Markets absorbed last night’s FOMC decision without much surface reaction, but the takeaway was straightforward: the Fed is content to keep financial conditions accommodative. That stance weighed on the U.S. dollar and pushed yields lower, while gold and equities edged higher on solid earnings. In essence, the Fed did nothing to challenge the prevailing market narrative. Attention now shifts back to the charts, which are beginning to tell a compelling story.

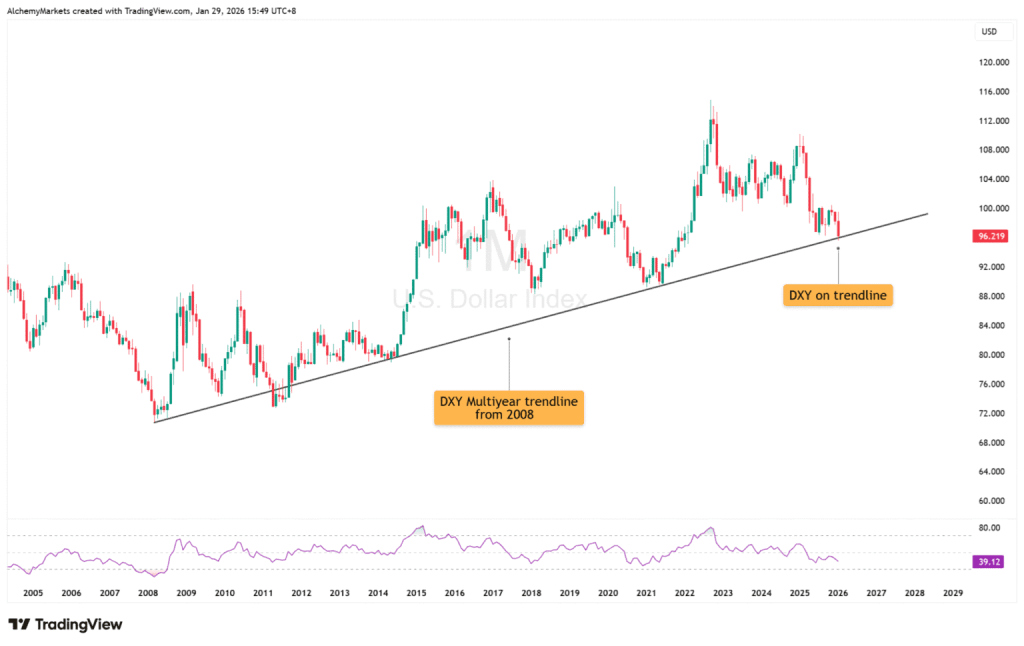

Is It Possible? DXY Slips Back to Its 2008 Trendline

The DXY has drifted back into a long-term monthly trendline zone that has previously served as a key structural floor. For now, this move represents a test rather than a confirmed breakdown.

What matters next:

A decisive weekly close below this support area would confirm a genuine structural breakdown. Conversely, if the DXY stabilizes and rebounds, it would be an early signal that the crowded “short USD” trade may be vulnerable to a squeeze.

This is precisely the kind of setup where long-term sentiment can be right, yet short-term positioning gets punished.

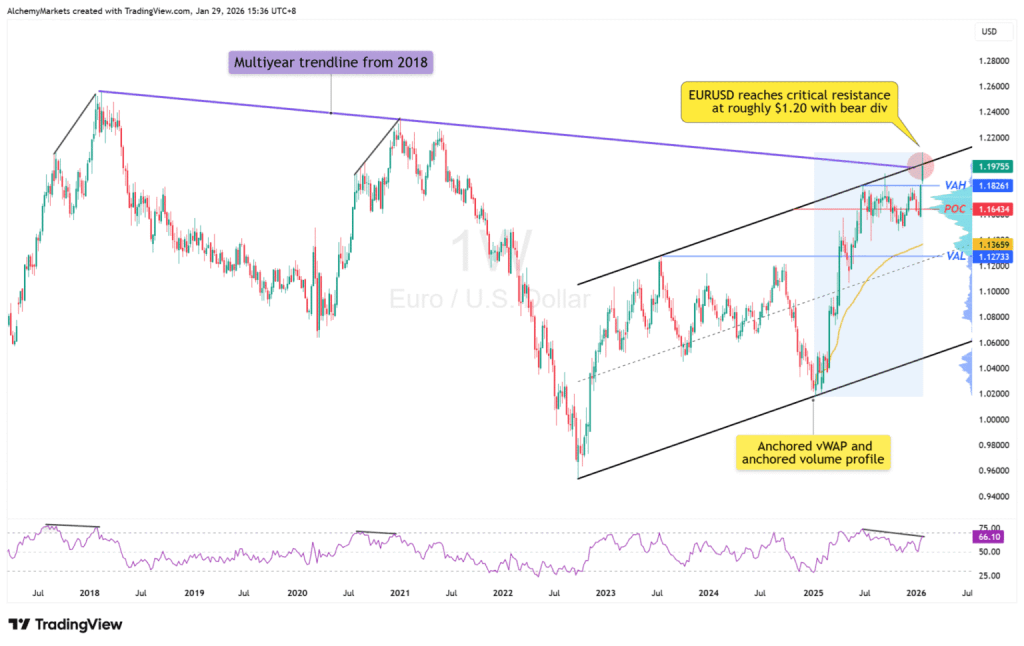

EUR/USD Points to a Near-Term Pause as the Dollar Regains Some Strength

EUR/USD is pushing into a dense resistance cluster, including the 1.20 psychological level, a multi-year trendline, channel alignment, and a bearish divergence on the weekly RSI.

That combination typically leads to at least a pause or pullback, even if the longer-term bias remains bullish for EUR/USD (and bearish for the dollar). If EUR/USD does roll over, it would offer the cleanest “risk-on USD bounce” setup without having to guess.

Key takeaway: A stall in EUR/USD here gives the DXY room to breathe.

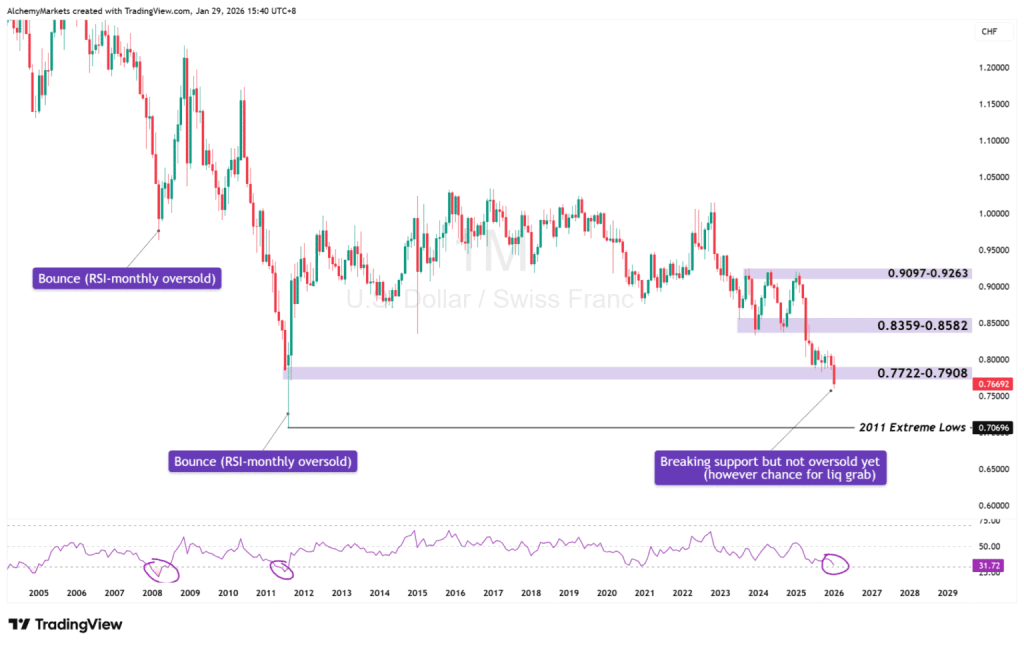

USD/CHF Is Also Trading at Extreme Levels

USD/CHF is one of the clearest expressions of U.S. dollar pessimism. When it reaches extreme levels, two patterns typically emerge: downside momentum begins to fade as the trade becomes crowded, and volatility increases as even minor catalysts trigger repositioning.

Even if dollar weakness persists, this is a zone where smooth continuation should no longer be assumed.

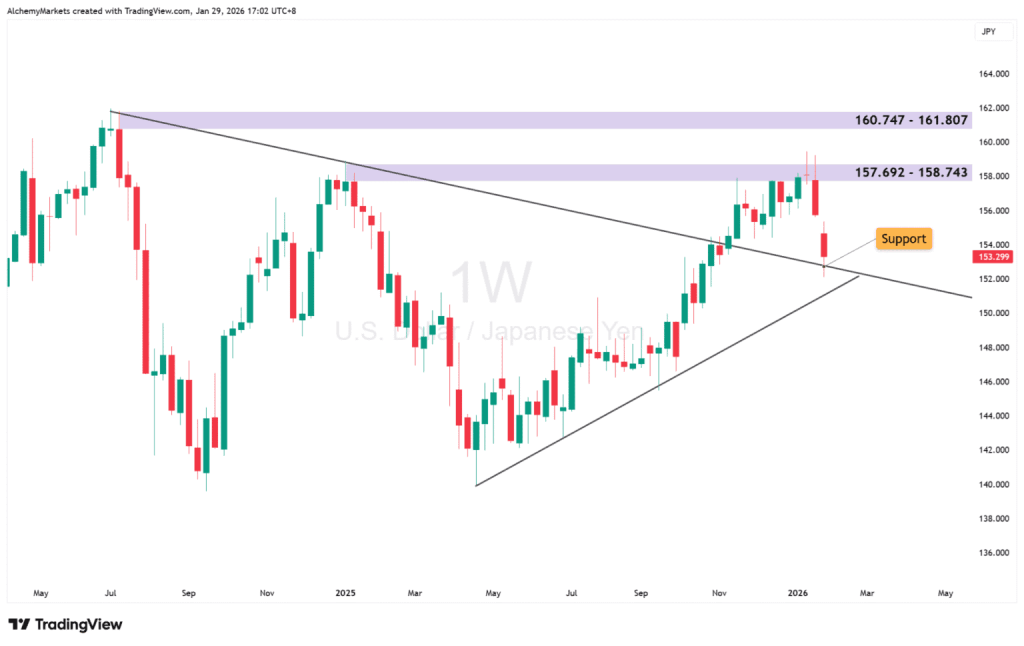

USD/JPY: A Key Pressure Zone for a Potential Dollar Reversal

USD/JPY is where macro theory collides with market reality. If a meaningful USD squeeze is going to materialize, this pair is almost certain to play a role.

On the weekly chart, USD/JPY is interacting with a major structural pivot, pulling back into a former resistance area that is now attempting to act as support around 151–153. For now, price has printed a wick at this support zone, suggesting USD/JPY may pause here before any further downside acceleration.

If this support holds, a rotation higher becomes increasingly plausible, with upside targets back toward the prior supply zones at 157.7–158.7, followed by 160.7–161.8.

That wouldn’t imply the start of a new USD bull market, but rather a crowded-trade unwind, especially with the current consensus loudly focused on a yen carry unwind and broad USD bearishness.

Bank of Japan Policy Decision

The next Bank of Japan policy meeting is scheduled for 18–19 March 2026, with market expectations largely aligned:

No rate hike is expected in March

Attention will center on guidance, messaging, and any indications of follow-through later in 2026

A continued bias toward verbal intervention and tactical signaling, rather than immediate or aggressive FX action

In short, the BOJ meeting is unlikely to be the catalyst itself. More often, it serves as the narrative justification after price has already picked a direction.

That’s why USD/JPY should be viewed as a leading indicator rather than a reactive trade. Focus on the key levels, and let positioning and price action do the talking.

The Japanese yen edged lower after softer-than-expected Tokyo CPI data dampened expectations for an imminent Bank of Japan rate hike.

