This week will remain driven by developments in the Middle East, although a packed schedule of economic data—including the FOMC March minutes, February personal income, and March CPI—will also draw significant focus.

President Donald Trump said Wednesday night that the United States could wind down its role in the Iran conflict within two to three weeks, offering a potential exit from tensions that have unsettled energy markets since late February. Still, oil prices remain elevated amid ongoing concerns over the Strait of Hormuz, which Trump indicated the U.S. would leave to other nations to reopen.

However, over the weekend, Trump warned that if the strait is not reopened immediately, Monday would mark “Obliteration Day,” with the U.S. prepared to strike Iran’s power infrastructure.

The March 17–18 Federal Reserve minutes (Wednesday) will provide insight into how policymakers viewed the early phase of the conflict. Meanwhile, the March CPI report (Friday) will offer the first indication of how rising gasoline prices are feeding into broader consumer inflation.

Below are the key U.S. economic releases likely to influence investor expectations for growth, inflation, and the path of monetary policy this week:

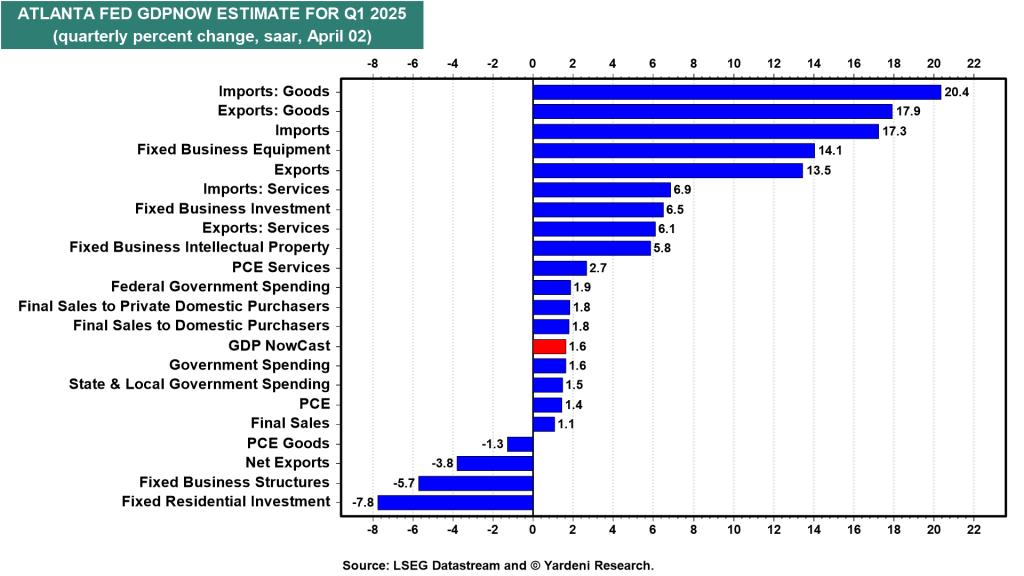

GDP

Thursday’s final Q4 2025 GDP revision is expected at 0.7% (SAAR), a backward-looking figure that is unlikely to sway markets, having been weighed down by the government shutdown. The bigger focus is on Q1 2026, where the Federal Reserve Bank of Atlanta’s GDPNow model has eased to 1.6% (see chart).

