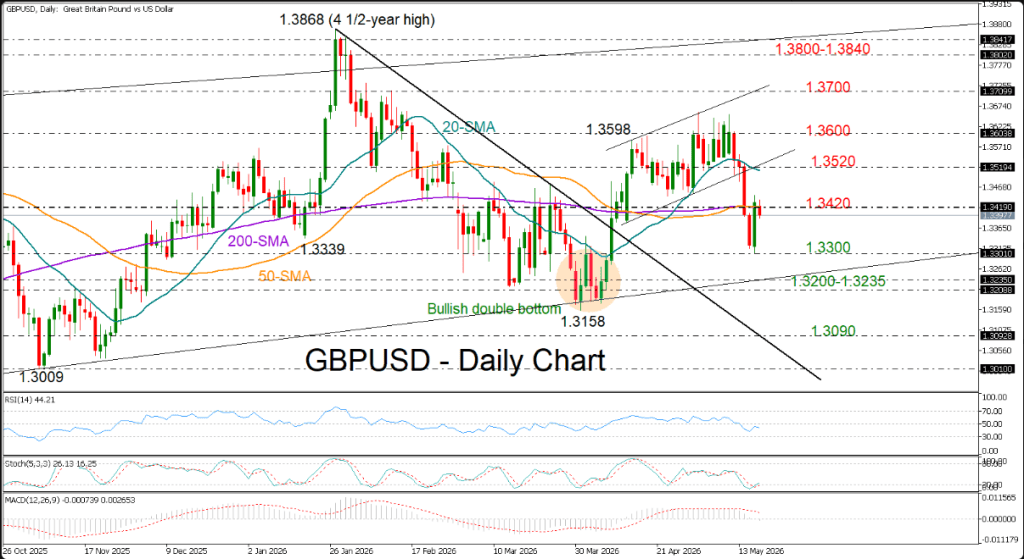

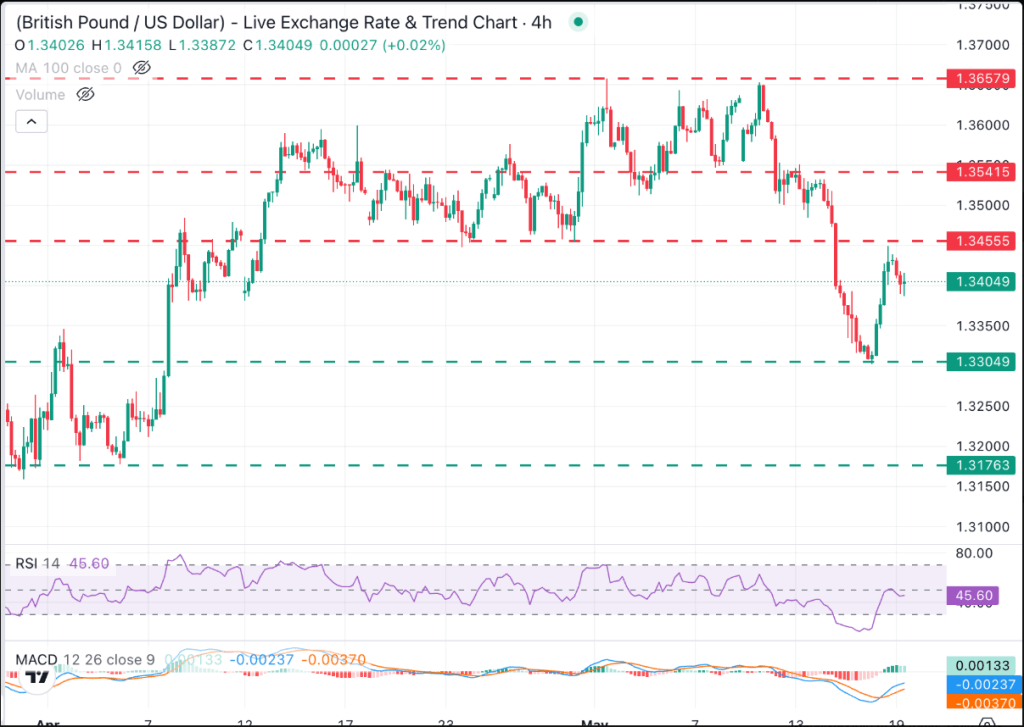

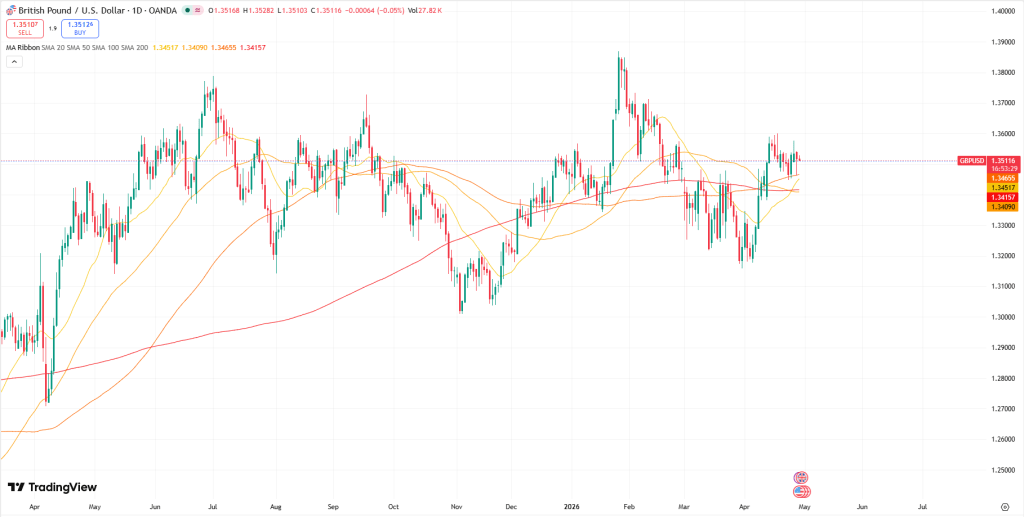

GBP/USD remains subdued below the SMAs near 1.3420 as the UK unemployment rate ticks higher.

The near-term outlook stays bearish, with additional selling pressure likely below 1.3200.

GBP/USD remains under pressure below its 50- and 200-day simple moving averages (SMAs) around 1.3420 as traders weigh weak political sentiment and softer UK economic data. Earlier on Tuesday, the UK unemployment rate rose to 5.0%, while April employment showed a decline of 100,000 jobs.

Technically, near-term momentum continues to favor the downside, with the RSI staying below the neutral 50 threshold and the MACD drifting into negative territory.

If resistance at 1.3420 continues to cap gains, the pair could revisit support near 1.3300. A stronger support region may then emerge around 1.3200–1.3235 before the broader outlook turns decisively bearish, opening the door for a deeper slide toward 1.3090.

On the upside, confirmation of Monday’s bullish engulfing candle through a break above 1.3420 could pave the way for a move toward the 20-day SMA and the 1.3520 area. A sustained rise beyond 1.3600 may also allow the pair to print a fresh short-term high near 1.3700, reviving the broader recovery trend.

Overall, GBP/USD remains vulnerable while trading beneath the 50- and 200-day SMAs near 1.3420. Still, a more pronounced bearish outlook would likely require a decisive breakdown below the 1.3200–1.3225 support zone.

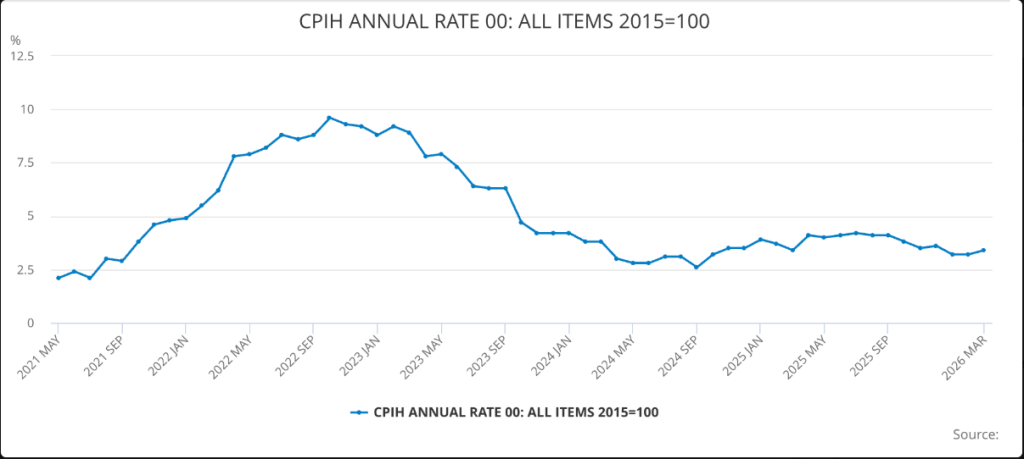

UK annual headline inflation is expected to soften in April even as monthly inflation edges higher.

The upcoming UK CPI report could give the BoE additional room to leave interest rates unchanged in June.

Pressure on the Pound Sterling remains to the downside, while an inflation figure above forecasts may add to the currency’s weakness.

The Office for National Statistics is set to release the UK Consumer Price Index (CPI) data for March at 06:00 GMT.

As inflation remains a key focus for central banks, investors will closely examine April’s CPI figures for clues on the next policy move by the Bank of England. Any significant divergence from market expectations could trigger short-term volatility in the British Pound (GBP).

What to expect from the upcoming UK inflation report

UK annual inflation is projected to ease to 3% in April from 3.3% in March, although monthly CPI growth is expected to accelerate slightly to 0.9% from the previous 0.7% reading.

The reduction in Ofgem’s energy price cap ahead of the Iran conflict appears to have helped limit the impact of higher energy costs, while fading Easter-related price effects have also contributed to moderating inflation pressures.

Core CPI, which excludes volatile items such as energy, food, alcohol, and tobacco, is projected to slow to 2.6% YoY in April — the weakest pace since July 2021 — reinforcing expectations for softer overall inflation.

Alongside the CPI report, the Office for National Statistics will also release April’s Producer Price Index (PPI) data. PPI Input inflation is forecast to cool sharply to 1% from 4.4% in March, while PPI Output inflation is expected to edge up slightly to 1% YoY from 0.9%.

If confirmed, easing inflation pressures could reduce the urgency for the Bank of England to raise interest rates, particularly as UK unemployment continues to rise following Tuesday’s labor market data. However, the relief may prove temporary. Ofgem is scheduled to revise the energy price cap in July, likely leading to higher household energy bills and renewed upward pressure on headline inflation. The BoE currently expects inflation to peak around 4% later this year.

Analysts at TD Securities noted that while the latest inflation figures may offer short-term reassurance, the full impact of higher energy costs is expected to emerge in the third quarter, with potential second-round inflation effects later in the year.

How could the UK CPI report impact GBP/USD?

Inflation remains a central factor in BoE policymaking and therefore has a major influence on the British Pound. Still, Sterling has been weighed down in May by mounting political uncertainty following the Labour Party’s poor performance in local elections, creating additional pressure on the currency.

In this context, a softer-than-expected inflation reading could offer some support to the Pound by giving the BoE more flexibility to monitor domestic conditions and assess the economic fallout from tensions in the Middle East before adjusting interest rates. BoE Deputy Governor Sarah Breeden warned on Monday that political uncertainty is affecting the business climate and cautioned policymakers against acting too aggressively on rates.

On the other hand, a stronger-than-expected inflation print could place the BoE in a more difficult position and potentially deepen bearish sentiment toward the Pound.

From a technical standpoint, Guillermo Alcala believes the British Pound remains under pressure following last week’s decline. He noted that although Monday’s bullish engulfing pattern on the daily chart helped reduce some downside momentum, the near-term outlook for GBP remains bearish. According to Alcalá, buyers still require stronger momentum to reclaim the former support zone near 1.3450 and shift attention toward the mid-May highs around 1.3530–1.3540.

On the downside, he highlighted Monday’s low near 1.3305 as an important support level. A decisive break below that area could pave the way for further losses toward the late-March and early-April highs around 1.3175.

USD/CHF moves higher as the US Dollar finds support after President Trump threatened to renew attacks on Iran.

Meanwhile, the US 30-year Treasury yield eased to 5.181% after reaching a near 19-year peak of 5.200% on Wednesday.

In Switzerland, preliminary data showed the economy expanded 0.5% in the first quarter, marking its strongest quarterly growth in a year and pointing to a recovery in economic activity.

USD/CHF continued to climb for a second straight session, trading near 0.7890 during Wednesday’s Asian session as demand for safe-haven assets boosted the US Dollar. Market sentiment remained cautious after a Bloomberg report indicated that President Donald Trump had threatened to restart attacks on Iran within days in an effort to pressure Tehran into ending the conflict with Israel. The warning followed a temporary pause in military action after Iran reportedly presented a new proposal aimed at de-escalation.

Concerns over rising energy prices linked to the conflict have also fueled fears of stronger inflationary pressures in the United States. Higher oil prices reinforced expectations that the Federal Reserve could keep interest rates elevated for a longer period or potentially tighten policy further if inflation remains persistent.

Meanwhile, US Treasury yields stayed near multi-month highs. The 30-year Treasury yield eased slightly to 5.181% after touching a nearly 19-year high of 5.200% earlier on Wednesday. At the same time, the 10-year yield hovered close to a 16-month peak of 4.687%, while the 2-year yield remained near a 15-month high of 4.139%, both levels reached on Tuesday.

In Switzerland, preliminary data showed the economy expanded by 0.5% quarter-over-quarter in the first quarter of 2026, up from 0.2% growth in the previous quarter. The reading marked the country’s strongest quarterly growth in a year and suggested that the Swiss economy continues to recover steadily. Investors are now awaiting Switzerland’s first-quarter Industrial Production data, scheduled for release on Thursday.

