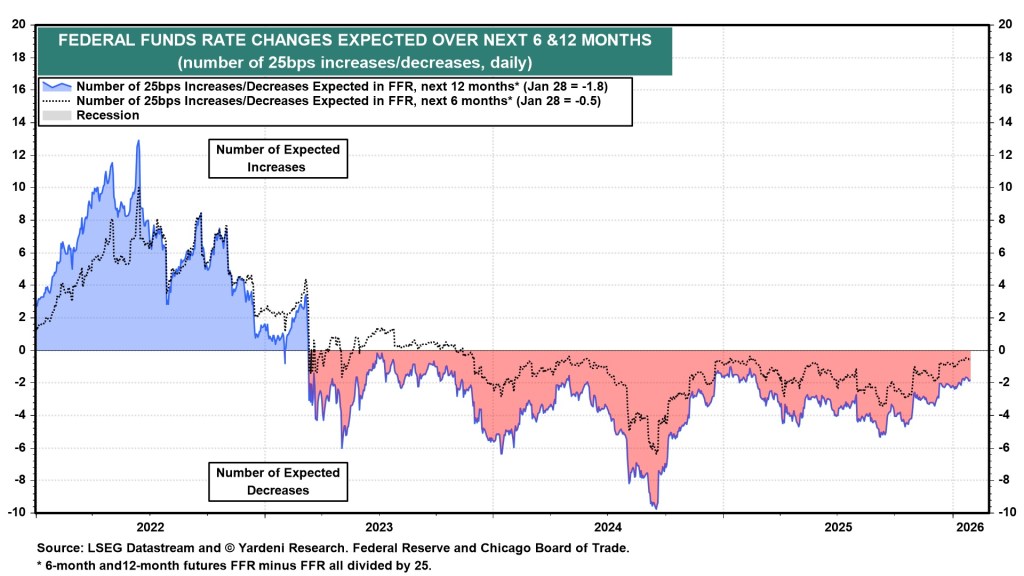

Austan Goolsbee said in a Friday interview with Yahoo Finance that while interest rates are likely to decline further, any additional cuts will depend on continued progress in bringing down services inflation.

He described the latest CPI report as mixed, with both positive signals and lingering concerns, noting that services inflation remains elevated and above target. Goolsbee expressed hope that the peak effects of tariffs have passed and pointed to strong January employment data as evidence of a broadly stable labor market with only modest cooling. Although he believes rates could be reduced further, he stressed the need for clearer improvement in inflation before accelerating cuts, warning that persistently high services inflation is a risk.

He added that the U.S. consumer remains the economy’s strongest pillar and should stay resilient if the job market holds steady and inflation eases. If inflation returns to 2%, he said, the Fed would have room to implement several more rate cuts.

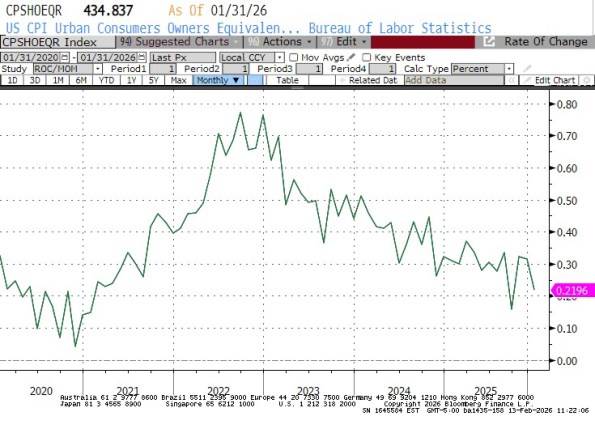

A few months ago, a government shutdown led to a missed CPI release because the Bureau of Labor Statistics (BLS) lacked sufficient data to calculate the October 2025 figure. The bigger issue, however, was methodological: when compiling the November index, the BLS was effectively required to assume that prices in several major categories—especially rents—were unchanged in October. This created an artificial drop in year-over-year inflation.

While some of that distortion has already begun to reverse, a more significant rebound is expected in a few months when the Owners’ Equivalent Rent (OER) survey rotation triggers a sharp offsetting increase—precisely six months after the initial dip. Until that adjustment plays out, inflation data will remain hard to interpret, and the annual comparisons will understate true price pressures. So claims that the latest report shows the smallest yearly increase in core inflation since 2021, suggesting the Federal Reserve is near its target, are misleading.

In reality, core year-over-year inflation is roughly 0.25%–0.3% higher than reported. Markets for CPI fixings already anticipate headline inflation rising to about 2.82% in four months—not because of energy prices, but due to this statistical catch-up.

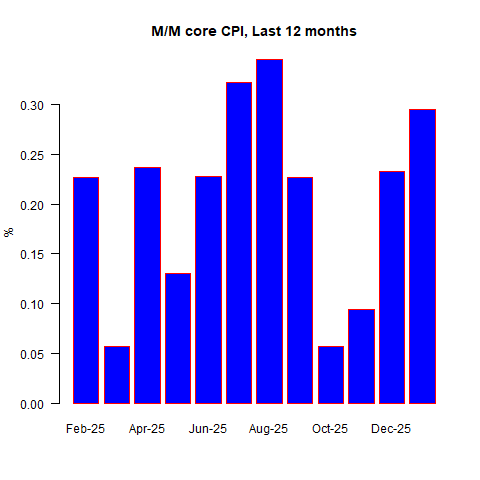

January is typically a challenging month for inflation data anyway, as businesses often offer discounts in December before implementing annual price hikes in January. Because these adjustments are irregular, they are difficult to seasonally adjust, making January surprises common. This time, consensus forecasts called for a 0.27% month-over-month rise in headline CPI and 0.31% in core, with some estimates—such as from Barclays—as high as 0.39% for core. Much of the speculation centered on whether remaining tariff-related price increases would be passed through at the start of the year. Ultimately, they were not. The actual figures came in at +0.17% for headline and +0.30% for core.

The weaker headline reading was largely due to gasoline pricing dynamics. Although gas prices increased over the course of January, the monthly average was still lower than December’s average, because prices had fallen sharply in December. Since the BLS calculates CPI based on average monthly prices rather than end-of-month levels, this produced a softer headline figure.

Core inflation, meanwhile, appeared close to target at first glance: the 2.5% year-over-year rate is the lowest since March 2021. Yet the 0.30% monthly increase was the third-highest in the past year and translates to an annualized pace of 3.6%. That hardly signals a smooth return to 2% inflation—raising questions about whether it is truly “mission accomplished” for the Fed.

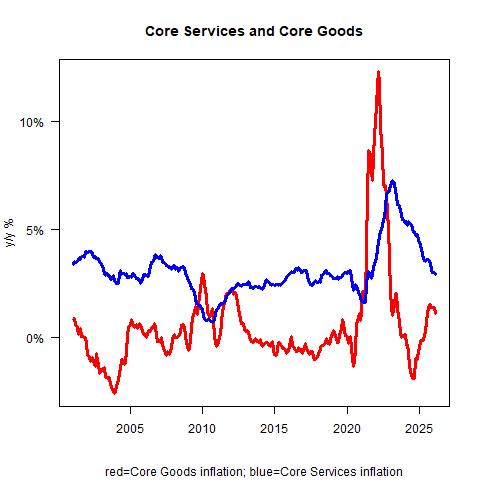

Core inflation was also somewhat flattered by a sharp 1.84% month-over-month decline in used car prices. In reality, used car prices did rise in January, but by less than the typical seasonal pattern, which translated into a sizable seasonally adjusted drop and created a noticeable drag on the core figure. (That said, it’s important not to dismiss components simply because they don’t align with the broader narrative.) Overall, core goods inflation slowed to 1.1% year over year from 1.4%, while core services edged down to 2.9% from 3.0%.