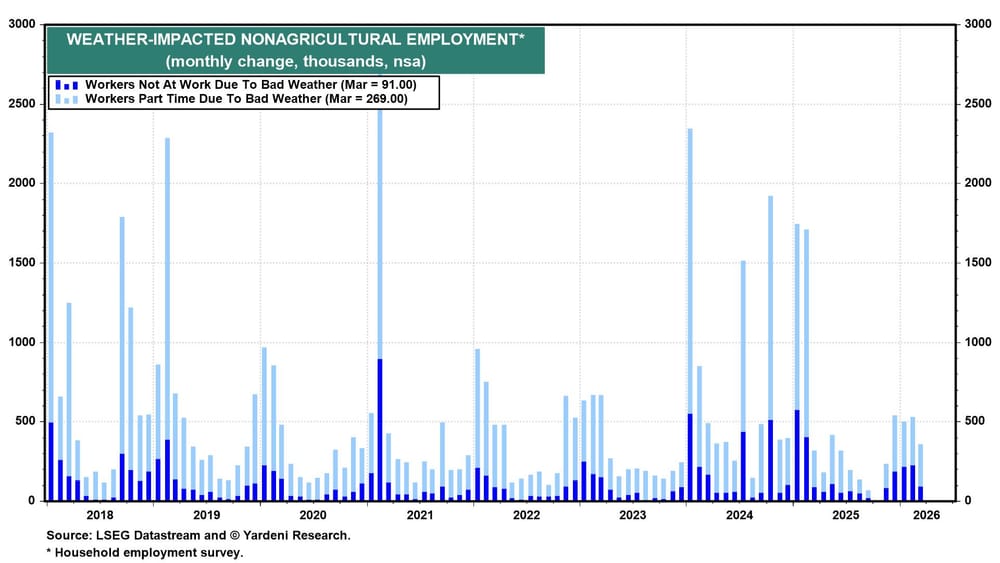

We believe unusually severe winter weather in December, January, and February weighed on recent real GDP growth. Over this period, there was a notable rise in the number of workers who either missed work or shifted to part-time due to harsher-than-normal conditions (see chart).

