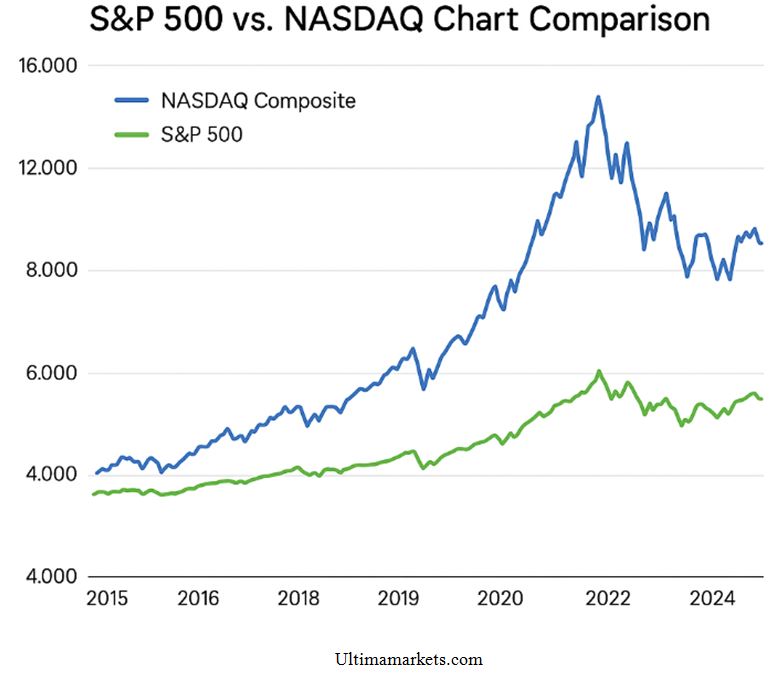

NASDAQ Composite — and technology stocks more broadly — are like a finely tuned sports car. They can easily lap your grandmother’s Oldsmobile — the Dow Jones Industrial Average — but they also require more maintenance and can stall at inconvenient moments.

Since its launch, and particularly since 2015, the NASDAQ has outperformed both the Dow and the S&P 500. Still, it’s very much a hare-and-tortoise story: the speedy rabbit occasionally takes long naps, yet ultimately wins the race — provided investors can tolerate the volatility that comes with tech-heavy exposure.

That dynamic is playing out again in the current market rotation. Since November 1, 2025, the Dow has gained 4.34%, while the NASDAQ has slipped 3.54% — a near mirror image. Once again, capital has rotated out of high-flying tech names (the flashy sports car) and into the steadier reliability of the Dow’s blue-chip stalwarts.

In April, Consumer Discretionary stocks tumbled during a tariff-driven selloff. Although they initially sank, they’ve since rebounded strongly. Betting against the U.S. consumer has historically been a mistake, especially when sentiment temporarily sours.

Over the past year, Consumer Discretionary shares outpaced Consumer Staples, though a recent rotation has narrowed that gap.

Yes, the NASDAQ can test your patience — even break your heart — but history suggests that endurance can pay off.

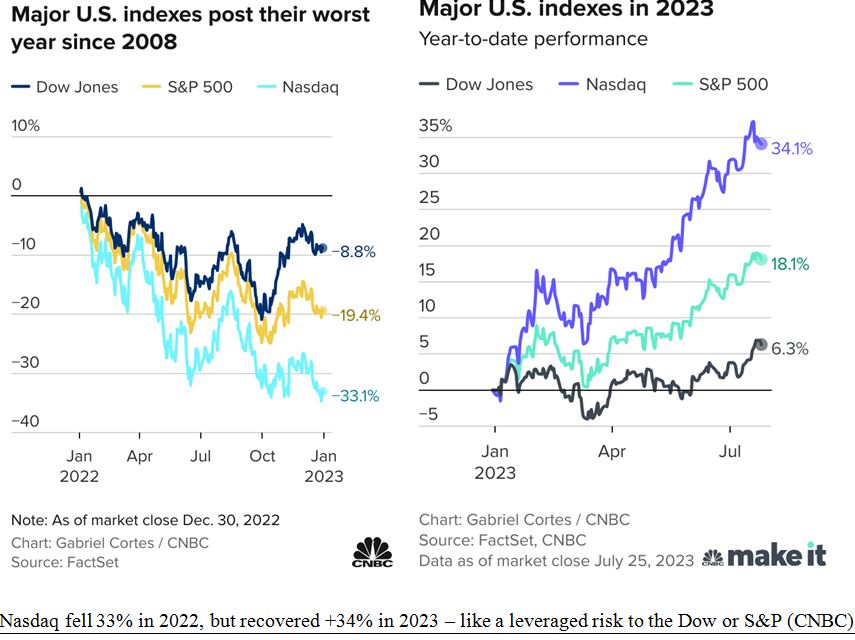

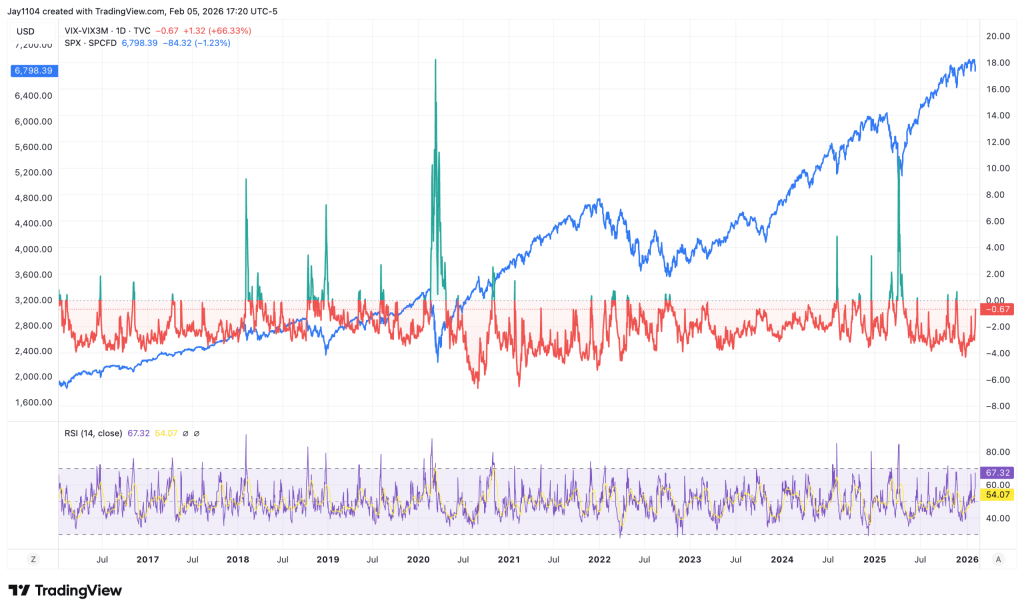

Consider late 2021. While Federal Reserve officials were still describing inflation as “transitory,” markets began adjusting. On November 19, 2021, the NASDAQ reached an all-time high of 16,057. Over the next 13 months, it plunged 36.4%, closing at 10,213 on December 28, 2022. During that same stretch, the S&P 500 fell about 19%, and the Dow declined just 7.65%.

Investors heavily concentrated in high-growth tech during 2022 likely felt significant pain. Yet those wounds healed quickly. From 2023 through 2025, the NASDAQ surged 122%, compared with a 78% gain for the S&P 500 and a more modest 45% rise for the Dow.

Short-term breakdowns in tech can be dramatic — but historically, they have often laid the groundwork for powerful long-term outperformance.

The Biggest NASDAQ Disaster – The Y2K Crash

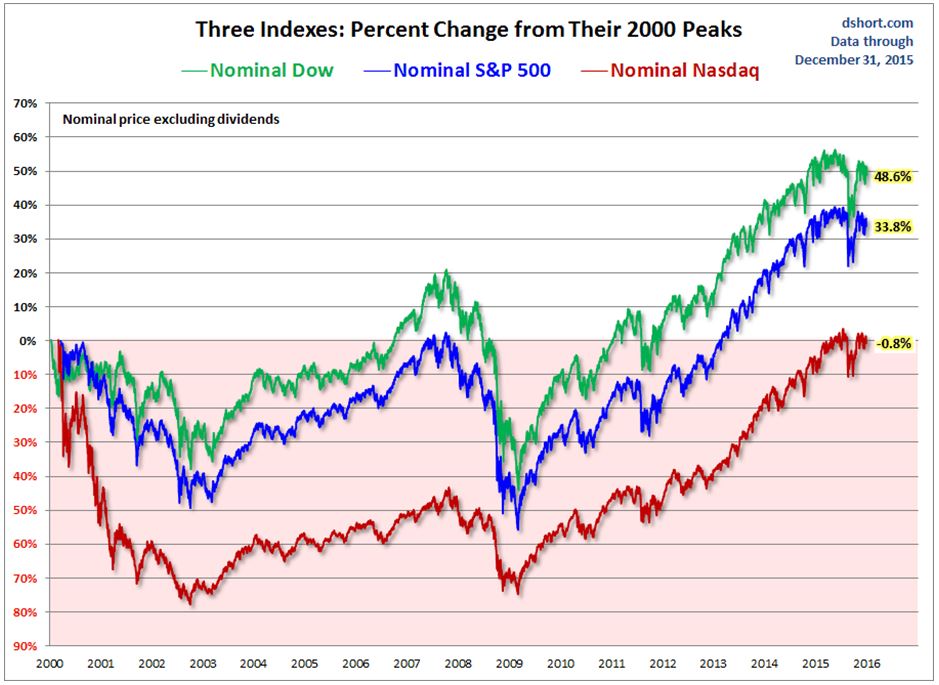

In 1999, the NASDAQ Composite was on a tear, doubling between June 1999 and March 2000, while the Dow Jones Industrial Average seemed half-asleep by comparison. That divergence flipped abruptly in March 2000. The Dow began climbing just as the NASDAQ collapsed, ultimately losing 50% or more in short order.

In February 2000, the NASDAQ experienced a classic “melt-up” even as the Dow drifted lower. By mid-April, the opposite occurred: the NASDAQ suffered its worst week, plunging while the Dow actually advanced. From the start of 1999 through the end of February 2000, the NASDAQ had soared 122%, compared with gains of just 16% for the S&P 500 and 17% for the Dow. Then came the reversal. Between March and May, the blue-chip indexes gained about 4%, while the NASDAQ tumbled 28%. In a single week — April 11–15 — the NASDAQ dropped 25.3%, even as the Dow rose 3.4%.

The aftermath was even more sobering. It took 16 years for the NASDAQ to reclaim its March 2000 peak. Meanwhile, the Dow and S&P 500 briefly reached new highs by 2007 and went on to establish lasting all-time highs by 2012. Over that 16-year span, the Dow climbed 48.6%, the S&P 500 gained 33.8%, and the NASDAQ was still slightly below its prior peak.

Still, comparisons between 2026 and the dot-com era can be misleading. The 1999 boom was driven largely by speculative internet companies with little or no earnings. Today’s technology leaders, by contrast, generate substantial revenues and profits, with strong forward guidance tied to tangible business applications. This is a very different foundation.

Over the long haul — since its launch 55 years ago — the NASDAQ has dramatically outperformed both the Dow and the S&P 500, often by multiples of two to four times. Since 1971, the NASDAQ has surged nearly 260-fold, rising from 89.61 to 23,242 at the start of 2026. Over the same period, the Dow has increased about 57-fold and the S&P 500 roughly 74-fold.

So while volatility can test investors’ patience, history suggests resilience. Not every four-letter ticker deserves a four-letter rebuke.

Each week, host and Zacks stock strategist Tracey Ryniec teams up with guest experts to break down the most compelling trends in stocks, bonds, and ETFs — and what they mean for investors’ everyday lives.

The era of the “Magnificent 7” may be winding down. Before that, investors rallied around the FANG stocks, which later evolved into FANGMAN. At one point, some pushed to include Tesla, transforming the group into the Magnificent 7.

Now, with several of those mega-cap names losing momentum, that once-dominant lineup appears to be fading.

Moving Past Apple and Microsoft

For years, mega-cap tech giants like Apple and Microsoft have led the market. But what if leadership shifts?

Tracey highlights five non–big tech companies that could emerge as the “new” magnificent stocks. All five are trading at fresh five-year highs and are projected to deliver double-digit earnings growth in 2026.

Are you prepared to look beyond Apple and Microsoft to discover the market’s next generation of winners?

5 New “Magnificent” Stocks to Consider for 2026

MasTec, Inc. (MTZ)

MasTec operates across communications, energy, and utilities infrastructure — positioning it as a potential AI infrastructure beneficiary. The stock has surged 225% over the past five years and is trading at fresh five-year highs.

While it has yet to report Q4 2025 results (due Feb. 26, 2026), earnings are projected to climb 61.8% in 2025 and another 28.6% in 2026. However, with a forward P/E of 33.5, the valuation is well above traditional value levels.

Does an infrastructure-focused growth name like MasTec deserve a spot on your watchlist?

Caterpillar Inc. (CAT)

Known for its construction and mining equipment, Caterpillar is benefiting from renewed infrastructure and development activity. Shares are up 262% over the past five years, also marking new five-year highs.

Earnings are expected to grow 18.9% in 2026. Yet, like MasTec, Caterpillar trades at a premium, with a forward P/E of 33.6.

Is there still upside ahead, or have investors already priced in the growth?

Walmart Inc. (WMT)

One of America’s largest retailers, Walmart has significantly expanded its online presence since 2020. The strategy appears to be paying off: shares have gained 164% over five years and sit at new highs.

Despite projected earnings growth of 11% in fiscal 2027, Walmart trades at a lofty 42.6 forward P/E — even higher than NVIDIA at roughly 25x.

Has Walmart become overheated, or is its transformation still underappreciated?

Eli Lilly & Company (LLY)

Eli Lilly, a pharmaceutical heavyweight, is riding strong momentum driven partly by its weight-loss treatments and an upcoming pill launch. The stock has soared 404% over five years, outperforming the S&P 500 and hovering near record highs.

Earnings are forecast to rise 39.6% in 2026. With a forward P/E of 30, Lilly isn’t cheap, but it’s more moderately valued compared to some peers.

Could healthcare leadership define the next “magnificent” cycle?

Howmet Aerospace Inc. (HWM)

Operating in aerospace and defense, Howmet has delivered one of the most remarkable runs of the group, climbing 798% over the past five years and reaching new all-time highs.

Earnings are projected to grow 18.8% in 2026. Still, its forward P/E of 56 signals a steep premium.

Can a high-growth defense supplier sustain its momentum at these levels?