Although core goods inflation declined more than expected due to the sharp move in used cars, some moderation isn’t surprising. The real issue isn’t whether core goods will reaccelerate to 3–4%, but whether it remains in positive territory or slips back into the persistent deflation that characterized the sector for many years. That distinction matters, even if core goods make up only about 20% of the CPI basket. Until recently, the narrative centered on tariffs; going forward, it may shift toward onshoring. The decades-long trend of goods deflation—driven by offshoring production to low-wage countries—may not reassert itself if manufacturing activity continues to migrate back. That’s the broader theme to monitor, though it’s not the main takeaway from January 2026’s data.

On autos specifically, new car prices posted a modest increase. It’s worth considering how changes in sales composition might evolve now that electric vehicles are no longer being actively promoted by the executive branch. Traditional gasoline-powered cars tend to be cheaper upfront, so if buyers shift back toward them—absent tax incentives for EVs—the average transaction price could decline. However, it’s unclear how significantly overall sales patterns will change, or how production strategies will adjust now that automakers may feel less pressure to meet EV quotas. It’s also uncertain how granular the Bureau of Labor Statistics survey is in accounting for shifts in fleet composition. If there is any measurable impact on CPI, it would likely be slightly negative—and probably modest in size.

As for rents, Owners’ Equivalent Rent (OER) rose 0.22% month over month, down from 0.31% previously, while Rent of Primary Residence increased 0.25%, slightly below last month’s 0.27%. The month-to-month trend in OER shows a clear deceleration—though notably, it omits the artificial zero recorded in October due to the earlier data disruption.

While the slowdown is evident, my model suggests the pace should now be stabilizing around this level rather than continuing to decline sharply. In other words, rents are cooling, but likely nearing a plateau. That isn’t the defining story of January 2026—but it may well become one of the central inflation themes for the rest of 2026.

Medicinal drug prices slipped 0.15% month over month. Some observers had anticipated a much larger decline, partly due to efforts by the Trump Administration to push manufacturers to align U.S. drug prices more closely with those abroad. So far, however, no clear downward trend is evident. A potentially more consequential development is the Trump RX initiative, aimed at increasing pricing transparency and reducing the role of intermediaries in the highly opaque pharmaceutical distribution chain—long dominated by three major wholesalers and three large pharmacy benefit managers.

If successful, it could meaningfully reduce out-of-pocket drug costs for consumers. That said, when medications are paid for by insurers rather than directly by households, the impact does not show up straightforwardly in the CPI, appearing only indirectly—an accounting nuance that complicates interpretation. In short, consumer drug prices may decline, but the timing and visibility of that effect in CPI data remain uncertain.

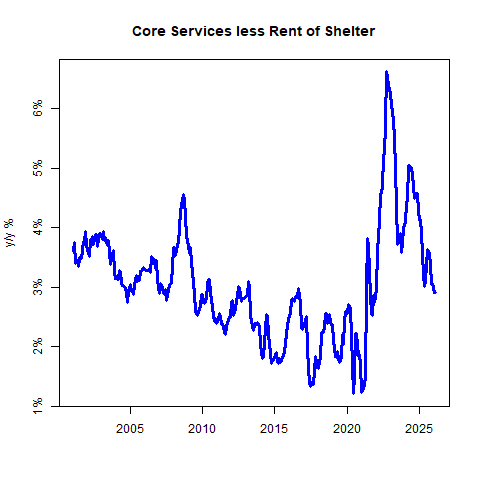

The most encouraging element of the report was the continued slowdown in core services excluding rents—often referred to as “supercore” inflation—which eased further even as airfares jumped 6.5% on the month.

Gotcha. The apparent improvement in “supercore” inflation is another illusion created by the missing October data, which flatters the year-over-year comparison. On a month-over-month basis, core services ex-rents actually surged 0.59% (seasonally adjusted)—the largest increase in a year.

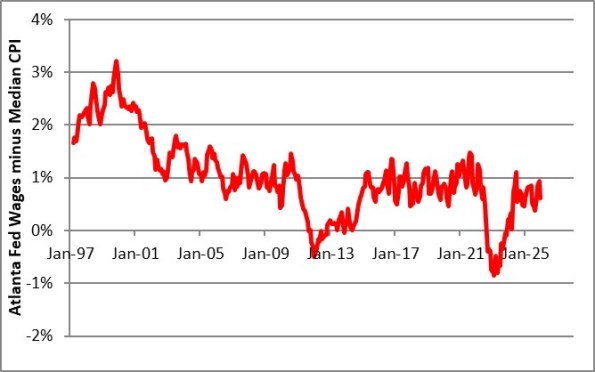

Even so, the broader trend may still be one of gradual cooling, particularly as median wage growth continues to decelerate. Admittedly, that data is also somewhat noisy at the moment. Still, the gap between median wage growth and median inflation remains around 1%, suggesting real income growth is positive, even if inflation progress is bumpier than headline figures imply.

There are tentative signs that wage growth’s downward drift may be stabilizing. If so, that would naturally limit how quickly supercore inflation can cool. At the same time, brewing cost pressures in insurance markets are likely to surface over the next six months. Still, none of that defines January 2026.

The real story this month is that inflation data remain clouded by the government-shutdown gap. The missing October observations continue to flatter year-over-year comparisons, overstating the degree of progress. That statistical quirk makes it easier for the Administration to claim victory, even though underlying inflation does not appear to be cleanly converging back to target.

Assuming the Federal Reserve recognizes these distortions, the policy outlook seems relatively straightforward. Core inflation—abstracting from the shutdown gap—appears to be running near 3.5%, labor market data have surprised to the upside, and the current Fed leadership has shown little inclination to accommodate political pressure. Under those conditions, there is scant reason to expect a near-term adjustment in overnight rates; if anything, the argument for tightening may be stronger than for easing.

To be fair, rents continue to decelerate even after adjusting for the October distortion, though my model suggests that slowdown is unlikely to persist much further. Even if it does, a return to outright housing deflation seems improbable. Moderation in supercore inflation is encouraging, but probably insufficient to deliver the degree of cooling the Fed would require. Core goods inflation also looks to have peaked; the open question is whether it settles into low positive territory or slips back into deflation.

Taken together, my modeling suggests that median inflation around 3.5% (excluding the shutdown effect) may represent something close to a new equilibrium. It’s not unreasonable to see constructive signals in the recent data, but neither do they justify expectations of imminent easing. If disinflation trends persist and leadership dynamics shift—potentially with someone like Kevin Warsh assuming the chair—the door to rate cuts later in the year could open.

Asian equities retreated on Friday, following a decline in U.S. technology stocks overnight as fresh concerns about stretched artificial intelligence valuations weighed on investor sentiment. Despite the pullback, regional markets remained on track for solid weekly gains after a strong rally earlier in the week fueled by AI enthusiasm and upbeat corporate earnings.

On Nasdaq Composite, shares fell as investors reassessed elevated AI-related valuations, pressuring semiconductor and growth stocks across Asia. Meanwhile, U.S. stock index futures were mostly flat by late evening trading (22:04 ET / 03:04 GMT).

KOSPI climbed to a new all-time high and is on track to post a weekly gain of about 9%.

In South Korea, the KOSPI rose 0.5% to a fresh record of 5,558.82, bucking the broader regional weakness and heading for an impressive weekly gain of nearly 9%, driven by major chipmakers. Samsung Electronics climbed almost 15% this week on optimism surrounding its HBM4 high-bandwidth memory rollout and expanding edge AI prospects, while SK Hynix was poised for a roughly 6% weekly advance.

Japan’s Nikkei 225 slipped 0.7% after reaching record highs above 58,000 in the prior session but remained on course for a weekly rise of about 6%, supported by renewed trade optimism following the election victory of Sanae Takaichi. The broader TOPIX fell 1% on Friday, though it was still set for a weekly gain of around 4%.

Australian shares were poised for a weekly advance, supported by strong earnings from major banks.

Elsewhere, Australia’s S&P/ASX 200 dropped 1.3% on the day but remained on track for a 3% weekly increase, supported by strong bank earnings. Singapore’s Straits Times Index fell 1%, while futures linked to India’s Nifty 50 were little changed.