Persistent fiscal challenges and political uncertainty continued to pressure the currency, although fears of official intervention helped limit losses.

Meanwhile, concerns over the Federal Reserve’s independence could restrain any rebound in the U.S. dollar and cap gains in the USD/JPY pair.

The Japanese yen (JPY) came under renewed selling pressure during Asian trading on Friday after data showed consumer inflation in Tokyo, Japan’s capital, slid sharply to a near four-year low in January. The weaker inflation reading reduces urgency for the Bank of Japan (BoJ) to move toward near-term rate hikes. In addition, concerns over Japan’s fiscal outlook, linked to Prime Minister Sanae Takaichi’s reflationary agenda, along with political uncertainty ahead of the February 8 snap election, continue to weigh on the currency. Coupled with modest U.S. dollar (USD) strength, these factors pushed USD/JPY toward the 154.00 level and the key 100-day Simple Moving Average (SMA) resistance.

That said, expectations of coordinated intervention by U.S. and Japanese authorities to support the yen may discourage aggressive bearish positioning. At the same time, lingering trade uncertainty stemming from President Donald Trump’s tariff threats and broader geopolitical risks is tempering risk appetite, as reflected in the cautious tone across equity markets, which could help limit downside in the safe-haven JPY. Meanwhile, the USD may struggle to gain sustained traction amid expectations of further Federal Reserve rate cuts and ongoing concerns over the central bank’s independence, potentially capping further upside in USD/JPY.

Japanese yen comes under pressure from soft Tokyo CPI, fiscal concerns and political uncertainty

A government report released earlier on Friday showed that Tokyo’s headline Consumer Price Index (CPI) fell to 1.5% in January from 2.0% previously, marking its lowest level since February 2022. Core inflation, which strips out fresh food prices, also softened to 2.0% from 2.3% in December, while a broader measure excluding both food and energy eased to 2.4% from 2.6% the month before.

The data signals easing demand-driven inflation pressures and diminishes the urgency for further monetary tightening by the Bank of Japan, following its December rate hike that lifted the policy rate to 0.75%, the highest level in three decades.

Meanwhile, concerns over Japan’s fiscal outlook persist as Prime Minister Sanae Takaichi has anchored her snap election campaign on expanded stimulus measures and pledged to suspend the consumption tax on food, raising questions about fiscal sustainability.

Adding another layer of complexity, reports of an unusual rate check by the New York Federal Reserve last Friday, following a similar move by Japan’s Ministry of Finance, have fueled speculation about potential coordinated U.S.-Japan intervention to curb yen weakness.

On the geopolitical front, U.S. President Donald Trump announced plans on Thursday to decertify all Canada-made aircraft and threatened to impose 50% tariffs unless U.S.-built Gulfstream jets receive certification in Canada. The move marks a fresh escalation in U.S.-Canada trade tensions.

These developments, alongside rising U.S.-Iran frictions and the prolonged Russia-Ukraine conflict, could help limit downside pressure on the safe-haven yen. The United States continues to deploy warships and fighter jets across the Middle East, while Secretary of War Pete Hegseth stated that Washington stands ready to act decisively under President Trump’s directives.

Russia has also reiterated its invitation for Ukrainian President Volodymyr Zelensky to travel to Moscow for peace talks, although prospects for a deal remain slim amid deep divisions between the two sides.

Meanwhile, the U.S. dollar received a modest boost amid speculation that Kevin Warsh may be appointed as the next Federal Reserve chair, lending additional support to the USD/JPY pair. President Trump is expected to announce his choice for Fed chair on Friday morning.

Looking ahead, traders will take further cues from the release of the U.S. Producer Price Index (PPI), which, alongside comments from Federal Reserve officials, is likely to influence dollar demand and provide direction for USD/JPY into the weekend.

USD/JPY bulls look for a sustained break above the 100-day SMA before adding new positions

The 100-day Simple Moving Average (SMA) continues to trend higher and is currently located near 153.98, with USD/JPY trading just below this level. This keeps near-term sentiment on the heavy side, despite the broader uptrend suggested by the rising trend filter. A sustained move back above this dynamic resistance would help steady the short-term outlook.

Momentum indicators show tentative signs of stabilization. The Moving Average Convergence Divergence (MACD) remains in negative territory, although its recent narrowing points to fading downside pressure. Meanwhile, the Relative Strength Index (RSI) stands at 37.81, below the neutral 50 mark but rebounding from oversold levels, indicating that bearish momentum is beginning to ease.

On the upside, the 38.2% Fibonacci retracement of the 159.13–152.07 decline, located at 154.77, is likely to act as initial resistance. A daily close above this level would enhance the recovery setup and open the door to further gains as momentum improves. Conversely, failure to break above this barrier would keep rebounds limited and reinforce a cautious near-term bias.

Federal Reserve Chair Jerome Powell offered few substantive remarks during his press conference on Wednesday, sidestepping multiple questions about the upcoming leadership transition as his term ends on May 15. He declined to comment on President Donald Trump’s potential nominee to succeed him, as well as on the president’s public criticism of his tenure.

Powell also avoided addressing questions related to the Department of Justice investigation involving him and the ongoing Supreme Court case concerning the possible removal of Fed Governor Lisa Cook. In response to these issues, he repeatedly indicated that he had nothing further to add.

“I have nothing on that for you.”

He repeated that response seven times in total. On four occasions, he simply said,

“I don’t have anything on that for you.”

After the FOMC voted to keep the federal funds rate in a range of 3.50%–3.75%, Powell provided no additional forward guidance beyond reiterating the Fed’s data-dependent, meeting-by-meeting approach. He did, however, acknowledge the underlying strength of the U.S. economy.

Powell noted that the unemployment rate has remained low at around 4.4% in recent months, even as job growth has slowed. He also said inflation is expected to ease as the effects of President Trump’s tariffs fade.

Overall, Powell characterized the risks of higher inflation and rising unemployment as balanced, signaling little urgency for policy action. This assessment increases the likelihood that the federal funds rate will remain unchanged at his final two meetings as FOMC chair.

Officials in the Trump administration broadly share our “Roaring 2020s” outlook, which assumes stronger-than-expected productivity growth will lift real GDP while easing inflation pressures as unit labor cost growth falls toward zero. They argue that this expectation supports additional cuts to the federal funds rate—a view echoed by two dissenting members of the FOMC, who expressed similar reasoning at the latest meeting.

We take a different view. Cutting the federal funds rate further from current levels would heighten the risk of financial instability, particularly by fueling a melt-up in equity markets. A similar dynamic is already evident in precious metals. Additional rate cuts would also put further downward pressure on the dollar, potentially reigniting inflationary pressures.

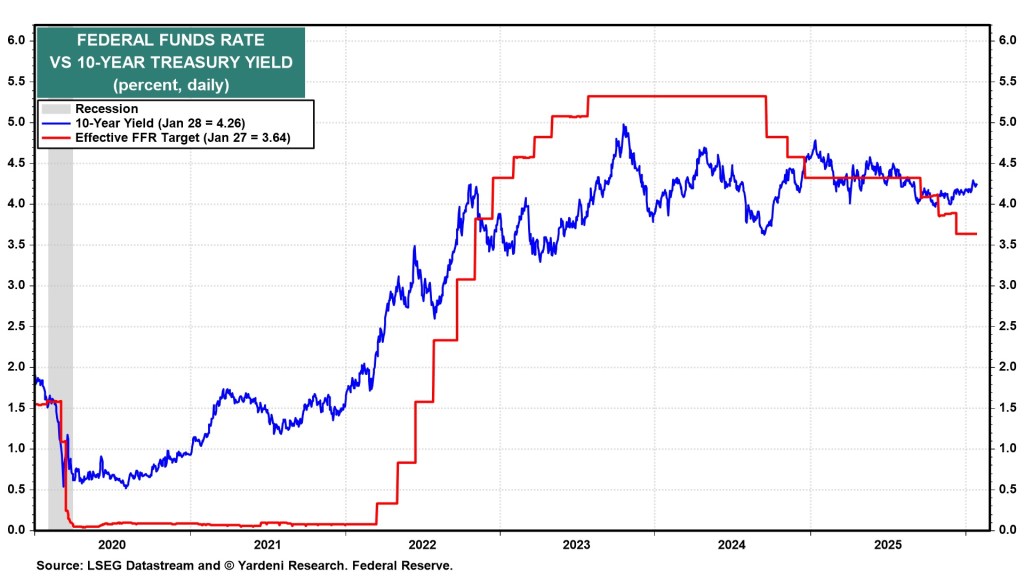

Bond markets appear to share this skepticism. When the Fed reduced the federal funds rate by 100 basis points in late 2024, the 10-year Treasury yield rose by a similar amount. Even after another 75-basis-point cut late last year, the yield held around 4.00% and has since climbed to 4.26%. We continue to expect the 10-year yield to trade largely between 4.25% and 4.75% this year—levels that were typical in the period before the Global Financial Crisis.

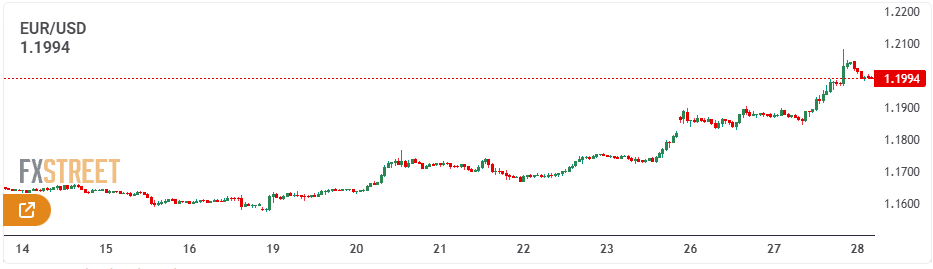

The U.S. dollar showed a limited reaction to the latest Federal Reserve meeting, with EUR/USD pushing toward the 1.20000 level. While the Fed’s messaging pointed to a low likelihood of a key rate cut in March—given that economic growth is now characterized as “solid”—market attention during the press conference shifted toward political issues.

This focus, according to Commerzbank analysts Volkmar Baur and Michael Pfister, suggests a growing change in how investors perceive the Federal Reserve’s independence.

Fed meeting weighs on US dollar

Overall, the market appeared to place greater emphasis on the Fed’s slightly hawkish tone and policy tweaks. Expectations for additional rate cuts were trimmed marginally, but the adjustment was too small to have a meaningful impact on the currency.

“The perception that political considerations are gradually influencing the Fed—or at least that markets believe this to be the case—was also reflected in Christopher Waller’s vote in favor of another cut to the key policy rate.

Ultimately, even if the Fed remains capable of conducting an independent monetary policy, this perception alone could become problematic. If markets lose confidence in that independence, the U.S. dollar is likely to come under pressure.”

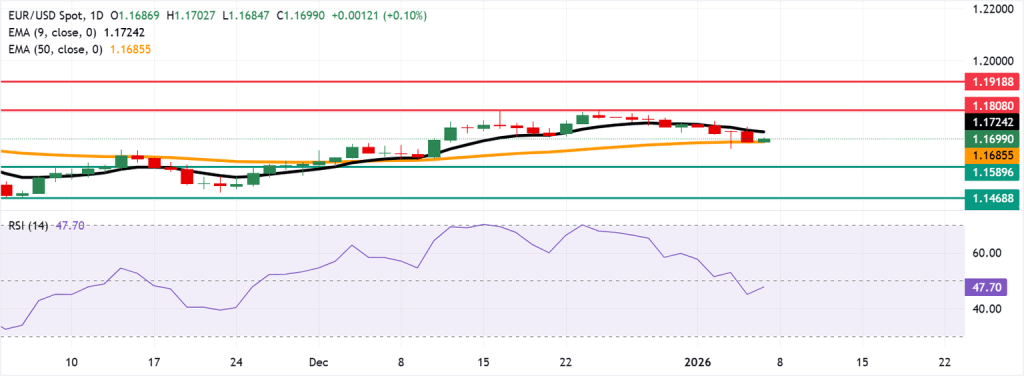

EUR/USD extended Monday’s positive momentum, pushing closer to the key 1.2000 level and reaching highs not seen since June 2021. The latest advance reflects continued selling pressure on the U.S. dollar, supported by a constructive risk backdrop and renewed investor focus on potential tariff-related risks stemming from the White House.

