- This week, market attention will be on CPI inflation figures, retail sales data, and the kickoff of the Q4 earnings season.

- Morgan Stanley is expected to see gains driven by robust quarterly results.

- Meanwhile, Capital One Financial is likely to face challenges due to a proposed cap on credit card interest rates.

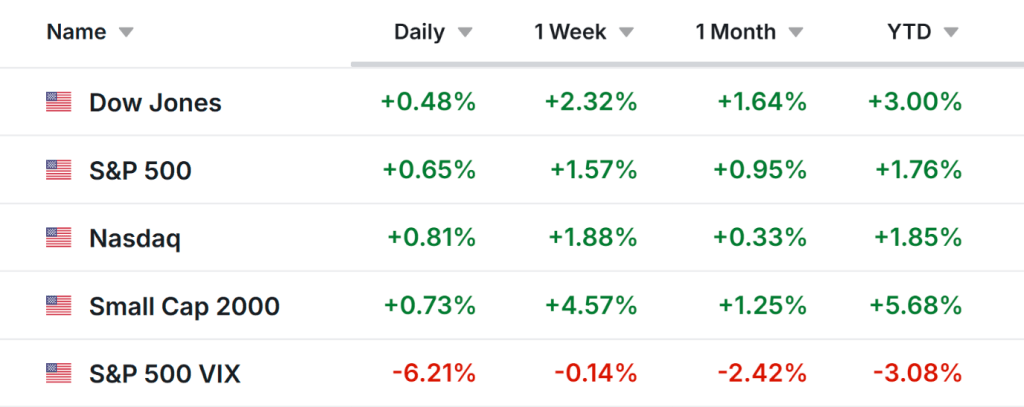

The stock market closed the first complete trading week of 2026 with the Dow Jones Industrial Average and S&P 500 reaching record levels, buoyed by the latest employment report.

Wall Street’s major indexes enjoyed a strong week, with the Dow Jones Industrial Average rising 2.3%, the S&P 500 gaining 1.6%, the tech-focused Nasdaq Composite climbing 1.9%, and the small-cap Russell 2000 soaring 4.6%.

Looking ahead, the upcoming week promises significant market activity as investors assess economic prospects and interest rate trends.

