A major Australian pension fund has increased hedging on its international equities, arguing the Australian dollar is undervalued as the Reserve Bank of Australia tightens policy while most major central banks pause or prepare to cut rates.

Jeff Brunton, head of portfolio management at HESTA, which manages A$100 billion in assets, said the fund has raised its exposure to the Australian dollar, citing long-term valuation models that point to persistent undervaluation. By increasing currency hedging, HESTA aims to protect portfolio returns if a stronger Aussie dollar erodes the local-currency value of overseas investments.

The move contrasts with the traditionally low level of currency hedging among Australian investors in U.S. equities, where the U.S. dollar has typically been viewed as a shock absorber. HESTA is the second large fund to adjust its strategy recently, following similar steps by Australian Retirement Trust.

Analysts note that increased Australian dollar buying by pension funds could add upward pressure to the currency, which rose 4.3% last month to a three-year high and has gained nearly another 1% in February. Support has also come from the RBA’s recent 25-basis-point rate hike to 3.85%, strong commodity-driven trade surpluses, and Australia’s yield advantage over other G10 economies.

HESTa currently holds A$23.45 billion in international equities, and Brunton said the fund remains underweight foreign currencies relative to both its long-term targets and its peers.

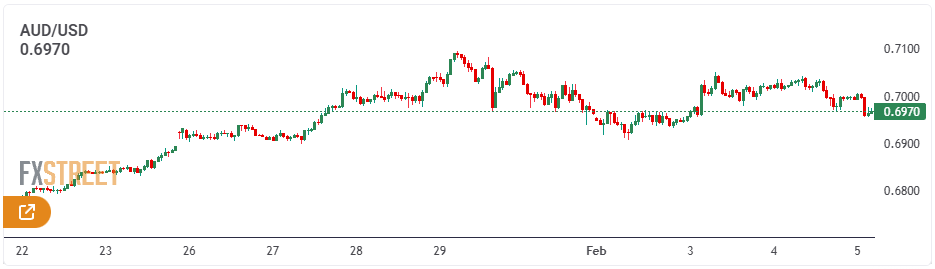

AUD/USD is trading lower below the key 0.7000 psychological level during Thursday’s Asian session, pressured by mixed Australian trade data. The pair is also weighed down by a firm U.S. dollar, which is hovering near a two-week high. With limited domestic catalysts, traders are now turning their attention to the upcoming U.S. JOLTS job openings data for fresh direction.

AUD/USD Technical Outlook

Should bullish momentum intensify, AUD/USD is likely to encounter its next resistance at the 2026 peak of 0.7093 (Jan 29), followed by the 2023 high at 0.7157 (Feb 2).

On the downside, a break below the February low at 0.6908 (Feb 2) may trigger a deeper pullback toward the interim 55-day SMA at 0.6693, ahead of the 2026 trough at 0.6663 (Jan 9). Additional downside support is seen at the 100-day SMA at 0.6628, with stronger support at the 200-day SMA at 0.6563 and the November low at 0.6421 (Nov 21).

Momentum indicators remain constructive and point to further upside potential, although the pair’s overbought readings suggest the risk of a near-term correction. The RSI hovers near 72, while the ADX around 50 continues to signal a strong underlying trend.

Bottom line

AUD/USD continues to be heavily influenced by global risk appetite and developments in China’s economy. A sustained move above the 0.7000 handle would reinforce a more credible bullish outlook.

For the time being, a weaker U.S. dollar, stable—though not particularly strong—domestic data, a still-hawkish tilt from the RBA, and modest backing from China leave the balance of risks skewed toward further upside rather than a pronounced pullback.

Fundamental Analysis

AUD/USD remains entrenched in its broader uptrend despite renewed selling pressure emerging on Wednesday. Any near-term pullbacks are expected to attract buying interest, as the Reserve Bank of Australia continues to project a clearly hawkish stance following its latest rate decision.

The Australian Dollar is struggling to extend Tuesday’s advance, easing back and once again testing the psychologically significant 0.7000 mark.

