The idea that “fiat is dying” has become a popular slogan among supporters of digital assets, gold enthusiasts, and cryptocurrency advocates. At the center of this argument is the belief that central banks have created enormous amounts of money, leading to currency debasement and ultimately making the U.S. dollar obsolete. We have addressed this debasement narrative before.

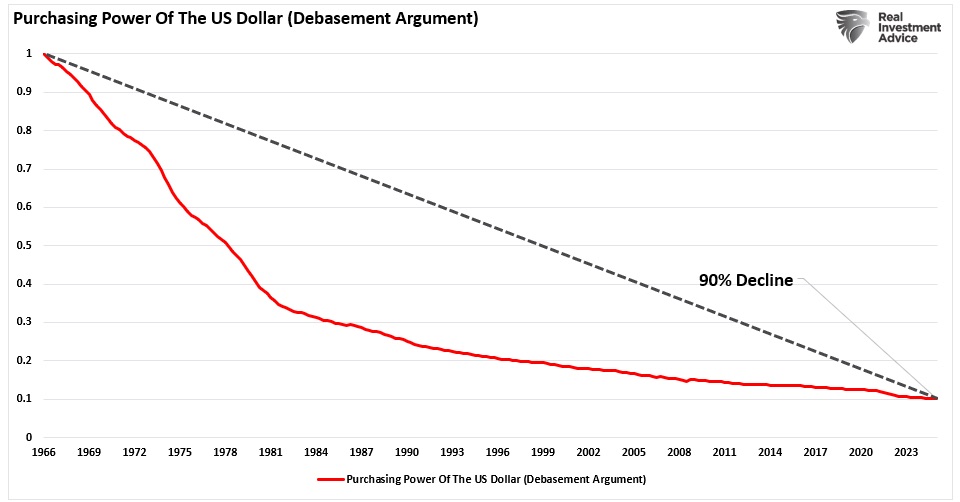

It’s an appealing storyline: inflation is spiraling, governments keep printing money, and the dollar is supposedly nearing its end. While there are legitimate risks to monitor, many headlines emphasize fear more than facts. The message can be powerful, especially when promoters of gold, silver, or other “doomsday” assets use it to push people into acting quickly. A commonly cited piece of evidence in this debasement argument is the familiar chart claiming the U.S. dollar has lost about 90% of its purchasing power since 1966.

But here’s the key point: that chart doesn’t actually demonstrate currency debasement. It simply reflects inflation—an expected and well-understood feature of a growing economy. Prices tend to rise over time as demand increases, driven by population growth, higher incomes, and expanding consumption. This dynamic is particularly evident in a modern, service-based economy that encourages credit expansion and capital investment. In that sense, it’s not so much that the dollar is losing value, but rather that the economy itself is growing.

Those who promote the “debasement” argument often overlook how modern inflation and economic systems function. What the chart really illustrates is the declining purchasing power of idle cash. Money that remains uninvested naturally loses value over time relative to inflation. That doesn’t signal the collapse of fiat currency—it simply highlights the importance of putting capital to work.