Hong Kong’s Hang Seng Index declined 2% on Friday and was poised to finish the week flat, diverging from the broader regional trend. In mainland China, the CSI 300 slipped 0.5% and the Shanghai Composite fell 0.7%, though both were still set for modest weekly gains of around 1%.

Investors were also looking ahead to upcoming U.S. consumer price index data for further guidance on the Federal Reserve’s rate outlook, after stronger-than-expected U.S. employment figures earlier in the week reduced expectations for near-term interest rate cuts.

Standard Chartered analysts Steve Englander and Dan Pan note that the latest US Nonfarm Payrolls report delivered a stronger-than-expected rebound in hiring, with job growth accelerating and the unemployment rate declining.

Although substantial downward benchmark revisions were made to prior data, they believe the latest figures signal a gradual labour-market recovery extending into 2025 and 2026.

NFP strength suggests continued stabilization

The January employment report surprised to the upside, exceeding nearly all forecasts and indicating renewed momentum in the labour market.

Faster job creation, a lower unemployment rate, and a rise in the employment-to-population ratio all point to improving labour conditions toward late 2025 and into 2026, despite significant downward revisions to historical data.

While health care and social assistance remained the primary contributors to job growth, other sectors are beginning to show early signs of recovery.

That said, uncertainties remain regarding the durability of this improvement. The analysts caution that one month of stronger data is not enough to eliminate broader labour-market concerns, particularly amid weak sentiment indicators and potential disruptions related to artificial intelligence.

Commerzbank’s Antje Praefcke suggests that the delayed January U.S. jobs report is unlikely to significantly move the Dollar, with Nonfarm Payrolls projected at about 70,000 and the unemployment rate holding at 4.4%. She notes that investors are likely to pay closer attention to the outlook for Federal Reserve policy under Kevin Warsh and to ongoing concerns about the Fed’s independence, which she views as the main medium-term risk facing the Dollar.

Employment report takes a back seat to Fed-related risks

“I’m not convinced this will trigger any significant moves in the US dollar, for two reasons.”

“In that context, a reading of roughly 70,000 – or even 60,000 – should not unsettle markets, as it would still point to a labor market that is softening but not collapsing. As such, there is little justification for making substantial changes to interest rate expectations tied to the Fed’s employment mandate.”

“While key data releases will likely continue to drive short-term swings in the dollar, the overriding issue remains the Fed’s independence, which is effectively the sword of Damocles hanging over the currency.”

“Ultimately, the future independence of the Fed is the central question and the greatest risk for the greenback. Clarity on this matter is unlikely before spring.”

The U.S. House of Representatives on Tuesday narrowly defeated a push by Republican leaders to prevent lawmakers from challenging President Donald Trump’s tariffs, voting 217-214. The outcome could allow Democrats to move forward with efforts to overturn the trade measures.

Three Republicans sided with all 214 Democrats in opposing the proposal, which sought to bar any tariff-related challenges until July 31. The restriction had been folded into a procedural resolution meant to advance debate on three separate, unrelated bills.

The setback marks a notable blow to House Speaker Mike Johnson, who oversees a razor-thin 218-214 Republican majority, leaving virtually no margin for dissent on party-line votes. With Democrats united in opposition, Johnson can afford to lose no more than one Republican on any given measure.

In the wake of the vote, Democrats could push for a House vote as soon as Wednesday to end Trump’s reliance on a national security emergency declaration to justify tariffs on Canada and other key U.S. allies. They have also drafted additional resolutions aimed at blocking tariffs on Mexico and several other nations.

Republicans had enforced procedural rules since March of last year to shield the tariffs from legislative challenges, extending them through January. However, the latest extension lapsed amid internal GOP resistance, as some members raised concerns about the economic burden on American households and businesses reliant on global trade.

The vote came as Supreme Court Justice Ketanji Brown Jackson signaled that the Court will need additional time to rule on the legality of Trump’s tariff policies.

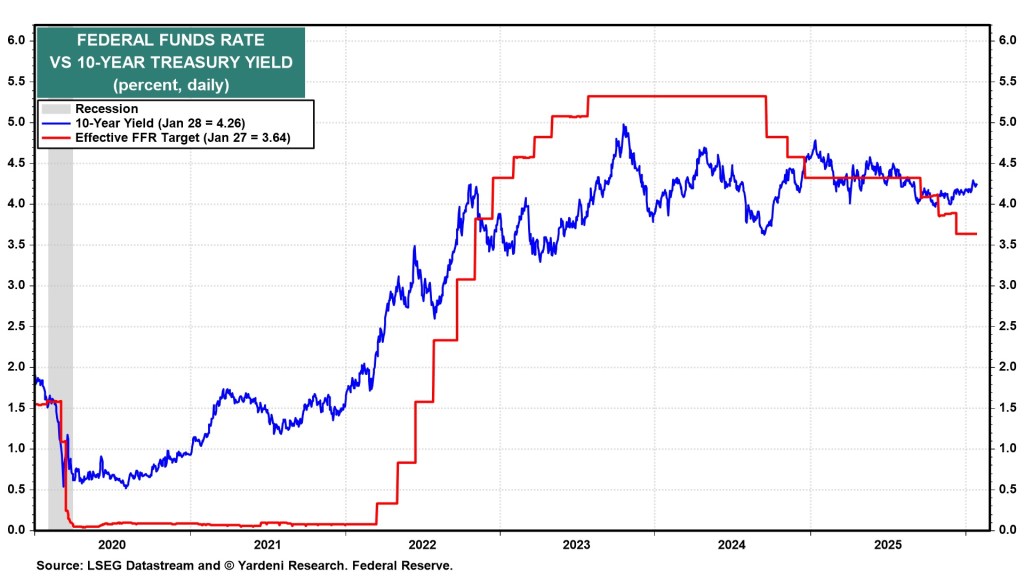

It has become increasingly clear that Treasury Secretary Scott Bessent favored Kevin Warsh for the role. Warsh has advocated for tighter coordination between the Federal Reserve and the Treasury Department, particularly in managing the yield curve and conducting open market operations. The Treasury yield curve is currently at its steepest level in four years, suggesting that Bessent has been effective in resolving the inversion that occurred under his predecessor, Janet Yellen. If Warsh is confirmed as the next Fed Chair, Bessent’s influence is likely to grow further—an important factor if the Fed aims to reduce interest rates.

According to the Financial Times, some economists question Warsh’s belief that artificial intelligence will have a deflationary effect. Warsh argues that AI will spark “the most productivity-enhancing wave of our lifetimes—past, present and future,” boosting output and allowing the Fed to lower key rates without fueling inflation. Such remarks are expected to draw significant attention during his Senate confirmation hearing.

On Tuesday, the Commerce Department reported that retail sales were flat in December. However, November’s figures were revised upward to a 0.6% increase, up from the previously reported 0.3%. Economists had anticipated a 0.4% rise in December, making the latest data disappointing. Because of the federal government shutdown, the report was released a month late, and the substantial upward revision to November’s data has somewhat diminished the report’s impact. Following the release, Treasury yields fell, increasing the likelihood of another Fed rate cut.

Meanwhile, after a month-long pursuit, the U.S. Navy seized its eighth Venezuelan crude oil tanker in the Indian Ocean. The vessel, Aquila II, had attempted to bypass the U.S. blockade. The Navy’s intensified crackdown on so-called “shadow tankers” is expected to worry countries like Iran and Russia, which have also relied on similar methods to transport oil despite sanctions.

In diplomatic developments, U.S. and Iranian officials met in Oman to discuss dismantling Iran’s nuclear program. Washington is pressing Tehran to halt uranium enrichment, limit its ballistic missile program, and end support for regional proxy groups. Iran, however, has stated it is only willing to negotiate over its nuclear activities. If talks collapse, the U.S. could carry out another military strike, which explains its significant naval buildup in the region. Notably, Iran seized two oil tankers before the negotiations but later described the discussions as “positive.”

