The inflation print investors had been bracing for came in cooler than expected.

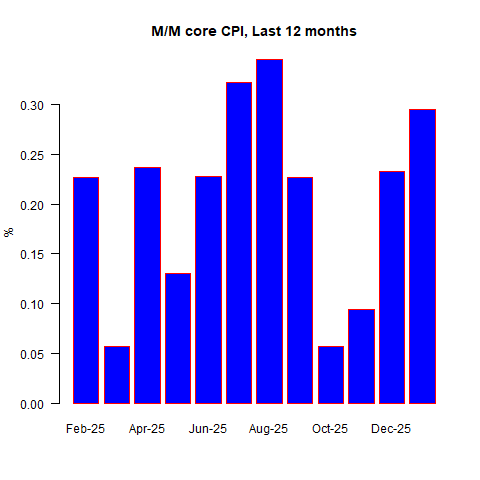

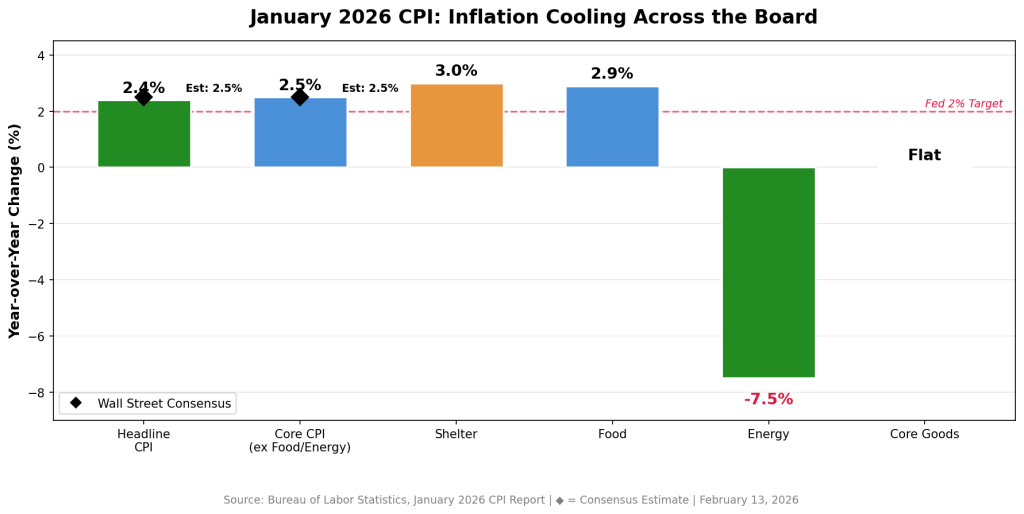

Friday’s January CPI showed headline inflation at 2.4%—below the 2.5% consensus forecast and the lowest annual reading since May 2025. Core CPI, which excludes food and energy, eased to 2.5%, marking its softest level since April 2021. On a monthly basis, prices rose just 0.2%, the smallest increase since July.