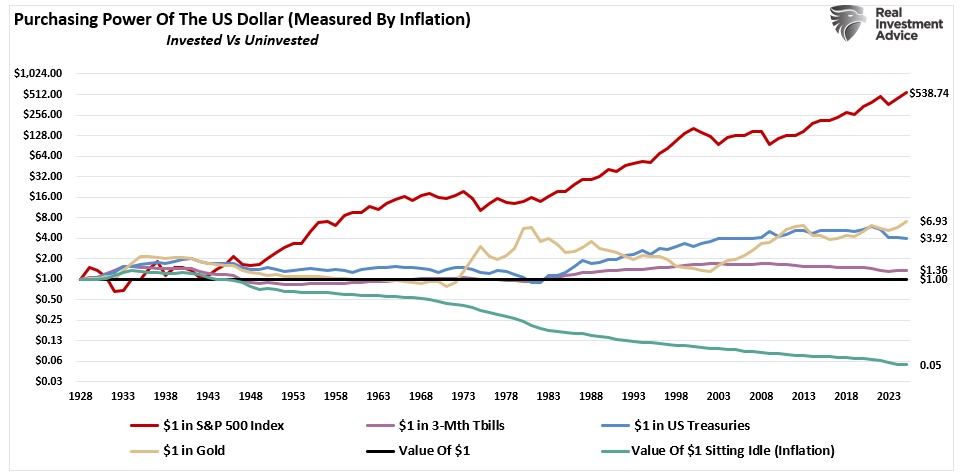

While gold advocates frequently argue that gold protects against debasement (in other words, inflation)—which can be true—other assets can serve the same purpose. Short-term U.S. Treasury bills and longer-term Treasury bonds have also preserved value on a real, inflation-adjusted total-return basis. Still, historically, a single dollar invested in the S&P 500 has been the most effective way to maintain—and significantly grow—the purchasing power of the U.S. dollar.

Most importantly, the term “debasement” does not mean a currency is collapsing. Rather, it reflects the impact of inflation on money that remains uninvested. Inflation gradually reduces purchasing power when income and investment returns fail to keep up. For example, a $100 bill today buys less than it did in 2010 because the overall price level of goods and services tends to rise as the economy expands. While this effect is real, it is a normal outcome of economic growth and monetary policy working together—not evidence of a fundamental loss of confidence in the currency.

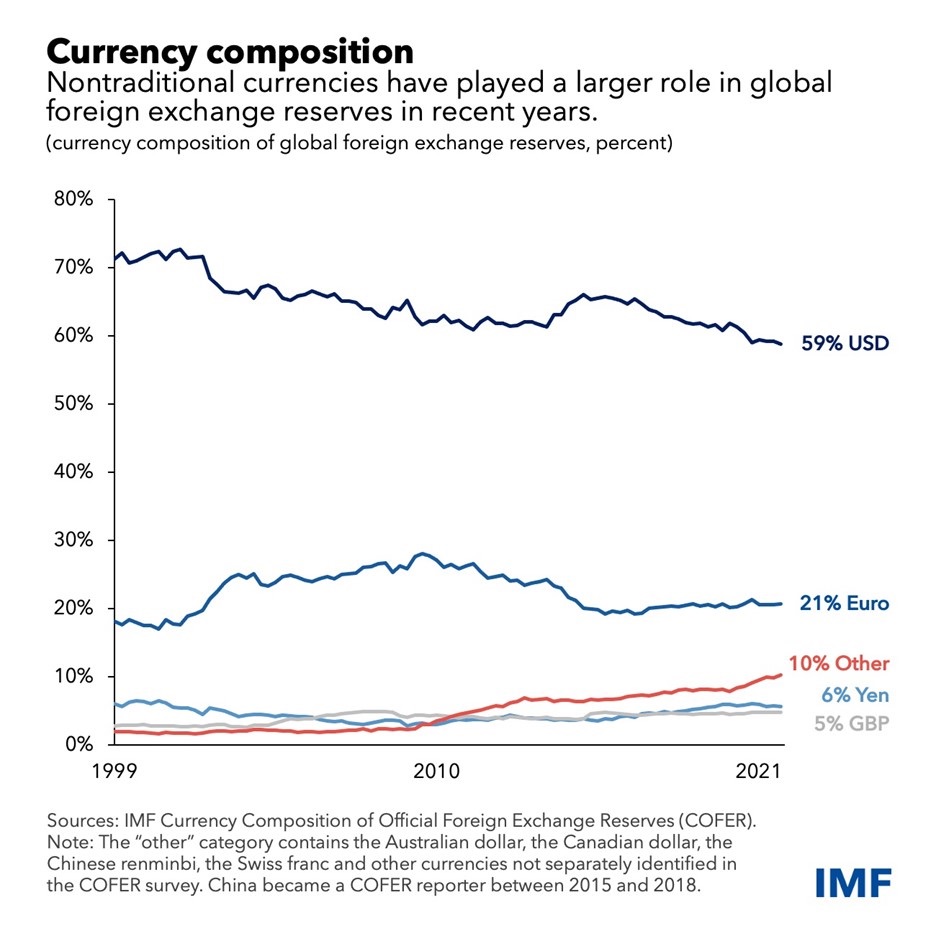

In reality, the U.S. dollar continues to hold a dominant position in the global financial system. As discussed in “The Dollar’s Death Is Greatly Exaggerated,” several key facts highlight this strength:

- Around 80% of global transactions are still conducted using the U.S. dollar as the primary unit of account or settlement currency.