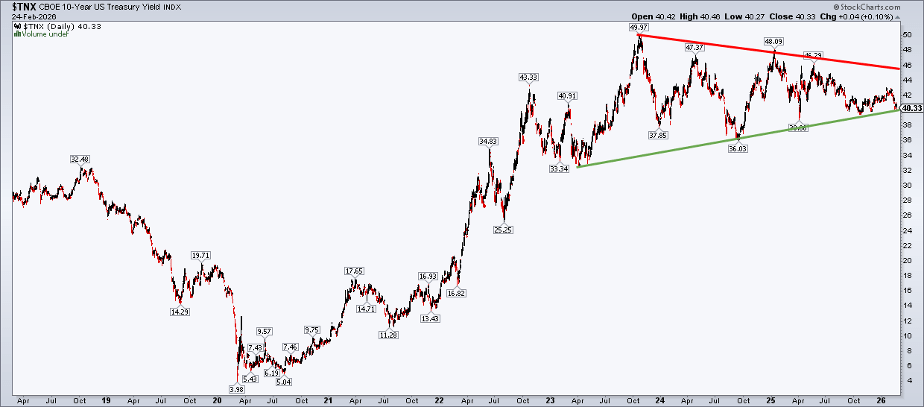

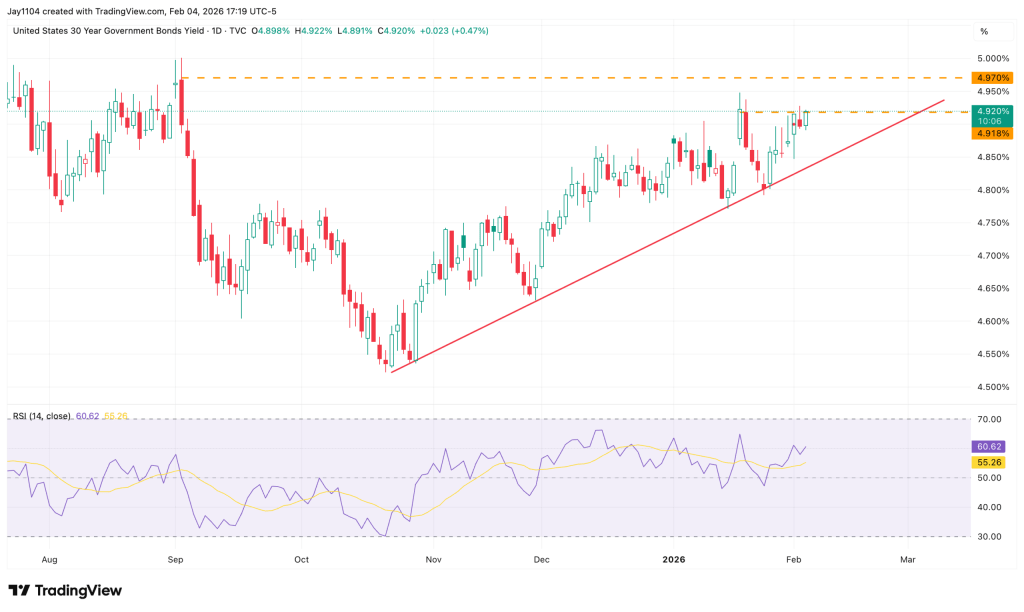

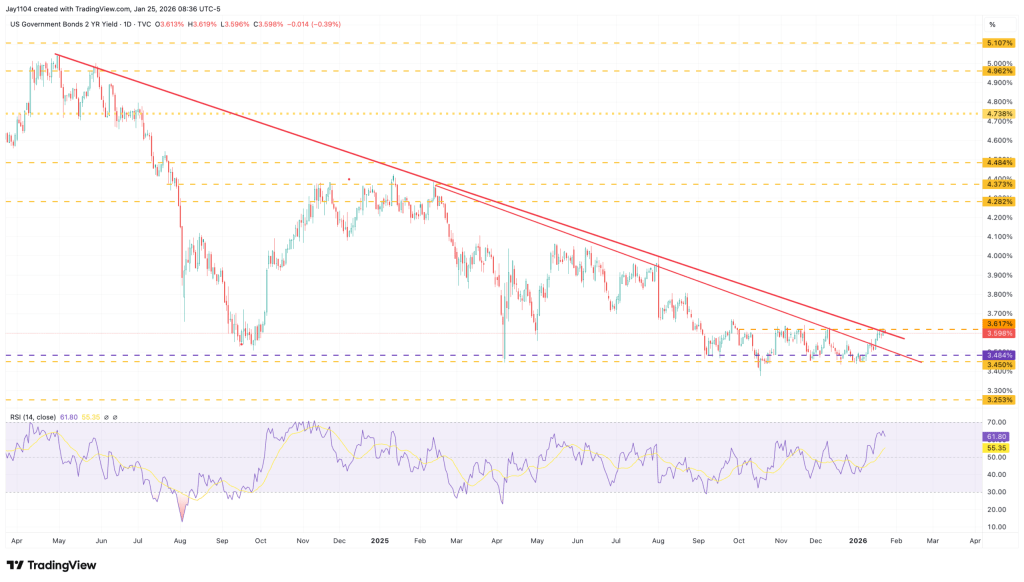

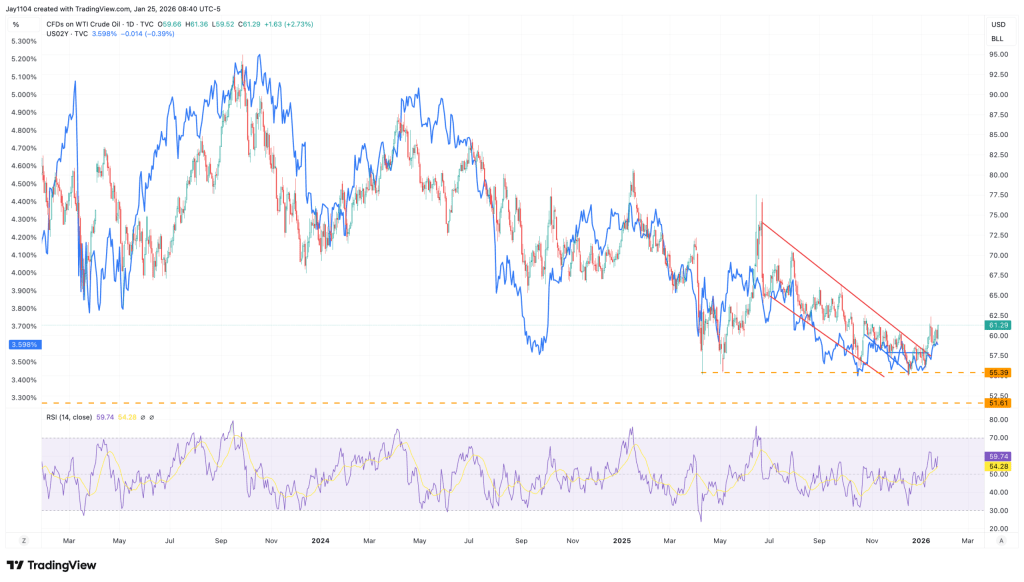

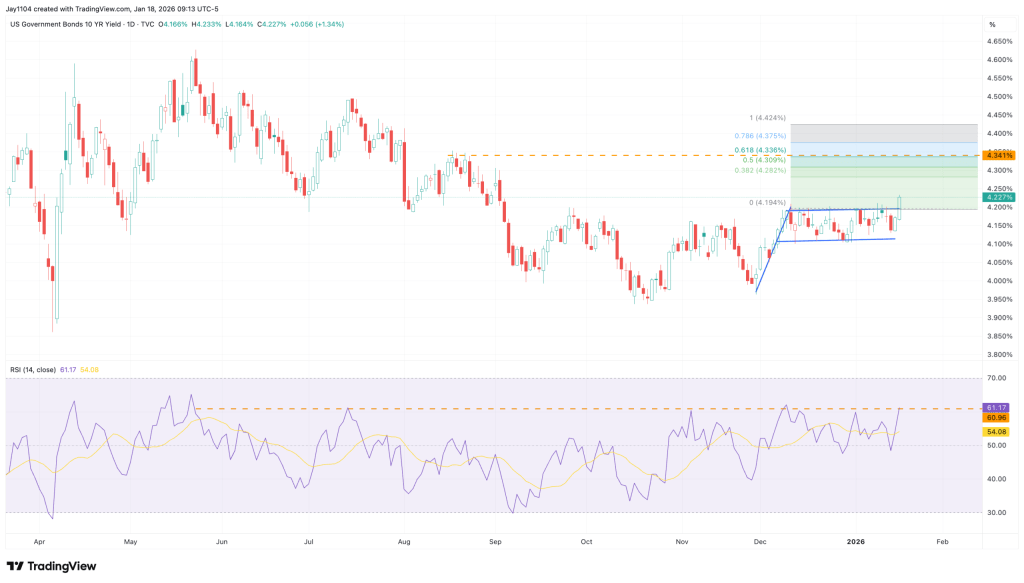

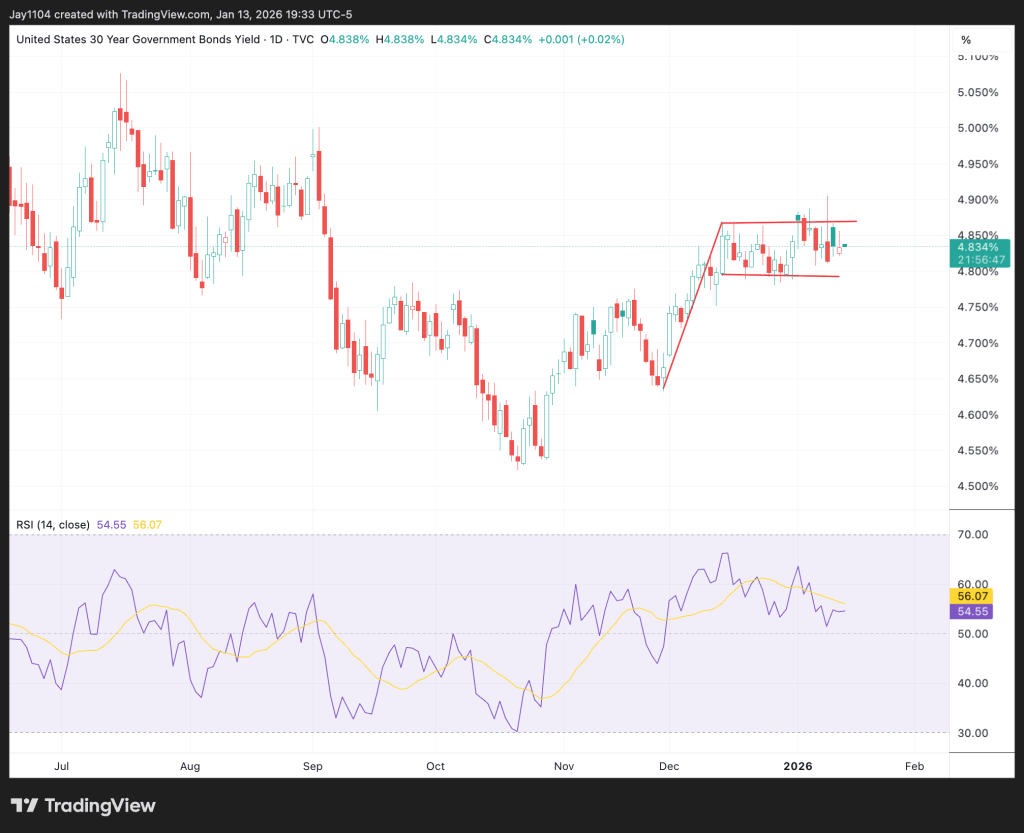

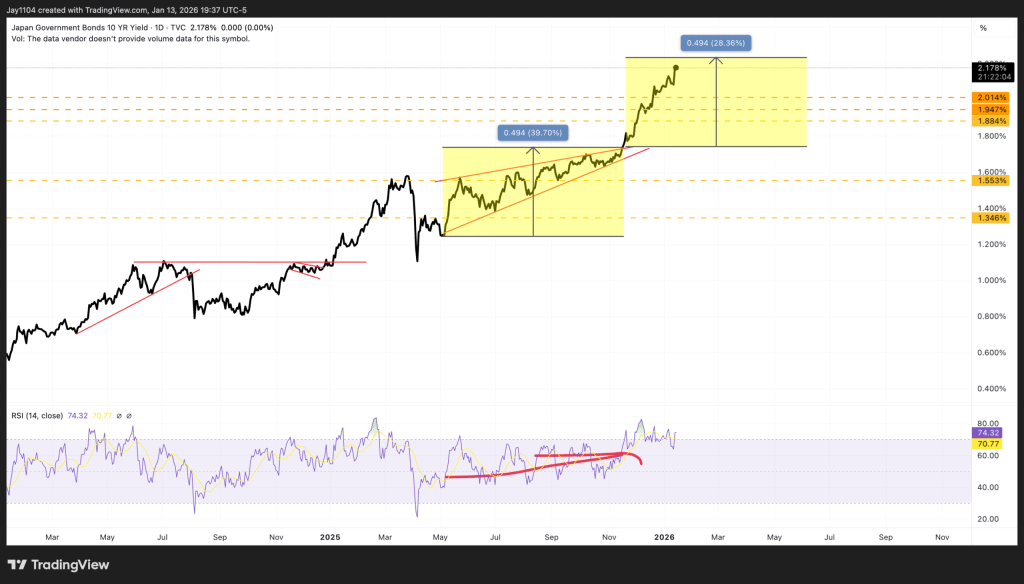

The benchmark 10-year Treasury yield is testing critical support, with downside pressure beginning to build.

Equities and bond yields are sliding in tandem — an unusual combination that may reflect deteriorating macro-risk conditions.

A strengthening US dollar alongside declining yields could point to a broader defensive rotation across markets.

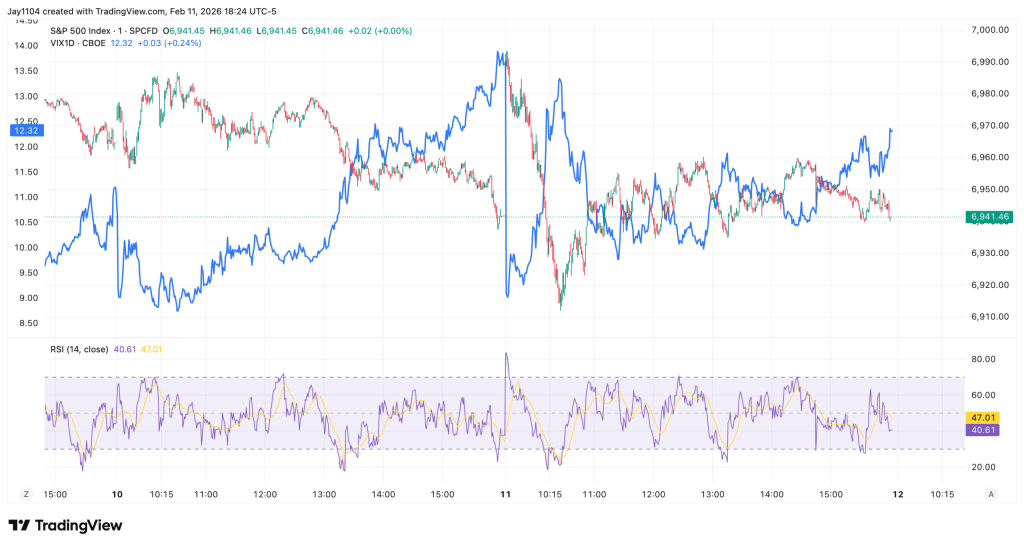

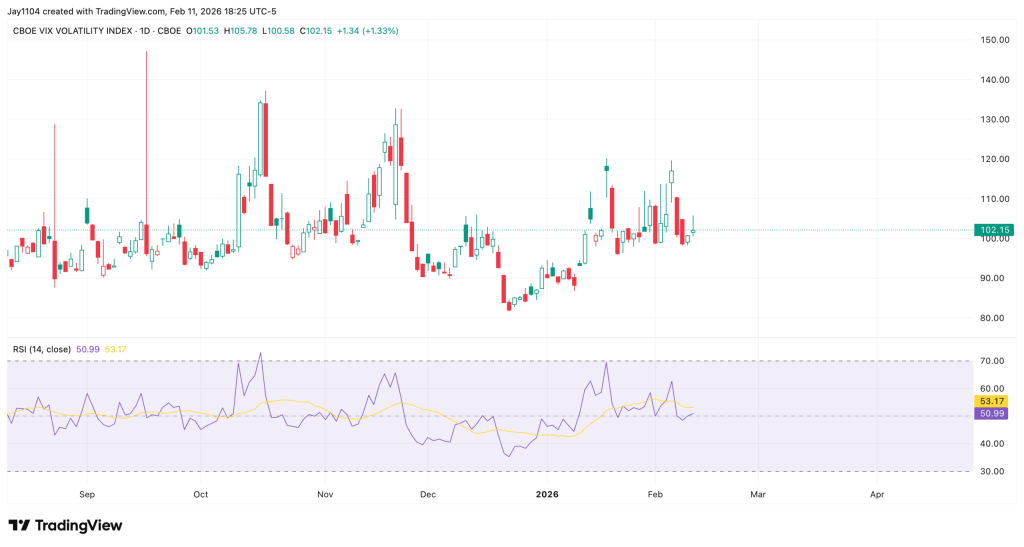

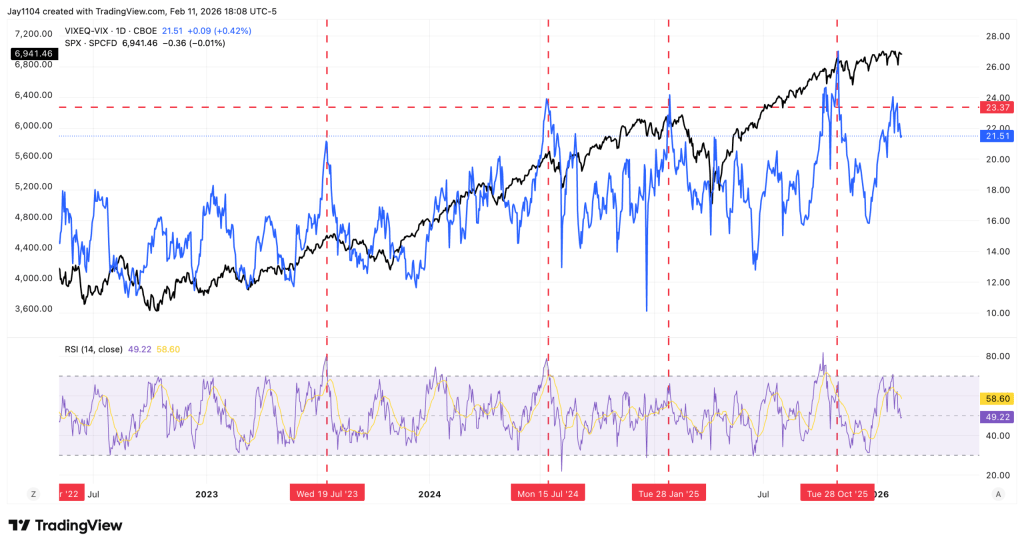

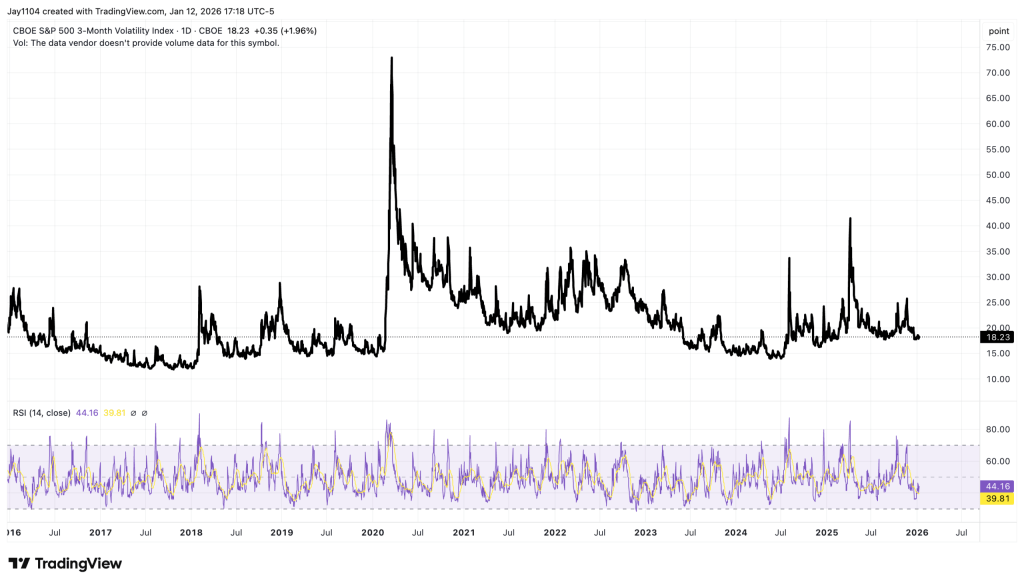

Last week, attention was drawn to the danger zone in the CBOE Volatility Index. Historically, when Wall Street’s “fear gauge” climbs into the mid-20s, equity markets have tended to experience heightened turbulence.