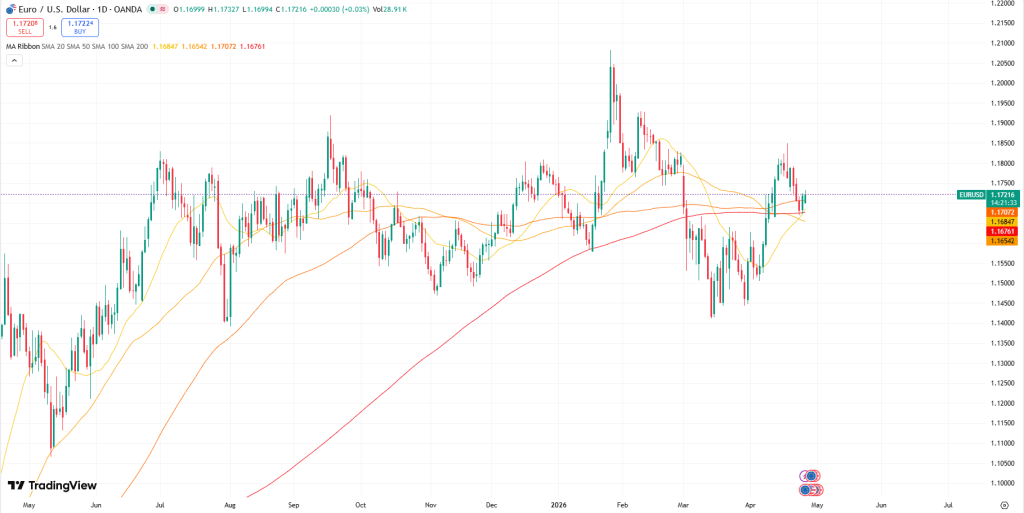

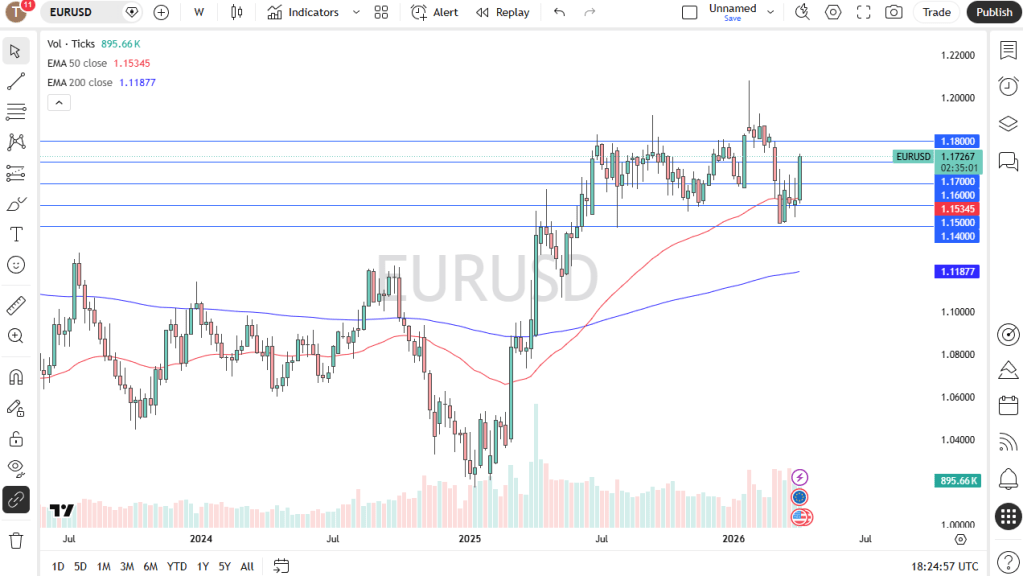

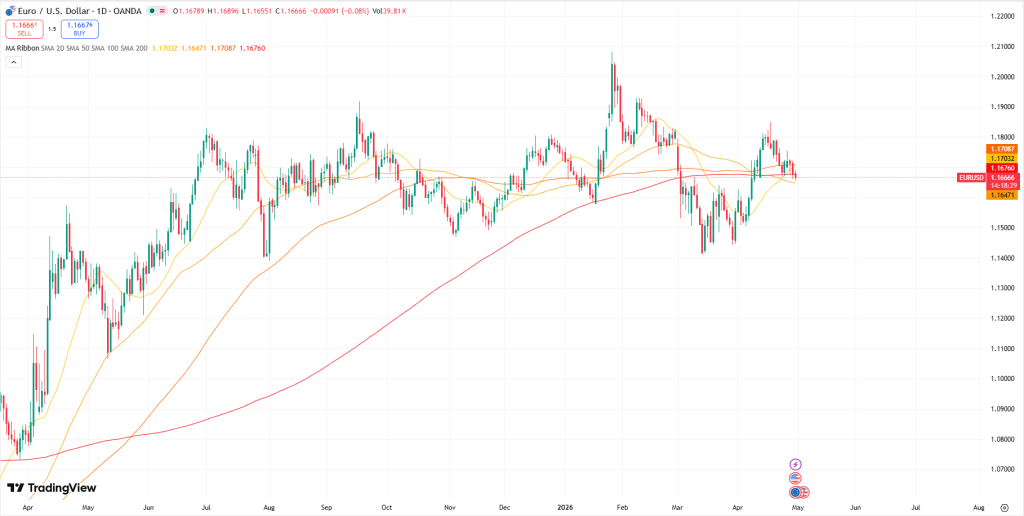

EUR/USD edged lower to around 1.1645 during Tuesday’s early Asian trading session as the US Dollar gained support from ongoing geopolitical uncertainty. President Trump said he had postponed a planned strike on Iran following requests from Gulf nations. Meanwhile, European Central Bank officials signaled that another interest rate hike could be needed to contain persistent inflation expectations.

EUR/USD remains under pressure near 1.1645 during Tuesday’s early Asian session as the Euro weakens against the US Dollar amid ongoing geopolitical uncertainty tied to Iran. Investors are also awaiting remarks later in the day from ECB Chief Economist Philip Lane.

US President Donald Trump stated that he had delayed a planned military strike on Iran following appeals from leaders of Qatar, Saudi Arabia, and the United Arab Emirates, noting that “serious negotiations are now taking place,” according to the BBC.

Still, market caution persists after Trump warned that the US could launch a “full, large-scale attack on Iran” at any time if negotiations fail to produce an acceptable agreement. Concerns over an extended Middle East conflict continue to support safe-haven demand for the US Dollar, weighing on the EUR/USD pair in the short term.

Meanwhile, hawkish rhetoric from European Central Bank officials may help limit losses for the Euro. ECB Governing Council member Yannis Stournaras said over the weekend that a moderate rate hike could help contain inflation without significantly harming economic growth.

A Reuters survey also showed that roughly 85% of economists expect the ECB to raise its deposit rate by 25 basis points to 2.25% in June, compared with just over half holding that view before the April policy meeting.

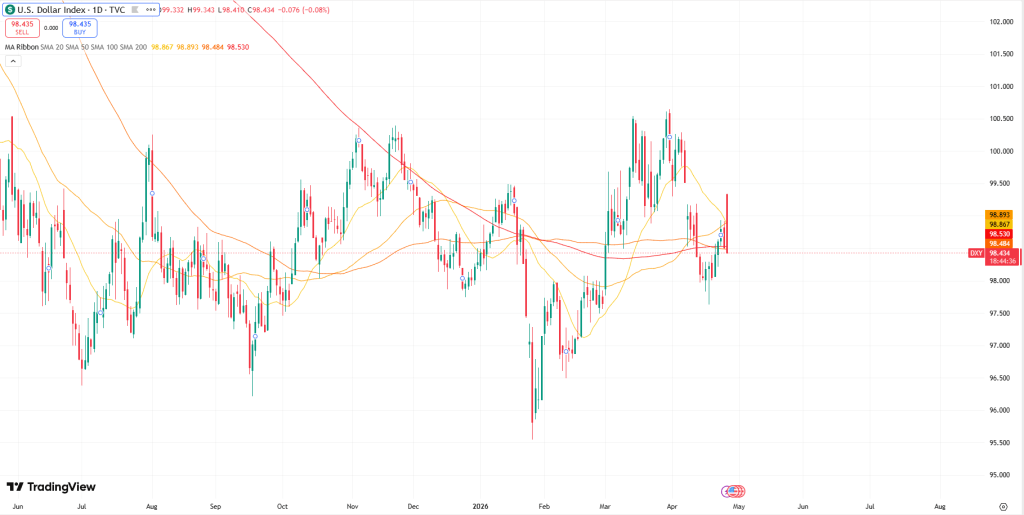

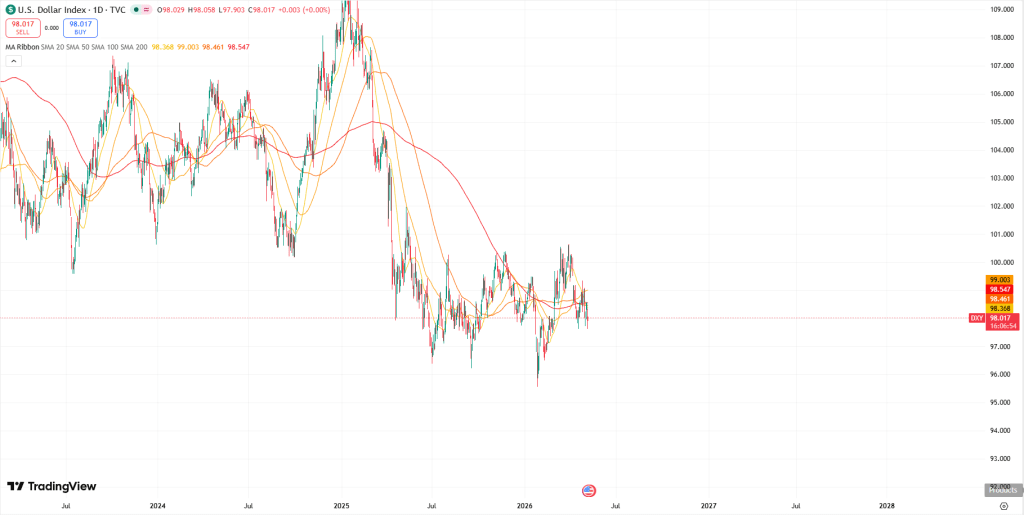

The US Dollar Index remains supported by growing expectations that the US Federal Reserve will maintain a more hawkish policy stance.

Meanwhile, the benchmark 10-year US Treasury yield briefly surged to 4.659% — its highest level since February 2025 — before pulling back to around 4.591%.

Geopolitical tensions also eased temporarily after President Trump postponed a planned military strike on Iran following requests from Gulf states.

The US Dollar Index (DXY), which tracks the US Dollar (USD) against a basket of six major currencies, edged higher during Tuesday’s Asian session, recovering after posting mild losses in the previous trading day and hovering near the 99.10 mark.

The Greenback found support from growing expectations that the US Federal Reserve (Fed) could maintain a more hawkish monetary policy stance. Overnight, the benchmark 10-year US Treasury yield climbed to 4.659% — its highest level since February 2025 — before easing back to around 4.591%. The spike in yields reflected investor concerns that persistently high energy prices may feed into consumer inflation, potentially forcing the Fed to keep interest rates elevated for longer.

Investors are also paying close attention to developments within the US central bank. According to Reuters, DRW Trading market strategist Lou Brien said recent market volatility has been driven by investors assessing how newly appointed Fed Chair Kevin Warsh will respond to inflationary pressures. Brien noted that markets are looking for reassurance that Warsh will uphold the Fed’s traditional policy mandate and remain independent from political influence coming from the White House.

Despite the Dollar’s strength, improving market sentiment limited safe-haven demand for the currency. Sentiment improved after US President Donald Trump announced a delay to a planned military strike on Iran. Reports indicated that Trump suspended the scheduled Tuesday attack after Persian Gulf allies urged Washington to allow more time for diplomatic negotiations. While the US administration stated it remains ready to act militarily if talks fail, officials have not provided a specific deadline for any potential action.

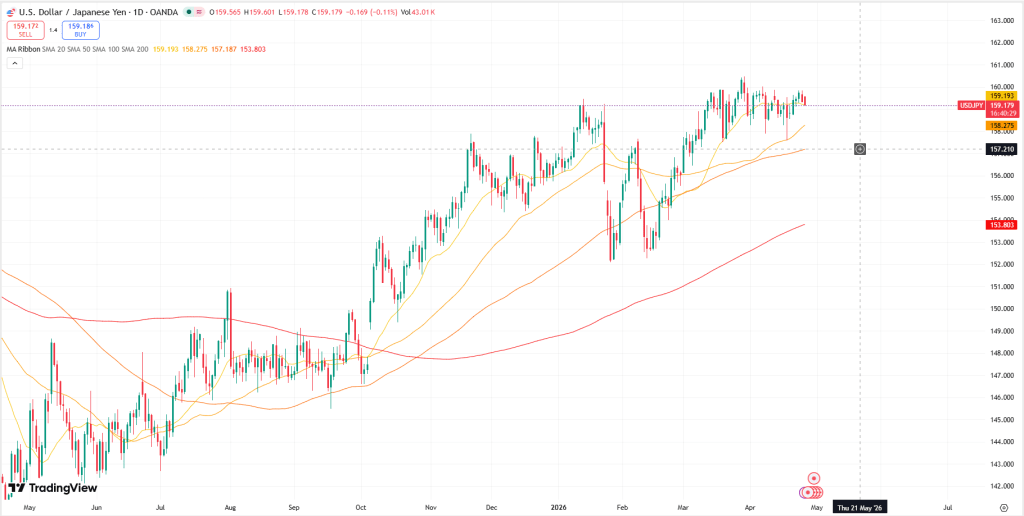

The US Dollar strengthened notably against the Japanese Yen during the week, climbing back above the key ¥158 level. The widening interest rate gap remains a primary factor driving the pair higher, as Japan continues to face limitations in tightening monetary policy too aggressively.

