Since the pandemic, the distinction between passive investing and outright speculation has increasingly blurred. The current surge in speculative behavior extends well beyond traditional financial markets. A similar mindset can be seen in the rapid growth of Sports betting industry as well as the rising popularity of event-prediction platforms such as Kalshiand Polymarket.

Within financial markets, signs of heightened risk-taking are evident. Margin debt has climbed to record levels, while zero-day-to-expiry options (0DTE) now represent roughly half of total options trading volume. At the same time, the number of leveraged exchange-traded funds (ETFs) and their trading activity have expanded significantly.

As highlighted by The Kobeissi Letter, the technology sector has become the primary focus of this trend. There are currently 108 long and 31 short leveraged ETFs tied to technology stocks, bringing the total to 139 funds. That figure is three times larger than the next-largest sector, financials, which has 47 leveraged ETFs. For comparison, consumer discretionary has 44, and communication services has 34. In other words, the technology sector alone now hosts more leveraged ETFs than the next three sectors combined.

Although it is harder to measure than indicators like margin debt or sports wagering, aggressive speculation is increasingly visible within so-called passive investment vehicles. One clear example is the rapid and often intense rotations occurring between sector and factor exchange-traded funds (ETFs).

In this article, we examine how today’s speculative environment is influencing trading behavior within passive ETFs. We also explore methods for identifying sector and factor rotations and discuss how investors may be able to take advantage of these shifts—effectively turning the increasingly aggressive behavior of passive investors into potential opportunities.

Passive Investment Strategy Timeline

The intellectual foundation for passive investing dates back to Harry Markowitz, who introduced Modern Portfolio Theory in 1952. His research demonstrated that diversification across a broad market portfolio could maximize expected returns for a given level of risk. Markowitz’s work ultimately laid the groundwork for what would later become known as index investing, the core principle behind many passive investment strategies today.

John C. Bogle is widely regarded as the “father of indexing.” In 1976, he introduced the First Index Investment Trustat Vanguard Group, a fund designed to track the S&P 500. It became the first index mutual fund accessible to retail investors. At the time, competitors ridiculed the concept, referring to it as “Bogle’s Folly.” Decades later, Vanguard oversees more than $12 trillion in assets, demonstrating the success of Bogle’s low-cost, long-term passive investing philosophy. Ironically, Bogle also cautioned that the intraday liquidity of exchange-traded funds might encourage the kind of frequent trading behavior he spent his career advising investors to avoid.

In 1993, the SPDR S&P 500 ETF Trust became the first exchange-traded fund available to U.S. investors, allowing them to trade a passive index product throughout the day just like a stock.

Passive investment strategies were originally designed to promote discipline and long-term thinking. Rather than attempting to outperform the market by actively trading individual securities, passive approaches aim to replicate overall market performance through broad diversification.

Bogle’s Warning

Despite the strong long-term rationale behind passive investing, investor behavior has evolved in ways Bogle anticipated. ETFs, with their ease of trading and intraday liquidity, have encouraged some passive investors to adopt more active strategies.

In recent years, sharp performance differences have emerged across broad-market indexes, sector ETFs, and factor-based ETFs. Instead of simply buying a diversified market ETF and holding it over time, many investors now frequently rotate between products tracking major indexes like the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average, as well as sector-focused funds (such as technology, consumer staples, or financials) and factor strategies (including momentum, value, or market-cap tilts).

Another clear example of speculative behavior within the passive universe is the growing popularity of leveraged ETFs. These funds reset their exposure on a daily basis, which can gradually erode returns over time and makes them better suited for short-term trading rather than long-term investing. This effect, known as Volatility Decay, is significant enough that regulators require warnings in leveraged ETF prospectuses. As stated in the prospectus for Direxion ETFs:

“If a Fund’s shares are held for a period other than a calendar month, the Fund’s performance is likely to deviate from the multiple of the underlying exchange-traded fund performance for the period the Fund is held. This deviation will increase with higher underlying volatility and longer holding periods.”

