The year ahead offers a clear divide between bullish and bearish outcomes for investors. Will 2026 deliver another period of above-average returns, or mark a turning point toward disappointment? Optimists contend that the foundations for a sustained rally remain intact. A robust technology cycle, heavy corporate investment, and supportive policy settings all suggest further upside. Pessimists, however, warn that key growth drivers are losing momentum, market leadership has become uncomfortably narrow, and underlying economic stress is increasingly evident.

After a strong 2025, investors are entering a shifting market environment. Liquidity is still plentiful, but concerns over stretched valuations, labor-market pressure, and consumer resilience are mounting. Much hinges on how long optimism can outweigh economic realities, and whether expected gains from artificial intelligence and capital spending arrive quickly enough to counteract the drag from debt burdens, interest costs, and widening inequality.

Sentiment remains broadly constructive, though far from unanimous. Equity strategists are split, while bond markets reflect expectations of rate cuts alongside rising recession risk. Fiscal stimulus may postpone a downturn, but it also exacerbates longer-term imbalances. For investors, the central challenge is maintaining objectivity. Both the bullish and bearish narratives are credible, and timing will be decisive. In fact, 2026 could validate elements of both cases, making adaptability the most valuable strategy.

Below, we examine the bullish and bearish scenarios for 2026 in detail, assessing the macroeconomic and market forces behind each view. By translating these dynamics into practical portfolio considerations, investors can prepare for either outcome. Ultimately, success in 2026 will hinge less on forecasting accuracy and more on disciplined risk management.

The Bullish Case

The bullish thesis rests on several core pillars: a fresh surge in technology-led investment, accommodative fiscal policy, improving liquidity conditions, and the ongoing strength of both corporate balance sheets and consumer activity. Together, these forces have propelled markets higher, and proponents argue they will continue to support gains through 2026.

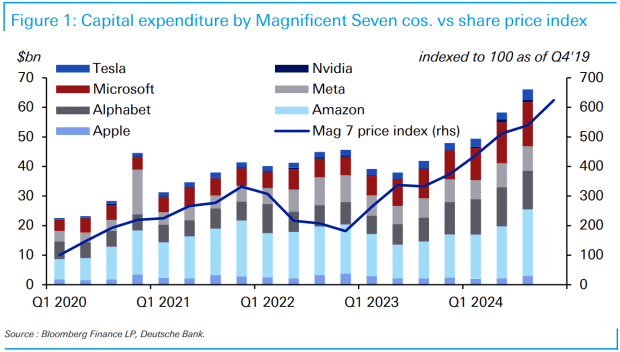

Central to the bull case is the rise of a potentially transformative technology cycle driven by artificial intelligence and large-scale infrastructure upgrades. Unlike earlier tech booms fueled primarily by optimism, this cycle is already translating into substantial capital spending. The so-called “Magnificent Seven” have collectively pledged over $600 billion toward data centers, semiconductor capacity, and AI-related services. This investment is rippling across software, energy, and industrial supply chains. Should the anticipated productivity improvements materialize, corporate earnings could accelerate, providing fundamental support for elevated valuations.

