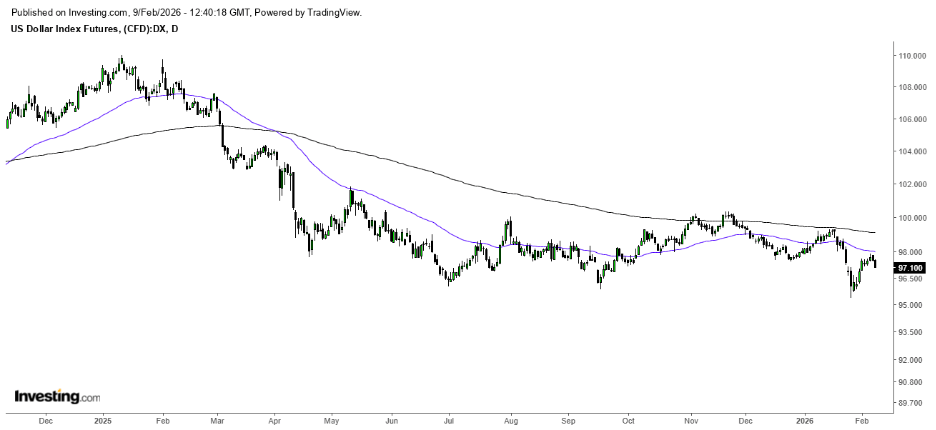

The U.S. dollar is in focus this week as investors await key economic data, including Non-Farm Payrolls and inflation figures that were postponed last week due to delays in passing a government spending bill. Recent data, such as the ADP report released on February 4, point to a cooling labor market. Attention will also turn to inflation readings due on Friday.

While high-frequency and analytical indicators suggest inflation is no longer accelerating and is gradually easing, it remains sticky—particularly in the services sector—keeping core inflation above the Federal Reserve’s 2% target.

CME FedWatch data indicate that markets continue to expect a gradual easing cycle from the Fed. The probability of a March rate cut remains low, at around 20–23%, with investors instead anticipating potential cuts later in the year as clearer signals emerge from inflation and labor market trends. Longer-term pricing implies a base case of 50–75 basis points of cumulative rate cuts by 2026. These expectations appear to be limiting further upside for the U.S. dollar.

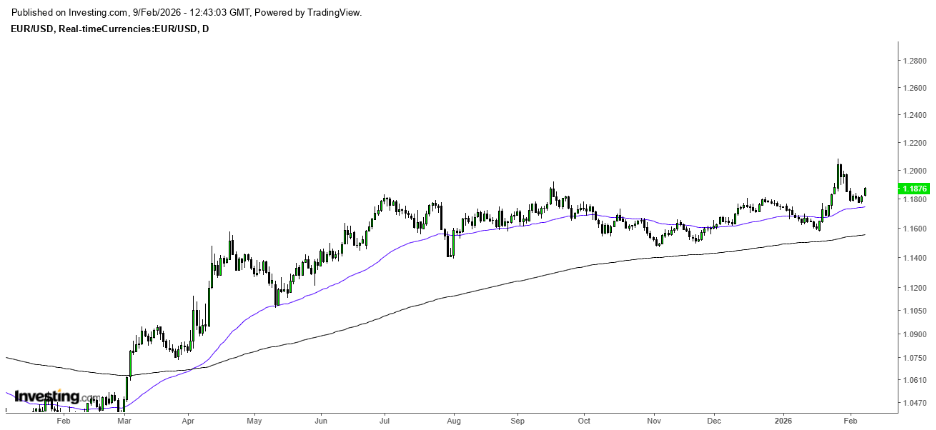

In the euro area, inflation has already fallen to around or below target. ECB President Christine Lagarde said last week that inflation is in a good place, even though readings may fluctuate in the coming months due to unpredictable geopolitical risks, stressing that policy will not react to every data point.

Euro-area money markets are therefore pricing in a much firmer policy stance. Current market pricing implies roughly a 90% chance of no rate change at the March 2026 Governing Council meeting, with very limited easing expected over the year—around 0–10 basis points and, in some scenarios, no cuts at all. With inflation already subdued and a stronger euro adding further disinflationary pressure, euro-area rates are seen as relatively stable.

By contrast, U.S. front-end rates are expected to decline more quickly, by around 50–75 basis points. This narrowing of short-term rate differentials in favor of the euro provides mechanical support for further upside in EUR/USD.

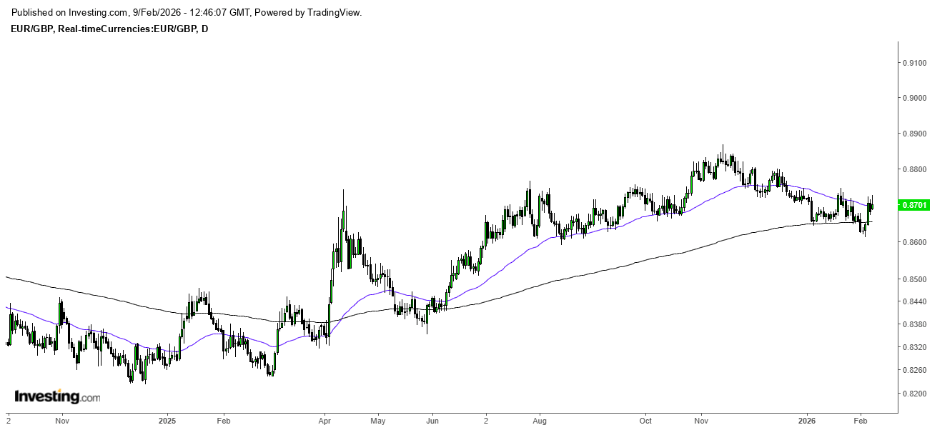

Last week, the Bank of England kept its policy rate unchanged at 3.75%, but the decision was narrowly split 5–4, with an unexpected four members voting for an immediate 25 basis point cut. Forward guidance indicated that rates are “likely to be reduced further.” The BoE expects inflation to ease toward 2% from April, and both markets and economists are leaning toward a rate cut in the spring, around March or April.

Compared with the BoE, the ECB is seen as maintaining a steadier policy stance. As a result, the BoE’s signal that cuts are more likely later on does not, by itself, justify further downside in EUR/GBP unless the ECB were to shift unexpectedly toward a more dovish hold. Upcoming UK data through March and April—particularly wage growth, services CPI, and the April CPI release—will be crucial in determining whether the probability of an April rate cut rises, which would likely weigh on the pound.

In conclusion, interest rate differentials are narrowing, but unevenly. The Fed’s eventual easing bias caps sustained strength in the U.S. dollar, the ECB’s comparatively stable stance supports the euro, and the Bank of England’s closer proximity to further rate cuts creates relative downside risk for sterling.

Sources: Dennis Mwenga

Leave a comment