The coming week is set to be tense as developments in the Middle East continue to unfold. In the nine days since the United States and Israel launched strikes on Iran, the conflict has spread across several neighboring countries.

Tehran’s actions to effectively close the Strait of Hormuz have triggered sharp jumps in oil and gas prices, forcing economic forecasters to rethink their outlook. Brent crude climbed above $100 a barrel on Monday evening. Against this backdrop, upcoming reports from OPEC and the International Energy Agency (IEA) on disruptions to Persian Gulf energy shipments could strongly influence markets. The outlook has already tightened after the United Arab Emirates and Kuwait cut oil production due to a lack of storage capacity.

Attention is now focused on whether the conflict escalates further and how it might affect inflation expectations. Investors have already started trimming forecasts for interest-rate cuts this year, including expectations surrounding the Federal Reserve’s March 17–18 policy meeting. Several Federal Open Market Committee members remain concerned about the slow progress toward bringing inflation back to the Fed’s 2% target.

In fact, minutes from the January meeting showed that several policymakers even saw the possibility that rate hikes might still be necessary.

As a result, this week’s economic releases could carry greater significance than usual for already jittery bond markets. February consumer price data due Wednesday and January PCE inflation figures on Friday will be closely watched. The PCE index — the Fed’s preferred measure of inflation — could be particularly influential, as it has remained stubbornly near 3%.

Beyond the United States, markets will also receive updates on inflation trends in China, India, Brazil, and Mexico. Meanwhile, economic indicators from the Eurozone (industrial production), Japan (GDP), Canada (trade and employment), and the United Kingdom (monthly GDP) will offer insight into how President Donald Trump’s tariffs are affecting the global economy.

The following U.S. data releases are the ones most likely to move financial markets this week, though events in the Middle East may dominate attention.

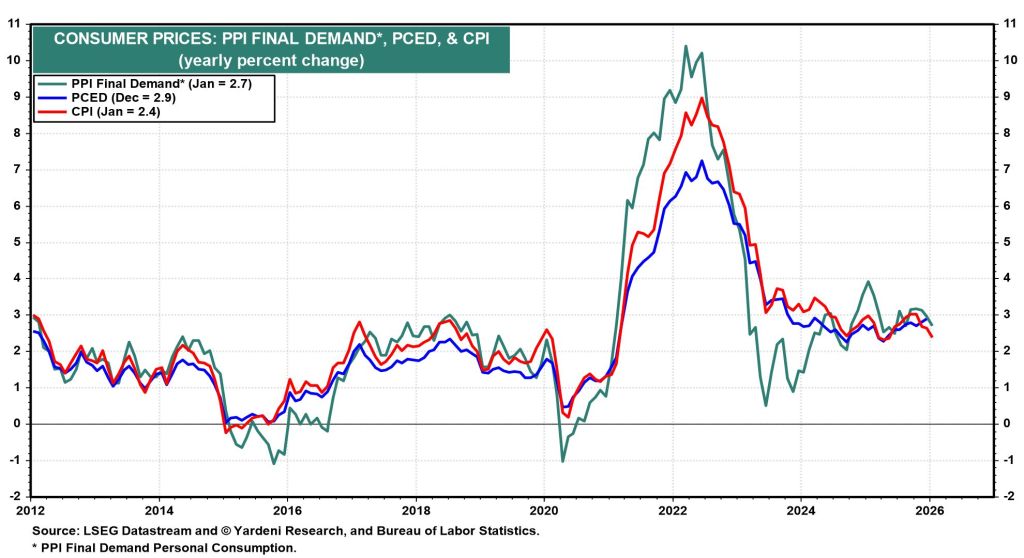

PCE Inflation

After registering 2.9% year-over-year in December, the Cleveland Fed’s Inflation Nowcasting model suggests that headline PCE inflation may cool slightly to 2.8% in January (see chart). Such a reading could offer some reassurance to the more dovish policymakers at the Federal Reserve. However, with inflation trends shifting quickly, many officials may choose to look beyond any short-term improvement.

CPI

After easing to 2.4% year over year in January, with core inflation at 2.5%, consumer prices are widely expected to remain broadly stable in February. The Federal Reserve Bank of Cleveland’s nowcasting model points to roughly a 0.2% month-over-month rise in both headline and core CPI. Still, such stability could prove temporary if stronger inflation pressures emerge in the months ahead.