U.S. President Donald Trump said Monday he would immediately seek talks with Canada to secure compensation for a bridge under construction between Ontario and Michigan, insisting the U.S. should own at least 50% of it. In a Truth Social post, Trump claimed the project moved forward without U.S. approval and accused the Obama administration of allowing Canada to bypass “Buy American” requirements. He also criticized Canada’s efforts to expand trade with China, making unsubstantiated remarks in the process.

Canada’s Chamber of Commerce warned that threatening to block bridges would be counterproductive, noting that the Trump administration itself had backed the project as a priority in 2017. The Gordie Howe International Bridge, funded entirely by the Canadian government at an estimated cost of C$6.4 billion, is being built by the Windsor-Detroit Bridge Authority and is expected to open in early 2026. Trump’s comments come as U.S.–Canada relations remain strained amid trade tensions and Canada’s pivot toward China.

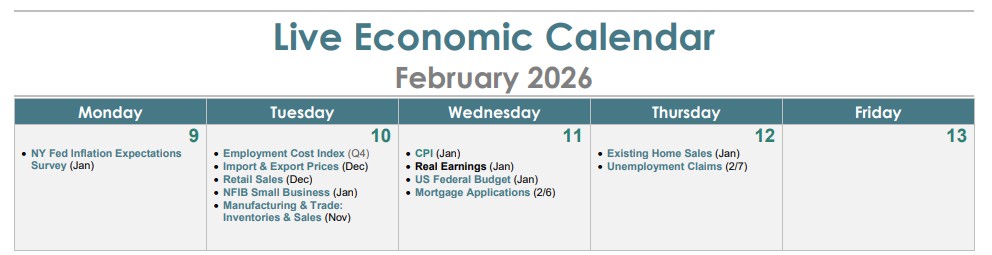

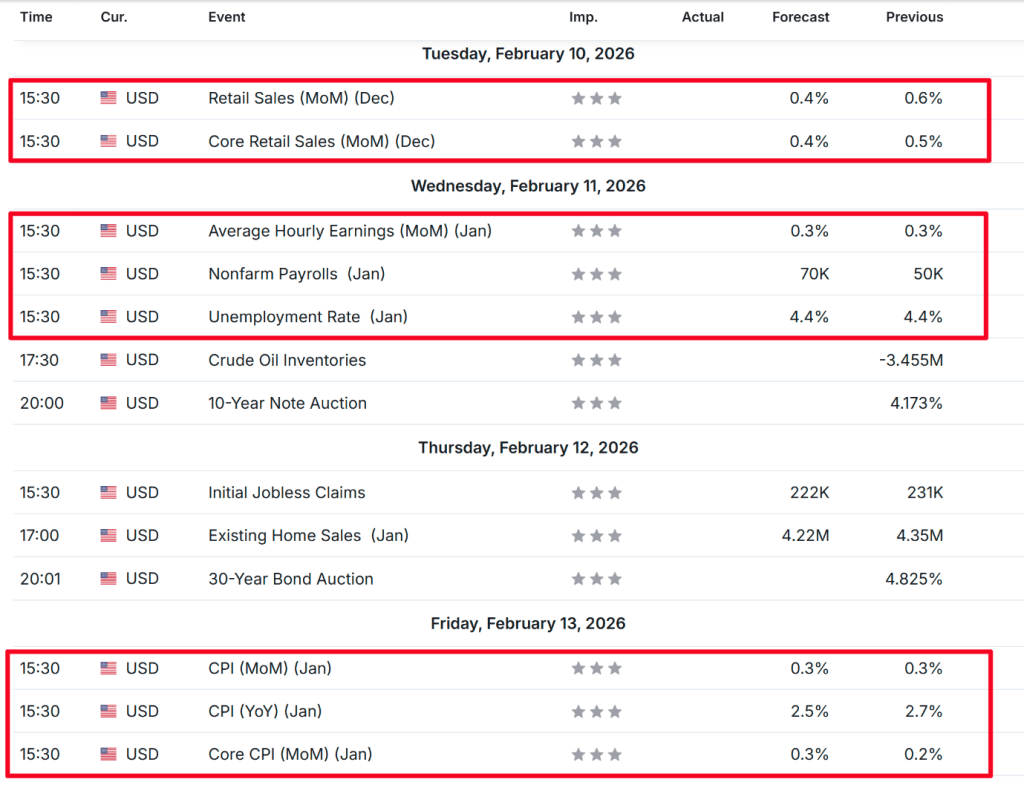

As a polar vortex brings arctic conditions across the U.S., the economic calendar is set to heat up. The week ahead features two of the most consequential data releases for shaping Federal Reserve policy expectations: the January employment report and the Consumer Price Index (CPI).

Owing to recent government shutdowns, the January employment report (Wednesday) and CPI release (Friday) will be published unusually close together. The labor report is particularly significant, as January data typically incorporates annual revisions to employment figures, raising the possibility of notable downward adjustments for the year through March 2025.

A key reference point will be the Federal Reserve’s own assessment of potential overstatement in jobs growth. In December, Fed Chair Jerome Powell noted that internal research suggested official figures may have overstated monthly job gains by as much as 60,000 since April. Given that reported job growth averaged just under 40,000 per month over that span, the scope of upcoming revisions could have meaningful implications for the FOMC’s March policy decision.

The week also features remarks from several Fed officials, including Governors Christopher Waller (Monday), Stephen Miran (Monday and Thursday), and Michelle Bowman (Wednesday). Among voting Fed presidents this year, Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan are both scheduled to speak on Tuesday.

Markets will also be watching price action on Wall Street following last week’s record close for the Dow Jones Industrial Average above 50,000. The ongoing AI-led shakeout among major technology stocks bears close scrutiny, as does the renewed “old economy” rotation bringing previously sidelined sectors—such as oil and gas, chemicals, transportation, and regional banks—back into focus. Adding to the cross-currents is gold’s continued rally, occurring alongside a sharp pullback in bitcoin.

The following data releases carry the greatest potential to move markets and shape the Federal Reserve’s assessment of whether further rate cuts are warranted:

Employment

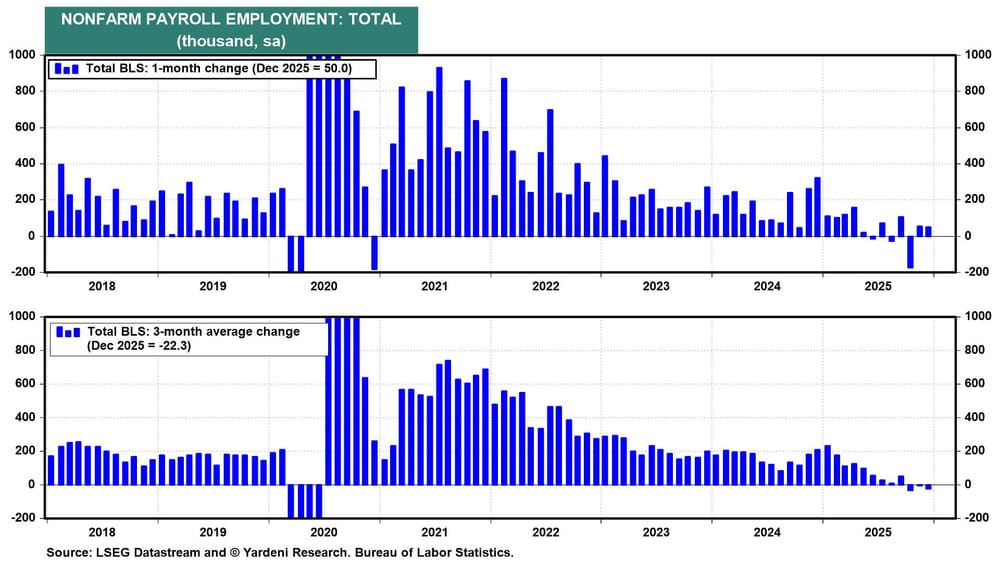

We expect nonfarm payrolls to rise by 60,000 in January, following a 50,000 increase in December (see chart). Markets will be closely focused on the size and direction of revisions to prior data. A meaningful downside surprise could increase pressure on Chair Powell to consider a rate cut later this month, even though we do not believe monetary policy can directly address the underlying weaknesses in the labor market.