Macro & Fundamental Overview

EUR/USD’s bullish momentum remains firmly intact, closely mirroring persistent selling pressure on the U.S. dollar, which continues to be weighed down by concerns over trade policy, questions surrounding the Federal Reserve’s independence, and renewed shutdown risks.

The pair extended its advance for a fourth straight session on Tuesday, edging closer to the pivotal 1.2000 level for the first time since June 2021.

The latest leg higher reflects a further deterioration in the dollar’s outlook amid revived trade tensions and geopolitical uncertainty, all ahead of the Federal Reserve’s interest rate decision due on Wednesday.

Meanwhile, sentiment surrounding U.S.–European Union trade relations has improved after President Donald Trump softened his rhetoric last week regarding potential tariffs tied to the Greenland dispute. Markets have interpreted this shift positively, boosting risk appetite and lending support to the euro alongside other risk-sensitive currencies.

By contrast, the U.S. dollar continues to underperform. The Dollar Index (DXY) remains under heavy pressure, extending its decline toward the 96.00 area — levels last seen in late February 2022.

The FED: Rates on hold, politics in focus

The Federal Reserve delivered its widely anticipated December rate cut, but the key signal came from its messaging rather than the policy action itself. A divided vote and Chair Jerome Powell’s measured language suggested that additional easing is far from assured.

The Fed begins its two-day policy meeting today, with markets largely expecting rates to remain unchanged when the decision is released on Wednesday.

However, monetary policy may not be the primary focus this time. Market attention has increasingly turned to questions surrounding the Fed’s independence after reports earlier this month of a Justice Department investigation involving Chair Powell.

Compounding the uncertainty, President Trump has indicated that an announcement on his nominee for the next Fed Chair could be imminent, keeping scrutiny on the central bank well beyond the outcome of this week’s meeting.

ECB urges patience, not complacency

The European Central Bank left interest rates unchanged at its December 18 meeting, adopting a more measured and patient tone that has pushed expectations for near-term rate cuts further into the future. Modest upward revisions to growth and inflation projections helped underpin this approach.

Minutes from the meeting, released last week, showed policymakers saw little immediate need to adjust policy. With inflation hovering near target, the ECB has room to remain patient, while still retaining flexibility should risks materialize.

Governing Council members emphasized that patience does not equate to complacency. Monetary policy is viewed as appropriately calibrated for now, but not on autopilot. Markets appear to have absorbed this message, currently pricing in just over 4 basis points of easing over the coming year.

Positioning remains constructive, but confidence has softened

Speculative positioning remains tilted toward the euro, although bullish conviction appears to be easing.

CFTC data for the week ended January 20 show non-commercial net long positions declining to a seven-week low of around 111.7K contracts. At the same time, institutional participants also reduced short positions, which now stand near 155.6K contracts.

Meanwhile, open interest slipped to approximately 881K contracts, breaking a three-week streak of increases and suggesting that market participation may be thinning alongside fading confidence.

Key Events Ahead

Near term: The FOMC meeting is set to keep attention firmly on the U.S. dollar, while flash inflation data from Germany and preliminary GDP readings for the euro area will dominate the regional data calendar later in the week.

Risk: A more hawkish-than-expected outcome from the Fed could quickly tilt momentum back in favor of the dollar. In addition, a clear break below the 200-day simple moving average would increase the risk of a deeper medium-term correction.

EUR/USD Technical Outlook

EUR/USD continues to exhibit a firm bullish bias, trading at levels last seen in mid-2021 while gradually shifting focus toward the key 1.2000 psychological handle.

On the downside, initial support is located at the 2026 low of 1.1576 (January 19), reinforced by the closely watched 200-day simple moving average. A more pronounced correction could open the door to the November 2025 trough at 1.1468, followed by the August base at 1.1391.

Momentum indicators remain broadly supportive of further gains, although elevated conditions may challenge the immediate upside. The Relative Strength Index is hovering near 75, pointing to overbought territory, while an Average Directional Index reading above 26 confirms the presence of a well-established trend.

Bottom Line

For the time being, EUR/USD continues to be influenced primarily by U.S.-centric developments rather than euro area dynamics.

Absent clearer signals from the Federal Reserve on the extent of potential policy easing, or a more compelling cyclical recovery in the eurozone, any additional upside is likely to unfold in a steady, incremental manner rather than marking the beginning of a decisive breakout.

The Japanese yen finds it hard to build on recent strong gains as worries over Japan’s fiscal position persist. However, a relatively hawkish Bank of Japan stance and concerns about potential currency intervention could continue to support the yen. Meanwhile, the US dollar remains near a four-month low on expectations of Fed rate cuts, helping to limit upside in USD/JPY.

The Japanese yen comes under modest selling pressure during Tuesday’s Asian session, pulling back further from its strongest level against the US dollar since November 2025, reached a day earlier. Sentiment toward the yen remains fragile as investors worry about Japan’s fiscal outlook, driven by Prime Minister Sanae Takaichi’s expansive spending proposals and tax cut plans. A broadly upbeat mood in equity markets, along with domestic political uncertainty ahead of the snap election scheduled for February 8, is also weighing on the safe-haven currency.

However, downside pressure on the yen may be limited by expectations that Japanese authorities could intervene to prevent excessive weakness, especially given the Bank of Japan’s relatively hawkish stance. Meanwhile, the US dollar stays near a four-month low as markets price in two additional Federal Reserve rate cuts this year. The ongoing “Sell America” theme further dampens demand for the greenback, which should help restrain USD/JPY movements as investors turn their attention to the key two-day FOMC meeting beginning later today.

Japanese yen bears remain cautious as intervention speculation offsets political uncertainty.

Japan’s already stretched public finances have come under sharper scrutiny following Prime Minister Sanae Takaichi’s campaign pledge to suspend the sales tax on food items ahead of the snap lower house election on February 8. Concerns over the country’s fiscal outlook have been a major driver behind the recent jump in long-dated Japanese government bond yields, which raises debt servicing costs and, in turn, limits the Japanese yen’s upside.

Data released earlier on Tuesday showed a slowdown in wholesale inflation, with the Producer Price Index rising 2.4% year-on-year in December, down from 2.7% in November. Additional figures indicated that the Corporate Service Price Index increased 2.6% YoY, slightly lower than the previous reading. Overall, the data offered little to challenge the Bank of Japan’s tightening trajectory and had a limited impact on the yen.

The BoJ recently raised its economic and inflation forecasts while keeping short-term rates unchanged at the conclusion of its two-day meeting last Friday, signaling its readiness to continue gradually lifting still-low borrowing costs. This stance contrasts sharply with expectations for a more dovish US Federal Reserve, leaving the US dollar under pressure near a four-month low and lending support to the yen amid fears of possible official intervention.

Reinforcing this view, Prime Minister Takaichi said on Sunday that authorities are prepared to take action against speculative and highly abnormal market moves, following rate checks by Japan’s Ministry of Finance and the New York Fed on Friday. Still, traders appear reluctant to take aggressive positions ahead of the two-day FOMC meeting beginning today, which is expected to be a key driver for the US dollar and the USD/JPY pair in the near term.

USD/JPY needs to establish a sustained break below the 100-day SMA to strengthen the case for further downside.

The USD/JPY pair showed signs of resilience below its 100-day Simple Moving Average (SMA) on Monday, although it continues to trade beneath the 154.75–154.80 horizontal support zone. The MACD histogram has moved further into negative territory, with the MACD line below the signal line, reflecting bearish momentum that remains below zero. Meanwhile, the RSI stands near 32, close to oversold territory, suggesting that the downside move may be becoming stretched.

A daily close below the 100-day SMA at 153.81, which currently provides near-term support, would give bears greater control. In contrast, sustained trading above this level would keep the broader bias supported by the rising SMA. Signs of stabilization would include a flattening MACD histogram and a move back toward the zero line, while an RSI rebound toward 50 would improve the overall tone. On the other hand, a dip below 30 on the RSI would increase the risk of deeper losses.

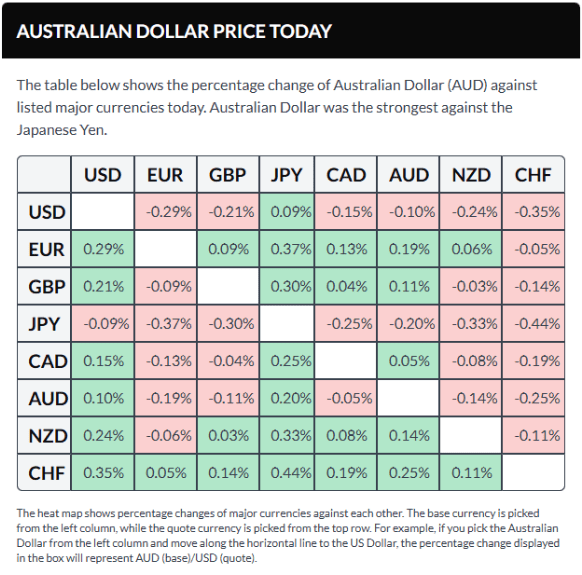

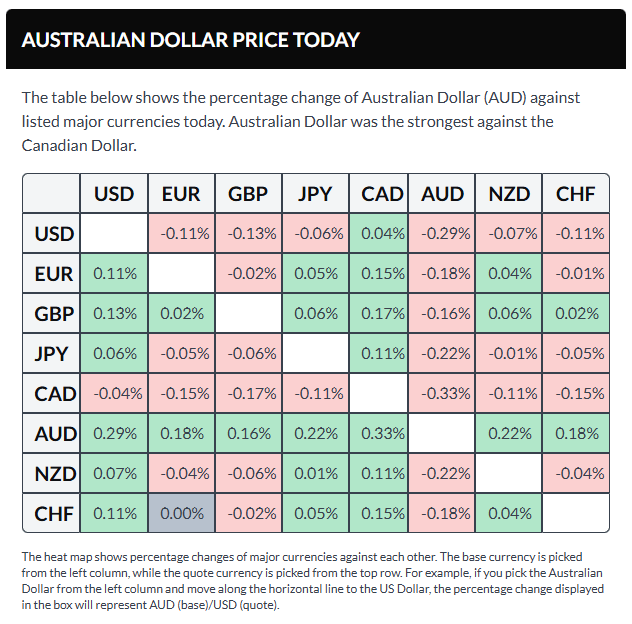

AUD/USD hovers near its 16-month high of 0.6940, supported by rising Australian three-year bond yields at 4.27%, while a weaker US Dollar amid political uncertainty and shutdown risks adds to the upside.

AUD/USD is holding near its 16-month high of 0.6940 set in the prior session, trading around 0.6920 during Tuesday’s Asian hours, as markets await Australia’s December CPI data on Wednesday for fresh cues on the RBA’s policy outlook.

The Australian Dollar is underpinned by higher government bond yields, with the policy-sensitive three-year yield climbing to 4.27%, its highest since November 2023, supported by confidence in Australia’s strong credit rating and the RBA’s relatively hawkish stance.

Australia’s strong PMI and employment data have strengthened expectations of tighter RBA policy. While inflation has eased from its 2022 peak, recent figures point to renewed upward pressure, with headline CPI slowing to 3.4% YoY in November but still above the RBA’s 2–3% target range.

AUD/USD may find further support as the US Dollar weakens on rising political uncertainty, with the risk of a partial US government shutdown ahead of the January 30 funding deadline after Senate Democratic leader Chuck Schumer vowed to oppose a key funding bill.

Market caution is also heightened by uncertainty around the Federal Reserve, after President Donald Trump said he would soon name a successor to Fed Chair Jerome Powell, raising speculation over a more dovish policy stance. Attention now turns to Wednesday’s Fed decision.

