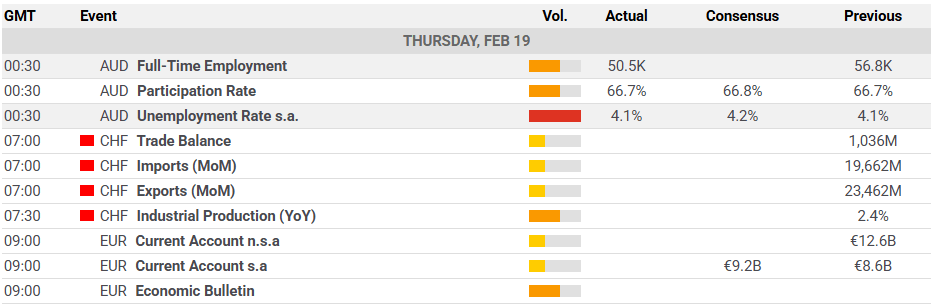

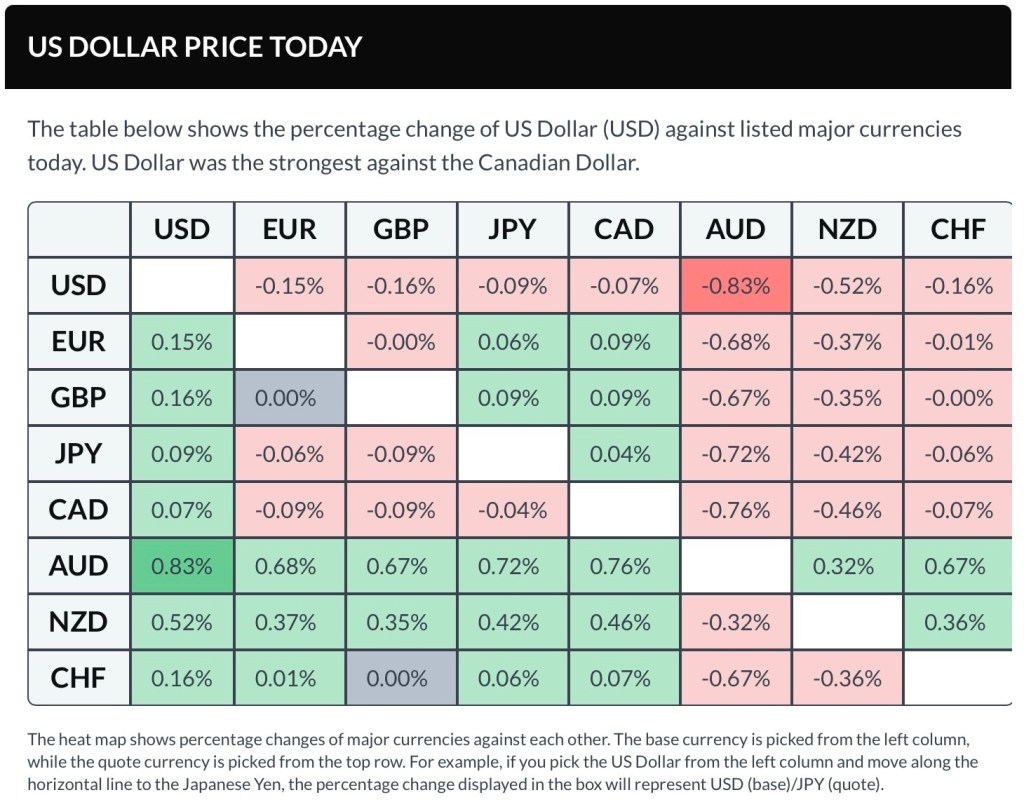

Recent weeks have clearly shown that President Trump’s domestic, foreign, and trade policy actions continue to weigh on the US dollar. Several of his tariff measures were struck down by the Supreme Court, creating frustration within the administration and adding fresh uncertainty. The independence of the Federal Reserve may also face scrutiny under the designated Fed Chair Kevin Warsh, who is seen as politically aligned with Trump. At the same time, the risk of military tensions with Iran adds another layer of geopolitical concern. In addition, shifting relative growth dynamics and a narrowing US interest rate advantage are likely to favor the euro. Overall, we see persistent headwinds for the USD and expect further depreciation against the EUR.

Yen – Weak despite Takaichi’s decisive win

Despite Prime Minister Takaichi’s landslide election victory, the yen remains under pressure. With her coalition securing a three-quarters majority and the LDP holding two-thirds of parliamentary seats, attention now turns to whether promised stimulus measures and tax cuts — including a potential suspension of VAT on food — will be implemented. BoJ Governor Ueda reiterated that rate hikes would depend on supportive economic data. Given the current political backdrop, we expect the BoJ to keep policy rates unchanged for now. As a result, EUR/JPY is likely to move sideways.

CHF – Strength amid rising uncertainty

Amid persistent trade and geopolitical uncertainty — much of it originating from the US — defensive currencies like the Swiss franc have benefited. Switzerland’s solid structural fundamentals, including economic resilience and strong fiscal and external positions, reinforce its safe-haven status. However, we anticipate a modest depreciation of the CHF in 2026, supported by stronger eurozone growth momentum, unless equity markets correct sharply or geopolitical risks intensify again. We view the franc’s current strength as temporary. With EUR/CHF near 0.90, the risk of Swiss National Bank intervention cannot be ruled out. Further CHF appreciation would be unwelcome given inflation remains extremely low at just 0.1% year-on-year, as it would deepen imported deflationary pressures.

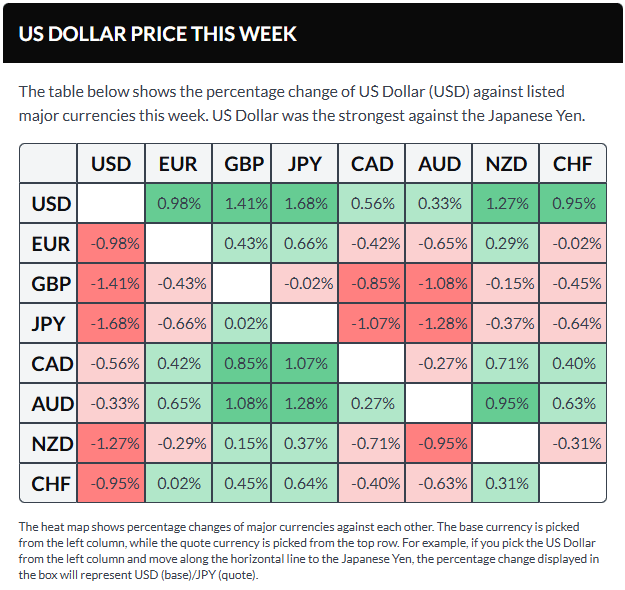

The U.S. dollar weakened this week amid ongoing geopolitical tensions and renewed uncertainty over U.S. trade policy. The setback followed a ruling by the Supreme Court of the United States declaring the Trump administration’s tariffs illegal, prompting President Donald Trump to announce a fresh round of levies. Even stronger-than-expected Producer Price Index (PPI) data failed to revive the greenback.

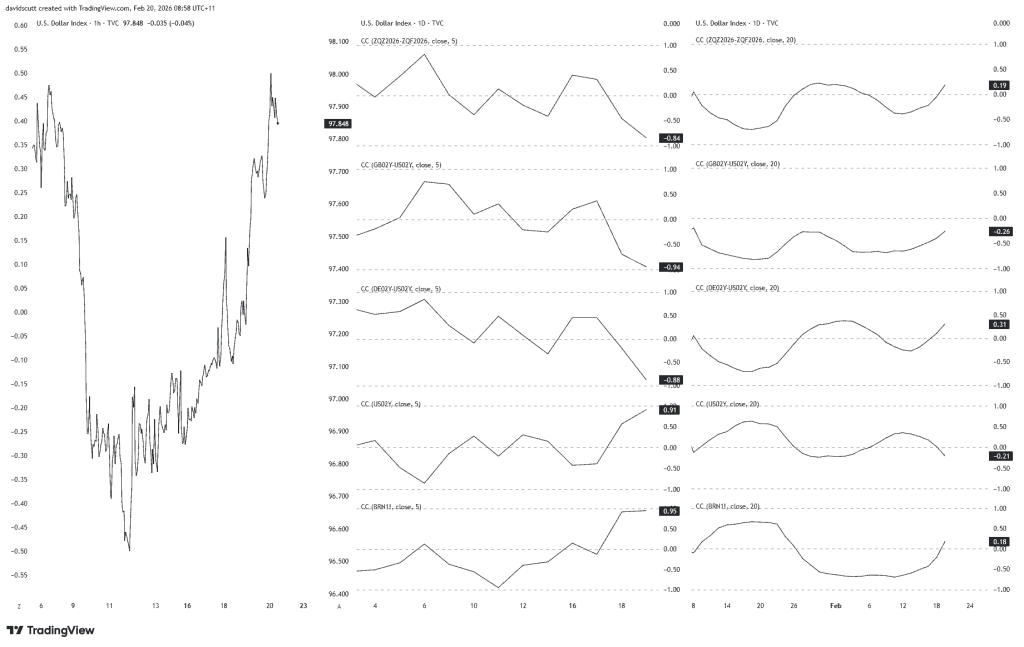

The U.S. Dollar Index (DXY) hovered near the 97.60 area, down about 0.20% on the day and ending the week modestly lower, as traders remained cautious amid trade and geopolitical uncertainty.

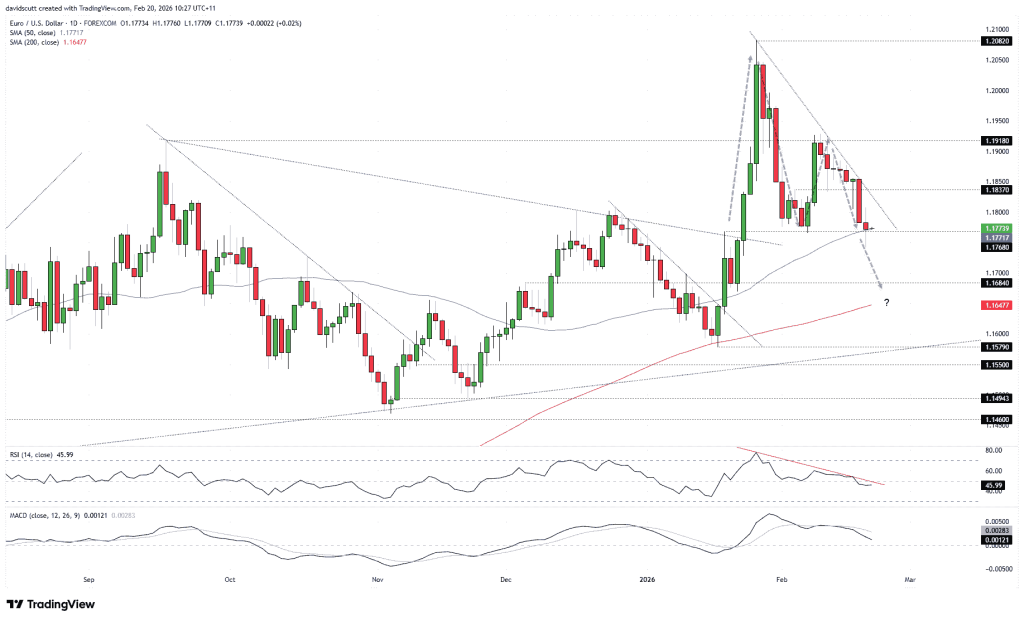

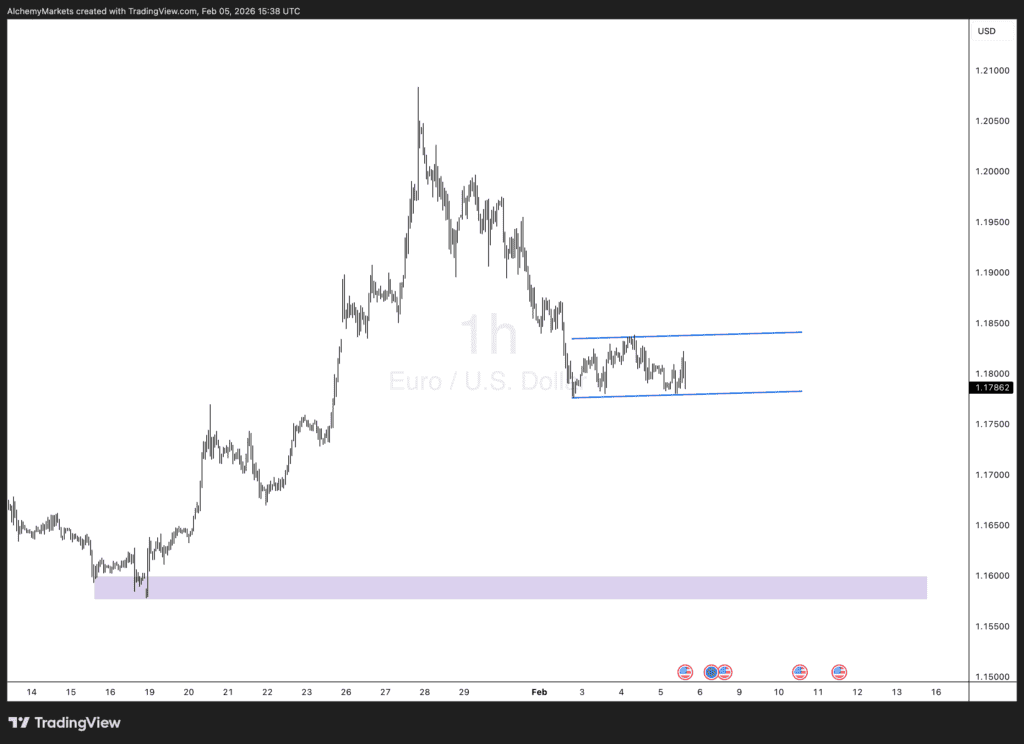

EUR/USD traded around 1.1810, edging higher during the U.S. session after Germany’s flash Harmonized Index of Consumer Prices (HICP) for February came in softer than expected at 2% year-on-year (vs. 2.1% forecast) and 0.4% month-on-month (vs. 0.5%). Investors also evaluated testimony from Christine Lagarde, President of the European Central Bank, before the European Parliament. Lagarde reiterated that inflation is gradually returning to the 2% target and said she intends to complete her term, dismissing speculation about an early departure.