Now, focus shifts to the benchmark 10-year US Treasury yield. Recently, declining yields have supported the S&P 500 — particularly small- and mid-cap shares — since the so-called Liberation Day and the development of the expansive One Big Beautiful Bill Act (OBBBA). Additional fiscal stimulus or tax relief may still be forthcoming, as suggested by Donald Trump during Tuesday night’s State of the Union address.

Importantly, the surge in yields last April and May was not confined to the United States. Global bond markets reached multi-decade highs, pulling US Treasuries higher in tandem. Despite narratives around “selling America,” the primary US bond bear market unfolded between August 2020 and October 2023, when the 10-year yield climbed sharply from 0.504% to 4.997%. The past two and a half years have largely represented a consolidation phase rather than a fresh structural breakout.

The key question now: is that consolidation nearing resolution — and if so, in which direction?

10-Year Treasury Yield: A historic tightening pattern after the major bond bear market. Chart courtesy of StockCharts.com.

Treasuries Under the Spotlight

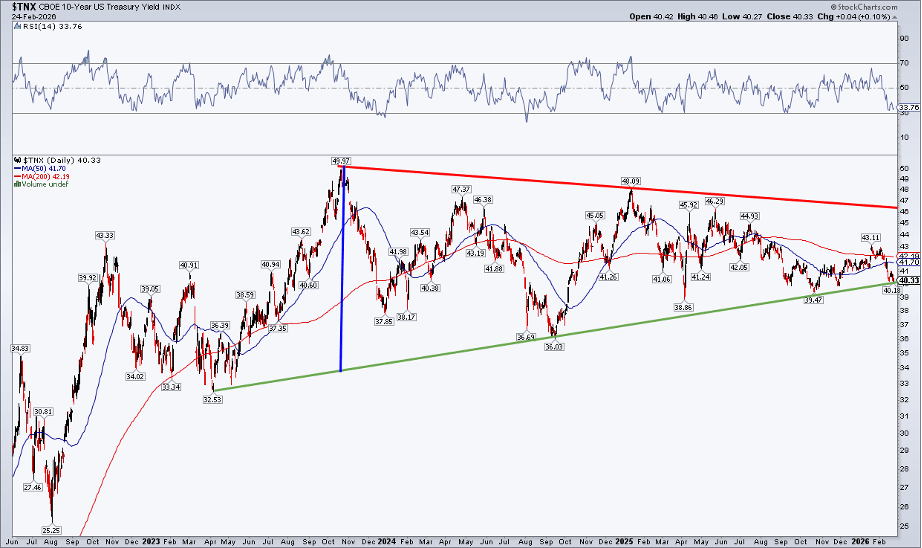

The chart below suggests that the 10-year Treasury yield could be slipping beneath a critical support level. A brief upside breakout in January quickly reversed as sellers stepped in, and now the benchmark rate is hovering near the 3% mark. It’s worth reminding traders that diagonal trendlines can be unreliable, while horizontal support and resistance levels tend to carry more weight. Additionally, log-scale charts are generally better suited for evaluating wide swings in price or yield.

With those caveats noted, what is the chart signaling? Trading below both the 50-day and 200-day moving averages, the primary trend favors Treasury price bulls (and lower yields). Meanwhile, the RSI has eased back toward the 30 level after failing to reach 70 during the fourth-quarter rate advance. The green upward-sloping support line is now pivotal — a decisive break beneath it, along with a drop below the late-2025 low of 3.947%, could push the 10-year yield down into the low 3% range.

10-Year Treasury Yield: Multi-Year Consolidation With Key Support at Risk (Log Scale). Chart courtesy of StockCharts.com.

In isolation, increasing exposure to Treasuries would be logical if yields break down and bond prices attract strong demand. But stepping back with an intermarket perspective, the bigger question becomes: what would that move signal for the broader financial markets?

A Potential Shift in the Stock–Bond Dynamic?

For stocks, a move toward 3–4% intermediate-term rates would likely coincide with softer economic conditions — perhaps a weak jobs report, sharply cooling CPI or PCE inflation, a downturn in sentiment indicators such as the ISM Manufacturing survey, or another disappointing Retail Sales release.

That said, with the fourth-quarter earnings season mostly wrapped up — including NVIDIA’s (NASDAQ: NVDA) results released Wednesday — it would probably take truly bleak off-season earnings updates or a wave of negative preannouncements to significantly rattle equities.

Another potential driver of a renewed bond bull market could be the ever-intensifying AI theme. In a “sell first, ask questions later” climate, fresh cautionary analyses or existential-impact discussions around artificial intelligence could further unsettle investors and sustain demand for safe-haven assets.

When Trading Ranges Start to Break Down

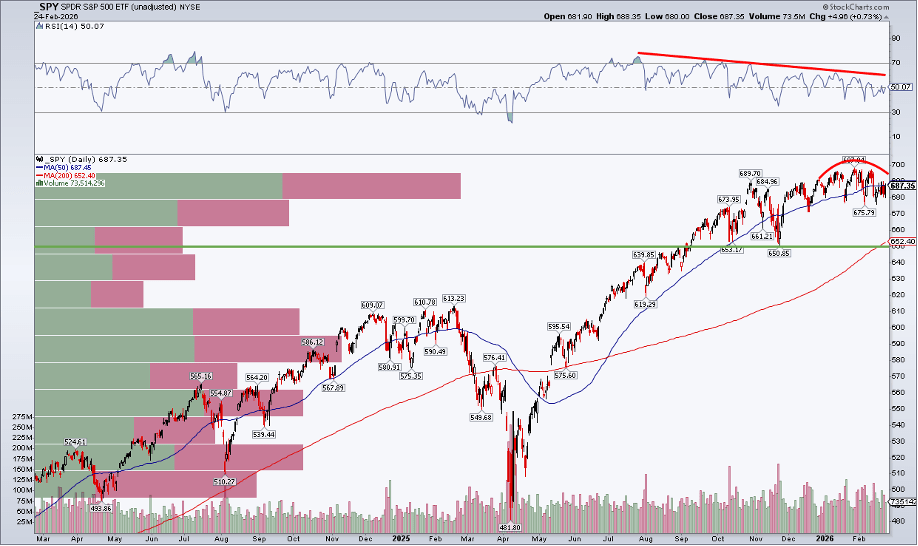

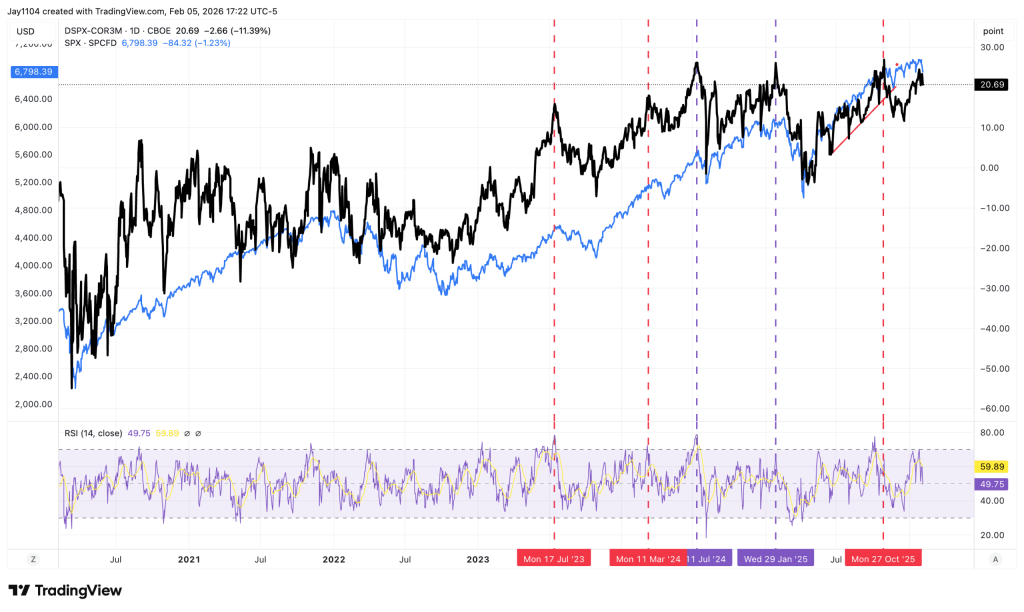

Regardless of the underlying catalyst, it’s evident that stocks and bonds are no longer moving in sync the way they did last spring and summer. The S&P 500 — like the 10-year Treasury yield — has been edging lower in recent weeks. We’re now nearly a month past the SPDR S&P 500 ETF Trust (SPY) intraday record of $697.84. Although much attention has focused on the tight trading range since late November, one could argue that a rounded-top formation is beginning to take shape.

A glance at the RSI momentum oscillator reinforces this view. Momentum has been trending lower since July. Much like a ball tossed into the air slows before changing direction, RSI often decelerates ahead of a price reversal. The unfolding narrative could be this: bond yields break down first — and equities eventually follow.

SPY: Emerging Rounded-Top Pattern, RSI Deteriorating, 200-Day Moving Average Around $650. Chart courtesy of StockCharts.com.

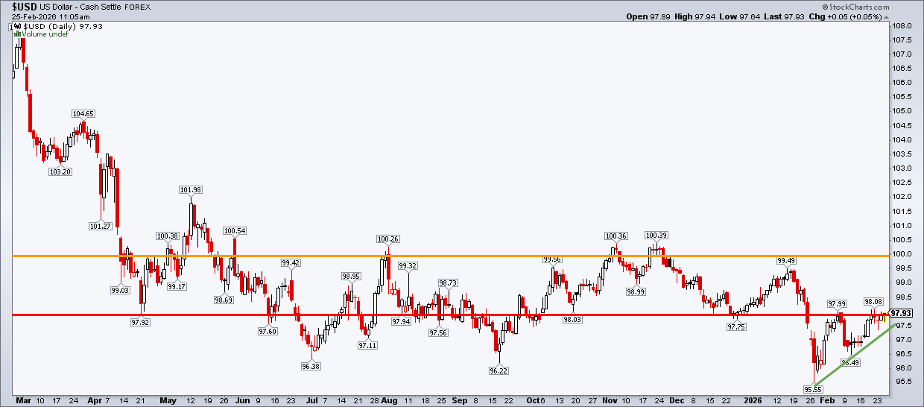

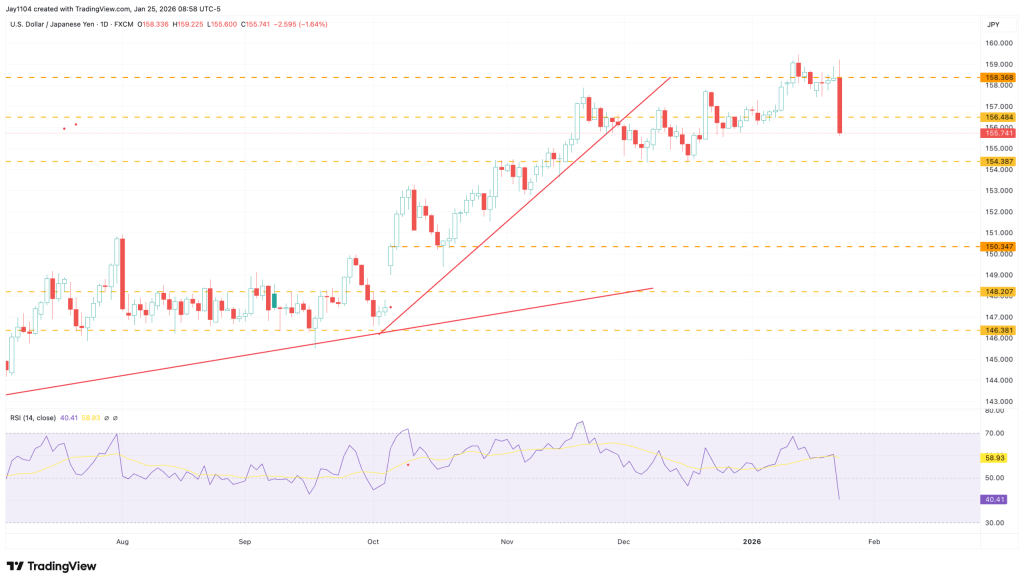

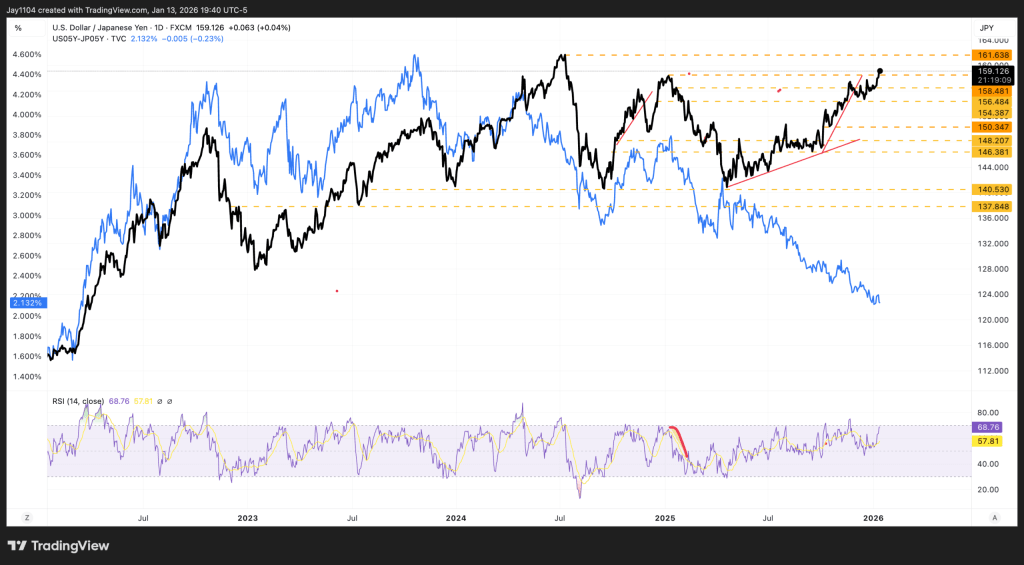

Don’t Overlook the Dollar

Largely flying under the radar is the US Dollar Index (USD). The greenback carved out a low near 95.55 around the same time U.S. large-cap equities peaked. Since then, the 98 level has surfaced as a potential breakout zone.

A setup featuring falling Treasury yields, declining stocks, and a strengthening dollar would reflect a classic risk-off macro environment. Based on a measured-move projection, the USD could target the 100 area — just shy of the zone where the dollar encountered resistance from May through November 2025.

US Dollar Index: Short-Term Ascending Triangle Pattern Points Toward 100. Chart courtesy of StockCharts.com.

The Bottom Line

Is this a doomsday forecast? Not at all. Market corrections are a normal part of the cycle. On average, the S&P 500 experiences an intra-year drawdown of about 14.2%, yet it has still finished higher in 35 of the past 46 years.

Rather than sounding alarms, this is simply a cross-asset check-in as we head into a month that has historically delivered heightened volatility. I tend to think of March as October’s little brother — price swings can become exaggerated. And with the CBOE Volatility Index still hovering around 20, disciplined risk management deserves to remain front and center.

