This may be the single most important chart in global bond markets right now.

Japanese investors rank among the world’s largest exporters of capital. Collectively, they hold a substantial share of European sovereign debt and U.S. Treasuries, with ownership running into the trillions of dollars. However, the economics underpinning these investments may soon begin to break down.

If that happens, Japan could see a meaningful repatriation of capital—away from foreign bond markets and back into domestic fixed-income assets.

The consequences for both global bond yields and currency markets would be significant. To understand why, it helps to look at the basic math.

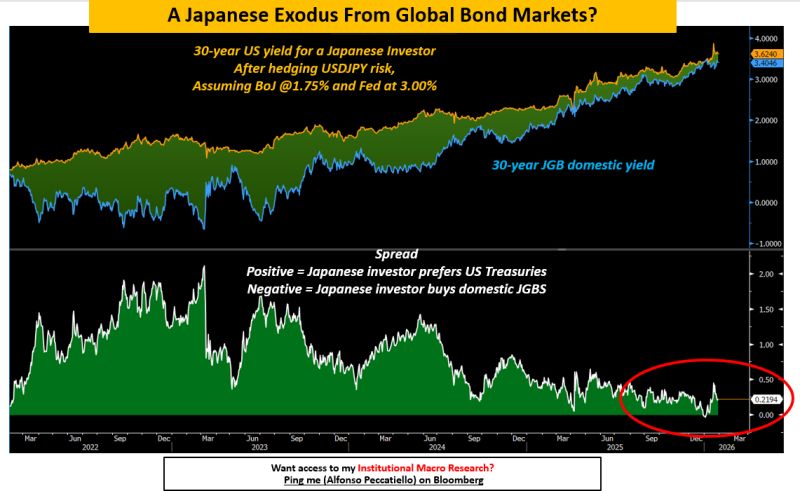

The chart compares the 30-year Japanese government bond yield (blue) with the hedged yield on the 30-year U.S. Treasury (orange), adjusted for USD/JPY currency-hedging costs. The scenario assumes the Bank of Japan gradually lifts policy rates toward 1.75%, while the Federal Reserve cuts rates to around 3% over time.

Note how the two yields are now converging.

At current levels, Japanese investors gain little—if any—advantage from purchasing 30-year U.S. Treasuries on a currency-hedged basis versus simply holding long-dated Japanese government bonds at home. The picture becomes even more compelling when considering a longer-standing behavior.

For years, Japanese investors have also allocated heavily to foreign bonds without hedging currency risk—and for a clear reason.

The prevailing assumption was that the yen would continue to depreciate, allowing Japanese investors to benefit not only from higher foreign yields but also from favorable FX moves.

- Earn higher yields in foreign bond markets

- Gain additional returns from yen depreciation

With the United States signaling its willingness to prevent further yen weakness, and Japanese bond yields having risen sharply, this long-standing equation no longer holds.

Should Japanese investors begin to scale back capital outflows to overseas bond markets, the ripple effects across global bond yields and currency markets could be substantial.

Sources: Alfonso Peccatiello

Leave a comment