OPEC+ delegates indicated that the group is expected to keep oil production steady at their upcoming meeting on Sunday, despite ongoing political tensions between key members Saudi Arabia and the UAE, as well as the recent U.S. capture of Venezuela’s president.

The Sunday meeting involves eight OPEC+ members—Saudi Arabia, Russia, the UAE, Kazakhstan, Kuwait, Iraq, Algeria, and Oman—who together produce about half of the world’s oil supply. This session follows a challenging 2025, during which oil prices plunged over 18%, marking their steepest annual decline since 2020 amid concerns over oversupply.

From April to December 2025, these eight members raised oil output targets by roughly 2.9 million barrels per day, representing nearly 3% of global oil demand. They agreed in November to pause further output increases for January through March 2026.

According to three OPEC+ sources, Sunday’s meeting is unlikely to alter this policy.

OPEC Faces Multiple Crises Amid Market and Political Challenges

Tensions between Saudi Arabia and the UAE escalated last month over a decade-long conflict in Yemen, when a UAE-aligned group seized territory from the Saudi-backed government. This crisis sparked the biggest rift in decades between the former close allies, exposing years of divergence on key issues.

Historically, OPEC has managed to navigate serious internal disputes—such as during the Iran–Iraq War—by prioritizing market stability over political conflicts. However, the group now faces multiple challenges. Russian oil exports remain under pressure from U.S. sanctions related to the Ukraine war, while Iran grapples with widespread protests and threats of U.S. intervention.

These overlapping crises put OPEC’s cohesion and its ability to manage the global oil market to a critical test.

On Saturday, the United States reportedly captured Venezuelan President Nicolás Maduro. U.S. President Donald Trump announced that Washington would assume control of the country until a transition to a new administration can be arranged, though he did not specify how this process would be carried out.

Venezuela holds the world’s largest proven oil reserves, surpassing even those of OPEC’s leader, Saudi Arabia. However, its oil production has sharply declined over the years due to chronic mismanagement and international sanctions.

Analysts caution that a significant increase in crude output is unlikely in the near future, even if U.S. oil majors follow through on the multibillion-dollar investments promised by President Trump.

Financial markets extended the holiday-thinned mood on the first trading day of the new year, with investors largely staying on the sidelines. Markets remain in a wait-and-see mode ahead of a data-heavy week.

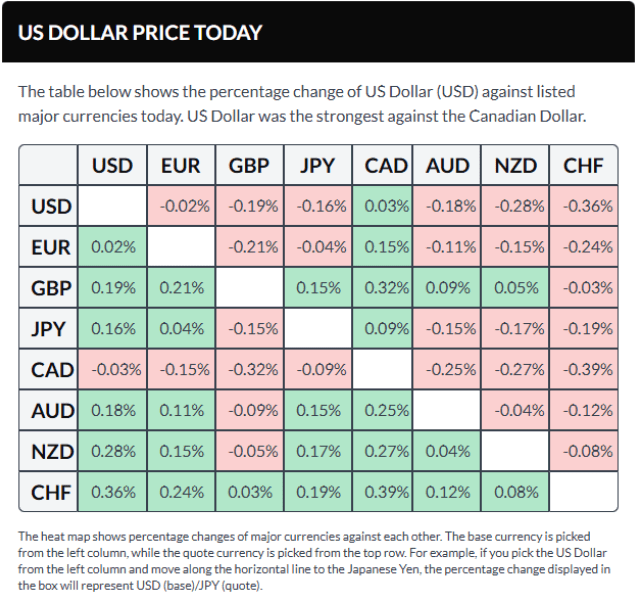

The US Dollar Index (DXY) traded near the 98.40 area on Friday, paring a significant portion of its New Year losses.

Gold (XAU/USD) traded around the $4,320 level, surrendering all intraday gains following the New Year’s break. Expectations of lower US interest rates and elevated geopolitical tensions have continued to support precious metals in recent sessions.