In many ways, this market continues to reward traders who hold US Dollars instead of Japanese Yen, largely due to the attractive yield advantage. The broader sentiment remains bullish, though traders should closely monitor the ¥160 region, as it has previously prompted intervention from Japan’s central bank.

EUR/USD

The Euro fell sharply during the week and now appears likely to move toward the lower end of the broader trading range that has been in place for months. A decline toward the 1.14 level would not be surprising, as that area has served as a major support zone since around March.

In the end, persistent high interest rates in the United States continue to support the bullish outlook for the US Dollar, keeping demand for the currency strong. At the same time, markets increasingly appear to be pricing in the risk of energy-driven inflation shocks across the global economy.

Natural Gas

Natural gas prices moved higher during the week, although the $3 level continues to stand out as a significant resistance zone. Selling into excessive bullish momentum still appears attractive, particularly if prices approach the $3 mark again.

I don’t view this as the beginning of a major or long-term move higher. Instead, it seems more like a short-term “fade the rally” setup, especially since this period of the year typically brings softer natural gas demand.

Crude Oil

The light sweet crude oil market posted strong gains during the week, although price action remains extremely volatile. That instability is likely to persist as traders continue reacting to geopolitical headlines and developments coming out of the Middle East.

Ongoing concerns surrounding energy inflation continue to shape market sentiment, with traders increasingly fearing that further economic pressure could lie ahead before conditions improve. Global markets are also beginning to feel the impact of reduced Middle Eastern oil flows, as previously stored supplies on tankers are gradually being depleted. As a result, crude oil is likely to remain a highly volatile and unpredictable market in the near term.

Bitcoin

Bitcoin declined over the course of the week, but the broader bullish pressure remains intact as the market continues to test higher levels. Notably, Bitcoin showed relative strength while many other assets struggled, marking a shift from its behavior in previous periods when it often moved lower alongside broader market weakness.

Despite elevated interest rates, Bitcoin’s resilience has been difficult to ignore. Under normal circumstances, the market could have experienced a much deeper pullback months ago, yet buyers have consistently stepped in to support prices. Sometimes it is more important to focus on what the market is actually doing rather than what it is theoretically supposed to do, and right now Bitcoin still appears to be attracting buyers.

Gold

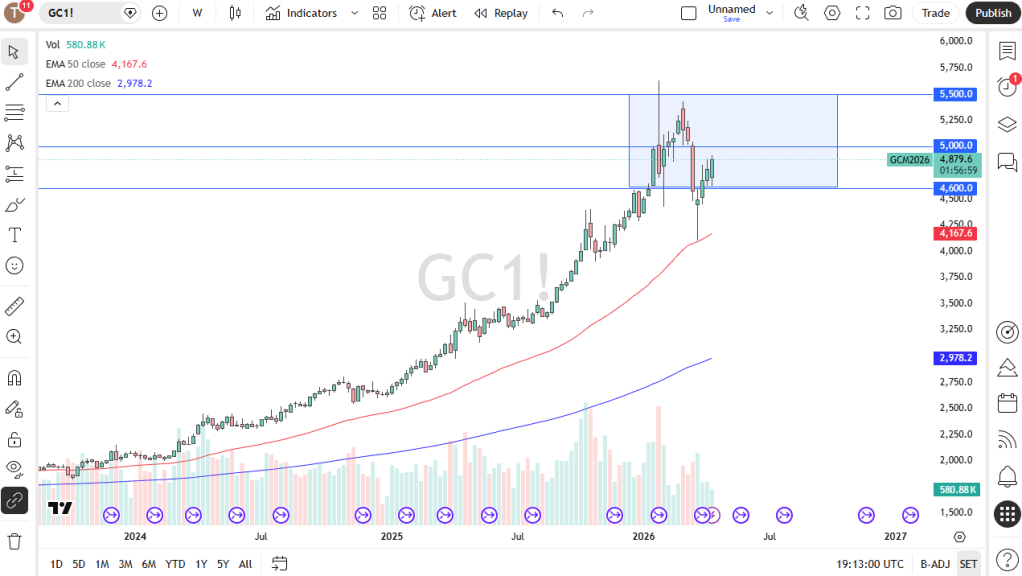

Gold prices came under heavy selling pressure during the week, and continued increases in interest rates are likely to remain a major headwind for the market. With prices now trading below the $4,600 level, attention is shifting toward the $4,500 area as the next key support zone.

A break below the $4,500 level could pave the way for a deeper decline toward the 50-week EMA. On the upside, short-term rebounds are likely to face resistance near the $4,800 region, and as long as US 10-year Treasury yields remain elevated, gold may continue to encounter selling pressure.

Silver

Silver endured a very difficult week after initially appearing ready for a major breakout higher. However, the $90 level once again acted as strong resistance, effectively halting the rally. Rising interest rates in the United States have continued to weigh heavily on silver prices, which has historically been a negative factor for the metal over the longer term.

Silver is now forming a very bearish-looking weekly candlestick pattern, which could signal additional downside pressure ahead. A decline back toward the $70 level would not be surprising, as that area has previously served as a major support zone. Overall, silver remains an extremely risky and volatile market at the moment.

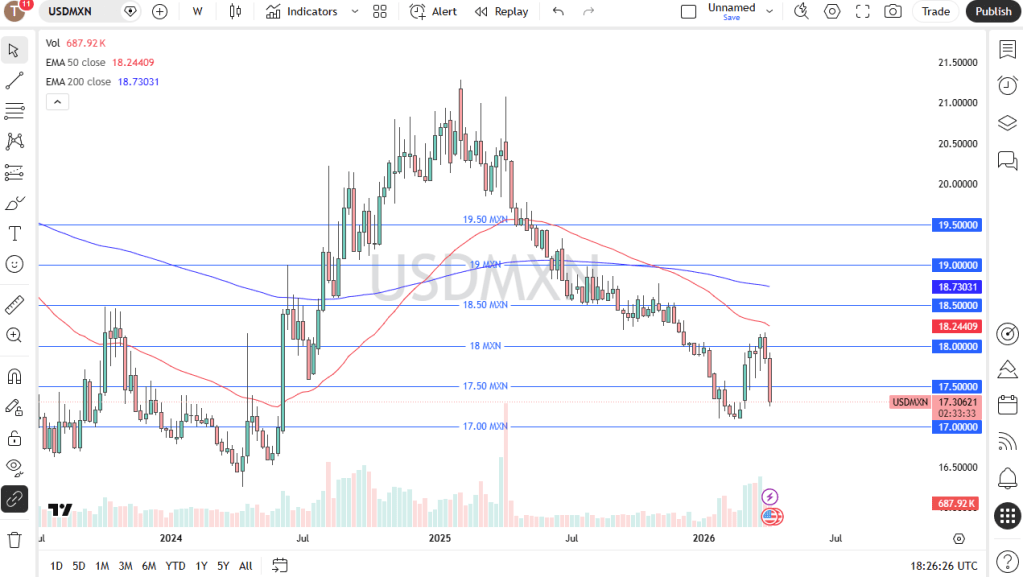

USD/MXN

The US Dollar strengthened against the Mexican Peso during the week, although the pair remains stuck within the broader consolidation range that has been in place for some time. The 17.50 level continues to act as a major resistance barrier, while the 17.20 area underneath provides important support.

The pair is likely to remain range-bound for now, as the stronger US Dollar is being offset by the attractive interest rate differential offered by the Mexican Peso. While the Dollar has been gaining against many currencies, the yield advantage in Mexico still encourages traders to sell rallies in USD/MXN. As a result, the market may continue moving sideways until broader macroeconomic uncertainties become clearer.

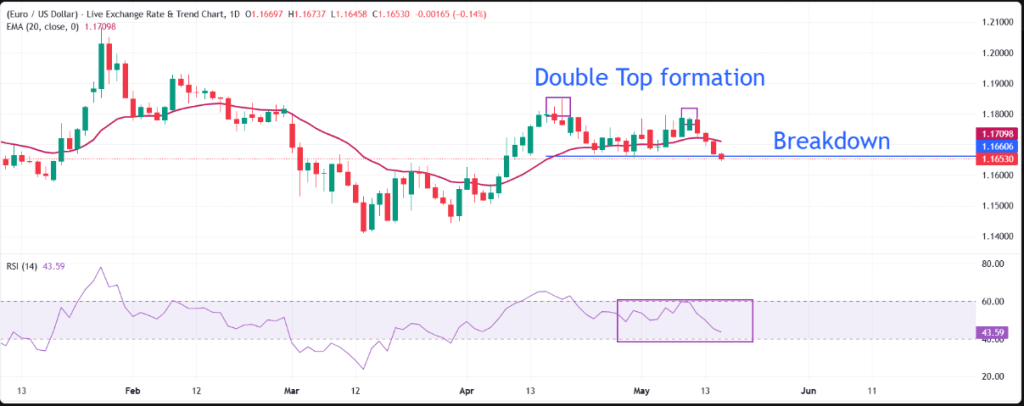

EUR/USD declines further toward 1.1655 as the US Dollar continues to strengthen amid several supportive factors.

Both the US and China maintain that the Strait of Hormuz should remain open.

The Federal Reserve is expected to keep interest rates unchanged this year.

The EUR/USD pair continues its decline for a fourth consecutive session on Friday, slipping 0.15% to around 1.1653 during Asian trading hours. The pair remains under pressure as the US Dollar (USD) strengthens further after encouraging developments from Thursday’s meeting between United States (US) President Donald Trump and Chinese President Xi Jinping.

At the time of writing, the US Dollar Index (DXY), which measures the Greenback against a basket of six major currencies, is up 0.15% near 99.00, marking its highest level in two weeks.

Remarks from both Trump and Xi suggested improving trade relations between the US and China, while both leaders also emphasized the importance of keeping the Strait of Hormuz open.

The US Dollar is also drawing support from growing expectations that the Federal Reserve (Fed) will keep interest rates unchanged throughout this year.

Meanwhile, in the Eurozone, most economists surveyed by Reuters expect the European Central Bank (ECB) to implement an interest rate hike at its June policy meeting.

Technical Analysis

EUR/USD remains under pressure around 1.1653 during the Asian session, with the pair maintaining a bearish short-term outlook as it trades below the 20-day Exponential Moving Average (EMA) at 1.1710. A confirmed breakdown of the Double Top pattern after falling beneath the April 30 low at 1.1655 signals the potential for further downside extension.

Meanwhile, the Relative Strength Index (RSI) near 44 continues to point lower, suggesting bearish momentum remains active and selling pressure has not yet faded.

To the upside, the first resistance level is seen at the 20-day EMA around 1.1710. A move back above this zone could reduce near-term bearish pressure and support a broader recovery toward 1.1800. On the downside, key support levels are located at the April 8 low of 1.1589 and the April 6 low near 1.1505.

The US Dollar Index strengthened after April Retail Sales rose 0.5% month-over-month, surpassing market expectations. Meanwhile, Stephen Miran’s resignation from the Fed Board has paved the way for Kevin Warsh to take over as Federal Reserve Chair. At the same time, President Trump said US-China relations could become “better than ever,” while Chinese President Xi signaled a willingness to help ease tensions surrounding the Iran conflict.

The US Dollar Index (DXY), which tracks the US Dollar (USD) against a basket of six major currencies, extended its rally for a fifth straight session, trading near 99.10 during Friday’s Asian session.

The Greenback strengthened after the release of solid US Retail Sales data, which showed a 0.5% month-over-month increase in April, highlighting the resilience of US consumer spending despite persistently high borrowing costs.

Support for the US Dollar also came from developments within the Federal Reserve, as Stephen Miran’s resignation from the Board of Governors has opened the door for Kevin Warsh to become the next Fed Chair.

At the same time, rising inflationary pressures tied to escalating Middle East tensions have strengthened expectations that the Fed could keep interest rates elevated for longer or potentially raise them further.

Meanwhile, US President Donald Trump said on Thursday that he hopes relations with China will become “stronger and better than ever before,” adding that President Xi had offered support in helping ease tensions surrounding the Iran conflict. The improving diplomatic tone boosted market risk sentiment, which typically limits demand for the US Dollar’s safe-haven appeal.

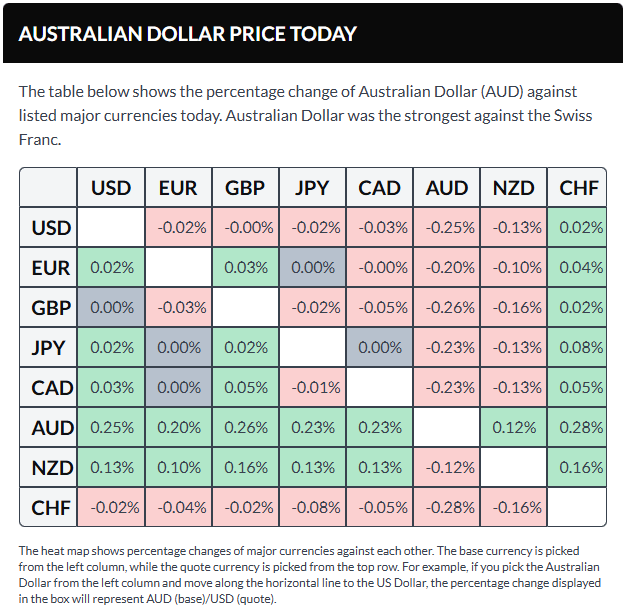

AUD/USD eases to near 0.7250 during Thursday’s Asian trading session.

US producer inflation unexpectedly posted its sharpest increase in four years.

Donald Trump is set to meet with Xi Jinping in China for a closely watched high-level discussion.

The AUD/USD pair declines toward 0.7250 during Thursday’s Asian session as stronger-than-expected US inflation figures lend support to the US Dollar against the Australian Dollar. Investors are also keeping a close eye on the summit between US President Donald Trump and Chinese President Xi Jinping in Beijing, along with the upcoming release of US April Retail Sales data later in the day.