CPI

Markets are seeking further confirmation that inflation continued to ease in January. December’s 2.6% year-over-year reading matched a four-year low in core CPI inflation (see chart). The Cleveland Fed’s Inflation Nowcasting model currently projects a 0.22% month-over-month increase in core inflation, translating to a 2.45% annual rate. Additional insight on inflation pressures will come from the Q4 2025 Employment Cost Index and December import and export prices, both due Tuesday, as well as the New York Fed’s January inflation expectations survey on Monday.

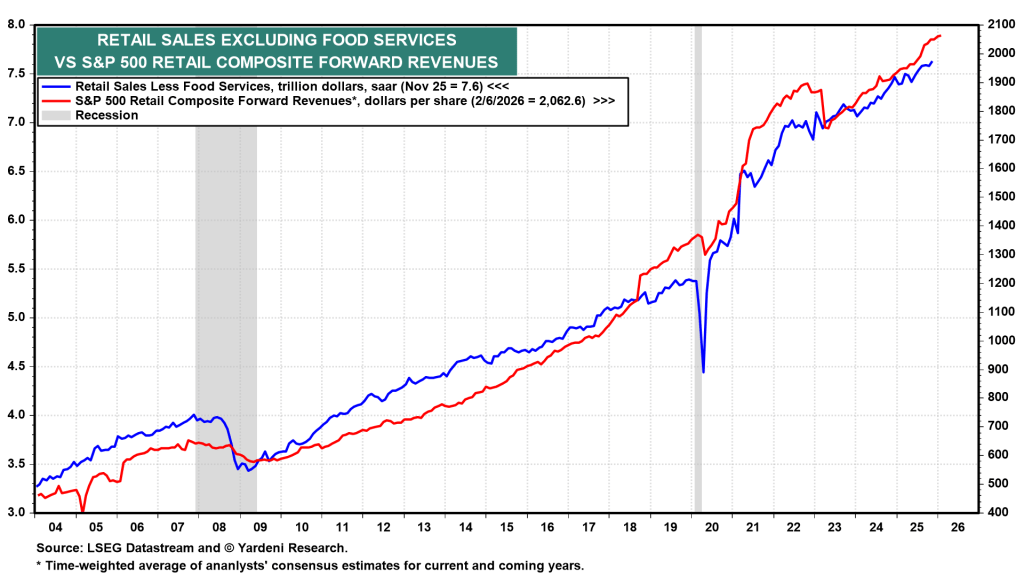

Retail sales

Despite ongoing concerns about the cost of living and a fragile labor market, household spending continues to show resilience. Retail sales in December, due Tuesday, are expected to post another solid gain following November’s 0.6% month-over-month increase. Looking ahead, larger annual tax refunds should help sustain consumer spending momentum. Reflecting this strength, forward earnings for the S&P 500 Retail Composite climbed to a record high during the week of February 6 (see chart).

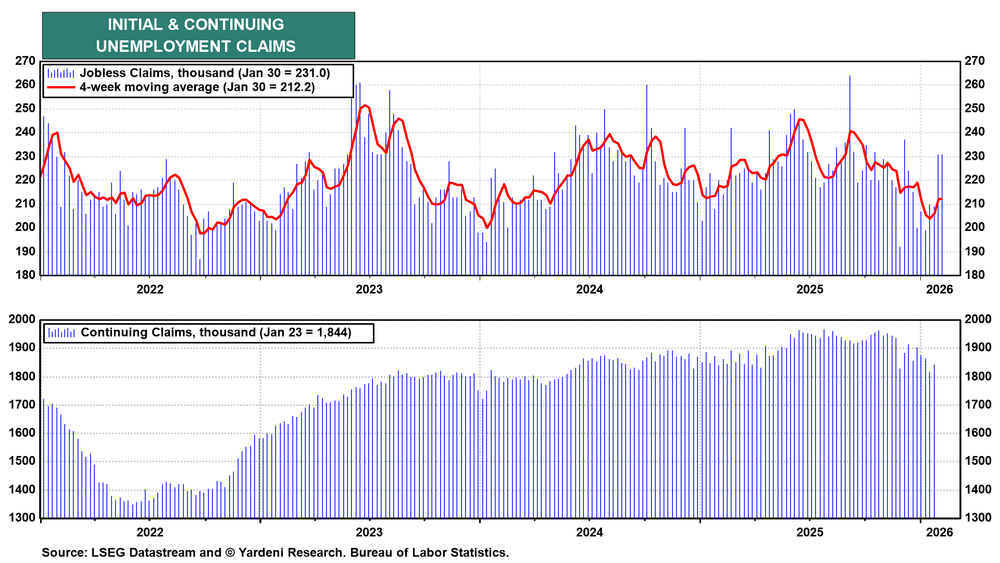

Jobless claims

Initial jobless claims due Thursday will draw heightened scrutiny as investors look to determine whether last week’s jump to 231,000 was driven by severe winter storms rather than a broader acceleration in layoffs. The balance of evidence points to a weather-related distortion, which would likely reassure the Fed that the labor market remains on relatively stable footing.

Key U.S. economic data—including the jobs report, CPI inflation, retail sales—and another round of corporate earnings will be in focus this week.

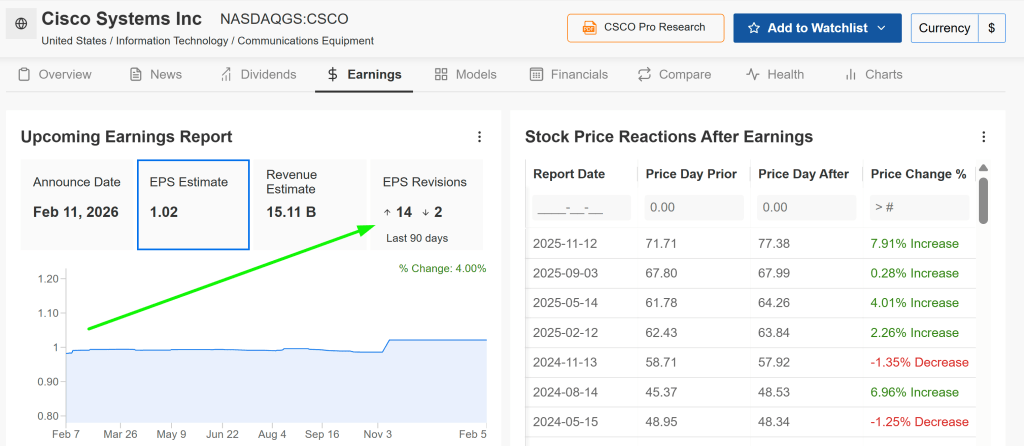

Cisco is expected to post strong earnings along with upbeat guidance, positioning the stock as a high-conviction potential outperformer in the near term.

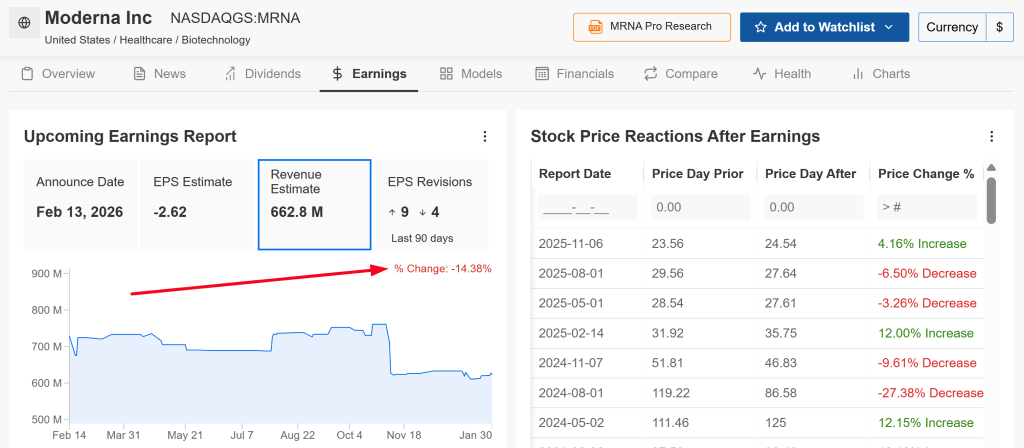

By contrast, Moderna faces pressure from declining revenue and anticipated losses, leaving the stock vulnerable to downside risk this week.