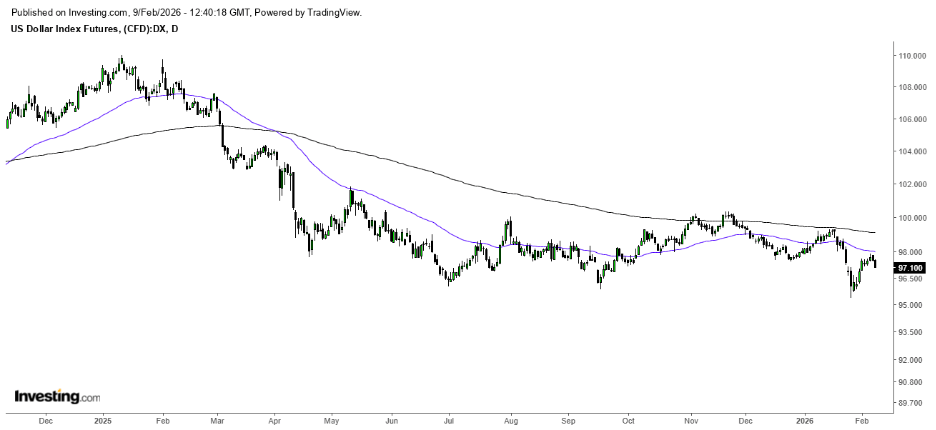

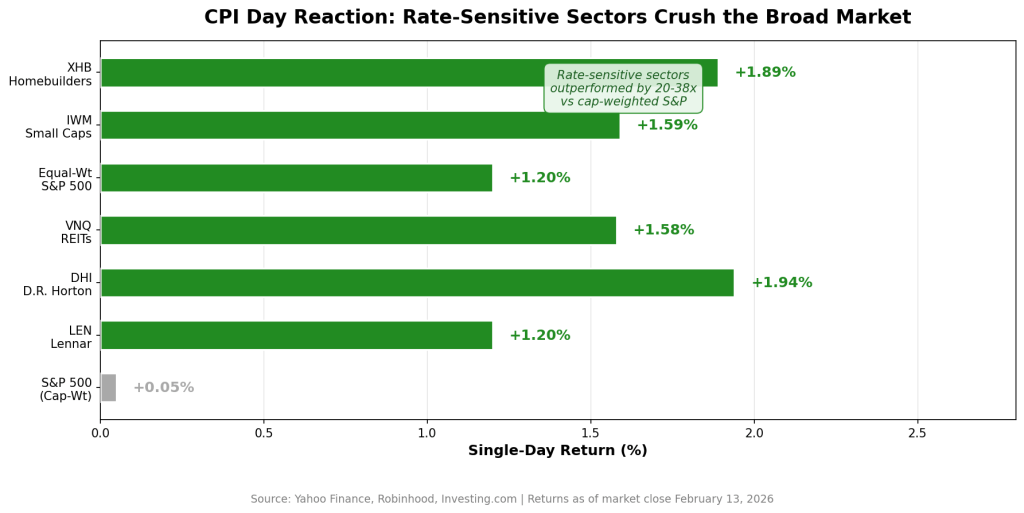

Markets reacted swiftly. Homebuilder stocks rallied sharply, small caps climbed 1.2%, and the 10-year Treasury yield slid to its lowest point since early December.

My takeaway: the market may have just received the confirmation it was waiting for. And the most compelling opportunities from here likely aren’t the mega-cap tech leaders that have dominated performance, but rather rate-sensitive sectors that were punished under the “higher for longer” narrative and are now repricing for a potentially different 2026 backdrop.

What the CPI Report Really Signals

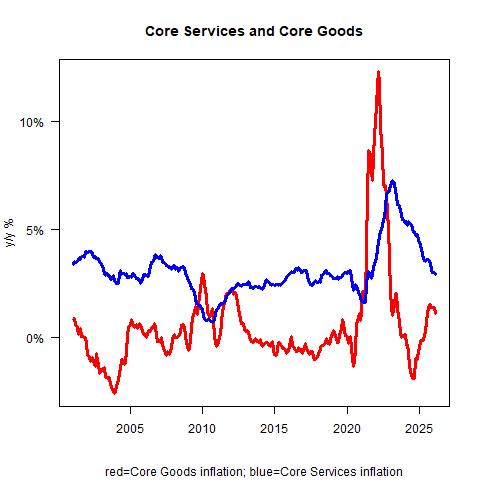

Shelter—by far the largest CPI component and the category that has stubbornly kept headline inflation elevated—rose only 0.2% in January, bringing the annual rate down to 3%. That’s a notable slowdown and perhaps the clearest indication yet that the housing inflation lag is beginning to unwind.

Energy prices declined 1.5%, with gasoline tumbling 3.2% during the month. Food inflation held at 2.9% year over year—still somewhat elevated, but not alarming. Importantly, core goods prices were flat, helping to counter concerns that renewed tariffs would reignite goods inflation.

“Headline CPI inflation was a touch softer than expected in January, delivering a welcome surprise to the downside at the beginning of the year,” said Bernard Yaros, lead economist at Oxford Economics. He added that tariff-related price pressures “are largely behind us.”

Lindsay Rosner of Goldman Sachs Asset Management was even more direct: “Trust the groundhog. The Fed’s path to normalization cuts appears clearer now.”

