Every few months, headlines claim the U.S. dollar’s dominance as the world’s reserve currency is ending. Arguments often cite China selling Treasuries, central banks stockpiling gold, BRICS creating a new monetary system, or the 2022 sanctions that froze $300 billion of Russia’s reserves—suggesting that dollar-denominated assets are no longer “safe” and that the supposedly risk-free asset has become a weapon.

Yet the data tells a different, more important story—one often overlooked by investors chasing simple narratives, exposing the risk of being badly misled.

The Numbers Don’t Support a “Flight from the Dollar”

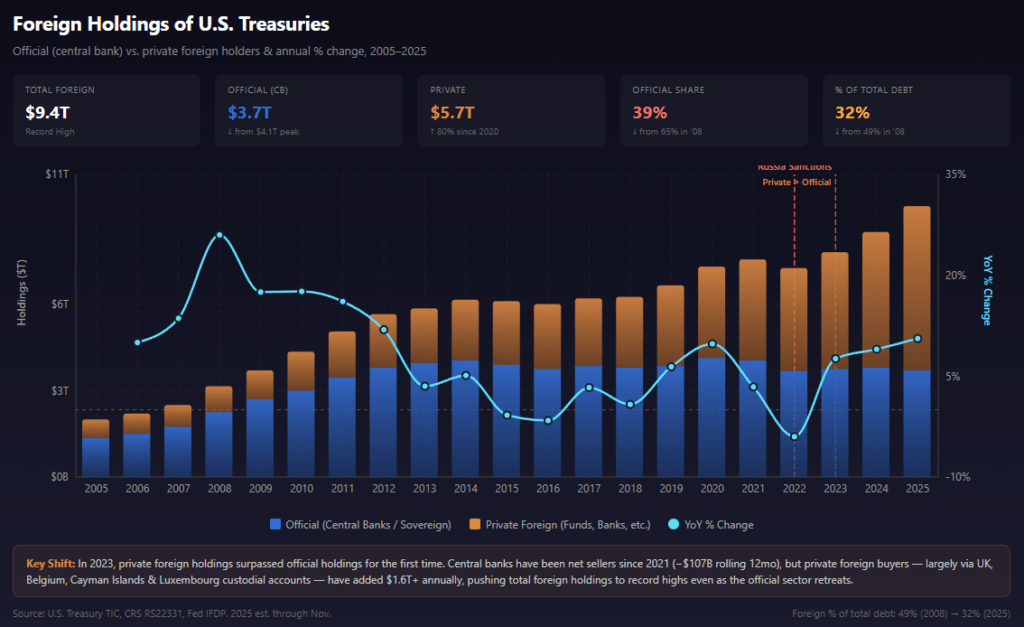

Foreign holdings of U.S. Treasury securities hit a record $9.4 trillion in December 2025, up from $8.7 trillion the previous year—an increase of over $700 billion, or about 8%. Since 2020, foreign holdings have grown from roughly $7.1 trillion, a gain of more than $2.3 trillion. Rather than fleeing, foreign investors are buying U.S. dollar assets at an accelerating pace.

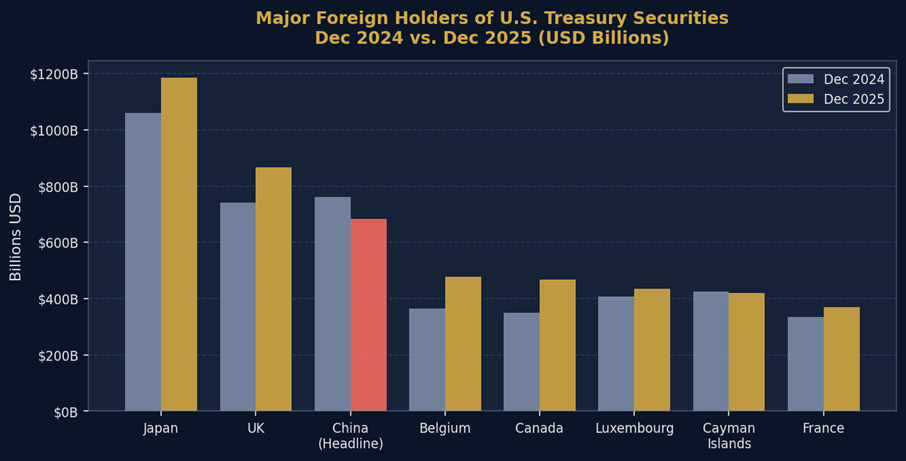

From November 2024 to November 2025, the UK, Belgium, and Japan were the top buyers of U.S. debt, each purchasing over $115 billion. The UK led the pack, boosting its holdings by around $150 billion in just one year. Belgium, which hosts Euroclear—the world’s largest international central securities depository—recorded a 26% increase in its U.S. Treasury holdings, the highest percentage gain among major holders.

