MUFG’s Michael Wan says Brent crude has slipped below US$110 per barrel after President Trump halted a US-backed operation to assist vessels leaving the Strait of Hormuz, as negotiations with Iran continue. He emphasizes that disruptions in the Strait go beyond oil prices, potentially triggering wider shortages in products such as energy, petrochemicals, and fertilizers—placing import-reliant economies at greater risk.

Hormuz tensions pressure Brent Oil

“Brent crude dropped under US$110/bbl and the Dollar weakened after President Trump announced a pause in a US-led mission to help stranded ships leave the Strait of Hormuz, allowing time to see whether a deal with Iran to end the conflict can be reached.”

“More broadly, as we’ve noted over the past two months, the implications of disruptions in the Strait of Hormuz extend beyond oil, raising the risk of shortages across a wide range of goods, including energy, petrochemicals, and fertilizers.”

“Countries that rely heavily on Middle Eastern oil, have limited ability to shift to domestic energy sources, and depend more on imported energy and food are generally more exposed to various risk scenarios.”

Oil remains supported as disruptions in the Strait continue and diplomatic efforts show little progress.

Geopolitical tensions keep the risk premium elevated amid tanker incidents and stalled U.S.–Iran negotiations.

Brent’s outlook stays bullish, with prices potentially pushing toward $110 unless supply conditions improve.

Crude oil pulled back from earlier highs by mid-morning in the London session as markets opened the week with uncertainty over the timing and outcome of the US–Iran standoff.

Reports from Axios suggested that Iran has proposed a potential reopening of the Strait of Hormuz, offering a tentative sign of progress in what has been a slow and uneven path toward any agreement. However, this falls short of a true breakthrough. Following last week’s strong rally, the balance of risks for oil prices still leans to the upside.

What’s Driving the Oil Market?

Over the weekend, Donald Trump said he had canceled plans to send Special Envoy Steve Witkoff and Jared Kushner to Pakistan for talks with Iran. This came after Iran’s Foreign Minister Hossein Amir-Abdollahian left Islamabad without agreeing to meet US officials—hardly a sign of easing tensions.

Looking ahead, the outlook remains unclear. Tehran appears unwilling to engage while the naval blockade persists, while Washington is holding back its negotiators. This leaves markets in a holding pattern. While broader risk assets try to anticipate a resolution, oil traders are focused on the tangible factor: the actual flow—or lack thereof—through the Strait of Hormuz.

In this environment, oil prices are likely to continue edging higher unless disrupted by an unexpected shift. Recent tanker seizures and increased military activity in the Strait have reinforced the geopolitical risk premium embedded in prices.

If tensions escalate into open conflict, there is clear room for a sharper upside move. For now, as long as access through the Strait remains constrained, that premium is unlikely to fade. Rhetoric alone—no matter how constructive—has limited impact without real changes on the ground.

Ultimately, oil’s direction depends heavily on how the US–Iran situation evolves. Until there is meaningful progress, the path of least resistance remains upward, with Brent approaching a potential test of $110.

All About Oil Flows: Demand Destruction Highly Unlikely

While additional supply from producers like the United States and Russia may offer some relief, the global economy still relies heavily on energy shipments from the Gulf—underscoring the critical role of the Strait of Hormuz. The longer disruptions persist, the more pronounced the supply imbalance becomes. Demand may soften at the margins through rationing or reduced consumption, but it is unlikely to fully offset the shortfall.

In simple terms, a meaningful decline in oil prices would likely require a full reopening of the Strait and a normalization of shipping flows. Until that happens, the balance of risks remains tilted to the upside.

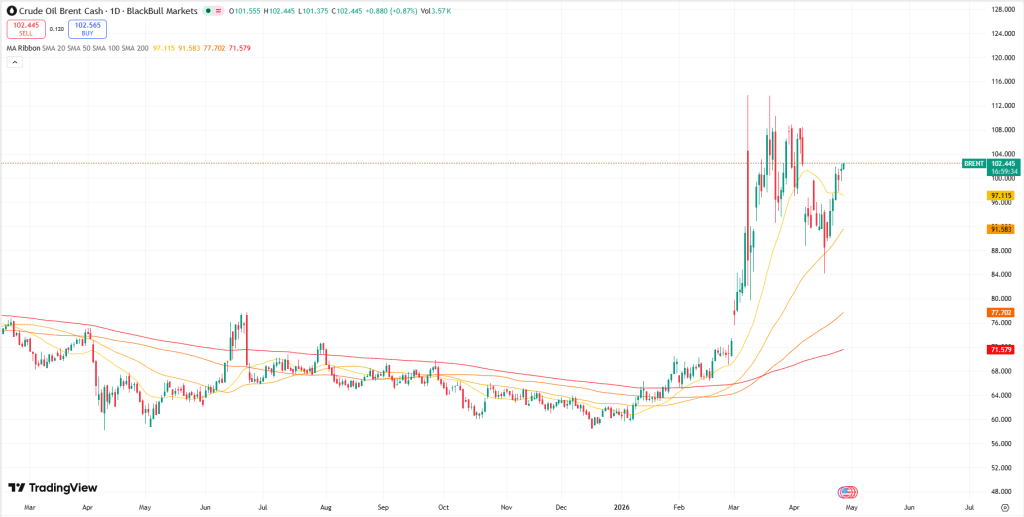

Technical Analysis and Levels to Watch on Brent

From a technical perspective, Brent continues to trend higher, with steady gains over recent sessions and only shallow pullbacks along the way. The move back above the $100 per barrel mark—broken earlier last week—has reinforced a bullish bias, with prices finding support on short-term dips.

Dip-buying is likely to remain a dominant theme unless conditions around the Strait of Hormuz worsen significantly. Key downside levels to watch include $103.50 and the psychological $100 mark.

In the near term, Friday’s high at $107.45 and Thursday’s high at $107.35 form an important zone. The $107.35–$107.45 range now acts as the first support area to monitor.

On the upside, resistance remains relatively thin until the $110 level, which could be tested soon barring any unexpected geopolitical breakthrough. Beyond that, the next potential resistance levels are $111, followed by $115 and $120 if bullish momentum persists.