The US Dollar Index stays under pressure near 97.00 in Tuesday’s Asian session as concerns over Fed independence grow ahead of expectations that rates will remain unchanged at Wednesday’s meeting.

The US Dollar Index (DXY) weakened toward 97.00 in Asian trading on Tuesday, with investors awaiting the US ADP Employment Change and Consumer Confidence data later in the day.

Concerns over the Federal Reserve’s independence have pushed the DXY to its lowest level since September 18, 2025, after President Donald Trump said he would soon name a successor to Fed Chair Jerome when his term ends in May. According to Reuters, betting markets see BlackRock executive Rick Rieder as the leading candidate.

Tim Duy, chief US economist at SGH Macro Advisors, noted that the actions of the next Fed chair cannot be separated from broader economic conditions or their influence on other FOMC members.

Adding to the USD’s downside risks are fears of a US government shutdown, with Senate Democratic leader Chuck Schumer pledging to block a funding bill that includes Homeland Security appropriations. Lawmakers face a January 30 deadline to avoid a partial shutdown.

Meanwhile, the Fed is widely expected to keep rates unchanged at Wednesday’s meeting after three straight cuts late in 2025. Markets will focus on the press conference for signals on the economic outlook and future rate path, with any hawkish tone potentially limiting near-term USD losses.

Wednesday brings the FOMC meeting and Chair Powell’s press conference, and it wouldn’t be surprising if President Trump chose that moment—ideally around 2:30 p.m. ET—to announce his pick for the next Fed chair. Such timing would dominate headlines, catch financial media off guard, and inject maximum uncertainty into markets.

That said, the Fed is not expected to cut rates at this meeting, which should keep the event relatively uneventful. In the bigger picture, what the Fed does between now and May may prove less important, particularly if a new chair is appointed and moves quickly toward easing.

Markets appear to be dialing back expectations for aggressive rate cuts. Current pricing suggests the fed funds rate settles near 3.25% by December, with little additional easing beyond that. To meaningfully shift those expectations, the nominee would likely need to be notably dovish—something markets already anticipate, given the widespread assumption that Trump will select a policy-leaning accommodator.

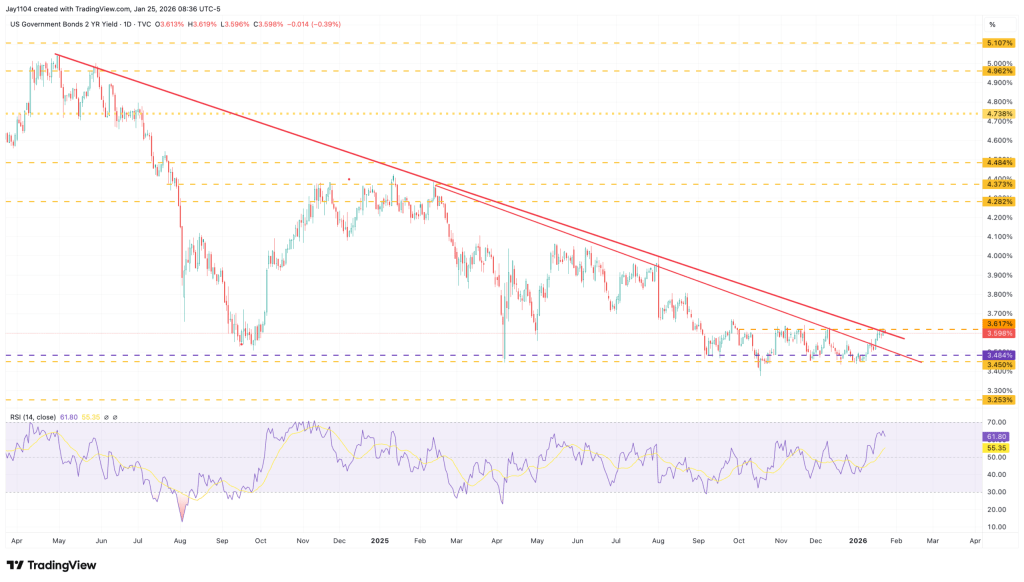

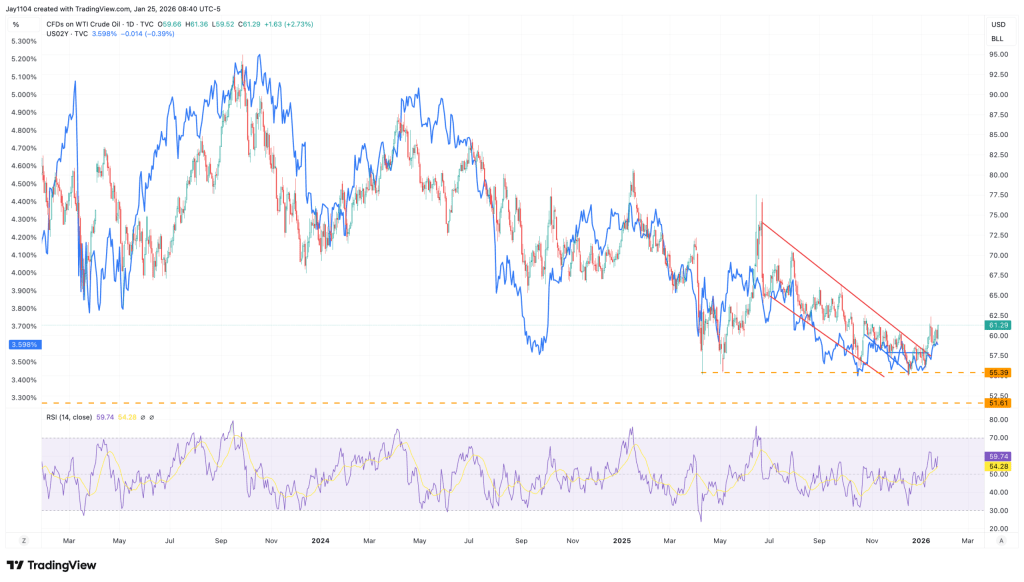

As a result, the risk of a breakout in the 2-year Treasury yield appears increasingly credible, with initial resistance near 3.62%. Beyond that, a move back toward the 4% level cannot be ruled out. From a technical perspective, the setup supports this view: the 2-year yield has formed multiple bottoms in recent months, and the RSI has begun to turn higher, signaling building upside momentum.

The direction of the 2-year yield may ultimately be more closely linked to oil prices. With inflation still hovering near 3% and crude having fallen to around $60 from highs in the $120s, the message is clear: a rebound in oil prices could quickly reignite inflation pressures. That dynamic likely explains why the price action in oil and the 2-year yield charts has begun to look strikingly similar.

The Bank of Japan once again chose to kick the can down the road, leaving rates unchanged and, in my view, offering little in the way of a clear policy roadmap. The yen’s strength on Friday appeared to be driven solely by reports of a possible “rate check” by the New York Fed on behalf of the U.S. Treasury—widely interpreted as a warning signal that currency intervention could be imminent. Perhaps the strategy is to keep markets stable until after the snap election in February. It’s hard to say, but it should be telling to see how markets react once Japan reopens on Monday.

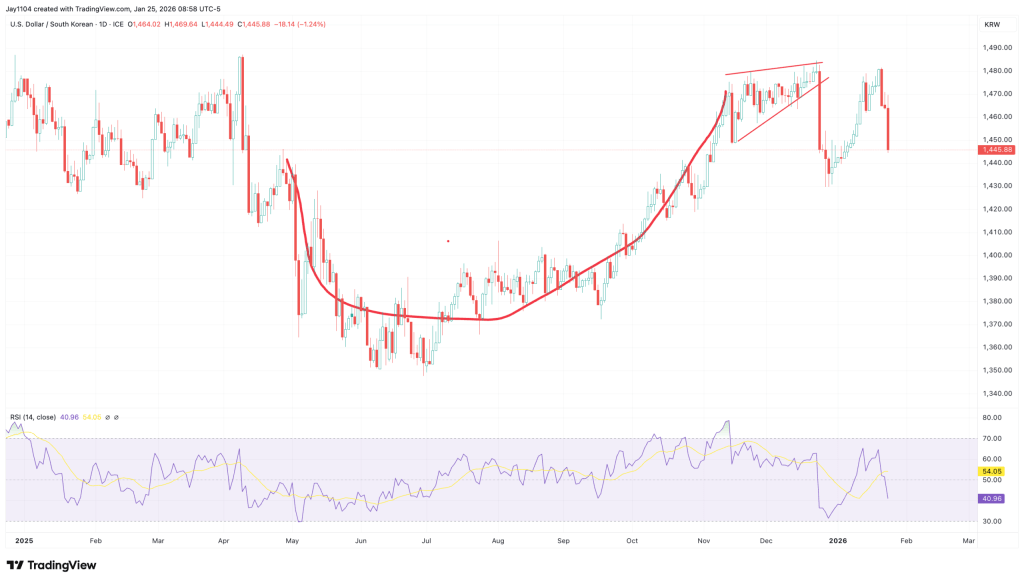

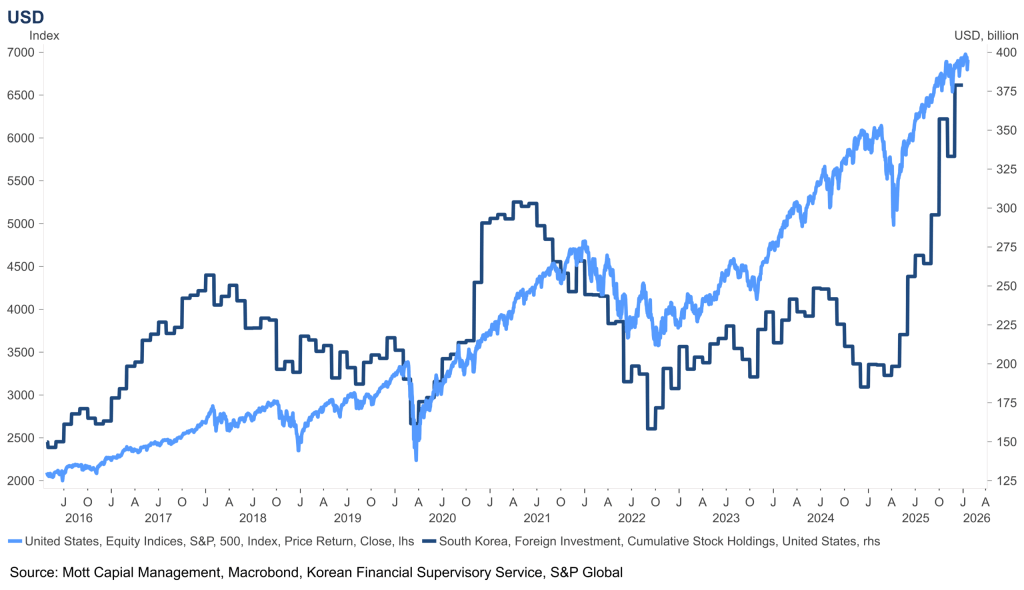

The Korean won also strengthened notably against the U.S. dollar on Friday. In recent weeks, there has been growing chatter that the KRW had become excessively weak, so it’s likely the currency took the developments around the yen as a warning signal and moved to reprice accordingly.

The Korean won likely matters more than many investors realize, given the sizable exposure South Korean investors have built up in U.S. equities. That dynamic is probably one of the reasons the KRW has weakened so significantly in the first place—buying U.S. stocks requires selling won for dollars.

If the KRW begins to strengthen from here, it could start to put pressure on that trade. For investors who are unhedged on the currency side, a stronger won increases the risk of FX-related losses on their U.S. equity holdings, potentially prompting position adjustments.

Of course, this week also brings major earnings reports from Microsoft, Apple, Tesla, and Meta. From what I can see, all four stocks are currently sitting in positive gamma with positive delta positioning. Implied volatility typically builds into earnings because of the event risk, which sets up a familiar dynamic: unless a company delivers truly blowout results, the reaction can easily turn into a sell-the-news move. Once earnings are released, implied volatility collapses and hedges are unwound as delta decays, potentially putting pressure on the shares.

