Federal Reserve Chair Jerome Powell offered few substantive remarks during his press conference on Wednesday, sidestepping multiple questions about the upcoming leadership transition as his term ends on May 15. He declined to comment on President Donald Trump’s potential nominee to succeed him, as well as on the president’s public criticism of his tenure.

Powell also avoided addressing questions related to the Department of Justice investigation involving him and the ongoing Supreme Court case concerning the possible removal of Fed Governor Lisa Cook. In response to these issues, he repeatedly indicated that he had nothing further to add.

“I have nothing on that for you.”

He repeated that response seven times in total. On four occasions, he simply said,

“I don’t have anything on that for you.”

After the FOMC voted to keep the federal funds rate in a range of 3.50%–3.75%, Powell provided no additional forward guidance beyond reiterating the Fed’s data-dependent, meeting-by-meeting approach. He did, however, acknowledge the underlying strength of the U.S. economy.

Powell noted that the unemployment rate has remained low at around 4.4% in recent months, even as job growth has slowed. He also said inflation is expected to ease as the effects of President Trump’s tariffs fade.

Overall, Powell characterized the risks of higher inflation and rising unemployment as balanced, signaling little urgency for policy action. This assessment increases the likelihood that the federal funds rate will remain unchanged at his final two meetings as FOMC chair.

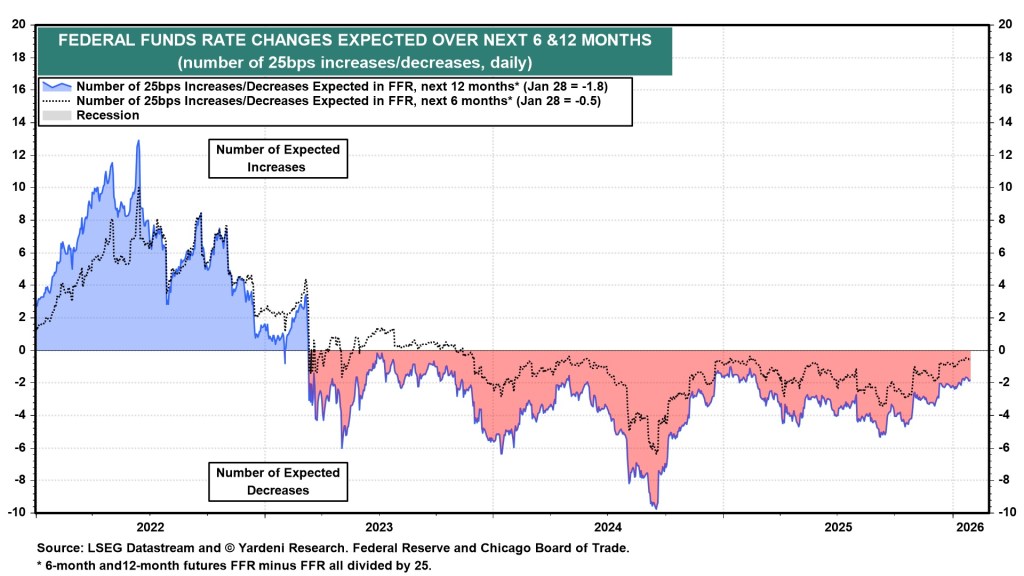

Officials in the Trump administration broadly share our “Roaring 2020s” outlook, which assumes stronger-than-expected productivity growth will lift real GDP while easing inflation pressures as unit labor cost growth falls toward zero. They argue that this expectation supports additional cuts to the federal funds rate—a view echoed by two dissenting members of the FOMC, who expressed similar reasoning at the latest meeting.

We take a different view. Cutting the federal funds rate further from current levels would heighten the risk of financial instability, particularly by fueling a melt-up in equity markets. A similar dynamic is already evident in precious metals. Additional rate cuts would also put further downward pressure on the dollar, potentially reigniting inflationary pressures.

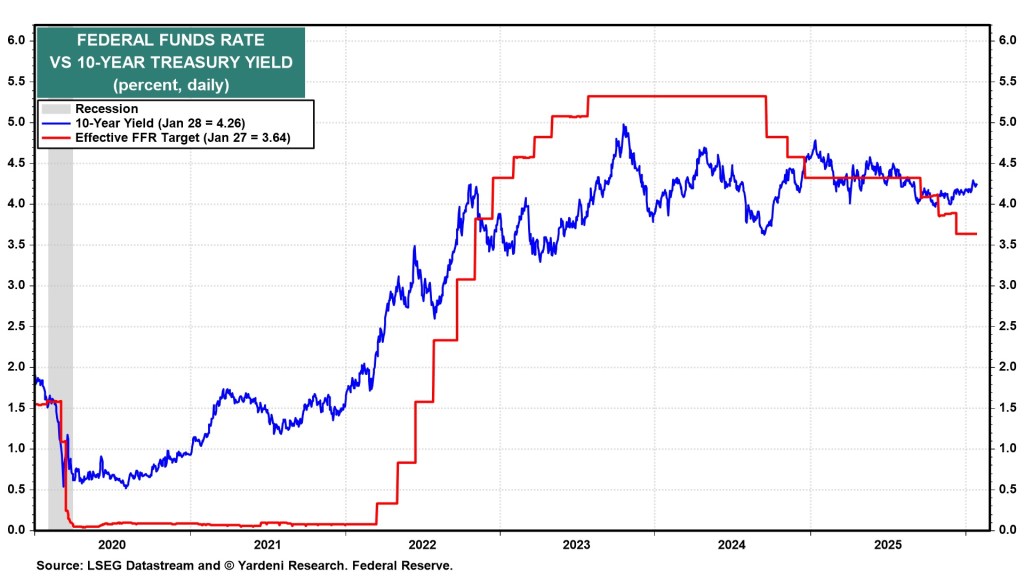

Bond markets appear to share this skepticism. When the Fed reduced the federal funds rate by 100 basis points in late 2024, the 10-year Treasury yield rose by a similar amount. Even after another 75-basis-point cut late last year, the yield held around 4.00% and has since climbed to 4.26%. We continue to expect the 10-year yield to trade largely between 4.25% and 4.75% this year—levels that were typical in the period before the Global Financial Crisis.

Sources: Ed Yardeni

Leave a comment