The retreat comes as the U.S. Dollar regains some traction, with markets having largely absorbed the RBA’s hawkish hike and refocusing attention on U.S. economic and monetary policy developments.

Australia: Growth Is Cooling, Not Collapsing

Recent Australian data have been underwhelming rather than alarming, reinforcing a well-established narrative. Economic activity is slowing, but in a controlled manner, with momentum easing rather than breaking down—supporting the soft-landing view.

January PMI surveys align with this assessment, as both Manufacturing and Services strengthened and remained firmly in expansion territory, at 52.3 and 56.3 respectively. Retail sales continue to show resilience, and although the trade surplus narrowed to A$2.936 billion in November, it remains solidly positive.

Growth is moderating only gradually, following a 0.4% quarter-on-quarter rise in GDP in Q3. On an annual basis, output expanded by 2.1%, matching the RBA’s projections.

The labour market remains a standout performer. Employment jumped by 65.2K in December, while the unemployment rate unexpectedly edged down to 4.1% from 4.3%.

Inflation, however, continues to be the key challenge. December CPI surprised to the upside, with headline inflation accelerating to 3.8% year-on-year from 3.4%. The trimmed mean rose to 3.3%, in line with market expectations but slightly above the RBA’s 3.2% forecast. On a quarterly basis, trimmed mean inflation increased to 3.4% in the year to Q4, marking the highest level since Q3 2024.

China: A Backdrop of Support, Not a Catalyst

China continues to offer a generally supportive backdrop for the Australian dollar, though without the momentum needed to drive a sustained upswing.

Economic growth ran at an annualised 4.5% in the October–December quarter, with quarter-on-quarter expansion at 1.2%. Retail sales rose 0.9% year-on-year in December—respectable, but not particularly compelling.

More recent indicators point to a renewed loss of momentum. Both the NBS Manufacturing PMI and the Non-Manufacturing PMI slipped back into contraction territory in January, at 49.3 and 49.4 respectively.

By contrast, the Caixin surveys painted a slightly brighter picture, with the Manufacturing PMI edging up to 50.3 to remain in expansion, while the Services PMI increased to 52.3.

Trade stood out as a relative bright spot, as the surplus widened sharply to $114.1 billion in December, supported by nearly 7% growth in exports and a solid 5.7% rise in imports.

Inflation signals remain mixed. Consumer prices were unchanged at 0.8% year-on-year in December, while producer prices stayed firmly negative at -1.9%, underscoring that deflationary pressures have yet to fully fade.

For now, the People’s Bank of China is maintaining a cautious stance. Loan Prime Rates were left unchanged in January at 3.00% for the one-year and 3.50% for the five-year, reinforcing expectations that policy support will remain gradual rather than aggressive.

RBA: Leaning Hawkish, In No Hurry to Ease

The RBA raised the cash rate to 3.85% in a decisively hawkish move that largely met expectations. Upward revisions to both growth and inflation forecasts signal firmer economic momentum and increasingly broad-based price pressures. Core inflation is now projected to remain above the 2–3% target band for much of the forecast horizon, reinforcing the case for a restrictive policy stance.

The central message is that inflation is becoming more demand-driven. The RBA cited stronger-than-expected private demand as a key justification for tighter policy, even as productivity growth remains subdued. While Governor Bullock described the move as an “adjustment” rather than the beginning of a renewed hiking cycle, the signal was clear: policymakers are uneasy with the upward drift in inflation.

For markets, this implies interest rates are likely to stay higher for longer, limiting the scope for near-term easing. From an FX perspective, this provides marginal support for the Australian dollar—particularly against low-yielding peers—even as the RBA’s emphasis on full employment tempers the likelihood of an aggressive tightening phase.

In the wake of the decision, markets are now pricing in nearly 40 basis points of additional tightening by year-end.

Positioning: Shifting Sentiment Toward the AUD

The latest positioning data suggest the worst of the bearish sentiment toward the Australian dollar may have passed. CFTC figures show that non-commercial traders have returned to a net long stance for the first time since early December 2024, although the position remains modest at just over 7.1K contracts in the week ending January 27.