US producer inflation recorded its strongest annual increase in four years in April, reinforcing demand for the Greenback. According to data published by the US Bureau of Labor Statistics on Wednesday, the Producer Price Index (PPI) climbed 6.0% year-over-year, up from 4.3% previously. On a monthly basis, PPI advanced 1.4% in April after rising 0.7% in March, significantly exceeding market expectations of 0.5%.

Market participants are now turning their attention to Thursday’s US Retail Sales report. Economists forecast retail sales growth of 0.5% month-over-month in April, following a 1.7% increase in March. Stronger-than-anticipated data could further strengthen the US Dollar and weigh on the AUD/USD pair.

Meanwhile, Bloomberg reported Wednesday that Trump arrived in Beijing for an official state visit, where he is expected to meet Xi Jinping to discuss trade relations and the conflict involving Iran. The trip marks the first state visit to China by a US president in nearly a decade. Any constructive outcomes from the US-China discussions may support the Australian Dollar, given Australia’s close trade ties with China.

The US Dollar Index remained steady as President Trump’s remarks on the Middle East fueled geopolitical uncertainty and market volatility. Hotter-than-expected CPI figures reinforced expectations that the Federal Reserve may keep interest rates elevated for longer to contain persistent inflation pressures. Investors are now turning their attention to upcoming producer inflation data for further clues on how the conflict with Iran is affecting the broader US economy.

The US Dollar Index (DXY), which tracks the Greenback against a basket of six major currencies, held steady near 98.30 during Wednesday’s Asian session after posting gains over the previous two days. The US Dollar continued to draw support from escalating geopolitical tensions in the Middle East following recent remarks by President Donald Trump. Although Trump stated that Iran was “under control,” he warned that the situation would ultimately end either with a new agreement or with complete “decimation.” Meanwhile, Iranian Deputy Foreign Minister Kazem Gharibabadi reiterated that any acceptable peace deal must involve reparations, recognition of Iran’s sovereignty over the Strait of Hormuz, and the full removal of US sanctions.

Additional support for the Greenback came from stronger-than-expected US inflation data, which reinforced hawkish expectations for the Federal Reserve. Investors increasingly believe the Fed will keep interest rates elevated for longer in an effort to contain persistent inflationary pressures. According to data released by the Bureau of Labor Statistics on Tuesday, the US Consumer Price Index (CPI) rose 0.6% month-over-month in April, lifting annual inflation to 3.8%, the highest reading since May 2023. Core CPI, which excludes food and energy prices, also increased, posting a 2.8% annual gain.

With expectations for a Fed rate cut this year largely fading, markets are now pricing in the possibility of a quarter-point rate hike by December. Attention is now turning to upcoming producer inflation figures, which could offer further insight into how the ongoing conflict involving Iran is affecting the broader US economy.

USD/CAD advances as escalating Middle East tensions strengthen the US Dollar’s appeal as a safe-haven currency.

President Trump has expressed growing frustration over the lack of progress in peace negotiations, raising concerns about a possible change in the region’s conflict approach.

Meanwhile, higher oil prices provide support for the Canadian Dollar, though they also create challenges for the Bank of Canada by adding to ongoing inflation pressures.

USD/CAD edges higher after closing nearly unchanged in the previous session, hovering around 1.3690 during Tuesday’s Asian trading hours. The pair is regaining upward momentum as the US Dollar strengthens amid escalating geopolitical tensions.

Investor sentiment has shifted toward safe-haven assets following reports of worsening diplomatic conditions in the Middle East. Markets are increasingly pricing in the risk of renewed large-scale military conflict, a development that typically drives demand for the Greenback against more risk-sensitive currencies.

A CNN report published Monday stated that US President Donald Trump has become increasingly dissatisfied with the lack of progress in negotiations aimed at ending regional hostilities. Sources close to the administration indicated that Washington is now giving more serious consideration to renewed military operations. Adding to market concerns, Iranian Parliament Speaker Mohammad Bagher Ghalibaf said, according to Reuters, that Iran’s armed forces are fully prepared to respond to any future attacks, placing the already fragile ceasefire under additional pressure.

Despite broad USD strength, the Canadian Dollar continues to receive support from rising oil prices. As Canada is the largest crude supplier to the United States, the CAD tends to benefit from gains in energy markets. Concerns that escalating regional tensions could disrupt global supply flows and reduce Middle Eastern exports have pushed crude prices sharply higher, helping cap further upside in USD/CAD.

At the same time, surging energy prices are reviving inflation concerns in Canada. March inflation data already reflected the impact of volatile oil prices, with annual CPI rising to 2.4%, the highest level seen in a year. While elevated crude prices generally strengthen the CAD, they also complicate the Bank of Canada’s policy outlook. Although the BoC recently kept interest rates unchanged and suggested that energy-related inflation may remain temporary, a prolonged geopolitical conflict could eventually force policymakers to reconsider their current stance.

After reaching a peak near 1.36450 on Wednesday, GBP/USD closed the week around 1.36274. The pair has largely mirrored broader FX market movements, tracking shifts in USD-driven sentiment across different trading sessions.

With WTI crude oil volatility easing and market risk appetite improving, the US dollar has remained under mild pressure. This USD weakness has helped support GBP/USD, which continues to hold above levels seen prior to the early-March Iran-related escalation.

From a technical standpoint, the pair is now approaching territory last traded around the 16–17 February period, suggesting a potential retest of earlier resistance zones as broader sentiment and risk conditions evolve.

Dynamic Range in GBP/USD

The opening of trading for GBP/USD on Monday is likely to be shaped by prevailing market sentiment surrounding the Middle East conflict, which remains relatively calm but still fragile. Alongside this, attention may also turn to reactions from the UK local elections held late last week.

In those results, the Labour Party performed poorly, a development that reflects negatively on its current leadership and raises questions about internal stability. Market participants and financial institutions could respond to these political outcomes at the start of the week, potentially adding an additional layer of volatility to GBP/USD price action on Monday.

Although the leadership of the Labour Party may come under renewed scrutiny, it will also be important to observe whether financial institutions interpret the election outcome as validation of their existing expectations about the UK’s political trajectory.

For short-term traders, the key takeaway is that GBP/USD could see heightened volatility at the start of Monday’s session. As London markets open, price action may become more dynamic as participants react to both political developments and broader sentiment shifts.

Higher Marks in GBP/USD and Correlation Outlook

The GBP/USD may continue to trade with an upward bias in the coming sessions if broader market sentiment keeps the US dollar in a relatively weaker phase across the global FX space. Under such conditions, dollar softness would likely continue to support additional buying interest in the pound.

From a technical perspective, traders may look back toward early-February price levels as potential reference points or interim targets. However, the 1.37000 region still appears to be a more distant objective rather than an immediate trading focus.

For intraday participants, restraint remains important. Rather than chasing extended upside moves, it may be more practical to focus on nearer, more realistic price zones that sit within the day’s typical volatility range, helping to avoid exposure to sharp reversals.

There is also a case for caution around the London open, where institutional flows can introduce abrupt price adjustments, particularly as market participants reassess positioning in light of recent UK political developments.

Although the current government remains in place, market sentiment increasingly reflects speculation about potential political change ahead. Still, GBP/USD pricing is likely to remain anchored in medium-term expectations, which continue to incorporate the existing policy direction and mandate of the current administration.

GBP/USD Weekly Outlook

The current conditions shaping GBP/USD continue to create active two-way price dynamics that appeal to short-term traders. The pair offers frequent opportunities for positioning, though volatility remains a defining feature rather than a stabilizing force.

After the initial activity of Monday’s open fades, trading conditions may settle somewhat. However, market participants still need to account for the risk of sudden catalysts, including developments related to Middle East tensions and ongoing domestic political uncertainty in the UK, both of which could quickly shift sentiment.

From a technical standpoint, GBP/USD holding above the 1.36300–1.36400 area in early Monday trade would likely be viewed as constructive. Sustained stability above this zone could encourage larger market participants to maintain or extend bullish positioning in the days ahead.

That said, even institutional flows remain vulnerable to abrupt sentiment shifts. With global FX conditions still influenced by uneven risk appetite and intermittent geopolitical headlines, the market is unlikely to settle into a smooth trend environment just yet.

The US Dollar Index strengthened as rising risk aversion followed the rejection of each other’s latest peace proposals by President Trump and Iran.

President Trump dismissed Iran’s latest peace offer, describing it as “totally unacceptable.”

Meanwhile, US Nonfarm Payrolls increased by 115K in April, surpassing market expectations despite easing from March’s revised 185K gain.

The US Dollar Index (DXY), which tracks the US Dollar (USD) against a basket of six major currencies, remained firm after posting modest losses in the previous session, trading near 98.10 during Monday’s Asian session.

The Greenback continued to strengthen amid heightened risk aversion after US President Donald Trump and Iran rejected each other’s latest peace efforts aimed at easing tensions in the Middle East. According to Bloomberg, Trump dismissed Iran’s recent peace proposal on Sunday, calling it “totally unacceptable.” Meanwhile, Iranian state television cited an Iranian official as saying Tehran’s response focused on ending the conflict across all fronts, especially in Lebanon, while also addressing the security of shipping lanes through the strait, although no specifics were given regarding the reopening of the crucial waterway.

Ongoing tensions in the Middle East, along with the fragile ceasefire between the US and Iran, are likely to sustain safe-haven demand for the US Dollar, which could continue to pressure major currency pairs in the near term.

Data released by the US Bureau of Labor Statistics on Friday showed that Nonfarm Payrolls (NFP) increased by 115K in April, slowing from March’s revised 185K gain but still beating market expectations of 62K. Meanwhile, the Unemployment Rate held steady at 4.3% in April, in line with analyst forecasts.

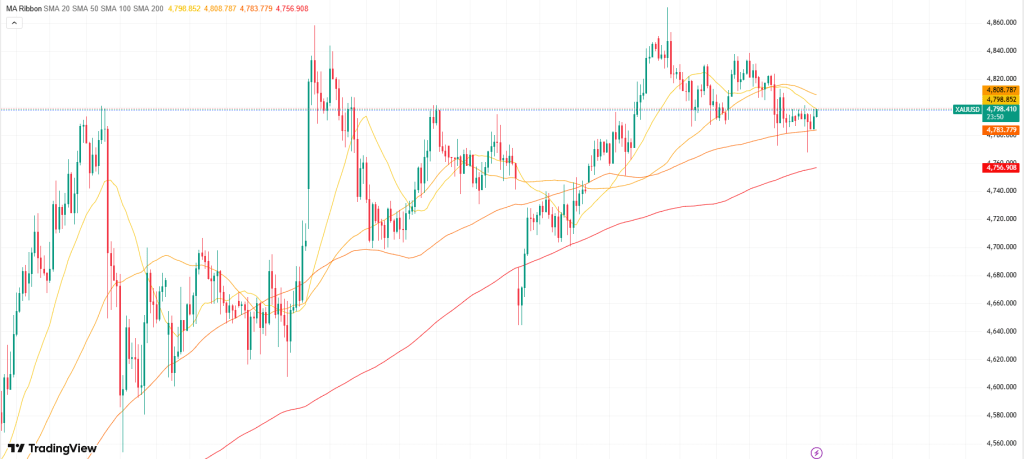

The gold market initially pulled back during the week but later rebounded and regained strength. The $4,600 level remains a key area to watch closely, as it has repeatedly acted as both support and resistance in the past.

Gold still appears to have solid potential to gradually move higher, although interest rate markets continue to create headwinds. In this environment, gold is likely to remain volatile and range-bound in the short term. Despite that, the longer-term outlook still looks strongly bullish, and I believe the market could eventually reach the $5,000 level. However, that would likely require several supportive factors to align, including a de-escalation of tensions in the Middle East.

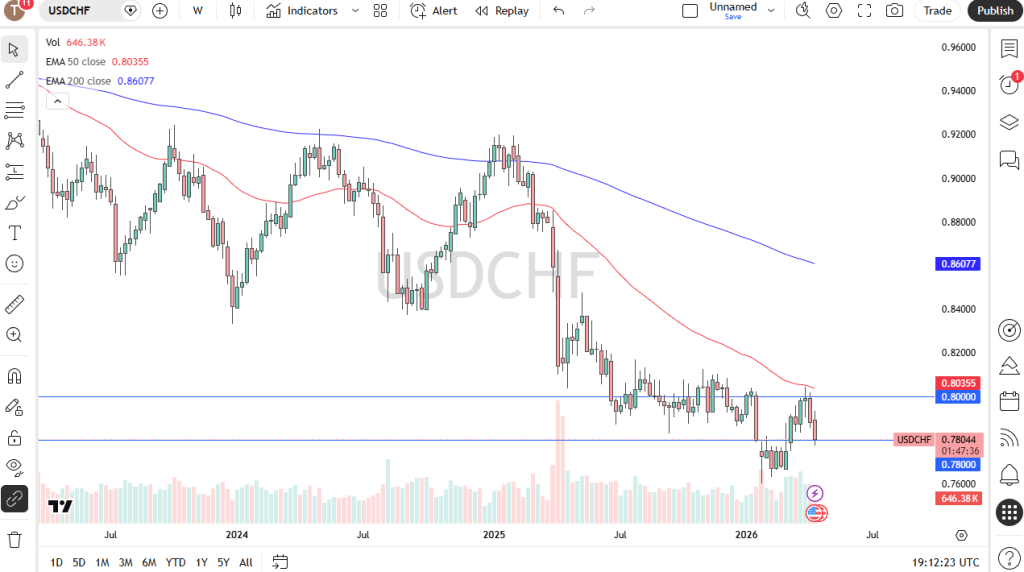

USD/CHF

The US dollar initially strengthened against the Swiss franc but has since pulled back quite sharply. The pair is now testing a potential support zone around the 0.7750 level. Among the major currency pairs, this is one where I still favor the US dollar over the longer term. However, falling interest rates and growing concerns that geopolitical conflicts could escalate are boosting demand for safe-haven assets like the Swiss franc.