- The dollar represents nearly 60% of the world’s foreign-exchange reserves held by central banks.

- No other currency or asset currently offers the same depth, liquidity, and institutional credibility as the U.S. dollar.

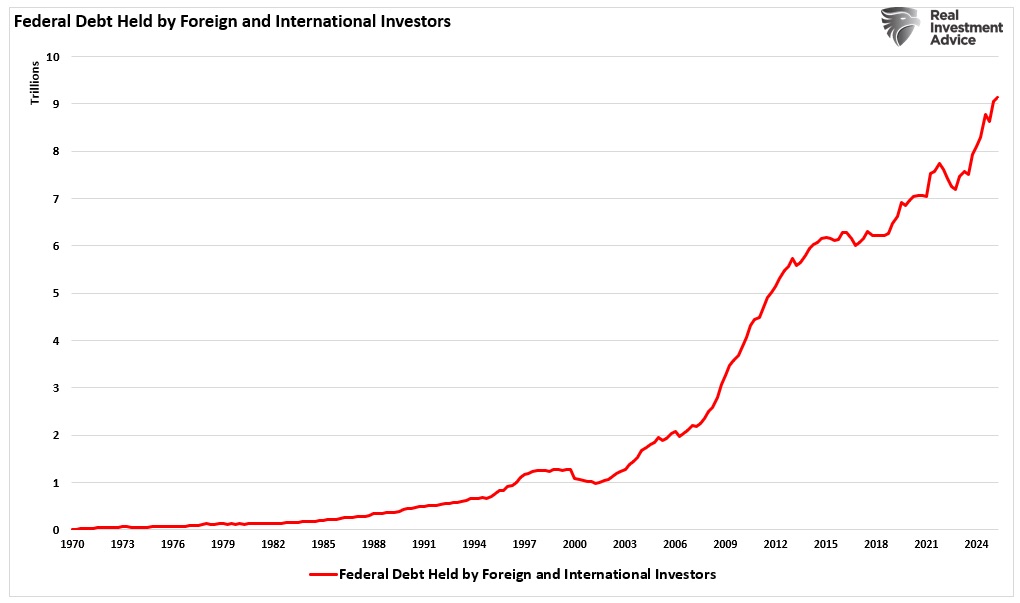

These facts challenge the claim that the world is turning away from fiat currencies or the U.S. dollar. The idea that the dollar is in decline overlooks strong evidence of its ongoing global demand and widespread use—reflected in the record surge of foreign purchases of U.S. Treasuries.

The Illusion of Escape

Those who claim that investors are turning to gold or Bitcoin based on the “currency debasement” narrative either deliberately mislead others or lack a proper understanding of how the modern monetary system works—particularly how pricing, exchange, and settlement function within today’s economy.

We fully agree that investors should put their “idle” dollars to work in assets such as bonds, gold, stocks, or Bitcoin to help preserve purchasing power over time. However, when these assets rise in nominal terms, the gains mostly reflect shifts in relative valuations rather than a true rejection of the dollar. Many investors, influenced more by headlines than by underlying facts, buy gold or Bitcoin as perceived “safe havens,” believing they are moving away from fiat currency due to fears of debasement.

In reality, that isn’t the case. These assets are still priced and settled in dollars. Bitcoin commonly trades in USD pairs, and the global price of gold is quoted in dollars. When investors want to spend or use those holdings outside the digital-asset ecosystem, they typically convert them back into the dollar-based system. The notion of fully escaping fiat currency is largely philosophical; in practice, value transfer and financial utility still revolve around the dollar. Historically, the most effective way to protect purchasing power from debasement has been participation in the U.S. stock market.

Although the debasement narrative often portrays U.S. Treasuries as outdated remnants of a failing system, the reality is quite the opposite. U.S. Treasuries remain the most liquid and trusted financial instruments in the world, forming the backbone of global interest-rate benchmarks, risk-free rate calculations, collateral markets, and international reserves.

Moreover, a new development in the modern financial system may strengthen the dollar’s influence even further: the rapid growth of USD-denominated stablecoins.

