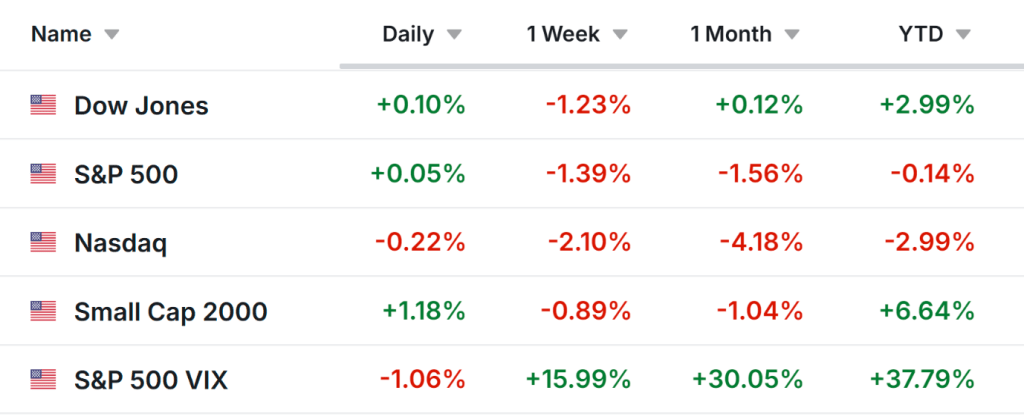

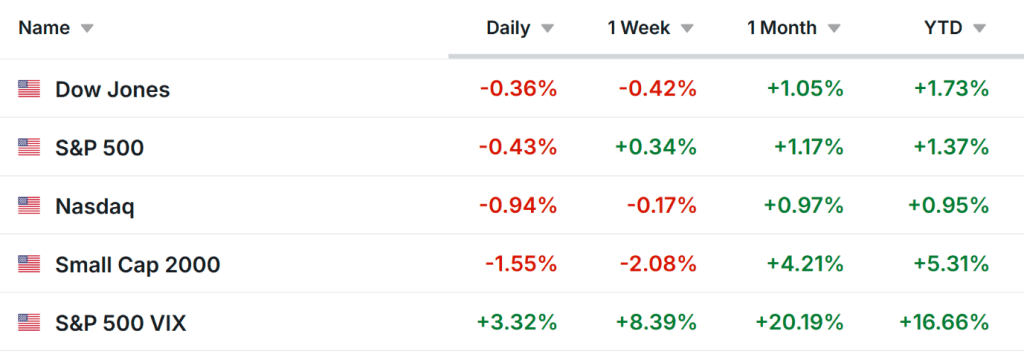

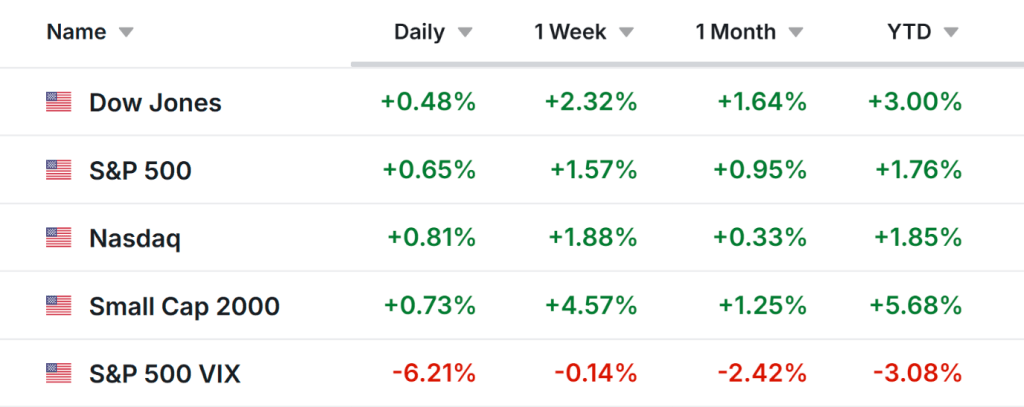

Volatility in the S&P 500 has led to repeated swings without the steady upward momentum that characterized much of late 2025. With concerns about a potential correction—such as the bursting of an AI-driven bubble—investors may look toward more defensive options like dividend-paying stocks.

That said, dividend investing spans a wide spectrum. While many gravitate toward globally recognized, ultra-stable companies favored by figures like Warren Buffett, lesser-known firms can sometimes offer both dependable income and greater growth potential. Three under-the-radar dividend payers worth noting are Hancock Whitney Corp., NewMarket Corp., and Horace Mann Educators Corp..

A Well-Capitalized Southern Bank Gaining Momentum

Hancock Whitney Corp. is a bank holding company best known in the Gulf South. Through Hancock Whitney Bank, it provides commercial and retail banking along with wealth management services.

The company offers a solid 2.53% dividend yield and maintains a conservative payout ratio of 31.7%. In Q4 2025, earnings per share narrowly exceeded expectations by one cent, though revenue fell short.

Looking ahead to 2026, several factors strengthen its outlook. The company recently completed a bond portfolio restructuring expected to lift net interest margin by about 7 basis points and boost annual EPS by roughly $0.23. Loan growth is improving, and a strong capital position supported share buybacks totaling about 3% of outstanding shares in Q4 alone. That same capital base reinforces dividend sustainability, making it appealing for risk-conscious investors.

NewMarket: Resilient Income Despite Market Pressures

NewMarket Corp., a specialty chemicals company focused on lubricants and petroleum additives, has seen its shares decline roughly 14% year to date following its latest earnings release.

Lower net income and EPS in 2025—largely due to a higher effective tax rate—pressured results, while fourth-quarter petroleum additive shipments fell about 6% year over year amid softer demand.

However, its specialty materials division has performed strongly, bolstered by the October acquisition of aerospace propellant firm Calca. The company plans to invest $1 billion to expand this segment further in 2026.

Despite a Wall Street “Hold” rating, NewMarket continues generating strong cash flow. Last quarter alone, it returned $183 million to shareholders through dividends and buybacks. The stock yields 2.01%, carries a payout ratio just over 27%, and has consistently raised its dividend over multiple years.

Horace Mann’s Broad Strength Supports Its Dividend

Horace Mann Educators Corp., which provides retirement, property, and casualty insurance products tailored to U.S. school employees, has posted several strong quarters.

Its latest results included a 3-cent EPS beat and record full-year EPS of $4.71. Forecasts for 2026 align with the company’s 10% compound annual growth target.

Much of this improvement stems from its property and casualty segment, where both the combined ratio and core earnings improved significantly—more than doubling last year. Growth in individual supplemental and group sales has further diversified the business.

An early retirement initiative is expected to generate $10 million in annual savings, helping the company reduce its expense ratio by 100–150 basis points over the next three years. This should enhance cash flow for additional buybacks—after $21 million in repurchases in 2025—and continued dividend support. The stock currently offers a 3.25% yield with a 35.9% payout ratio.

In a market environment marked by uneven performance, these lesser-known dividend stocks combine income stability with strategic growth initiatives, making them compelling options for investors navigating potential turbulence in 2026.

Sources: Nathan Reiff