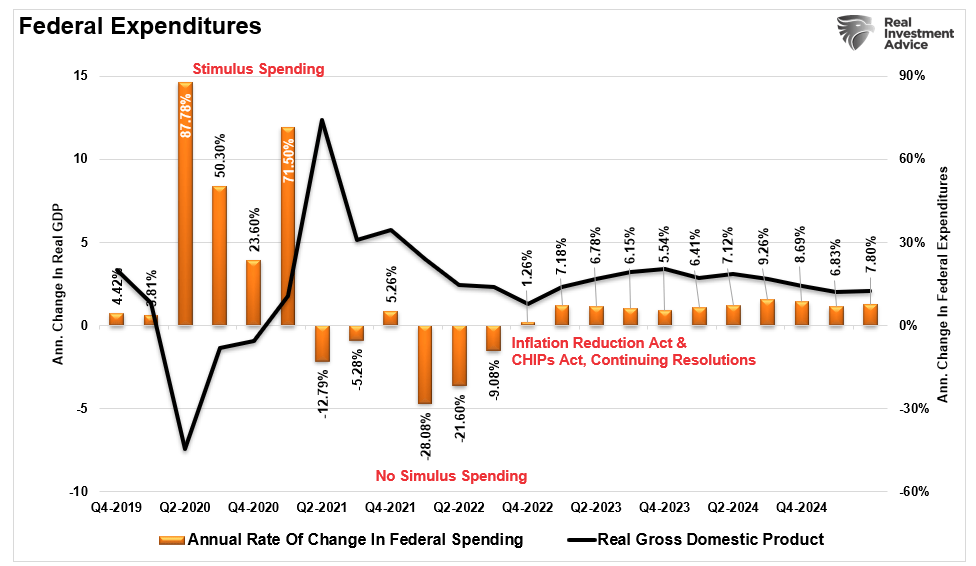

Fiscal policy is also positioned to support growth. Under a Trump-led administration, proposed tax cuts and direct transfers are expected to bolster both corporate activity and consumer spending. While $2,000 stimulus checks may not appear dramatic on their own, they can meaningfully lift short-term consumption and provide relief to small businesses. When paired with income tax reductions, these initiatives create a favorable backdrop for GDP growth and market sentiment. As recent history shows, following the 2022 market correction and widespread recession concerns, ongoing fiscal support has continued to play a stabilizing role in economic expansion.

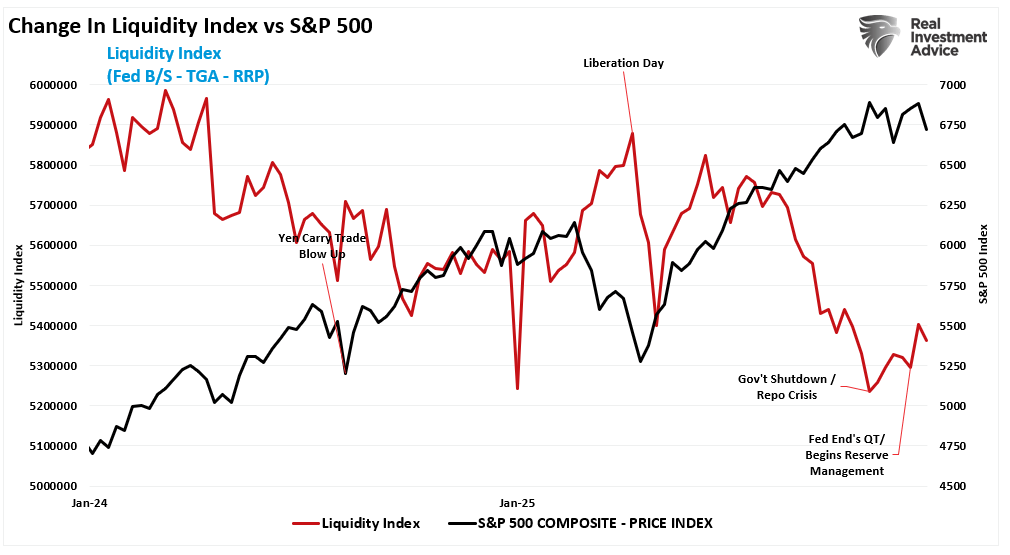

The monetary environment is also turning more supportive for bulls. Quantitative tightening concluded in December 2025, and the Federal Reserve has since shifted toward what many describe as “QE Lite,” combining rate cuts with monthly purchases of roughly $40 billion in short-term Treasuries. Officially framed as “reserve management,” the objective is to maintain ample liquidity within the financial system. As interest rates decline, credit conditions are likely to loosen, providing a favorable backdrop for risk assets. Rising liquidity has historically supported higher equity valuations, with technology and growth stocks typically benefiting the most from this dynamic.