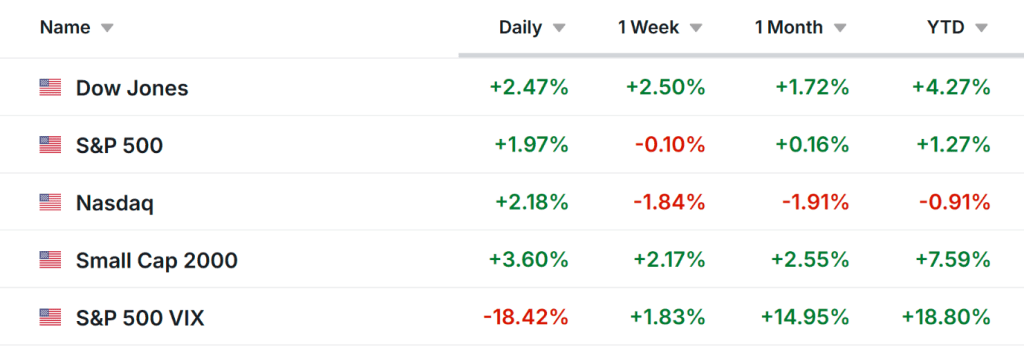

Wall Street stocks surged on Friday, posting their strongest gains in months as the Dow Jones Industrial Average finished above the landmark 50,000 level for the first time.

The rally came after three consecutive sessions of declines driven by artificial intelligence-related concerns, with software stocks particularly pressured on fears that AI could intensify competition across the sector.

For the week, the benchmark S&P 500 and the tech-heavy Nasdaq Composite edged lower by 0.1% and 1.8%, respectively, while the 30-stock Dow Jones Industrial Average gained 2.5% and the small-cap Russell 2000 advanced 1.8%.

Volatility may remain elevated in the days ahead as investors weigh the outlook for economic growth, inflation, interest rates, and corporate earnings.

On the economic front, delayed December retail sales data is set for release on Tuesday. However, Wednesday’s postponed January U.S. jobs report could prove more influential amid mounting concerns over labor-market conditions. January CPI inflation data due on Friday will also be closely watched for further evidence on whether price pressures are truly easing.

Earnings season also rolls on, with a busy slate of high-profile results due in the coming days. Notable reports include Coca-Cola, McDonald’s, Ford, Cisco, Robinhood, Coinbase, and Arista Networks, alongside key software names such as AppLovin, Shopify, and Datadog.

Regardless of broader market direction, below I highlight one stock that is likely to attract buying interest and another that could face renewed downside pressure. Note that this view is strictly short term, covering the week ahead from Monday, February 9 through Friday, February 13.

Stock To Buy: Cisco

Cisco’s upcoming earnings report is the key catalyst for the stock this week, with the risk–reward profile appearing skewed to the upside. CSCO is set to report fiscal second-quarter results after the market closes on Wednesday at 4:05 p.m. ET.

Market expectations remain relatively modest, suggesting that even a small beat on revenue and earnings per share, coupled with steady or slightly optimistic guidance, could be enough to spark a post-earnings rally.

Analyst sentiment has been notably constructive heading into the release. According to InvestingPro data, 14 of the last 16 EPS revisions have been upward, underscoring growing confidence in Cisco’s ongoing expansion.

As a leading player in networking hardware, cybersecurity, and an increasingly important provider of AI infrastructure, Cisco is well positioned to capitalize on multiple tailwinds that could support a strong quarterly performance despite a mixed macroeconomic backdrop.

Consensus forecasts call for adjusted earnings per share of $1.02, representing a 9% increase from a year earlier. Revenue is expected to rise 8% year over year to $15.1 billion, supported by AI-driven demand and solid product sales.

Analysts see potential for longer-term upside from Cisco’s partnership with Nvidia to develop AI networking solutions for the enterprise market. Meanwhile, Cisco’s security segment underperformed in fiscal first quarter results despite the acquisition of Splunk, and investors will be watching closely for signs of a rebound in that business.

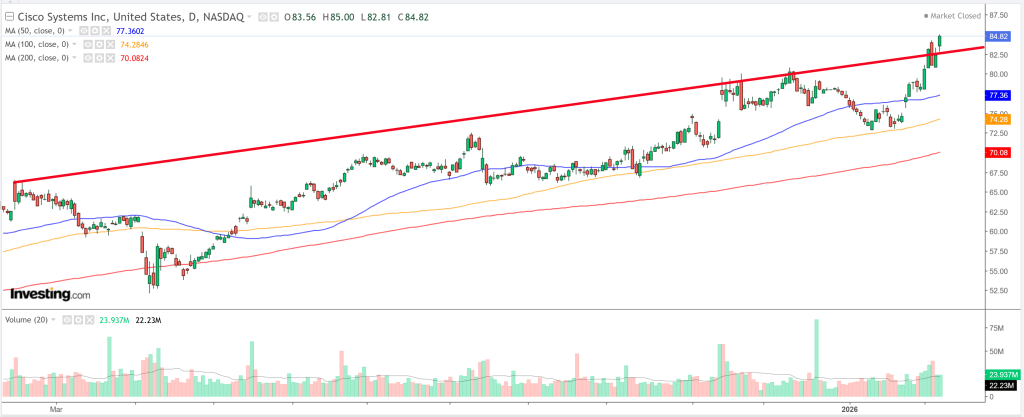

Cisco’s shares have been on a strong run, notching a string of fresh 52-week highs in recent sessions. The stock closed at $84.82 on Friday, underscoring solid momentum heading into the earnings release.

Valuation and sentiment also remain supportive. Cisco continues to trade at a reasonable earnings multiple relative to both the broader technology sector and its own historical averages, while offering an appealing dividend yield underpinned by robust free cash flow.

Trade setup:

Entry: Near current levels (~$84–85)

Target: $90–$95 (potential upside of ~5.8%–10.8%)

Stop-loss: $80 (downside risk of ~5.8%)

Stock To Sell: Moderna

Moderna, meanwhile, faces a tougher setup this week as it heads into its fourth-quarter earnings release scheduled for before Friday’s opening bell at 6:35 a.m. ET. Options markets are pricing in a sharp post-earnings swing of around ±16%, underscoring the heightened risk of a downside surprise.

After its blockbuster pandemic-era success with the mRNA COVID-19 vaccine, the biotech company has struggled with the transition from reliance on a single product to a broader—yet still largely unproven—development pipeline.

Analyst sentiment has turned increasingly cautious ahead of the report, with consensus sales estimates cut by roughly 14%, reflecting growing concerns over Moderna’s near-term revenue outlook.

Consensus expectations point to a sizable loss, with earnings per share projected at around –$2.62 on revenue of $662.8 million, representing a steep year-over-year decline of more than 30% from sales of $966 million.

Moderna is grappling with slowing revenue growth and a lack of near-term catalysts to counter weakening demand, as vaccine sales continue to fade.

At the same time, the company must maintain elevated spending on research, development, and manufacturing to advance a broad pipeline spanning respiratory viruses, oncology, and other therapeutic areas. This combination is weighing on near-term profitability and increasing pressure on cash burn.