Germany’s IFO Institute is set to release its January Business Survey on Monday at 09:00 GMT.

The headline IFO Business Climate Index is forecast to edge up to 88.1 in January, from 87.6 in December. In the previous release, the Current Assessment Index stood at 85.6, while the Expectations Index came in at 89.7.

How might the German IFO Survey influence the EUR/USD exchange rate?

EUR/USD could trade sideways if the German IFO Business Survey meets expectations, as heightened safe-haven demand continues to cap upside momentum despite the pair opening with a gap higher. Meanwhile, the Euro may hold relatively steady after Eurozone PMI figures signaled weakness in the services sector in January, reinforcing expectations that the European Central Bank (ECB) will keep interest rates unchanged. Earlier data from Germany was more constructive, with the Services PMI exceeding forecasts and remaining in expansionary territory, while the Manufacturing PMI showed improvement but stayed below the 50 threshold.

The pair comes under pressure as the US Dollar regains intraday strength, supported by rising risk aversion linked to trade and geopolitical concerns. US President Donald Trump warned of potential 100% tariffs on Canadian imports should Ottawa pursue a trade agreement with China. Canadian Prime Minister Mark Carney clarified that Canada has no intention of negotiating a free trade deal with Beijing. Trump also noted that a US aircraft carrier strike group is en route to the Middle East amid escalating tensions with Iran.

From a technical perspective, EUR/USD pulls back after opening at four-month highs and is trading near 1.1860 at the time of writing. Despite the dip, the broader bullish structure remains intact, with the 14-day Relative Strength Index (RSI) hovering around 69.00, indicating strong—though stretched—momentum. The pair could attempt a retest of the four-month peak at 1.1897, close to the key psychological resistance at 1.1900. On the downside, immediate support is seen at the nine-day Exponential Moving Average (EMA) near 1.1739.

GBP/USD is extending its strong weekly rally and is edging closer to the 1.3600 handle on Friday, marking fresh four-month highs. The pair’s upside momentum is being fueled by a deepening decline in the US Dollar, while supportive UK economic data further reinforces the bullish trend.

Fundamental Analysis Overview

The latest PMI data signaled a strong expansion in overall business activity, driven by a notable pickup in both manufacturing and services. The Composite PMI surged to 53.9 in January from 51.4 in December, comfortably surpassing market expectations of 51.7.

The Services PMI climbed to 54.3, exceeding both the forecast of 51.7 and the previous reading of 51.4, while the Manufacturing PMI also improved markedly, rising to 51.6 from 50.6.

In addition, UK Retail Sales rebounded in December after two consecutive monthly declines. Data from the Office for National Statistics (ONS) showed that Retail Sales, a key gauge of consumer spending, increased by 0.4% month-over-month, defying expectations for a 0.1% contraction.

On a year-on-year basis, consumer spending rose sharply by 2.5%, well above the consensus forecast of 1% and up from a revised 1.8% in November (previously reported at 0.6%).

The stronger-than-expected Retail Sales figures are likely to reduce market expectations for near-term interest rate cuts by the Bank of England (BoE).

Looking ahead, the UK economic calendar is relatively light next week, leaving broader market sentiment and expectations surrounding the BoE’s February policy decision as the primary drivers of Pound Sterling performance.

GBP/USD Technical Outlook

GBP/USD is trading around 1.3437 at the time of writing. The 20-day Exponential Moving Average is hovering near 1.3439, with price currently testing this dynamic resistance. A daily close above the moving average would strengthen near-term momentum. The Relative Strength Index (RSI) stands at 52, edging higher but still signaling broadly neutral momentum.

Using the move from the 1.3780 peak to the 1.3006 trough, the 50% Fibonacci retracement at 1.3393 continues to act as a hurdle on rebounds, while the 61.8% retracement at 1.3485 limits upside potential. A decisive break above the latter would suggest the broader bearish bias is losing strength and could pave the way for a deeper recovery, whereas rejection at that level would likely keep the pair confined to a range.

Bank of Japan (BoJ) Governor Kazuo Ueda is speaking at a press conference, outlining the rationale for keeping the benchmark interest rate unchanged at 0.75% at the January policy meeting.

Key takeaways from the BoJ press conference

Japan’s economy is showing a moderate recovery and is expected to continue growing at a steady pace.

The government’s economic stimulus package has improved the overall outlook.

Underlying inflation is projected to rise gradually and move closer to the 2% target.

Board members Takata and Tamura suggested revisions to the outlook report.

The BoJ will continue to raise interest rates if economic and price projections are realized.

Lending rates tied to the BoJ’s policy rate are already trending higher.

Financial conditions remain accommodative despite the December rate hike.

Foreign exchange movements are influenced by multiple factors.

The governor refrained from commenting on specific yen levels but emphasized close monitoring of FX developments.

Government bond yields are increasing at a rapid pace.

The BoJ stands ready to conduct bond-buying operations flexibly in exceptional circumstances.

Measures may be taken to support stable yield formation when necessary.

Currency movements, particularly the yen, may be having a stronger impact on prices.

Greater attention will be paid to foreign exchange trends going forward.

The rise in long-term yields is partly influenced by end-of-fiscal-year factors.

Price developments in April will be an important consideration when assessing the timing of future rate hikes.

The section below was published at 3:35 GMT on January 23 to cover the Bank of Japan’s monetary policy announcement and the initial market reaction.

The Bank of Japan (BoJ) board voted to keep the short-term policy rate unchanged at 0.75% at the conclusion of its two-day monetary policy meeting on Friday, a move that was widely expected.

As a result, borrowing costs remain at their highest level in roughly three decades.

Key takeaways from the BoJ’s policy statement

Japan’s economy is expected to continue a moderate recovery.

Consumer inflation is likely to pick up gradually.

The virtuous cycle in which wage growth and inflation reinforce each other is expected to be sustained.

The output gap is projected to improve over time and expand at a moderate pace.

Medium- to long-term inflation expectations are seen rising gradually.

No major imbalances are observed in Japan’s financial activity.

The overall financial system remains stable.

Firms’ moves to pass higher wages on to selling prices could strengthen more than previously anticipated.

The recent increase in food prices, including rice, mainly reflects temporary supply-side factors.

Significant uncertainty surrounds the global economic outlook, particularly due to trade policies that could push up import prices through supply-side channels.

Trade measures announced so far may weigh on global economic growth.

Regarding the US economy, close attention is needed on how tariffs could affect employment and income via weaker corporate profits.

High uncertainty persists around China’s economic outlook, especially the future pace of growth.

A sharp rise in import prices could further reinforce households’ cautious stance on spending.

Current trade policies could lead to a shift in the long-term trend of globalisation.

The Board raised its median real GDP growth forecast for fiscal 2025 to +0.9% from +0.7% in October.

The fiscal 2026 median growth forecast was revised up to +1.0% from +0.7%.

The fiscal 2027 median growth forecast was lowered to +0.8% from +1.0%.

BoJ’s Quarterly Outlook Report: Key Highlights

The Board kept its median core consumer price index forecast for fiscal 2025 unchanged at +2.7%, the same as in October.

The median real GDP growth forecast for fiscal 2025 was revised up to +0.9% from +0.7% in October.

Real interest rates remain at significantly low levels.

Risks to the economic outlook are assessed as roughly balanced.

The impact of foreign exchange volatility on prices has become more pronounced than in the past, as firms are more willing to raise prices and wages.

Core consumer inflation is expected to slow to below 2% during the first half of this year.

Companies’ efforts to pass higher wages on to selling prices could strengthen more than anticipated.

Japan’s economy is projected to continue a moderate recovery.

Market reaction following the BoJ policy announcements

USD/JPY climbed further toward 158.60 in an immediate reaction to the Bank of Japan’s (BoJ) decision to keep interest rates unchanged, rising 0.11% on the day.

The section below was published at 23:00 GMT on January 22 as a preview of the Bank of Japan’s interest rate decision.

The Bank of Japan is widely expected to leave interest rates unchanged at 0.75% on Friday.

The central bank is likely to wait and assess the effects of December’s rate hike before considering further tightening.

February’s general elections introduce an additional layer of uncertainty to the BoJ’s monetary policy outlook.

The Bank of Japan (BoJ) is widely expected to keep its benchmark interest rate unchanged at 0.75% following the conclusion of its two-day monetary policy meeting next Friday.

The Japanese central bank raised interest rates to their highest level in three decades in December and is now likely to keep policy unchanged on Friday to better evaluate the economic impact of earlier hikes.

BoJ Governor Kazuo Ueda is expected to reaffirm the bank’s commitment to continued policy normalisation. As a result, investors will closely scrutinise his press conference for clues on the timing and extent of the next phase of the tightening cycle.

What to anticipate from the Bank of Japan’s interest rate decision?

The Bank of Japan is broadly expected to leave interest rates unchanged in January while signaling the possibility of further tightening if economic conditions unfold as projected.

In December, the BoJ raised rates by 25 basis points to 0.75%, and the meeting minutes showed that some policymakers favor additional tightening, noting that real interest rates remain sharply negative once inflation is taken into account.

Markets, however, have ruled out consecutive rate hikes, especially following Prime Minister Sanae Takaichi’s surprise call for snap elections and her proposal to suspend food and beverage taxes for two years to ease the burden on households amid rising inflation.

While the implications of these political developments for monetary policy remain uncertain, the BoJ has emphasized a cautious, gradual normalization of policy, aiming to withdraw stimulus without undermining economic growth. As a result, the central bank is likely to wait for greater political clarity and for the effects of past rate increases to become clearer before moving again.

Meanwhile, the yen has weakened steadily amid speculation surrounding the snap election. This raises the question of whether the currency’s depreciation will push the BoJ to adopt a firmer stance on monetary tightening.

How might the Bank of Japan’s monetary policy decision influence the USD/JPY exchange rate?

Markets have fully priced in a Bank of Japan rate pause on Friday, but the central bank will need to clearly signal further monetary tightening to curb the Yen’s ongoing weakness.

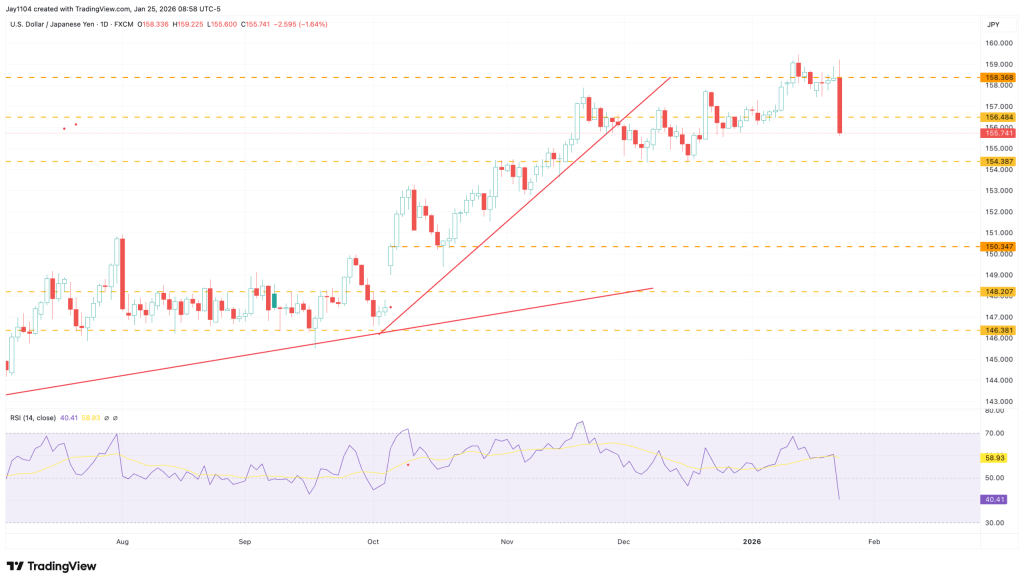

Yen sellers have eased off in recent days, helped by broad US Dollar softness linked to the EU–US trade dispute following President Donald Trump’s threats over Greenland. Even so, USD/JPY is still up roughly 0.7% year to date and remains close to last week’s 18-month peak around 159.50.