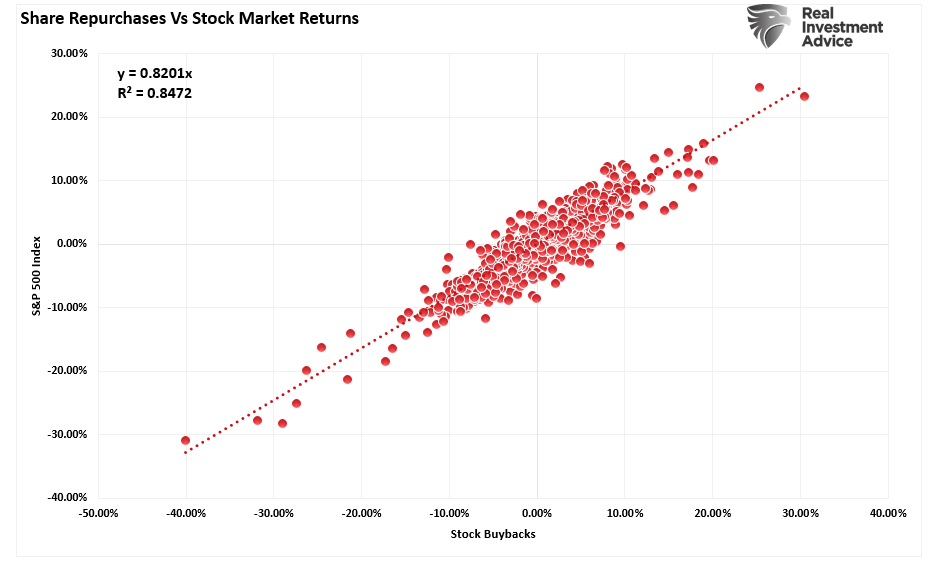

Corporate actions further reinforce the bullish narrative. Share buyback authorizations are projected to reach a new record of more than $1.2 trillion in 2026. Although often framed as a “capital return strategy”—a characterization that misses the point—buybacks have shown a strong correlation with equity market performance. Notably, since 2000, corporate repurchases have accounted for nearly all net equity demand, underscoring their outsized influence on stock prices.

Importantly, the notion that buybacks signal management’s confidence in future earnings is misleading. In practice, repurchases are frequently used as a form of financial engineering to boost per-share results and beat Wall Street expectations. This dynamic is likely to intensify in 2026, further supporting reported earnings growth and reinforcing the bullish case.

Finally, deregulation tied to the so-called “Big Beautiful Bill” is expected to relax capital requirements for banks, enabling them to hold a greater amount of collateral. While this should support the Treasury market, it also expands overall lending capacity. Much of that capacity is likely to flow into leverage for hedge funds and Wall Street trading desks, as looser regulatory constraints encourage greater risk-taking.

The bullish thesis ultimately rests on a reinforcing feedback loop: innovation spurs capital investment, rising investment lifts earnings, policy measures inject liquidity, and investors respond by increasing risk exposure. As long as each link in this chain remains intact, the upward trend can persist.

The Bearish Case

The bearish case starts with a key observation: many of the forces that powered the 2025 rally are now fading or already fully reflected in prices. Elevated valuations, softening economic data, and rising speculative excesses suggest that current market momentum may be masking deeper structural vulnerabilities. With that in mind, it is worth examining several of these risks more closely.