The rapid growth in leveraged ETF products and trading volume—mentioned earlier—reflects the increasing presence of short-term speculation within instruments originally designed for passive investing.

Another sign of this trend is the sharp rise in thematic ETFs. Funds centered on popular narratives—such as Artificial Intelligence, clean energy, or precious metals—often attract substantial inflows when investor enthusiasm is strong. When the narrative loses momentum, however, those same funds can experience rapid outflows. In many cases, this behavior resembles momentum chasing wrapped in the appearance of passive investing.

In fact, many investors who consider themselves passive might find—if they reviewed their transaction history closely—that their activity resembles active trading far more than traditional buy-and-hold investing.

Rotation Analysis

Recognizing that investors are aggressively rotating across sectors and factors using passive instruments is only the first step. The real challenge is identifying how to profit from these movements. One approach is technical analysis, which can help detect when rotations begin, gain momentum, stall, or reverse.

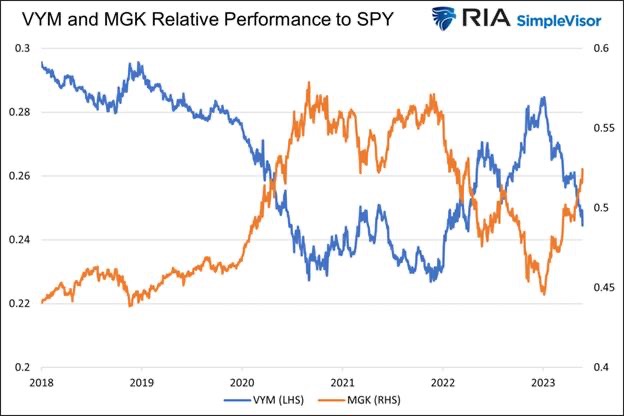

We first explored this concept in detail in our 2023 article, Relative Rotation – Unlocking the Hidden Potential. One of the most compelling illustrations from that research compares the relative performance of Vanguard High Dividend Yield ETF and Vanguard Mega Cap Growth ETF against the SPDR S&P 500 ETF Trust. The chart demonstrates a recurring pattern: when one ETF begins to outperform the broader market, the other often underperforms. This dynamic creates a rotation effect that, when identified early through technical analysis, may provide trading opportunities.

The more aggressively passive investors rotate between sectors and factors, the more consistent and exploitable these technical patterns can become.

Narrative Analysis

While technical analysis can signal when a rotation is beginning or gaining momentum, narrative analysis helps explain why investors are moving capital. Understanding the narrative behind a trade allows investors to determine whether the underlying story is supported by fundamentals or driven primarily by speculation.

In today’s market—where passive instruments are frequently traded in an aggressive, short-term manner—narratives spread quickly and can have a powerful impact. A compelling theme can generate billions of dollars in ETF inflows within days, often well before the fundamentals justify the move, if they ever do.

However, not all market narratives carry the same weight. Some sector or factor rotations are triggered by genuine shifts in economic conditions or changes in monetary policy. These developments tend to produce more durable trends. Others arise largely from momentum and media attention. In such cases, a popular theme gains traction, investors pour money into ETFs aligned with that story, and the momentum feeds on itself until enthusiasm fades.

Distinguishing between these two types of narratives is just as important as identifying the rotation itself. A strong technical signal paired with a weak fundamental story may produce only a short-lived opportunity.

Summary

One of the great ironies of modern passive investing is that instruments originally designed to encourage patience and long-term discipline have increasingly become vehicles for short-term speculation. Many investors who consider themselves passive are, in practice, behaving much like active traders—rapidly rotating between sectors and factors based on evolving narratives.

Recognizing this dynamic is the first step toward maintaining stronger investment discipline. Through our blog posts, daily commentary, podcasts, and the weekly Bull Bear Report, we aim to help investors distinguish meaningful signals from the noise created by constantly shifting market narratives.

Sources: Michael Lebowitz

Leave a comment