Investors are also concerned that Prime Minister Takaichi could secure stronger parliamentary backing after the elections, allowing her to push ahead with expansionary fiscal policies such as higher spending and tax cuts. This has heightened worries about Japan’s already stretched public finances, driving the Yen lower and pushing long-term government bond yields to record highs amid fears of a potential fiscal crisis.

Meanwhile, recent remarks from BoJ Governor Ueda have reinforced the bank’s cautious tightening stance, suggesting Japan is transitioning toward a more sustainable inflation environment where wages and prices rise together. For the Yen’s recent, still-fragile rebound to continue, markets will need clearer evidence that interest rate hikes are on the horizon.

USD/JPY 4-Hour Chart

From a technical standpoint, FXStreet analyst Guillermo Alcalá views USD/JPY as undergoing a bearish correction, with an important support zone just above 157.40. He notes that while the pair has pulled back from recent highs, Yen buyers would need to push it below the 157.40–157.60 support area to invalidate the short-term bullish structure and open the door to a move toward the early-January lows near 156.20.

A cautious or non-committal message from the BoJ would likely disappoint markets and weaken the Yen. In that scenario, Alcalá expects USD/JPY to climb to new long-term highs. He points out that technical signals are improving, with the 4-hour RSI rebounding from the 50 level, indicating strengthening bullish momentum. At the time of writing, the pair is challenging resistance around 158.70 (the January 16 high), which stands as the final hurdle before the 18-month peak close to 159.50.

UK retail sales increased by 0.4% month-on-month in December, rebounding from a 0.1% decline in November, according to data released Friday by the Office for National Statistics.

Markets had expected retail sales to fall by 0.1% during the month. Core retail sales, which exclude auto fuel, rose 0.3% month-on-month in December, reversing a revised 0.4% decline previously reported. The reading exceeded market expectations for a 0.2% fall.

On an annual basis, UK retail sales increased 2.5% in December, up from a revised 1.8% previously and above the consensus forecast of 1.0%. Annual core retail sales also strengthened, climbing 3.1% compared with a revised 2.6% gain earlier, outperforming expectations of a 1.4% rise.

Market response to the UK Retail Sales data

The positive UK Retail Sales report has failed to lift the Pound Sterling, with GBP/USD down 0.06% on the day, trading at 1.3488 at the time of writing.

The following section was published on January 23 at 5:11 GMT as a preview of the UK Retail Sales report.

Overview of UK Retail Sales

The UK calendar features the release of the December Retail Sales figures from the Office for National Statistics (ONS) on Friday at 07:00 GMT.

Retail Sales are forecast to edge down by 0.1% month-on-month in December, following an identical 0.1% decline in November. On a yearly basis, sales are expected to increase by 1%, slightly higher than the previous 0.6% rise.

Core Retail Sales, which exclude motor fuel, are also projected to slip by 0.2% MoM, in line with the prior reading, while annual growth is anticipated to improve to 1.4% from 1.2% in November.

How might UK retail sales influence the GBP/USD exchange rate?

The GBP/USD pair could show little reaction even if UK Retail Sales for December exceed expectations, as markets largely anticipate the Bank of England to maintain a cautious, gradual easing stance despite stronger price pressures seen in December. Attention is likely to shift instead to the preliminary January S&P Global PMI readings from both the UK and the US, scheduled for release later in the day.

Sterling may find support if the US Dollar weakens amid rising risk aversion linked to geopolitical tensions. Earlier, US President Donald Trump threatened tariffs on European nations opposing his Greenland initiative, but later eased his stance after reaching a NATO framework agreement that opened the door to a potential deal.

From a technical perspective, GBP/USD is holding firm after climbing more than 0.5% in the previous session, hovering near the 1.3500 level at the time of writing. The pair could aim for the three-month peak at 1.3562 as the next resistance. On the downside, initial support is seen at the nine-day EMA around 1.3451, followed by the 50-day EMA near 1.3398.

The Australian dollar moved higher after stronger-than-expected employment data reinforced expectations of a tighter policy stance from the Reserve Bank of Australia. Seasonally adjusted employment in Australia increased by 65.2K in December, while the unemployment rate declined to 4.1%. Meanwhile, the U.S. dollar firmed after Bloomberg reported that President Trump would pause tariffs on European countries opposing his push over Greenland.

The Australian dollar strengthened against the U.S. dollar on Thursday after seasonally adjusted employment data from Australia reinforced expectations of a tighter monetary policy stance by the Reserve Bank of Australia. Data from the Australian Bureau of Statistics showed employment rose by 65.2K in December, reversing a revised loss of 28.7K jobs in November and well above the market forecast of a 30K increase. Meanwhile, the unemployment rate fell to 4.1% from 4.3%, beating expectations of 4.4%.

Sean Crick, head of labour statistics at the ABS, noted that a rise in employment among people aged 15–24 helped lift overall employment levels and contributed to the drop in the unemployment rate. Meanwhile, the International Monetary Fund has called on the RBA to proceed cautiously, pointing out that inflation has remained above the Bank’s 2%–3% target range for an extended period, despite headline CPI easing faster than expected in November.

U.S. dollar rises as Trump eases tariff threats against Europe

The U.S. Dollar Index (DXY), which tracks the greenback against six major currencies, was steady after posting modest gains in the previous session, trading around 98.80 at the time of writing. The dollar found support after Bloomberg reported on Wednesday that President Donald Trump said he would step back from imposing tariffs on goods from European countries opposing his bid to take control of Greenland. Earlier, Trump had insisted there was “no going back” on his ambitions for Greenland and had threatened to impose new 10% tariffs on eight European Union nations.

Trump also stated that the United States and NATO had “established the framework of a future deal on Greenland,” though he provided no details, leaving the scope and substance of the proposed agreement unclear.

U.S. labor market data has pushed expectations for further Federal Reserve rate cuts back to June, with Fed officials signaling little urgency to ease policy until there is clearer evidence that inflation is moving sustainably toward the 2% target. Morgan Stanley analysts revised their 2026 outlook, now projecting one rate cut in June and another in September, compared with their earlier expectations for cuts in January and April.

In Asia, the People’s Bank of China announced on Tuesday that it would keep its Loan Prime Rates unchanged, with the one-year and five-year LPRs remaining at 3.00% and 3.50%, respectively. Developments in China remain important for the Australian dollar, given the close trade relationship between the two economies.

China’s industrial production grew 5.2% year-on-year in December, accelerating from 4.8% in November, supported by resilient export-led manufacturing. However, retail sales increased just 0.9% year-on-year, falling short of expectations of 1.2% and slowing from November’s 1.3%.

In Australia, the TD-MI Inflation Gauge rose to 3.5% year-on-year in December from 3.2%, while monthly inflation jumped 1.0%, the fastest pace since December 2023 and a sharp acceleration from 0.3% in the previous two months.

RBA policymakers acknowledged that inflation has eased significantly from its 2022 peak, but recent data points to renewed upward pressure. Headline CPI slowed to 3.4% year-on-year in November, the lowest level since August, yet remains above the RBA’s 2–3% target range. Trimmed mean CPI edged down to 3.2% from 3.3% in October.

The RBA assessed that inflation risks have modestly tilted to the upside, while downside risks—particularly from global factors—have eased. Policymakers expect only one additional rate cut this year, with underlying inflation projected to stay above 3% in the near term before easing toward around 2.6% by 2027.

Australian dollar tests the 0.6800 level near the top of its ascending channel

AUD/USD was trading near 0.6790 on Thursday. Daily chart signals show the pair continuing to climb within an ascending channel, reflecting a sustained bullish bias. The nine-day exponential moving average remains above the 50-day EMA, with prices holding above both indicators, reinforcing the positive momentum and keeping upside pressure intact. Meanwhile, the 14-day Relative Strength Index stands at 69.93, close to overbought territory, suggesting momentum is becoming stretched.

The pair is currently challenging immediate resistance at the psychological 0.6800 level, followed by the upper boundary of the ascending channel near 0.6810. A decisive break above the channel could open the door to 0.6942, marking the highest level since February 2023.

On the downside, initial support is seen at the nine-day EMA around 0.6732. A move below this short-term support would undermine bullish momentum, bringing the lower boundary of the ascending channel near 0.6680 into focus, ahead of the 50-day EMA at 0.6656.

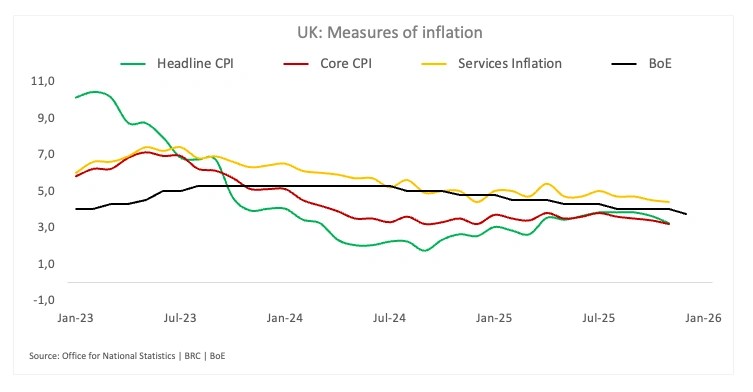

The UK’s Office for National Statistics (ONS) is set to release December CPI data on Wednesday. Headline inflation is expected to edge up to 3.3%, while core inflation is projected to remain sticky above 3.0% year-on-year.

The UK Office for National Statistics (ONS) is scheduled to publish December Consumer Price Index (CPI) data at 07:00 GMT on Wednesday, a release closely watched by financial markets. Economists anticipate a mild pickup in inflationary pressures.

UK inflation remains a key consideration for the Bank of England (BoE) and is typically a significant driver of Sterling movements. With the Monetary Policy Committee (MPC) due to meet on February 5, markets largely expect policymakers to leave the bank rate unchanged at 3.75%, though this week’s inflation figures are likely to influence the guidance and tone of the decision.

What might the upcoming UK inflation report reveal?

Headline UK CPI is projected to tick up to 3.3% year-on-year in December, compared with 3.2% in November. On a monthly basis, inflation is expected to rebound by 0.4%, reversing the 0.2% month-on-month decline seen previously.

Meanwhile, core inflation—which excludes volatile food and energy prices and is more closely monitored by the Bank of England—is anticipated to remain steady at 3.2% annually. Month-on-month, core CPI is forecast to rise by 0.3% after falling 0.2% in November.

What impact will the UK CPI data have on GBP/USD?

In December, the Bank of England’s Monetary Policy Committee narrowly voted 5–4 to reduce the bank rate by 25 basis points to 3.75%, marking its fourth cut in 2025. Although policymakers pointed to easing inflation pressures and initial signs of a softening labour market, they emphasised that any additional policy loosening would proceed cautiously.

The December Decision Maker Panel (DMP) survey largely reinforced this outlook and failed to alter expectations around the policy path. Persistent wage pressures continue to constrain the potential for significant repricing at the short end of the yield curve.

One-year-ahead wage growth expectations rose slightly to 3.7% from 3.6%, while actual pay growth over the past year remains in the mid-4% range. Both indicators remain well above levels consistent with a sustained return of inflation to the BoE’s target.

Overall, the survey does little to shift sentiment and supports the argument against accelerating rate cuts. Markets currently price in just over 42 basis points of easing for the year, with the BoE widely expected to keep rates unchanged at its next meeting.

From a technical perspective, Pablo Piovano highlights that GBP/USD is facing resistance near its yearly lows around 1.3340, recorded on January 19. A further decline could open the door to the 55-day simple moving average at 1.3309, followed by the December low at 1.3179. Conversely, if buyers regain control, the year-to-date high at 1.3567 may act as the first upside hurdle, with little resistance beyond that until the September 2025 peak at 1.3726.