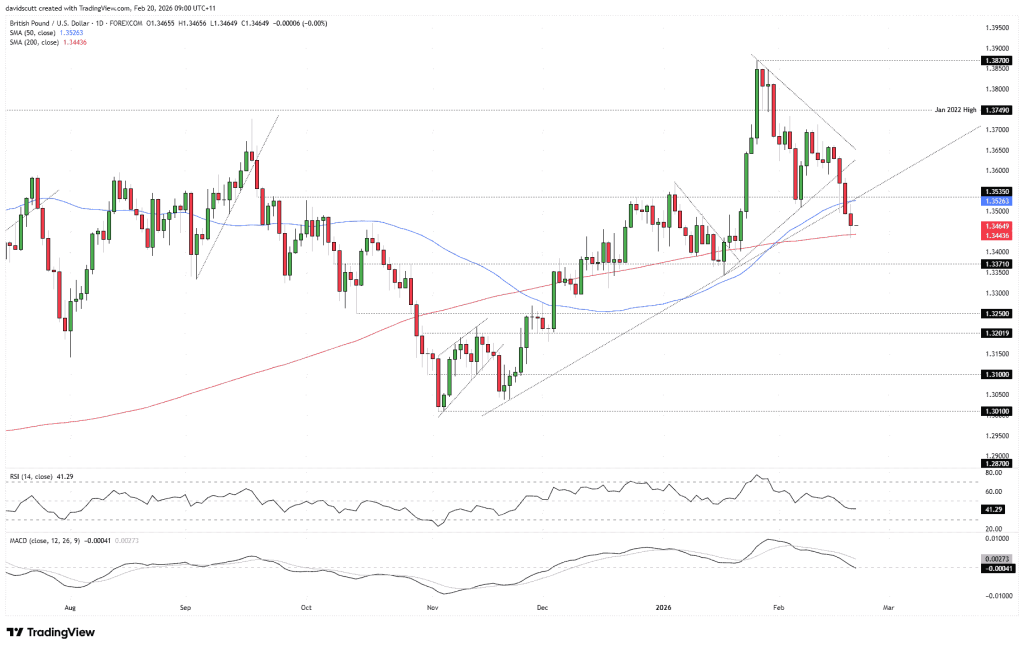

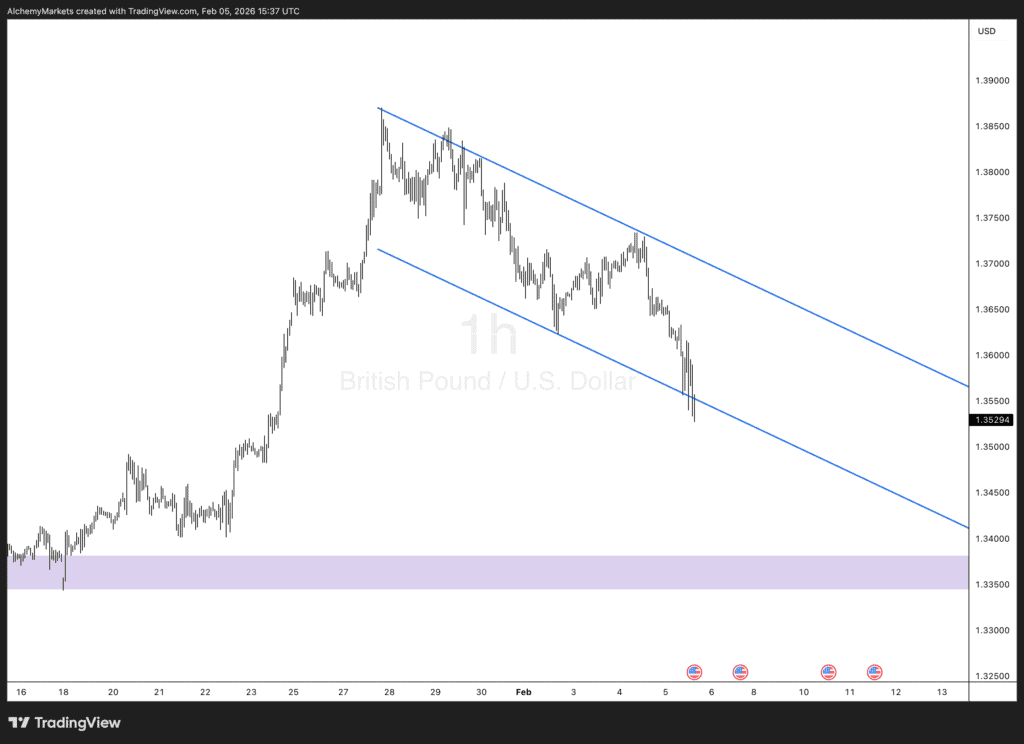

GBP/USD hovered near 1.3470, rebounding after nearly revisiting a one-month low earlier in February. Meanwhile, Andrew Bailey, Governor of the Bank of England, indicated there is room for rate cuts as inflation is expected to move back toward the 2% target.

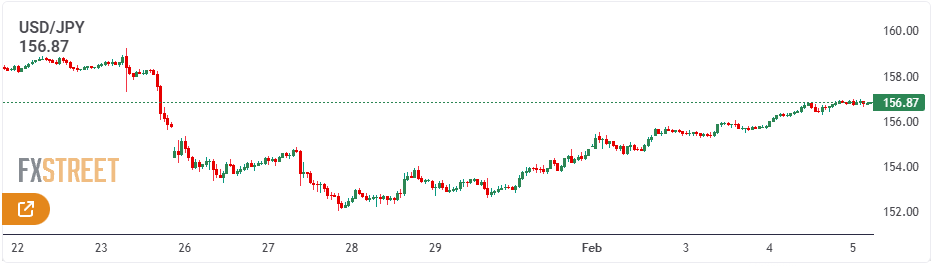

USD/JPY traded near 156.00, stabilizing after recouping most of its intraday losses. Tokyo’s February CPI rose 1.6% year-on-year, with the core measure excluding fresh food falling below the Bank of Japan’s 2% target for the first time since 2024.

AUD/USD climbed back toward 0.7120, turning positive after reversing earlier declines. Attention now shifts to Australia’s TD-MI Inflation Gauge, due Monday.

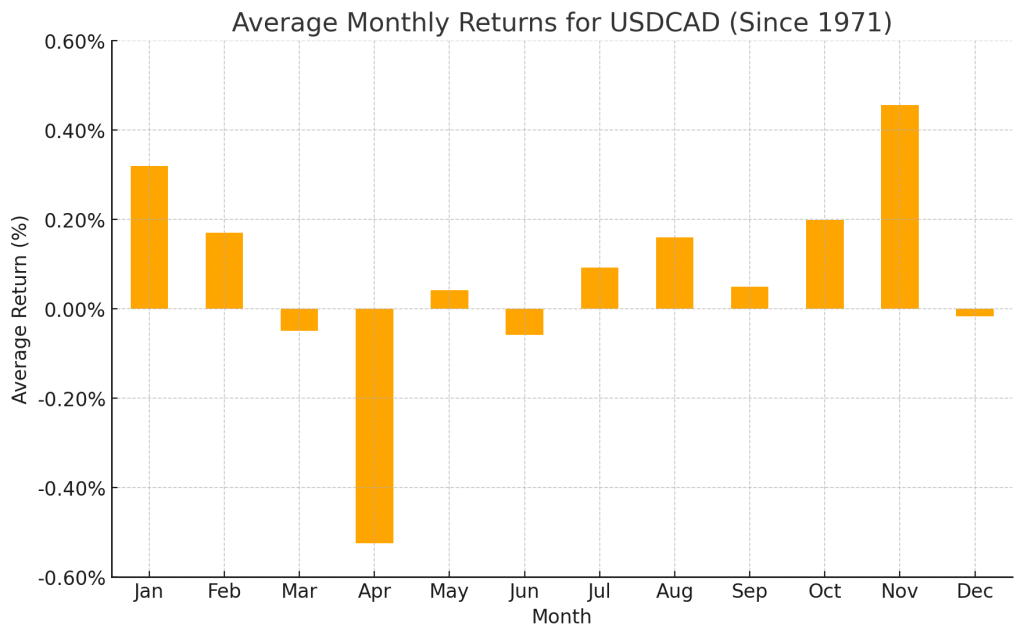

USD/CAD hovered around 1.3630, marking nearly a two-week low, as markets assessed economic data from both sides of the border. According to Statistics Canada, Canada’s GDP contracted at an annualized 0.6% rate in the fourth quarter, following a revised 2.4% expansion in Q3.

Gold traded near $5,260, reaching a one-month high amid persistent geopolitical uncertainty. The precious metal is attempting to retest its all-time high of $5,598 set earlier this year.

Anticipating economic perspectives: Key voices in focus

Sunday, March 1

Joachim Nagel – European Central Bank

Monday, March 2

Frank Elderson – European Central Bank

Joachim Nagel – European Central Bank

Christine Lagarde – European Central Bank

Dave Ramsden – Bank of England

Michele Bullock – Reserve Bank of Australia

Tuesday, March 3

Kazuo Ueda – Bank of Japan

John C. Williams – Federal Reserve

Olaf Sleijpen – European Central Bank

Martin Kocher – European Central Bank

Neel Kashkari – Federal Reserve

Wednesday, March 4

Piero Cipollone – European Central Bank

Tiff Macklem – Bank of Canada

Luis de Guindos – European Central Bank

Thursday, March 5

Luis de Guindos – European Central Bank

Martin Kocher – European Central Bank

Christine Lagarde – European Central Bank

Friday, March 6

Piero Cipollone – European Central Bank

Mary Daly – Federal Reserve

Beth Hammack – Federal Reserve

Scott Paulson – Federal Reserve

Central bank meetings and key data releases set to steer monetary policy outlook

Monday, March 2

Australia: TD-MI Inflation Gauge

China: February RatingDog Manufacturing PMI

Germany: January Retail Sales

Switzerland: January Real Retail Sales

Spain: February HCOB Manufacturing PMI

Italy: February HCOB Manufacturing PMI

Germany: February HCOB Manufacturing PMI

Canada: February S&P Global Manufacturing PMI

U.S.: February ISM Manufacturing Employment Index

U.S.: February ISM Manufacturing New Orders Index

U.S.: February ISM Manufacturing PMI

U.S.: February ISM Manufacturing Prices Paid

New Zealand: January Building Permits (s.a.)

Japan: January Unemployment Rate

Tuesday, March 3

Australia: January Building Permits

Eurozone: HICP (Harmonized Index of Consumer Prices)

The U.S. dollar slipped on Friday but remained on course for its first monthly advance since October, supported by escalating geopolitical tensions and a more hawkish Federal Reserve stance.