EUR/USD hovered near 1.1740 after edging lower earlier in the week, remaining under pressure as investors await upcoming economic data.

GBP/USD traded close to the 1.3480 area, little changed during the first US session of the year.

USD/JPY hovered around the 156.50 region, trading slightly lower on the day with limited intraday movement.

AUD/USD traded near the 0.6690 area on Friday, posting modest gains after paring nearly half of its intraday advance.

Key Economic Data Ahead: Upcoming Releases Set to Shape Market Sentiment

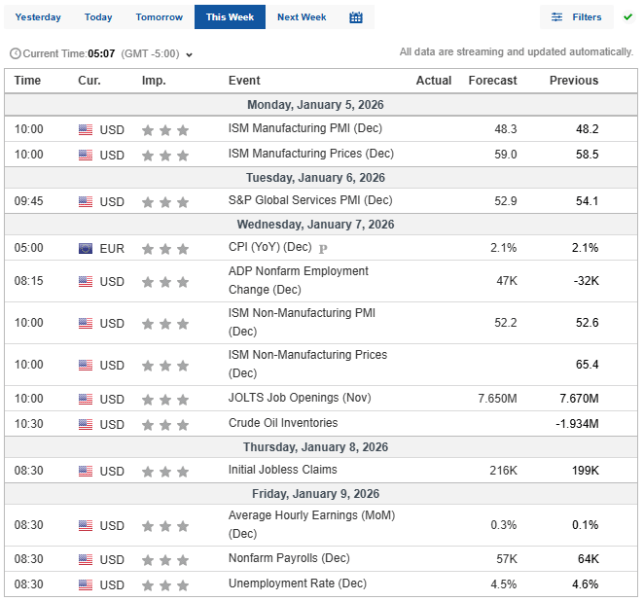

Over the coming days, investors will closely watch US employment figures and global inflation data, which are expected to influence central bank policies.

Monday: The US Institute for Supply Management (ISM) releases the Manufacturing Purchasing Managers’ Index (PMI) for December.

Tuesday: Germany’s Harmonized Index of Consumer Prices (HICP) and Australia’s Consumer Price Index (CPI) are scheduled for publication.

Wednesday: The US ADP Employment Change report (December), ISM Services PMI (December), and the preliminary Eurozone HICP (December) will be released.

Thursday: The US Trade Balance for October and Consumer Credit data for November are due.

January 9: The highly anticipated US Nonfarm Payrolls (NFP) report for December and the preliminary January Michigan Consumer Sentiment Index will be published.

These releases are expected to set the tone for market direction and provide clues on the pace of monetary tightening by major central banks.

Gold and silver prices rose as investors sought safe-haven metals amid heightened geopolitical tensions following the U.S. capture of Venezuelan leader Nicolás Maduro.

The capture of Venezuela’s President Maduro has raised concerns about how quickly the country can increase oil production, with analysts skeptical about major oil companies committing new investments amid the ongoing uncertainty.

Crude oil prices fluctuated as traders weighed the impact of Maduro’s capture on global supply and Venezuela’s energy sector. Brent crude dropped up to 1.2% before bouncing back near $61 per barrel, while WTI stayed above $57. Despite the instability, Venezuela remains a relatively small supplier in an already oversupplied market.

U.S. airlines are resuming Caribbean routes after a U.S. military operation in Venezuela caused regional airspace closures, which stranded thousands of travelers. Airlines like American and Delta responded by adding extra flights and larger planes, with American alone providing nearly 5,000 additional seats.

Upcoming jobs data, particularly the January 9 report, is set to influence markets. Labor market softness prompted the Fed to cut rates in its last three meetings in 2025, supporting stocks, but the potential for further rate cuts in 2026 remains uncertain.

The S&P 500 slipped toward the end of the year but still posted a strong 16% gain for 2025. January promises to be busy, with Q4 earnings and crucial inflation figures scheduled for release.