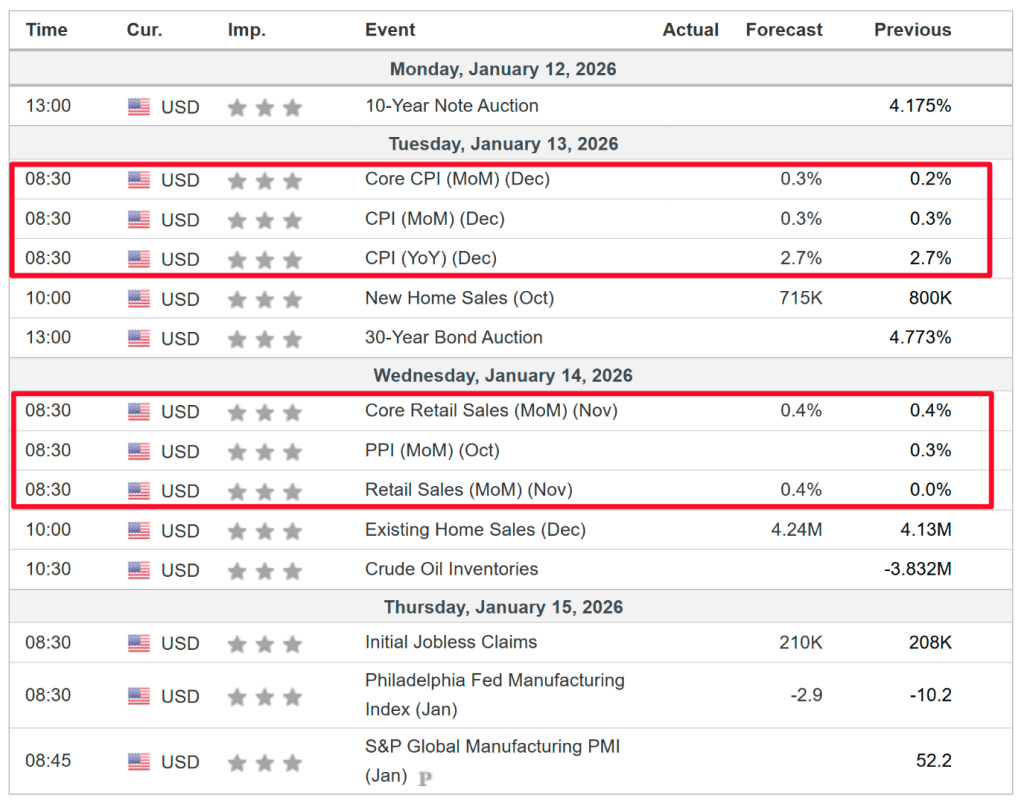

Key events on the economic calendar include Tuesday’s U.S. consumer price inflation report for December, which could trigger market volatility if the data exceeds expectations. This report will be released alongside producer price figures, offering a broader view of inflation, as well as the December retail sales numbers.

Additionally, the Q4 earnings season is about to begin, featuring major companies such as JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, Goldman Sachs, Morgan Stanley, BlackRock, Delta Air Lines, and Taiwan Semiconductor set to report their results.

Additionally, the Supreme Court may deliver a ruling on the Trump tariffs this week, after not doing so last Friday.

No matter how the market moves, below I identify one stock expected to attract buying interest and another that might face renewed selling pressure. Keep in mind, my outlook covers just the upcoming week, from Monday, January 12 to Friday, January 16.

Morgan Stanley: Top Stock Pick to Buy

Morgan Stanley is set to deliver one of the strongest earnings reports in the financial sector this quarter, fueled by a notable rebound in mergers and acquisitions, a thriving IPO underwriting business, and strong results across its core investment banking divisions.

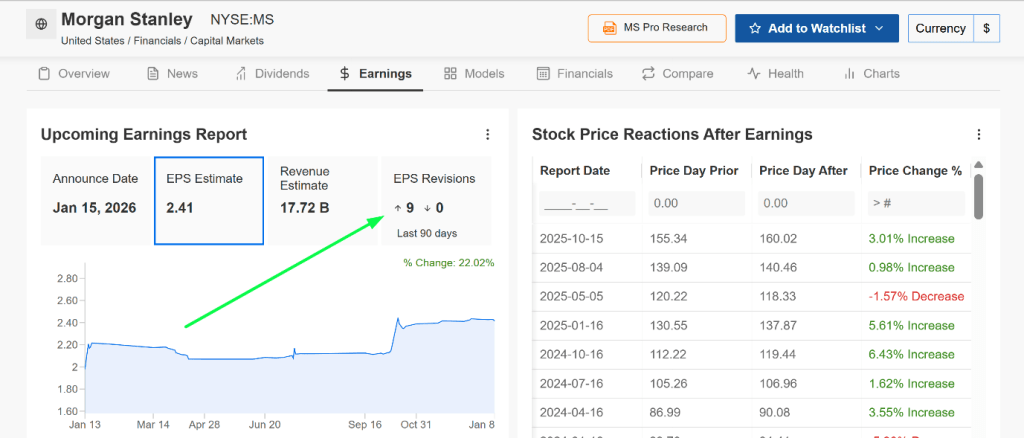

The company will release its Q4 results before the market opens on Thursday at 7:30 AM ET. Investors anticipate significant volatility in MS shares following the announcement, with options markets pricing in a potential move of about ±4.2% post-earnings.

Analysts hold a positive outlook, with all nine recent earnings revisions reflecting upward adjustments, highlighting Morgan Stanley’s strong presence in high-growth sectors such as AI-related financing and capital markets.

Morgan Stanley is projected to earn $2.41 per share, an 8.5% increase compared to last year, while revenue is expected to rise 9.4% year-over-year to $17.72 billion. This growth is anticipated to be driven by a rebound in global mergers and acquisitions, alongside robust performance in IPO underwriting and trading revenues.

In recent quarters, Morgan Stanley has effectively increased its market share in high-margin advisory services while sustaining its leading role in equity and debt underwriting, both of which contribute significant fee income when market conditions are favorable.