As of 15:11 ET (20:11 GMT), the Dollar Index — which measures the greenback against a basket of six major currencies — was down 0.2% at 97.59, though it was still headed for a roughly 0.6% gain for the month.

Dollar supported by heightened geopolitical tensions

The dollar has drawn support from concerns that the U.S. military buildup in the Middle East could escalate into a conflict with Iran, even as both sides continue discussions over Tehran’s nuclear program.

While the United States and Iran reportedly made some progress in Thursday’s talks, mediator Oman said negotiations concluded without a breakthrough that might prevent potential U.S. military action.

U.S. President Donald Trump told reporters Friday that he was “not exactly happy” with how Iran was handling the negotiations. He added that Tehran had not shown willingness to meet key U.S. demands and reiterated his dissatisfaction with the pace of progress.

Analysts at ING noted that any further escalation in U.S.-Iran tensions currently poses the greatest upside risk for the dollar. They pointed out that prediction market Polymarket still assigns a relatively elevated 55% probability of a U.S. strike on Iran by the end of March, which they believe is limiting further dollar weakness for now.

The greenback has also benefited from a slightly more hawkish tone at the Federal Reserve, after several policymakers signaled at January’s meeting that additional rate hikes remain possible if inflation stays persistent.

Supporting that view, January’s U.S. Producer Price Index (PPI) data released Friday came in well above expectations.

“Near-term factors continue to favor further USD strength, though renewed tariff uncertainty has reinforced the dollar’s risk premium,” ING added, expecting the currency to stabilize barring any major geopolitical developments.

Euro slips in February

In Europe, EUR/USD rose 0.2% to 1.1822 on the day, but the single currency remained on track for a roughly 0.2% monthly decline, as markets expect the European Central Bank to keep interest rates unchanged in the coming months.

Data showed Germany’s unemployment total edged up by 1,000 in February to 2.977 million, reflecting the prolonged economic slowdown that has weighed on Europe’s largest economy over the past three years.

Meanwhile, French consumer prices increased 1.1% year-on-year in February, exceeding expectations and marking a pickup after inflation slowed to a more than five-year low in January.

Analysts at ING said the 1.180 level is likely to continue acting as a near-term anchor for EUR/USD, as heightened uncertainty surrounding Iran discourages strong directional bets.

Elsewhere, GBP/USD was little changed at 1.3485 but was poised to end a three-month winning streak, with sterling down about 1.5% for February.

UK Prime Minister Keir Starmer saw his Labour Party suffer a notable by-election defeat, losing one of its safest seats to the left-wing Green Party of England and Wales.

The result adds to political pressure on Starmer after weeks of turbulence and renewed calls for his resignation. ING noted that developments perceived as weakening Starmer’s position have recently weighed on the pound, as a stronger showing by the Greens may raise expectations of a more left-leaning successor should he step down prematurely.

Yen on track for monthly decline

In Asia, USD/JPY slipped 0.1% to 156.00 on the day, but the pair remained poised for a 0.8% gain in February, reflecting continued weakness in the Japanese currency. The yen has come under pressure as investors assess the fiscal implications of Prime Minister Sanae Takaichi’s stimulus and tax cut proposals.

Takaichi’s ruling coalition strengthened its position after securing a supermajority in Japan’s lower house, clearing the way for her fiscal agenda.

At the same time, uncertainty over the timing of the next rate hike from the Bank of Japan has weighed on the yen. Soft February consumer price data from Tokyo — often viewed as a leading indicator of nationwide inflation — showed core CPI slipping below the BOJ’s 2% annual target for the first time in nearly four years, potentially limiting the scope for further tightening.

Elsewhere, USD/CNY rose 0.3% to 6.8579 after the People’s Bank of China removed a key foreign exchange risk reserve requirement for certain forward contracts, effectively making it cheaper to buy dollars domestically.

The move followed a strong rally in the yuan in recent months, partly fueled by exporters selling dollars amid a robust trade surplus with the United States.

AUD/USD gained 0.2% to 0.7120, with the Australian dollar set for a more than 2% monthly advance, supported largely by a more hawkish policy outlook from the Reserve Bank of Australia.

Indices: Tech Drags as Futures Edge Lower Before PPI

U.S. equity futures slip slightly after a weak session led by semiconductor losses. The tech-heavy Nasdaq 100 (-1.2% to 25,034) paced declines, followed by the S&P 500 (-0.5% to 6,908), while the Dow 30 (flat at 49,499) avoided closing in the red. Treasury yields eased across the curve, with the 10-year hovering near the 4% threshold, as investors await January PPI data. CME FedWatch pricing still points to rate cuts in July and October as the base case.

Stocks: Chip Selloff; Media Takeover Saga Nears Conclusion

Nvidia (-5.5%) slid despite beating earnings and revenue expectations, dragging the broader semiconductor space lower, including AMD (-3.4%), Intel (-3%), and ASML (-4.1%).

The contest for Warner Bros Discovery (-1.7% AH) appears to be wrapping up, with Netflix (+8.5% extended) stepping aside after Paramount Skydance (+10% close; +6.2% AH) presented a stronger bid.

Block (+23.6%) surged in extended trading after earnings and announcing plans to cut over 4,000 jobs.

IonQ (+21.7%) rallied on upbeat revenue guidance, with Morgan Stanley lifting its price target.

Meta (-0.7% AH) dipped after reports its in-house chip project faced hurdles and that it struck a deal to lease Google TPUs for AI development.

PayPal (-3.7%) declined after denying talks of a potential sale.

Meme stock movers included Beyond Meat (+2.9%), GoPro (+3.3%), Krispy Kreme (+27.8%), Opendoor (+8.6%), and BlackBerry (+2.6%).

Earnings Highlights:

Dell Technologies beat on both earnings and revenue; shares rose 11.6% after hours.

Zscaler missed on deferred revenue and billings; shares fell 9.5% AH.

Synopsys disappointed with full-year guidance; shares dropped 5.2%.

Rolls-Royce beat expectations, raised its profit outlook, and announced £2.5bn in buybacks; shares closed up 5.2%.

Baidu missed revenue forecasts; shares slid 5.7%.

Commodities:

Gold volatility eased as prices hovered near $5,200 but failed to sustain gains above that level, amid geopolitical uncertainty and a firmer dollar. Silver reclaimed $90, narrowing the gold/silver ratio below 58. The World Gold Council flagged stretched valuations.

WTI crude steadied around $65 after elevated intraday swings, with attention on Geneva talks and lingering U.S. military rhetoric. Traders are also focused on Sunday’s OPEC+ meeting amid speculation of a possible April output increase.

FX / Central Banks / Crypto:

Bitcoin retreated toward $68K, while Ether remained above $2K.

The U.S. Dollar Index firmed back into the 97 area, reversing prior losses on stronger labor data and reduced expectations for near-term Fed easing.

Fed officials offered mixed signals: Miran backed four quarter-point cuts this year, while Goolsbee cautioned against easing too quickly before inflation cools.

ECB President Lagarde reiterated inflation is expected to return to the 2% target over the medium term, emphasizing a data-dependent approach and monitoring — not targeting — FX markets.

Data: Stronger-Than-Expected Labor Figures

U.S. initial jobless claims came in at 212K (vs. 217K forecast), with continuing claims falling to 1.833m. Kansas Fed manufacturing improved sharply to 10 from -2.

Tokyo headline CPI rose to 1.6% y/y, though core measures eased. Retail sales rebounded 1.8% y/y, while industrial production disappointed at 2.2% growth (vs. 5.3% expected).

Ahead:

U.S. PPI, Chicago PMI, and Baker Hughes rig count data due later today.

In Europe, German preliminary CPI, import prices, and labor data.

Saturday: Earnings from Berkshire Hathaway.

Sunday: OPEC+ meeting to determine April output levels.

Most Asian currencies slipped on Friday as investors weighed a mixed interest rate outlook across the region. The Australian dollar was on track for a solid monthly gain, while the Japanese yen remained under pressure.

The Chinese yuan declined after Beijing lowered a key reserve requirement to make dollar purchases cheaper domestically, though the currency continued to hover near three-year highs.

Meanwhile, the dollar index and dollar index futures edged down about 0.1% in Asian trading. Despite the dip, the greenback was up 0.7% for February, supported by safe-haven demand and lingering uncertainty over the direction of interest rates.

Japanese yen subdued after weak Tokyo CPI, February decline in focus

The Japanese yen saw the USD/JPY pair slip 0.2% on Friday and was on track to gain 0.7% for February.

Pressure on the yen intensified as uncertainty grew over the timing of the Bank of Japan’s next interest rate hike. Those doubts deepened following softer-than-expected consumer price index data from Tokyo for February.

The reading—often viewed as a leading indicator for nationwide inflation—showed core CPI falling below the BOJ’s 2% annual target for the first time in nearly four years, potentially complicating the central bank’s plans for further rate increases.

The yen had weakened earlier in February amid concerns about the fiscal implications of Prime Minister Sanae Takaichi’s proposed stimulus measures and tax cuts. However, she appeared to gain momentum for advancing her fiscal agenda after her ruling coalition secured a supermajority in Japan’s lower house of parliament.

Chinese Yuan slips after PBOC lowers FX risk reserve ratio

The Chinese yuan’s USD/CNY pair rose 0.2% on Friday after the People’s Bank of China removed a key foreign exchange risk reserve requirement for certain forward contracts—a step that makes dollar purchases cheaper domestically.

The move follows a strong rally in the yuan against the dollar in recent months, partly fueled by exporters offloading the greenback amid a robust trade surplus with the United States.

However, rapid appreciation of the yuan can weigh on Chinese exporters by shrinking returns on overseas sales. Friday’s decision suggests the central bank may be aiming to curb further strength in the currency.

The yuan had approached a three-year high on Thursday before pulling back.

Australian dollar set for February gains on hawkish RBA outlook

The Australian dollar’s AUD/USD pair climbed 0.25% on Friday, ranking among Asia’s top performers for the month.

The Aussie was on track to advance 2.3% in February, largely supported by a more hawkish stance from the Reserve Bank of Australia. The central bank raised interest rates by 25 basis points earlier in the month and signaled it would tighten further if inflation fails to ease.

Stronger-than-expected January CPI data released this week reinforced expectations that the RBA could deliver additional rate hikes.

Elsewhere in the region, most Asian currencies edged lower on Friday. The South Korean won’s USD/KRW pair ticked up slightly but remained down 1.3% for February.

The Indian rupee’s USD/INR pair steadied after climbing back above the 91-per-dollar mark, though it was still 0.8% weaker this month, despite gaining support from a U.S.–India trade agreement.

Meanwhile, the Singapore dollar’s USD/SGD pair was little changed on the day and down 0.7% for February.

The U.S. dollar steadied on Thursday, recovering from earlier declines after upbeat earnings from AI heavyweight Nvidia, as investors looked ahead to further clarity on upcoming U.S. tariff measures.

As of 03:00 ET (08:00 GMT), the US Dollar Index, which measures the greenback against six major peers, was up 0.1% at 97.650. Despite the modest rebound, the index remained on course for a weekly drop of roughly 0.2%.

Dollar Holds Steady Following Strong Results from Nvidia

The dollar steadied after starting the session under pressure, as stronger-than-expected earnings from Nvidia lifted investor sentiment and reduced demand for the traditional safe-haven currency.

The world’s most valuable company reported January-quarter revenue that topped analyst forecasts and projected current-quarter sales above market expectations, reinforcing optimism around the AI theme.

“Improved sentiment has weighed on the dollar over the past 24 hours, with only the yen faring worse among G10 currencies yesterday,” analysts at ING Group noted.

Markets are also watching how the Trump administration responds to the February 20 Supreme Court decision that invalidated the president’s emergency tariffs. Meanwhile, U.S. Trade Representative Jamieson Greer said Wednesday that tariff rates for certain countries will increase to 15% or more from the newly introduced 10%, though he did not specify which trading partners would be affected.

In addition, U.S. and Iranian officials are set to meet in Geneva to discuss a potential nuclear agreement, with Donald Trump warning that “bad things” could occur if meaningful progress is not made.

According to ING, any escalation in tensions could serve as the most credible trigger for a broader dollar rally, particularly given the supportive backdrop from Nvidia’s results and the absence of major economic data releases. Overall, while the dollar may find some near-term stability, downside risks persist as the positive spillover from Nvidia’s earnings keeps investors leaning away from defensive currencies for now.

Euro edges lower

In Europe, EUR/USD slipped 0.1% to 1.1798 ahead of the latest Eurozone consumer confidence data due later in the session.