Dow Jones futures dipped slightly Sunday night, while S&P 500 and Nasdaq futures edged up. Over the weekend, former President Donald Trump claimed that the U.S. would “run” Venezuela following the capture of President Nicolás Maduro, though Maduro’s government remains intact.

The annual CES technology conference officially begins Tuesday in Las Vegas, with artificial intelligence expected to take center stage. CES 2026 will showcase major presentations from AI chip leaders Nvidia (NASDAQ: NVDA) and Advanced Micro Devices (NASDAQ: AMD), highlighting AI’s tangible applications across devices—from smart glasses and wearable life-loggers to robotaxis and humanoid robots.

Industrial technology will also receive attention, with keynote speeches from the CEOs of Caterpillar (NYSE: CAT) and Siemens (SIEGY). The four-day event will run through Friday.

Nvidia, AMD, and Taiwan Semiconductor Manufacturing (NYSE: TSM) will be key players at CES 2026 in Las Vegas.

$NVDA – Jensen Huang’s keynote: January 5 at 4:00 PM ET

$AMD – Lisa Su’s keynote: January 5 at 9:30 PM ET

$MRVL – Matt Murphy’s fireside chat: January 6 at 12:00 PM ET

$TSM – Monthly sales data release: January 9

Stocks dropped in the final trading session of 2025, causing the S&P 500 to register a loss for December. However, the index still posted a strong gain of over 16% for the year, marking its third consecutive year with double-digit growth, while the VIX remained near yearly lows.

After a quiet year-end, 2026 is expected to start actively with important economic reports, a Supreme Court decision on President Trump’s tariffs, his nominee for the next Federal Reserve chair, and the beginning of earnings season. Although next week’s earnings calendar is relatively light, a few companies such as AAR (NYSE: AIR), Commercial Metals (NYSE: CMC), and Acuity (NYSE: AYI) are scheduled to report.

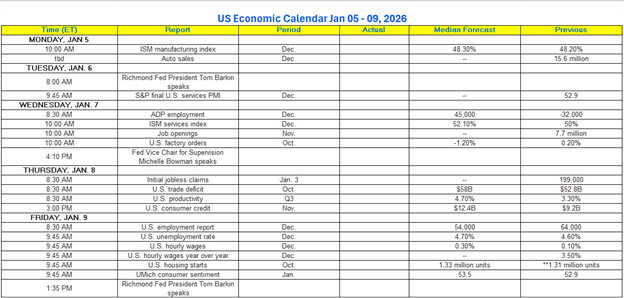

US Economic Data

A series of key economic reports will be released during the first full week of January. Scheduled releases include the ISM manufacturing and services indexes, Commerce Department data on housing starts and building permits, and the Labor Department’s JOLTS report. The highlight will be Friday’s release of December payrolls.

On December 30, the Chicago Fed reported that its labor market model indicated only minor shifts in layoffs, quits, and hiring of unemployed workers for the month, projecting the unemployment rate to remain steady at 4.56%.

The tech boom and onshoring efforts are set to trigger a significant surge in capital spending. The majority of this investment is expected from the “Big Four” tech giants—Microsoft, Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOGL), and Meta (NASDAQ: META)—all of which have indicated their 2026 capital expenditures will likely surpass those of 2025.

The “Magnificent 7” — which includes Microsoft, Amazon, Alphabet, Meta, Apple (NASDAQ: AAPL), Nvidia, and Tesla (NASDAQ: TSLA) — are projected to collectively invest over $500 billion in capital expenditures in 2026. Although not officially committed to this amount, their guidance in late 2025 suggests an acceleration of substantial AI infrastructure spending in the coming year.

Onshoring also plays a crucial role in driving capital investment, as the Trump administration’s tariff team has secured commitments from foreign governments and companies to establish manufacturing facilities in the U.S. in return for reduced tariff rates.