Overall, unless a clear lower low and reversal pattern emerges, the path of least resistance for oil prices continues to point upward.

Breakdown in negotiations boosts oil, pressures risk assets, and adds strain on gold.

Higher yields and stagflation concerns introduce new headwinds for gold prices.

Gold stays range-bound amid rising volatility and an uncertain outlook.

With much of the optimism already priced in, markets responded to the weekend’s no-deal outcome largely as expected—starting the week on a weaker footing, while oil surged at the Monday open. Gold did rebound from overnight lows and pared some losses during the European session, but the overall tone appears to have shifted slightly more bearish for the time being.

What Failed Talks Mean for Gold?

The recently announced US–Iran ceasefire had initially eased market tensions, with cautious optimism that discussions in Islamabad could extend the two-week window. However, those talks have now concluded without a deal, suggesting the Strait of Hormuz is likely to remain effectively closed for now, continuing to strain energy markets.

As a result, oil prices may stay elevated for longer, raising the risk of renewed stagflation concerns, pushing bond yields higher, and bringing back headwinds for gold, along with equities and currencies.

Oil has already surged roughly 7–8% after reports that Washington plans to deploy a naval blockade on Iranian ports. While the exact implementation and its full impact remain uncertain, the situation now points to escalation rather than the de-escalation markets had hoped for.

That said, investors may still question whether any underlying progress was made. Even without a formal agreement, it is possible that these talks have set the stage for further negotiations within the remaining ceasefire period. For now, however, risk-sensitive assets—including gold—are once again facing pressure.

Gold Technical Analysis

Gold has held onto a solid portion of the gains accumulated over the past couple of weeks, though it continues to trade within a range. In the near term, immediate resistance is seen around $4,730, aligning with Friday’s low.

Last week, gold struggled to break above the $4,800–$4,850 resistance zone, which remains the key level to watch this week. This area represents a strong confluence—former support turned resistance, the underside of a broken trendline, and the 61.8% Fibonacci retracement of the March decline all aligning.

Until this zone is decisively cleared, it’s hard to build a convincing case for sustained upside.

Beyond that, the next major level comes in at $5,000—significant not only from a psychological standpoint but also technically, as the 78.6% retracement lies just below it. A firm break above $5,000 would likely tilt momentum more clearly in favor of the bulls.

Support Levels to Watch

Gold’s recent rally was underpinned by a weaker dollar, falling yields, and generally stronger equities, helping prices recover from the $4,100–$4,200 zone, where the 200-day moving average sits.

Attention now turns to $4,600 as the first key support level—an area that previously acted as resistance and may now provide a floor.

Below that, $4,500 remains a relevant level.

However, the most critical support to watch is $4,400. It held firmly in early February and, despite a brief breakdown in March, the quick rebound above it suggests it still carries significance. A decisive move and close below $4,400 would signal a more meaningful—and notably bearish—shift in market structure.

As long as gold trades between $4,400 on the downside and $5,000 on the upside, the broader picture remains range-bound.

This isn’t necessarily negative—it simply favors a different strategy. With heightened volatility, opportunities have been present, but the focus is more on trading within the range rather than positioning for sustained trends.

A clear breakout on either side should provide stronger directional cues. Until then, flexibility remains key.

U.S. President Donald Trump said Sunday evening that he was unconcerned about whether Iran would return to negotiations after ceasefire talks over the weekend failed to produce an agreement.

He also confirmed that the United States intends to impose a blockade on the Strait of Hormuz starting Monday morning, accusing Iran of failing to honor its commitment to reopen the vital shipping route. Speaking to reporters at Joint Base Andrews, Trump stated that the U.S. would be fine even if Iran chose not to resume talks.

His remarks followed a report indicating that several countries are attempting to restart diplomatic efforts after lengthy discussions in Islamabad ended without a deal. Despite the breakdown, sources suggested that further negotiations could take place within days, while regional governments are working with Washington to extend a fragile two-week ceasefire.

The Islamabad meeting represented the highest-level direct engagement between U.S. and Iranian officials since 1979, with 21 hours of talks concluding without progress. Vice President JD Vance said the U.S. had clearly outlined its conditions, but Iran declined to accept them.

U.S. demands reportedly included ending uranium enrichment entirely, dismantling key nuclear facilities, surrendering enriched materials, reopening the Strait of Hormuz without fees, promoting broader regional stability, and ceasing support for groups such as Hezbollah and the Houthis. Iran, however, proposed limited enrichment or reducing its stockpile, but the two sides failed to reach a compromise.

In response to Trump’s blockade announcement, Iranian Parliament Speaker Mohammad Bagher Qalibaf warned that Iran would not back down under pressure, stating that any confrontation would be met with force.

The U.S. plans to enforce the blockade on all vessels entering or leaving Iranian ports from 10 a.m. ET on April 13, covering areas along the Arabian Gulf and Gulf of Oman. It remains unclear whether U.S. allies will participate. Trump also criticized NATO for its lack of involvement and said Washington is reassessing its relationship with the alliance.