Open interest has also climbed to its highest level in several weeks, exceeding 252K contracts, indicating that traders are beginning to re-engage with the market. That said, the move appears tentative rather than a strong conviction call on a sustained appreciation in the AUD, at least for now.

Key Drivers Ahead

Near term: Market attention is shifting back toward the United States. Incoming economic data, tariff-related developments, and ongoing geopolitical headlines are likely to drive movements in the U.S. dollar. For the Australian dollar, the key swing factors remain domestic labour market and inflation data, and how these shape expectations for the RBA’s next policy decision.

Risks: The AUD remains highly sensitive to global risk sentiment. A sharp deterioration in risk appetite, renewed concerns over China’s outlook, or an unexpected resurgence in the U.S. dollar could quickly unwind recent gains.

The Australian Dollar softened even as China’s RatingDog Manufacturing PMI edged up to 50.3 in January from 50.1. Meanwhile, Australia’s TD-MI Inflation climbed 3.6% year over year, though the monthly increase eased to 0.2%, its slowest pace since August. The US Dollar could gain further support after Donald Trump nominated Kevin Warsh as Fed Chair, a move seen as signaling a more cautious stance on monetary easing.

The Australian Dollar weakened against the US Dollar on Monday, extending losses after falling more than 1% in the prior session. The AUD/USD pair stayed under pressure despite China’s RatingDog Manufacturing PMI ticking up to 50.3 in January from 50.1 in December, in line with market expectations. While the reading signaled a modest expansion in factory activity, it marked the strongest growth since October.

Meanwhile, Australia’s TD-MI Inflation Gauge rose to 3.6% year over year in January from 3.5% previously. On a monthly basis, inflation increased by 0.2%, easing sharply from December’s two-year high of 1% and registering its slowest pace since August.

ANZ Job Advertisements surged 4.4% month over month in December 2025, rebounding from a revised 0.8% decline and marking the first increase since July. The rise was also the strongest monthly gain since February 2022, pointing to renewed hiring momentum toward the end of the year.

The data come ahead of the Reserve Bank of Australia’s policy meeting on Tuesday, following the central bank’s decision to keep the cash rate unchanged at 3.6% for a third consecutive meeting in December. Policymakers are widely expected to maintain a cautious stance, as underlying inflation remains above target and labor market conditions stay relatively tight, supporting a restrictive and data-dependent policy approach.

Meanwhile, Australia’s Consumer Price Index increased 3.8% year over year in December, up from 3.4% previously. With headline inflation still exceeding the RBA’s 2–3% target range, recent PMI and employment indicators strengthen the argument for a tighter monetary policy bias.

US Dollar edges lower ahead of ISM Manufacturing PMI

The US Dollar Index (DXY), which tracks the Greenback against six major currencies, is edging lower after posting gains of more than 1% in the previous session, trading near 97.10 at the time of writing. Market attention is turning to the release of the US ISM Manufacturing PMI for January later in the day.

Despite the modest pullback, the US Dollar had recently drawn support following President Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair, a move markets viewed as signaling a more disciplined and cautious approach to monetary easing. The Greenback also benefited from improved risk sentiment after the US Senate reached an agreement to advance a government funding package, averting a potential shutdown, according to Politico.

US producer-side inflation data further underpinned the Dollar, reinforcing the Federal Reserve’s restrictive policy stance. Headline PPI remained unchanged at 3.0% year over year in December, exceeding expectations for a slowdown to 2.7%. Core PPI, which excludes food and energy, accelerated to 3.3% YoY from 3.0%, defying forecasts for a decline to 2.9% and highlighting persistent upstream price pressures.

Federal Reserve officials echoed a cautious tone on easing. St. Louis Fed President Alberto Musalem said additional rate cuts are not justified at present, describing the current 3.50%–3.75% policy rate range as broadly neutral. Atlanta Fed President Raphael Bostic also urged patience, arguing that monetary policy should remain modestly restrictive.