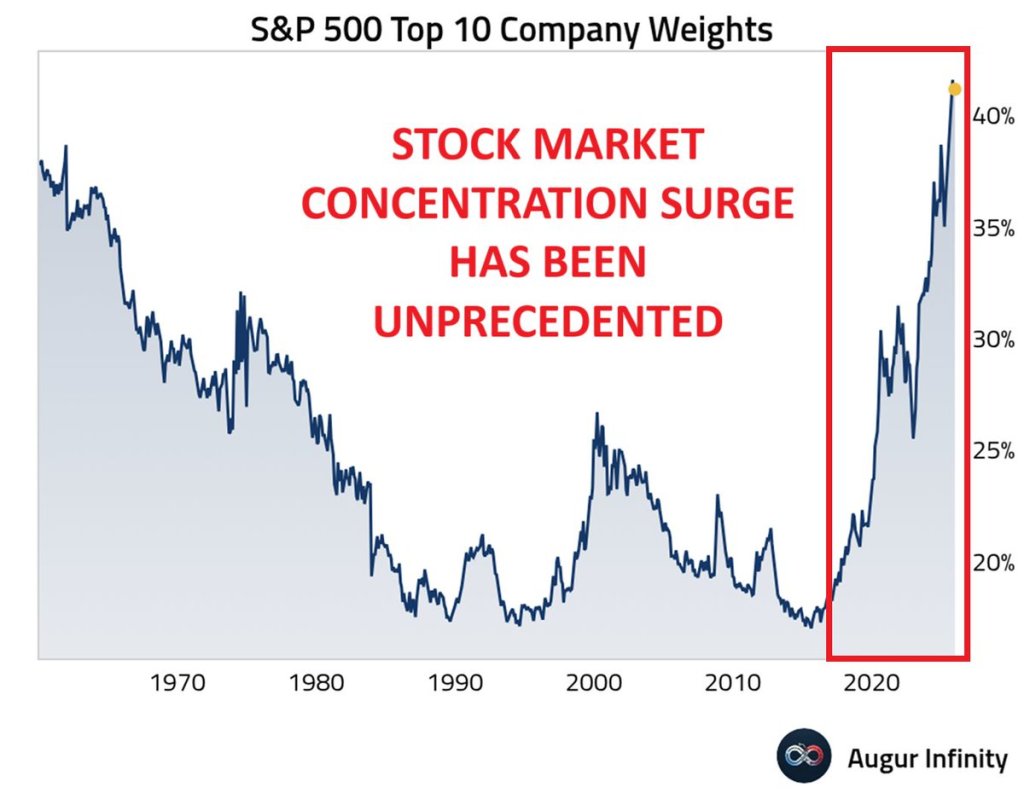

One of the most visible concerns is market concentration. In 2025, the bulk of equity gains came from just 10 companies on a market-capitalization-weighted basis, a dynamic amplified by the continued shift into passive ETF investing.

Passive investing has evolved from a niche approach into the dominant force shaping equity markets. Index funds and ETFs now represent more than half of U.S. equity ownership. Because these vehicles allocate capital according to market capitalization rather than valuation, fundamentals, or business quality, the largest companies attract a disproportionate share of inflows. This has created a powerful feedback loop in which rising prices draw in more capital, and those inflows, in turn, push prices even higher.

This narrow leadership is inherently fragile. Should investor flows into ETFs reverse, a disproportionate share of selling—roughly 40%—would be concentrated in the same 10 stocks. History shows that when market performance depends on a small handful of names, volatility tends to increase and drawdowns can be sharp.