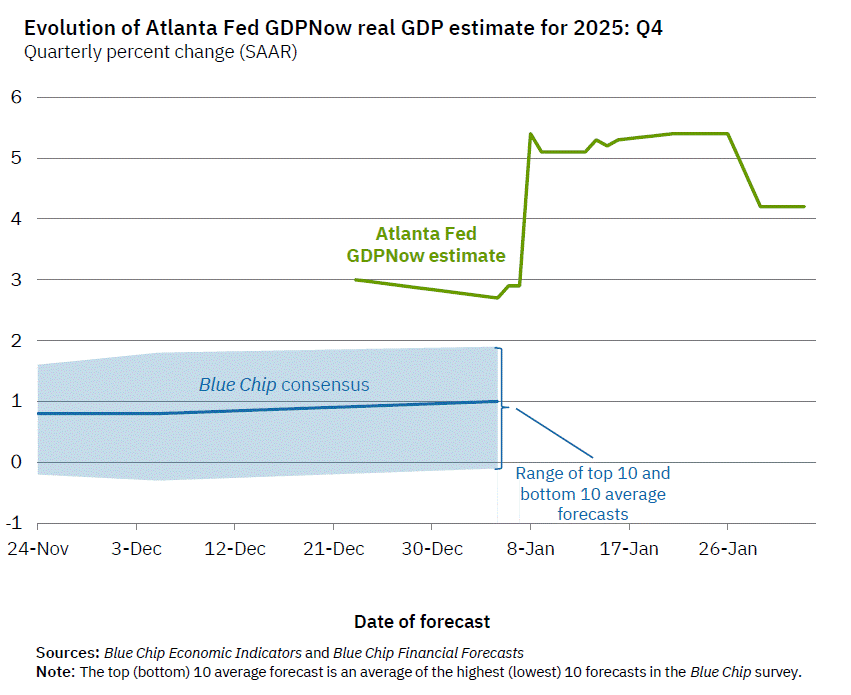

Recent U.S. growth data have pointed to notable economic resilience — but consumer sentiment tells a more cautious story.

According to the Federal Reserve Bank of Atlanta, real Gross Domestic Product is projected to have expanded at an annualized pace of 4.2% in the fourth quarter of 2025. That figure exceeded expectations and represents one of the strongest quarterly performances in the past two years.

The expansion was supported by steady consumer spending, firmer exports, and higher government expenditures. Household consumption climbed 3.5%, its fastest rate of increase this year. On the surface, these numbers portray a macroeconomy that remains firmly in growth mode.

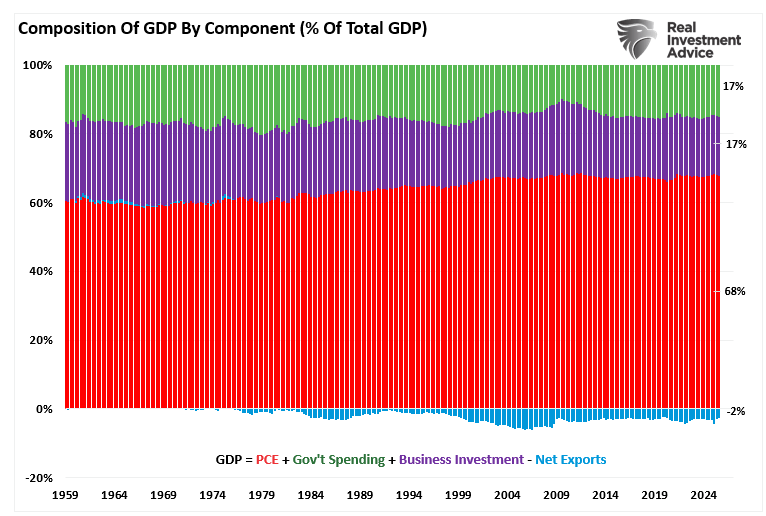

Gross Domestic Product (GDP) represents the total value of goods and services produced within the United States. Of that total, personal consumption expenditures (PCE) account for roughly 68%. Put simply, the consumer is the backbone of the U.S. economy — as household spending goes, so too goes overall economic growth.

When GDP rises, it reflects an increase in overall economic activity — stronger consumer demand that supports higher production and broader expansion. For that reason, growth rates are closely watched by policymakers, investors, and corporate leaders. Strong GDP figures are often interpreted as a signal of improving sales prospects and profit potential.

However, GDP does not tell the whole story of household financial well-being.

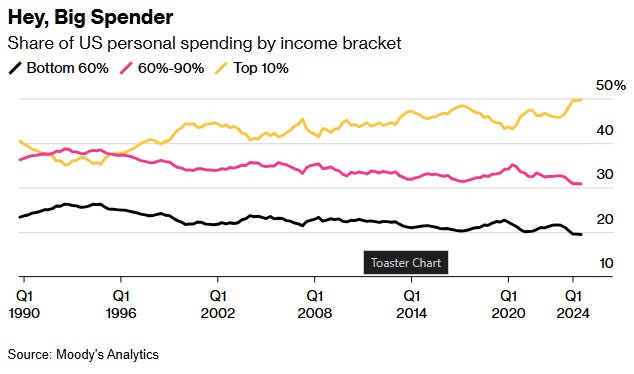

By design, economic growth data measure aggregate output. They do not reveal how income is distributed, how conditions vary across regions, or how millions of families actually experience the economy. A clear illustration is the breakdown of consumer spending by income level. At present, roughly half of all U.S. consumer spending is driven by the top 10% of earners — a share that has been increasing — while the spending contribution from the bottom 90% has been declining.

In other words, headline growth can appear solid even as the underlying breadth of participation narrows.

In short, strong headline growth can conceal areas of financial strain among households and small businesses. Expansion driven primarily by exports or government spending may not meaningfully filter through to broad segments of workers, creating a disconnect between aggregate output and lived experience.

A clear example of this distortion appeared in 2025. In the first quarter, a surge in imports aimed at front-running tariffs weighed heavily on GDP. When those trade fears subsided in the second quarter, import flows normalized, producing a sharp rebound in growth. Yet these swings in trade data had limited direct impact on most consumers. The volatility was largely statistical rather than reflective of a dramatic shift in household conditions.