In Australia, inflation and trade data pointed to continued price pressures. The RBA’s Trimmed Mean inflation rose 0.2% month over month and 3.3% year over year, while the monthly CPI jumped 1.0% in December from zero previously, exceeding forecasts of 0.7%. Export prices increased 3.2% quarter over quarter in Q4 2025, rebounding from a 0.9% decline in Q3 and marking the strongest gain in a year, while import prices climbed 0.9%, beating expectations for a fall and reversing a prior decline.

Following the data, markets now price in more than a 70% probability of a 25-basis-point rate hike by the Reserve Bank of Australia from the current 3.6% cash rate, up from around 60% previously. Rates are fully priced at 3.85% by May and near 4.10% by September.

Australian Dollar slides toward key confluence support near 0.6900

The AUD/USD pair is trading near 0.6940 on Monday. Analysis of the daily chart shows the pair continuing to move higher within an ascending channel, pointing to a sustained bullish bias. The 14-day Relative Strength Index has eased from the 70 level to around 67, suggesting a cooling in bullish momentum rather than a trend reversal.

On the upside, AUD/USD could recover toward 0.7093, its highest level since February 2023, reached on January 29. A sustained break above this level would open the door for a test of the channel’s upper boundary near 0.7190. On the downside, initial support is seen at a confluence zone around the nine-day Exponential Moving Average at 0.6927, which aligns closely with the lower boundary of the ascending channel near 0.6920.

AUD/USD hovers near its 16-month high of 0.6940, supported by rising Australian three-year bond yields at 4.27%, while a weaker US Dollar amid political uncertainty and shutdown risks adds to the upside.

AUD/USD is holding near its 16-month high of 0.6940 set in the prior session, trading around 0.6920 during Tuesday’s Asian hours, as markets await Australia’s December CPI data on Wednesday for fresh cues on the RBA’s policy outlook.

The Australian Dollar is underpinned by higher government bond yields, with the policy-sensitive three-year yield climbing to 4.27%, its highest since November 2023, supported by confidence in Australia’s strong credit rating and the RBA’s relatively hawkish stance.

Australia’s strong PMI and employment data have strengthened expectations of tighter RBA policy. While inflation has eased from its 2022 peak, recent figures point to renewed upward pressure, with headline CPI slowing to 3.4% YoY in November but still above the RBA’s 2–3% target range.

AUD/USD may find further support as the US Dollar weakens on rising political uncertainty, with the risk of a partial US government shutdown ahead of the January 30 funding deadline after Senate Democratic leader Chuck Schumer vowed to oppose a key funding bill.

Market caution is also heightened by uncertainty around the Federal Reserve, after President Donald Trump said he would soon name a successor to Fed Chair Jerome Powell, raising speculation over a more dovish policy stance. Attention now turns to Wednesday’s Fed decision.

The Australian Dollar weakens after the trade surplus narrowed to 2,936M MoM in November.

The Australian Dollar weakens after the trade surplus narrowed to 2,936M MoM in November.

The US ISM Services PMI climbed to 54.4 in December, up from 52.6 and above the 52.3 forecast.

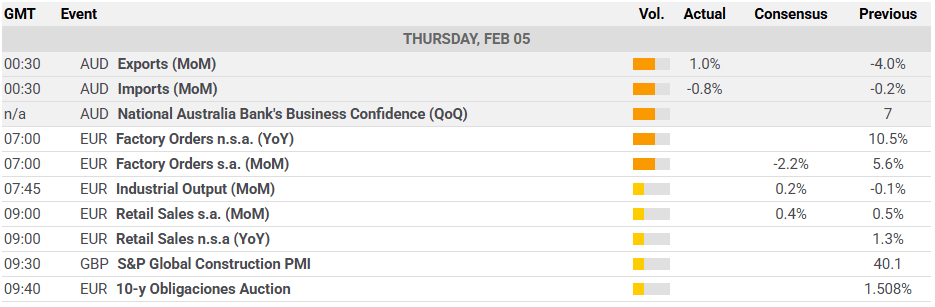

The Australian Dollar (AUD) edges lower against the US Dollar (USD) on Thursday following Australia’s Trade Balance data, which showed that the trade surplus narrowed to 2,936M MoM in November versus 4,353M (revised from 4,385M) in the previous reading.