Still, both these figures and Friday’s inflation release are unlikely to move the needle much for the single currency, as the European Central Bank is widely expected to leave interest rates unchanged for the foreseeable future.

“For now, the EUR/USD short-term rate differential remains unsupportive for the pair, but we haven’t seen a sufficient rebound in dollar confidence to call for a significant downside break. We continue to view 1.1750 as solid support, absent a major escalation involving Iran,” analysts at ING Group said.

Meanwhile, GBP/USD declined 0.3% to 1.3523, with sterling failing to gain traction despite improved sentiment data from the UK’s business and professional services sector.

The latest quarterly survey from the Confederation of British Industry showed optimism in the sector rebounded sharply to -3 in February from -50 in November — its strongest reading since August 2024.

Yen Strengthens Following Interview with Kazuo Ueda

In Asia, USD/JPY slipped 0.3% to 156.01 after Kazuo Ueda, governor of the Bank of Japan, told the Yomiuri Shimbun that policymakers will внимательно assess incoming data at their March and April meetings, keeping the door open to another rate hike if inflation and wage growth remain solid.

His comments bolstered expectations that Japan will stay on a gradual path toward policy normalization.

The yen had weakened the previous day following reports that Prime Minister Sanae Takaichi adopted a cautious stance on additional rate increases, alongside news that two dovish-leaning nominees were selected for the BOJ board.

Meanwhile, USD/CNY declined 0.4% to 6.8392, hitting a fresh 34-month low amid anticipation of supportive measures ahead of China’s annual legislative gathering, the National People’s Congress. Investors are looking for growth targets and potential fiscal stimulus signals from the meeting, which typically outlines Beijing’s economic agenda for the year.

Elsewhere, AUD/USD eased 0.1% to 0.7114, while NZD/USD fell 0.2% to 0.5988.

Most Asian currencies traded in a tight range on Thursday as lingering uncertainty over U.S. trade policy kept sentiment cautious, though the Chinese yuan and Japanese yen stood out on domestic drivers.

The US Dollar Index slipped 0.1% during Asian trading hours, with its futures also down 0.1% as of 00:22 ET (05:22 GMT).

Chinese yuan surges to 34-month high on policy hopes

China’s onshore yuan strengthened, with USD/CNY sliding 0.5% to a new 34-month low of 6.834 ahead of the country’s annual parliamentary session, the National People’s Congress. Markets are betting on fresh policy backing as investors look for growth targets and potential fiscal stimulus signals that will shape Beijing’s economic agenda for the year.

The offshore yuan also advanced, with USD/CNH touching its weakest level since mid-April 2023.

Elsewhere in the region, currencies were mostly subdued as concerns over U.S. tariffs persisted. President Donald Trump’s 10% global tariffs came into force earlier this week, with plans underway to raise them to 15%.

The South Korean won was little changed after the Bank of Korea kept its benchmark rate steady at 2.5%, in line with expectations. The Singapore dollar edged 0.1% higher against the greenback, while the Indian rupee gained 0.1%. The Australian dollar rose 0.2%.

Yen rebounds on BOJ rate hike expectations

The Japanese yen strengthened, with USD/JPY falling 0.4%, after Kazuo Ueda, Governor of the Bank of Japan, said policymakers would carefully assess incoming data at their March and April meetings, leaving room for another rate hike if inflation and wage growth remain solid.

His comments bolstered expectations that Japan will stay on a gradual path toward policy normalization.

The yen had weakened a day earlier following reports that Prime Minister Sanae Takaichi adopted a cautious stance on further tightening and after two more dovish-leaning members were nominated to the BOJ board.

Analysts at ING said the addition of new board members would broaden the range of views in policy discussions, though no single perspective is likely to dominate. They added that a June rate hike appears more likely than one in April, pending confirmation of strong spring wage gains and April inflation data.

GBP/USD extended its advance for a fourth straight session, hovering near 1.3510 in Wednesday’s Asian trading. The pair is benefiting from continued softness in the US Dollar after US President Donald Trump delivered the first State of the Union address of his second term before a joint session of Congress.

Technical Analysis

GBP/USD continues to draw support near the 200-period Simple Moving Average (SMA) on the four-hour chart, around the 1.3550 area, which now serves as an important short-term pivot. The MACD histogram remains in negative territory, reflecting that the MACD line is still below the Signal line near the zero threshold. Meanwhile, the RSI stands at 40 — leaning neutral-to-bearish — after bouncing from earlier lows, indicating that upside moves may lack strong conviction.

As long as price holds above the upward-sloping 200-period SMA, the near-term bias remains constructive. However, a decisive break back below this level would tilt momentum in favor of sellers. A turn of the MACD histogram into positive territory would signal easing bearish pressure. For a stronger recovery outlook, the RSI would need to climb back above 50; remaining below that mark would likely keep rallies contained and shift focus toward consolidation rather than a sustained advance.

Fundamental Analysis

The GBP/USD pair edges lower for a second consecutive session on Tuesday, sliding to its weakest level in over a week — around the mid-1.3500s — during early European trading after the release of the UK labor market data.

Figures from the UK Office for National Statistics showed the ILO unemployment rate rose to 5.2% in the three months to December, up from 5.1% previously and marking the highest reading since early 2021. Meanwhile, jobless claims increased by 28.8K in January, signaling further softening in the labor market at the start of 2026.

Wage growth also cooled notably. Average Earnings Excluding Bonus rose 4.2% in the three months to December, easing from 4.6% in the prior quarter and hitting the slowest pace in nearly four years. Earnings Including Bonuses likewise slowed to 4.2% from 4.6%. Unless UK inflation data due Wednesday delivers an upside surprise, the latest employment figures reinforce expectations that the Bank of England could cut rates as soon as March, adding pressure on the British Pound.

At the same time, the US Dollar strengthens to a one-week high, further weighing on GBP/USD. However, the greenback’s upside appears limited by dovish Federal Reserve expectations. Following softer US inflation data last Friday, markets increased bets that the Fed may begin easing policy in June. Current pricing suggests at least two rate cuts in 2026, and lingering concerns about the Fed’s independence also restrain bullish USD momentum.

With traders hesitant to take aggressive positions ahead of clearer guidance on the Fed’s path, attention now shifts to the FOMC Minutes on Wednesday and the US Personal Consumption Expenditure (PCE) Price Index on Friday. These releases will be pivotal for shaping expectations around US monetary policy and, in turn, the direction of the dollar. Additionally, Wednesday’s UK CPI report could inject fresh volatility into GBP/USD as the week progresses.

US stock futures stabilized on Tuesday following a shaky start to the week, as renewed selling linked to AI disruption concerns unsettled investors. Sentiment was also dented by fresh uncertainty around US President Donald Trump’s tariff agenda. Anxiety over artificial intelligence’s potential to disrupt software and wider industries intensified after a bearish report from Citirni Research highlighted AI-related risks extending beyond the tech sector.

While the intensity of the “AI scare” trade appears to be easing and traders are stepping back into some beaten-down tech names, markets remain cautious amid ongoing tariff confusion. This comes after Friday’s turbulence triggered by the US Supreme Court’s decision to overturn President Trump’s sweeping tariff measures.

The US100 is trying to stabilize after sliding 1.13% in the previous session, breaking below a medium-term ascending trendline drawn from the August lows. The index is trading just beneath the 38.2% Fibonacci retracement of the October 30–November 21 decline from the record peak of 24,757. Immediate support is seen at the 23.6% Fibonacci level around 24,400, while a recovery could prompt a retest of the short-term SMAs near 25,075 and 25,300.

Tariff uncertainty and US-Iran tensions support Gold

Gold is retreating from a three-week high near 5,250 as a firmer US dollar and profit-taking pressure prices after a rally fueled by tariff uncertainty and geopolitical risks in the Middle East. Investors are awaiting further clarity on President Trump’s trade policy after the Supreme Court invalidated his earlier global tariff framework. The administration has since introduced temporary 15% tariffs aimed at addressing what it describes as a balance-of-payments crisis, a characterization questioned by many economists.

Attention also remains on escalating US-Iran tensions ahead of a third round of talks, as the White House signals it may be edging closer to potential military action related to Iran’s nuclear program, including additional naval deployments. Later today, President Trump’s State of the Union address could add another layer of volatility.

Technically, gold has snapped a four-day winning streak and is testing firm support at 5,141 — the 61.8% Fibonacci retracement of the January 29–February 2 decline from its record high. Further support lies near the 20-day SMA around the key 5,000 mark. Despite the pullback, the broader bias remains positive, with both MACD and RSI still in bullish territory, albeit turning cautious. A rebound could target 5,342, with scope for fresh highs above 5,420.

Yen ahead of CPI

The yen extended its decline against a stronger dollar as tariff concerns resurfaced and reports suggested Japanese Prime Minister Sanae Takaichi voiced caution about additional Bank of Japan rate hikes during discussions with Governor Kazuo Ueda. The yen’s rebound following the February 8 election has faded, reviving the so-called “Takaichi trade” amid fears that fiscal expansion could further weaken the currency.

Yen weakness also shifts attention to Friday’s Tokyo CPI data. Current fiscal measures may struggle to keep inflation anchored at the BoJ’s 2% target, while recent figures indicate earlier cost-push pressures are easing. Continued currency softness could bring forward expectations for the next BoJ rate hike from December to as early as April.

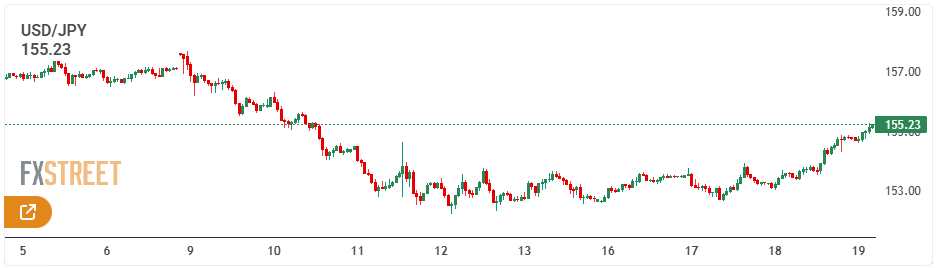

Technically, USD/JPY is approaching an upside breakout from a symmetrical triangle pattern, testing two-week highs around 156.30. Momentum remains modest, with the RSI hovering near the neutral 50 level and the MACD still below zero. A daily close above the 50-day SMA — coinciding with the triangle’s upper boundary — could pave the way toward 157.60. On the downside, a move below the 20-day SMA may expose the psychological 154.00 level.

The U.S. dollar recovered on Tuesday after the prior session’s slide, supported by upbeat economic data, while investors stayed cautious amid fresh volatility tied to President Donald Trump’s tariff policies.

At 15:24 ET (20:24 GMT), the Dollar Index—measuring the greenback against six major currencies—rose 0.2% to 97.86, after falling as much as 0.5% a day earlier.

Strong data underpin dollar

Encouraging economic releases lent the dollar some backing. ADP reported a gain of 12.8K in private payrolls last week, exceeding the previous reading. In addition, the Conference Board’s consumer confidence index for February surprised to the upside at 91.2.

According to José Torres, senior economist at Interactive Brokers, the stronger-than-expected figures nudged both the dollar and yields modestly higher, with a bear-flattening move led by shorter-dated maturities that are more sensitive to monetary policy.

He noted that firmer labor data are pushing rates up, as improving employment conditions weaken the case made by dovish Federal Reserve members for interest rate cuts based on softening job trends.

Trade tensions cloud outlook

Despite the rebound, uncertainty surrounds the U.S. currency as Trump’s revised tariff plans take shape following a Supreme Court ruling that his use of a 1977 emergency law to impose tariffs overstepped his authority.

In response, Trump said he would lift a temporary import tariff from 10% to 15% on goods from all countries. The move has cast doubt on the reliability of trade agreements reached prior to the ruling. Reflecting this uncertainty, the European Parliament delayed a vote on the European Union’s trade pact with the United States due to the new import tax.

Trade concerns have resurfaced at a time when questions are also emerging over the durability of heavy investment in artificial intelligence and the resilience of the U.S. economy after last week’s weak growth data.

Euro steady; Yen under pressure

In Europe, EUR/USD slipped 0.1% to 1.1779, with the euro largely steady after ECB President Christine Lagarde reiterated in Washington that the European Central Bank’s rate policy remains in a “good place,” while emphasizing the need for flexibility.

GBP/USD edged up 0.1% to 1.3501 ahead of parliamentary testimony from four Bank of England rate-setters, which may shape expectations before the March policy meeting.