USD Stablecoins and Why They Matter

As discussed, the U.S. dollar remains—and is likely to remain—the backbone of the global financial system. This dominance is unlikely to change in either the near or distant future, largely because no credible alternative currently exists. If anything, the rapid rise of USD-denominated stablecoins may reinforce that position even further.

Today, nearly 99% of fiat-backed stablecoins are pegged to the U.S. dollar. This mirrors the dollar’s dominance in global foreign-exchange reserves, where its share still exceeds that of all other major currencies combined. Despite periodic concerns about inflation or monetary debasement, global confidence in the dollar remains strong. In fact, the growth of USD stablecoins reflects the dollar’s strength rather than signaling its decline.

But what exactly are USD stablecoins? They are digital tokens designed to maintain a 1:1 value with the U.S. dollar. Unlike volatile cryptocurrencies such as Bitcoin or Ethereum, whose prices can fluctuate dramatically, stablecoins aim to provide price stability by backing their tokens with reserves of highly liquid assets.

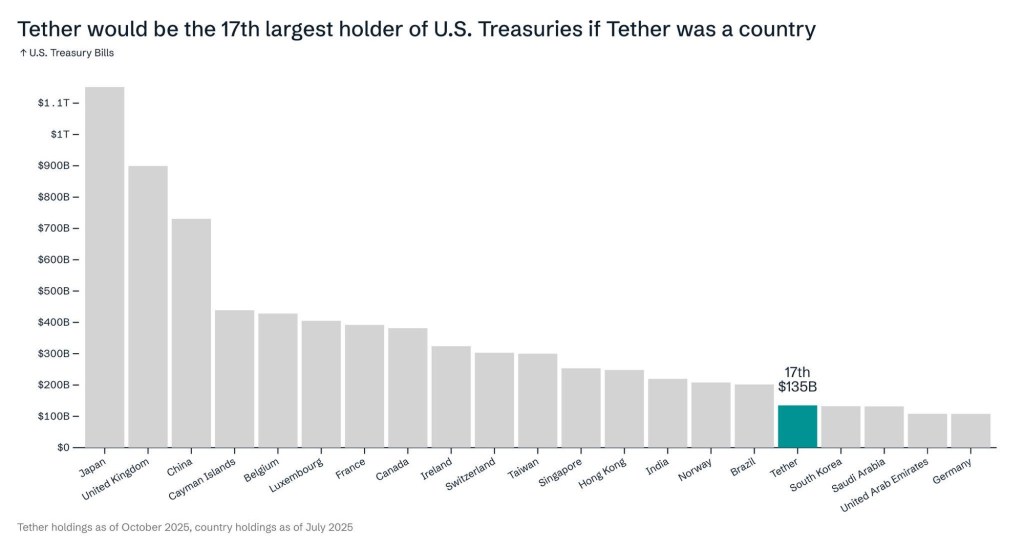

Two of the largest examples are Tether (USDT) and USD Coin (USDC), which together account for more than 90% of the USD-stablecoin market. By late 2025, the company behind USDT—Tether Holdings—held over $135 billion in U.S. Treasury securities. That level of holdings would rank it roughly 17th among global holders of U.S. sovereign debt, exceeding the Treasury holdings of several countries, including South Korea, Saudi Arabia, Germany, and the United Arab Emirates.

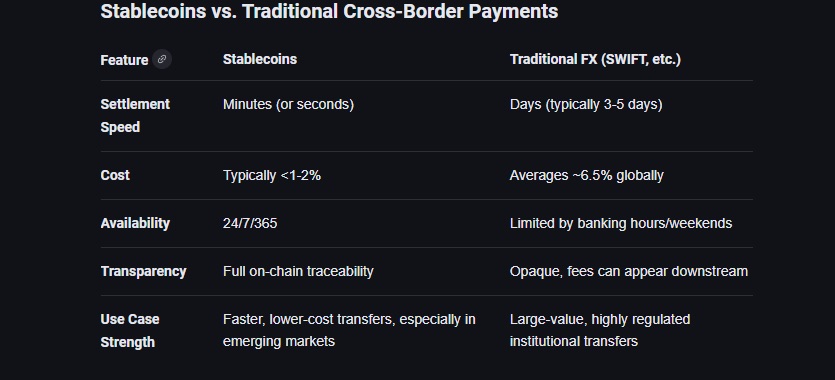

This development is particularly important when examining claims about the “death of the dollar.” USD stablecoins function on blockchain networks, allowing digital dollars to be transferred and settled globally in real time without relying on traditional banking intermediaries. This feature makes them especially useful for cross-border payments, remittances, and financial activity in regions where banking infrastructure is limited or less developed.