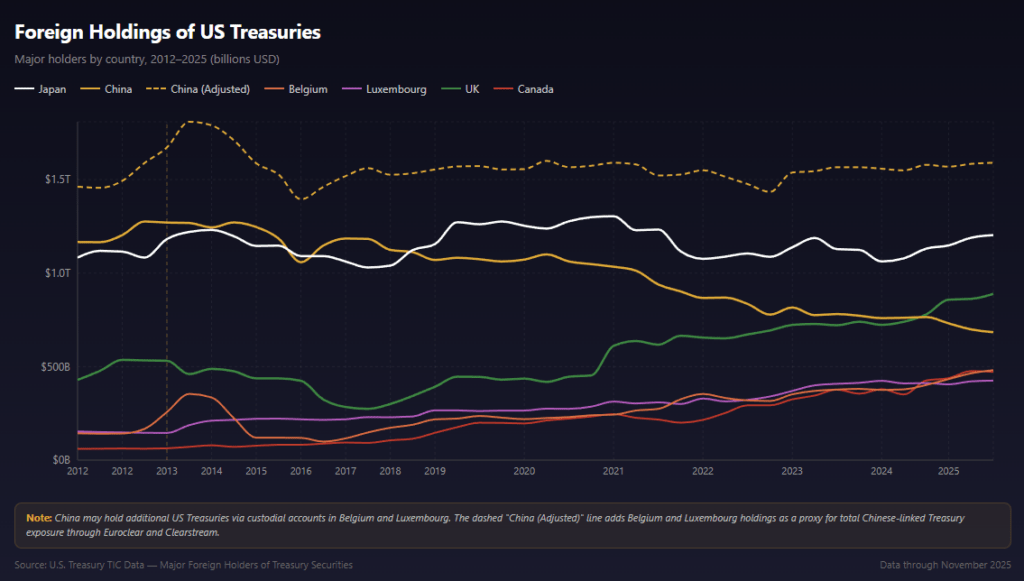

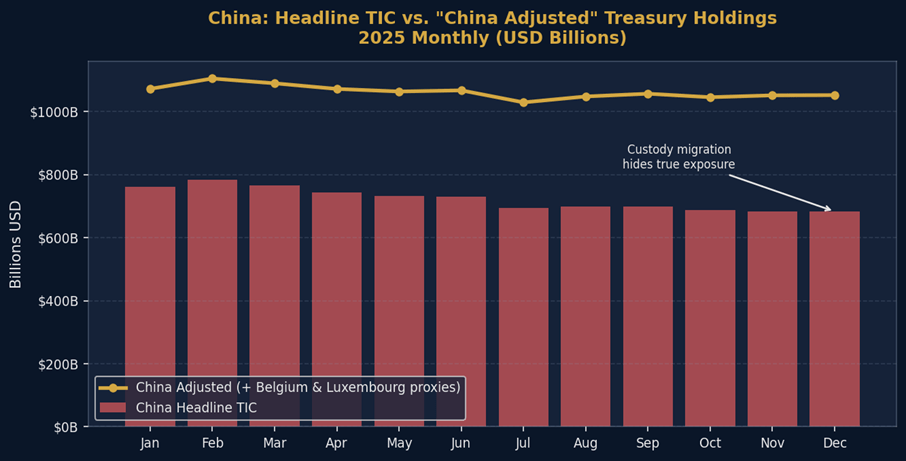

China, on the other hand, trimmed its U.S. Treasury holdings by about $86 billion during the same period. However, the reported TIC figure of $683 billion understates China’s true exposure, since it only counts securities held in U.S. custody. A substantial and increasing portion of China’s Treasury holdings is actually custodied through European intermediaries—mainly the Belgian and Luxembourg accounts that have been expanding so rapidly.