In Asia, USD/JPY jumped 1% to 155.76 as expectations for near-term tightening by the Bank of Japan softened. The yen was also pressured by a Nikkei report suggesting U.S. authorities led recent rate-check efforts aimed at supporting Japan’s currency.

USD/CNY fell 0.4% to 6.8830 after the People’s Bank of China kept its one-year and five-year loan prime rates unchanged, signaling Beijing’s preference for calibrated support while balancing growth and financial stability. Chinese markets reopened Tuesday following the Lunar New Year holiday.

Elsewhere, AUD/USD rose 0.1% to 0.7060, while NZD/USD advanced 0.2% to 0.5967.

The U.S. dollar weakened on Monday as investors assessed the implications of the Supreme Court of the United States decision to strike down tariffs introduced by Donald Trump, along with the administration’s subsequent response.

Traders were also monitoring renewed nuclear negotiations between Washington and Tehran.

As of 14:12 ET (19:12 GMT), the Dollar Index — which measures the greenback against a basket of six major currencies — was down 0.2% at 97.65. The currency had posted a gain of roughly 1% last week, marking its strongest weekly advance in more than four months.

Dollar pressured by mounting trade uncertainty

The Supreme Court of the United States ruled on Friday that sweeping tariffs introduced by Donald Trump exceeded his authority. In response, Trump criticized the court and unveiled a blanket 15% levy on imports.

The new duties are set to remain in place for 150 days, but it remains unclear whether the U.S. government must reimburse importers for tariffs already collected, as the Court did not address that issue.

The uncertainty could trigger prolonged legal battles and further confusion as Trump explores alternative mechanisms to reinstate broad-based global tariffs on a more permanent footing.

Thierry Wizman, global FX and rates strategist at Macquarie, said the firm’s bearish U.S. dollar outlook for 2026 was based on the view that tariffs signal U.S. “disengagement” from the rules-based order underpinning free trade. He added that tariff conflicts themselves generate uncertainty centered on the United States — a negative for the dollar.

“In that sense, while the Supreme Court ruling may have strengthened institutional checks, it also heightens uncertainty, as Trump is likely to revive the tariff war through different — and more legally grounded — channels that have yet to be detailed. We see no reason to revise our broader expectation for a weaker USD in 2026,” Wizman said.

Beyond trade policy, investors are also watching a U.S. military buildup in the Middle East aimed at pressuring Iran to abandon its nuclear ambitions, with further talks between Washington and Tehran expected later this week.

Euro advances as confidence in Europe strengthens

In Europe, EUR/USD rose 0.2% to 1.1799, with the single currency drawing support from trade-driven weakness in the dollar.

Growing confidence in the region’s economic outlook also underpinned the euro, following data on Friday showing eurozone business activity expanded faster than expected this month, as manufacturing returned to growth for the first time since October.

Momentum was reinforced on Monday as Germany’s Ifo business climate index climbed to 88.6 from 87.6 the previous month, signaling improving sentiment in Europe’s largest economy.

Meanwhile, GBP/USD added 0.1% to 1.3497, with sterling firming ahead of key event risks this week — including testimony before the Treasury Committee by Andrew Bailey, governor of the Bank of England, and Thursday’s UK by-election in Gorton and Denton.

Yen edges higher

In Asia, USD/JPY fell 0.4% to 154.48, with the Japanese yen supported by its traditional safe-haven appeal as investors remained cautious about the economic impact of higher U.S. tariffs. Trading volumes were thinner due to a public holiday in Japan.

USD/CNY was little changed at 6.9087, with Chinese markets shut for New Year holidays. Elsewhere, AUD/USD declined 0.3% to 0.7060, while NZD/USD also dropped 0.3% to 0.5961.

Thierry Wizman of Macquarie said that while the dollar could remain under pressure amid persistent U.S.-driven uncertainty, some currencies — such as the yuan and the euro — may outperform, whereas others, including the Canadian and Mexican pesos, could lag. He added that even in the face of potential credit rating actions, long-term U.S. Treasury yields might rise due to uncertainty over revenue replacement, and equities could come under strain if higher yields lead to valuation compression.

The US dollar at one stage surged sharply against the Mexican peso, but by week’s end it had given back some of those gains. The 17.00 area below continues to act as a key support zone, and a decisive break beneath it could open the door for a move toward 16.50.

While short-term bounces are possible, the broader setup suggests selling into strength. The 17.50 region remains a significant resistance barrier, and the wide interest rate differential still strongly favors the Mexican peso.

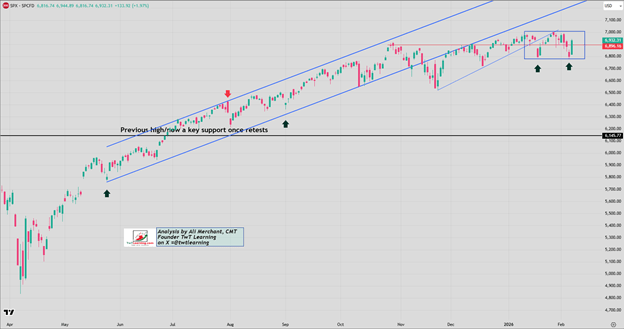

S&P 500

The S&P 500 pulled back early in the week but appears to be stabilizing as it continues to trade within a broader consolidation range. Since early December, price action has been confined between 6,800 and 7,000, suggesting a market building momentum for its next major move.

The bias still leans to the upside. A decisive daily close above 7,000 could trigger a stronger breakout and accelerate gains. On the other hand, a breakdown below 6,800 would signal a shift in tone and mark a more bearish development.

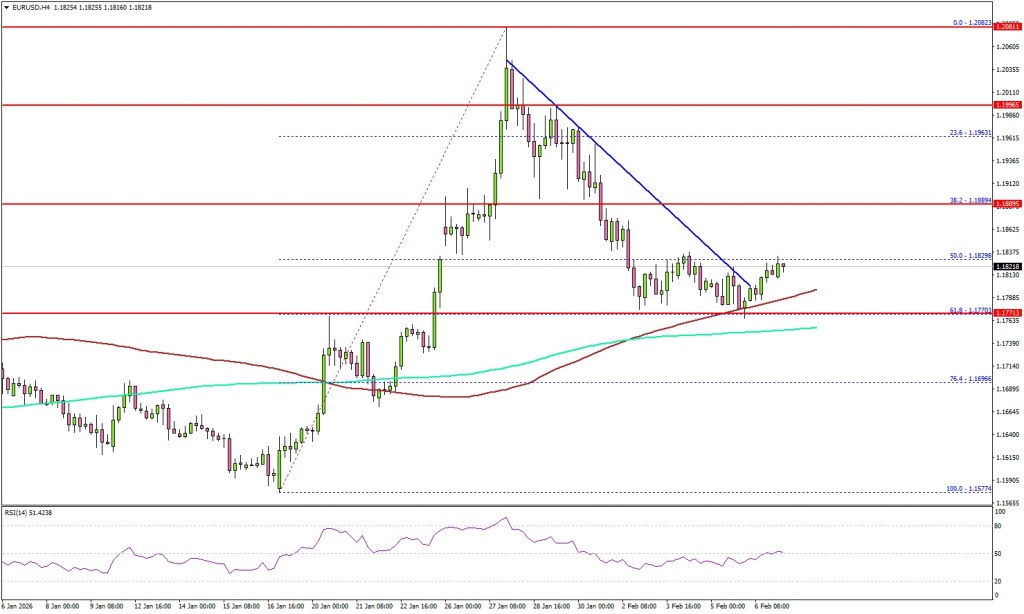

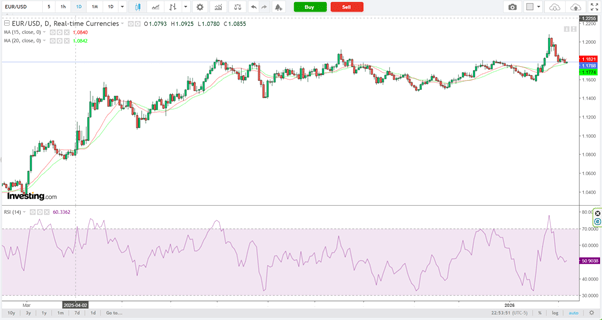

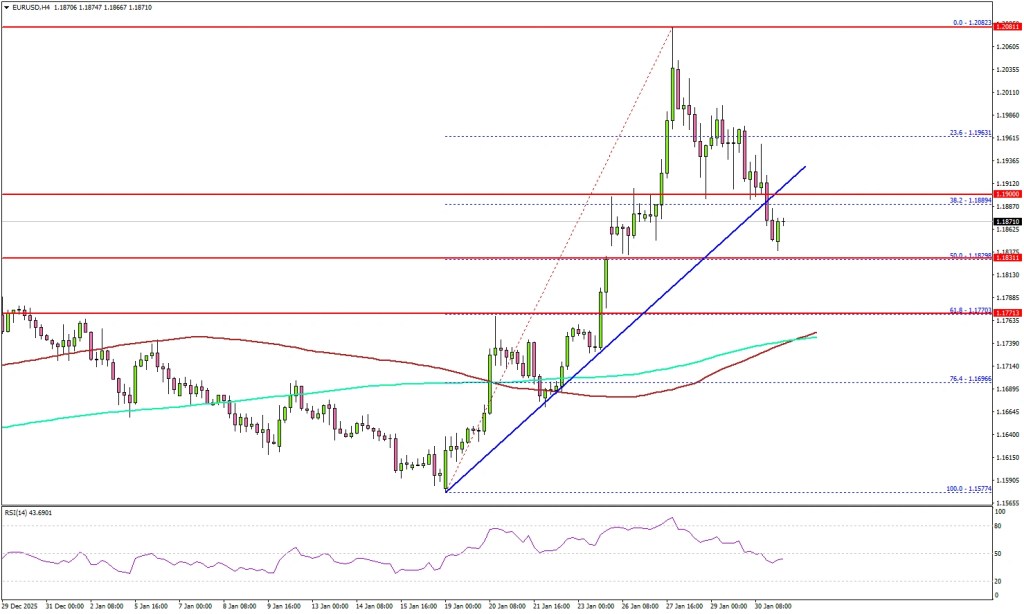

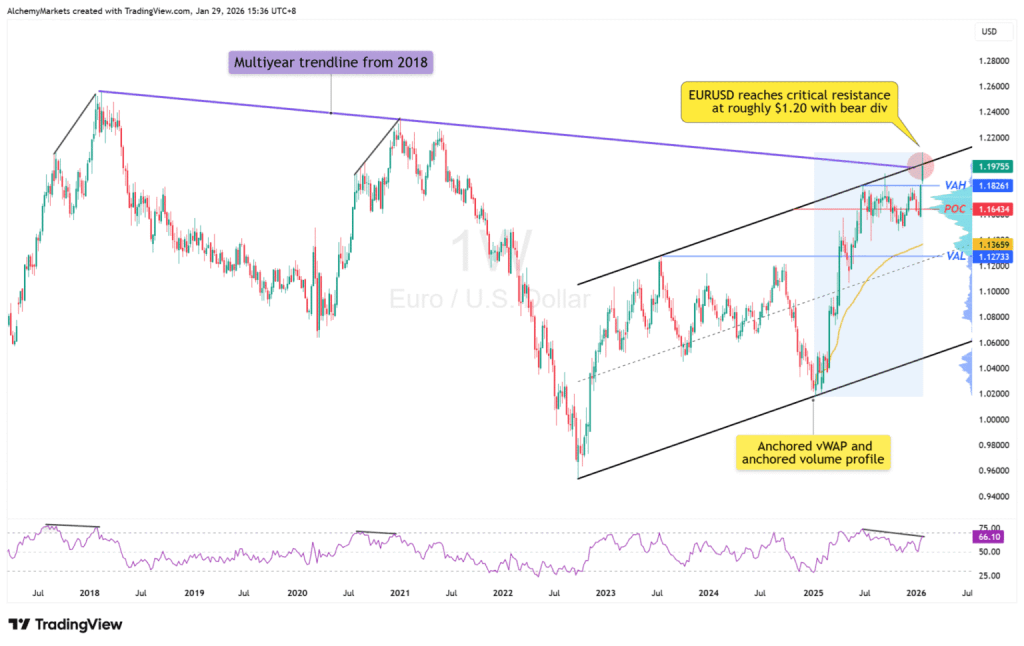

EUR/USD

The euro declined notably over the course of the week, but it continues to find buyers near the 1.18 level, making that area especially important to watch. Given the current structure, caution is warranted when trading this pair.