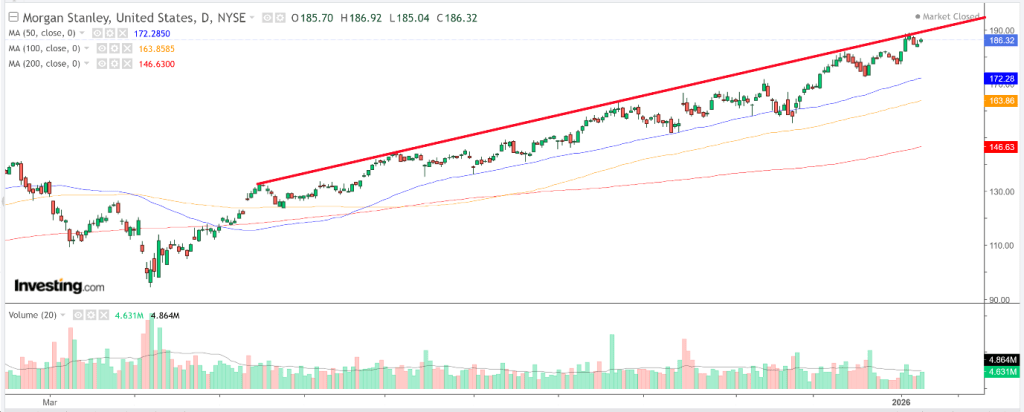

Technically, Morgan Stanley’s shares closed near $186.50 on Friday, trading above key moving averages and displaying bullish momentum ahead of the earnings report. Should the company deliver strong results with an optimistic outlook, the stock could push toward $200 shortly, making it an appealing buy for investors confident in the financial sector’s continued strength.

InvestingPro’s AI-driven quantitative model assigns Morgan Stanley a ‘GOOD’ Financial Health Score of 2.65, indicating solid capital reserves, strong liquidity, and a long history of dependable dividends.

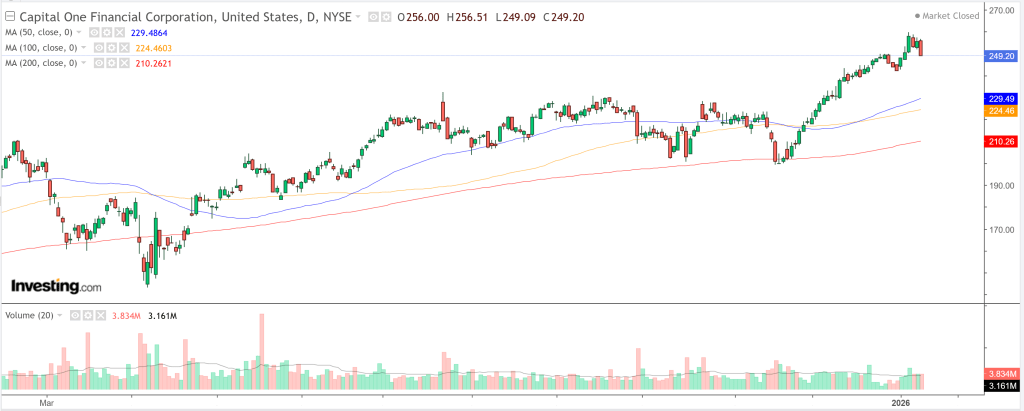

Capital One Financial: Recommended Sell

On the other hand, Capital One Financial, a leading credit card lender, is expected to face considerable selling pressure this week following President Trump’s announcement of a temporary 10% cap on credit card interest rates. This policy, designed to alleviate consumer financial strain, poses a direct threat to the profitability of lenders that depend heavily on interest income from credit cards.

Given its large consumer credit card portfolio, Capital One is particularly exposed. With average credit card interest rates typically between 20-30%, a 10% cap would wipe out most of the company’s net interest income, which forms the backbone of its overall profits.

The proposed interest rate cap poses an urgent and substantial challenge to Capital One’s financial results, forcing the company to either accept sharply lower profits or withdraw from large segments of the credit card market that would no longer be financially viable.

Even prior to this announcement, Capital One Financial was struggling with increasing charge-offs and slowing loan growth, leaving the stock susceptible to further declines.

Shares closed around $250 on Friday, but if upcoming earnings (due January 22) reveal worsening credit quality or management signals concerns about future profitability, the stock could drop to $229 or below—a decline of 8-10% from current levels.

Whether you’re a beginner investor or an experienced trader, using InvestingPro can help you discover investment opportunities while managing risks in today’s challenging market environment.

Sources: Investing

Leave a comment