The Australian Bureau of Statistics (ABS) reported on Thursday that Exports fell by 2.9% MoM in November from a rise of 2.8% (revised from 3.4%) seen a month earlier. Meanwhile, Imports grew by 0.2% MoM in November, compared to a rise of 2.4% (revised from 2.0%) seen in October.

Australia’s mixed November Consumer Price Index (CPI) has left the Reserve Bank of Australia’s (RBA) policy path unclear, shifting attention to the quarterly CPI release later this month for stronger direction.

RBA Deputy Governor Andrew Hauser commented Thursday that November’s inflation figures were broadly in line with expectations, and noted that rate cuts are unlikely in the near term.

Data from the Australian Bureau of Statistics (ABS) on Wednesday showed annual inflation easing to 3.4% in November from 3.8% in October. The figure came in below the 3.7% forecast but remained above the RBA’s 2–3% target band. It was the lowest print since August, with housing costs rising at their weakest pace in three months.

US Dollar steadies amid market caution

The US Dollar Index (DXY), which tracks the Greenback against six major peers, is holding steady near 98.70 at the time of writing.

The Dollar is firm as soft recent data highlights a fragile US economy ahead of Friday’s pivotal jobs release, keeping sentiment subdued.

Traders are watching Thursday’s Initial Jobless Claims data, with focus shifting to Friday’s Nonfarm Payrolls report, expected to show a slowdown to 55,000 new jobs in December from 64,000 in November.

The ISM reported Wednesday that the US Services PMI strengthened to 54.4 in December from 52.6, beating forecasts of 52.3.

ADP data showed private payrolls increased by 41,000 in December, following a revised drop of 29,000 in November and slightly below the 47,000 consensus.

Fed Governor Stephen Miran said Tuesday the Federal Reserve may need to cut rates aggressively this year to sustain economic momentum, while Minneapolis Fed President Neel Kashkari cautioned that unemployment could “pop” higher.

Richmond Fed President Tom Barkin, who is not voting on policy this year, said Tuesday that rate adjustments will need to be carefully calibrated to incoming data, highlighting risks to both inflation and employment, per Reuters.

CME FedWatch pricing suggests an 88.9% chance the Fed will leave rates unchanged at its January 27–28 meeting.

China’s RatingDog Services PMI slipped to 52.0 in December from 52.1, while last week’s Manufacturing PMI ticked up to 50.1 from 49.9. Shifts in the Chinese economy are closely watched due to Australia’s deep trade ties with China.

November CPI in Australia was flat month-on-month, matching October. The RBA’s Trimmed Mean rose 0.3% MoM and 3.2% YoY. Seasonally adjusted Building Permits surged 15.2% MoM to nearly four-year highs of 18,406 units, rebounding sharply from October’s revised 6.1% drop. Annual permits climbed 20.2%, overturning a revised 1.1% decline.

The Australian Financial Review reported that the RBA may still have tightening ahead, with economists expecting sticky inflation and penciling in at least two further rate hikes.

The Australian Dollar is holding close to 0.6700 after retreating from its 15-month peak, with AUD/USD trading near 0.6720 on Thursday

Daily chart signals show the pair staying inside an ascending channel, maintaining a bullish structure. The 14-day RSI at 64.42 reinforces positive momentum.

On the upside, AUD/USD could retest 0.6766 — its highest level since October 2024 — and possibly climb toward the channel’s upper boundary near 0.6840.

Initial support is located around 0.6720 at the channel’s lower boundary, followed by the nine-day EMA at 0.6706. A break beneath that confluence area could expose downside toward the 50-day EMA at 0.6626.