Narrative control functions by offering ready-made answers to every doubt or challenge. At its core, the prevailing narrative claims that the Federal Reserve and the central government possess sufficient tools to quickly counter any decline in GDP—otherwise known as a recession—and steer the economy back toward growth.

Implicit in this view is the assumption that recessions are inherently harmful, while uninterrupted expansion is inherently desirable. Few question the fact that this framework departs from true free-market capitalism. Instead, central banking and government intervention are justified as mechanisms to smooth out capitalism’s rough edges through a form of state capitalism—one that can create or borrow as much money as needed to neutralize economic disruptions, including recessions.

What this narrative leaves out is the role recessions play as a natural and necessary part of market dynamics. Instead, it reduces economic cycles to a simplistic binary: contraction is bad, expansion is good. Yet markets are ultimately driven by human behavior—particularly fear and greed—which express themselves through borrowing and speculation. During periods of confidence, when growth appears limitless, participants take on increasing levels of debt and channel capital into progressively riskier investments in pursuit of higher returns.

As borrowed funds flow into speculative assets, prices rise, boosting the value of collateral and enabling even more borrowing to finance further speculation. Debt, asset prices, collateral and risk-taking thus reinforce one another, creating the illusion of an endlessly self-sustaining expansion in which everyone appears to grow wealthier.

However, this layering of debt and paper wealth carries within it two forces that eventually unwind the process: interest and risk. Every loan carries an obligation to pay interest, which compensates lenders for the risks they assume. As overall debt grows—and as investments become more speculative—debt servicing costs increase accordingly, especially for higher-risk borrowers.

While central banks can attempt to suppress interest rates even as risk rises, their influence is inherently limited. They control only a portion of total outstanding debt and therefore cannot dominate the market entirely.

Their role in prolonging debt expansion and speculation relies less on absorbing most new debt and more on signaling. By projecting the message that the Federal Reserve will step in to backstop losses, recapitalize lenders, and cap interest rates below market-clearing levels, policymakers encourage continued borrowing and risk-taking. This reinforces the belief that debt and speculation can keep expanding indefinitely.

Yet signaling alone cannot solve the underlying problem. It does not increase the income required to service growing debt burdens, nor does it ensure speculative investments will deliver returns. These limitations expose the fundamental weakness of the central banking “perpetual motion” model. For most borrowers—both private and public—income does not automatically rise alongside debt. Instead, income depends on market conditions, technological change, government policy, and the broader cycle of credit expansion or contraction.

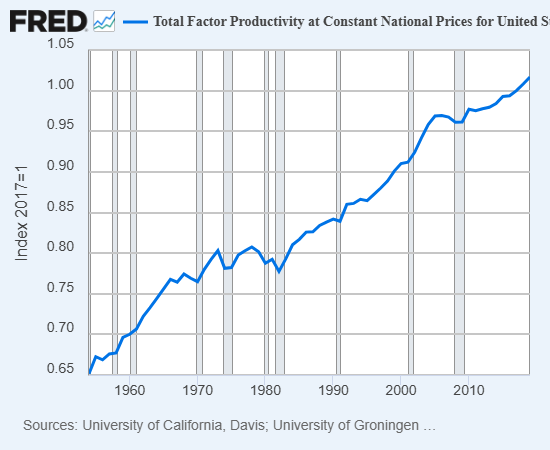

At the level of the overall economy, what ultimately matters is total factor productivity and how its gains are distributed among workers, businesses, asset owners, and the state, which extracts revenue from each through taxation. This distribution is not fixed; it shifts with changing social, political, and financial forces.

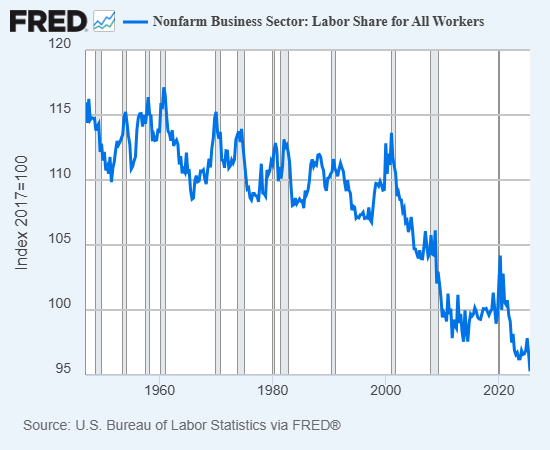

Over the past five decades, the benefits of productivity growth have increasingly accrued to capital—corporations and asset owners—rather than to workers. As a consequence, households and small businesses are left servicing debt with a diminishing share of overall economic income. This imbalance makes additional borrowing progressively more hazardous for both borrowers and lenders alike.

As a growing share of economic output accrues to corporations and asset owners, their collateral values, income streams, and perceived creditworthiness strengthen. This allows them to borrow larger sums at lower interest rates than wage earners and small businesses. Greater access to cheap credit enables further asset accumulation, which in turn generates additional income—creating a self-reinforcing cycle.