The International Monetary Fund has noted that while most stablecoin transactions today are still linked to cryptocurrency trading, cross-border usage is expanding quickly, indicating that these digital dollars could play a larger role in the global financial system in the future. As highlighted by Chainstack, …

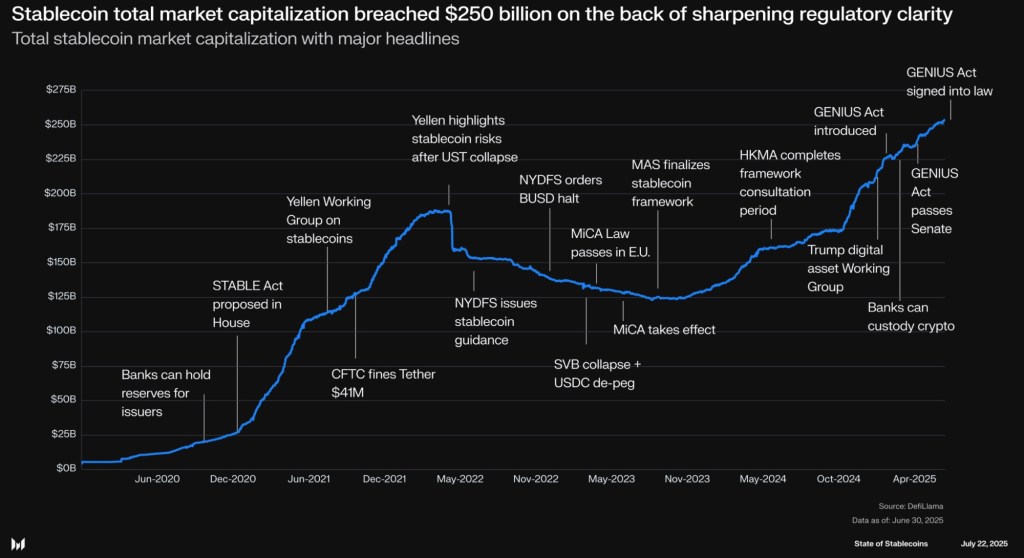

“Stablecoins have entered mainstream finance, creating a bridge between traditional banking systems and digital asset networks. Dollar-pegged tokens already process transaction volumes comparable to major payment networks, with activity rivaling systems such as ACH, Visa, and PayPal. By mid-2025, the total supply of stablecoins had surpassed $250 billion, highlighting growing demand for faster, always-available payment solutions.”

Although stablecoin transaction activity still represents a very small share—roughly 1% of the global cross-border payments market, which totals around $2 quadrillion annually—there are several factors that lead many analysts to expect significant expansion in the USD stablecoin sector in the years ahead.

These applications align with the ongoing modernization of global payment systems. If USD stablecoins achieve wider adoption, they could evolve into a key layer of infrastructure for digital money movement, which would, in turn, increase the importance of U.S. Treasuries within the global financial system.

How USD Stablecoins Could Increase the Importance of U.S. Treasuries

USD stablecoin reserves often include these assets, highlighting that digital dollar infrastructure is closely linked to U.S. sovereign debt markets rather than operating independently from them. As the stablecoin market continues to expand, its connection to U.S. Treasuries may grow even stronger. Issuers must hold liquid, low-risk assets to preserve their dollar pegs and satisfy both regulatory standards and market expectations. Short-term U.S. Treasuries are a natural fit because they are highly liquid and widely accepted as collateral.