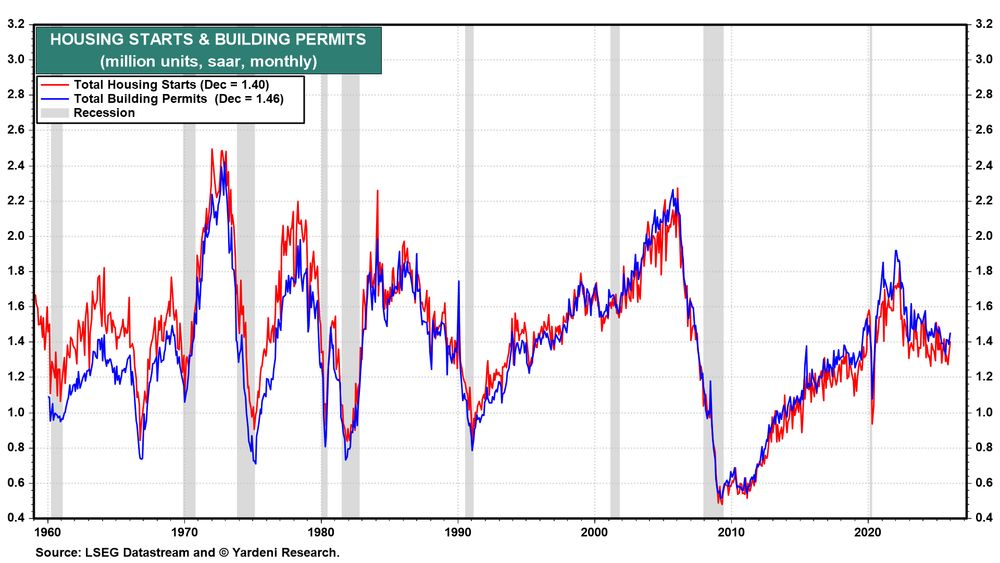

Housing Data

A series of housing indicators scheduled for release this week could provide valuable clues about U.S. consumer confidence as bond yields and the broader economic outlook continue to fluctuate. Markets will be watching February existing home sales and housing affordability data on Tuesday, followed by January housing starts on Thursday, for signs of how the housing sector is coping with shifting financial conditions.

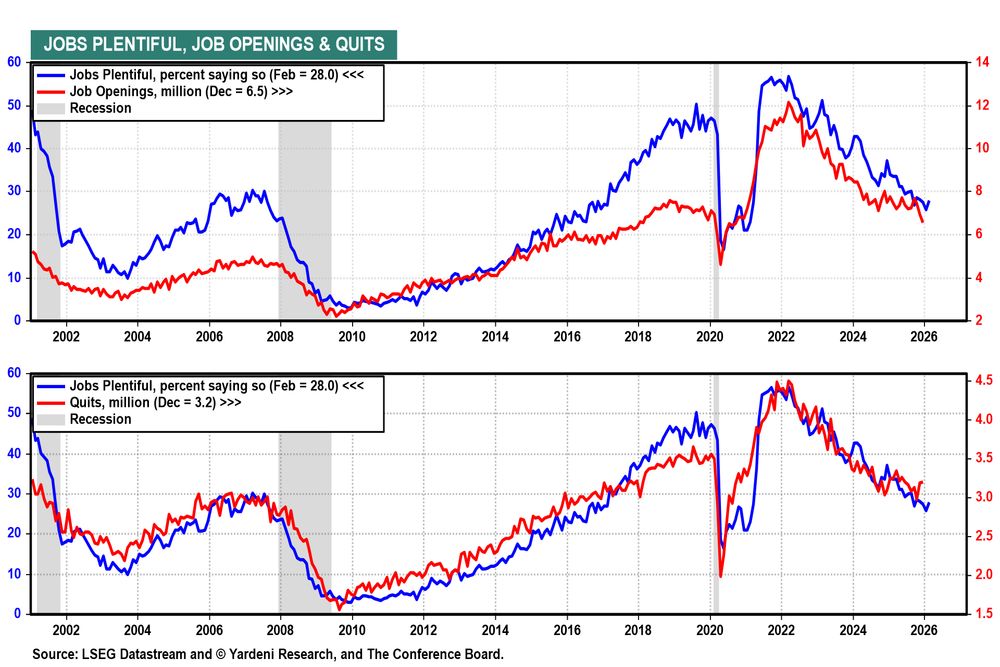

JOLTS and Jobless Claims

Recent data showing that U.S. job openings fell to their lowest level in more than five years in December aligns with other indications that the labor market may be gradually cooling. Investors will be watching the January JOLTS report on Friday for signs of any additional softening.

At the same time, weekly initial jobless claims, due Thursday, will provide another gauge of labor market conditions. Claims totaled 213,000 in the previous week, a level that still suggests a relatively stable job market with limited layoffs.

Sources: Ed Yardeni

Leave a comment