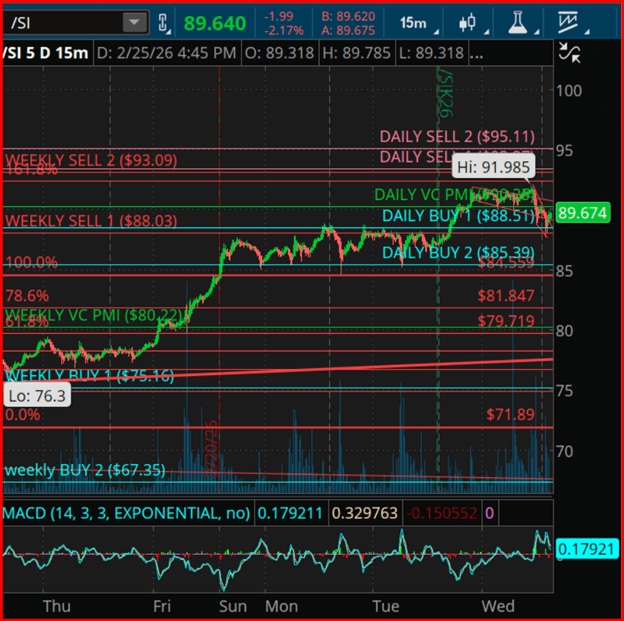

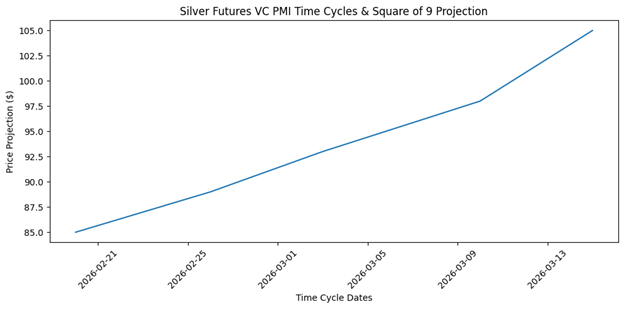

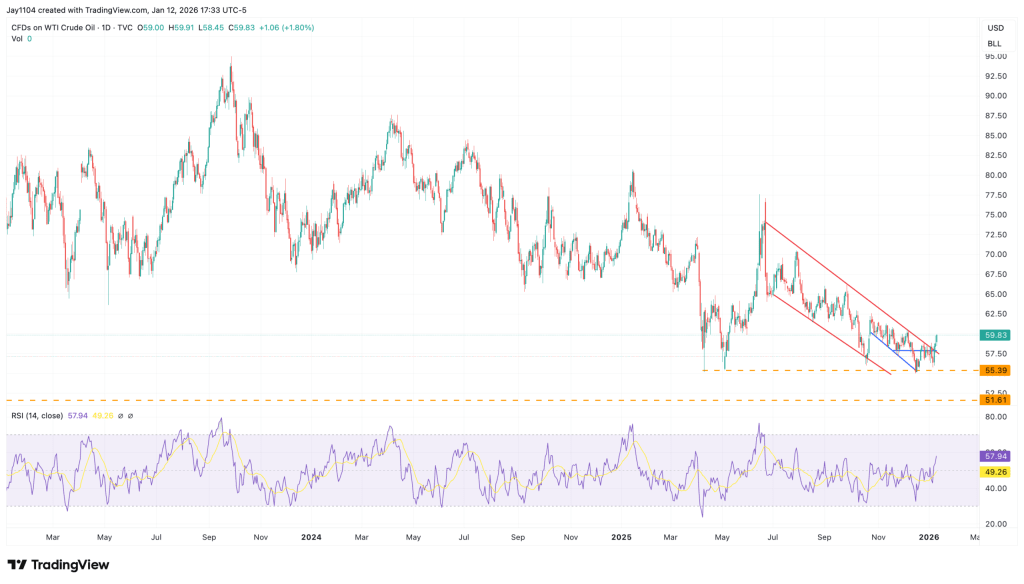

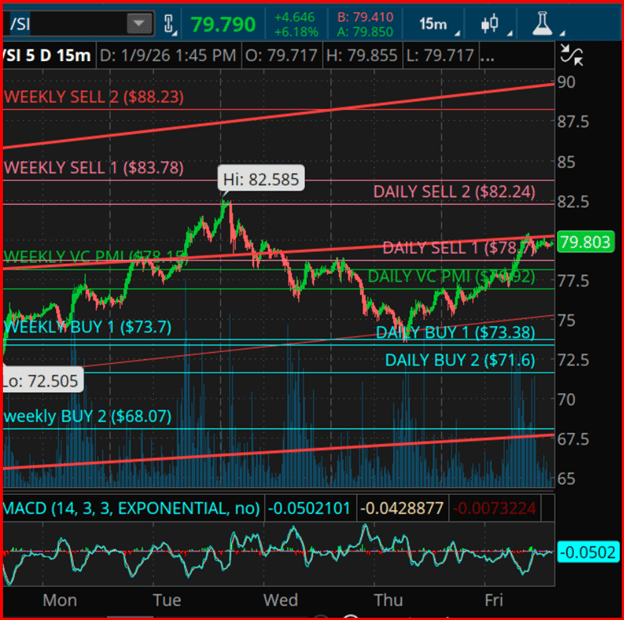

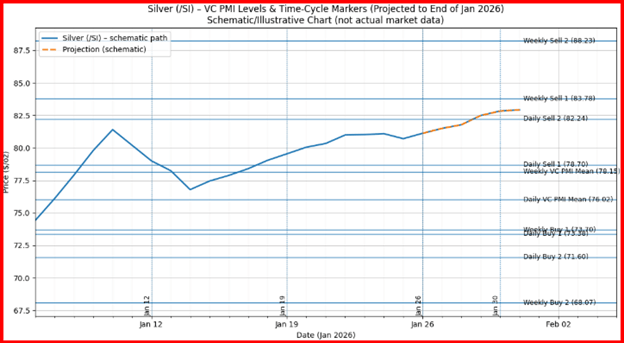

The February 26–March 3 cycle represents a projected volatility expansion window. If price maintains support above the weekly mean and regains upside momentum, the next bullish targets come in at $98, $105, and potentially $120. However, a breakdown below the $85.39 daily Buy-2 level would postpone the expansion phase and shift the market back into a deeper accumulation range between $81.85 and $79.71.

Silver futures are currently trading within a structured VC PMI mean-reversion model, signalling a transition from distribution into a fresh decision phase as price oscillates around both the daily and weekly averages. Within the VC PMI framework, the mean represents equilibrium — the point where supply and demand balance. Moves toward Buy-1/Buy-2 or Sell-1/Sell-2 define statistically extreme zones, carrying a 90%–95% probability of reverting back toward the mean.

Around the $89 area, silver has pulled back from upper resistance and is now rotating toward the daily mean in the $89–$90 zone. The weekly Sell-1 level at $88.03 and Sell-2 at $93.09 frame the upper distribution band. A decisive close above $93.09 would confirm a bullish breakout into the next fractal structure, flipping resistance into support and opening harmonic upside projections toward $98–$105 based on Square of 9 geometric expansion.

On the downside, failure to sustain trade above the weekly mean near $80.22 would keep silver locked in a broader consolidation pattern. In that scenario, Buy-1 at $75.16 and Buy-2 at $67.35 define longer-term accumulation levels.

Time-cycle analysis highlights February 26 to March 3 as a pivotal rotational window — a period when corrective phases often conclude and directional momentum emerges. This timing aligns with the current consolidation around the mean, increasing the probability of volatility expansion into early March. A secondary cycle window between March 8 and 12 historically signals either continuation or reversal, depending on whether price holds above or below the mean established during the initial cycle.

These cyclical harmonics are derived from recurring liquidity patterns and repetitive market behavior rather than macro fundamentals, underscoring the quantitative foundation of the VC PMI framework.

Square of 9 geometry reinforces the current technical framework, highlighting harmonic resistance around $93 and $100 as key angular levels projected from prior lows and rotational pivot points. On the downside, support harmonics cluster near $85, $81.85, and $79.71, creating a geometric staircase of demand zones where the probability of institutional accumulation increases. When time and price harmonics converge, markets tend to generate accelerated directional moves — particularly if price pushes above the Sell-2 extreme or breaks below the Buy-2 threshold.

By integrating VC PMI, cyclical timing analysis, and Square of 9 geometry, this methodology offers a structured, rules-based trading approach. The emphasis remains on statistical probability, market structure, and disciplined execution rather than emotional decision-making.

Square of 9 geometry reinforces the current technical framework, highlighting harmonic resistance around $93 and $100 as key angular levels projected from prior lows and rotational pivot points. On the downside, support harmonics cluster near $85, $81.85, and $79.71, creating a geometric staircase of demand zones where the probability of institutional accumulation increases. When time and price harmonics converge, markets tend to generate accelerated directional moves — particularly if price pushes above the Sell-2 extreme or breaks below the Buy-2 threshold.

By integrating VC PMI, cyclical timing analysis, and Square of 9 geometry, this methodology offers a structured, rules-based trading approach. The emphasis remains on statistical probability, market structure, and disciplined execution rather than emotional decision-making.

Futures tied to the main U.S. stock benchmarks edged lower as investors focused on key earnings from the technology sector. Nvidia, a heavyweight in the U.S. equity market, delivered stronger-than-expected results, though investors are seeking clearer guidance on when its substantial cash flow will translate into greater shareholder returns. Salesforce shares declined after issuing a softer revenue outlook. Meanwhile, oil prices held steady ahead of crucial nuclear negotiations between U.S. and Iranian officials.

Futures Edge Lower

U.S. equity futures moved down Thursday as markets digested earnings from AI leader Nvidia.

As of 03:05 ET (08:05 GMT), Dow futures were down 122 points, or 0.3%, S&P 500 futures slipped 0.1%, and Nasdaq 100 futures also fell 0.1%. This followed gains across all major Wall Street indices in the previous session, when investors positioned ahead of Nvidia’s earnings release.

Sentiment had improved on renewed optimism surrounding artificial intelligence, marking another shift in what has been a volatile narrative around the emerging technology. The Nasdaq led prior gains as investors regained confidence that AI could eventually deliver broad economic benefits — contrasting with earlier concerns that new AI models might disrupt software firms and limit returns on heavy data center spending.

Remarks from Richmond Fed President Tom Barkin also supported equities, as he noted uncertainty over whether automation would significantly raise unemployment and suggested AI could instead improve labor market efficiency.

Nvidia Little Changed Despite Strong Results

Nvidia reported better-than-expected earnings for the January quarter and issued revenue guidance above forecasts for the current period, yet its shares were mostly flat in after-hours trading.

Some investors questioned whether the chipmaker is returning sufficient capital to shareholders. Yvette Schmitter, CEO of Fusion Collective, pointed out that while Nvidia generated $35 billion in cash during the fourth quarter, it returned just 12% to shareholders — sharply lower than 52% a year earlier.

She also raised concerns about reduced buybacks despite record cash generation, especially as Nvidia highlights strong demand for its sold-out Ampere chips.

These concerns echoed questions raised during the company’s earnings call, including from a UBS analyst who asked whether Nvidia plans to distribute more of the anticipated $100 billion in cash expected this year. CFO Colette Kress emphasized ongoing investment in the broader AI ecosystem, while CEO Jensen Huang underscored AI’s foundational role in the future of computing.

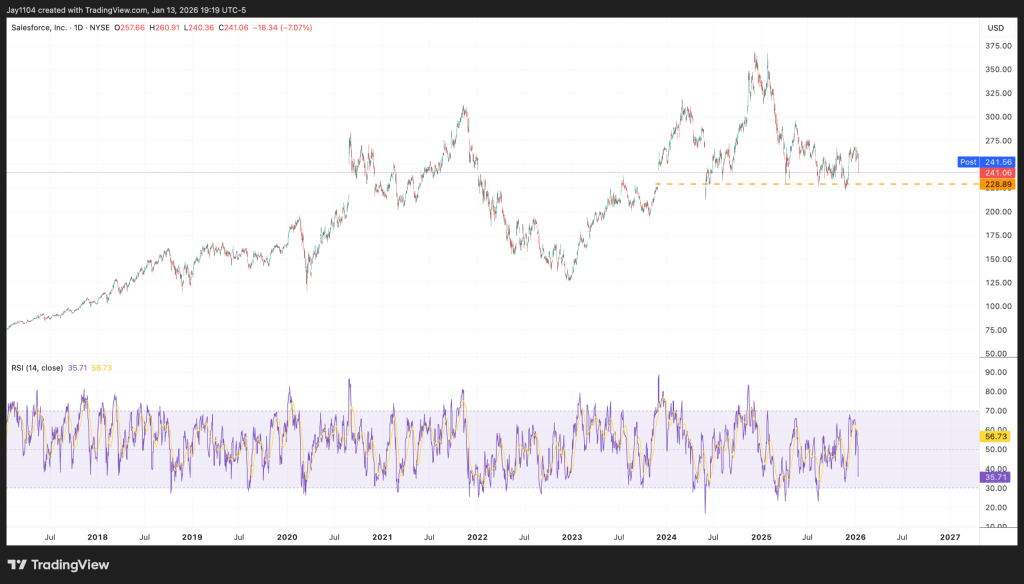

Salesforce Drops on Soft Revenue Outlook

Salesforce shares fell in extended trading after the company issued fiscal 2027 revenue guidance below Wall Street expectations, suggesting softer demand for enterprise software amid economic uncertainty and tighter corporate budgets.

The company projected full-year revenue between $45.80 billion and $46.20 billion, slightly below consensus estimates at the midpoint.

Salesforce continues to invest heavily in artificial intelligence to counter investor concerns that emerging AI models, such as those developed by startups like Anthropic, could erode demand. These pressures have contributed to stock volatility as the company works to defend its position within the software-as-a-service industry.

However, Salesforce raised its fiscal 2030 revenue forecast to $63 billion from $60 billion, citing expected growth from agentic AI offerings. Analysts at Vital Knowledge described the report as not flawless but “good enough,” highlighting strong AI product momentum, stable core performance, and solid cash flow generation.

Oil Steady Before U.S.- Iran Talks

Oil prices were largely unchanged Thursday, remaining near seven-month highs as markets prepared for a third round of nuclear discussions between Washington and Tehran.

Brent crude gained 0.2% to $70.84 per barrel, while U.S. West Texas Intermediate rose 0.2% to $65.62 per barrel.

U.S. representatives, including special envoy Steve Witkoff and adviser Jared Kushner, are scheduled to meet Iranian officials in Geneva as negotiations continue over Iran’s nuclear program. President Donald Trump has warned that failure to make meaningful progress could lead to serious consequences, raising concerns that prolonged tensions may disrupt supply from Iran, a key OPEC producer.

Gold Edges Higher

Gold prices ticked up as uncertainty surrounding U.S. trade tariffs bolstered safe-haven demand, with investors also monitoring developments in the U.S.-Iran nuclear talks.

Spot gold rose 0.6% to $5,196.55 per ounce, while U.S. gold futures dipped 0.5% to $5,200.54 per ounce.

Markets are also evaluating the implications of newly announced U.S. tariffs following a Supreme Court ruling that struck down President Trump’s sweeping reciprocal tariff measures. Attention now turns to upcoming U.S. economic data, including weekly jobless claims. So far this year, gold has remained supported by geopolitical tensions, central bank buying, and portfolio diversification trends.

U.S. stock index futures edged higher on Monday night after growing uncertainty surrounding Donald Trump’s tariff policies and concerns about AI-related disruption in the software sector triggered steep losses on Wall Street.

Lingering unease over a potential U.S.-Iran conflict, along with caution ahead of this week’s closely watched earnings from NVIDIA Corporation (NASDAQ: NVDA), also kept sentiment restrained.

As of 19:30 ET (00:30 GMT), S&P 500 Futures were up less than 0.1% at 6,855.0 points. Nasdaq 100 Futures gained 0.1% to 24,781.0 points, while Dow Jones Futures added nearly 0.1% to 48,873.0 points.

FedEx sues U.S. government to recover tariff payments

FedEx Corporation (NYSE: FDX) filed a lawsuit against the U.S. government on Monday evening, seeking a “full refund” of emergency tariffs it paid over the past year.

The action comes only days after the Supreme Court of the United States ruled the levies illegal, with the tariffs scheduled to be lifted from midnight Tuesday.

FedEx is the first company to formally pursue reimbursement following the Court’s decision, joining a broader wave of firms mounting legal challenges against tariff measures introduced under Donald Trump.

However, the ruling did not clarify how the more than $160 billion in revenue already collected from the invalidated tariffs will be handled.

Wall Street battered by tariff uncertainty and AI concerns

Wall Street’s major indexes each dropped more than 1% on Monday as uncertainty surrounding Donald Trump’s tariff policies and mounting concerns about artificial intelligence disrupting the software industry kept investors in a risk-off mood.

Technology sentiment remained fragile ahead of quarterly results from NVIDIA Corporation (NASDAQ: NVDA), scheduled for Wednesday. Widely viewed as a key gauge of AI demand, the world’s most valuable company is expected to post robust earnings growth compared with last year.

Markets also grappled with renewed tariff worries after Trump unveiled a 15% universal tariff under a different legal authority. A report from The Wall Street Journal indicated the administration is considering additional levies on at least six more sectors.

The president appeared to double down on his trade agenda, even as several countries that recently reached agreements with Washington sought greater clarity on the scope and implementation of the tariffs. He also cautioned that nations retreating from newly negotiated trade deals could face steeper duties.

The S&P 500 declined 1%, while the NASDAQ Composite fell 1.1%. The Dow Jones Industrial Average led losses, tumbling 1.7%.

Technology stocks continued to lag, with software names hit by renewed selling pressure amid rising anxiety over AI-driven disruption. Part of the concern stemmed from a speculative note by Citrini Research envisioning a June 2028 scenario in which rapid AI adoption leads to widespread displacement of white-collar jobs.

U.S. PPI inflation data and Nvidia’s earnings will take center stage in the coming week.

Nvidia appears set to post another standout quarter.

Meanwhile, Intuit is confronting mounting fundamental and technical pressures ahead of its results.