Price action appears largely range-bound, with 1.18 acting as a central pivot or magnet. Resistance stands near 1.1850, while solid support can be found around 1.1750, reinforcing the broader sideways pattern.

USD/CAD

The US dollar has advanced against the Canadian dollar, but price action remains choppy around the 1.3750 zone — an area that has repeatedly proven significant. The pair appears to be oscillating as traders assess whether momentum can build for a sustained move higher.

A decisive push and hold above 1.3750 would signal renewed strength for the US dollar. Conversely, a breakdown below 1.35 would represent a notably bearish shift in sentiment.

Major Technical Support and Resistance Levels

Gold (XAU/USD)

Gold remains choppy, initially easing back during the week, yet buyers continue to emerge on dips, stepping in whenever prices soften. The 4,800 level appears to be firm support, while the 5,000 mark is likely to act as a psychological magnet for price action.

The broader bias still favors buying pullbacks, with the expectation of an eventual move higher. However, volatility may persist after the sharp turbulence seen in recent weeks, following what had previously been a near one-way surge. Over the longer term, a retest of the highs seems plausible, though it will likely require patience amid ongoing fluctuations.

Bitcoin (BTC)

The Bitcoin market is still searching for renewed upside momentum, but the encouraging development is that price action has at least stabilized. Given the prolonged weakness seen in recent periods, simple stability is a constructive step forward for the market.

The $60,000 level remains a crucial support zone and a major psychological benchmark. Holding above this area is essential if Bitcoin is to maintain any realistic prospect of a sustained recovery.

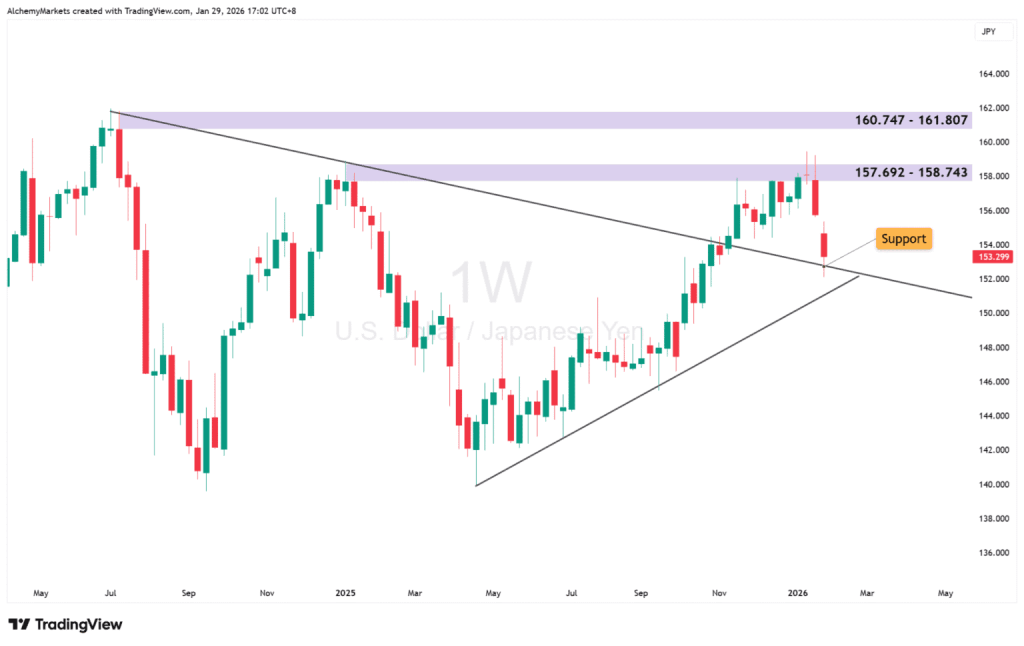

USD/JPY

The US dollar posted solid gains against the Japanese yen over the week, with the ¥152 level continuing to provide strong support. The 50-week EMA is positioned just beneath that area, reinforcing the floor and encouraging dip-buying as the interest rate differential remains in favor of the US dollar.

With the Bank of Japan maintaining its current policy stance, there appears to be little immediate catalyst for a structural shift. As a result, the pair may be entering a consolidation range between ¥152 on the downside and ¥158 on the upside. A decisive move above ¥160 would represent a significant breakout, clearing a resistance zone that has been in place since 1990.

GBP/USD

The British pound declined sharply during the week, dropping to test the 1.35 level — a large, round psychological threshold that has proven important on multiple occasions. The fact that buyers are attempting to defend this area is at least a constructive short-term signal.

However, recent UK economic data has been somewhat underwhelming. As a result, sterling may currently be one of the weaker major currencies against the US dollar. This pair deserves close monitoring, as broader dollar strength could translate into pronounced downside pressure here, potentially making GBP/USD particularly vulnerable.

The U.S. dollar edged lower on Friday as investors digested the impact of the Supreme Court’s decision to invalidate President Donald Trump’s broad tariff measures. Despite the pullback, the greenback remained on track for its strongest weekly advance since November, supported by a more hawkish tone from the Federal Reserve and ongoing geopolitical tensions between the U.S. and Iran.

As of 17:31 ET (22:31 GMT), the Dollar Index slipped 0.2% to 97.72, though it was still poised to post a weekly gain of around 1%, its best showing in nearly three months.

The Supreme Court ruled 6–3 that Trump lacked authority under the International Emergency Economic Powers Act (IEEPA) to implement sweeping reciprocal tariffs. The president criticized the decision as “deeply disappointing” and indicated that tariffs would remain in effect through alternative legal channels, alongside a new 10% global levy.

According to Jeff Buchbinder of LPL Financial, removing the tariff overhang eliminates a drag on economic growth that had been expected to lift costs and pressure corporate margins. With that risk easing, growth may stabilize and inflation expectations embedded in bond markets could cool more quickly, potentially prompting a modest reassessment of Fed rate-cut expectations and weighing slightly on the dollar.

Even so, the dollar had attracted demand earlier in the week, underpinned by resilient U.S. economic data, hawkish Fed meeting minutes, and heightened Middle East tensions.

Friday’s data, however, delivered mixed signals. Core PCE — the Fed’s preferred inflation measure — rose 0.4% month-over-month and 3.0% year-over-year in December 2025, marking the highest annual reading since November 2023 and remaining well above the 2% target. Meanwhile, preliminary fourth-quarter GDP growth came in at 1.4%, falling short of the 2.8% consensus forecast.

In Europe, EUR/USD ticked up 0.1% to 1.1781, though the euro was still headed for a 0.7% weekly decline amid uncertainty surrounding ECB President Christine Lagarde’s tenure and softer German producer price data. Analysts at ING noted that while sentiment indicators such as the ZEW survey disappointed, the eurozone composite PMI is expected to stay above the 50 threshold, limiting downside pressure on the euro.

GBP/USD rose 0.1% to 1.3474, but sterling hovered near a one-month low and was set for a weekly loss of about 1.3%. Strong January retail sales — up 1.8% month-over-month and 4.5% year-over-year — failed to provide sustained support. ING analysts said markets are pricing in a Bank of England rate cut in March, with another possible move in June, while political risks continue to weigh on the pound.

In Asia, USD/JPY held steady at 155.06 after data showed Japan’s inflation slowed to 1.5% in January, slipping below the Bank of Japan’s target for the first time in nearly four years. Core inflation excluding fresh food and fuel also moderated, reinforcing uncertainty over the timing of the next rate hike. Separate data showed Japanese factory activity expanded at its fastest pace in over four years in February.

USD/CNY was unchanged at 6.9087, with Chinese markets closed. Meanwhile, AUD/USD climbed 0.5% to 0.70892, although the Australian dollar trimmed some gains after unemployment held at 4.1% in January, signaling a still-tight but gradually cooling labor market.

Macro uncertainty is intensifying just as EUR/USD and GBP/USD test pivotal technical zones. With interest-rate expectations shifting and tail risks mounting, the next directional move may depend more on macro catalysts than chart patterns.

Both pairs are hovering near critical support and resistance levels, while a dense lineup of U.S. and European data raises the prospect of increased volatility. The dollar continues to trade in close correlation with Treasury yields and evolving Federal Reserve rate pricing, reinforcing the macro-driven backdrop.

At the same time, tariff developments and geopolitical tensions are injecting additional tail risk ahead of the weekend, leaving markets vulnerable to sharp, sentiment-driven swings.

Summary

As the week moves into its final stretch, both Europe and the United States face a heavy slate of economic releases—and this is unlikely to be mere background noise for markets. Recent price action has already underscored how reactive EUR/USD and GBP/USD are to changes in relative rate expectations across the U.S., U.K., and euro area.

With both currency pairs now positioned near critical technical thresholds, the incoming data flow carries the potential to do more than simply inject volatility. It may ultimately determine whether the latest directional moves gain traction—or begin to lose momentum and reverse.

Heavy Data Calendar Lifts Volatility Threat

Flash PMIs rarely fail to generate movement in EUR/USD and GBP/USD, largely because European participants tend to respond far more decisively to the releases than traders elsewhere. In the euro area, the focus is likely to center on price components and new orders, especially in light of the recent resilience in the single currency. In the UK, attention may gravitate toward price pressures, employment trends, and overall activity, reflecting the economy’s persistent softness.

The more consequential headline risk, however, lies in the United States. The advance Q4 GDP print stands out. While backward-looking and heavily estimate-based, it still carries the potential to influence how the dollar closes the week. An upside surprise would reinforce the narrative of U.S. exceptionalism. A downside miss, on the other hand, could reignite expectations for Federal Reserve rate cuts—expectations that have recently been scaled back after generally firm data and relatively hawkish FOMC minutes.

December’s core PCE deflator rarely delivers genuine surprises these days. Enhanced data mapping has largely diminished its shock factor, shifting attention toward the consumption and income components instead. Markets will scrutinize the consumption data for signs that recent weakness in goods demand has spilled into services, while income figures should provide a clearer indication of households’ capacity to sustain spending.

US flash PMIs, meanwhile, have produced inconsistent market reactions and are often overshadowed when more significant releases land on the same day. Broadly speaking, they have tended to exaggerate the signal seen in ISM surveys. As a result, a stronger market response may emerge if there are clear signs of softening—particularly within the services sector.

Weekend Risk Premium Builds

Beyond the dense data schedule, traders also face mounting tail risks heading into the weekend. A ruling from the Supreme Court of the United States on the legality of tariffs imposed under the International Emergency Economic Powers Act (IEEPA) could arrive around 10 a.m. U.S. time, although there is no certainty a decision will be issued today. Even the possibility is sufficient to keep markets cautious, given the potential implications for Treasury yields and overall risk sentiment.

At the same time, Donald Trump has set a 10-day deadline for Iran to reach a deal or face potential military action. Considering the risks to global energy supply—and the United States’ position as a major energy producer—any pre-emptive strike would likely support the dollar against European currencies, particularly if it sparks a renewed wave of risk aversion.

Regarding tariffs, the market reaction may remain relatively muted regardless of the court’s decision—unless investors begin to question whether any shortfall in government revenues can be covered through alternative channels. Should doubts arise on that front, both the dollar and longer-dated Treasuries could face meaningful downside pressure as fiscal concerns move to the forefront.

Dollar Catalysts Return to Center Stage

Underscoring the significance of the upcoming data and event risk, the US Dollar Index (DXY) has shown a notably tight correlation over the past week with Fed rate-cut expectations, front-end yield differentials, US two-year Treasury yields, and even Brent crude, as illustrated in the middle panel of the chart above. In practical terms, the dollar has reverted to trading primarily as a rates-and-yields narrative, with an added layer of sensitivity to energy prices.

Yet the 20-day correlation metrics shown on the right paint a much less compelling picture. Over the past month, these relationships have been weak and statistically insignificant, serving as a reminder that the recent alignment may prove temporary rather than structural.

GBP/USD Faces Growing Downside Pressure

As discussed in earlier analysis this week, the release of key UK labour market and inflation figures acted as the catalyst that pushed GBP/USD out of its consolidation phase. Combined with firm U.S. data, the move triggered a decisive break below multiple technical markers, including the November uptrend and the 50-day moving average, before finding support at the 200-day moving average. Whether assessed through pure price action or momentum indicators, the bias now tilts toward increasing downside risk.

The 14-period RSI continues to trend lower below the 50 mark, while MACD has crossed beneath its signal line and moved into negative territory—both reinforcing the build-up of bearish momentum. As a result, selling rallies appears more favorable than buying dips. That said, the pair’s proximity to the 200DMA provides a clearly defined reference point for structuring trades as incoming data and headlines shape sentiment.