Piovano also notes that momentum indicators remain supportive, with the Relative Strength Index rebounding to around 54 and the Average Directional Index near 20, pointing to a reasonably firm underlying trend.

Most Asian currencies traded within narrow ranges on Tuesday, while the U.S. dollar weakened as President Donald Trump’s renewed demands over Greenland dampened appetite for U.S. assets.

Regional markets showed little response to China’s decision to keep a key lending rate unchanged, as expected, while the Japanese yen was steady after Prime Minister Sanae Takaichi called a snap election for early February.

A U.S. market holiday on Monday limited overnight signals, leaving Asian markets broadly risk-averse after President Trump announced tariffs on Europe over Greenland over the weekend.

Japanese yen little changed ahead of snap vote and BOJ meeting

The Japanese yen weakened slightly on Tuesday, with USD/JPY slipping 0.1%, though the pair remained near recent highs amid a lack of strong supportive signals for the currency. Prime Minister Sanae Takaichi said on Monday that she will dissolve Japan’s lower house this week and call a snap election for February 8.

With Takaichi enjoying solid approval ratings, the early election is expected to strengthen her mandate for additional fiscal stimulus. However, markets questioned the scope for further government spending, as Japanese government bonds extended their selloff, which in turn pressured the yen.

The election announcement also comes ahead of a Bank of Japan policy meeting on Friday, with investors divided over whether the central bank has sufficient momentum to raise interest rates again.

The central bank raised interest rates at its final meeting of 2025 and signaled that further hikes would be driven by sustained gains in inflation and wages. However, the BOJ may pause before tightening again until it gains clearer insight into Japan’s spring wage negotiations, scheduled for March–April.

Dollar under pressure as Trump–Greenland tensions persist

The dollar index and its futures slipped about 0.1% in Asian trading, as the greenback faced pressure from growing caution toward U.S. assets amid President Trump’s push to acquire Greenland.

European leaders largely rejected Trump’s tariff threats and reiterated that Greenland should remain part of the Kingdom of Denmark. Trump on Monday renewed his demands for the island and declined to rule out the use of military force.

The U.S. president is now set to attend the World Economic Forum in Davos, Switzerland, where he may hold discussions with European leaders on the Greenland issue. Asian currencies remained mostly subdued amid broader risk aversion linked to Trump’s Greenland stance.

The Chinese yuan saw USD/CNY edge slightly lower, showing little response to the People’s Bank of China’s decision to leave its loan prime rate unchanged. The currency, however, stayed near its strongest levels in two and a half years after a series of firm midpoint fixings by the PBOC. Elsewhere, USD/TWD rose 0.3%, while AUD/USD gained 0.3%, with the Australian dollar supported by the softer U.S. dollar.

The South Korean won weakened slightly, with USD/KRW rising 0.2%, while the Singapore dollar also softened as USD/SGD added 0.1%. The Indian rupee saw USD/INR edge up 0.1% and hover near the 91-per-dollar level, as growing concerns over the health of India’s economy weighed on the currency.

Few analysts had a U.S. invasion of Greenland anywhere near the top of their 2026 market outlooks. President Trump’s surprise weekend tariff move has triggered a classic risk-off reaction, with gold rallying around 2%, equities down 1.0–1.5%, and the dollar coming under modest pressure. This week’s World Economic Forum in Davos is now set to become a focal point for U.S.–European diplomacy, with elevated FX volatility likely.

USD: Too Early to Embrace the ‘Sell America’ Narrative

Washington escalated its pursuit of Greenland over the weekend, with the threat of 10% tariffs—potentially rising to 25%—on eight European countries appearing consistent with a broader “maximum pressure” strategy to force a deal. Political commentary in Europe suggests this could mark the end of the EU’s long-standing policy of accommodation toward the U.S., with France emerging as a key advocate for deploying the EU’s Anti-Coercion Instrument, which allows for retaliatory measures spanning tariffs, taxation, and investment restrictions against coercive trade actions.

The issue, alongside growing concerns about strains within NATO, is set to dominate the policy agenda in a week that might otherwise have focused on Ukraine. President Donald Trump is scheduled to speak at the World Economic Forum in Davos on Wednesday, followed by an EU leaders’ meeting on Thursday. A central question is whether Europe adopts China’s approach from last year—matching U.S. tariffs one-for-one—to ultimately force a de-escalation from Washington.

Initial market reactions have been cautious but telling: gold has gapped roughly 2% higher, German DAX futures are down around 1.5%, and the U.S. dollar is marginally weaker. While U.S. cash markets are closed for the Martin Luther King Jr. holiday, S&P 500 futures are indicating losses of about 0.8%. Still, it may be premature to revive the “Sell America” narrative. As with last April’s near-50% “Liberation Day” tariff threats, investors appear reluctant to chase what often proves to be aggressive rhetoric that ultimately gives way to diplomatic negotiation.

Nonetheless, these developments are likely to inject a degree of volatility into what has otherwise been a relatively calm investment environment. On the broader “Sell America” theme, we noted on Friday that there was little concrete evidence of meaningful de-dollarisation last year. Even in a scenario where geopolitical tensions were to escalate materially, it appears unlikely that the dollar would experience a sell-off on the scale of last year’s near-10% decline, particularly given that the buy-side was then unusually under-hedged in U.S. dollar exposure.

Beyond the Greenland issue, this week may also bring clarity on the future leadership of the Federal Reserve. President Trump could announce his nominee to succeed Jerome Powell as Fed Chair. The dollar rallied on Friday after reports suggested Trump wants Kevin Hassett to remain at the National Economic Council, with Kevin Warsh now viewed as the leading candidate—an outcome that would be modestly supportive for the dollar if confirmed.

Overall, U.S. economic data are likely to take a back seat to political developments in the coming days. In the near term, the dollar may probe lower levels. For DXY, gap resistance around 99.35 could cap upside, while a corrective move toward the 98.80–98.85 zone remains the mild tactical bias.

EUR: Unwelcome Developments

The renewed tensions surrounding Greenland and the prospect of fresh tariffs are particularly negative for European industry. This comes just as industrial confidence had begun to recover, with firms appearing to have adapted to last year’s tariff-related volatility. The latest developments are likely to sharpen the focus among European policymakers on boosting domestic demand and may even add momentum to long-delayed reforms such as the Savings and Investment Union, aimed at strengthening Europe’s capital markets and enhancing their competitiveness relative to the U.S.

In FX markets, EUR/USD has established support just below 1.1600. Initial intraday resistance is seen near 1.1650, with scope for a move toward the 1.1690–1.1700 area if that level is cleared. Short-dated implied volatility for EUR/USD, both one-week and one-month, has edged higher, reflecting the elevated uncertainty surrounding the week ahead.

GBP: Poised for Relative Outperformance This Week

We believe this week’s U.K. data — November employment figures and December CPI — may offer modest support to sterling, potentially extending the short-covering rally that has been underway since late November. While EUR/GBP was initially seen as the more vulnerable cross, with downside risks toward 0.8600, early-week dollar softness could shift the bulk of the move into GBP/USD. A sustained break above the 1.3415–1.3420 zone would open scope for a move toward 1.3450–1.3460.

That said, sterling historically underperforms during pronounced risk-off phases, and the current environment remains fluid with multiple cross-currents at play.

Futures tied to major U.S. stock indexes fell after President Donald Trump raised the prospect of imposing tariffs as part of his push to acquire Greenland. European leaders discussed possible retaliation against the measures, which they described as a form of blackmail. Gold climbed to a fresh record high, while oil prices edged lower as traders assessed Trump’s remarks and the EU’s response. Elsewhere, China’s economic growth slowed in the fourth quarter but still met Beijing’s 2025 target.

U.S. futures and global stocks decline

U.S. stock futures pointed lower on Monday as investors weighed President Donald Trump’s threat to impose tariffs on several European countries until the United States is allowed to acquire Greenland.

By 03:05 ET (08:05 GMT), Dow futures were down 404 points, or 0.8%, S&P 500 futures had fallen 66 points, or 1.0%, and Nasdaq 100 futures were off 336 points, or 1.3%.

With U.S. cash markets closed for the Martin Luther King Jr. Day holiday, the immediate reaction to Trump’s latest tariff threat will be delayed. Risk-off sentiment has spread globally, dragging equities lower across Europe and Asia.

ING analysts said Trump’s comments, following last year’s sweeping global tariffs, have pushed trade tensions into “an entirely new dimension,” driven less by economic considerations and more by political motives. They added that while past experience suggests caution in reacting to dramatic announcements, some of Trump’s threats over the past year have ultimately been carried out.

Focus on Trump’s Greenland tariffs

European leaders agreed on Sunday to intensify efforts to counter President Donald Trump’s tariff threats, with reports suggesting EU officials are considering strong retaliatory measures if the levies are imposed.

On Saturday, Trump said he would introduce 10% tariffs on exports from eight European countries—Denmark, Sweden, France, Germany, the Netherlands, Finland, Norway and the United Kingdom—until the United States is able to acquire Greenland. He added that the tariffs would be raised to 25% if the purchase of the semi-autonomous Danish territory does not go ahead. Trump has framed the move as a national security necessity, a claim European governments have rejected, describing it as blackmail.

Ahead of an emergency EU summit in Brussels on Thursday, member states are expected to debate a range of responses, including a potential €93 billion tariff package on U.S. imports and the possible use of the bloc’s “Anti-Coercion Instrument,” which could restrict U.S. access to investment, banking and services markets. Reuters, citing an EU source, reported that the tariff package currently has broader backing.

Trump’s latest tariff threat has also cast doubt over the future of a U.S.–EU trade agreement reached last year, with EU officials saying they cannot approve the deal while Washington pursues control of Greenland. ING analysts said that while the outcome of the dispute remains uncertain, it underscores the lack of predictability in global trade and tariff policy.

Gold reaches record high

Gold prices climbed to record highs in Asian trade on Monday, nearing $4,700 an ounce, as investors rushed into safe-haven assets following President Trump’s latest tariff threat.

Spot gold rose 1.6% to $4,667.33 an ounce by 02:26 ET (07:26 GMT), after earlier touching a record $4,690.75. U.S. gold futures also hit a new peak at $4,697.71 an ounce.

Silver prices surged more than 4% to a fresh all-time high of $94.03 an ounce, supported by safe-haven demand as well as its role as an industrial metal.

Oil prices edge lower

Oil prices edged lower, giving back part of last week’s gains as markets weighed the growing risk of a trade dispute linked to Greenland. Brent crude slipped 0.1% to $59.74 a barrel, while U.S. West Texas Intermediate fell 0.1% to $55.95.

Crude had rallied early last week on concerns that unrest in Iran could threaten oil supplies from the Middle East, a region that accounts for a significant share of global output. Much of that risk premium faded after President Trump ruled out immediate U.S. military action, leading prices to pull back before stabilizing toward the end of the week.

China’s economy meets 2025 growth target

China’s economy grew slightly more than expected in the fourth quarter of 2025, data released on Monday showed, as policy stimulus and a pickup in consumption helped the country meet its annual growth target.

Gross domestic product rose 4.5% year on year in the October–December period, in line with forecasts but down from 4.8% in the previous quarter, marking the slowest pace in three years. On a quarter-on-quarter basis, GDP expanded 1.2%, marginally above expectations of 1.1%.

The result brought full-year 2025 growth to 5%, meeting Beijing’s target. The government is widely expected to set a similar 5% growth goal again, as it continues to face heightened U.S. trade tensions, weak consumer demand and a prolonged property sector downturn.

EUR/USD edges higher toward the 1.1625 area in early European trading on Monday, as the euro finds support from signs that Europe is prepared to respond to U.S. tariff measures.

The move follows President Donald Trump’s announcement of a 10% tariff on goods from several European countries, prompting pushback from European leaders.

Meanwhile, expectations that the Federal Reserve will keep interest rates unchanged at its January meeting—amid a resilient labor market and still-elevated inflation—have weighed on the U.S. dollar, providing additional support for the pair.