U.S. equities closed higher on Friday after the Supreme Court invalidated President Donald Trump’s tariffs. Trump criticized the decision as a “disgrace” and said in a Truth Social post on Saturday that he would introduce a new 15% global tariff, just one day after announcing a 10% levy.

After Friday’s gains, the 30-stock Dow Jones Industrial Average finished the week up about 0.3%. The S&P 500 advanced 1.1%, while the tech-heavy Nasdaq Composite broke a five-week slide with a 1.5% surge. The small-cap Russell 2000 added nearly 0.7%.

Markets may see heightened swings in the days ahead as investors weigh prospects for growth, inflation, interest rates, and corporate earnings against a backdrop of renewed trade frictions.

With a relatively light economic calendar, attention will center on Friday’s January U.S. producer price index report. As of Sunday morning, traders are pricing in slightly better than even odds that the Federal Reserve will lower rates by its June meeting.

On the earnings front, Nvidia’s (NASDAQ: NVDA) report will headline the week as the season winds down. Beyond Nvidia, investors will be tracking several major tech names, particularly software companies facing pressure from concerns that AI could disrupt their core businesses, including Salesforce (NYSE: CRM), Intuit (NASDAQ: INTU), Snowflake (NYSE: SNOW), Zscaler (NASDAQ: ZS), and Zoom Video Communications (NASDAQ: ZM).

AI infrastructure providers Dell Technologies (NYSE: DELL) and CoreWeave (NASDAQ: CRWV) are also set to post results. Outside the tech space, prominent retailers such as Home Depot (NYSE: HD), Lowe’s Companies (NYSE: LOW), and TJX Companies (NYSE: TJX) are scheduled to report.

At the same time, markets will be parsing President Trump’s State of the Union address on Tuesday and monitoring any developments involving the U.S. and Iran.

No matter which way markets move, below I outline one stock that could attract buying interest and another that may face renewed downside pressure. Keep in mind, this outlook covers only the week ahead—Monday, February 23 through Friday, February 27.

Stock to Buy: Nvidia

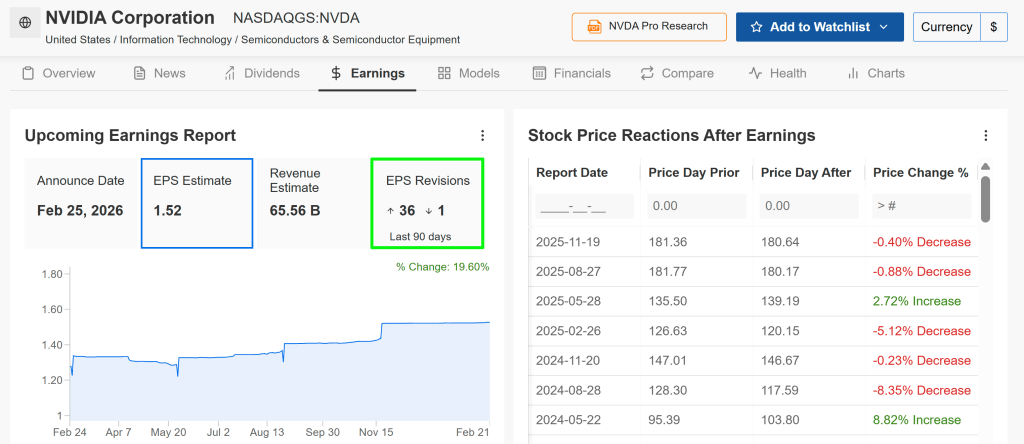

Nvidia heads into its earnings report with analysts anticipating another “beat-and-raise” performance, fueled by robust demand for AI infrastructure. Fourth-quarter results are scheduled for release after Wednesday’s market close at 4:20 p.m. ET, followed by a 5:00 p.m. ET conference call with CEO Jensen Huang.

According to an InvestingPro survey, profit forecasts have been lifted 36 times in recent weeks, compared with just one downward revision—highlighting growing optimism around Nvidia’s earnings outlook. In the options market, traders are pricing in a potential move of roughly ±6% in NVDA shares following the announcement.

Wall Street expects the AI powerhouse to deliver earnings of $1.52 per share, up 71% from a year earlier. Revenue is forecast to climb 67% to $65.6 billion, underscoring the company’s ongoing strength in the AI chip space.

Citi recently suggested that January-quarter revenue could exceed $67 billion, with projections pointing to even stronger results in the April quarter.

Another solid showing in data-center sales, along with widening margins and healthy free cash flow, would bolster the view that Nvidia remains firmly in the midst—not at the tail end—of an AI supercycle.

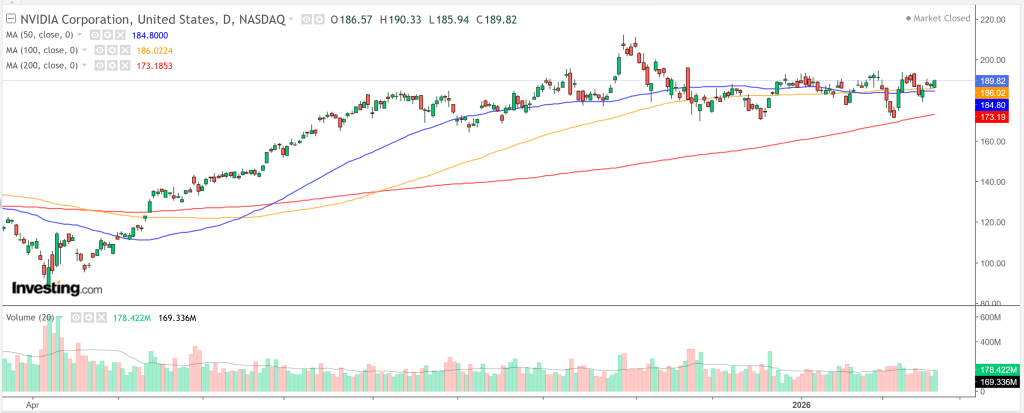

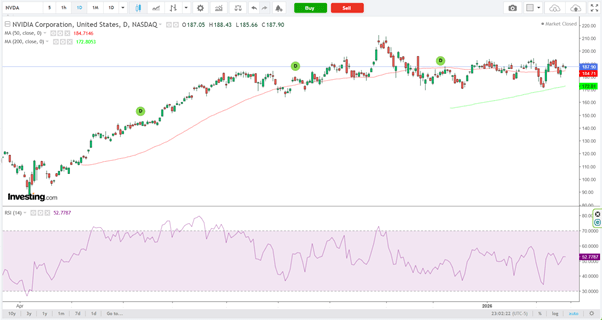

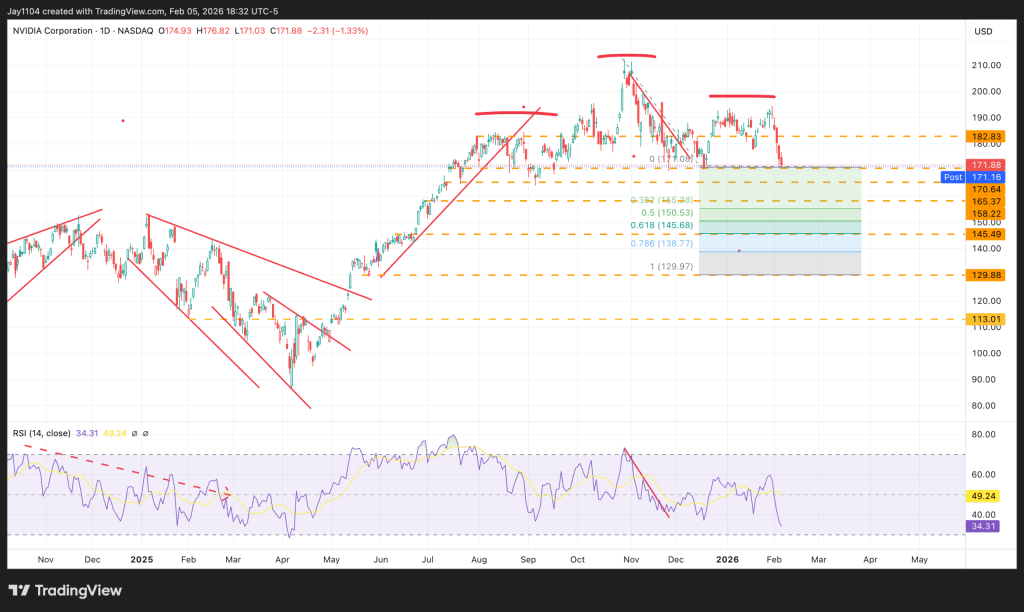

NVDA shares ended Friday at $189.82, consolidating after a strong advance but still positioned to move higher on favorable catalysts. Across multiple timeframes—from intraday charts to the monthly view—technical indicators and moving averages continue to signal a “strong buy.”

A beat-and-raise report could ignite another leg up, particularly if management emphasizes longer-term visibility into 2026–2027 growth driven by next-generation architectures such as Rubin.

Trade Setup:

Entry: Near current levels (around $190)

Target: $210 (approximately 10% upside)

Stop-Loss: $184 (roughly 3.5% downside risk)

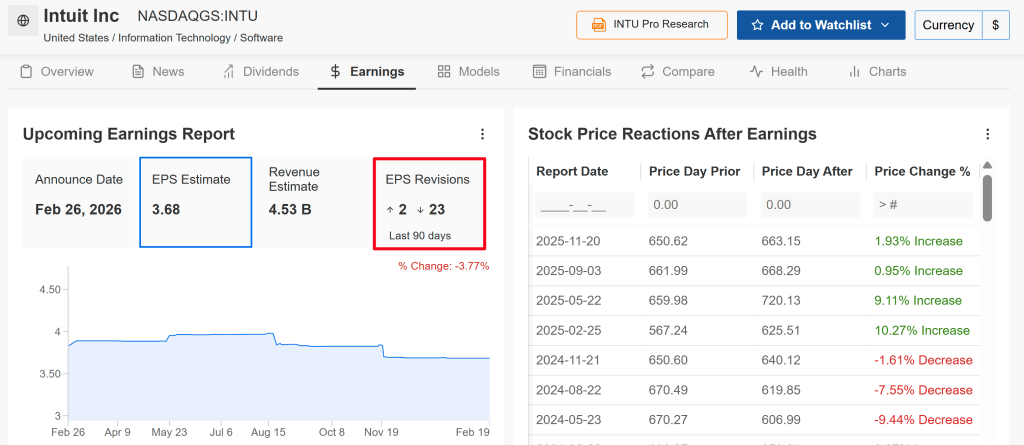

Stock to Sell: Intuit

Intuit—the parent company of TurboTax, QuickBooks, Credit Karma, and Mailchimp—heads into earnings week facing mounting pressure. Concerns have escalated in early 2026 that generative AI tools could weaken its competitive moat across tax prep, accounting, and financial software by enabling free or lower-cost alternatives, custom AI agents, or in-house solutions for small businesses and consumers.

This anxiety has fueled broader “SaaSpocalypse” sentiment, with the software sector shedding trillions in market value. INTU shares have been particularly hard hit in recent months, sliding sharply alongside peers such as Salesforce.

Analyst sentiment has also turned more cautious ahead of the report, with 23 of the last 25 estimate revisions moving lower—signaling growing skepticism around near-term performance.

Wall Street expects Intuit to post earnings of $3.68 per share, up roughly 11% year over year, on revenue of about $4.5 billion. The bigger concern, however, centers less on the headline numbers and more on the narrative surrounding AI-driven disruption.

Although Intuit has made significant investments in artificial intelligence, investors seem to view these efforts as largely defensive—designed to protect its existing franchises rather than meaningfully expand them or counter broader competitive threats. TD Cowen recently cut its price target, pointing to doubts about the strength of Intuit’s AI strategy and intensifying competition.

Any remarks about rising competitive pressures, decelerating growth in key segments, or conservative forward guidance could amplify downside risks—particularly in a stock that may be technically oversold but remains vulnerable in a sentiment-driven market.

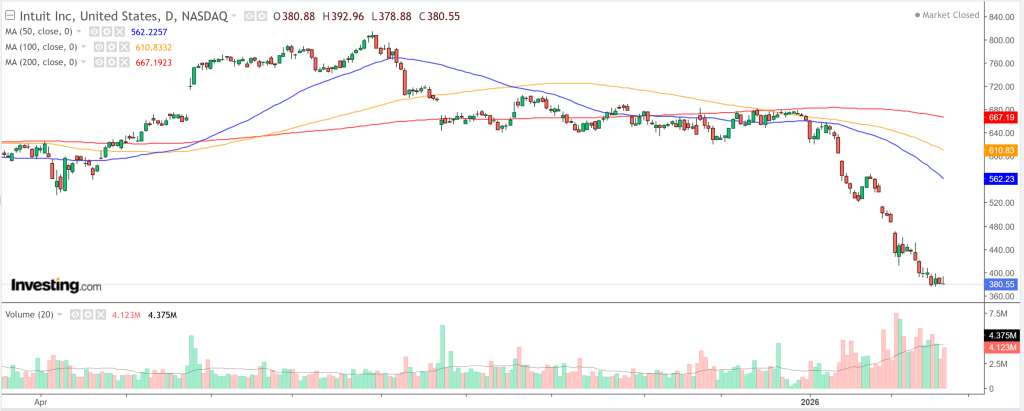

Shares of Intuit have fallen 42.5% over the past three months and are now hovering just above their 52-week low of $375.40. Technical signals remain decisively negative: across timeframes—from hourly charts to the monthly view—both moving averages and momentum indicators continue to flash “strong sell.”

With management’s outlook likely to face intense scrutiny, any earnings miss or cautious commentary reflecting a more competitive, AI-driven environment could deepen the selloff.

The artificial intelligence trade faces its biggest test of the year this week as three cornerstone companies in the AI infrastructure ecosystem prepare to deliver quarterly earnings. With tech stocks showing signs of fatigue, investors want more than simple earnings beats. They’re looking for proof that heavy capital expenditure is translating into the successful deployment of next-generation hardware. All attention will turn to the after-market close (AMC) on Wednesday and Thursday to see whether the AI rally still has momentum.

NVIDIA: The undisputed AI infrastructure leader

NVIDIA (NVDA) is set to report fiscal Q4 2026 results on Wednesday, Feb. 25, after market close. As the dominant supplier of GPUs powering large language models, NVIDIA remains the clearest gauge of the AI trade’s health. Wall Street is anticipating a “beat and raise,” with consensus revenue estimates around $65.6 billion — an impressive 67% year-over-year increase.

Investors are especially focused on the production ramp of its Blackwell architecture chips. Any updates on supply chain constraints or the development timeline for the upcoming Rubin platform could influence not only tech stocks but the broader S&P 500. Options markets imply a potential 6.5% swing in either direction, making NVIDIA’s earnings the week’s must-watch event for global investors.

Hardware and cloud players: CoreWeave and Dell under the spotlight

On Thursday, Feb. 26, AMC, attention shifts to the physical backbone of AI infrastructure. CoreWeave (CRWV), a specialized cloud provider and key NVIDIA partner, will report against high expectations driven by its sizable revenue backlog. Analysts project Q4 revenue of roughly $1.53 billion, but the more significant figure is its $56 billion backlog — a forward-looking signal of how much computing capacity AI firms and tech giants are securing

Also reporting Thursday is Dell Technologies (DELL), which has repositioned itself as a major supplier of AI-optimized servers. Consensus forecasts call for earnings of $3.53 per share on $31.6 billion in revenue. Dell recently earned a spot on Evercore’s “Tactical Outperform” list, supported by a sharp rise in AI server orders and an $18.4 billion backlog exiting last quarter. The key question for Dell will be whether it can preserve margins while rapidly scaling production to meet surging demand for AI infrastructure.

After a powerful rally in large-cap technology shares, investors are once again asking whether smart money is beginning to rotate.

With AI enthusiasm pushing tech valuations higher and energy names still trading at comparatively modest multiples, there are early signs that capital flows may be shifting beneath the surface. Here’s a closer look at the current landscape — and where institutional positioning may be headed.

The Case for Tech: Structural Growth Still Intact

Companies such as Nvidia (NASDAQ: NVDA), Microsoft (NASDAQ: MSFT), and Apple (NASDAQ: AAPL) remain central pillars of institutional portfolios.

Technology continues to lead in earnings expansion, fueled by AI infrastructure investment, cloud migration, and ongoing software monetization.

Why capital is still favoring tech:

Revenue growth outpacing the broader market

High operating margins and robust free cash flow

Sustained AI-driven capex cycles

Strong balance sheets with significant liquidity

Mega-cap tech remains a structural core holding for institutional investors. Even during brief pullbacks, dip-buying has been persistent — a sign that long-term conviction in the sector remains strong.

That said, valuations in select segments have stretched beyond historical norms. If earnings momentum moderates, the probability of sector rotation increases, particularly as investors reassess risk-reward at elevated multiples.

The Case for Energy: Undervalued and Cash-Generative

Integrated majors such as Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) are drawing renewed attention as investors reassess sector allocations.

Energy equities typically trade in cycles influenced by crude prices, global demand dynamics, and geopolitical developments. After extended periods of relative underperformance, the sector often becomes a magnet for value-oriented capital.

