Geopolitical tensions are rising as President Trump moves ahead with threats to levy tariffs on eight NATO allies while continuing his push regarding Greenland. Although overall markets have weakened, these frictions may spur higher defense budgets, accelerated resource reshoring, and expanded infrastructure investment. Below, we identify five U.S.-based companies that stand to gain from the intensifying U.S.–NATO standoff.

As tensions between the U.S. and NATO escalate over fresh tariffs and Greenland’s strategic resource base, defense, mining, and industrial shares appear well positioned for a strong upswing. Against this backdrop, five companies stand out—Lockheed Martin (NYSE:LMT), RTX (NYSE:RTX), Critical Metals (NASDAQ:CRML), Teck Resources (NYSE:TECK), and Caterpillar (NYSE:CAT). Each is set to benefit from increased U.S. defense spending, intensifying competition for Arctic resources, and ongoing efforts to shift supply chains away from Europe and China.

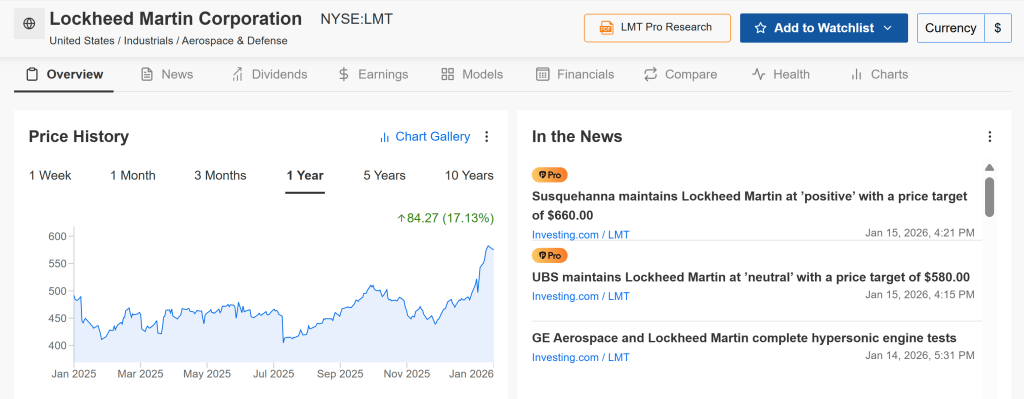

Lockheed Martin: A Leader in Arctic Defense Capabilities

Lockheed Martin appears to be among the primary beneficiaries of rising U.S.–NATO tensions, particularly as Greenland’s strategic value elevates the need for enhanced Arctic defense capabilities. The company’s advanced military platforms and surveillance systems are well suited to the region’s demanding operational environment.

Its F-35 fighter aircraft, along with missile defense and radar solutions such as the “Golden Dome,” play a central role in Arctic security, where Greenland’s geographic position strengthens U.S. monitoring capacity and deterrence against potential Russian and Chinese advances.

So far in 2026, Lockheed Martin’s shares are up roughly 19% year to date, supported by President Trump’s proposed $1.5 trillion defense budget for 2027, which points to expanded procurement activity. In periods of sustained geopolitical strain, investors typically favor companies with stable revenues and long-term contracts. Against this backdrop, Lockheed’s robust order backlog, strong free cash flow generation, and reliable dividend profile position it as a traditional “geopolitical hedge” stock.