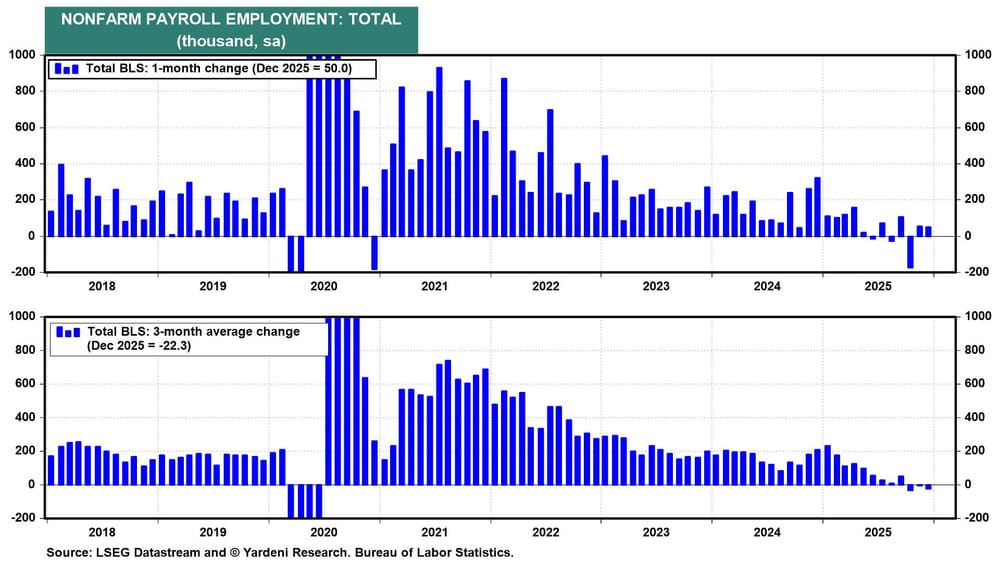

The timing is critical. A stronger-than-expected January jobs report—130,000 payrolls versus forecasts of 55,000—had pushed expectations for rate cuts further out, likely into the summer. This softer CPI reading shifts that outlook. Economists surveyed by Bloomberg now anticipate as much as 100 basis points of easing this year, with the first cut potentially arriving in June—or even March if disinflation continues.

Why Rate-Sensitive Stocks Stand Out

One key dynamic investors often overlook is that by the time the Federal Reserve actually begins cutting rates, much of the upside in rate-sensitive sectors has already played out. Markets tend to price in policy shifts well in advance.

Friday’s CPI data appeared to give institutional investors the confidence to begin reallocating toward sectors poised to benefit from lower yields. The equal-weight version of the S&P 500 and the Russell 2000 both climbed 1.2%, notably outperforming the traditional cap-weighted S&P 500, which was little changed.

That divergence is often viewed as a textbook signal of sector rotation—away from mega-cap dominance and toward more rate-sensitive, economically cyclical areas of the market.

Capital is rotating down the market-cap ladder and into economically sensitive groups. Three segments stand out most clearly: homebuilders, REITs, and small caps.

