan’s attack on Pearl Harbor on December 7, 1941; the assassination of President John F. Kennedy on November 22, 1963; and the September 11, 2001 attacks.

History also shows a striking pattern in which US presidents elected in seven consecutive election years, spaced 20 years apart, died in office: William Henry Harrison (1840), Abraham Lincoln (1860), James Garfield (1880), William McKinley (1900), Warren Harding (1920), Franklin Roosevelt (1940), and John F. Kennedy (1960). One might argue that this grim sequence made the outcome seem almost “predictable.” The streak ended two decades later, when Ronald Reagan survived an assassination attempt in March 1981, with John Hinckley’s bullet narrowly missing his heart.

Following the survival of Reagan—and Pope John Paul II six weeks later—three major Black Swan events marked the late 1980s. The first was the 1986 Challenger explosion, followed by the 1987 Black Monday market crash, which shocked investors far more than the general public. The decade closed with the fall of the Berlin Wall in 1989, a swan-like event, even though many had anticipated the eventual collapse of Gorbachev’s Soviet Union.

The stock market shrugs off most Black Swan events

The stock market posted an unexpected rally in the week and year following President Kennedy’s assassination and rebounded swiftly after the September 11, 2001 attacks. These Black Swan events appeared to have little lasting effect on Wall Street, as traders largely focused on other—primarily financial—developments and trends.

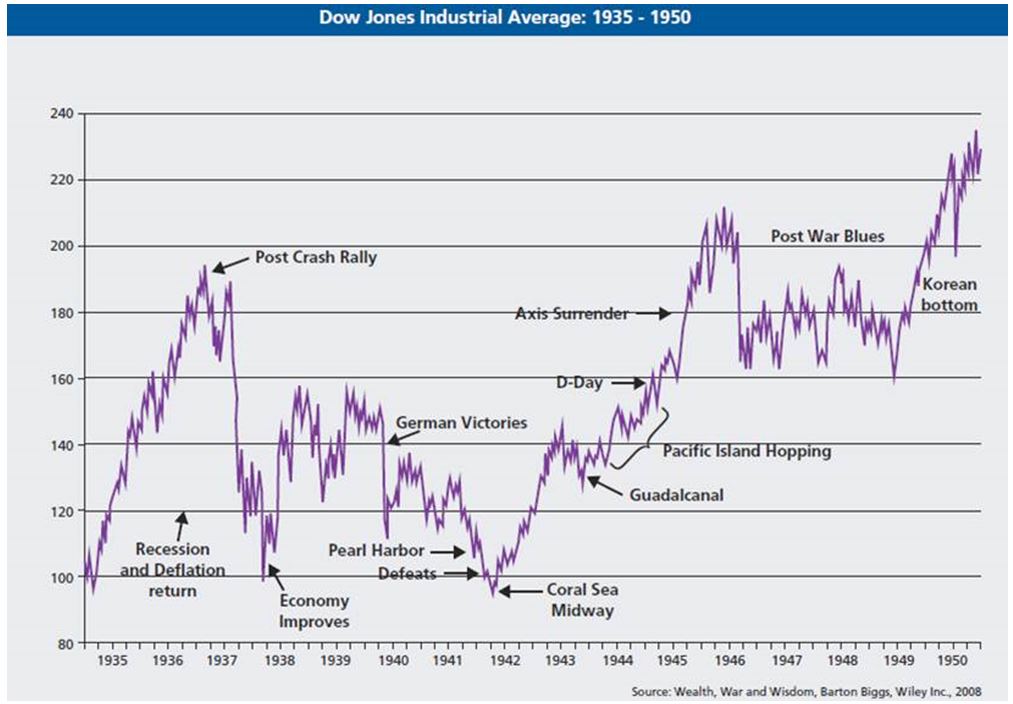

Markets also tended to rise during many 20th-century wars, most of which began with surprise attacks. The abrupt onset of World Wars I and II, the unexpected outbreak of the Korean War, and the August 1964 Gulf of Tonkin escalation of the Vietnam War all triggered initial sell-offs that were followed by strong market recoveries.

The accompanying diagram illustrates the market’s detailed reaction after the attack on Pearl Harbor in late 1941 and following the North Korean invasion in June 1950. These two episodes were separated by a period of post-war, largely “Swan-less,” malaise in the late 1940s.

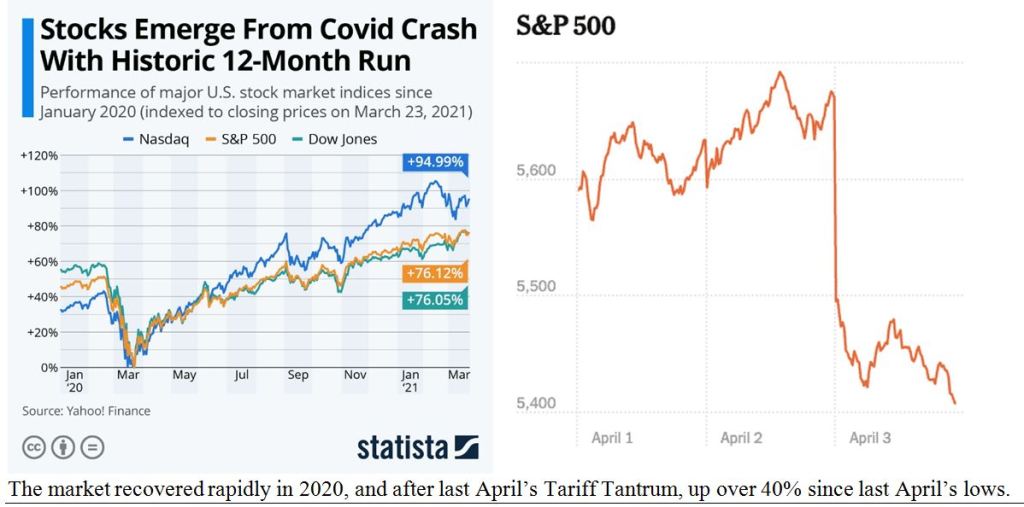

In the two most recent Black Swan episodes, markets followed a familiar pattern. First, the abrupt escalation of the COVID-19 crisis in March 2020 triggered a stunning 35% market collapse in just 35 days, which was then followed by one of the strongest recoveries on record later that year. Second, markets sold off sharply after President Trump and Interior Secretary Lutnick unveiled sweeping high-tariff measures on “Liberation Day” in April 2025, yet the S&P 500 has since rebounded and is now up roughly 40% from those lows.

Most of the Dow’s top five annual gains over its 130-year history followed major Black Swan events.

By definition, the next Black Swan event is unknowable, but the market’s response may not be. With or without a short-term correction, prices are likely to be higher a year later.

Sources: Louis Navellier

Leave a comment