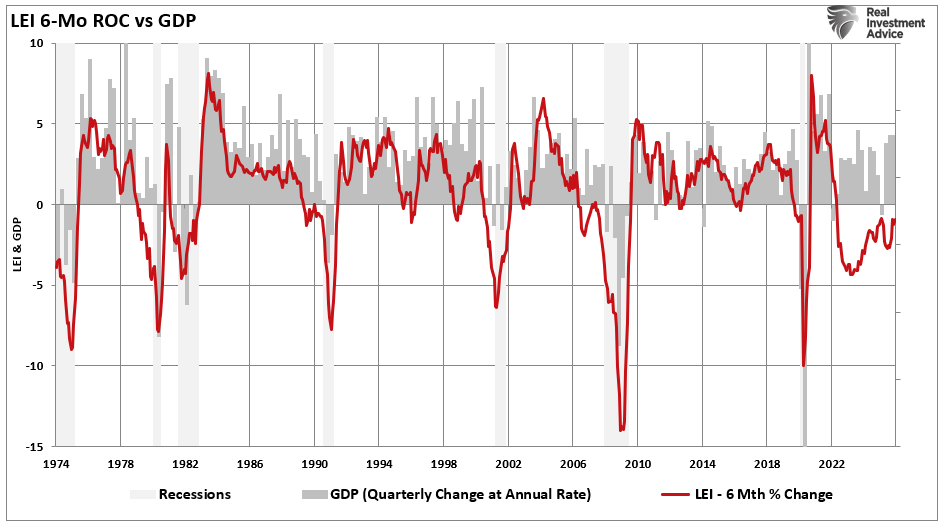

While GDP figures suggest a sturdy economic backdrop, other coincident and leading indicators tell a more cautious story. The The Conference Board Leading Economic Index (LEI), which historically leads the U.S. economy by roughly six months, has remained in contraction for an extended period. Its six-month rate of change has long been regarded as one of the more reliable signals of impending slowdowns or recessions.

Notably, however, despite the prolonged weakness in the LEI, the broader economy has not formally entered recession — underscoring the growing divergence between traditional warning signals and realized economic outcomes.

At first glance, headline growth data suggest the economy remains on firm footing. Output is expanding, spending is holding up, and aggregate indicators point to continued resilience.

But a closer examination reveals a more nuanced picture. Beneath the surface, several crosscurrents — from uneven income distribution and trade-related distortions to persistent weakness in leading indicators — point to a mixed underlying environment.

That divergence helps explain why economic sentiment can feel far weaker than the headline numbers imply. Strong aggregate growth does not automatically translate into broad-based confidence, particularly if gains are concentrated or forward-looking indicators continue to flash caution.

The Gap Between Rising Stocks and Weak Consumer Sentiment

Historically, it makes sense that stock markets and economic data would trend in the same direction over the long run. Corporate earnings ultimately derive from economic activity, and sustained growth in output and income should support higher equity valuations over time.

As discussed in “Return Expectations Are Too High,” long-term market returns are anchored to the growth of the underlying economy, productivity gains, and profit expansion — not simply short-term momentum or sentiment-driven rallies.

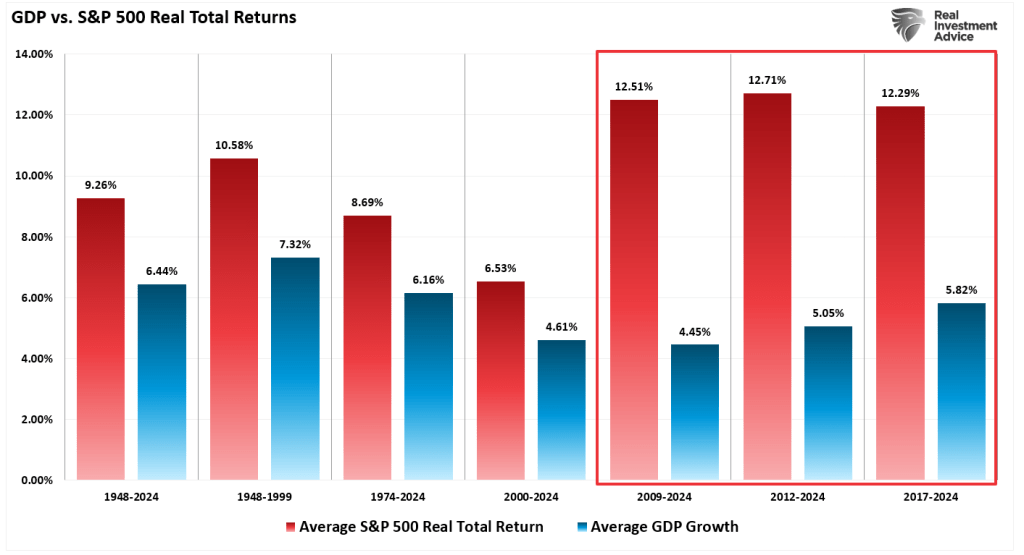

“The chart illustrates average annual inflation-adjusted total returns (including dividends) dating back to 1948, using total-return data compiled by Aswath Damodaran at the NYU Stern School of Business. From 1948 through 2024, the stock market delivered an average real return of 9.26%.

However, in the years following the 2008 financial crisis, inflation-adjusted total returns increased by nearly three percentage points across the last three measured periods.

Here’s the challenge: real (inflation-adjusted) equity returns are relatively straightforward to conceptualize. Over time, they reflect economic growth (GDP) plus dividend income, minus inflation. That relationship broadly held from 1948 to 2000.

Since 2008, though, the math has diverged. Nominal GDP growth has averaged roughly 5%, and dividend yields have hovered near 2%. Yet actual market returns have significantly exceeded what that underlying economic engine would normally justify in terms of sustainable earnings expansion.”

That 15-year divergence is not particularly surprising. As discussed in “Pavlov Rings the Bell,” markets have repeatedly been cushioned from deeper corrections by aggressive fiscal and monetary intervention.

Over the past decade and a half, major drawdowns were often met with policy stimulus — whether through deficit spending or actions by the Federal Reserve. Each episode of support was followed by market recovery, reinforcing a powerful feedback loop: intervention became associated with rising asset prices.

In effect, investors were conditioned to expect rescue during periods of stress — to buy every dip under the assumption that policymakers would step in. That conditioning ties directly to the concept of “moral hazard.”

Moral hazard (noun, economics): A reduced incentive to guard against risk when one is shielded from its consequences — as with insurance protection.

Following the Global Financial Crisis, near-zero interest rates and repeated rounds of quantitative easing strengthened the belief that a policy backstop would reappear whenever volatility increased. Over time, that expectation hardened into a reflexive behavior: assume support, assume recovery, assume higher prices.