This dynamic sits at the heart of widening wealth and income inequality. Those at the top grow richer not simply because they earn more, but because they can finance income-producing assets at costs far below those faced by workers. Unlike wages, income derived from assets tends to rise alongside asset values, which can be leveraged as collateral to support even more borrowing.

At a deeper structural level, the system becomes unstable once economic growth fails to raise household incomes enough to support higher debt servicing. The entire framework of expanding credit, collateral, and speculation then comes under strain. Asset-driven income ultimately depends on one or more of three forces: continued credit expansion, increased risk-taking in financial markets, or sustained consumer spending. These forces are tightly linked, as any slowdown in borrowing, investing, or spending eventually undermines the ability to service debt and brings the credit cycle to a halt.

Because debt inherently carries default risk, an economic model reliant on ever-expanding borrowing also amplifies systemic vulnerability—particularly when household incomes stagnate while debt levels and interest obligations continue to rise.

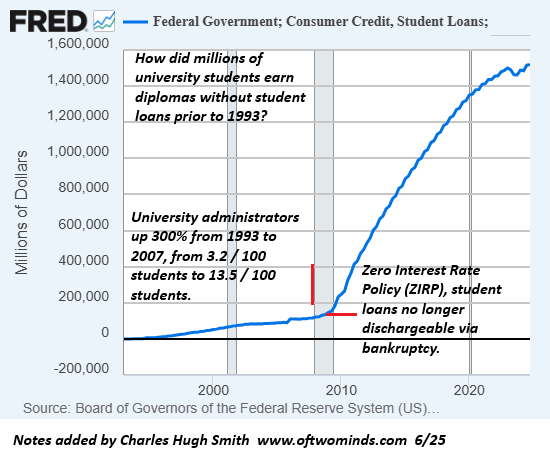

With the share of output flowing to wages declining for decades, households have increasingly relied on borrowing to sustain consumption. Before the 2000s, student debt was relatively limited; today it totals trillions of dollars. Auto loans and credit card balances have also surged, alongside less visible forms of leverage such as installment-based financing and other shadow-banking channels that are often underreported.

Speculative investments carry intrinsic risk, as there is no guarantee they will generate returns. When such speculation is financed through borrowing, failure does not only harm the investor—it also inflicts losses on the lender, as both sides are exposed when the bet collapses.

Taken together, stagnant income growth, rising reliance on debt to sustain consumption, and increasingly risky, debt-backed speculation have produced an economy dependent on credit-driven asset bubbles. Growth now hinges on the continual expansion of debt to support spending and fuel speculative activity that inflates asset prices, thereby boosting collateral values and enabling even more borrowing.

When income growth can no longer keep pace with rising debt obligations, defaults begin to ripple through the system. Households fall behind on rent, auto loans, student debt, credit cards, and mortgages, triggering a collapse in consumer spending. The resulting strain spreads to lenders and employers, who respond by tightening credit, cutting back borrowing, and laying off workers—further eroding income across the economy.

Speculative investments that appeared viable during the expansion unravel as credit conditions tighten. Lenders withdraw from riskier loans, household demand dries up, and asset prices fall as investors rush to sell risk assets in order to raise cash and reduce leverage. Collateral values deteriorate rapidly, amplifying losses.

Economies dependent on credit-fueled asset bubbles function as tightly interconnected systems. Any decline in income or asset prices, any increase in interest rates, any reduction in available credit, or any erosion of collateral feeds back into the broader structure. These shocks reinforce one another, creating a downward spiral marked by defaults, layoffs, and falling valuations.

In an economy already saturated with debt, policy stimulus no longer produces real growth; instead, it fuels inflation, which constrains central banks’ ability to respond. Once markets lose confidence in the belief that policymakers will always step in to backstop losses, both speculation and the borrowing that sustained it begin to dry up. As the flow of new, credit-funded investment slows, asset prices enter a self-reinforcing decline.

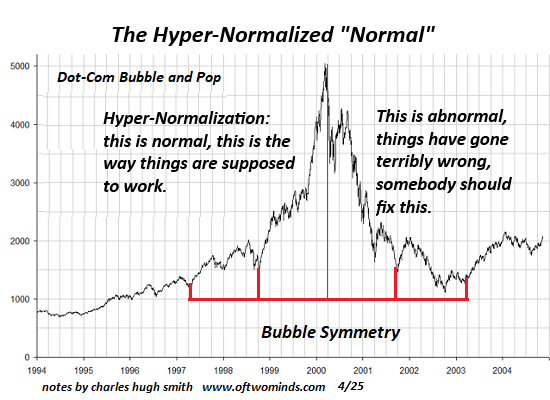

In a credit-asset-bubble-dependent system, this inevitable unwinding is often perceived not as a structural outcome, but as a sudden and unforeseen crisis.