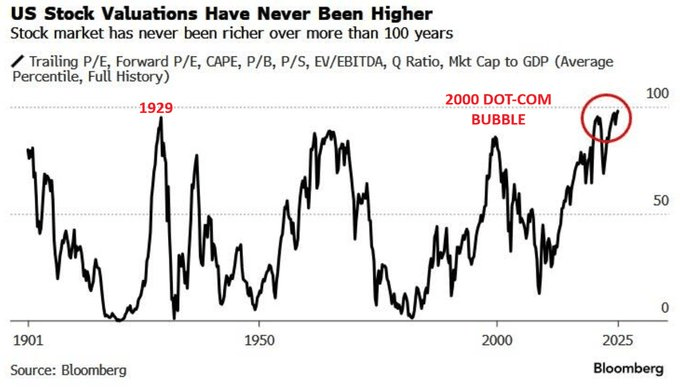

Valuations present another clear risk. Price-to-earnings multiples on the S&P 500 remain near cycle peaks, leaving little room for error. Growth assumptions are ambitious, and even modest earnings disappointments could trigger a meaningful repricing. While enthusiasm around AI has driven a surge in investment, much of this spending is circular—companies are investing in AI largely to produce and sell AI-related products. That dynamic may prove self-limiting over time, particularly if end demand weakens or costs begin to outstrip returns.

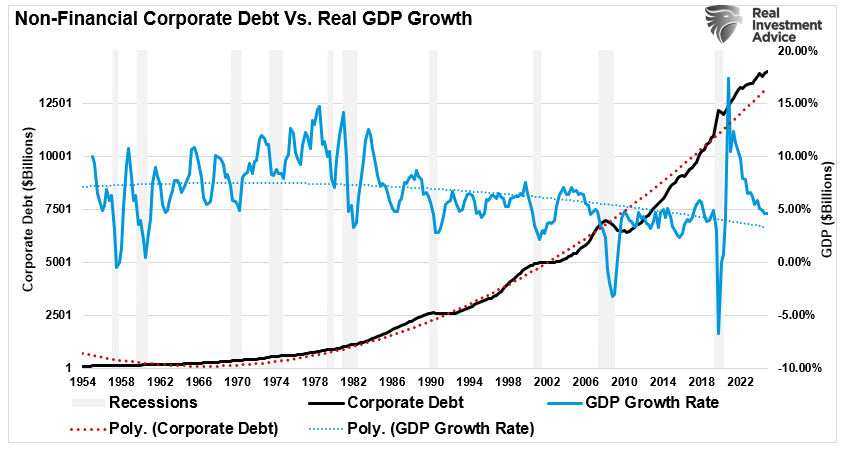

A significant portion of the current investment cycle is also being financed with debt, as companies borrow to fund capital spending, repurchase shares, and sustain dividend payouts. If interest rates remain high or credit conditions deteriorate, rising debt-servicing costs could quickly erode earnings gains.

The broader economic risk is that the reallocation of capital toward technology and automation could sideline large segments of the workforce. While the buildout of data centers may employ thousands during construction, only a fraction of those jobs—perhaps a few hundred—remain once operations begin. Over time, this dynamic could weigh on employment growth, increase the risk of demand destruction, and may already be showing early warning signs.

This dynamic underpins the concept of a “K-shaped economy.” While high-income households and asset owners continue to prosper, lower-income consumers are facing increasing strain. Consumption patterns are diverging as financially pressured households cut back, leaving the top 20% of earners responsible for nearly half of total consumer spending. Signs of stress are already emerging, with rising auto loan and credit card delinquencies, stagnant real wages for many workers, and persistently high costs for housing and essential goods.

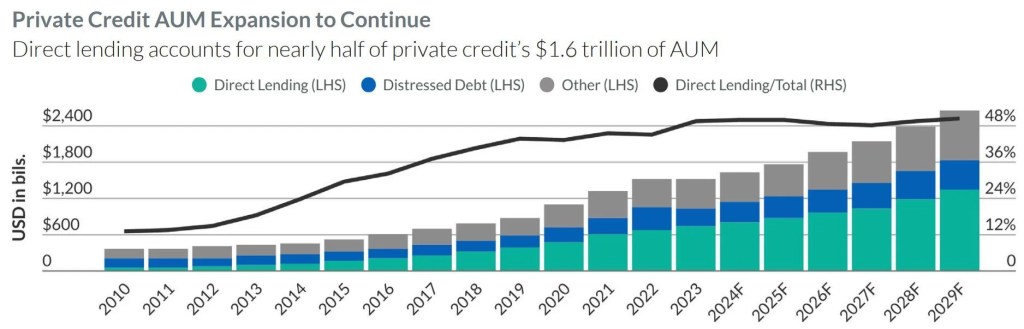

At the same time, risks within the credit system—particularly in private markets—are growing. Private credit has expanded rapidly in recent years, yet limited transparency makes it difficult to fully assess systemic vulnerabilities. Regulators have begun to pay closer attention, and default rates in middle-market lending are climbing. Should these stresses intensify, the fallout could extend across banks, hedge funds, and pension portfolios.