Ironically, if geopolitical tensions ease and peace returns, interest rates in the United States may decline, but demand for the safe-haven Swiss franc would likely weaken as well. As a result, this pair is expected to remain heavily influenced by headlines and market sentiment. Over the longer term, however, I still believe USD/CHF has room to move higher.

EUR/USD

The euro initially moved lower before rebounding and showing renewed strength. However, the pair continues to face strong resistance around the 1.18 level, extending up to 1.1850. The 1.1850 zone has remained a significant area of selling pressure, keeping the market contained since the summer of last year.

Going forward, we will need to see whether EUR/USD can finally break above this resistance zone, especially since the pair has attempted to do so several times already. Each breakout attempt, however, has been met with heavy selling pressure that quickly pushes the market back down. For now, I suspect the broader trading range will continue to hold.

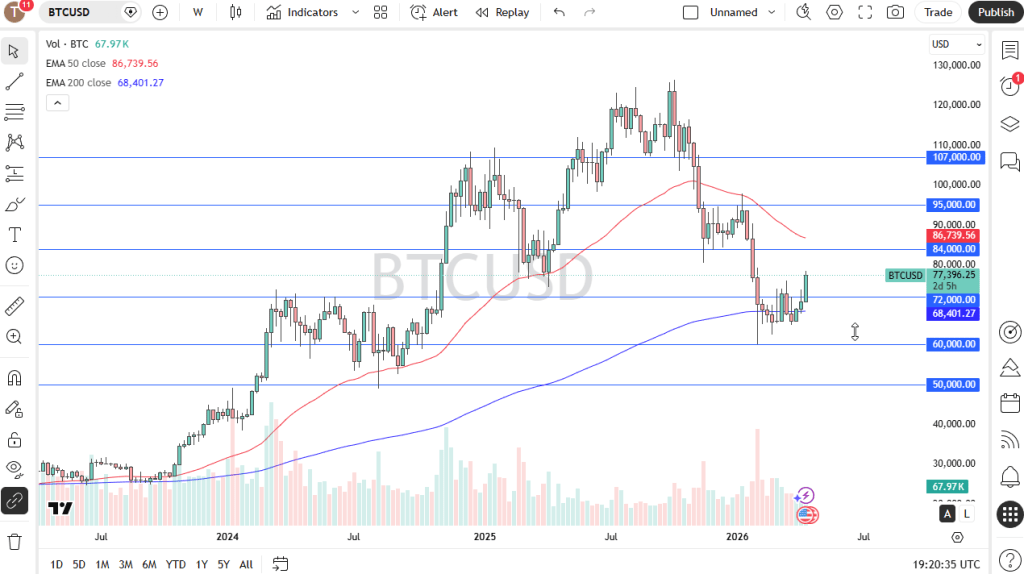

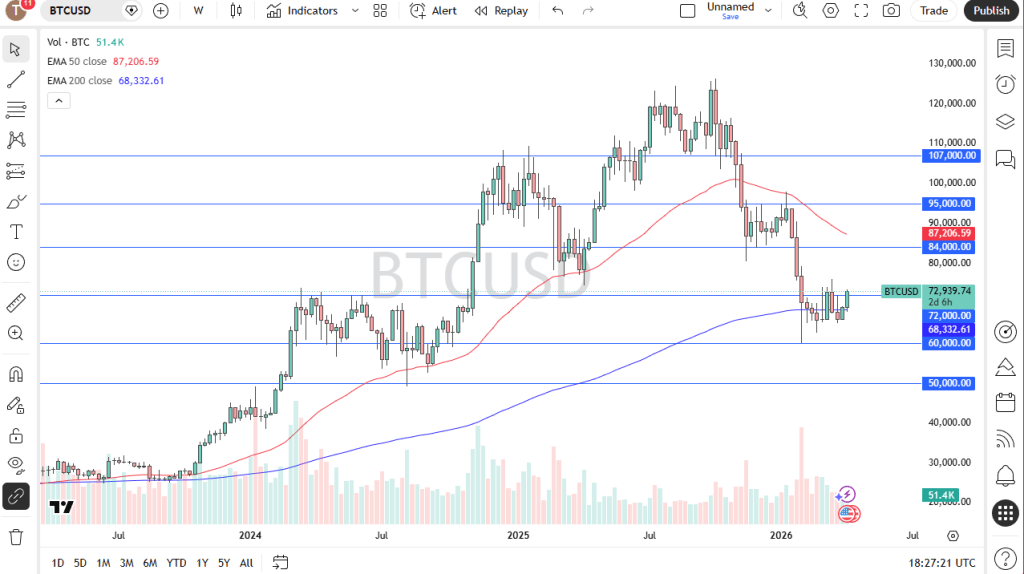

BTC/USD

Bitcoin moved higher during the week but later surrendered part of its gains. Even though the latest candlestick resembles a shooting star, it is important to note that the previous candle formed a hammer pattern. This combination suggests that Bitcoin could enter a period of sideways consolidation in the near term.

A break above the $84,000 level would be a strong bullish signal and could pave the way for a much larger upward move. In the meantime, I believe short-term pullbacks will likely continue to attract buyers, with many traders viewing dips as potential buying opportunities.

USD/ZAR

If you were searching for volatility, the South African rand certainly delivered during the week. The pair initially attempted to move higher, but later turned lower as the US dollar continued to weaken. That remains the key theme in this market — traders are likely to keep selling into short-term rallies, especially as the interest rate differential continues to favor South Africa and is expected to do so for the foreseeable future.

With that in mind, I believe the market will likely drift back toward the 16.20 level over time, although the move is expected to be gradual rather than aggressive. In the end, this remains more of a carry trade environment, where traders are primarily focused on earning positive swap returns.

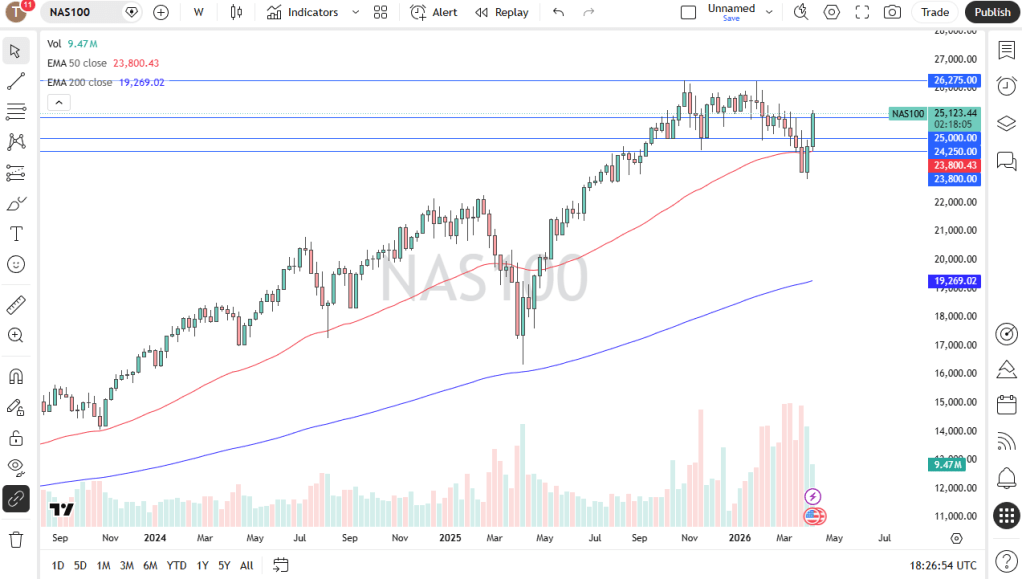

NASDAQ 100

The Nasdaq 100 continues to defy gravity and now appears extremely overbought. The index remains locked in a remarkably strong uptrend, but sooner or later, a sizable pullback is likely to occur — one that could catch overly aggressive or greedy traders off guard.

That said, I believe the 28,000 level will be a key area to watch, as many traders are likely to look for signs of support and renewed buying interest if the market pulls back toward that zone.

USD/MXN

The US dollar has remained weak against the Mexican peso for quite some time. The 17.50 level continues to act as a significant resistance barrier, as it has repeatedly attracted strong selling pressure in the past. Overall, the pair still appears to be trapped within a broader trading range, with support near 17.20 and resistance around 17.50.

Ultimately, I believe that if USD/MXN can break above the highs of the last two weekly candlesticks, it could open the door for a move toward the 18.00 level. However, such a rally would likely require a broader risk-off or fear-driven market environment. For now, the overall setup still appears to favor a “sell the rally” approach rather than a sustained bullish trend.

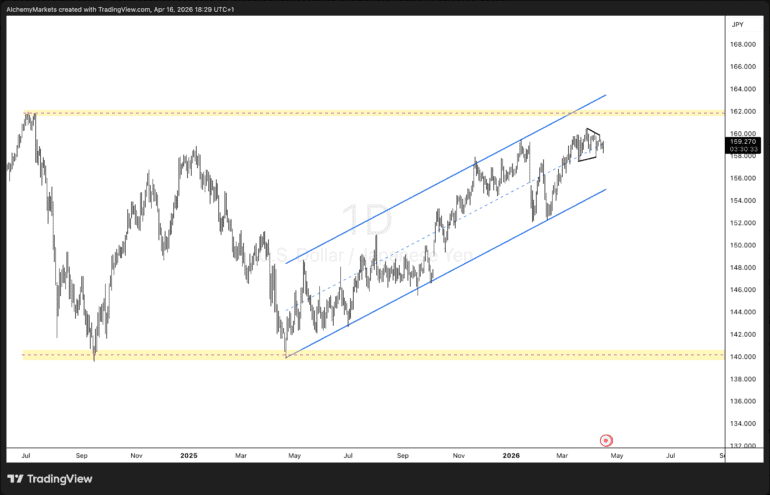

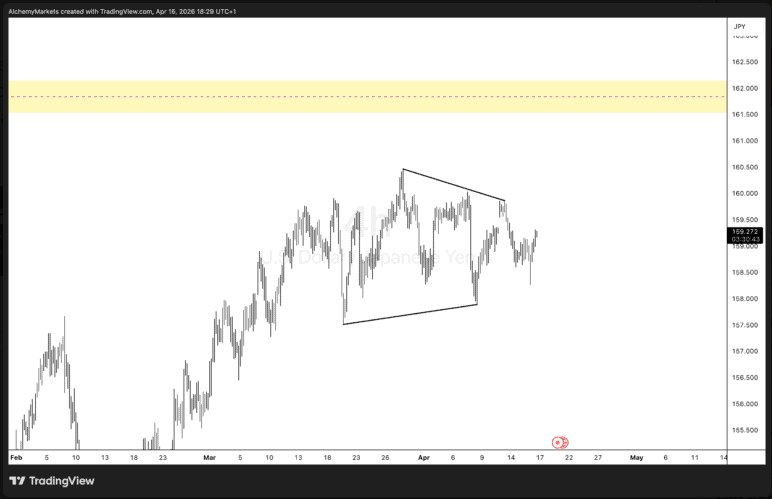

USD/JPY

The US dollar traded in a highly volatile manner against the Japanese yen throughout the week, following last week’s intervention by the Bank of Japan.

That said, the pair is beginning to form a candlestick pattern that suggests stabilization, indicating there is a genuine possibility of another move higher. A breakout above the 160.50 level — or potentially even the 162.00 region — could pave the way for fresh multi-decade highs, with resistance levels stretching back to 1990.

USD/JPY is trading in a subdued manner near 157.00 during Friday’s Asian session, extending its overnight recovery in line with the US Dollar’s rebound. However, gains remain limited as markets stay cautious about the risk of Japanese FX intervention. Investors are also holding back ahead of the US April employment report due later in the day.

USD/JPY Technical Analysis Overview

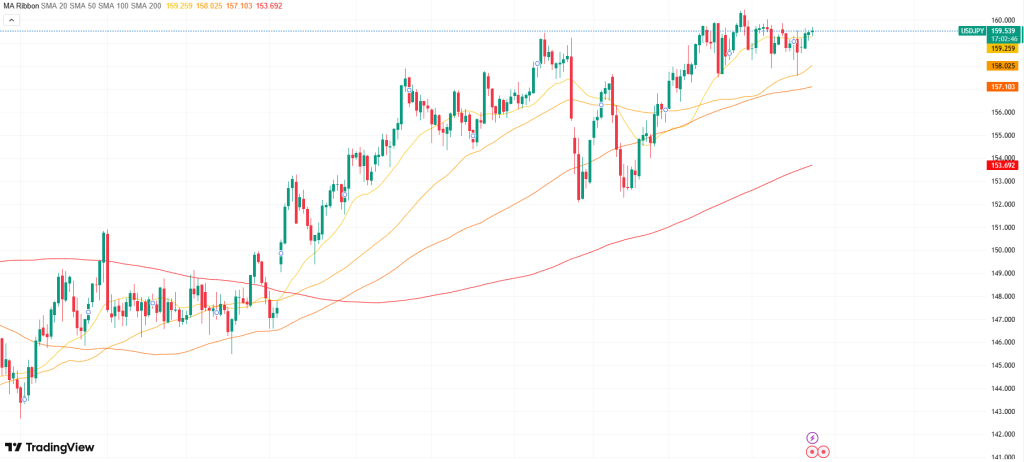

On the 15-minute chart, USD/JPY is trading around 159.62, staying above the session open at 159.36. This keeps a slight intraday bullish tone intact as price continues to edge higher within a narrow consolidation range. The Stochastic RSI is positioned near the mid-50s, indicating improving upward momentum without entering overbought territory, which suggests buyers still retain short-term control.