Why institutional money may rotate toward energy:

Lower forward P/E multiples compared to technology

Strong and visible free cash flow generation

Dividend yields frequently above the broader market average

Ongoing share repurchase programs

If crude prices remain stable or trend higher, integrated oil majors can produce substantial cash flows, offering a mix of income, capital return, and relative defensiveness.

In an environment where parts of the technology sector appear valuation-stretched, energy provides a compelling contrast on both multiples and yield.

Sector ETF Signals: Tracking Institutional Flows

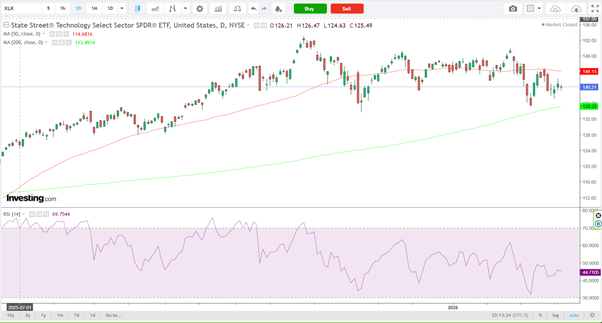

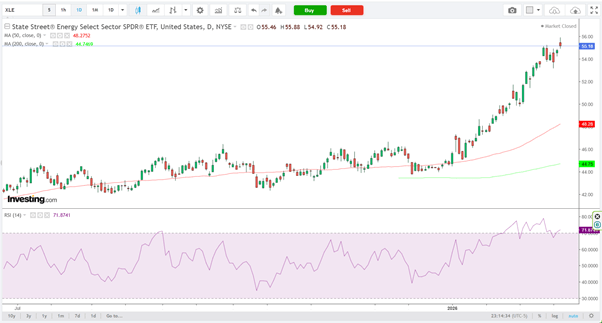

Sector ETFs can offer valuable insight into how institutional capital is rotating beneath the surface. Two key vehicles to monitor are the Technology Select Sector SPDR Fund (NYSE: XLK) and the Energy Select Sector SPDR Fund (NYSE: XLE).

ETF performance and fund flow data often act as real-time indicators of positioning shifts:

If XLK continues to outperform, it suggests growth leadership remains firmly in place.

If XLE begins to show sustained relative strength versus XLK, it may signal that rotation into energy is gaining traction.

Historically, sector leadership transitions tend to coincide with:

Shifts in interest rate expectations

Narrowing earnings growth differentials

Sharp moves in commodity prices

Monitoring the relative strength ratio between XLE and XLK can provide early confirmation of whether capital is merely rebalancing tactically — or whether a broader structural rotation is unfolding.

Macro Forces Driving Sector Rotation

1. Interest Rates Elevated yields tend to weigh more heavily on high-multiple technology stocks, as future cash flows are discounted at higher rates. In contrast, energy companies—often valued on nearer-term cash generation—can prove more resilient. If bond yields move higher, defensive value sectors may attract incremental capital at the expense of growth.

2. Commodity Prices Oil prices remain a primary earnings driver for energy producers. A sustained rally in crude can rapidly alter sector performance dynamics, drawing capital into integrated majors and upstream names as profit expectations improve.

3. Earnings Revisions Institutional allocation models closely track forward earnings revisions. If analyst upgrades begin to slow in technology while turning more constructive for energy, portfolio rebalancing flows may follow.

4. Risk Appetite Technology typically outperforms in strong risk-on environments characterized by abundant liquidity and growth optimism. Energy, by contrast, can gain relative strength during inflationary phases or periods of geopolitical tension, when commodity exposure and cash yield become more attractive.

What Institutional Capital Is Likely Doing Now

Rather than making an outright “either/or” shift, institutional investors typically adjust exposure more subtly. That can mean trimming extended technology positions, selectively adding energy holdings, or rotating within sectors—such as moving from mega-cap AI leaders into second-tier beneficiaries of the theme.

The real driver is relative earnings momentum, not headlines.

Which Sector Offers More Upside?

Tech Upside Scenario

Continued acceleration in AI-related spending

Consistent earnings beats from mega-cap leaders

Declining bond yields that support higher valuation multiples

Energy Upside Scenario

Oil prices establish a sustained uptrend

Inflation concerns re-emerge

Technology valuations compress

In the near term, technology remains the structural growth narrative, supported by AI infrastructure, cloud expansion, and software monetization. However, energy presents potential asymmetric upside if commodity dynamics shift in its favor.

Sector rotation is rarely abrupt. More often, it unfolds gradually through portfolio rebalancing rather than wholesale liquidation.

While tech continues to dominate leadership, energy’s relative valuation discount and strong cash generation could attract incremental capital if macro conditions evolve.

Key indicators to monitor:

Relative strength between the Energy Select Sector SPDR Fund and the Technology Select Sector SPDR Fund

Forward earnings revisions

Oil price trends

Bond yield movements

The critical question is not whether rotation will occur — but whether it is already quietly underway beneath the surface.

Volatility in the S&P 500 has led to repeated swings without the steady upward momentum that characterized much of late 2025. With concerns about a potential correction—such as the bursting of an AI-driven bubble—investors may look toward more defensive options like dividend-paying stocks.

That said, dividend investing spans a wide spectrum. While many gravitate toward globally recognized, ultra-stable companies favored by figures like Warren Buffett, lesser-known firms can sometimes offer both dependable income and greater growth potential. Three under-the-radar dividend payers worth noting are Hancock Whitney Corp., NewMarket Corp., and Horace Mann Educators Corp..

A Well-Capitalized Southern Bank Gaining Momentum

Hancock Whitney Corp. is a bank holding company best known in the Gulf South. Through Hancock Whitney Bank, it provides commercial and retail banking along with wealth management services.

The company offers a solid 2.53% dividend yield and maintains a conservative payout ratio of 31.7%. In Q4 2025, earnings per share narrowly exceeded expectations by one cent, though revenue fell short.

Looking ahead to 2026, several factors strengthen its outlook. The company recently completed a bond portfolio restructuring expected to lift net interest margin by about 7 basis points and boost annual EPS by roughly $0.23. Loan growth is improving, and a strong capital position supported share buybacks totaling about 3% of outstanding shares in Q4 alone. That same capital base reinforces dividend sustainability, making it appealing for risk-conscious investors.

NewMarket: Resilient Income Despite Market Pressures

NewMarket Corp., a specialty chemicals company focused on lubricants and petroleum additives, has seen its shares decline roughly 14% year to date following its latest earnings release.

Lower net income and EPS in 2025—largely due to a higher effective tax rate—pressured results, while fourth-quarter petroleum additive shipments fell about 6% year over year amid softer demand.

However, its specialty materials division has performed strongly, bolstered by the October acquisition of aerospace propellant firm Calca. The company plans to invest $1 billion to expand this segment further in 2026.

Despite a Wall Street “Hold” rating, NewMarket continues generating strong cash flow. Last quarter alone, it returned $183 million to shareholders through dividends and buybacks. The stock yields 2.01%, carries a payout ratio just over 27%, and has consistently raised its dividend over multiple years.

Horace Mann’s Broad Strength Supports Its Dividend

Horace Mann Educators Corp., which provides retirement, property, and casualty insurance products tailored to U.S. school employees, has posted several strong quarters.

Its latest results included a 3-cent EPS beat and record full-year EPS of $4.71. Forecasts for 2026 align with the company’s 10% compound annual growth target.

Much of this improvement stems from its property and casualty segment, where both the combined ratio and core earnings improved significantly—more than doubling last year. Growth in individual supplemental and group sales has further diversified the business.

An early retirement initiative is expected to generate $10 million in annual savings, helping the company reduce its expense ratio by 100–150 basis points over the next three years. This should enhance cash flow for additional buybacks—after $21 million in repurchases in 2025—and continued dividend support. The stock currently offers a 3.25% yield with a 35.9% payout ratio.

In a market environment marked by uneven performance, these lesser-known dividend stocks combine income stability with strategic growth initiatives, making them compelling options for investors navigating potential turbulence in 2026.

U.S. stock index futures were largely unchanged Wednesday night after the minutes from the Federal Reserve’s January meeting delivered mixed signals on interest rates, adding to uncertainty about the longer-term policy path.

Investors are now turning their attention to upcoming earnings from retail heavyweight Walmart Inc (NYSE:WMT) for fresh insight into the health of the U.S. economy.

Markets were also pressured by rising geopolitical tensions involving Iran, as reports pointed to a stronger U.S. military presence in the Middle East despite continued talks between Tehran and Washington.

As of 20:00 ET (01:00 GMT), S&P 500 Futures dipped slightly to 6,892.0, Nasdaq 100 Futures edged down nearly 0.1% to 24,942.75, and Dow Jones Futures slipped 0.1% to 49,685.0.

Futures held steady after Wall Street posted gains in the regular session, driven mainly by an ongoing rebound in technology stocks and data showing resilience in the U.S. economy. However, caution surrounding the Fed’s outlook kept major indexes below their intraday peaks.

Fed minutes reveal divisions on inflation and rates

Minutes from the Fed’s January meeting showed officials unanimously agreed to keep interest rates steady at 3.50%–3.75%. Still, policymakers appeared divided over the next move. Several members warned that inflation could take longer than expected to return to the central bank’s 2% target.

A number of officials also suggested that rate hikes could be considered if inflation remains elevated for an extended period — a tone that contrasts with market expectations for further easing this year.

Artificial intelligence emerged as a key area of debate, with officials split on whether the rapidly expanding sector will ultimately fuel inflation or help contain it.

Walmart earnings in focus

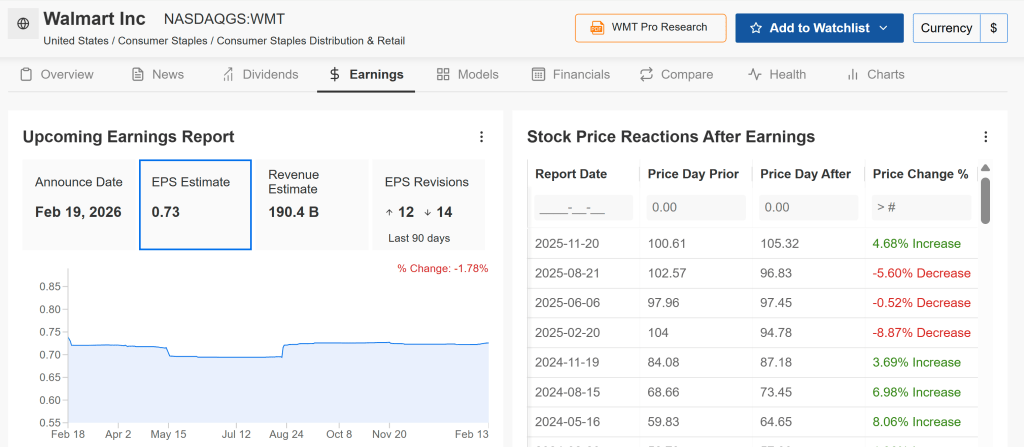

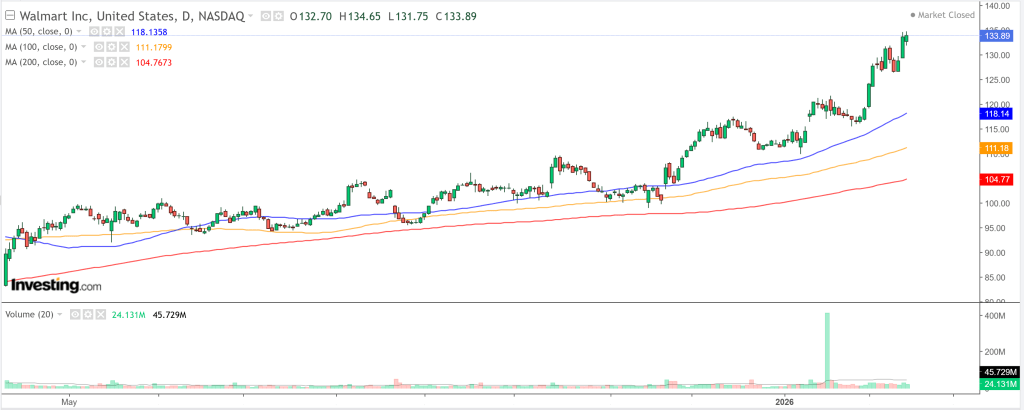

Walmart Inc (NYSE:WMT) is scheduled to report fourth-quarter results on Thursday, with particular attention on its 2026 outlook, which may offer broader clues about U.S. consumer strength.

According to Investing.com data, Walmart is expected to post earnings per share of $0.7269 on revenue of $190.4 billion.

As the world’s largest retailer by valuation and a widely followed barometer of U.S. consumer spending, Walmart’s results come at a time when sticky inflation is showing signs of straining retail demand.

Also due Thursday are U.S. December trade data and weekly jobless claims.

Wall Street gains led by tech rebound

Wall Street ended higher on Wednesday, led by technology stocks as the sector extended its recovery from recent declines.

Still, both major indexes and tech shares retreated from session highs amid lingering concerns about the impact of artificial intelligence. Worries over AI-driven disruption have recently weighed on software and logistics companies, while concerns about heavy AI-related capital spending have pressured firms exposed to data centers.

The S&P 500 rose 0.6% to 6,881.32, the NASDAQ Composite gained 0.8% to 22,753.64, and the Dow Jones Industrial Average added 0.3% to 49,662.66.

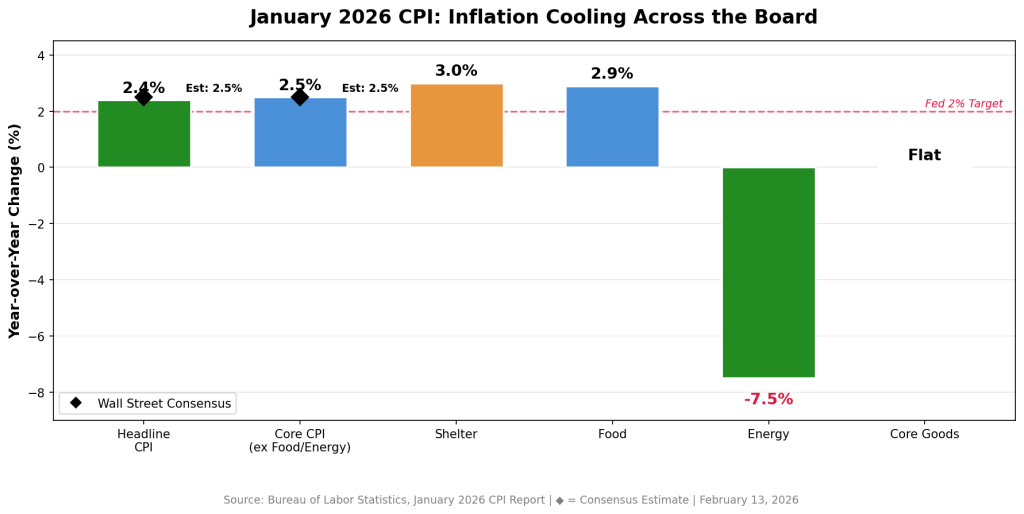

The inflation print investors had been bracing for came in cooler than expected.

Friday’s January CPI showed headline inflation at 2.4%—below the 2.5% consensus forecast and the lowest annual reading since May 2025. Core CPI, which excludes food and energy, eased to 2.5%, marking its softest level since April 2021. On a monthly basis, prices rose just 0.2%, the smallest increase since July.

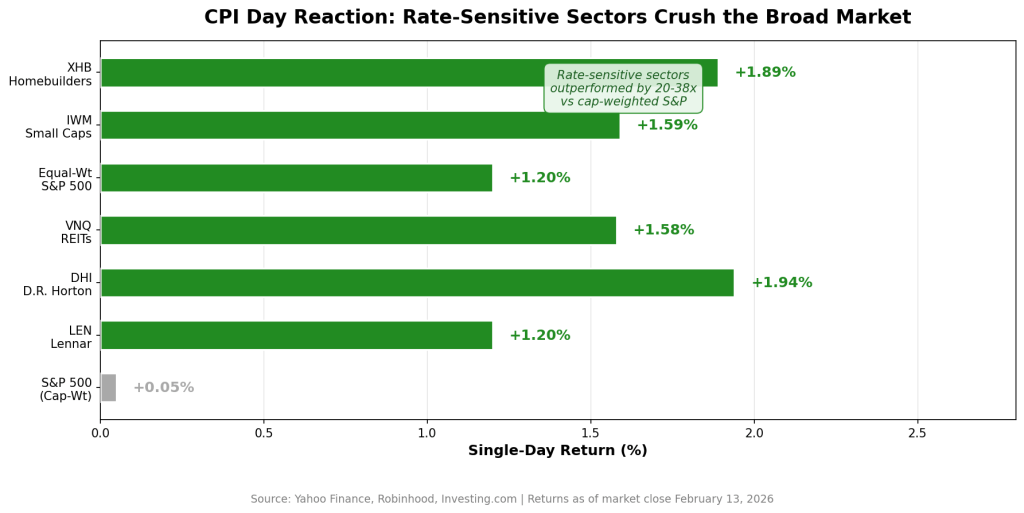

Markets reacted swiftly. Homebuilder stocks rallied sharply, small caps climbed 1.2%, and the 10-year Treasury yield slid to its lowest point since early December.