Regulatory developments further reinforce this relationship. For example, the GENIUS Act, passed in 2025, requires stablecoin issuers to back their tokens with high-quality liquid assets such as U.S. dollars or short-term Treasury securities. This requirement increases the likelihood that stablecoin reserves remain closely tied to U.S. government debt. Additionally, if the STABLE Act is enacted, it would impose further rules obligating issuers to maintain safe and highly liquid assets as backing for their tokens.

Industry forecasts suggest that the USD stablecoin market could expand to $2–$3 trillion by 2030, supported by clearer regulatory frameworks and broader financial adoption. If this scenario materializes, stablecoin issuers could become a meaningful source of demand for U.S. Treasuries. Their reserves would likely position them as incremental buyers in money markets, potentially reinforcing traditional sources of Treasury demand. According to Reuters, as much as 80% of current stablecoin reserves are already held in Treasury bills and repurchase agreements, indicating that reserve management is already heavily oriented toward Treasuries.

Academic research also indicates that stablecoin demand may already be influencing short-term interest rates. One study found that stablecoin purchases of Treasury bills were associated with noticeable downward pressure on one-month yields, suggesting that reserve demand tied to digital dollars can have tangible effects on real financial markets.

That said, any discussion of USD stablecoins must also acknowledge the risks involved. Much of this outlook assumes that stablecoins will evolve into a widely used global transaction tool. While possible, that outcome is far from guaranteed. At present, most stablecoin activity remains concentrated in cryptocurrency trading and settlement, rather than everyday commerce or sovereign-level payments. Future adoption will largely depend on regulatory clarity, institutional participation, and sustained global confidence.

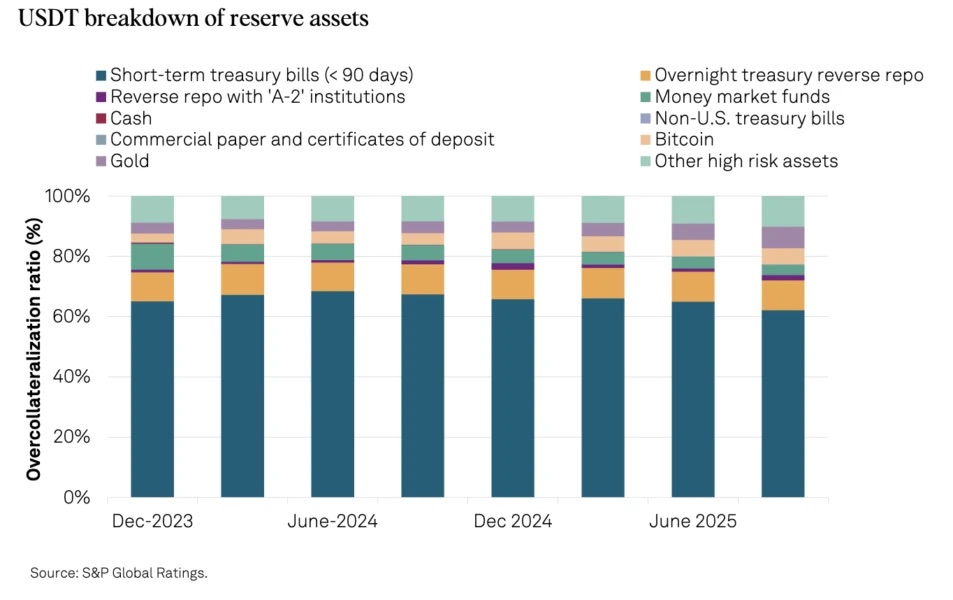

Custodial and transparency risks also remain important considerations. S&P Global Ratings recently downgraded the stability assessment of Tether, citing that only 64% of its reserves were held in short-term U.S. Treasuries and highlighting ongoing concerns around transparency. This emphasizes the need for stronger reporting standards, improved governance, and more regulated custody arrangements if stablecoins are to scale safely.

As S&P Global Ratings noted:

“Bitcoin represents 5.6% of USDT in circulation, exceeding the 3.9% overcollateralization marginassociated with a collateralization ratio of 103.9%. A decline in the price of bitcoin or other higher-risk assets could therefore reduce collateral coverage.”

Another potential challenge comes from the rise of central bank digital currencies, or Central Bank Digital Currency. Governments may prefer to develop their own digital payment infrastructure, which could limit the role of privately issued USD stablecoins in some applications. Even so, if CBDCs gain widespread adoption, they would likely still rely on reserves backed by U.S. Treasuries, given their liquidity, safety, and central role in the global financial system.