Immediate support is located at 159.36, the day’s open. A break below this level could trigger a deeper pullback toward earlier intraday lows. Although no major moving averages are active on this timeframe, the pattern of higher closes continues to favor buying on dips as long as the pair holds above 159.36.

On the daily chart, USD/JPY also trades at 159.62 and maintains a constructive bullish outlook. Price remains firmly above the 50-day EMA at 158.44 and the 200-day EMA at 155.10, preserving the broader uptrend structure. The Stochastic RSI has recovered toward mid-range levels, reflecting renewed upside momentum after a phase of consolidation within the ongoing bullish trend.

Key support is seen at the 50-day EMA around 158.44, where a pullback would still be consistent with the broader uptrend as long as the 200-day EMA at 155.10 holds. A daily close below the 50-day EMA would signal a potential shift toward a deeper correction, while sustained trading above current levels keeps the bullish structure intact and leaves room for another attempt at recent highs.

Fundamental Analysis Overview

Recent comments follow a series of warnings from Japan’s Ministry of Finance. Finance Minister Satsuki Katayama reiterated last week that authorities are prepared to act against excessive speculative movements in the yen. This stance has kept markets alert after recent sharp swings in USD/JPY, which many participants interpret as possible signs of official intervention.

At the same time, the Bank of Japan’s (BoJ) March meeting minutes, released on Thursday, revealed that several policymakers see room for further interest rate hikes if the energy shock from the US-Iran conflict persists and leads to broader inflationary pressures. Some members also suggested that Japan may need to gradually move away from deeply negative real interest rates.

This increasingly hawkish tone from the BoJ has strengthened expectations for a potential rate increase as early as June. However, analysts remain cautious, noting that sustained support for the yen would likely require either lower US Treasury yields or easing oil prices in addition to tighter domestic policy.

Strategists at OCBC, including Sim Moh Siong and Christopher Wong, suggest that recent USD/JPY fluctuations resemble intervention activity, with the perceived intervention threshold now around 158 rather than 160. They also note that further action could drive the pair toward the 150–155 range, though they emphasize that intervention alone may not be sufficient to change the broader trend without a stronger shift in BoJ policy.

In the US, attention is shifting to Friday’s April employment data. Forecasts point to around 60,000 new Nonfarm Payrolls, with unemployment expected to remain steady at 4.3%. Weekly Initial Jobless Claims, due earlier on Thursday, will also be closely monitored for additional labor market signals.

Meanwhile, the US Dollar Index (DXY) remains under pressure, hovering near two-month lows around 97.90. Markets continue to anticipate a more dovish Federal Reserve outlook, which is limiting the dollar’s upside potential against the yen.

GBP/USD rose to 1.3599 on Thursday, with the pound briefly touching its strongest levels since mid-February. Sterling’s advance was supported by ongoing US dollar weakness, as demand for the greenback’s safe-haven status eased amid increasing optimism over a potential US–Iran agreement.

Axios reported that the White House is nearing a framework memorandum with Iran, which could open the door to ending the conflict and beginning nuclear negotiations. Tehran is expected to respond within 48 hours, though a final deal has not yet been reached.

Meanwhile, investors are watching UK local elections closely, with polling indicating potential setbacks for Keir Starmer’s party.

On the monetary policy side, expectations for the Bank of England have been adjusted, with markets now pricing in around 50 basis points of tightening by year-end—roughly two rate hikes—down from earlier expectations of up to three increases.

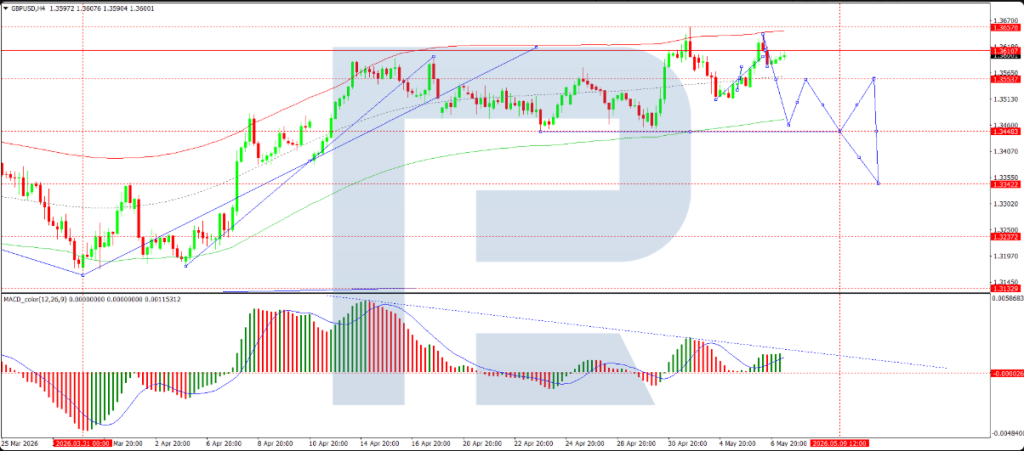

Market technical review

On the H4 timeframe, GBP/USD is moving within a wide consolidation band above 1.3515, with price action currently stretching toward 1.3650. A pullback toward 1.3344 is still on the table before any further range-bound movement resumes. A decisive break to the upside would expose the 1.3650 area again, while a break lower could accelerate declines toward 1.3344. The MACD also aligns with this outlook, as the signal line remains above the zero line but is turning downward, suggesting weakening bullish momentum.

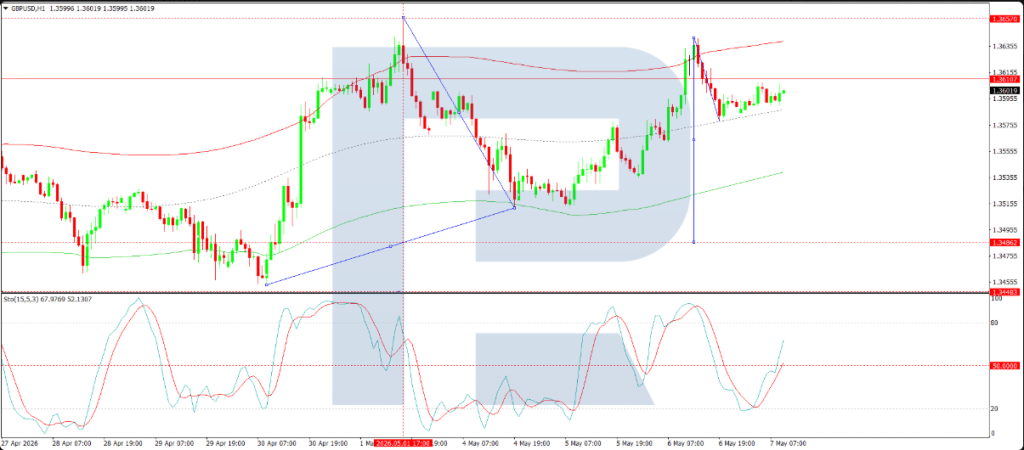

On the H1 timeframe, GBP/USD is consolidating in a tight range around 1.3615. Price has recently extended lower toward 1.3578 and is now attempting a recovery back to 1.3615 for a potential retest from below. This rebound may be short-lived, with a further decline toward 1.3565 still likely. The Stochastic oscillator supports this bearish short-term bias, with the signal line below 50 and trending down toward 20, indicating rising downside pressure.

Conclusion

The pound continues to find support from improved global risk sentiment and weaker demand for the US dollar as a safe-haven asset. However, ongoing political uncertainty in the UK, along with evolving expectations for Bank of England policy, may cap further gains. In the near term, GBP/USD is expected to remain highly reactive to geopolitical developments and shifts in broader market sentiment.

USD/JPY slips toward 156.85 in Friday’s Asian session, pressured by renewed reports of Japanese FX intervention during the May holidays. Market attention now shifts to the US April employment report, which is expected to be the key macro driver for the session.

USD/JPY weakened to around 156.85 during Friday’s Asian session as the Japanese yen gained strength after reports of another round of FX intervention by Japanese authorities. Traders also turned cautious ahead of the upcoming US April employment data.

According to Reuters, citing a familiar source, Japanese officials reportedly intervened in the FX market during the early May holiday period, following yen-buying operations on April 30. The source noted that “the intervention since the start of May was timed to coincide with the holiday period, when market liquidity was thin.”

Expectations of further intervention may continue to support the yen and weigh on USD/JPY. Japan’s top foreign exchange official Atsushi Mimura also stated on Thursday that authorities stand ready to respond to speculative currency moves across all fronts.

Attention now shifts to the US April jobs report, due later on Friday. Markets expect around 62,000 new jobs, a notable slowdown from March’s 178,000 increase, while the unemployment rate is forecast to remain unchanged at 4.3%.

Nonfarm Payrolls are forecast to increase by 62K in April, while the Unemployment Rate is expected to remain unchanged at 4.3%. The USD could face elevated volatility ahead of the weekend.

The United States Bureau of Labor Statistics is set to release the April Nonfarm Payrolls (NFP) report on Friday at 12:30 GMT, with markets closely watching the data for clues on the Federal Reserve’s interest-rate path later this year.

Economists expect the US economy to add 62K jobs in April, a sharp slowdown from March’s stronger-than-expected 178K gain. The Unemployment Rate is forecast to remain steady at 4.3%, while annual wage growth, measured by Average Hourly Earnings, is seen accelerating to 3.8% from 3.5%.

Analysts at TD Securities expect signs of stabilization in the labor market after several volatile months. They forecast payroll growth of around 80K, driven mainly by hiring in healthcare and leisure & hospitality, while government employment may decline slightly. They also expect monthly wage growth to stay modest at 0.2%.

Additional labor indicators released earlier this week painted a mixed picture. ADP reported that private-sector employment rose by 109K in April, improving from March’s revised 61K increase. Meanwhile, the Employment Index in the Institute for Supply Management Services PMI climbed to 48 from 45.2, signaling that service-sector hiring is still contracting, though at a slower pace.

What impact will the US March Nonfarm Payrolls have on EUR/USD?

EUR/USD is likely to remain highly sensitive to the upcoming US Nonfarm Payrolls (NFP) report, as investors reassess the outlook for the Federal Reserve and the broader direction of the US Dollar.

Despite the Fed’s relatively hawkish April meeting, the USD has struggled to gain traction amid improving global risk sentiment and easing geopolitical tensions in the Middle East. Comments from Fed Chair Jerome Powell reinforced a data-dependent approach, while Austan Goolsbee acknowledged that labor market conditions have softened, even if they remain broadly stable.

Markets currently expect the Fed to keep rates unchanged through the end of 2026, though traders still see some probability of either a rate hike or cut depending on incoming data. A weak NFP reading — particularly below 30K alongside a higher Unemployment Rate — could strengthen expectations for rate cuts later this year. In that scenario, the USD may weaken further, allowing EUR/USD to extend gains.

On the other hand, a stronger-than-expected payrolls figure could reduce expectations for monetary easing and help the USD stabilize. This would likely cap EUR/USD upside, although a sustained dollar rally may remain limited if risk appetite stays strong heading into the weekend.

From a technical perspective, FXStreet analyst Eren Sengezer notes that EUR/USD maintains a bullish near-term bias. The pair continues to trade above its 100-day and 200-day Simple Moving Averages, while the Relative Strength Index trends toward bullish territory.

Key resistance is seen around 1.1800–1.1810, followed by 1.1900–1.1910 and the psychological 1.2000 level. On the downside, major support stands in the 1.1710–1.1680 zone, with further downside targets at 1.1650 and 1.1560 if selling pressure intensifies.

The conclusion of Operation Epic Fury is lifting risk sentiment.

Japan is expected to keep cracking down on speculators.

The US Dollar weakened after the White House announced the end of the two-month “Operation Epic Fury” and highlighted progress in talks with Iran. Markets are interpreting the developments as a sign of easing tensions in the Middle East, triggering a selloff in Brent crude and pushing the dollar index back toward two-month lows amid improving risk sentiment.

The more optimistic backdrop could support further gains in EUR/USD, though much will depend on how quickly oil prices decline. Damage to energy infrastructure across the Persian Gulf is expected to keep Brent and WTI well above the $65–70 range seen before the conflict erupted, maintaining underlying inflationary pressure.

US services PMI data continues to point to the strongest price pressures since 2022, while futures markets are increasingly pricing in the possibility of additional Fed tightening. That complicates any effort by Kevin Warsh to deliver the aggressive policy easing sought by Donald Trump. For now, however, traders remain focused almost entirely on developments in the Middle East.

The prospect of a ceasefire has already lifted EUR/USD toward 1.1760, and the pair could extend gains if de-escalation continues. On the other hand, a collapse in negotiations or renewed friction between the US and Iran would likely trigger a reversal, especially as Washington continues expanding its military presence in the Persian Gulf despite softer rhetoric.

Meanwhile, Wednesday’s sharp drop in USD/JPY has fuelled speculation that Japanese authorities intervened in the currency market again. Tokyo appears determined to discourage speculative dollar buying during periods of USD weakness.

Gold has also surged more than 3% on hopes of easing geopolitical tensions, climbing above $4,700. Lower oil prices reduce the risk of persistent inflation and lessen pressure on central banks to tighten policy further, potentially reviving demand for gold as a debasement hedge.

Huge swings across USD/Asia as Japan’s MOF keeps intervening in USD/JPY, while Axios continues to publish reports pointing to progress on an Iran deal. It’s difficult not to view the headlines with some skepticism, but markets react sharply to every update, making them impossible to ignore. Regardless of how the probabilities around an Iran resolution are assessed, the market response has been so significant that questioning the credibility of the news flow becomes secondary.