My takeaway: the market may have just received the confirmation it was waiting for. And the most compelling opportunities from here likely aren’t the mega-cap tech leaders that have dominated performance, but rather rate-sensitive sectors that were punished under the “higher for longer” narrative and are now repricing for a potentially different 2026 backdrop.

What the CPI Report Really Signals

Shelter—by far the largest CPI component and the category that has stubbornly kept headline inflation elevated—rose only 0.2% in January, bringing the annual rate down to 3%. That’s a notable slowdown and perhaps the clearest indication yet that the housing inflation lag is beginning to unwind.

Energy prices declined 1.5%, with gasoline tumbling 3.2% during the month. Food inflation held at 2.9% year over year—still somewhat elevated, but not alarming. Importantly, core goods prices were flat, helping to counter concerns that renewed tariffs would reignite goods inflation.

“Headline CPI inflation was a touch softer than expected in January, delivering a welcome surprise to the downside at the beginning of the year,” said Bernard Yaros, lead economist at Oxford Economics. He added that tariff-related price pressures “are largely behind us.”

Lindsay Rosner of Goldman Sachs Asset Management was even more direct: “Trust the groundhog. The Fed’s path to normalization cuts appears clearer now.”

The timing is critical. A stronger-than-expected January jobs report—130,000 payrolls versus forecasts of 55,000—had pushed expectations for rate cuts further out, likely into the summer. This softer CPI reading shifts that outlook. Economists surveyed by Bloomberg now anticipate as much as 100 basis points of easing this year, with the first cut potentially arriving in June—or even March if disinflation continues.

Why Rate-Sensitive Stocks Stand Out

One key dynamic investors often overlook is that by the time the Federal Reserve actually begins cutting rates, much of the upside in rate-sensitive sectors has already played out. Markets tend to price in policy shifts well in advance.

Friday’s CPI data appeared to give institutional investors the confidence to begin reallocating toward sectors poised to benefit from lower yields. The equal-weight version of the S&P 500 and the Russell 2000 both climbed 1.2%, notably outperforming the traditional cap-weighted S&P 500, which was little changed.

That divergence is often viewed as a textbook signal of sector rotation—away from mega-cap dominance and toward more rate-sensitive, economically cyclical areas of the market.

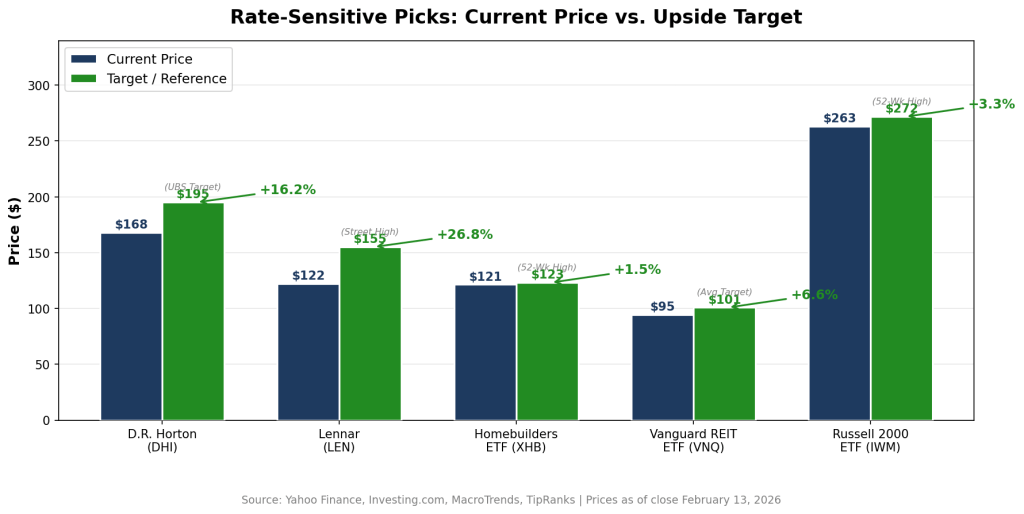

Capital is rotating down the market-cap ladder and into economically sensitive groups. Three segments stand out most clearly: homebuilders, REITs, and small caps.

How to Position

D.R. Horton (DHI)

Closing Friday at $167.78, DHI is arguably the purest expression of the housing-affordability theme. The largest U.S. homebuilder by volume posted solid fiscal Q1 results in January, with revenue of $6.89 billion (ahead of $6.59 billion estimates) and EPS of $2.03 (vs. $1.93 expected).

At roughly 15.3x trailing earnings, the stock trades at a notable discount to the broader market. Beyond the rate backdrop, there’s also a policy angle: the Trump administration’s reported “Trump Homes” initiative has involved direct engagement with builders around affordability measures—potentially creating a dual tailwind of lower mortgage rates and regulatory support.

The median analyst price target is $170, with UBS as high as $195—suggesting upside potential of roughly 16%.

Lennar (LEN)

Trading at $122.28, Lennar offers a slightly different profile as the second-largest U.S. builder. Its “land-light” model—optioning land instead of holding it outright—reduces balance-sheet risk and positions it well for a rate-cutting cycle.

The stock has rebounded about 40% from its April 2025 lows but remains below its 2024 peak. With fiscal Q1 earnings due in late March, improving mortgage application trends could serve as a near-term catalyst if rates continue to ease.

SPDR S&P Homebuilders ETF (XHB)

At $121.36, XHB is up nearly 18% year-to-date and recently marked a fresh 52-week high of $123.13. As an equal-weighted ETF, it offers diversified exposure across the housing ecosystem—not just large builders, but also building products manufacturers, home improvement retailers, and construction suppliers.

For investors who prefer sector exposure over single-stock risk, XHB provides a balanced approach.

Vanguard Real Estate ETF (VNQ)

Trading near $94.59—close to its 52-week high—VNQ provides broad exposure to the REIT space, one of the most rate-sensitive areas of the market. The ETF holds over 150 REITs across healthcare, industrial, data center, and retail subsectors.

Its largest holdings include Welltower, Prologis, and American Tower.

With an average analyst target near $100.81, implied upside sits around 8%, in addition to a dividend yield of roughly 3.6%. After significant underperformance during the rate-hiking cycle, REITs are positioned to benefit mechanically as yields decline.

iShares Russell 2000 ETF (IWM)

At approximately $263, IWM tracks small-cap equities—arguably the most interest-rate-sensitive segment of the equity market. Smaller firms tend to carry more floating-rate debt and are disproportionately affected by elevated borrowing costs. That dynamic can reverse sharply when policy eases.

IWM surged 1.6% on Friday’s CPI release alone. With its 52-week high of $271.60 within reach, sustained rate declines could drive a prolonged catch-up rally in small caps.

The Big Picture

If inflation continues to moderate and rate-cut expectations firm, the leadership baton may continue shifting away from mega-cap growth and toward housing, real estate, and smaller domestically oriented companies. Markets typically front-run the policy cycle—and this rotation suggests that repositioning may already be underway.

The Bear Case (and Why It May Be Overstated)

There are valid reasons for caution. Fox Business pointed out that January’s CPI could carry a downward bias tied to last fall’s government shutdown. During that period, the Bureau of Labor Statistics missed portions of October data collection and relied on a “carry-forward” methodology that may influence inflation readings into spring 2026. In short, the 2.4% headline figure could be somewhat understated.

There’s also the Federal Reserve itself. Policymakers are not signaling urgency. Oxford Economics continues to project cuts in June and December rather than March. Meanwhile, although the labor market is cooling—annual benchmark revisions show 2025 job growth was the weakest since 2003 outside recessionary periods—it is far from collapsing. Jerome Powell has consistently emphasized the need for a sustained disinflation trend, not a single favorable report.

The Counterargument

Even if the Fed waits until June, markets won’t. Yields have already declined meaningfully. Mortgage rates are edging lower. And sectors that trade on rate expectations—rather than the actual fed funds rate—are beginning to reprice now. By the time the first official cut arrives, much of the move in rate-sensitive equities could already be behind us.

What to Watch

Three near-term catalysts will likely shape the next phase:

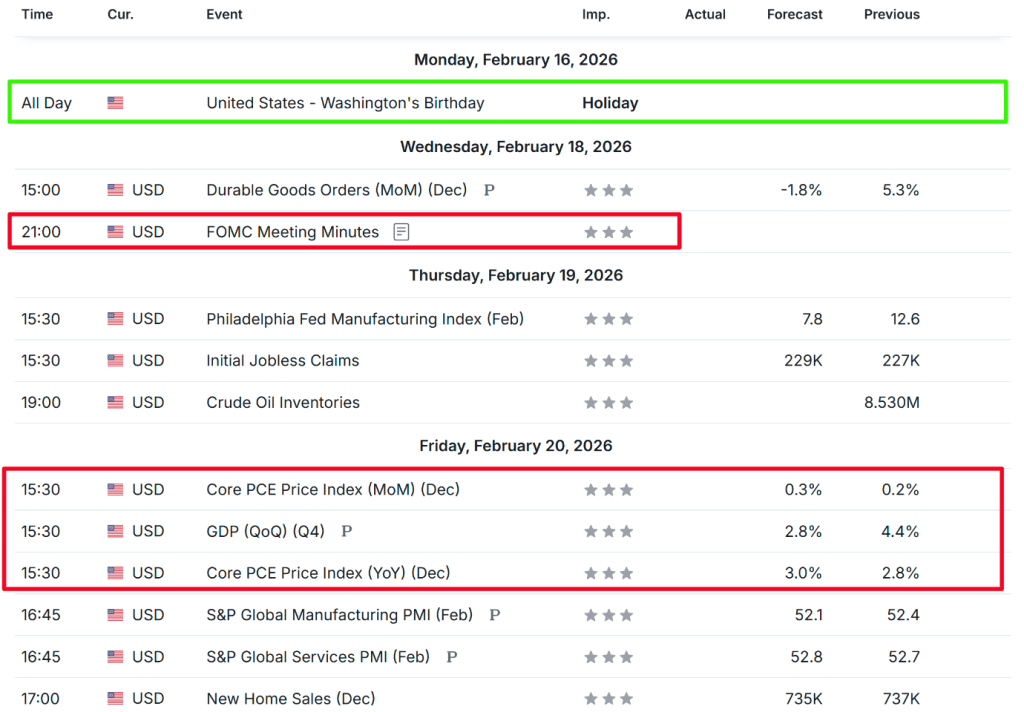

Fed Minutes (Feb. 18): The release of the latest policy meeting minutes could shift expectations quickly. Any dovish commentary on inflation progress or labor-market softness may pull forward rate-cut pricing.

Walmart Q4 Earnings (Feb. 19): As the largest U.S. retailer—now with a market cap above $1 trillion and up 13% year-to-date—Walmart’s guidance will offer real-time insight into consumer spending trends. If easing inflation is translating into stronger purchasing power, that reinforces the soft-landing narrative.

PCE Price Index (Later This Month): The Fed’s preferred inflation gauge will be pivotal. Confirmation of CPI’s cooling trend would likely solidify expectations for a June cut and intensify debate around a possible March move—potentially fueling the next leg higher in rate-sensitive stocks.

Bottom Line

The inflation backdrop has shifted in a way that favors investors. The opportunity isn’t complex—but it does require stepping away from the mega-cap tech trade that has dominated for the past two years and leaning into sectors positioned to benefit most from falling yields.

U.S. stock index futures slipped modestly on Tuesday night as a fragile rebound in technology shares showed signs of strain, with investors remaining cautious ahead of a wave of economic data and Federal Reserve signals.

Futures pulled back following a mildly upbeat session on Wall Street, where tech stocks attempted to bounce from recent declines. The recovery, however, was uneven, as lingering concerns over AI-driven disruptions continued to cloud sentiment in the sector.

By 19:55 ET (00:55 GMT), S&P 500 futures were down 0.1% at 6,851.50, Nasdaq 100 futures fell 0.2% to 24,721.0, and Dow Jones futures slipped 0.1% to 49,553.0.

Economic data, Fed minutes in focus

Attention now turns to several key economic releases and the minutes from the Fed’s January meeting, due Wednesday afternoon. Investors are looking for greater clarity on the central bank’s interest rate outlook after policymakers kept rates steady last month and signaled ongoing caution over persistent inflation and softening labor market conditions.

January industrial production figures are scheduled for Wednesday, followed by December’s PCE price index on Friday — the Fed’s preferred inflation measure and a key input into its longer-term rate projections.

Uncertainty surrounding the Fed has weighed on markets in recent weeks, particularly after President Donald Trump’s nomination of Kevin Warsh as the next Fed Chair was interpreted as a less dovish shift in leadership.

Nvidia, Meta pare gains; AMD cuts losses

NVIDIA and Meta Platforms gave back some after-hours gains but still rose about 0.6% each after announcing a multi-year partnership to expand AI infrastructure, with Nvidia set to supply millions of chips to Meta.

Rival AMD, which had dropped as much as 4% following the announcement, reduced its losses to trade roughly 2% lower.

Technology stocks remain sensitive after weeks of declines fueled by concerns about AI-related disruption — especially within software — as well as skepticism over elevated AI spending and the sector’s long-term growth outlook.

Wall Street posts modest gains

Major indexes ended Tuesday slightly higher, supported by a patchy tech rebound and strength in financial stocks. The S&P 500 rose 0.1% to 6,843.22, the Nasdaq Composite added 0.1% to 22,578.38, and the Dow Jones Industrial Average gained 0.07% to 49,533.19.

While some dip-buying helped tech shares recover modestly, heavyweight names including Microsoft, Tesla, Alphabet, and Oracle extended last week’s declines.

Markets also drew limited support from reports of progress in U.S.-Iran nuclear discussions, easing some concerns about escalating geopolitical tensions in the Middle East.

The S&P 500 E-mini bears are targeting a decisive breakdown below the February 5 low and the 20-week EMA, followed by strong and sustained selling pressure. In contrast, bulls want the 20-week EMA to hold as support, and if prices decline, they are looking to the November 21 low as a key support level.

S&P 500 E-Mini Futures – Weekly Chart

This week’s candlestick formed an inside bear bar that closed in the lower half of its range while testing the 20-week EMA. As mentioned last week, the market was likely to continue moving sideways in the near term, and so far it remains confined within an 11-week tight trading range.

From the bearish perspective, the chart shows a wedge top (December 11, December 26, and January 12), a double top (October 29 and January 28), and a smaller double top (January 12 and January 28). Bears want the October 29 high to serve as resistance. Their goal is a strong breakout below the February 5 low and the 20-week EMA, followed by continued selling that could project a measured move down toward 6,500, based on the height of the 11-week range. To shift the market into an Always In Short condition, bears need consecutive strong bear bars closing well below the 20-week EMA. If the market moves higher, they prefer weak follow-through buying to raise the probability of a failed breakout.

Bulls, on the other hand, see a large double-bottom bull flag (December 17 and February 5), along with a High 4 buy setup. They need a powerful breakout above the January 28 high with sustained follow-through to increase the likelihood of trend continuation, targeting a measured move toward 7,300, based on the range height. Bulls want the 20-week EMA to hold as support, and if prices fall, they expect the November 21 low to provide backing.

The market has traded in a tight range for 11 weeks, reflecting a balance between buyers and sellers as bearish pressure has caught up with the prior uptrend. Over the past two weeks, bulls have been unable to break above previous highs and have seen progressively lower closes within the range.

Until a decisive breakout occurs, traders may continue to apply a Buy Low, Sell High strategy within the range. Market participants will watch whether bears can push through the bottom of the 11-week range with strong follow-through selling, or whether bulls can retest and break above the all-time high. However, even if a new high is reached, lack of sustained buying would increase the risk of a failed breakout.

Alternatively, the market may continue to consolidate around the October 29 high. Most traders will likely wait for a clear breakout with strong follow-through—either above the all-time high or below the 20-week EMA—before committing aggressively. The longer price stalls near the October 29 high without breaking higher, the greater the probability of a deeper pullback.

Daily S&P 500 E-Mini Chart

The market edged higher early in the week. Although Tuesday and Wednesday opened with gap-ups, both sessions reversed and closed as bear bars. On Thursday, a large bear bar formed, testing the 100-day EMA, and Friday printed a doji, signaling hesitation.

Last week, traders were monitoring whether price would stall near the 20-day EMA and develop a second sideways-to-down leg, or whether bulls could produce enough follow-through buying to push to new all-time highs. So far, price action is pausing around both the 20-day EMA and the all-time high zone.

From the bullish perspective, the chart shows a large double-bottom bull flag (December 17 and February 5), a wedge bull flag (January 2, January 20, and February 5), and a smaller double bottom (February 5 and February 13). Bulls are aiming for a decisive breakout above the January 28 high with sustained buying momentum, targeting a measured move toward 7,300 based on the height of the 11-week range. If the market declines, they want the November 21 low or the 200-day EMA to provide support. To improve the odds of a successful breakout and renewed uptrend, bulls need consecutive strong bull bars.

Bears, meanwhile, want the 20-day EMA to cap price as resistance. Their objective is a clear breakdown below the 11-week trading range, with a projected move toward 6,500 based on the same range measurement. To shift the market into an Always In Short condition, they need consecutive strong bear bars breaking below the December 17 low and the 100-day EMA. If the market rallies to a new all-time high, bears prefer to see weak follow-through buying to raise the likelihood of a failed breakout.