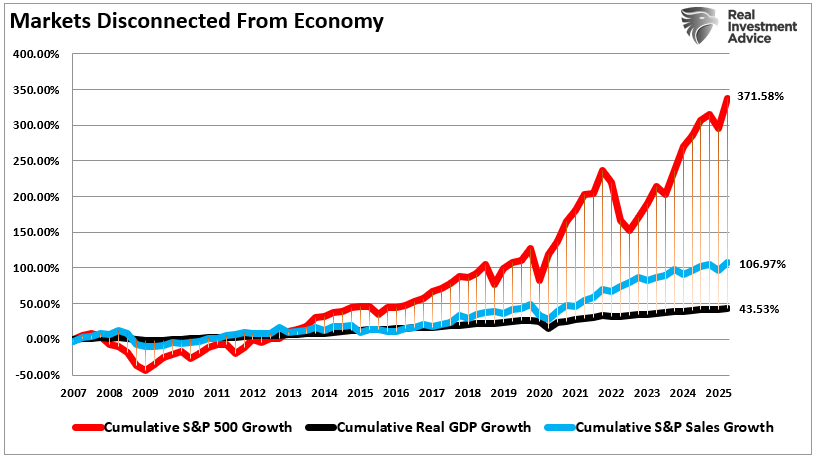

Those sustained supports — in both the real economy and financial markets — helped drive a wedge between underlying economic fundamentals and realized financial returns. In other words, policy intervention became a key force behind the growing disconnect between economic reality and asset-price performance.

At present, GDP growth has continued to surprise to the upside, and several macro indicators reflect ongoing resilience. At the same time, major equity benchmarks such as the S&P 500 have climbed to record levels. That advance has been fueled less by current consumer sentiment and more by expectations of future earnings growth.

The challenge, however, is that equity valuations appear increasingly disconnected from underlying revenue growth. Markets are pricing in optimism about future expansion, even as broad-based income and demand trends remain uneven.

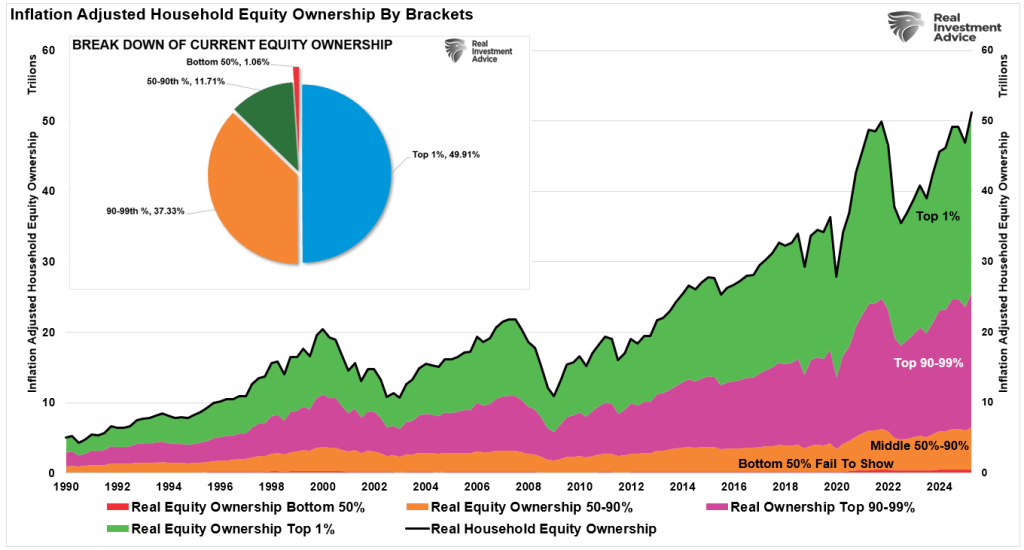

There is also a structural limitation embedded in the “wealth effect.” Rising stock prices can support consumption by boosting household net worth. Yet equity ownership in the United States is highly concentrated. Roughly 87% of equities are owned by the top 10% of households. As a result, the transmission from higher stock prices to broader economic activity is narrower than headline gains might suggest.

That concentration is reflected in spending patterns as well. The top 40% of income earners now account for approximately 80% of total consumption. Consequently, while financial asset values have surged, the macroeconomic lift from those gains is disproportionately tied to higher-income households — leaving sentiment among the broader population more subdued than market performance alone would imply.

That divergence goes a long way toward explaining the disconnect between subdued consumer sentiment and robust headline economic data.

When growth and market gains are concentrated among higher-income households — and asset-price appreciation primarily benefits those with significant equity exposure — aggregate statistics can remain strong even as large segments of the population feel financial strain.

In other words, the macro numbers reflect the strength of those driving the bulk of spending and asset ownership, while sentiment surveys capture the broader lived experience. The result is an economy that looks resilient on paper but feels far less secure to many households.