A sustained break below the 200DMA would strengthen the bearish case, opening the door for short positions with stops placed just above the average. Initial downside targets would sit at 1.3371, followed by 1.3300 and 1.3250. Conversely, if price manages to hold above the 200DMA, the setup could shift tactically. Long positions above the level, with stops placed beneath, would target 1.3535—a zone where several technical indicators, including the 50DMA, currently converge. A reclaim of that area would undermine the newly established bearish bias and shift directional risks back toward a sideways-to-higher outlook.

Triangle Formation Brings Breakout Levels Into View

With EUR/USD coiling within a descending triangle and momentum indicators drifting lower, downside risks appear to be gradually building. A decisive break beneath the confluence of the 50-day moving average and horizontal support at 1.1768 may prove pivotal in unlocking further weakness. Thursday’s doji candle aligns with that narrative, highlighting a degree of indecision among market participants at a technically sensitive juncture.

While the bearish case in GBP/USD looks more straightforward—given recent UK data and the repricing of Bank of England rate expectations—the outlook for the euro is less clear-cut. That ambiguity reinforces the importance of upcoming data and headlines in shaping near-term direction. RSI (14) has slipped just below 50, offering a neutral-to-soft signal, while MACD has rolled over but remains marginally above zero, underscoring the lack of decisive momentum so far.

The descending triangle structure keeps the downside break scenario firmly in focus, but confirmation is still required. A sustained break and close below the 50DMA/1.1768 area would strengthen the bearish case, with short positions targeting 1.1684 initially, followed by the 200-day moving average. Stops could be placed just above the broken support zone for protection.

Conversely, if the pair manages to hold this confluence area, a tactical long setup may be considered with tight stops below, initially targeting the January downtrend line. Should price test but fail to clear that trendline convincingly, it may favor squaring positions or re-establishing shorts with stops above, aiming for a retest of the 50DMA/1.1768 region. A clean upside breakout, however, would alter the landscape, opening scope toward 1.1837 and potentially 1.1918, shifting directional risks back toward a sideways-to-higher bias.

Here’s what you need to know for Friday, February 20:

The US Dollar Index (DXY) maintains its upward momentum, hovering near 98.00 after reaching a near one-month high on Thursday. The economic agenda for Friday features preliminary February Purchasing Managers’ Index (PMI) data from Germany, the Eurozone, the UK and the US. The spotlight, however, will be on the first estimate of fourth-quarter Gross Domestic Product (GDP) growth and the December Personal Consumption Expenditures (PCE) Price Index, both to be released by the US Bureau of Economic Analysis.

The US Dollar outperformed major peers on Thursday amid a risk-off market tone fueled by rising tensions between the US and Iran. According to BBC, US President Donald Trump warned that Iran must strike a deal or face serious consequences. Iran, in communication with UN Secretary-General Antonio Guterres, stated it does not seek conflict but would not tolerate military aggression. Iranian officials also reportedly cautioned that any US military move over the nuclear issue would be met with a decisive response. Early Friday, US stock index futures were modestly higher.

The US economy is expected to have expanded at an annualized pace of 3% in Q4, following a 4.4% increase in the prior quarter. Meanwhile, the core PCE Price Index — the Federal Reserve’s preferred inflation gauge — is forecast to rise 2.9% year-over-year in December, up slightly from 2.8% in November.

EUR/USD, which closed lower on Thursday, remains under pressure early Friday, trading near 1.1750. PMI figures from Germany and the Eurozone are anticipated to continue signaling expansion in private-sector activity for February.

GBP/USD extended its decline for a fourth straight session on Thursday and trades below 1.3450, marking its weakest level since late January. Data from the UK’s Office for National Statistics showed that Retail Sales climbed 1.8% month-over-month in January, significantly beating the 0.2% consensus estimate.

USD/JPY continues its weekly advance and holds comfortably above 155.00 in early Friday trading. Japan’s Prime Minister Sanae Takaichi stated that necessary expenditures would largely be financed through the initial budget, adding that efforts would be made to gradually reduce the debt-to-GDP ratio and restore fiscal discipline. Japan’s National Consumer Price Index rose 1.5% in January, down from 2.1% in December.

Gold benefited from safe-haven demand on Thursday but struggled to build momentum amid broad USD strength. XAU/USD edges higher during the European session on Friday, trading above $5,000.

In Australia, flash data from S&P Global showed the Composite PMI easing to 52 in February from 55.7 in January. AUD/USD largely brushed off the release and was last seen slightly lower on the day near 0.7050.

The United Kingdom is set to release its preliminary February Purchasing Managers’ Index (PMI) figures, with the data scheduled to be published by S&P Global on Friday at 09:30 GMT.

The Services PMI is forecast at 53.6, slightly lower than January’s reading of 54.0, signaling a modest slowdown in services sector growth.

Potential Impact on GBP/USD

If the Services PMI prints in line with expectations, GBP/USD could face pressure, as a softer services reading may counterbalance the recent strength seen in UK Retail Sales.

UK Retail Sales rose 1.8% month-over-month in January, well above December’s 0.4% gain and surpassing the 0.2% market forecast. Core Retail Sales increased 2.0% over the same period, improving from a 0.3% rise previously and exceeding expectations for a 0.2% uptick.

However, the pair may remain under strain as the US Dollar stays firm following the release of the January meeting minutes from the Federal Open Market Committee. The minutes revived speculation that the Federal Reserve could consider further rate hikes if inflation proves persistent. Although most officials favored holding rates steady, only a minority supported a cut, and policymakers suggested easing could be appropriate if inflation slows as projected.

From a technical standpoint, GBP/USD has stabilized after rebounding from daily losses, hovering near 1.3460 at the time of writing. Daily chart analysis points to a developing bearish tone, with the pair trading below an ascending channel formation. Immediate support is located near the two-month high of 1.3344. On the upside, resistance is seen at the 50-day EMA around 1.3524, followed by the nine-day EMA near 1.3548.

USD/JPY is consolidating Wednesday’s strong advance, hovering near the 155.00 mark early Thursday. The bullish bias remains intact as concerns over Japan’s fiscal outlook and a generally positive market sentiment continue to weigh on the safe-haven Japanese Yen.

At the same time, the latest FOMC Minutes revealed divisions among Fed officials regarding the need and timing of additional rate cuts amid lingering inflation risks. This uncertainty lends support to the US Dollar, providing an added tailwind for the pair.

USD/JPY Technical Overview

The US Dollar (USD) is trading with a mild bullish bias against the Japanese Yen (JPY) this week, hovering near the top of the 153.00 range. However, the pair remains confined within its weekly boundaries, as resistance around 154.00 continues to cap upside attempts ahead of the release of the minutes from the US Federal Reserve’s latest meeting.

Fundamental Overview

The Federal Reserve kept its benchmark rate unchanged at 3.5%–3.75% and signaled that policy is likely to remain steady in the near term. The meeting minutes are expected to underscore divisions within the committee—differences that are drawing added attention after last week’s softer U.S. inflation data and disappointing jobs report.

On Tuesday, Chicago Fed President Aistan Goolsbee pointed to those internal splits, noting that if inflation continues to ease, the central bank could lower rates multiple times this year.

In Japan, weak fourth-quarter GDP data released Monday have renewed worries about the country’s economic prospects, reinforcing Prime Minister Sanae Takaichi’s push for substantial fiscal stimulus and tax cuts.

Meanwhile, the International Monetary Fund cautioned that reducing the consumption tax could strain public finances and urged the Bank of Japan to tighten monetary policy further to keep inflation in check. As a result, the yen’s recent bullish momentum has faded somewhat, offering relief to the previously pressured U.S. dollar.

The US Dollar Index (DXY) is taking a breather after climbing to a more than one-week high in the previous session, trading in a tight range around 97.70 during Thursday’s Asian session and holding steady on the day.

Minutes from the Federal Reserve’s January meeting showed policymakers split over the timing and need for further rate cuts, given lingering inflation concerns. While some officials suggested additional easing could be appropriate if inflation cools as projected, others warned that cutting rates too soon might jeopardize the Fed’s 2% target. The relatively less dovish tone has helped curb expectations for aggressive policy easing and continues to lend support to the US dollar.

The upbeat January Nonfarm Payrolls report released last week has also reinforced the case for a cautious approach from the Fed, further underpinning the greenback. In addition, reports that the US military could be ready to strike Iran as soon as this weekend are keeping geopolitical risks elevated, sustaining demand for the dollar’s safe-haven appeal.

However, markets are still pricing in the likelihood of at least two Fed rate cuts in 2026. Softer US consumer inflation data released last Friday, combined with a generally positive risk tone, has limited stronger bullish momentum in the dollar. Attention now turns to Friday’s US Personal Consumption Expenditure (PCE) Price Index, which may offer fresh direction for the DXY.

GBP/USD is struggling to stage a meaningful rebound after dropping to a four-week low in Thursday’s Asian session, with the pair hovering just below the 1.3500 psychological level and appearing vulnerable to further losses. It is currently consolidating declines recorded over the past three days within a tight range near weekly lows.

The British pound remains under pressure amid growing expectations that the Bank of England will deliver a rate cut at its March meeting. Those bets were reinforced by weaker UK employment data and a slowdown in consumer inflation to its lowest level in nearly a year. Combined with a firm US dollar, this keeps the near-term bias tilted to the downside for GBP/USD.

Meanwhile, minutes from the Federal Reserve’s January meeting revealed divisions among policymakers regarding the timing and need for additional rate cuts, given persistent inflation concerns. While some officials signaled that easing could be appropriate if inflation continues to cool, others warned that premature cuts might jeopardize the Fed’s 2% target. The relatively less dovish tone has helped underpin the US dollar.

Geopolitical tensions also remain in focus, with reports suggesting the US military could be ready to strike Iran as soon as this weekend. Such risks have supported safe-haven demand for the greenback, allowing it to hold onto recent gains and reinforcing the case for an extension of the pair’s weekly downtrend. Any attempted recovery in GBP/USD may therefore attract fresh selling interest.

Traders now turn to Thursday’s US data releases, including weekly initial jobless claims, the Philadelphia Fed Manufacturing Index, and pending home sales. Speeches from key FOMC members are also due later in the North American session, though attention will ultimately center on Friday’s US Personal Consumption Expenditures (PCE) Price Index for clearer policy direction.

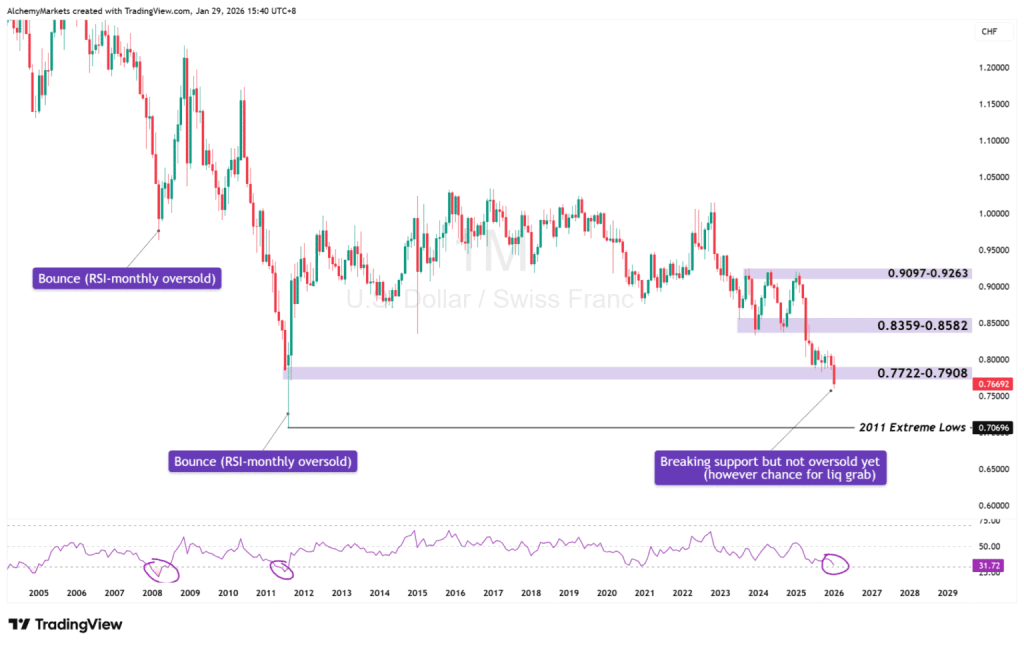

USD/CHF remains under pressure as the Swiss franc benefits from safe-haven inflows amid ongoing geopolitical tensions.