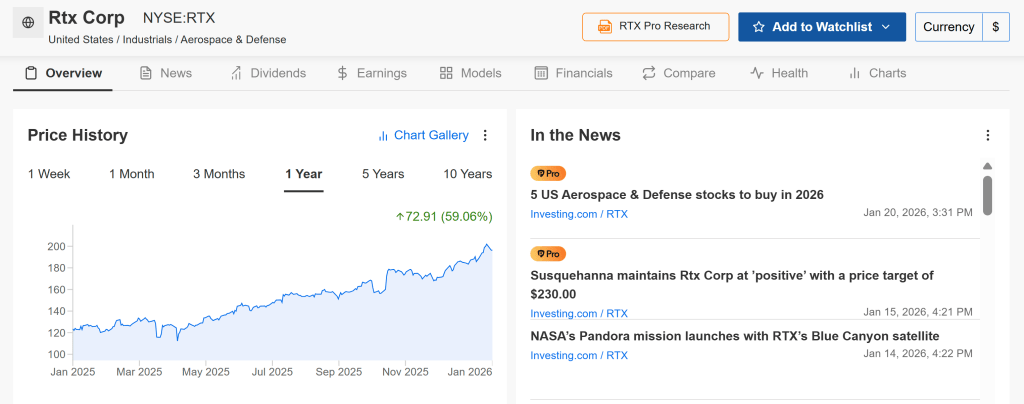

RTX: Rising Demand Across Aerospace and Missile Systems

RTX, formerly known as Raytheon, stands out as a key beneficiary due to its broad defense technology portfolio tailored to the demanding requirements of Arctic environments. The company’s missile defense and advanced radar solutions are central to securing and monitoring strategically vital regions such as Greenland.

In particular, RTX’s Patriot missile defense system is regaining prominence as governments prioritize battle-tested platforms capable of operating in extreme climates while defending against increasingly sophisticated threats.

RTX shares are up about 7% year to date in 2026, following a strong 60% advance in 2025, with a record backlog of $251 billion underpinning continued momentum.

Looking ahead through the rest of 2026, RTX remains attractive amid rising orders from the Middle East, its inclusion in leading defense-focused ETFs, and expectations for roughly 20% earnings growth.

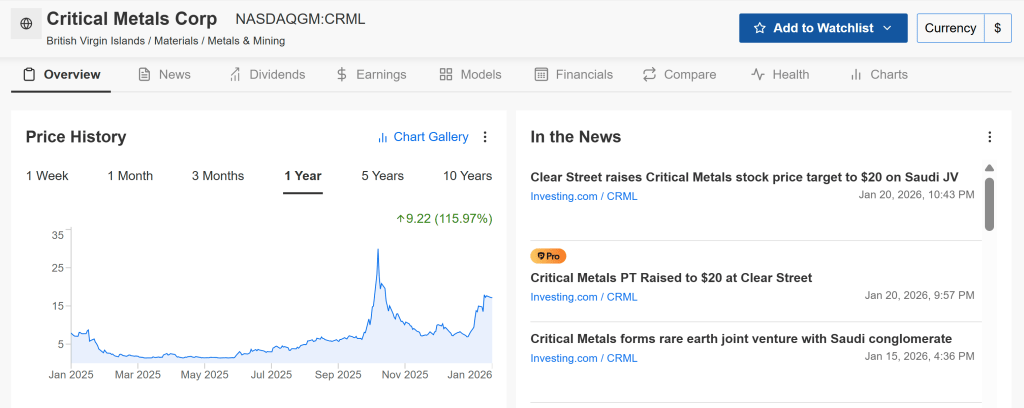

Critical Metals: Unlocking Greenland’s Rare Earth Potential

Critical Metals controls the Tanbreez project in Greenland, the largest non-Chinese rare earth deposit globally, directly linking the company to U.S. strategic resource objectives. Heightened geopolitical tensions could accelerate Washington’s push to secure access to these materials, which are essential for defense systems, missile technologies, and electric vehicles—reducing reliance on China and enhancing CRML’s strategic importance.

In addition, the company’s proprietary rare earth processing capabilities and its focus on North American operations position it to benefit from government initiatives aimed at strengthening domestic critical-materials supply chains and expanding strategic mineral stockpiles.

CRML shares have surged nearly 150% so far in 2026, propelled by strong high-grade drilling results and regulatory approval for its pilot processing plant in Greenland.

While the stock carries elevated risk, it offers substantial upside potential this year, with the possibility of capturing up to 50% of the Western rare earth supply. Despite ongoing volatility, secured offtake agreements and heightened U.S. national security priorities support the bullish case, with the stock still trading at an estimated 22% discount to net present value.