The market continues to trade within a range that began in late November, with bulls seeking an upside breakout and bears pushing for a downside resolution. Since late December, price action has shaped an expanding triangle, which can serve as either a continuation or reversal pattern and often traps traders with false breakouts before reversing.

Over the past two weeks, bear bars have been more pronounced than bull bars, suggesting gradually increasing and cumulative selling pressure. Traders are closely watching whether the market keeps stalling around the 20-day EMA and the all-time high area. A pattern of slightly lower highs accompanied by stronger bear bars would increase the probability of a downside breakout. Conversely, if bulls manage a breakout to new highs, traders will look for strong follow-through; without it, the risk of a failed breakout rises.

Until a decisive move with sustained momentum occurs in either direction, traders may continue applying a Buy Low, Sell High (BLSH) approach — buying near the lower third of the range and selling near the upper third.

The upcoming holiday-shortened trading week will spotlight the Federal Reserve’s FOMC minutes and Walmart’s earnings report.

Analog Devices enters its earnings release with Wall Street projecting a strong 41% increase in EPS alongside 28% revenue growth. Meanwhile, Walmart may face downside risk, as expectations appear stretched and the stock looks “priced for perfection” ahead of results.

On Friday, U.S. equities finished largely flat as investors digested softer-than-expected inflation data, reinforcing expectations that the Federal Reserve remains on course to cut interest rates this year.

Despite the muted close, major indexes posted weekly losses. Concerns over AI-driven disruption extended beyond technology shares, weighing on brokerages, commercial real estate companies, and logistics firms.

The S&P 500 declined 1.4%, marking its second straight weekly drop. The Dow Jones Industrial Average lost 1.2%, while the Nasdaq Composite slid 2.1%, notching its fifth consecutive weekly loss — its longest downturn since May 2022.

The week ahead is shaping up to be active as investors continue evaluating the outlook for growth, inflation, and monetary policy. U.S. markets will be closed Monday in observance of Presidents Day.

With limited economic data on the calendar, attention will center on the minutes from the Fed’s January FOMC meeting, which could provide further clues on the interest-rate trajectory. Friday will also bring the release of the latest core PCE price index, a key inflation gauge.

As of Sunday morning, markets are pricing in two 25-basis-point rate cuts by the end of 2026, with about a 50% probability of an additional reduction, according to Investing.com’s Fed Monitor Tool.

On the corporate front, Walmart’s earnings will headline the final stretch of reporting season. Other notable reports due include Deere, Palo Alto Networks, and Toll Brothers.

Investors are also awaiting a U.S. Supreme Court decision expected Friday regarding the legality of President Donald Trump’s global tariffs.

Regardless of market direction, below are one stock that could attract buying interest and another that may face renewed selling pressure in the week of Monday, February 16 through Friday, February 20.

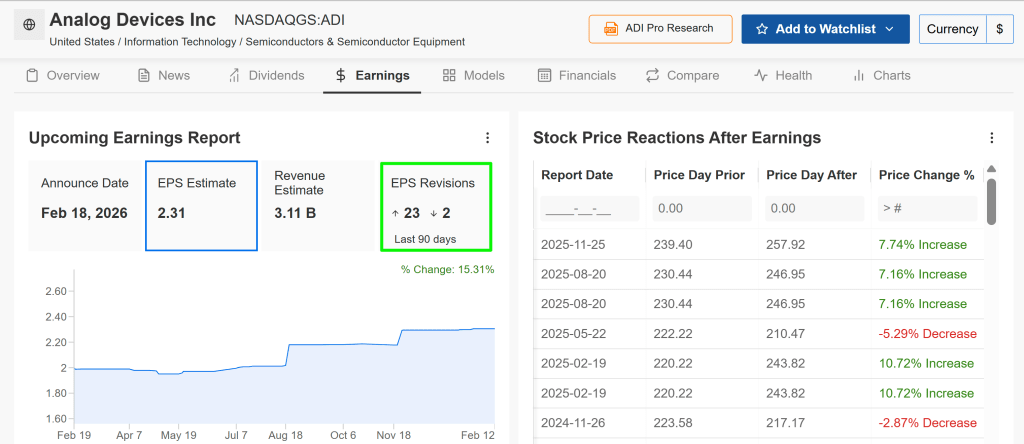

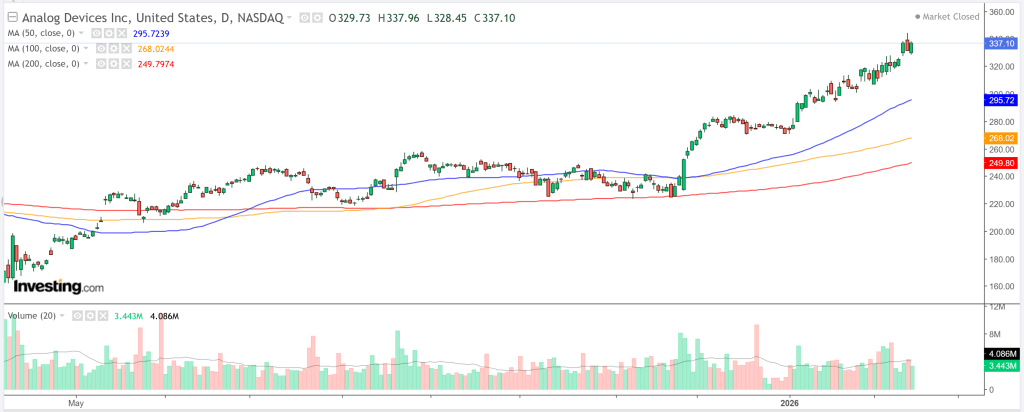

Stock to Buy: Analog Devices

Analog Devices (NASDAQ: ADI) remains well-positioned at the center of the industrial semiconductor recovery. The company is set to release its fiscal first-quarter results on Wednesday at 7:00 a.m. ET, with analysts forecasting a 41% jump in earnings per share and 28% revenue growth, driven by accelerating demand in robotics, automation, and AI-related infrastructure.

Sentiment heading into the report has been increasingly upbeat. InvestingPro data shows that 23 of the past 25 EPS revisions have been upward, reflecting rising confidence in the company’s growth trajectory. In the options market, traders are pricing in a potential post-earnings swing of approximately ±4.2%.

Analog Devices continues to benefit from long-term structural themes, including electrification, factory automation, and data-center expansion. Following prior inventory adjustments, recent quarters have demonstrated a solid rebound, supported by strong free cash flow generation that underpins dividends and share repurchases.

Technically, ADI has maintained a firm uptrend, recently reaching highs near $344 before experiencing a modest pullback. The stock remains comfortably above key moving averages and is showing relative strength versus the broader market. Immediate support lies in the $325–$330 range, while resistance stands near its record high around $344.

Across multiple timeframes, indicators point to strong bullish momentum. If earnings meet or exceed expectations, the technical setup suggests the potential for a breakout move.

Trade Setup:

Entry: Near current levels (~$337)

Target: $350–$360 (approximately 4%–7% upside)

Stop-Loss: $325 (around 3.5% downside risk)

Stock to Sell: Walmart

Walmart (NASDAQ: WMT) has just crossed the historic $1 trillion market cap milestone and is set to release earnings Thursday at 7:00 AM ET. Fundamentally, the company remains strong: it’s expanding grocery market share, scaling its high-margin advertising segment, and leveraging AI to improve efficiency.

However, valuation is the key concern. With a forward P/E of 50.6x, the stock appears priced for flawless execution. That leaves minimal margin for disappointment. Even a slight miss in forward guidance could spark a notable pullback as expectations reset. Options markets are implying a post-earnings swing of just over 8 points in either direction.

Wall Street expects EPS of $0.73 (around 10% year-over-year growth) on roughly $190 billion in revenue. This will be the first earnings report under new CEO John Furner, adding another layer of scrutiny. Analyst sentiment has turned more cautious recently, with more than half of the latest estimate revisions skewing lower.

Oppenheimer anticipates solid results but cautions that guidance may underwhelm—similar to last year’s Q4 report, when the stock dropped about 8%. Jefferies notes that Walmart benefits from price normalization and tighter consumer spending, but much of that optimism seems fully reflected in the share price.

After a sharp rally to fresh record highs in the $134–$135 range, momentum appears stretched. Short-term technical indicators, including RSI, signal overbought conditions. Buying volume has begun to fade, and a negative surprise could push shares back toward support near $125.

European equities moved modestly higher on Monday, helped by a broadly supportive earnings season, though trading volumes were thin due to holidays in both Asia and the United States.

At 03:02 ET (08:02 GMT), Germany’s DAX advanced 0.4%, France’s CAC 40 added 0.2%, and the UK’s FTSE 100 gained 0.2%.

Earnings season supports sentiment

The week began quietly, with much of Asia observing the Lunar New Year holiday and U.S. markets closed for George Washington’s birthday. Still, investor mood in Europe remained constructive, as corporate results have generally exceeded expectations amid signs of a gradual economic recovery.

According to LSEG data, companies accounting for 57% of Europe’s total market capitalization have reported fourth-quarter results so far, delivering average earnings growth of 3.9%—well above earlier projections for a 1.1% contraction. Around 60% of firms have beaten analyst estimates, compared with a typical quarterly average of 54%.

While Monday’s earnings calendar is light, attention this week will center on Europe’s four largest mining groups—Rio Tinto, Glencore, Anglo American, and Antofagasta—as metals prices hover near recent highs.

Meanwhile, Volkswagen is in focus after Manager Magazin reported that the carmaker plans to reduce costs by 20% across all brands by the end of 2028.

In the U.S., the key earnings event will be results from Walmart on Thursday, with the retail heavyweight’s report expected to provide fresh insight into consumer spending trends.

Economic data and oil markets

On the macro front, Eurozone industrial production data for December is due later Monday and is forecast to show a 1.5% monthly decline.

In the UK, property website Rightmove reported that average asking prices for newly listed homes dipped by just £12 in February to £368,019, following a sharp 2.8% rise in January.

Earlier in Asia, Japan’s fourth-quarter GDP rose just 0.2% on an annualized basis, significantly below the 1.6% forecast, reinforcing the case for stronger fiscal support under Prime Minister Sanae Takaichi.

Oil prices were broadly steady in holiday-thinned trading. Brent Crude futures edged down 0.1% to $67.66 per barrel, while West Texas Intermediate slipped 0.1% to $62.68. Both benchmarks had already fallen between 0.5% and 1% last week after comments from U.S. President Donald Trump suggesting a potential deal with Tehran.

The U.S. and Iran are scheduled to hold a second round of talks in Geneva on Tuesday as they continue efforts to address longstanding tensions over Tehran’s nuclear program.

The AI-driven displacement trade weighed on multiple sectors this week.

Logistics companies were particularly pressured, with C.H. Robinson (CHRW) dropping more than 14% on Thursday amid AI-related concerns. The stock has fallen over 10% for the week.

Brokerage firm Charles Schwab slid starting Tuesday and is down roughly 9% over the past week. Its CEO told Bloomberg TV that management was “disappointed and surprised” by the sell-off, noting the firm is actively integrating AI to benefit clients.

Real estate services company CBRE sank sharply on Wednesday and Thursday, leaving shares down about 15.2% for the week. While AI-related concerns contributed to the decline, weaker-than-expected revenue in its latest earnings report also weighed on sentiment.

Applied Materials

Applied Materials is on track to finish the week higher, surging more than 8% Friday (as of 13:20 ET) after posting quarterly results.

The company exceeded consensus estimates and delivered strong second-quarter guidance. Brokerage Summit Insights upgraded AMAT to Buy, citing anticipated strength in wafer fabrication equipment (WFE) spending through the second half of 2026.

Pinterest

Shares of Pinterest tumbled more than 18% Friday following its post-close earnings release Thursday, bringing its weekly loss to over 22%.

The company reported fourth-quarter earnings and revenue below analyst expectations and issued first-quarter guidance that also missed consensus. Loop Capital analyst Rob Sanderson said that while Pinterest has a compelling platform and strong user growth, challenges in monetization and exposure to unusual macro conditions are overshadowing its strengths.

Sanderson downgraded PINS to Hold, noting it may take several quarters to complete its sales reorganization, manage higher spending, and rebuild investor confidence.

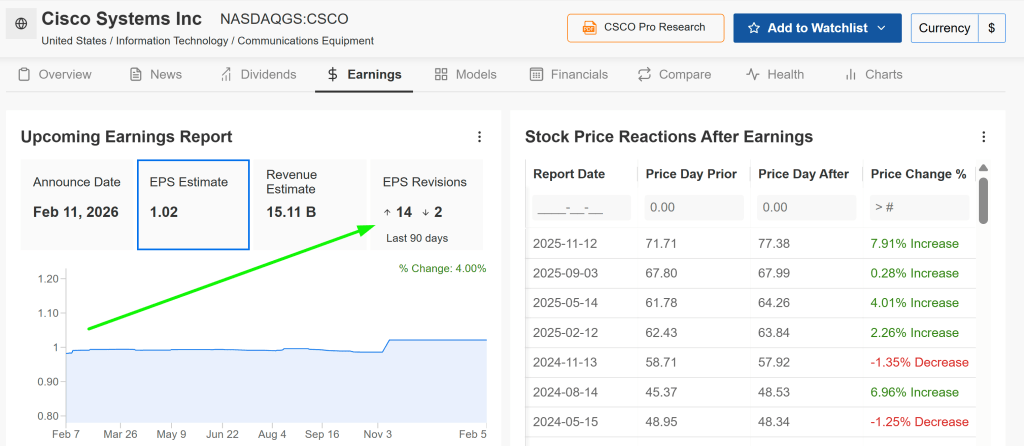

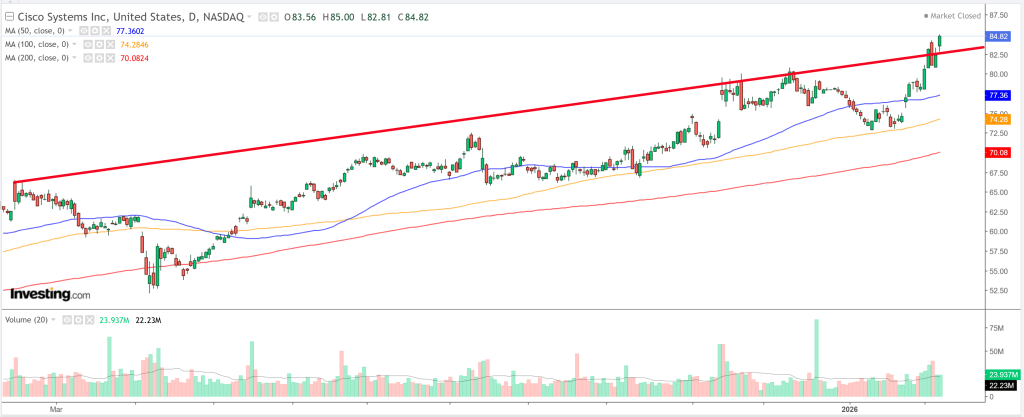

Cisco Systems

Shares of Cisco Systems dropped more than 12% Thursday following earnings.

Although Cisco beat profit and revenue expectations and offered upbeat guidance, investors reacted negatively to weaker-than-anticipated gross margins. UBS analyst David Vogt noted that higher memory input costs are expected to pressure margins over the next several quarters, lowering FY26 gross margin forecasts.

Unity Software

Unity Software plunged more than 26% Wednesday after earnings, with losses extending into Thursday and Friday. The stock is now down 21% over the past week.

While fourth-quarter results beat expectations, first-quarter revenue guidance disappointed investors. Despite that, Citizens analyst Andrew Boone maintained a positive stance, arguing that despite uncertainty around AI’s long-term impact, Unity’s platform remains essential for developers given the complexity of game creation and operations.

Oracle

After several weeks of declines tied to AI data center concerns, Oracle rebounded strongly, gaining more than 15% this week.

On Monday, DA Davidson analyst Gil Luria upgraded Oracle to Buy from Neutral. He suggested that a restructured OpenAI could reestablish itself as a leading challenger to Google and meet its commitments to Oracle this year, potentially removing a key overhang for the stock.

U.S. stock index futures edged down Thursday night after a sharp selloff in technology shares triggered heavy losses on Wall Street, with investors now awaiting key inflation data for further direction.

Wall Street declines as tech losses deepen; Cisco plunges.

Tech stocks slid as markets worried about fresh disruptions linked to artificial intelligence, while disappointing earnings from Cisco added to the pressure. Lingering uncertainty around U.S. rate cuts—particularly after this week’s strong nonfarm payrolls report—kept buyers cautious and prompted some profit-taking. By 19:57 ET, S&P 500 and Nasdaq 100 futures were each down 0.1%, while Dow futures were slightly lower.

On Thursday, major indexes fell steeply, led by renewed weakness in technology amid concerns over AI-driven disruption. Logistics and transportation stocks were also hit following reports that a new tool from Algorhythm Holdings could significantly streamline freight operations, potentially dampening demand across the sector.

The news sent trucking and logistics shares sharply lower, while Algorhythm surged nearly 30%. Meanwhile, Cisco Systems dropped 12% after posting weaker-than-expected results, dragging other major tech names lower, with the “Magnificent Seven” declining between 0.6% and 3%. The S&P 500 lost 1.6%, the Nasdaq Composite fell 2%, and the Dow Jones Industrial Average dropped 1.3%.

Investors await CPI report as interest rate uncertainty intensifies.