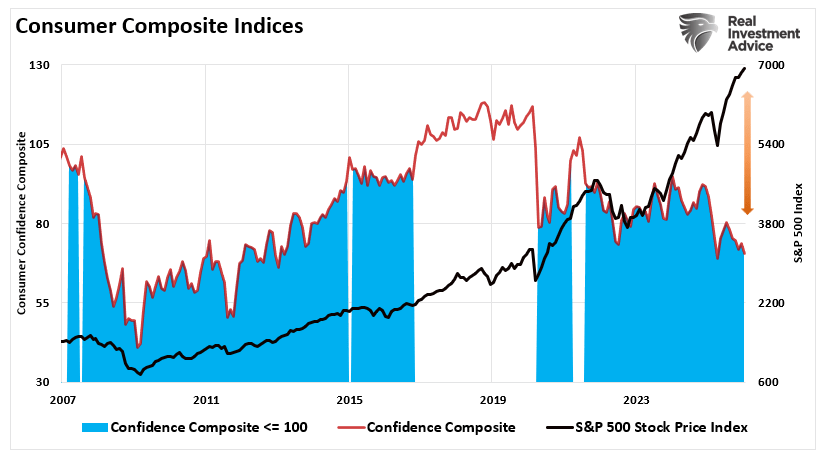

Consumer Confidence Surveys Remain Soft Even as Economic Data Stays Strong

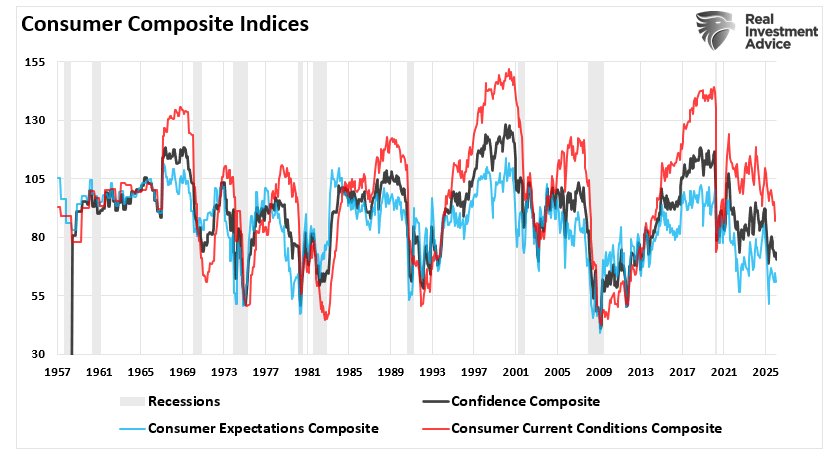

In clear contrast to upbeat macroeconomic indicators and strong equity market gains, consumer sentiment readings have deteriorated significantly. Both the Conference Board Consumer Confidence Index and the University of Michigan Surveys have fallen steeply over the past two years, even as stock prices have climbed. Historically, consumer sentiment tends to move in tandem with rising markets, which is intuitive. The chart below presents a composite measure combining these two leading sentiment indicators.

In both surveys, readings on current conditions and future outlook remain notably subdued, with the expectations component dropping to levels that have historically been linked to recession warnings.

The downturn in sentiment points to rising concerns over employment prospects, business conditions, and future income. Respondents frequently highlighted worries about inflation, elevated prices, food and energy expenses, the affordability of health insurance, and broader geopolitical and political uncertainty. Yet despite this widespread unease, GDP has continued to grow.

Importantly, the gap between soft sentiment data and hard economic figures is not unprecedented. Analysts have often observed that consumer attitudes tend to lag underlying economic performance, and sentiment could improve if expansion persists. In the near term, surveys typically capture prevailing fears and uncertainty, which can weigh on confidence even when actual spending remains relatively solid. Although nominal figures indicate that consumer spending is holding up, much of that resilience reflects paying higher prices for the same—or even fewer—goods, rather than an increase in real consumption, which helps explain the sustained weakness in sentiment readings.

Importantly, if consumer sentiment influences spending—and consumption accounts for roughly 68% of the economy—then that spending ultimately represents demand for businesses of all sizes. In a genuinely strong growth environment, we would expect improving demand to be mirrored by rising confidence across households. Yet, as the composite index illustrates, sentiment levels remain subdued. The historical relationship between confidence measures and the future trajectory of economic activity underscores why this divergence warrants attention.

Soft sentiment readings do not necessarily signal an imminent downturn. However, they do reflect a guarded mindset among both consumers and business owners. That caution can translate into more restrained spending across key components of GDP. If confidence remains depressed, a moderation in economic activity would be a reasonable outcome.

Why the Divergence Matters and What It May Signal Ahead

The gap between solid economic data, rising equity markets, and subdued consumer confidence carries meaningful implications. On the surface, macro indicators point to continued expansion, reinforcing higher stock prices and optimistic earnings forecasts. Yet beneath that strength, households and many business owners report lingering insecurity and pessimism about the future.

This disconnect prompts several key questions:

Can growth remain durable if confidence stays depressed?

Will corporate earnings hold up if consumers begin to retrench?

Could persistent pessimism eventually shape real-world behavior, leading to slower spending and softer growth?

History offers cautionary precedents where negative sentiment foreshadowed downturns—not because the hard data was inaccurate, but because sentiment ultimately influenced economic decisions.

The divergence also highlights distributional dynamics. Aggregate growth figures often mask disparities in income and wealth. Higher-income households account for roughly half of total consumption, while lower-income groups may not fully share in the benefits of expansion. That imbalance helps explain weaker sentiment readings. It also leaves markets vulnerable to any shock that prompts affluent consumers to scale back spending—particularly in an environment where the gap between economic “haves” and “have-nots” remains wide.

Investment Implications

For investors, this mixed backdrop argues for disciplined risk management. Markets may continue advancing on elevated earnings expectations, but those expectations can shift quickly as economic conditions evolve.

Scrutinize valuations. Rising indices do not preclude overpricing. Favor firms with strong balance sheets, reliable cash flows, and pricing power.

Diversify thoughtfully. Sector performance can diverge sharply. Defensive areas such as utilities, consumer staples, and healthcare often prove more resilient during sentiment-driven slowdowns.

Track leading indicators. Watch employment trends, consumer credit conditions, and forward-looking economic indices. Weak confidence can precede softer activity.

Maintain liquidity. Holding cash provides flexibility amid volatility created by divergence.

Consider hedging strategies. Exposure to bonds or volatility-linked instruments may help cushion downside risks.

Emphasize quality. Companies with durable competitive advantages are typically better positioned to navigate uncertainty.

The split between hard data, market performance, and consumer mood represents a meaningful economic signal. While there are persuasive arguments that markets can continue climbing and that pullbacks should be bought, prudence requires acknowledging alternative outcomes.

To borrow a well-known observation from Bob Farrell:

Historically, when “all experts agree,” discipline and preparation for the unexpected have often proven wise.

Gold prices were steady in Asian trading on Friday and remained on course for solid gains in February, supported by sustained safe-haven demand amid rising geopolitical tensions and economic uncertainty throughout the month.

Shifts in U.S. trade policy and worries about slowing growth in major global economies kept investors tilted toward defensive assets, helping bullion recoup much of its losses from late January.

Renewed conflict between Pakistan and Afghanistan also boosted demand for safe havens on Friday, although the fighting has so far remained contained between the two neighboring nations.