As highlighted previously:

“This isn’t a conspiracy—it’s simply financial plumbing. China relies on Belgium for custodial purposes not only to reduce geopolitical risk but also because Euroclear Bank, located there, sits at the center of cross-border settlement and collateral management. Similarly, Clearstream in Luxembourg serves the same global institutional clients. For central banks or state institutions seeking to hold large Treasury portfolios with flexible settlement and collateral options, these hubs provide crucial operational infrastructure.”

The Real Story: Debt Holders and Custody, Not the Dollar

The critical issue isn’t whether the U.S. dollar is losing its reserve status—it’s about who holds U.S. debt and where it is custodied.

Foreign official (central bank) holdings peaked at around $4.1 trillion in 2020 and have since declined to roughly $3.7–$3.8 trillion. Official institutions have been net sellers since 2021, with rolling twelve-month outflows of approximately $107 billion. This trend reflects risk management decisions by central banks, especially after the 2022 freeze of Russian reserve assets, which highlighted the importance of jurisdiction, legal frameworks, and operational controls in custody arrangements.

Yet private foreign investors—banks, asset managers, hedge funds, sovereign wealth funds, and corporate treasuries—have more than offset the decline in official holdings. In 2023, private foreign holdings surpassed official holdings for the first time and now stand near $5.7 trillion, an 80% increase since 2020. This is not de-dollarization but “de-officialization”: dollars continue to flow, but through different channels.

Custody Migration: Sanctions, Regulation, and Infrastructure

The key shift is in where Treasuries are held, not whether. Post-2022 sanctions accelerated migration of custody from New York-based institutions to European clearinghouses like Euroclear and Clearstream. Euroclear’s assets under custody exceeded €43 trillion in 2025, with turnover rising 20% year-over-year to €1,390 trillion—evidence of a growing, not declining, business.

While sanctions are part of the story, regulatory arbitrage is an even bigger driver. The SEC’s December 2023 mandate requiring central clearing of Treasury cash and repo transactions (compliance by December 2026 and June 2027) represents a massive structural change, potentially bringing $4 trillion in daily transactions under FICC’s central clearing. Combined with Basel III capital charges, Dodd-Frank derivatives margining, and post-trade transparency rules, the incentives to custody and trade Treasuries through European platforms rather than DTCC are substantial, independent of geopolitical concerns.

The 2022 freeze of Russian assets, held at Euroclear (~€185 billion), sent a strong signal that Western-custodied assets can be seized under extreme circumstances. Yet ironically, shifting custody from New York to Brussels doesn’t escape Western sanctions—it simply moves jurisdictional risk from U.S. law to Belgian and EU law, while still leveraging Euroclear’s robust operational infrastructure.