The EUR/USD pair advances to around 1.1625 in early European trading on Monday, snapping a four-day losing streak. The U.S. dollar comes under modest pressure against the euro after President Donald Trump threatened to escalate tariffs on eight European nations opposing his proposal for the United States to acquire Greenland.

U.S. markets are closed on Monday in observance of Martin Luther King Jr. Day.

Over the weekend, Trump announced a 10% tariff on goods from Denmark, Norway, Sweden, France, Germany, the Netherlands, Finland, and the United Kingdom, set to take effect on February 1. He added that the levy would rise to 25% in June unless an agreement is reached allowing the U.S. to purchase Greenland.

Europe is set to respond after President Donald Trump imposed additional tariffs on key allies, with European leaders expected to convene an emergency meeting in the coming days to consider potential retaliation. Renewed concerns over a trade war and the longer-term implications of Trump’s latest move have weighed on the U.S. dollar, providing support for the EUR/USD pair.

“While one could argue the tariffs are a threat to Europe, it is actually the dollar that is absorbing most of the impact, as markets appear to be pricing in a higher political risk premium for the U.S. currency,” said Khoon Goh, head of Asia research at ANZ.

That said, stronger-than-expected U.S. labor market data released last week have delayed expectations for further Federal Reserve rate cuts until June, which could help cap downside pressure on the dollar. According to the CME FedWatch tool, markets are pricing in nearly a 95% probability that the Federal Open Market Committee will leave rates unchanged at its January 27–28, 2026 meeting.

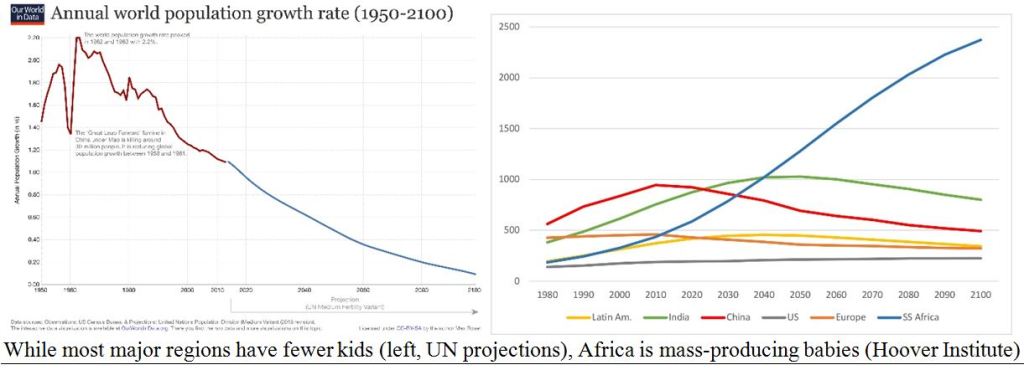

Economic growth depends on population expansion and the formation of new households. While the idea of fewer people—less congestion, smaller crowds, and reduced strain on infrastructure—may seem appealing, the risks associated with population decline are often understated. Much like deflation, a shrinking population poses serious and potentially greater threats to long-term economic stability.

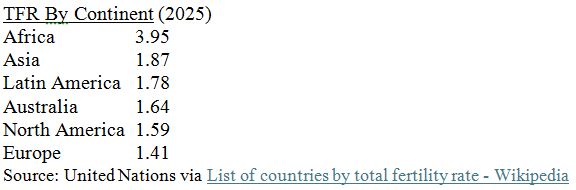

Demographers use the “total fertility rate” (TFR), defined as the average number of births per woman, as a key measure of population sustainability. A TFR of at least 2.1 is required to maintain a stable population, with the additional 0.1 accounting largely for infant mortality. Although the global TFR stood at 2.24 last year, this figure masks significant regional disparities. Excluding Africa, the global fertility rate falls well below 2.0.

In 2025, most major advanced economies reported TFRs under the replacement threshold of 2.0, underscoring the growing demographic challenge facing industrialized nations.

No major developed economy currently records a total fertility rate above the 2.1 replacement threshold. Outside of Africa, global population growth is already in decline. Historically, from 1950 to 1970, the world’s wealthiest nations averaged more than 2.7 births per woman. Since 1995, however, that figure has fallen sharply to around 1.6, reaching a record low of approximately 1.5 during the 2020–2025 period.

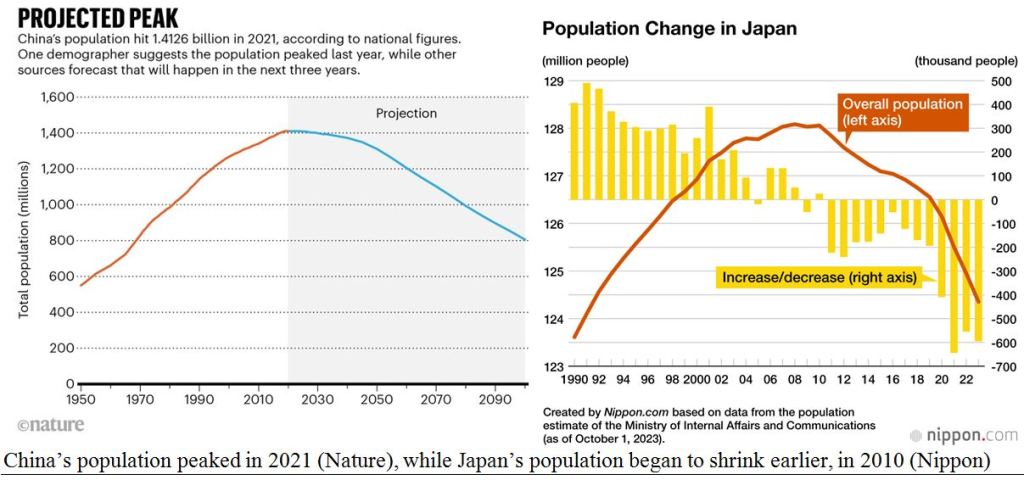

Globally, population growth remains marginally positive, driven largely by demographic expansion in Africa and rising life expectancy among older populations. However, Asia’s two largest economies—China and Japan—are experiencing population decline, a trend that constrains their long-term growth potential. More critically, shrinking cohorts of younger workers are increasingly unable to shoulder the financial burden of supporting aging populations that are living longer and often facing higher healthcare needs.

China has formally abandoned its long-standing one-child policy, but behavioral patterns shaped by decades of enforcement have proven difficult to reverse. Today, many young couples are reluctant to have even a single child, prioritizing career advancement and higher incomes instead. Compounding the challenge, the legacy of the policy produced severe demographic distortions. Prior to 2010, widespread prenatal sex selection—driven by the desire to raise a single male “heir” to support parents in old age—led to a significant gender imbalance, with roughly 118 male births for every 100 female births between 2002 and 2008. The result is a surplus of men and a shrinking pool of potential spouses.

In the mid-1990s, a typical Chinese household consisted of four grandparents, two parents, and one heavily relied-upon child—the so-called “young emperor.” This inverted demographic pyramid is financially unsustainable, as the burden of supporting multiple generations increasingly falls on a single income earner.

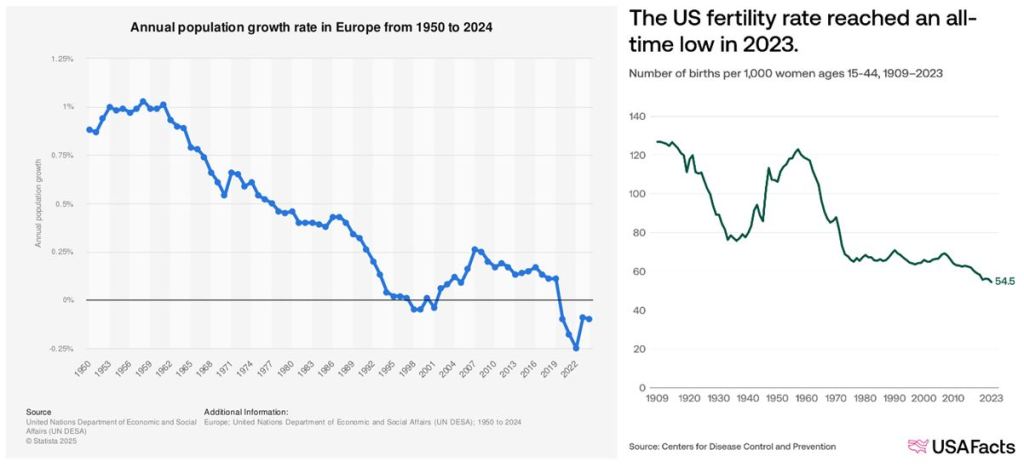

Europe faces an even steeper demographic challenge. With an average fertility rate of just 1.4 children per woman and a comparatively generous system of old-age pensions, the region confronts mounting fiscal pressure. These constraints help explain Europe’s historical reliance on the United States for security spending—a strategy that may prove risky as President Donald Trump presses European nations to assume greater responsibility for their own defense.

The United States remains in a stronger demographic position than Europe or much of Asia, in part because of its relatively effective assimilation of immigrants and higher rates of family formation in more conservative regions of the country. However, with the administration introducing tighter immigration restrictions and stepping up efforts to detain and deport undocumented workers, questions are emerging over whether there will be a sufficient supply of willing young workers to staff the growing number of factories being brought back onshore.

Another structural risk embedded in these demographic trends is the growing strain on Social Security and Medicare. These programs function as intergenerational compacts, in which today’s workers finance the retirement and rising healthcare costs of the elderly. Unlike 401(k) plans or IRAs, they are not savings vehicles but largely unfunded entitlements built on historical assumptions of higher birth rates and a broad, growing workforce.

As younger generations are increasingly less likely to marry, have children, or pursue stable, high-earning careers—instead relying more on gig-based employment—the system faces mounting pressure. These shifts raise serious concerns about the long-term sustainability of funding future benefits, particularly in a society producing fewer contributors to support the next generation of retirees.

The Australian dollar advanced after the TD-MI Inflation Gauge rose to 3.5% year-on-year in December.

China’s GDP grew 1.2% quarter-on-quarter in the fourth quarter of 2025, accelerating from the previous quarter and exceeding market expectations.

Meanwhile, the U.S. dollar struggled as risk aversion intensified amid escalating uncertainty surrounding U.S.–Greenland developments.

The Australian dollar strengthened against the U.S. dollar on Monday after Australia’s TD-MI Inflation Gauge rose to 3.5% year-on-year in December, up from 3.2% previously.On a monthly basis, inflation jumped 1.0% in December 2025, marking the fastest pace since December 2023 and a sharp acceleration from the 0.3% increases seen in the prior two months.

AUD/USD also found support from China’s key economic data, with developments in the Chinese economy closely watched given Australia’s strong trade links with China.

Data from China’s National Bureau of Statistics showed industrial production grew 5.2% year-on-year in December, accelerating from 4.8% in November, supported by resilient export-led manufacturing activity.

China’s GDP expanded 1.2% quarter-on-quarter in the fourth quarter of 2025, up from 1.1% in Q3 and above the market consensus of 1.0%. On an annual basis, GDP rose 4.5% in Q4, easing from 4.8% in the previous quarter but beating expectations of 4.4%.

Meanwhile, retail sales rose 0.9% year-on-year in December, falling short of forecasts for a 1.2% increase and November’s 1.3% reading.In contrast, industrial output exceeded expectations, rising 5.2% YoY versus estimates of 5.0% and improving from 4.8% a month earlier.

U.S. Dollar softens amid escalating uncertainty over the U.S.–Greenland dispute

The US Dollar Index (DXY), which tracks the Greenback against six major currencies, is under pressure and hovering near 99.20 at the time of writing. US financial markets remain closed on Monday in observance of Martin Luther King Jr. Day, resulting in thinner liquidity.

The Dollar has come under renewed pressure amid rising risk aversion, fueled by growing uncertainty surrounding the US–Greenland dispute. Over the weekend, US President Donald Trump reiterated plans to impose tariffs on eight European nations that have opposed his proposal for the United States to acquire Greenland.