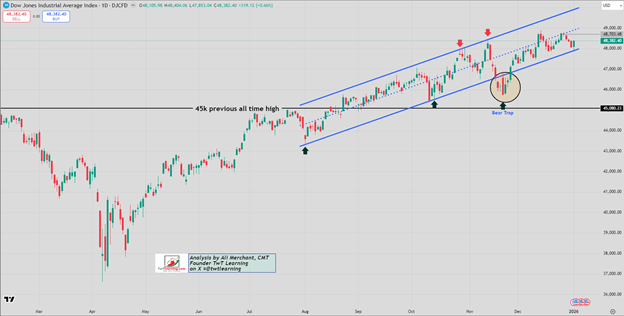

Technical Analysis

DJIA Index

The DJIA continues to trade within an upward channel that began from the lows in August 2025. On Friday, December 26, 2025, the index was unable to move above the channel’s midpoint. Support is found near the lower boundary of the channel, around 47,900. A decisive move either above or below this 47,900 level will likely determine the next direction for the index.

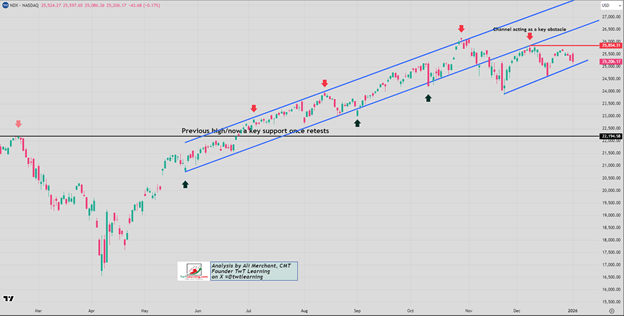

Nasdaq 100 Index

The NDX continues to face resistance in the 25,870–25,900 range. As long as this resistance holds, the index is expected to trade within a range between 25,900 and 24,645. A clear break below the 25,000 level could pave the way for a decline toward 24,645.

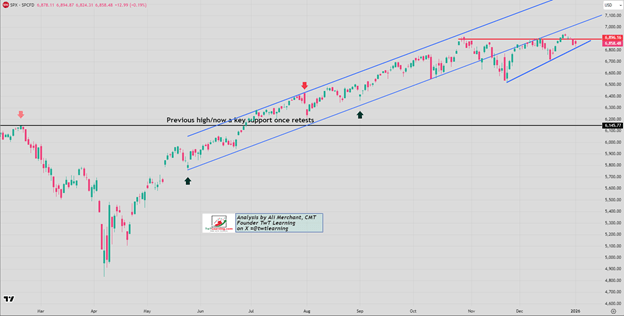

SPX Index

Last week, the SPX fell below the 6,896 resistance zone. As long as it remains under this level, a decline toward 6,820 seems probable. A strong and sustained break below 6,820 would suggest further downside potential toward the 6,740–6,720 range. Otherwise, the SPX is likely to trade sideways within the 6,890 to 6,820 range.

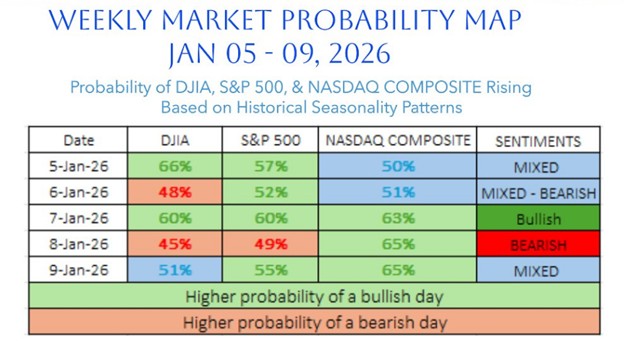

Weekly US Indices Probability Map

The U.S. weekly market probability map for January 5–9, 2026 indicates a week characterized by mixed trading patterns. These maps are based on historical seasonality trends, with sentiment readings generated using a seasonality-driven scoring system.