The pair trades near 0.7720 in Asian session dealings on Thursday, holding in negative territory after trimming earlier losses. The franc draws support from persistent strains between the United States and Iran, as well as stalled Russia-Ukraine negotiations. Investors are also looking ahead to Switzerland’s Trade Balance and Industrial Production figures due later in the day.

Additional support for the Swiss currency stems from expectations that the Swiss National Bank (SNB) will keep policy accommodative in the near term. January inflation in Switzerland came in at 0.1%, staying at the lower edge of the SNB’s 0–2% target band and matching its first-quarter forecasts, reinforcing market views.

SNB President Martin Schlegel recently noted that the central bank can tolerate brief periods of negative inflation while prioritizing medium-term price stability, adding that the threshold for a return to negative interest rates remains high.

Still, downside in USD/CHF may be limited as the US dollar stabilizes after rising more than 0.5% in the previous session, supported by hawkish Federal Reserve meeting minutes. The January FOMC minutes rekindled expectations that rates could be raised again if inflation remains persistent. While most policymakers favored keeping rates unchanged, only a small number supported cuts, and officials indicated a willingness to ease policy should inflation moderate as anticipated.

U.S. stock futures drifted near the flatline Tuesday as investors braced for a wave of economic data and corporate earnings in a holiday-shortened week.

As of 03:04 ET, Dow futures were down 26 points (0.1%), S&P 500 futures slipped 11 points (0.2%), and Nasdaq 100 futures dropped 99 points (0.4%). Wall Street’s main indexes were closed Monday for a public holiday.

Markets ended Friday mixed, with investors weighing the broader impact of new artificial intelligence models and questioning whether heavy AI infrastructure spending will generate strong returns for mega-cap tech firms. At the same time, cooler-than-expected U.S. consumer price data for January fueled expectations that the Federal Reserve could bring forward its next interest rate cut after pausing its easing cycle last month. The tech-heavy Nasdaq Composite edged down 0.2%, while the S&P 500 and Dow Jones Industrial Average posted gains.

Crude prices steady ahead of U.S.-Iran negotiations

In commodities, Brent crude ticked lower ahead of planned talks between the U.S. and Iran in Geneva over Tehran’s nuclear enrichment program. A firmer dollar, ahead of key economic releases and signals from the Fed, also weighed on oil prices. Brent for April delivery fell 0.7% to $68.13 a barrel, while West Texas Intermediate futures rose 0.6% to $63.11, with the move partly influenced by Monday’s U.S. market holiday.

U.S. and Iranian officials are scheduled to meet in Switzerland on Tuesday amid elevated tensions in the Middle East, as Washington increases its regional military presence. President Donald Trump has repeatedly warned of potential military action if Iran declines a U.S.-backed agreement.

Trading activity was subdued across Asia due to Lunar New Year holidays in China, Hong Kong, Taiwan, South Korea, and Singapore.

Gold declines

Gold prices moved lower Tuesday, with silver also retreating, as traders stayed cautious ahead of a slate of U.S. economic data due this week.

At 03:09 ET, spot gold fell 1.4% to $4,919.72 an ounce, while April gold futures dropped 2.2% to $4,941.74. Spot silver slid 2.0% to $75.0925 per ounce, whereas platinum edged up 0.2% to $2,024.79.

Precious metals have been volatile in recent weeks, posting sharp swings and remaining well below their late-January highs.

Investor focus is shifting to upcoming U.S. economic releases, along with minutes from the January meeting of the Federal Reserve, when policymakers kept interest rates unchanged at 3.5% to 3.75%.

U.S. industrial production figures are scheduled for release on Wednesday, followed by Friday’s PCE price index report — one of the Fed’s key measures of inflation.

Palo Alto Networks earnings ahead

Attention is also turning to results from Palo Alto Networks, due after U.S. markets close Tuesday, which could offer further insight into the outlook for tech firms grappling with rising competition from newly launched AI models.

The California-based cybersecurity group raised its full-year revenue and profit guidance in November, pointing to strong demand for its digital security solutions amid growing online threats.

Palo Alto also unveiled a $3.35 billion acquisition of cloud management and monitoring firm Chronosphere, saying it plans to fold the business into its Cortex AgentiX platform. The integration is designed to allow Palo Alto’s AI agents to leverage Chronosphere’s data to identify performance bottlenecks and pinpoint root causes more effectively.

Together with a separate agreement to acquire identity security specialist CyberArk Software, the Chronosphere transaction is slated to be finalized in the second half of Palo Alto’s fiscal 2026.

Nikkei extends slide

Japan’s benchmark Nikkei 225 slipped again, adding to Monday’s losses after data showed the country’s economy grew far less than expected in the fourth quarter.

Official figures revealed that gross domestic product expanded at an annualized rate of 0.2% in the October–December period — well below forecasts of 1.6%. Still, the reading marked a rebound from the prior quarter, when the world’s fourth-largest economy contracted by 2.6%.

The weak data highlights the economic hurdles facing Prime Minister Sanae Takaichi following her sweeping election victory earlier this month. While she appears to have secured a mandate to implement stimulus measures aimed at boosting growth, her government must contend with persistent cost-of-living pressures that continue to dampen domestic demand.

Adding to the complexity is the stance of the Bank of Japan, where policymakers are working to address stubborn inflation and yen weakness. Officials have indicated they intend to continue raising interest rates after years of ultra-loose monetary policy.

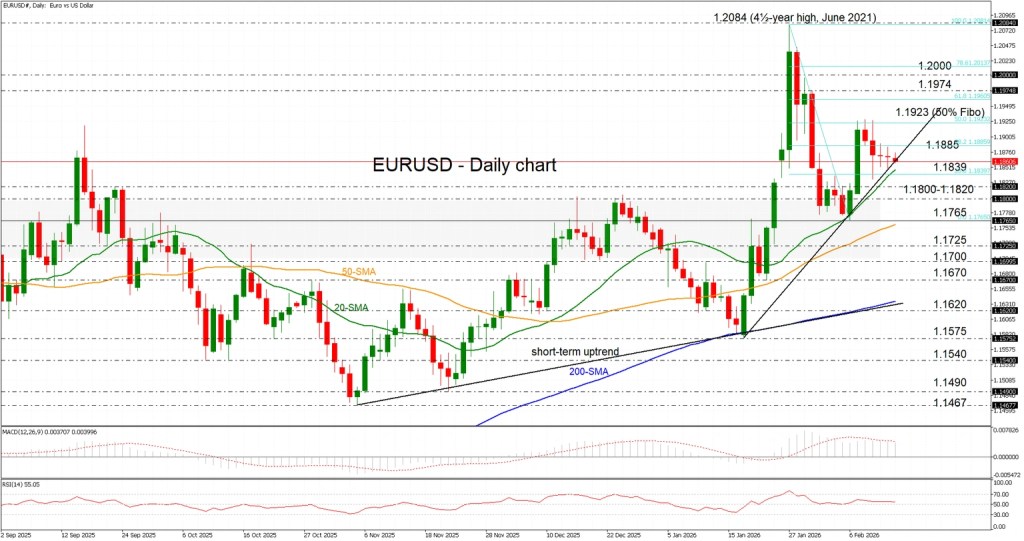

EUR/USD is slipping for a fifth consecutive session, though it continues to trade above the crucial 20-day SMA. Momentum indicators remain in positive-to-neutral territory, with the RSI hovering slightly above its midpoint and flattening, while the MACD stays above zero but just below its signal line — a sign that upside momentum has eased without fully turning bearish.

The pair is stabilizing around 1.1865, extending its retreat from the 1.1900 area even as the US dollar softened on Friday following weaker inflation data that strengthened expectations of Fed rate cuts. Trading conditions are relatively quiet on Monday due to the US President’s Day holiday.

If price rebounds from the short-term ascending trendline and breaks above the 38.2% Fibonacci retracement of the January 27–February 6 decline at 1.1885, the next resistance could appear near 1.1923, which aligns with the 50% Fibonacci level and recent monthly highs. A stronger push higher may target the 1.1960–1.1974 zone, just beneath the key 1.2000 mark — the highest level since mid-2021.

On the downside, further weakness could bring the pair back toward the 20-day SMA near the 23.6% Fibonacci level at 1.1839. Below that, attention would shift to the 1.1800–1.1820 area, followed by the February 6 low of 1.1765, which sits just above the 50-day SMA.

Overall, despite the recent pullback, the near-term outlook remains constructive as long as EUR/USD holds above the 20-day SMA, with the 50-day SMA acting as stronger support in case of a deeper correction.

The US dollar initially weakened against the Canadian dollar earlier in the week, slipping toward the 1.35 level before rebounding and showing renewed strength. This recovery is shaping a potential weekly hammer pattern. A break above the 1.3750 level could pave the way for further gains toward 1.40. Overall, the pair is likely to remain range-bound, continuing to trade within the broad sideways band that has held for more than a year.

EUR/USD

The euro climbed at the start of the week but now appears to be losing momentum, struggling to hold on to its gains. Traders are likely assessing whether the broader uptrend can be sustained. With the US dollar having been oversold against several currencies, the euro often serves as a key gauge for the greenback’s next move. Even if the pair breaks higher, the measured move from the prior consolidation range indicates that the upside may be limited to around 1.23.

GBP/USD

The British pound advanced early in the week but later surrendered roughly half of those gains amid continued choppy trading. The 1.3750 level remains a key area to monitor, as a decisive break above it could clear the path toward 1.39. On the downside, a pullback would likely find support around 1.35, followed by 1.33 if selling pressure intensifies. Overall, the US dollar appears to be regaining some strength.

USD/MXN

The US dollar has weakened further against the Mexican peso, with the pair appearing to drift toward the 17.00 level. A decisive break below that mark could open the door to a move toward 16.50. On the upside, any rebound is likely to face significant resistance around 17.50. That said, the pair may ultimately settle into a consolidation phase, similar to the range observed at this level in late 2023.

Silver

Silver remains highly erratic, with the week producing a volatile yet ultimately neutral candlestick. The $80 level appears to act as a pivot point and a magnet for price action. Strong support is seen near $70, while $90 stands out as a key resistance zone. Overall, the market is likely to continue exhibiting choppy and unpredictable movements.

Gold

Gold also moved in a back-and-forth manner throughout the week, with the $5,000 level emerging as a potential price magnet. A sustained break above $5,000 could signal the start of a stronger upward move. However, recent candlestick patterns tell a mixed story: a prominent Shooting Star formed a couple of weeks ago, followed by a hammer, suggesting ongoing uncertainty and likely consolidation. Still, the longer price holds near the $5,000 mark, the more it may indicate underlying bullish strength.

USD/CHF

The US dollar has declined against the Swiss franc, though the 0.76 level appears to be providing solid support. If the pair rebounds from this area, it could move toward the 0.79 level, which stands out as significant resistance. Overall, the market remains sensitive to potential action from the Swiss National Bank, and the risk of intervention if the franc strengthens too much makes taking short positions less appealing at this stage.

USD/JPY

The US dollar dropped sharply against the Japanese yen over the week and is now testing its 50-week EMA. A rebound from this area could see the pair target ¥156, with ¥158 as the next potential objective. On the longer-term charts, the ¥160 level—where price pulled back a few weeks ago—remains a significant resistance zone dating back to 1990.

Although this week’s candlestick appears bearish, there are likely plenty of buyers waiting below. It may simply be a matter of allowing the market to stabilize before considering fresh long positions. For now, it’s a pair worth monitoring closely, but staying on the sidelines seems prudent.

Here’s what you need to know for Monday, February 16:

Major currency pairs begin the week trading within established ranges, as investors remain cautious ahead of several key events and important macroeconomic releases scheduled for later in the week. In Europe, December Industrial Production figures are due on Monday. Meanwhile, US stock and bond markets are closed for the Presidents Day holiday.

The US Dollar Index ended last week on a softer note, as below-forecast inflation data prevented the greenback from gaining momentum before the weekend. According to the US Bureau of Labor Statistics, annual Consumer Price Index (CPI) inflation slowed to 2.4% in January from 2.7% in December, undershooting expectations of 2.5%. Early Monday, the USD Index is moving sideways around the 97.00 mark during European trading hours.

Early Monday, CBS News reported—citing two sources—that US President Donald Trump told Israeli Prime Minister Benjamin Netanyahu he would back Israeli strikes targeting Iran’s ballistic missile program. So far, markets have shown little reaction, with West Texas Intermediate crude trading largely flat near $62.80 per barrel.

EUR/USD remains in consolidation mode, hovering just above 1.1850 after ending last week slightly higher. European Central Bank policymaker Joachim Nagel is expected to speak later in the day.