Gold’s Signal Matters—It Complements, Doesn’t Replace, Other Indicators

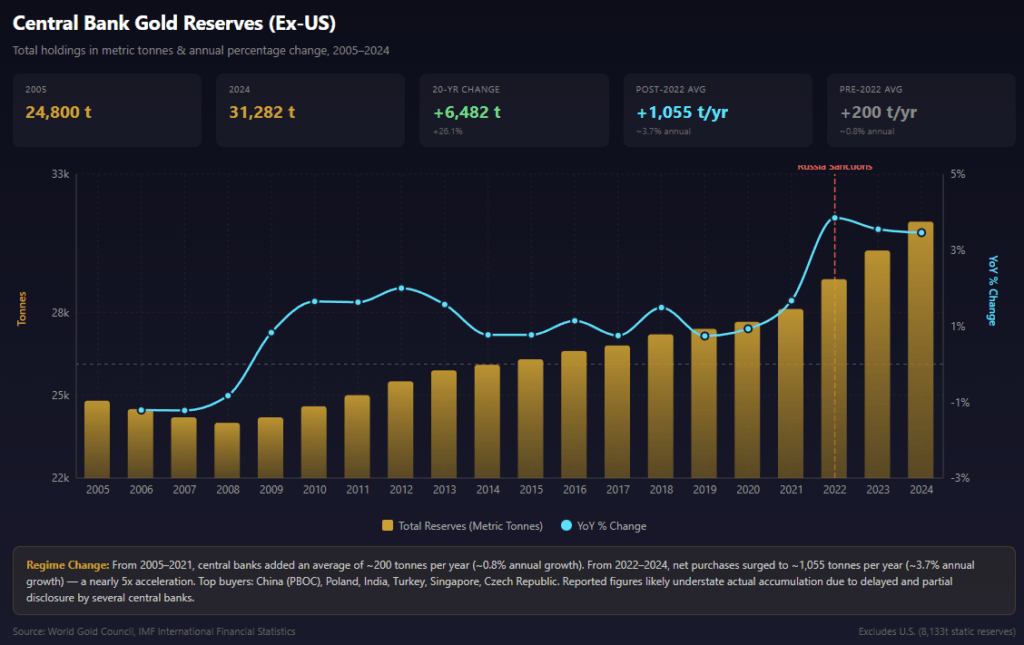

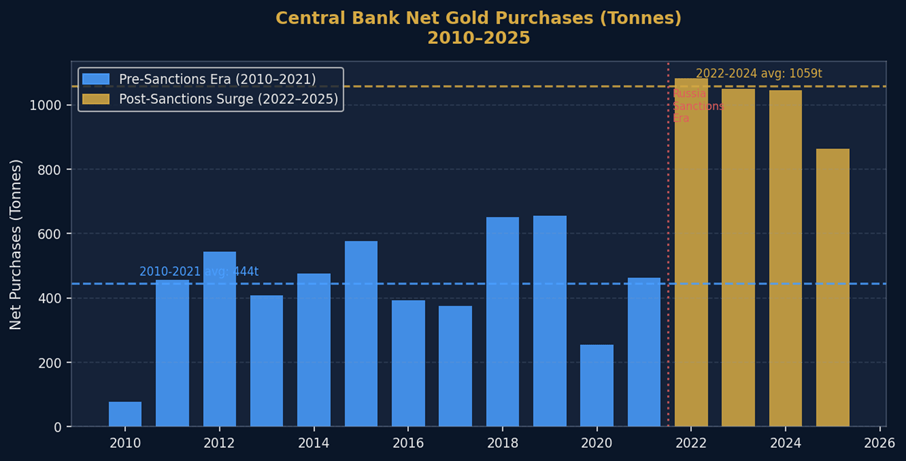

Central bank gold buying has been remarkable. Looking at tonnage—which removes price effects and shows actual physical accumulation—the trend is clear. Excluding the U.S., central bank gold reserves rose from about 24,800 tonnes in 2005 to 31,282 tonnes in 2024, a 26% increase (or roughly 1.3% annually) over two decades. However, this growth was uneven: from 2005 to 2021, central banks added only around 200 tonnes per year on average, a modest 0.8% annual increase.

Between 2022 and 2024, net gold purchases jumped to roughly 1,055 tonnes per year, representing a 3.7% annual growth rate. Remarkably, over half of the total twenty-year accumulation happened during just these three years. That said, purchase activity has since begun to slow.

Advocates of de-dollarization often cite this chart as “proof” of the dollar’s decline. Yet the data contains a fundamental paradox that few commentators address.

Gold is bought, sold, and settled using U.S. dollars.

The LBMA, the center of wholesale physical gold trading, publishes its benchmark price twice daily in U.S. dollars per troy ounce. Similarly, COMEX futures, which drive price discovery, are quoted and settled in U.S. dollars. When central banks like the PBoC, Reserve Bank of India, or National Bank of Poland buy gold, the transactions are denominated in dollars, cleared through dollar-based infrastructure, and the asset’s value is marked in dollars. Even the Shanghai Gold Exchange, which quotes prices in renminbi, effectively tracks the dollar-denominated LBMA benchmark adjusted for the USD/CNY rate.

This creates a fundamental paradox for the de-dollarization narrative. When a central bank sells $10 billion in U.S. Treasuries to buy $10 billion in gold, it has not meaningfully reduced dollar exposure. It has merely swapped one dollar-denominated asset (Treasuries, with counterparty risk, yield, and maturity) for another (gold, with no counterparty risk, yield, or maturity). While the gold itself is physically non-dollar, its acquisition, valuation, and future liquidation all involve dollars.

Central banks are not de-dollarizing—they are de-risking within the dollar system, moving from assets that could be frozen or sanctioned to assets that cannot. This distinction is crucial: gold accumulation does not weaken the dollar’s role as the global unit of account. Every tonne of gold purchased flows through dollar-denominated clearing infrastructure.

The proper framing is “gold vs. Treasuries”, not “gold vs. the dollar.” Gold is a rotation within the dollar ecosystem, shifting from an asset with counterparty risk to one without.