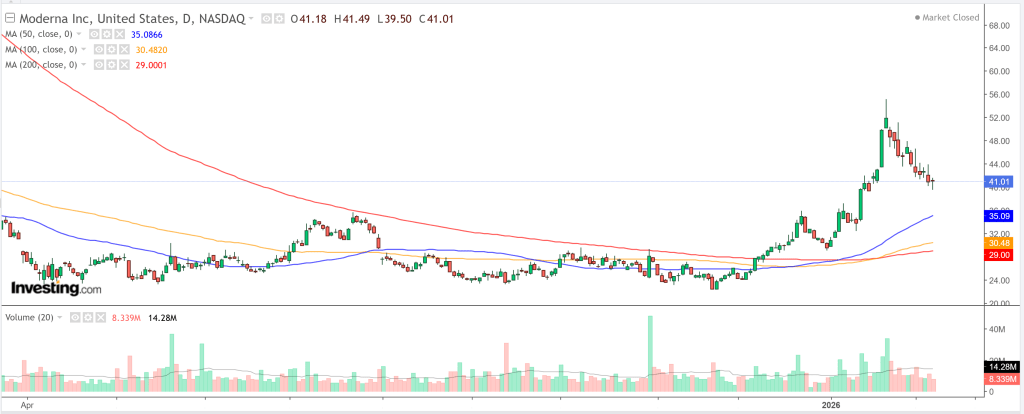

Moderna’s share price has started to lose momentum after a strong recent rally, ending Friday at $41.01. While the stock remains up 67.1% over the past three months and 21.1% in the last month, last week’s 7% decline points to waning upside traction.

In a market increasingly favoring growth and AI-linked themes, high-beta biotech stocks like Moderna are vulnerable to rotation, particularly if earnings fall short or forward guidance disappoints.

Trade setup:

Entry: Near current levels (~$40–41)

Target: $35 (potential gain of ~15%)

Stop-loss: $45 (risk of ~12.5%)

Whether you’re a newer investor or an experienced trader, tools like InvestingPro can help uncover opportunities while managing risk in a challenging and fast-moving market environment.

The S&P 500 remains highly volatile, with last week seeing the index test the 7,000 mark and briefly dip below 6,800 before rebounding. Overall, the price action suggests the market is still trying to determine its next direction, which is understandable given that earnings season is underway.

For now, the index continues to favor a buy-the-dip dynamic, with rebounds likely fueling further FOMO. A decisive move above 7,000 would likely open the door to further upside, although short-term choppiness is still to be expected.

EUR/USD

The euro traded in a choppy manner throughout the week as it tested the 1.18 level, an area that had previously acted as resistance. Last week’s price action formed a particularly ugly shooting star, leaving uncertainty about whether the euro has enough momentum to sustain an upside breakout.

A move below the low of last week’s candle could open the door for a pullback toward the 1.16 level, effectively returning the pair to its prior consolidation range. While short-term price action is likely to remain noisy, the broader outlook is clouded by ongoing uncertainty around ECB policy and whether the Federal Reserve will move quickly enough on rate cuts to satisfy market expectations. Overall, I remain neutral on this pair.

USD/CAD

The US dollar strengthened against the Canadian dollar but once again ran into resistance near the 1.37 level. Price is hovering around the 200-week EMA, and last week’s hammer candle suggests buyers may attempt to drive the pair higher, though confirmation is still needed.

From a technical perspective, this zone appears attractive for potential long positions, with the interest rate differential continuing to favor the US dollar. That said, this setup is better suited for short-term traders, as large or sustained moves are unlikely in the near term given the pair’s typically range-bound behavior.

USD/CHF

The US dollar has edged higher against the Swiss franc, pushing above the 0.78 level, a key psychological round number that many traders are closely monitoring. This pair is especially noteworthy given last week’s hammer formation and ongoing comments from the Swiss National Bank expressing discomfort with a strong franc.

Should the SNB maintain this stance, intervention remains a possibility, which would likely weaken the franc and lift USD/CHF along with other CHF-denominated pairs. While the positive swap favors long positions, the move higher is likely to be uneven and challenging, so traders should be mindful of potential volatility.

USD/MXN

The US dollar has been highly volatile against the Mexican peso, with the 17.50 level continuing to act as resistance. For now, the 17.00 area below appears to be the most likely short-term target.

From a longer-term perspective, there is substantial support beneath current levels, making a deeper breakdown uncertain. At the same time, the pair still offers an attractive carry trade, particularly for short-term participants. Given recent price action, this week is likely to remain as choppy as the last two, and significant moves seem unlikely.

DAX

The German DAX has maintained a bullish tone for most of the week but continues to face resistance near the 25,000 level. A decisive break above 25,000—ideally confirmed by a daily, if not weekly, close—would likely clear the way for further upside in the index.

A Global Search for Support

Over time, I expect that breakout to occur. This is not a market that lends itself well to short positions, as it is likely to receive ongoing support from the German government, which continues to inject significant spending into the economy. As a result, buying pullbacks in the DAX remains an attractive strategy.

USD/JPY

The US dollar has held up well against the Japanese yen this week, even in the wake of recent intervention efforts. The 158 level remains a major reference point on long-term charts, an area of significance that dates back to May 1990 and deserves close attention.

Looking further ahead, a sustained break above the 163 level—where the monthly chart shows a substantial resistance zone—could eventually open the door to much higher levels, potentially even toward 250 yen over the longer term. While such a move is not expected in the near future, it reflects the broader outlook for the yen unless there is a meaningful shift in underlying conditions.

GBP/USD

The British pound was highly volatile throughout the week, with the 1.3750 level once again acting as notable resistance. A break below 1.35 would be a strongly bearish signal for GBP/USD and could potentially open the door for a move toward the 1.30 area.

While it remains unclear whether the US dollar has definitively bottomed, it is beginning to show signs of attempting a base. If that proves to be the case, it could leave many traders positioned on the wrong side of the market.

Concerns that the U.S. dollar is heading into a phase of rapid debasement look exaggerated, despite ongoing longer-term headwinds. Although the currency has been volatile recently and briefly hit multi-year lows—reviving “Sell America” narratives—Bank of America says market evidence does not yet point to a structural shift away from U.S. assets.

While BofA remains bearish on the dollar over the long run, it expects any depreciation to play out gradually through 2026 and 2027 rather than through an abrupt decline. Investor positioning and capital flow data show little sign of a coordinated move out of U.S. assets. Dollar risk premia have risen only modestly, and options markets indicate that short-dollar positioning is not meaningfully larger than it was three months ago.

Cross-asset flows reinforce this view, with equity and bond data showing no substantial foreign capital flight from the U.S. Notably, there has been just one session this year in which both the dollar and U.S. equities sold off sharply at the same time—an outcome inconsistent with a broad debasement scenario.

Instead, BofA suggests that increased currency hedging is the more likely adjustment. European investors may hedge their U.S. exposure more actively, which could place steady, incremental pressure on the dollar without triggering a disorderly selloff.

Macro indicators also fail to signal rising debasement risks. Inflation expectations remain well anchored, and although fiscal concerns are widely discussed, they have not produced market stress indicative of eroding confidence in the dollar. Part of the expected dollar weakness may simply reflect improving conditions elsewhere, particularly in Europe, where stronger growth prospects, German fiscal stimulus, potential spillovers from Chinese stimulus, and longer-term structural factors such as higher defense spending and trade agreements could support the euro and other non-U.S. assets.

The opening weeks of the year have underscored how rapidly investor sentiment can change. In early 2026, markets saw a clear rotation into consumer staples, a sector traditionally favored for its defensive characteristics. As technology stocks came under pressure from elevated valuations and growing doubts about the durability of the AI-driven rally, consumer staples emerged as a relative safe haven.

The Consumer Staples Select Sector SPDR Fund (XLP), a widely followed benchmark, climbed roughly 13% year-to-date through early February—one of its strongest starts in more than ten years. By contrast, technology shares fell by about 3% over the same period, reflecting a classic shift toward lower-risk assets.