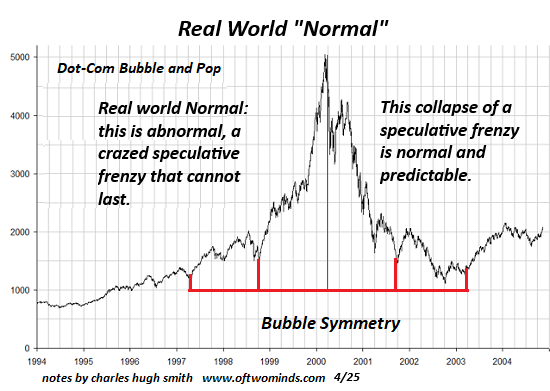

In an economic system that permits recessions to purge unsustainable debt and excess speculation, the bursting of credit-driven asset bubbles is seen as a natural and unavoidable process rather than an aberration.

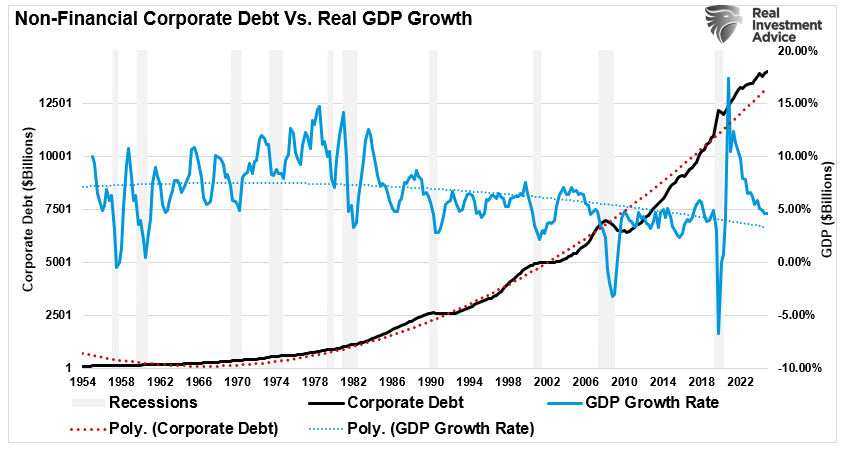

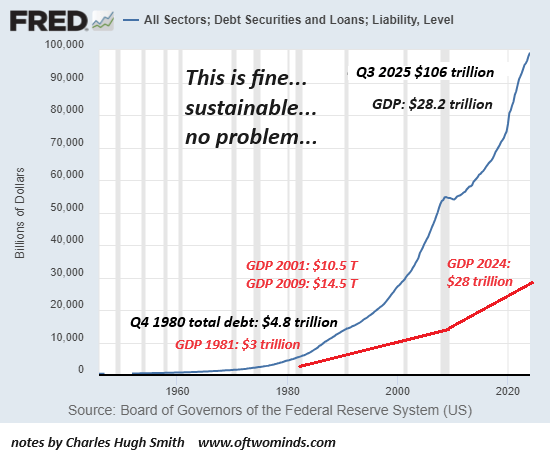

Few recognize two critical realities: first, the last true recession that meaningfully purged excess debt, leverage, and speculation occurred in 1980–82—more than four decades ago; second, the shock absorbers that enabled recovery back then no longer exist. In 1980, total debt stood at roughly 150% of GDP. Today, it is closer to three times GDP. This makes debt-driven expansion unworkable: borrowers are already struggling to service existing obligations, let alone take on more.

Nor can the Federal Reserve rescue the system simply by cutting rates to zero. The Fed holds only a small fraction of the roughly $106 trillion in outstanding debt; its primary influence is psychological, signaling that risk is low. In reality, risk continues to rise as debt burdens, interest costs, leverage, and speculation compound.

A repeat of the 2008-style bailout is equally implausible. Then, the system was stabilized by recapitalizing the financial sector—the engine of new credit creation. Today, however, the economy is saturated with debt, incomes have stagnated, and borrowers lack the capacity to sustain additional leverage. Meanwhile, housing and financial asset bubbles have expanded to historically fragile extremes.

This is why a recession that finally cleanses excess debt and speculation would leave behind an economy unable to rebound. The current system depends entirely on debt, leverage, and speculative excess not just for growth, but for basic stability. Once that structure collapses—as all bubbles eventually do—the confidence, signaling, and perceived wealth that sustained it will vanish as well.

Proposals to “save” the system by shifting fiat money into gold or cryptocurrencies offer no escape. The debt itself—and the income required to service it—would also be carried over, leaving the underlying dynamics unchanged. The collapse of credit-driven asset bubbles, and the economic activity built upon them, would still unfold.

For this reason, the next recession is likely to trigger a full-scale breakdown of a credit-asset-bubble-dependent economy. While policymakers may attempt to reflate another bubble as a solution, such an approach will no longer be sustainable. A durable recovery would instead require restructuring the economy around real productivity gains that are broadly shared, rather than concentrated among asset holders.

This transition will be slow and painful. Those who benefited most from the bubble economy will resist losing both extraordinary returns and their disproportionate share of gains. Yet neither can be preserved. The adjustment will demand time, sacrifice, and large, long-term investment in genuinely productive assets.

Ultimately, the systemic risks embedded in a credit-asset-bubble economy cannot be eliminated—only disguised or shifted elsewhere. These temporary fixes allow the bubble to grow larger, but the cost is borne by society at large when the system’s internal dynamics inevitably bring it crashing down.

Sources: Charles Hugh Smith