Even with the Iran peace deal easing geopolitical tensions, there are still four major risks that could drag markets lower. While the agreement reduced the worst-case war scenario, it did not fix the market’s deeper structural weaknesses.

Key Takeaways

- The peace agreement removed the extreme geopolitical risk, but markets still face underlying fragility. With war fears fading, equities must now rely on economic fundamentals again.

- According to Goldman Sachs strategist Brian Garrett, the recent rally appears driven more by short covering than by strong new bullish positioning. That type of momentum can spark a rebound, but often struggles to sustain a longer-term rally.

- Kevin Warsh’s upcoming Fed-related test could become critical. If markets interpret the Federal Reserve’s stance as more hawkish than expected, optimism from the peace deal may quickly fade under higher-rate concerns.

- AI regulation risks and an unprecedented wave of IPO supply are emerging as the next major pressure points. Potential government intervention in the AI sector, combined with massive fundraising from companies like SpaceX, Anthropic, and OpenAI, could pull liquidity away from existing equities.

The Bigger Concern for Markets

Bloomberg Markets Live columnist Jan-Patrick Barnert argues that removing Middle East war risk may have been the easy part. The bigger challenge now is navigating domestic and structural threats, including:

- A potentially hawkish Federal Reserve leadership path

- Washington increasing involvement in AI policy

- The largest equity issuance wave markets have ever seen

Although the US-Iran interim agreement scheduled for June 19 has helped calm fears surrounding the Strait of Hormuz, markets have already priced in much of that optimism. Brent crude has erased around 80% of its conflict-driven spike, suggesting investors largely expected this outcome.

Still, the situation remains fragile. Previous truces have weakened quickly, shipping conditions through Hormuz may normalize only gradually, and the agreement itself is not finalized yet. In other words, geopolitical risk has diminished — but it has not disappeared.

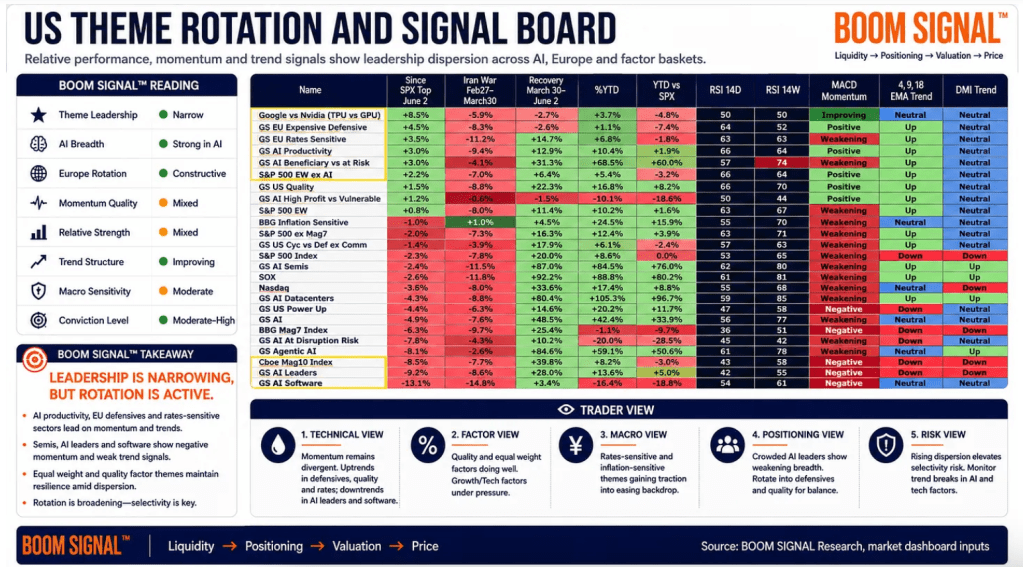

The first major concern is market positioning. Goldman Sachs derivatives strategist Brian Garrett argues that the recent early-summer rally has been fueled more by macro short covering than by genuine investor conviction. In other words, many bearish traders have simply been forced to close positions, rather than new bullish investors aggressively buying into the market.

Garrett explains that heavily crowded downside hedges have been unwound in a market that is still lacking a clear directional narrative. That is typical relief-rally behavior: price action may appear strong on the surface, but the momentum is being driven more by mechanical positioning adjustments than by fresh confidence in the economic outlook.

He also notes that investors are increasingly discussing the “broadening out” trade as they search for new opportunities beyond the dominant AI winners. Recently, popular AI-related stocks have slipped toward the bottom of short-term performance rankings, while broader and more defensive sectors have started to perform better.

However, Garrett stresses that the reason behind this broadening matters. If investors are rotating into new sectors because they see attractive growth opportunities and new alpha generation, that is constructive for markets. But if the rotation is mainly driven by traders covering crowded short positions, the rally becomes much more fragile and vulnerable to reversal.

Goldman’s prime brokerage data reinforces this concern. Hedge funds have increased exposure to US equities for four consecutive weeks, yet the latest buying activity was driven far more by the reduction of bearish beta shorts than by aggressive long positioning. According to Garrett, short covering exceeded new long buying by a ratio of 4.7-to-1.

That distinction is critical. A rally fueled primarily by bears exiting positions can ignite a sharp rebound, but sustaining a longer-term bull market usually requires genuine bullish capital stepping in with conviction.