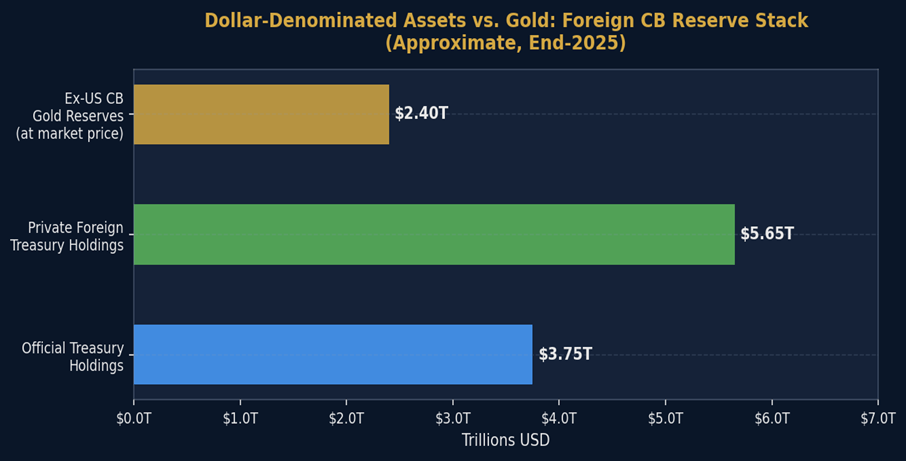

Even with this accumulation, gold remains a fraction of total holdings. Excluding the U.S., central bank gold is worth about $2.4 trillion, below the $3.7–$3.8 trillion in official Treasury holdings and far smaller than the $9.4 trillion in total foreign Treasury holdings. No central bank is abandoning Treasuries wholesale. For example, the PBoC still holds at least $684 billion in reported Treasuries (likely much more via intermediaries) versus roughly $200 billion in gold. Even the most aggressive gold-buying central banks are pursuing marginal diversification, not substitution.

In reality, central banks are accumulating gold incrementally as a hedge against potential dollar weaponization. However, none are selling off their Treasury holdings en masse to fund these purchases. Gold and Treasuries function as complementary assets within a diversification strategy, not as substitutes in a supposed currency battle.

The Real Story: A Five-Layer Shift in Global Dollar Dynamics

- Custody Migration, Not Asset Flight – U.S. Treasuries are relocating from New York-based custody to European clearinghouses. This shift is primarily a hedge against regulatory and sanctions risks. Importantly, these assets remain U.S. dollar-denominated obligations, leaving the dollar’s role as the global unit of account intact.

- Official-to-Private Rotation – Central banks are trimming their holdings, while private foreign investors—hedge funds, asset managers, and banks—are increasingly buying U.S. debt. The marginal buyer of Treasuries is no longer the PBoC or Bank of Japan, but private investors seeking yield and collateral.

- Share Erosion Despite Nominal Growth – Foreign ownership as a percentage of total U.S. debt has dropped from roughly 49% in 2008 to 32% in 2024. Yet in absolute terms, holdings have reached record levels. Because the U.S. continues to issue debt faster than foreign investors can buy it, domestic entities—like the Fed, banks, and money market funds—must absorb the difference.

- Gold as Insurance, Not Replacement – Central banks are accumulating gold at the fastest rate in decades as a hedge against geopolitical risks, including sanctions. This is prudent portfolio diversification, not a strategic move against the dollar.

- Regulatory Fragmentation – U.S. market structure changes—mandatory clearing, capital charges, and transparency rules—are encouraging Treasury trading and custody offshore. This is largely a self-inflicted structural shift, potentially posing a bigger long-term risk to U.S. financial primacy than Chinese gold purchases.

The Bottom Line

The narrative of de-dollarization is largely factually incorrect, yet it reflects a genuine shift in sentiment. The dollar is not collapsing—foreign demand for U.S. Treasuries remains at record levels. What is changing is the infrastructure through which the world accesses dollar assets. This shift isn’t driven by adversaries trying to dismantle the system, but by participants aiming to shield themselves from political and regulatory risks.

The world isn’t abandoning the dollar—it is hedging against those who control it. This distinction is crucial for investors in positioning portfolios and for policymakers considering the long-term impact of using the dollar as a geopolitical tool.

Sources: Lance Roberts

Leave a comment