How to Position

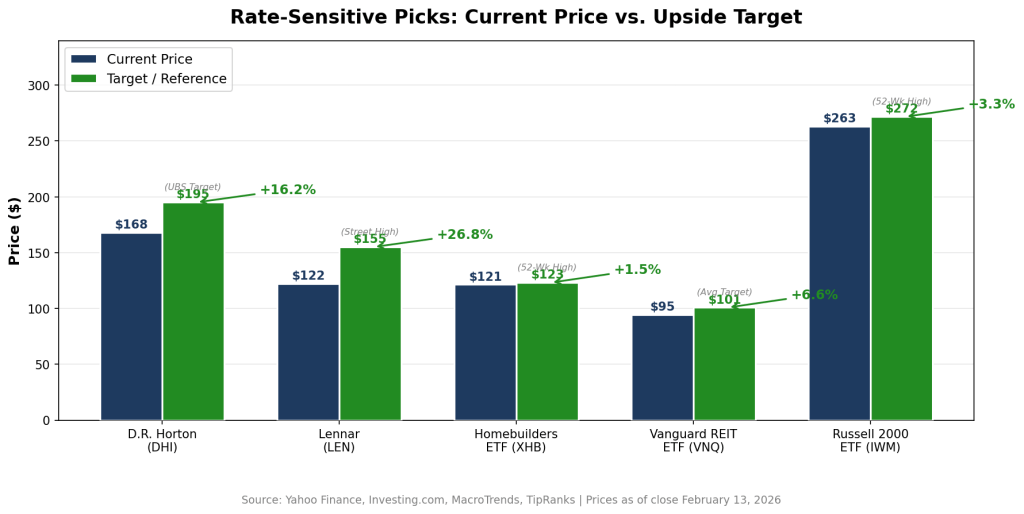

D.R. Horton (DHI)

Closing Friday at $167.78, DHI is arguably the purest expression of the housing-affordability theme. The largest U.S. homebuilder by volume posted solid fiscal Q1 results in January, with revenue of $6.89 billion (ahead of $6.59 billion estimates) and EPS of $2.03 (vs. $1.93 expected).

At roughly 15.3x trailing earnings, the stock trades at a notable discount to the broader market. Beyond the rate backdrop, there’s also a policy angle: the Trump administration’s reported “Trump Homes” initiative has involved direct engagement with builders around affordability measures—potentially creating a dual tailwind of lower mortgage rates and regulatory support.

The median analyst price target is $170, with UBS as high as $195—suggesting upside potential of roughly 16%.

Lennar (LEN)

Trading at $122.28, Lennar offers a slightly different profile as the second-largest U.S. builder. Its “land-light” model—optioning land instead of holding it outright—reduces balance-sheet risk and positions it well for a rate-cutting cycle.

The stock has rebounded about 40% from its April 2025 lows but remains below its 2024 peak. With fiscal Q1 earnings due in late March, improving mortgage application trends could serve as a near-term catalyst if rates continue to ease.

SPDR S&P Homebuilders ETF (XHB)

At $121.36, XHB is up nearly 18% year-to-date and recently marked a fresh 52-week high of $123.13. As an equal-weighted ETF, it offers diversified exposure across the housing ecosystem—not just large builders, but also building products manufacturers, home improvement retailers, and construction suppliers.

For investors who prefer sector exposure over single-stock risk, XHB provides a balanced approach.

Vanguard Real Estate ETF (VNQ)

Trading near $94.59—close to its 52-week high—VNQ provides broad exposure to the REIT space, one of the most rate-sensitive areas of the market. The ETF holds over 150 REITs across healthcare, industrial, data center, and retail subsectors.

Its largest holdings include Welltower, Prologis, and American Tower.

With an average analyst target near $100.81, implied upside sits around 8%, in addition to a dividend yield of roughly 3.6%. After significant underperformance during the rate-hiking cycle, REITs are positioned to benefit mechanically as yields decline.

iShares Russell 2000 ETF (IWM)

At approximately $263, IWM tracks small-cap equities—arguably the most interest-rate-sensitive segment of the equity market. Smaller firms tend to carry more floating-rate debt and are disproportionately affected by elevated borrowing costs. That dynamic can reverse sharply when policy eases.

IWM surged 1.6% on Friday’s CPI release alone. With its 52-week high of $271.60 within reach, sustained rate declines could drive a prolonged catch-up rally in small caps.

The Big Picture

If inflation continues to moderate and rate-cut expectations firm, the leadership baton may continue shifting away from mega-cap growth and toward housing, real estate, and smaller domestically oriented companies. Markets typically front-run the policy cycle—and this rotation suggests that repositioning may already be underway.

The Bear Case (and Why It May Be Overstated)

There are valid reasons for caution. Fox Business pointed out that January’s CPI could carry a downward bias tied to last fall’s government shutdown. During that period, the Bureau of Labor Statistics missed portions of October data collection and relied on a “carry-forward” methodology that may influence inflation readings into spring 2026. In short, the 2.4% headline figure could be somewhat understated.