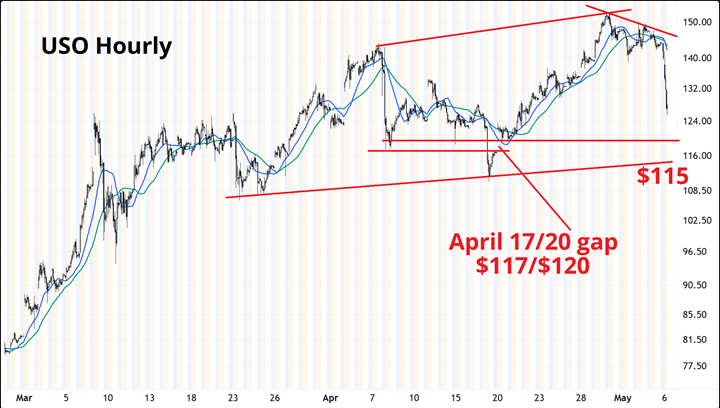

My long USD/CHF position has taken a heavy hit as the US Dollar tumbles alongside a sharp decline in oil prices. USO, the oil ETF, is down 11% today after Monday’s attacks on the UAE had traders positioned for a bullish breakout in crude that ultimately never materialized.

There still appears to be plenty of downside room before crude finds meaningful support. I’m using USO as the reference here, though the broader oil futures curve shows a very similar setup. Fresh optimism over a potential end to active conflict in the Middle East has fueled another rally in AI capex-related names, though it hasn’t translated into stronger USD demand as Japan’s MOF remains active and concerns over stagflation-driven rate hikes from the ECB and other central banks continue to ease.

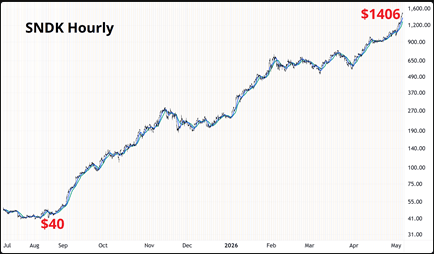

Apparently, the launch of the DRAM ETF was not the top for memory stocks after all.

SanDisk has now turned into a 35-bagger over the past year, soaring from $40 to $1,400 in just 12 months.

USD/JPY

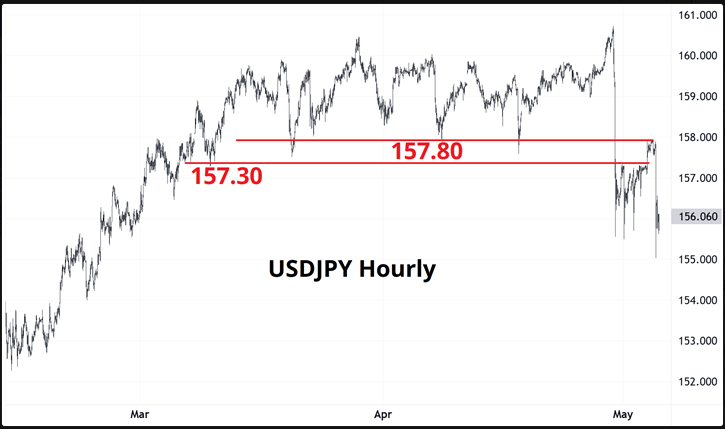

Interesting setup in USD/JPY. My initial strategy — selling into the 157.19–157.94 area in anticipation of MOF-driven upside exhaustion — turned out to be the correct call, but I got thrown off by a competing view that nonfarm payrolls would likely surprise to the upside. In hindsight, that was probably something to focus on Thursday rather than Monday. The chart still shows the former major low zone around 157.30–157.80 acting as resistance, and the repeated interventions suggest the MOF is serious about defending the area.

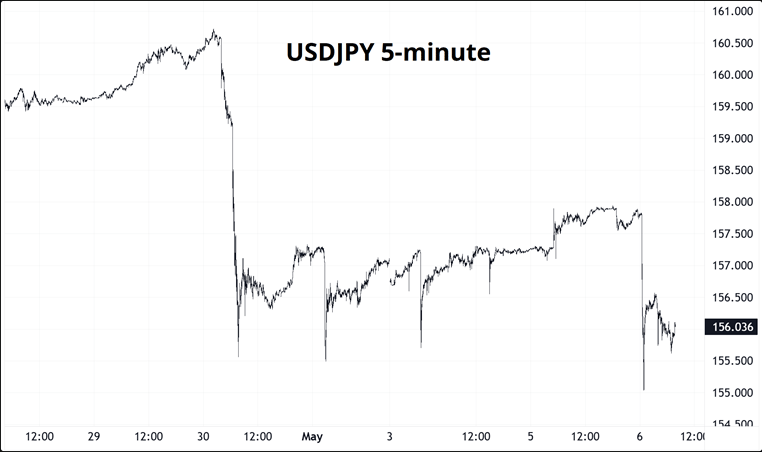

Here’s the 5-minute chart. It’s hard to say with certainty that every sharp drop was driven by the MOF, but several of them likely were.

I’m staying on the sidelines for now. Going long here makes little sense regardless of one’s NFP outlook, while shorting at the bottom of the range is equally unattractive. At this point, the MOF simply needs to keep hovering above 157.50 while hoping for lower yields and softer oil prices.

With the VIX sitting at 16.4 and oil down 10%, the hawkish Trump mean-reversion trade — long oil and long USD — probably offers positive expected value. The problem is that there’s still no concrete timeline attached to the latest “deal” or MOU narrative, making risk management on long oil positions extremely difficult.

In hindsight, I was too focused on NFP too early, if it even deserved attention at all in this environment. With oil and MOF activity overwhelmingly driving FX flows, concentrating on payrolls four days ahead of the release now feels misplaced.

Extend this analysis

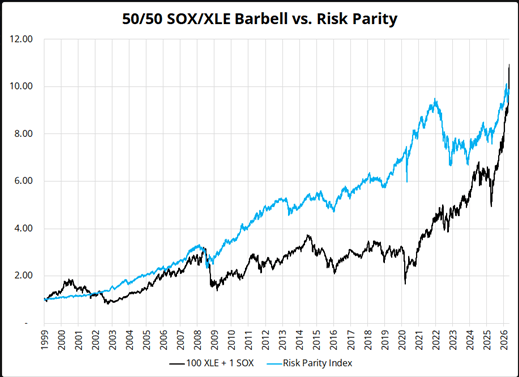

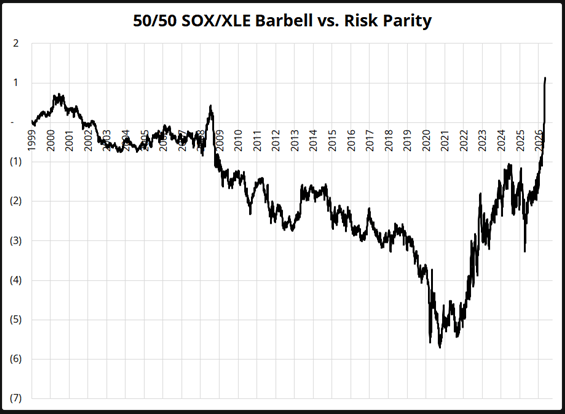

In recent weeks, a 50/50 barbell trade pairing semiconductors and oil has gained traction, with several bank strategists and Substack writers pitching it as a modern alternative to the traditional 60/40 stocks-and-bonds risk parity framework. In hindsight, the trade has delivered exceptional performance and offers some attractive characteristics: it largely sidesteps direct exposure to the U.S. consumer while remaining relatively resilient to stagflation pressures and tightening financial conditions.

That said, assuming the strategy will continue to work simply because it has worked recently feels like a dangerous exercise in extrapolation. Much of the enthusiasm may reflect performance chasing rather than a durable structural edge.

The following charts take a simplified approach by comparing a portfolio of 100*XLE + SOX against the Advance Research Risk Parity Index (RPARTR). I chose this particular risk parity benchmark because its data extends back to 1998, though using more sophisticated methodologies would likely produce a broadly similar picture.

The SOX+XLE barbell began outperforming after Russia’s latest invasion of Ukraine and continued to hold up even as oil prices eased post-Ukraine, largely because ChatGPT accelerated the AI capex boom. Still, after two wars and three years of markets pricing in the LLM theme, it’s difficult to argue that the trade still offers especially attractive risk/reward. Time will tell.

Traditional risk parity, meanwhile, outperformed across nearly every longer-term horizon except the past few years. The chart on the right indexes both strategies to January 1999 = 1, while the second chart highlights the performance gap between the two indexed series.

Worth keeping in mind.

Closing thoughts

EUR/USD is basically trading like oil.

Check who took the mound for the Cardinals on May 3 — Dustin May, wearing No. 3.

USD/GBP has remained under pressure since early April, driven mainly by uncertainty among central banks over how the conflict in Iran could affect inflation and energy prices. On Thursday, April 30, a fresh batch of economic data reinforced the cautious stance adopted by both the Federal Reserve (Fed) and the Bank of England (BoE).

Over the past month, the pair has fallen 2.8%, with ongoing tensions in the Middle East continuing to fuel market volatility.

While recent inflation data from both the United States and the United Kingdom drew attention, markets remained focused on the broader energy risks linked to the closure of the Strait of Hormuz, which has become a key factor behind the cautious outlook.

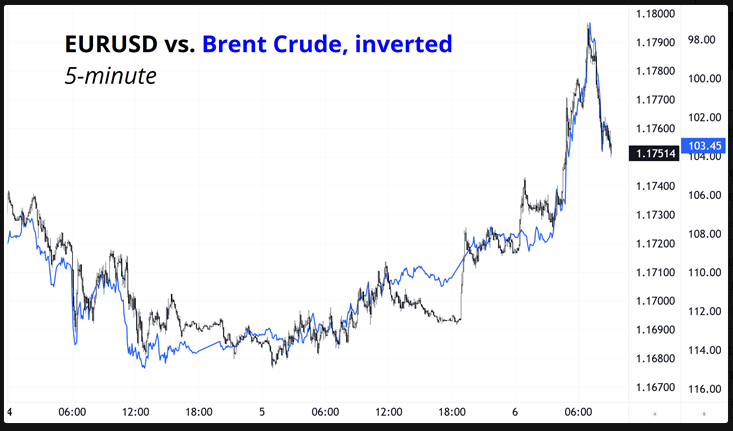

Energy driving USD/GBP

For currency traders, USD/GBP has increasingly behaved like a proxy for crude oil rather than reacting primarily to interest rate differentials, though energy market disruptions have also directly influenced monetary policy expectations on both sides of the Atlantic.

Over the past week, the pair has maintained a notably strong correlation with Brent crude, ranging between 0.96 and 0.97. In practical terms, this suggests that USD/GBP tends to rise alongside oil prices and fall when crude declines. Since correlations closer to 1 indicate an almost perfect relationship, the current pattern highlights the extent to which oil prices are steering movements in the pair.

Recent volatility in crude — which briefly surged nearly 7% to a four-year high of $126 per barrel — was largely triggered by reports that the US military was preparing to brief President Donald Trump on potential new actions involving Iran.

“We saw oil prices climb on fears over supply disruptions, making energy one of the few sectors to post gains,” Wealthify said in its monthly market summary. “Equity markets declined broadly, with losses across the US, Europe, the UK, and Asia, leaving investors with limited regional shelter.”

“The Federal Reserve kept rates unchanged in March, but rising oil prices and inflation concerns cast uncertainty over future rate cuts, pressuring bond prices lower. In the UK, mounting inflationary pressures alongside a softer labour market strengthened expectations that the Bank of England may keep rates elevated for longer, with the possibility of another hike later this year.”

The connection between energy markets and USD/GBP has therefore become a dominant force shaping sentiment, often overshadowing corporate earnings and other macroeconomic drivers. At the same time, interest rate expectations themselves are increasingly being influenced by the Middle East conflict, with recent central bank guidance offering key clues about the future direction of both the US Dollar and the British Pound.

Rates fuel cautious optimism

Thursday, April 30, 2026, brought a wave of central bank updates with important implications for USD/GBP.

The Bank of England (BoE) began the day by keeping its benchmark interest rate unchanged at 3.75%, while warning that the conflict in Iran could eventually trigger further inflation pressures and potentially require additional rate hikes.

The decision to hold rates passed by an 8–1 vote, though policymakers signaled that future tightening remains possible, including the prospect of more aggressive increases if inflation risks intensify.

Meanwhile, the United States released its March Personal Consumption Expenditures (PCE) Price Index data. Headline inflation came in slightly below expectations at 3.5%, versus forecasts of 3.6% from economists.

Excluding volatile food and energy prices, the Federal Reserve’s preferred core inflation measure rose 3.2%, matching market expectations and once again underscoring the uncertain influence of geopolitical tensions in the Middle East.

Additional US economic data released Thursday showed weekly jobless claims falling to 189,000 — the lowest level in more than 50 years — signaling ongoing resilience in the labor market and strengthening hopes for continued economic recovery.

While strong US labor data would normally support the Dollar against the Pound, expectations that the BoE may raise rates further are emerging as a key bullish factor for Sterling.

Markets now appear to be pricing in a more hawkish outlook for the UK, whereas sentiment in the United States is becoming comparatively more cautious despite elevated inflation linked to the Iran conflict. Although the Federal Reserve also left rates unchanged recently, several major financial institutions — including Capital One Financial, Synchrony Financial, and Marcus by Goldman Sachs — have already reduced yields on high-yield savings accounts.

These developments highlight growing differences in the monetary policy outlook between the two sides of the Atlantic, a divergence that forex traders are likely to monitor closely in the months ahead.

What’s next for USD/GBP?

The prospect of a more hawkish stance from the Bank of England, fueled by rising energy-driven inflation, could place further downward pressure on USD/GBP in the coming weeks. However, the key factor shaping the pair’s direction will remain developments surrounding the conflict in Iran and the continued closure of the Strait of Hormuz.

If the conflict drags on and keeps energy markets under strain, the BoE may be forced to respond with more aggressive rate hikes to contain inflationary pressures. In contrast, the Federal Reserve could continue facing political pressure from the US administration to lower interest rates, even as higher oil prices complicate the inflation outlook.