The bearish argument is not one of an imminent crash, but of growing fragility. Beneath the headline gains, the market appears increasingly exposed to earnings disappointments, tighter credit conditions, and weakening consumer demand.

The key takeaway is that 2026 may validate elements of both the bullish and bearish narratives. Preparation, rather than prediction, will be essential.

Navigating Whatever Comes Our Way

Investors should treat 2026 as a year in which both the bullish and bearish narratives may ultimately be validated. In the first half, bullish momentum is likely to persist, supported by strong sentiment, ample liquidity, and continued growth in corporate investment. Optimism around AI, fiscal support, and a potential pause in monetary tightening could propel equity indexes higher.

By the second half, however, underlying vulnerabilities may begin to surface. Elevated valuations increase sensitivity to earnings disappointments, while widening economic inequality could weigh on the outlook for consumer demand and corporate revenues. Should these pressures intensify, market sentiment could shift rapidly.

Navigating such a divided year will require a tactical approach—participating in early upside while avoiding excessive exposure to risks that may materialize later in the year.

Early 2026: Participate in Momentum, but Manage Exposure

- Overweight sectors poised to benefit from capital spending and ample liquidity, including technology, industrials, and energy.

- Prioritize high-quality growth companies with durable earnings and strong cash-flow generation, rather than momentum-driven narratives.

- Implement trailing stop-loss strategies to protect gains if market sentiment shifts.

- Use periods of volatility to add selectively, while scaling back position sizes as valuations become more stretched.

- Avoid excessive concentration in AI-related stocks, even during strong rallies, as crowding increases dispersion and downside risk.

Mid-to-Late 2026: Emphasize Defense and Cash-Flow Stability

- Gradually rotate toward defensive, value-oriented sectors such as healthcare, consumer staples, and utilities.

- Increase exposure to dividend-paying companies with strong balance sheets and resilient cash flows.

- Raise cash allocations or shift into short-duration Treasuries to preserve flexibility.

- Allocate selectively to high-quality credit while reducing exposure to private credit and high-yield debt.

- Monitor consumer credit conditions, labor-market trends, and bank earnings for early signs of financial stress.

Throughout the Year: Maintain Discipline and Objectivity

- Adhere to valuation discipline regardless of shifts in market narratives.

- Keep portfolios well diversified to withstand both volatility and sector rotation.

- Let data—not headlines—drive allocation decisions.

- Rebalance regularly, particularly if strong first-half performance leads to excessive concentration in certain sectors.

In 2026, tactical flexibility, risk awareness, and discipline are likely to matter more than adopting a purely bullish or bearish stance. It is a year in which both camps could be partially wrong. Markets rarely move in straight lines, but a sound investment process should remain consistent throughout.

The year ahead is likely to test investors with heightened volatility, as both the bullish and bearish arguments carry real weight. A new technology cycle may generate genuine economic momentum, yet it also introduces risks tied to elevated valuations, debt-fueled growth, and widening inequality. With markets effectively pricing in near-perfection, history suggests outcomes often fall short of expectations.

Whether 2026 delivers further gains or a sharp correction, performance will hinge on effective risk management. Avoid anchoring to any single narrative. Let data guide decisions, respect your signals, and remain willing to adjust as conditions evolve.

Ultimately, the objective is not to chase short-term returns, but to endure—and compound—across full market cycles.

Sources: Real Investment Advice

Leave a comment