CPI

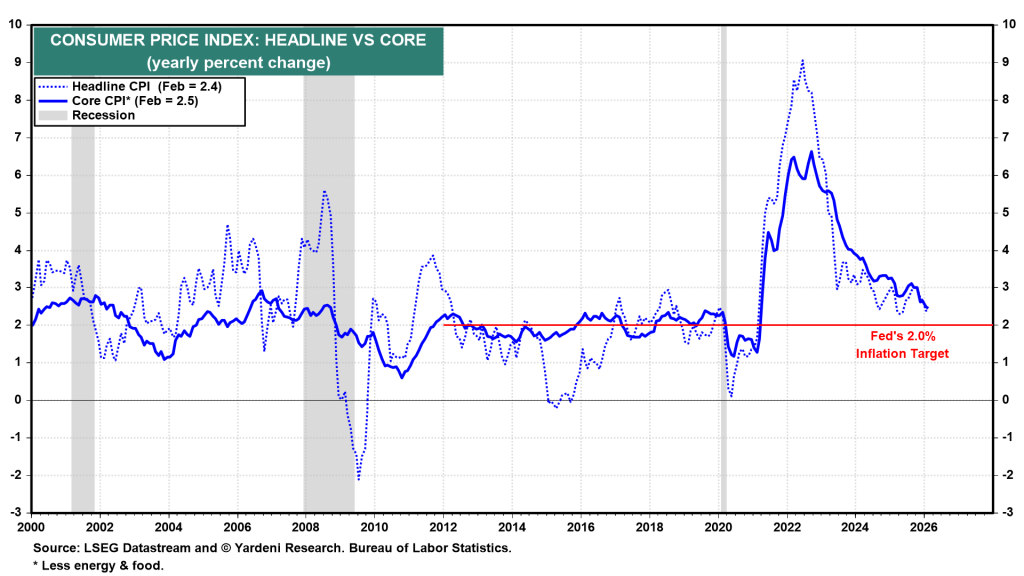

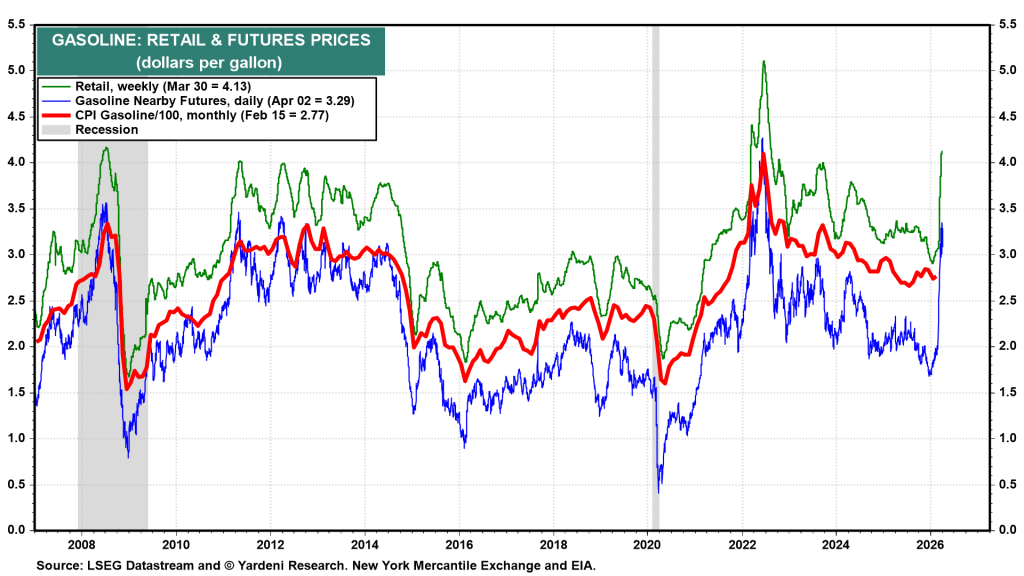

The March CPI report (Friday) is the most important release of the week. The Federal Reserve Bank of Cleveland’s Inflation Nowcasting model suggests headline and core inflation rose 0.84% and 0.20% m/m, respectively, or 3.25% and 2.60% y/y—up from 2.40% and 2.50% in February (see chart).

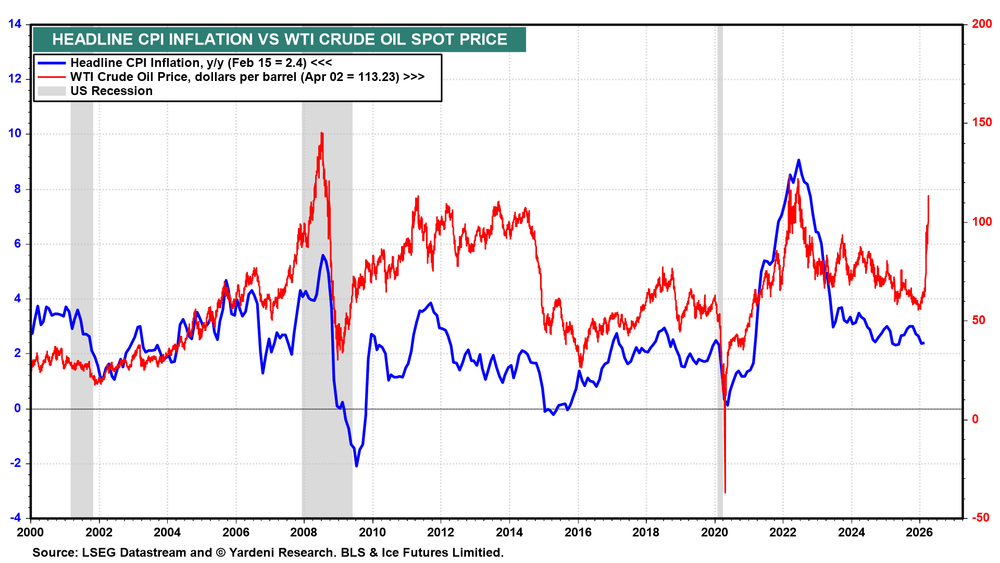

The historical link between oil prices and headline CPI makes the expected March increase largely predictable; every major surge in crude has typically been followed by a rise in headline inflation (see charts). We expect oil prices to peak within the next two months, although this will depend on a swift resolution of tensions in the Middle East.