Against this backdrop of heightened volatility and uncertainty, a prolonged Middle East conflict could potentially drive USD/GBP toward the 0.71 level. At the same time, expectations for future US rate cuts may extend the Dollar’s broader long-term weakness against major global currencies.

The US Dollar Index softens as optimism surrounding a potential US-Iran agreement dampens safe-haven demand. Lower oil prices are also easing inflation worries, reducing expectations that the Fed will maintain a hawkish stance for longer. Meanwhile, Fed official Austan Goolsbee cautioned that inflation has picked up since the conflict began, moving further away from the central bank’s 2% target.

The US Dollar Index (DXY), which tracks the Greenback against six major currencies, is stabilizing around 98.00 during Thursday’s Asian session after declining nearly 0.5% in the previous trading day.

The US Dollar remains under pressure as optimism over a possible US-Iran agreement reduces safe-haven demand. The prospect of easing tensions has driven oil prices sharply lower, helping to ease inflation concerns and diminishing expectations that the Federal Reserve will maintain a hawkish policy stance for an extended period.

Still, Chicago Fed President Austan Goolsbee warned that inflation has failed to continue moderating toward the Fed’s 2% target and has instead accelerated since the conflict started.

According to the BBC, Iran said on Wednesday that a US proposal aimed at ending the conflict is “still being considered,” despite growing speculation that both sides could be approaching a deal. Reports suggest Washington submitted a one-page memorandum of understanding that would gradually reopen the Strait of Hormuz and ease the US blockade on Iranian ports, while discussions on Tehran’s nuclear program would take place later. However, no final agreement has yet been reached.

Meanwhile, Donald Trump told CNBC that Iran would face bombing “at a much higher level” if it refuses to accept a peace deal. In a post on Truth Social, Trump added that the US military operation known as “Operation Epic Fury” would end if Iran “agrees to give what has been agreed to.”

EUR/USD remains flat near 1.1750 as traders stay cautious over Iran’s response to the US peace proposal. Risk appetite continues to improve amid growing optimism surrounding a potential US-Iran agreement, while investors focus on upcoming remarks from ECB President Christine Lagarde and the US April Nonfarm Payrolls report for fresh market direction.

EUR/USD moves within a narrow range near 1.1750 in Thursday’s early European session as investors await Iran’s response to the US peace proposal, which includes restrictions on Tehran’s uranium enrichment activities and the reopening of the Strait of Hormuz.

Market sentiment remains broadly positive after reports suggested the US and Iran are nearing a potential agreement. Although S&P 500 futures trade little changed in Europe, the index rallied nearly 1.5% in the previous session.

Meanwhile, the US Dollar Index (DXY), which measures the Greenback against a basket of six major currencies, stays cautious around the 98.00 level.

Traders are now turning their attention to Friday’s key events, including remarks from ECB President Christine Lagarde and the US April Nonfarm Payrolls report. Both releases are expected to provide fresh signals on the future monetary policy paths of the ECB and the Federal Reserve.

EUR/USD: Technical outlook points to cautious consolidation

EUR/USD continues to consolidate near 1.1750 at the time of writing. The pair has hovered around the 20-period Exponential Moving Average (EMA), currently at 1.1708, for nearly a month, signaling a lack of clear directional momentum.

Meanwhile, the Relative Strength Index (RSI) remains trapped within the 40.00–60.00 range, highlighting ongoing market indecision.

On the downside, immediate support is seen around the 20-day EMA at 1.1708. A daily close below this level could weaken the near-term bullish outlook and trigger a deeper correction towards the April 1 peak at 1.1627. On the upside, a breakout above the May 6 high of 1.1797 may pave the way for a move towards the April 17 high near 1.1850.

Gold draws buyers for a second consecutive session as optimism over a potential US–Iran peace agreement weakens the US dollar. Easing inflation concerns also dampen expectations of aggressive Fed tightening, supporting demand for the metal, while traders await the US ADP report for fresh direction ahead of Friday’s Nonfarm Payrolls release.

Gold (XAU/USD) holds firm near a more-than-one-week high, staying above $4,650 as the European session begins on Wednesday. A broadly weaker US Dollar—pressured by growing optimism over a potential US–Iran peace agreement—has supported the metal’s rebound from Monday’s one-month low around $4,500. At the same time, falling crude oil prices are easing inflation concerns and reducing expectations of a more aggressive Federal Reserve, further boosting demand for the non-yielding asset for a second consecutive day.

On the geopolitical front, US President Donald Trump announced a temporary pause in “Project Freedom,” the military effort to escort commercial vessels through the Strait of Hormuz, to allow room for negotiations with Iran. He noted meaningful progress toward a comprehensive deal, echoing earlier remarks from Defense Secretary Pete Hegseth that the US is not seeking renewed escalation and that the ceasefire with Iran remains intact. Additionally, Secretary of State Marco Rubio confirmed the conclusion of “Operation Epic Fury,” a joint US–Israel campaign launched on February 28.

These developments have strengthened expectations of a peace agreement that could end the US-Israeli conflict involving Iran and reopen the strategically crucial strait, lifting investor sentiment while weighing on the dollar’s appeal. Meanwhile, oil prices have dropped to a one-week low, helping to curb fears of rising inflation and allowing the Fed to maintain a more cautious policy stance. Still, according to CME Group’s FedWatch Tool, markets are pricing in more than a 35% chance of a rate hike by year-end, which may limit further downside in the USD and cap gold’s near-term upside.

Given this backdrop, traders may wait for stronger follow-through buying before confirming that gold has formed a bottom near $4,500 and positioning for additional gains. Attention now turns to the US ADP private employment report later in the North American session, along with remarks from key FOMC officials and ongoing geopolitical updates. The primary focus, however, remains Friday’s closely watched US Nonfarm Payrolls report, which is expected to play a decisive role in shaping the near-term outlook for both the dollar and gold.

Gold H4

Gold bulls remain in control as long as prices hold above the 200-period SMA breakout level on the H4 chart. The metal’s solid rebound from the $4,500 region—near the 50% retracement of the March–April rally—combined with a move above $4,600, supports a bullish outlook. Prices are now approaching the 200-period SMA at $4,651.69, which serves as the next key resistance.

Momentum indicators reinforce the positive bias. The RSI sits around 59, suggesting steady strength without entering overbought territory, while the MACD histogram remains positive and continues to rise, pointing to building bullish momentum as gold tests overhead resistance.

On the downside, immediate support is located at the 38.2% Fibonacci retracement level around $4,588.83. Further declines could find buying interest near the 50% level at $4,495.62, followed by the 61.8% retracement around $4,402.41. A decisive break below this last level would invalidate the bullish setup and shift the near-term outlook back in favor of the bears.

Commerzbank’s Antje Praefcke maintains that geopolitical tensions surrounding the Iran conflict continue to be the dominant force driving EUR/USD, overshadowing upcoming US indicators such as ADP and Nonfarm Payrolls (NFP). She highlights that recent US labor data has been inconsistent and is unlikely to meaningfully influence the dollar. As a result, EUR/USD is expected to remain within its recent range unless there is a clear escalation or easing of tensions in the Middle East, which is currently acting as a cap on major price movements.

Praefcke notes that attention will still turn to incoming US macro data, beginning with JOLTS job openings—which came in somewhat soft—followed by the ADP report and the official payrolls release. While a strong ADP reading might offer the dollar modest support, a weaker NFP figure could exert downward pressure.

However, given the recent volatility and lack of clear direction in employment data, she believes these figures will likely remain inconclusive. April job growth is expected to be moderate, suggesting little chance of a decisive signal emerging. Consequently, unless there are significant surprises, the data is unlikely to drive the USD in any meaningful way.

In her view, the broader narrative remains unchanged: until there are concrete signs of either de-escalation or escalation in the Middle East conflict, other factors—including US economic data—will take a back seat. Only a clear shift in the geopolitical backdrop is likely to push EUR/USD out of its established range.

Gold edges higher with modest gains, but the broader fundamentals suggest caution for bullish traders.

Persistent inflation concerns are reinforcing expectations of more hawkish central bank policies, weighing on the metal.

Meanwhile, rising US-Iran tensions bolster the US dollar’s safe-haven appeal, adding further pressure on gold.

Gold (XAU/USD) picks up some buying interest during Tuesday’s Asian session, partially recovering from the previous day’s drop to around the $4,500 level—its lowest in over a month. However, the rebound lacks a clear fundamental driver and could fade quickly, suggesting traders should remain cautious before expecting any sustained upside. Ongoing US-Iran tensions continue to stoke inflation fears and reinforce expectations of higher interest rates, which, alongside a stronger US Dollar (USD), is likely to cap gains in the non-yielding metal.

The fragile ceasefire between the US and Iran appears close to breaking down after renewed violence in the Persian Gulf on Monday. Both the United Arab Emirates (UAE) and South Korea reported attacks on vessels in the critical shipping lane, while the UAE confirmed a fire at the Fujairah oil port following Iranian missile and drone strikes. US President Donald Trump warned that Iran would face devastating consequences if it targeted American ships escorting vessels through the region under the “Project Freedom” initiative.

These developments heighten the risk of further escalation in the Middle East, pushing crude oil prices higher and reinforcing concerns that rising energy costs could reignite inflation. This, in turn, strengthens expectations that major central banks—including the US Federal Reserve (Fed)—may adopt a more hawkish policy stance. Data from CME Group’s FedWatch Tool now shows the probability of a Fed rate hike by year-end at around 35%, up sharply from below 10% last Friday.

The outlook supports higher US Treasury yields, which continue to underpin the USD. Additionally, tensions around the Strait of Hormuz further enhance the dollar’s appeal as a global reserve currency, adding to the bearish near-term outlook for gold. As a result, any upward moves in the metal are likely to attract selling interest, and traders may prefer to wait for stronger, sustained buying before concluding that gold has formed a bottom.

Gold (XAU/USD) 4-hour timeframe chart

Gold may find it difficult to build on its intraday gains given the prevailing bearish technical structure.

From a chart standpoint, XAU/USD continues to show a short-term negative bias as it remains below the 200-period Simple Moving Average (SMA) at $4,655.02. The metal is also constrained by the 38.2% Fibonacci retracement of the March–April rally, keeping prices trapped beneath a strong resistance zone despite a slight rebound from the $4,500 region, which aligns with the 50% retracement level.

Momentum signals are still weak, with the Relative Strength Index (RSI) staying below the neutral 50 mark at 39.84 and the Moving Average Convergence Divergence (MACD) lingering in negative territory. This suggests the current recovery attempt could lose steam near the 38.2% Fibonacci level at $4,595.23. Any further upside is likely to face resistance around the 200-period SMA at $4,655.02, followed by the 23.6% retracement at $4,711.12.

On the downside, immediate support is seen near the 50% retracement at $4,501.57, ahead of the 61.8% level at $4,407.90. If selling pressure intensifies, deeper support levels come into view at $4,274.55 and $4,104.68.

GBP/USD has come under selling pressure for a third consecutive session as renewed tensions between the US and Iran continue to support demand for the US Dollar.

Higher oil prices are stoking inflation concerns and reducing expectations for Federal Reserve rate cuts, further strengthening the greenback. Meanwhile, the Bank of England’s relatively hawkish stance may provide some support to the pound, helping to cap deeper losses in the pair.

GBP/USD is extending its decline for a third consecutive day on Tuesday, though selling pressure remains limited as the pair holds above the key 1.3500 level during the Asian session. The mixed fundamental landscape suggests traders should be cautious about expecting a deeper pullback from last Friday’s peak around 1.3655–1.3660, the highest level since mid-February.

The US Dollar continues to benefit from safe-haven demand amid rising tensions between the US and Iran around the Strait of Hormuz, alongside reduced expectations for Federal Reserve rate cuts in 2026. This stronger USD is weighing on GBP/USD. However, the Bank of England’s comparatively hawkish stance offers support to the British Pound, helping to cushion further downside.

Recent developments have heightened geopolitical risks, including reports of an explosion on a South Korean-flagged vessel in the strait. Former US President Donald Trump warned of severe retaliation if Iran targets US ships, while Iran reportedly launched missile and drone attacks on the UAE following the US announcement of “Project Freedom” to assist stranded vessels.

These escalating tensions are pushing crude oil prices higher, stoking inflation concerns and reinforcing expectations of tighter monetary policy from major central banks, including the Fed. This dynamic continues to support the USD and pressure GBP/USD, although the BoE’s indication that further rate hikes may be needed if inflation persists should help stabilize the pair.

Looking ahead, traders will monitor Tuesday’s US data releases—including ISM Services PMI, JOLTS job openings, and new home sales—along with comments from FOMC officials for short-term direction. Still, attention is firmly on Friday’s Nonfarm Payrolls report and ongoing geopolitical developments, both of which are likely to drive market volatility.

The US Dollar Index trades steadily near 98.20 during Monday’s early Asian session. Donald Trump stated that the United States will assist vessels in exiting the Strait, while traders turn their focus to the upcoming US April employment report scheduled for release on Friday.

The US Dollar Index (DXY), which tracks the US Dollar against a basket of six major currencies, is hovering around 98.20 during Monday’s Asian session. It remains relatively stable as market participants evaluate ongoing geopolitical tensions in the Middle East.

US President Donald Trump announced that starting Monday, the US will assist neutral vessels stranded in the Persian Gulf by escorting them through the Strait of Hormuz. According to Bloomberg, US Navy ships will remain on standby to deter potential Iranian attacks on commercial shipping in the area.

Meanwhile, an Iranian official cautioned that any US involvement in the Strait would be viewed as a breach of the ceasefire, emphasizing that the Persian Gulf is not a place for political posturing. Traders are keeping a close watch on developments in the region, particularly any continuation of the Hormuz blockade. Escalating tensions could support the US Dollar due to its safe-haven appeal.