Micron (MU) is a global leader in advanced memory and storage technologies, playing a critical role in converting data into actionable intelligence. The stock has surged amid the AI-driven rally, as Micron’s products have become an essential component of AI infrastructure, particularly in addressing persistent memory bottlenecks.

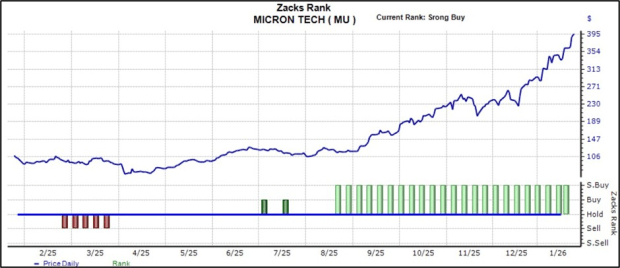

The shares also highlight the effectiveness of the Zacks Rank framework. In August of last year, Micron was upgraded to the highly sought-after Zacks Rank #1 (Strong Buy) following upward revisions to earnings estimates, a shift that has since been accompanied by a strong and sustained rally in the stock price.

As illustrated above, the Zacks Rank may also have helped mitigate downside risk last March.

Why Micron Shouldn’t Be Overlooked

Micron delivered outstanding results in its latest earnings report, surpassing consensus expectations on both revenue and earnings, driven by rapidly accelerating demand tied to AI workloads. Revenue surged more than 55% year-over-year to a record high, while adjusted EPS jumped an impressive 185%.

The company’s cash-generation profile also strengthened significantly amid the favorable demand backdrop. Operating cash flow reached a record $8.4 billion during the period, sharply exceeding the $5.7 billion generated in the same period last year.

The positive momentum appears set to continue, with Micron’s Q2 guidance pointing to new records across revenue, margins, earnings, and free cash flow. In short, Micron plays a critical role in enabling the AI boom, as memory capacity remains a key bottleneck in advanced systems. This strategic positioning places the company in a strong overall stance and helps shield it from concerns about being an AI “also-ran” or laggard.

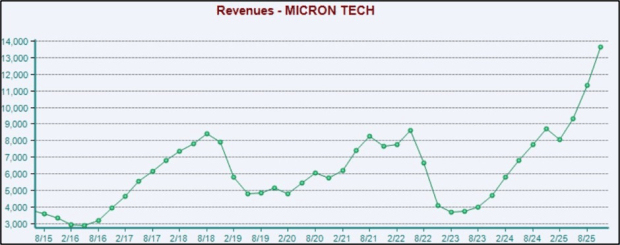

As illustrated below, Micron’s revenue has surged sharply in recent periods, reinforcing the strength of the current demand environment. The company’s top-line trajectory mirrors that of NVIDIA (NVDA – Research Report), widely regarded as the flagship beneficiary of the broader AI trade.

Micron vs. NVIDIA

While many AI-linked companies are likely to come under increased scrutiny in 2026, Micron represents a far more straightforward beneficiary of the broader infrastructure buildout. Memory remains a key bottleneck in AI systems, and MU has been capitalizing meaningfully on this constraint. The company recently announced its exit from the consumer memory segment, further underscoring its strategic focus on maximizing revenue from large-scale enterprise and data-center customers.

Micron noted that “AI-driven growth in the data center has led to a sharp increase in demand for memory and storage,” adding that the decision to wind down its Crucial consumer business was made to improve supply allocation and support for larger, strategic customers in faster-growing markets.

Overall, Micron stands out as one of the most compelling AI-related investment opportunities, drawing a clear parallel with NVIDIA. While NVIDIA dominates the GPU side of AI computing, Micron plays an equally critical role by supplying the high-performance memory required for those GPUs to operate efficiently.

Turning to NVIDIA, the company once again delivered a double beat versus consensus in its latest, record-setting earnings report. Revenue reached $57 billion, up 62% year-over-year, alongside a 67% surge in earnings per share. Data Center revenue climbed to $51.2 billion, representing a robust 66% annual increase and comfortably exceeding consensus expectations of $49.1 billion.

For investors looking to capitalize on the AI infrastructure buildout, both Micron (MU – Research Report) and NVIDIA (NVDA) stand out as premier choices, with each currently holding the highly sought-after Zacks Rank #1 (Strong Buy).

Leave a comment