Gold set for solid February gains, rebounds from late-January slide

Spot gold steadied at $5,187.18 an ounce as of 00:12 ET (05:12 GMT), while April gold futures rose 0.2% to $5,203.61 per ounce.

Spot prices were up 6.7% in February, having largely recovered from sharp losses earlier in the month after a brief speculative rally quickly unraveled. Prices had dropped to as low as $4,600 an ounce in early February before rebounding.

Heightened geopolitical tensions surrounding Iran played a major role in gold’s recovery, as Washington increased its military presence in the Middle East and warned of possible action if Tehran refused to agree to a nuclear deal.

Talks between the U.S. and Iran concluded this week without a breakthrough. However, both sides agreed to continue negotiations in the coming weeks, raising some hopes for a potential agreement.

Elevated uncertainty surrounding the U.S. economy also supported gold’s advance, particularly after the Supreme Court of the United States struck down most of President Donald Trump’s trade tariffs.

Trump responded by unveiling fresh tariffs under a separate legal authority and warning of additional levies, keeping investors wary of further economic disruption stemming from trade measures.

Other precious metals climbed on Friday and were poised for strong monthly performances. Spot silver jumped 1.7% to $89.7785 per ounce, bringing its February gain to 6%, while spot platinum rallied 3% to $2,351.63 per ounce, up 8.4% for the month.

Copper poised for modest February gains as China demand eyed

Among industrial metals, copper prices edged higher on Friday and were on track for mild gains in February, as investors looked for clearer signals from China—the world’s largest importer of the metal.

Benchmark copper futures on the London Metal Exchange rose 0.2% to $13,333.0 per ton, bringing monthly gains to 1.2%. Meanwhile, COMEX copper futures climbed 0.4% to $6.0480 per pound, up 1.1% for the month.

Copper’s relatively subdued performance in February was partly due to reduced activity during China’s Lunar New Year holiday, which kept mainland markets closed for more than a week and sidelined many buyers.

Analysts at ANZ noted that copper inventories in China increased more than expected over the holiday period, alongside a buildup in global stockpiles, amid mining and trade disruptions.

With Chinese markets having reopened this week, attention has shifted back to potential buying activity. Copper demand is widely expected to strengthen in the coming quarters, particularly as the global artificial intelligence buildout gathers pace.

The Nasdaq 100 has experienced heightened volatility over the past two weeks. As of this morning, futures are trading near the 25,280 level, rebounding from last Thursday’s sharp drop to around 24,200 during a wave of aggressive selling. For context, the index was trading near 26,260 on January 28. Recent sessions have delivered fast-moving conditions, demanding disciplined tactics from short-term traders.

Yesterday, the Nasdaq 100 reached a high near 25,350. At this stage, risk management is essential. While today’s modest pullback does not reflect panic selling, underlying nervousness remains evident. Determining whether this anxiety presents a buying opportunity or signals further downside is particularly challenging for short-term traders.

Interpreting Current Market Conditions

Technical traders may feel relatively comfortable navigating the volatility, but the rebound from last Thursday’s lows has not provided strong justification for aggressive bullish positioning. A key issue for buyers is the index’s inability to hold higher levels. Although this creates intraday opportunities to trade support and momentum, maintaining a cautious stance remains prudent.

The Nasdaq 100 is historically a fast-moving market, and sharp swings are part of the landscape for day traders. Today’s U.S. Retail Sales data and tomorrow’s employment report may generate volatility. However, the most influential release is likely Friday’s CPI inflation report. A softer-than-expected inflation reading could provide renewed bullish momentum.

Searching for Positive Catalysts

Still, Friday is several trading sessions away, leaving ample time for continued fluctuations. In the near term, choppy price action appears likely.

While it may be simplistic to label the environment as merely volatile, a balanced approach may be best. Conservative traders could consider looking for modest pullbacks while remaining alert for potential upside reversals.

Cautious sentiment continues to weigh on the market, and traders would be wise to remain disciplined as institutional investors await clearer economic signals and stronger catalysts.

Nasdaq 100 Short-Term Outlook: Volatility Likely to Persist

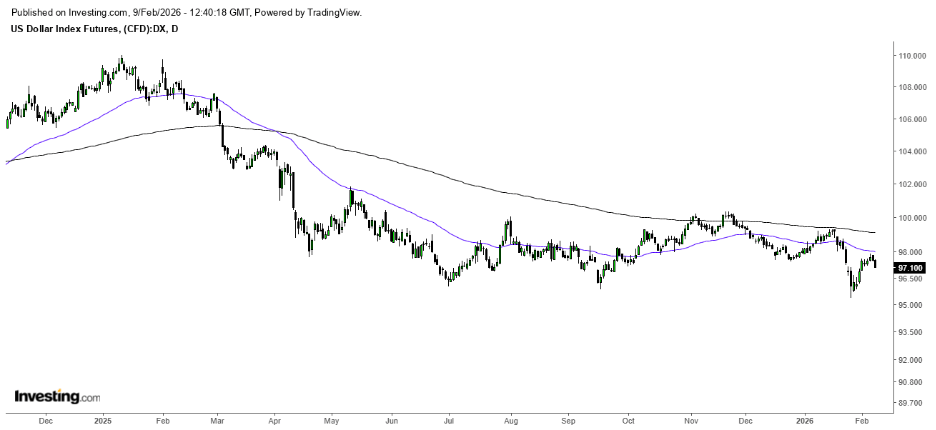

The U.S. dollar is in focus this week as investors await key economic data, including Non-Farm Payrolls and inflation figures that were postponed last week due to delays in passing a government spending bill. Recent data, such as the ADP report released on February 4, point to a cooling labor market. Attention will also turn to inflation readings due on Friday.

While high-frequency and analytical indicators suggest inflation is no longer accelerating and is gradually easing, it remains sticky—particularly in the services sector—keeping core inflation above the Federal Reserve’s 2% target.