Another consideration is that stronger demand for Treasuries could push yields lower. In response, stablecoin issuers might adjust how they structure their reserves. However, the key point is that these reserves would still consist of dollar-linked instruments. Whether issuers hold Treasury bills, repurchase agreements, or other short-term dollar assets, the peg remains tied to the U.S. dollar. As a result, the system continues to function within the existing dollar-based monetary framework rather than creating an entirely separate financial ecosystem.

Finally, it is important to recognize the possibility that these developments may not occur at the projected scale. Regulatory obstacles, technological limitations, or changes in macroeconomic conditions could slow or even halt the growth of stablecoins. While the future is uncertain, the evolving structure of USD stablecoins and the broader pace of financial technology innovation suggest that global payment systems are likely to change in the coming years—and that the United States Dollar will remain central to that transformation.

Conclusion and Investment Thesis

The claim that “fiat money is dying” is not supported by current data or economic reality. While inflation does erode purchasing power, it should not be confused with the type of currency debasement seen historically. Instead, it reflects the gradual loss of value in idle cash within a growing and expanding economy.

The United States Dollar continues to serve as the backbone of the global financial system. It dominates international trade, central-bank reserves, and cross-border settlements. At present, no alternative currency, asset, or financial structure offers the same level of liquidity, institutional credibility, or market depth as the dollar.

The belief that investors can fully escape fiat currencies by moving into assets like Gold or Bitcoin reflects a misunderstanding of how the modern monetary system operates. While these assets can serve as hedges against inflation, they still function within the broader fiat framework. Their pricing, settlement, and liquidity are deeply tied to the United States Dollar, meaning the idea of completely “escaping” fiat is more ideological than practical.

What appears to be unfolding is not the decline of the dollar but a reconfiguration of its infrastructure—a form of monetary “rebasement” driven by digital technology. USD stablecoins are not undermining the U.S. monetary system; they are extending it. By enabling near-instant digital payments on blockchain networks while holding reserves in U.S. Treasuries and cash equivalents, stablecoins effectively reinforce the dollar’s global dominance.

If USD stablecoins evolve into a widely used transactional layer—an outcome that remains a forward-looking assumption—the demand for Treasuries could rise substantially. With industry projections placing the stablecoin market at $2–$3 trillion by 2030, issuers could become meaningful buyers of Treasury securities. Such demand could deepen liquidity in money markets, help maintain lower yields, and further integrate Treasuries into the operational backbone of global finance.

At the same time, investors should remain aware of the risks. The widespread adoption of stablecoins is far from guaranteed. Regulatory frameworks could slow development, transparency and custody concerns persist with some issuers, and Central Bank Digital Currency initiatives could create competing payment systems. If stablecoins fail to expand beyond crypto-trading and settlement use cases, their broader economic impact may remain limited.

Even with those uncertainties, the broader investment thesis remains compelling:

- U.S. Treasuries continue to be a foundational global asset. Demand from both traditional institutional buyers and digital-dollar issuers reinforces their central role in financial markets.

- The growing USD stablecoin ecosystem may create opportunities for companies involved in custody, liquidity provision, and compliant digital payment infrastructure, including firms such as Circle Internet Financial, Coinbase, PayPal, Fiserv, Visa, and Mastercard.

- Financial institutions and fintech platforms operating at the intersection of blockchain settlement and regulatory compliance may also play a key role in this emerging architecture, including JPMorgan Chase, Bank of New York Mellon, Citigroup, Block Inc., and Stripe Inc..

The United States Dollar is not fading away—it is adapting and transforming. In many ways, USD stablecoins could act as the bridge between the traditional financial system and the emerging digital economy. As regulatory frameworks and financial technology continue to develop, these digital dollars are increasingly supported by the credibility of U.S. sovereign credit.

For investors prepared to position themselves for this shift, the opportunity lies in recognizing how the dollar’s role is evolving. The story is not about the collapse of the dollar system, but about the digitization and expansion of dollar dominance in the next era of global finance.

Sources: Lance Roberts

Leave a comment