The second major risk facing markets is the Federal Reserve. Bloomberg’s Jan-Patrick Barnert identifies Kevin Warsh’s first FOMC meeting on June 16–17 as a possible catalyst that could derail the peace-deal rally, particularly if markets run into a renewed interest-rate barrier.

Warsh has publicly criticized the Fed’s communication approach and hinted at the possibility of a broader policy regime shift. However, investors will focus less on the language itself and more on the practical signals coming from the meeting — the overall tone, the Fed’s dot plot projections, its tolerance for persistent inflation, and whether the new chair appears determined to restore policy credibility by tightening financial conditions more aggressively.

The backdrop makes the situation especially delicate. Inflation remains stubbornly elevated, energy markets have been unpredictable, and traders are still debating whether the Fed could ultimately raise rates again before December. At the same time, Warsh must demonstrate independence while operating under the scrutiny of a White House that strongly supported his appointment.

That creates a difficult balancing act. If markets hear a message centered on hawkish credibility rather than dovish reassurance, the optimism generated by the Iran peace agreement could quickly be overshadowed by renewed Fed concerns.

This is now the most important chart for investors to watch. Gold and the US dollar will likely react first, serving as early indicators of whether the Fed is beginning to hint at softer policy or preparing to maintain tighter conditions for longer.

The third major risk is AI policy uncertainty. Bloomberg’s Jan-Patrick Barnert highlights Washington’s actions against Anthropic as a significant escalation in the government’s involvement with the AI sector.

According to the report, the US Commerce Department instructed Anthropic to restrict foreign nationals from accessing its newest AI models, Claude Fable 5 and Mythos 5. In response, Anthropic reportedly suspended access to both platforms entirely. What makes this important is that the issue extends far beyond the usual semiconductor export restrictions. Washington is no longer focusing only on chips and hardware — it is now moving directly into controlling access to AI models themselves.

That shift fundamentally changes how investors must think about the AI trade. Until now, AI valuations were largely driven by expectations surrounding capital expenditure, computing power, semiconductor demand, electricity consumption, and future profit margins. Going forward, AI also becomes a political and regulatory access story.

The key question is no longer just which company has the strongest model, the most compute capacity, or the best revenue outlook. Investors must now also consider who is allowed to use these models, who can legally sell them, and how aggressively Washington may classify frontier AI as a strategic national asset subject to tighter controls.

This makes the AI leadership trade much harder to value. The AI sector is already heavily crowded, deeply embedded in major indexes, and responsible for a large portion of recent market gains. If government directives can suddenly restrict access to advanced models, then the premium investors are willing to pay for these companies becomes more difficult to justify.

That is why comparisons between the late-1990s NASDAQ Composite boom and the recent surge in semiconductor stocks continue to surface. The comparison is not exact, but the underlying concern is similar: investors are questioning how much future dominance and growth have already been priced into today’s valuations. If future success now depends partly on government policy decisions, the outlook becomes considerably less clear.

The fourth issue — and potentially the most important once the initial relief rally fades — is market supply. Bloomberg’s Jan-Patrick Barnert notes that SpaceX priced its IPO at $135 per share and began trading on June 12 with an estimated valuation of roughly $1.77 trillion, making it the largest IPO in history and nearly three times larger than the previous record.

At first glance, the debut looked highly encouraging. Investor demand was strong, the market successfully absorbed the offering, and the stock traded well after listing. But the bigger challenge is not the opening performance — it is whether markets can continue absorbing such enormous amounts of new equity supply in the months ahead.

That concern becomes even more significant with companies like Anthropic and OpenAI still potentially preparing to enter public markets. Together, these offerings could create an unprecedented wave of new shares competing for investor capital.

SpaceX alone reportedly raised more money than the entire combined US IPO market of 2024 and 2025. That makes the listing more than just a successful debut — it becomes a major capital absorption event. Large IPOs of this scale can redirect liquidity away from existing equities, particularly in a market where valuations are already stretched and investor positioning is crowded.

The core issue is simple: even if investor appetite for AI and growth companies remains strong, the market still has finite capital. As more massive listings arrive, existing stocks may face increasing competition for flows, making it harder for the broader rally to maintain momentum.

This is the market setup moving forward. If the current short-covering rally transitions into genuine alpha-driven buying, the broadening-out trade could gain real momentum. Stronger performance from defensive sectors, leadership beyond AI stocks, and fresh capital entering the market would help equities continue grinding higher. In that scenario, relief from the Iran peace agreement could become the first positive catalyst in a broader and more sustainable rally.

However, the risks remain significant. If investor conviction continues to lag, Kevin Warsh adopts a hawkish tone at the Fed, AI leadership increasingly becomes tied to Washington policy decisions, and the IPO pipeline keeps draining liquidity from the secondary market, then markets may face a much more difficult environment.

That is the core concern raised by analysts like Jan-Patrick Barnert, Brian Garrett, and Brent Donnelly Tchir. The Iran peace deal may have removed the extreme geopolitical tail risk, but it did not eliminate the market’s deeper structural vulnerabilities.

The broader message is clear: the war premium has largely disappeared, but elevated market valuations still need to justify themselves through real earnings growth, durable capital inflows, and stronger investor conviction.

Leave a comment