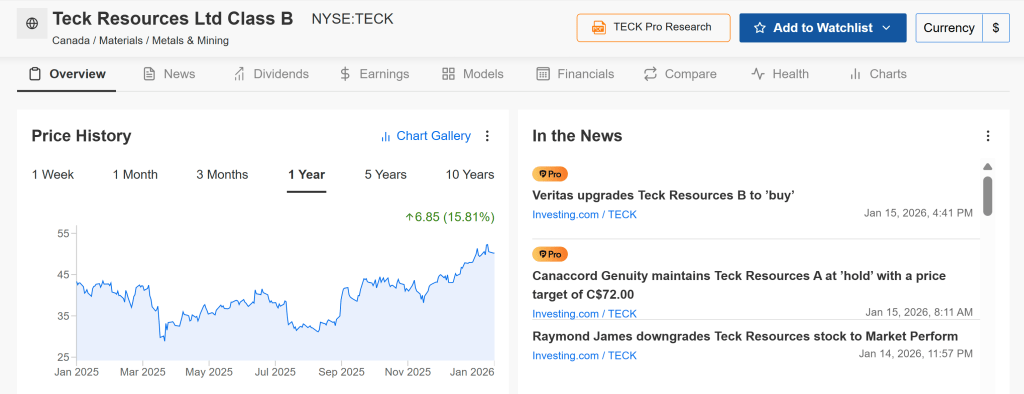

Teck Resources: A Global Metals and Mining Leader

Teck Resources is a leading diversified mining company with significant exposure to steelmaking coal, copper, zinc, and other essential industrial metals. While its operations are not exclusively Arctic-centric, Teck’s asset base firmly places it within the strategic raw materials space that underpins infrastructure development, defense manufacturing, and the global energy transition.

Should 2026 be marked by robust commodity demand, sustained decarbonization spending, and intensifying geopolitical rivalry, diversified miners such as Teck are well positioned to benefit from favorable pricing dynamics and rising shipment volumes.

TECK shares are up roughly 5% year to date, notching fresh 52-week highs as copper prices rally and investors rotate into the materials sector.

Looking ahead, Teck presents a compelling copper-focused opportunity, with its merger with Anglo American set to create a top-five global producer, unlock an estimated $800 million in synergies, and benefit from AI-driven demand growth. Analyst price targets in the $80–90 range are underpinned by structural supply constraints and sustained long-term commodity demand.

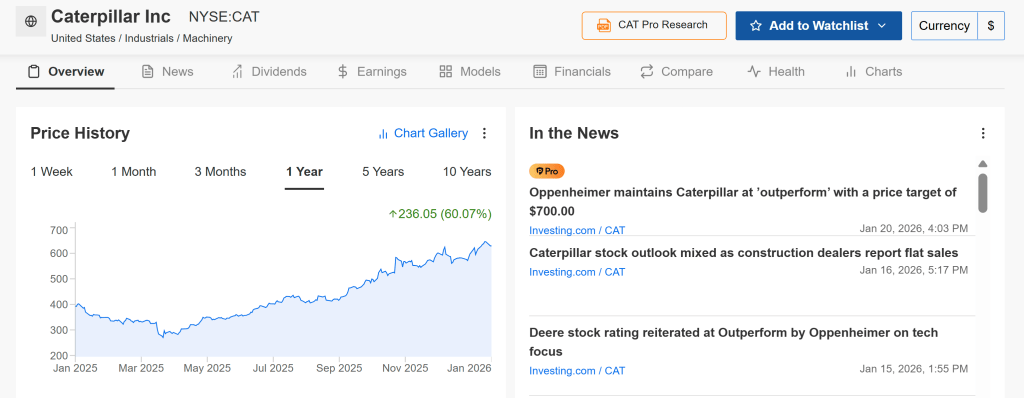

Caterpillar – Infrastructure & Arctic Expansion

Caterpillar stands out as a key beneficiary through its portfolio of heavy machinery and construction equipment critical to Arctic infrastructure expansion, including military installations, transportation networks, and mining projects.

Its specialized cold-weather and Arctic-rated equipment gives Caterpillar a distinct advantage in supporting development across Greenland and other high-latitude regions that gain strategic relevance amid heightened geopolitical tensions.

CAT shares are up roughly 10% year to date in 2026, building on a strong 58% gain in 2025, supported by a record backlog of $39.9 billion.

Looking ahead, Caterpillar remains a solid hold for 2026, with earnings per share projected to grow about 20.5%, aided by continued spending under the U.S. Infrastructure Act and expanding construction tied to AI-driven data center development.

Sources: Jesse Cohen

Leave a comment