CME FedWatch data indicate that markets continue to expect a gradual easing cycle from the Fed. The probability of a March rate cut remains low, at around 20–23%, with investors instead anticipating potential cuts later in the year as clearer signals emerge from inflation and labor market trends. Longer-term pricing implies a base case of 50–75 basis points of cumulative rate cuts by 2026. These expectations appear to be limiting further upside for the U.S. dollar.

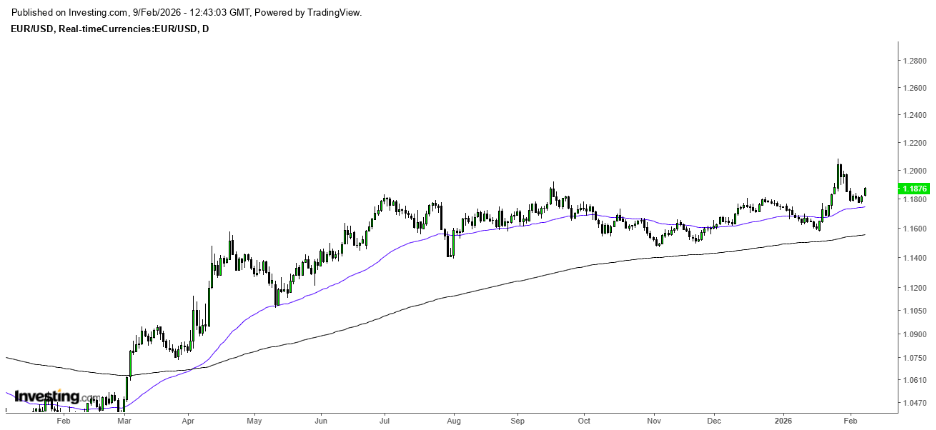

In the euro area, inflation has already fallen to around or below target. ECB President Christine Lagarde said last week that inflation is in a good place, even though readings may fluctuate in the coming months due to unpredictable geopolitical risks, stressing that policy will not react to every data point.

Euro-area money markets are therefore pricing in a much firmer policy stance. Current market pricing implies roughly a 90% chance of no rate change at the March 2026 Governing Council meeting, with very limited easing expected over the year—around 0–10 basis points and, in some scenarios, no cuts at all. With inflation already subdued and a stronger euro adding further disinflationary pressure, euro-area rates are seen as relatively stable.

By contrast, U.S. front-end rates are expected to decline more quickly, by around 50–75 basis points. This narrowing of short-term rate differentials in favor of the euro provides mechanical support for further upside in EUR/USD.

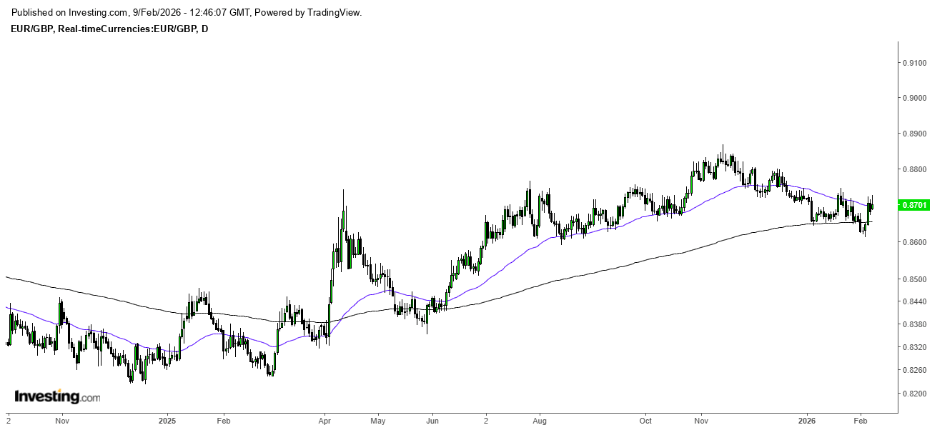

Last week, the Bank of England kept its policy rate unchanged at 3.75%, but the decision was narrowly split 5–4, with an unexpected four members voting for an immediate 25 basis point cut. Forward guidance indicated that rates are “likely to be reduced further.” The BoE expects inflation to ease toward 2% from April, and both markets and economists are leaning toward a rate cut in the spring, around March or April.

Compared with the BoE, the ECB is seen as maintaining a steadier policy stance. As a result, the BoE’s signal that cuts are more likely later on does not, by itself, justify further downside in EUR/GBP unless the ECB were to shift unexpectedly toward a more dovish hold. Upcoming UK data through March and April—particularly wage growth, services CPI, and the April CPI release—will be crucial in determining whether the probability of an April rate cut rises, which would likely weigh on the pound.

In conclusion, interest rate differentials are narrowing, but unevenly. The Fed’s eventual easing bias caps sustained strength in the U.S. dollar, the ECB’s comparatively stable stance supports the euro, and the Bank of England’s closer proximity to further rate cuts creates relative downside risk for sterling.

Brian Armstrong, CEO of Coinbase Global Inc. (NASDAQ: COIN), stated on Wednesday that the top U.S. cryptocurrency exchange cannot endorse a significant draft crypto regulation bill as it stands, delivering a setback to the bill’s chances as it advances to the Senate. Armstrong told lawmakers and industry participants that the recently introduced legislation includes “too many issues” and risks leaving the crypto sector in a worse position than under current regulations.

The bill seeks to create a clear regulatory framework for digital assets by defining when tokens qualify as securities or commodities and assigning the Commodity Futures Trading Commission (CFTC) oversight of spot crypto markets. However, Armstrong criticized parts of the bill that he believes would effectively ban tokenized equities, reduce the CFTC’s authority, and eliminate rewards on stablecoins—a key offering for Coinbase.

Without Coinbase’s support, the bill’s progress through the Senate Banking Committee is uncertain. Coinbase has played a significant role in shaping U.S. crypto policy and has contributed millions to political action committees backing pro-crypto candidates. Armstrong stated, “we’d rather have no bill than a bad bill,” but remains hopeful that ongoing negotiations could produce a better result. The Senate is expected to hold a markup session on the bill on Thursday, during which lawmakers will consider amendments and changes.