Unemployment

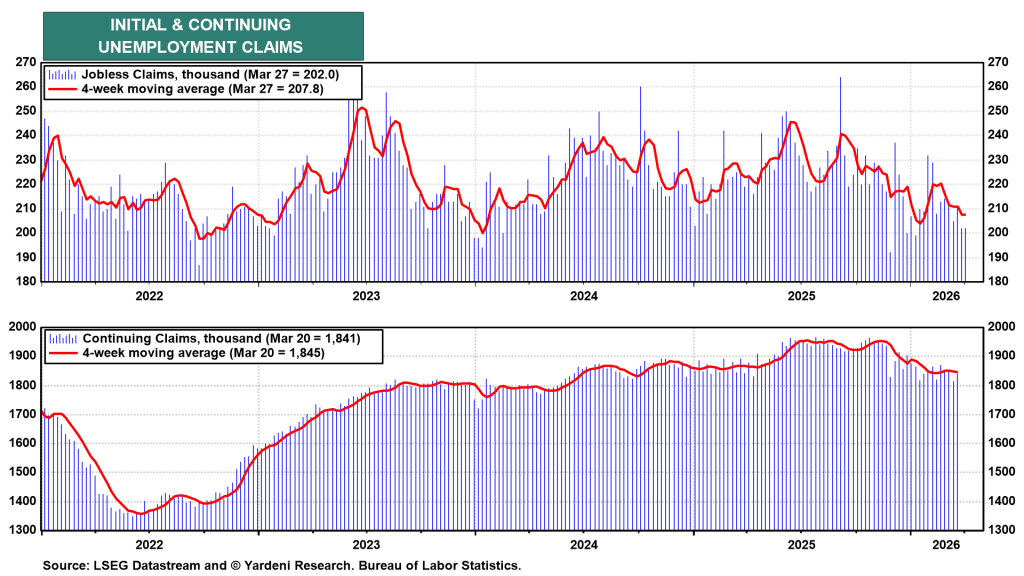

Friday’s payrolls report surprised to the upside, providing reassurance about the near-term strength of the labor market. Initial jobless claims (Thursday) have continued to trend lower, with the four-week moving average at 207,800 (see chart). So far, claims data show no signs that the war is weakening labor market conditions.

Consumer Sentiment

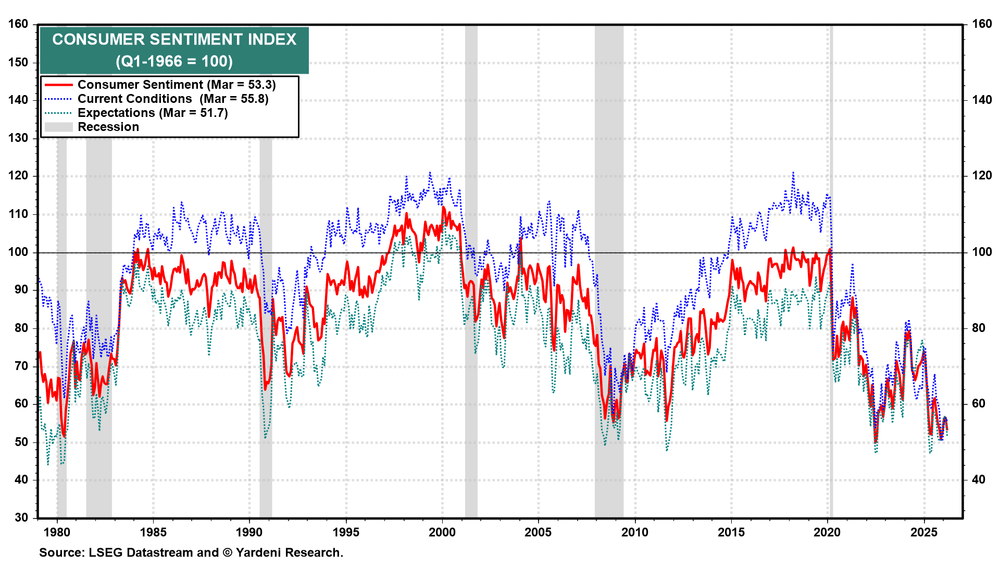

The preliminary University of Michigan Consumer Sentiment survey for April is expected to ease to 52.0 from 53.3 in March, with expectations already subdued at 51.7 (see chart). Meanwhile, The Conference Board consumer confidence surprised to the upside last week at 91.8, suggesting sentiment may be more resilient than consensus expectations imply.

Sources: Ed Yardeni

Leave a comment