There’s also the Federal Reserve itself. Policymakers are not signaling urgency. Oxford Economics continues to project cuts in June and December rather than March. Meanwhile, although the labor market is cooling—annual benchmark revisions show 2025 job growth was the weakest since 2003 outside recessionary periods—it is far from collapsing. Jerome Powell has consistently emphasized the need for a sustained disinflation trend, not a single favorable report.

The Counterargument

Even if the Fed waits until June, markets won’t. Yields have already declined meaningfully. Mortgage rates are edging lower. And sectors that trade on rate expectations—rather than the actual fed funds rate—are beginning to reprice now. By the time the first official cut arrives, much of the move in rate-sensitive equities could already be behind us.

What to Watch

Three near-term catalysts will likely shape the next phase:

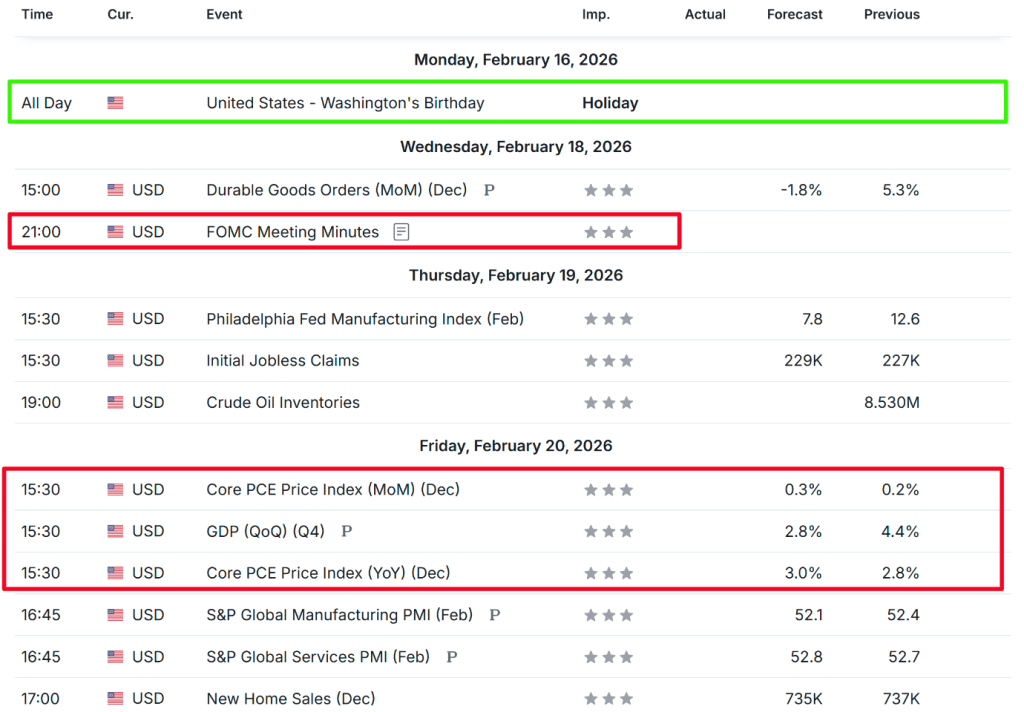

- Fed Minutes (Feb. 18): The release of the latest policy meeting minutes could shift expectations quickly. Any dovish commentary on inflation progress or labor-market softness may pull forward rate-cut pricing.

- Walmart Q4 Earnings (Feb. 19): As the largest U.S. retailer—now with a market cap above $1 trillion and up 13% year-to-date—Walmart’s guidance will offer real-time insight into consumer spending trends. If easing inflation is translating into stronger purchasing power, that reinforces the soft-landing narrative.

- PCE Price Index (Later This Month): The Fed’s preferred inflation gauge will be pivotal. Confirmation of CPI’s cooling trend would likely solidify expectations for a June cut and intensify debate around a possible March move—potentially fueling the next leg higher in rate-sensitive stocks.

Bottom Line

The inflation backdrop has shifted in a way that favors investors. The opportunity isn’t complex—but it does require stepping away from the mega-cap tech trade that has dominated for the past two years and leaning into sectors positioned to benefit most from falling yields.

Sources: Jaachi Mbachu