U.S. President Donald Trump told Reuters on Thursday that the United States should play a role in determining Iran’s next leader, adding that it would be “great” if Iranian Kurdish fighters based in Iraq crossed into Iran to attack government security forces.

In a phone interview, Trump said he believes the successor to the late Ali Khamenei is unlikely to be Khamenei’s son, Mojtaba Khamenei, who had been considered a leading candidate after his father was killed in a military strike at the beginning of the war.

“We’ll need to select that individual together with Iran,” Trump said, emphasizing that Washington must be involved in the decision.

The president also voiced support for Iranian Kurdish forces launching attacks against Iranian security forces. His comments came six days after the United States and Israel began strikes on Iran, a conflict that has killed more than 1,000 people—including at least six U.S. service members—and destabilized the wider Middle East.

“I think it would be great if they did that—I fully support it,” Trump said regarding Kurdish fighters.

Discussing Iran’s leadership transition, Trump compared the situation to Venezuela, where U.S. intervention removed Nicolás Maduro earlier in the year, leaving his deputy Delcy Rodríguez in power—a development Trump praised.

Trump said the United States wants to help shape Iran’s future leadership so the country does not repeatedly return to conflict every few years. He added that Washington hopes a new leader would benefit both the Iranian people and the nation as a whole.

After saying that Mojtaba Khamenei, who had been viewed as a leading contender to succeed his father, was unlikely to become Iran’s next leader, Donald Trump did not provide further details.

When asked whether the exiled Iranian crown prince Reza Pahlavi, the son of Iran’s last shah, could be considered for the role, Trump replied that all possibilities were still open, noting that the situation remained in its early stages.

Openness to Kurdish involvement

Responding to a question about whether the United States might provide air support for Iranian Kurdish forces considering an operation in western Iran, Trump declined to give a direct answer but suggested that their goal would be victory.

“If they decide to move forward with it, that’s fine,” he said.

According to three sources familiar with the matter, Iranian Kurdish militias have recently been in discussions with the United States about the possibility—and the strategy—of launching attacks on Iranian security forces in the country’s western regions.

The coalition of Iranian Kurdish groups, based along the Iran-Iraq border in the semi-autonomous Kurdistan Region, has reportedly been preparing for such an operation. Their aim would be to weaken Iran’s military while U.S. and Israeli strikes continue targeting sites across the country.

Trump also expressed confidence that the strategic shipping corridor known as the Strait of Hormuz would remain open.

Damage and energy market pressure

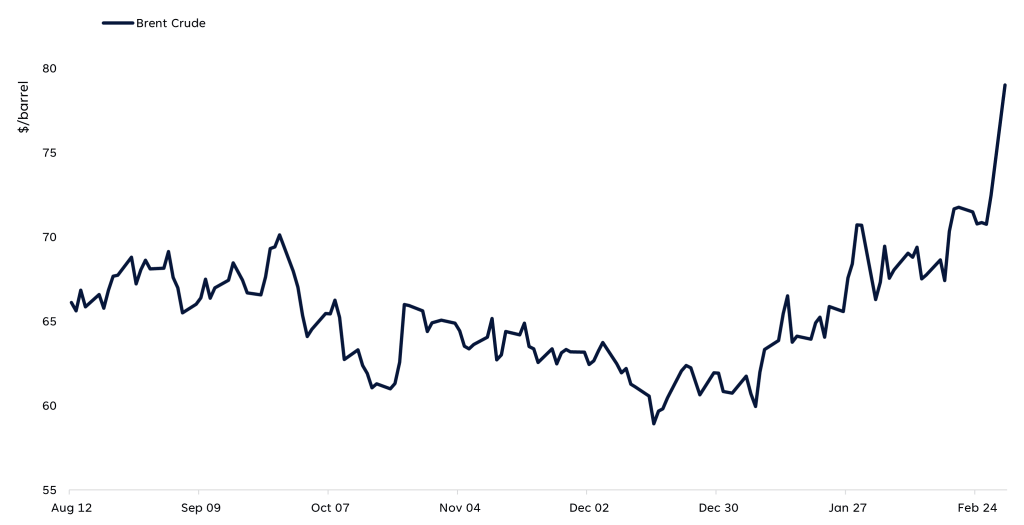

Iran has threatened to shut the Strait of Hormuz—a narrow passage between Iran and Oman—through which roughly one-fifth of global oil and liquefied natural gas supplies pass.

Shipping activity through the vital energy route has already slowed sharply after Iranian attacks struck six vessels, raising concerns about disruptions to global energy markets.

“They don’t really have a navy anymore—their fleet is essentially destroyed,” said Donald Trump, adding that he is monitoring the situation in the Strait of Hormuz very closely.

As the conflict intensified on Thursday, additional oil tankers were attacked in Gulf waters. At the same time, Iranian drones reportedly crossed into Azerbaijan, raising fears that the crisis could expand to involve more energy-producing regions. Since the fighting began, global oil prices have surged.

Trump said he was not worried about the rise in gasoline prices, arguing that they would likely fall quickly once the conflict ends. He added that even if fuel costs increase temporarily, the broader strategic issues at stake are far more important.

The president declined to estimate how long the war might continue but said events were progressing quickly and with greater force than many had anticipated. He added that, in his view, the conflict was unfolding faster and more decisively than expected.

Sources: Reuters