Why Investors Are Seeking Safety

The drivers behind this rotation are varied but grounded in clear logic. After years of leadership fueled by AI enthusiasm and an extended period of low interest rates, technology entered 2026 with lofty expectations. Rising concerns over escalating AI capital expenditures, potential regulatory pressure, and a more normalized rate environment triggered a wave of profit-taking.

At the same time, broader macro signals—including softening labor market conditions, pockets of persistent inflation, and heightened geopolitical risks—pushed investors toward more stable areas of the market. Consumer staples fit that role well. Demand for everyday necessities such as food, beverages, household goods, and tobacco alternatives remains steady, supporting reliable earnings, consistent dividend payouts, and lower overall volatility.

This shift mirrors historical patterns in which periods of uncertainty or market broadening drive capital away from high-growth, cyclical sectors and into defensive ones. Amid broader market pullbacks this year, consumer staples have stood out as one of the few areas of relative strength, drawing significant inflows as investors reduce risk. The sector’s limited sensitivity to economic cycles—consumers continue to buy essentials like toothpaste, soap, and snacks regardless of conditions—offers a cushion when discretionary spending weakens.

Consumer Staples Stocks Reaching Yearly Highs

Established industry leaders have been at the forefront of this move, combining defensive stability with incremental growth drivers. Philip Morris International (NYSE: PM) has been a notable example, with shares posting solid gains in early 2026 following a strong fourth-quarter 2025 earnings report. The company’s ongoing shift toward smoke-free alternatives—such as IQOS heated tobacco products and Zyn nicotine pouches—has delivered robust volume growth, more than offsetting declines in traditional cigarette sales.

Philip Morris exceeded Q4 expectations, reporting adjusted earnings per share of $1.70, up 9.7% year over year, alongside revenue growth of 6.8%. The stock currently holds a Zacks Rank #3 (Hold), reflecting stable near-term expectations. Consensus forecasts call for full-year 2026 EPS of roughly $8.34, representing nearly 11% annual growth, supported by strong pricing power and continued momentum in emerging markets.

Coca-Cola (NYSE: KO) completes the list of standout performers, benefiting from its unmatched global brand presence in beverages. Continued volume growth in emerging markets, along with broader diversification into non-carbonated offerings, has helped sustain the company’s momentum. Coca-Cola’s attractive dividend yield and dependable payout profile make the stock particularly appealing in income-focused environments. Currently holding a Zacks Rank #3 (Hold), consensus estimates suggest a steady, incremental improvement in earnings per share.

Bottom Line

These sector leaders highlight the core appeal of consumer staples: dependable, recurring revenue from essential products; strong balance sheets that support consistent dividends—often in the 3–4% yield range; and modest growth driven by innovation or international expansion. Valuations across the sector remain reasonable relative to growth prospects, with many names trading at forward price-to-earnings multiples in the high teens to low 20s, well below the elevated valuations seen in much of the technology space.

As recession concerns quietly build amid a softening labor market, consumer staples offer credible downside protection without materially compromising long-term total returns. For well-diversified portfolios, the sector serves as a stabilizing anchor—delivering steady performance in increasingly uncertain market conditions.

The U.S. and Iran are holding talks in Oman today focused on dismantling Iran’s nuclear program. Washington is pushing Tehran to halt uranium enrichment, scale back its ballistic missile development, and withdraw support for regional proxy groups that contribute to instability in the Middle East. Iran, however, has stated it is only prepared to negotiate on nuclear-related issues. If discussions collapse, the risk of renewed U.S. military action rises, underscored by the significant U.S. naval presence in the region. That said, Iran recently seized two oil tankers ahead of the talks and later described the discussions as “positive.”

Following the meeting, Iranian Foreign Minister Abbas Araghchi said on state television that both sides could reach a framework for future negotiations if talks continue along the same lines. He emphasized that the dialogue remains limited strictly to nuclear matters, with no broader issues under consideration. Given Iran’s history of prolonging negotiations and the U.S. military buildup aimed at Iranian nuclear and defense assets, it remains to be seen how long Washington will tolerate a narrow scope of engagement.

Meanwhile, despite some concerns on Wall Street about OpenAI’s momentum, activity in the data center sector continues to accelerate. Super Micro Computer (SMCI) reported a 123% year-over-year jump in fourth-quarter revenue to $12.7 billion, while earnings climbed to $0.69 per share. The company delivered a 22.1% revenue beat and a 40.8% earnings surprise, along with upbeat forward guidance. As one of Nvidia’s largest customers, Super Micro’s results suggest Nvidia could also deliver a strong upside surprise, even as analysts forecast robust growth of 66.7% in sales and 71.1% in earnings.

AI-driven productivity gains are expected to continue supporting stronger GDP growth. The data center expansion shows no signs of slowing, underscoring the durability of the AI revolution. Nvidia’s upcoming Vera Rubin GPU—offering five times the performance and ten times the energy efficiency of the Blackwell architecture—is likely to trigger a multi-year AI hardware replacement cycle. At the same time, pricing for advanced chips and memory remains resilient, allowing AI demand to sustain strong profitability across the semiconductor ecosystem, including Nvidia (NVDA), Micron (MU), and Seagate Technology (STX).

The U.S. economy is experiencing a powerful growth phase, with annual GDP growth of 5% potentially driven by an estimated $20 trillion in onshoring investments across data centers, semiconductors, pharmaceuticals, and automotive manufacturing. Energy independence gives the U.S. a structural advantage over global peers, as manufacturers can avoid tariffs by relocating production domestically. In addition, U.S. support for increased crude oil output in Venezuela should help keep global oil prices contained over the medium term.

Overall, the U.S. continues to outperform globally in domestic growth. With Kevin Warsh nominated as the next Federal Reserve Chair, the U.S. dollar is expected to strengthen further. While AI is clearly enhancing productivity, it is also contributing to job displacement across corporate America. As a result, the Federal Reserve is likely to cut policy rates at least three times this year amid ongoing labor market concerns. These rate cuts should, in turn, help lift consumer confidence in the months ahead.

Tech just suffered a selloff of a different kind. This was not about rates, recession fears, or a routine earnings disappointment. It was the market catching its own reflection in the AI mirror—and flinching.

When confidence cracks, the Nasdaq does not rotate. It drops the floor. The S&P followed along, dutifully diversified in theory, while tech still steers the wheel.

The trigger was AMD, but the message was broader. In a fully priced bull market, “good” results are not good enough when investors have already paid in advance for perfection. When expectations stretch into the stratosphere, even a strong quarter feels like a letdown. AMD was not punished for weakness—it was punished for failing to deliver magic commensurate with the valuation it carried.

What followed was less about fundamentals than positioning. This was the market unwinding a narrative that had become too tidy, too crowded, too self-assured. When everyone leans the same way, even a minor wobble turns into a shove.

And the shove traveled fast. Once the story lost its grip, selling turned indiscriminate. Yesterday’s AI champions were treated like stale trades. Hardware names sank alongside software darlings. Picks, shovels, and miners all landed in the same risk bucket as investors dumped exposure wholesale.

This was never just a chip story. The real fault line runs through software—and it is psychological. The market is now entertaining a new fear: not that AI lifts all boats, but that it punctures the hulls of those that assumed they were unsinkable.

Software cracked first because belief ran deepest there. It was the cleanest narrative in the market—AI as a quiet margin expander, a tailwind that boosted earnings without disrupting the underlying structure. That assumption is now being dismantled in real time.

The uncomfortable inversion is coming into focus. The companies that digitized the fastest may also be the most exposed. AI is not arriving as a polite consultant. It is entering as a tireless shadow workforce—one that never negotiates, never sleeps, and learns faster than corporate hierarchies can adapt. And it writes code, too.

That is why this moment feels like a break, not a revision. When markets stop debating how much something earns and start questioning why it exists, prices do not drift lower. They fracture.

You can see it in the tape. This is not a careful repricing—it is an exit rush. One day the debate is about margins; the next it is about whether the product becomes a feature inside a larger model.

Once that fear enters the room, it spreads quickly across anything tied to monetized knowledge work—data platforms, marketing software, legal tools, analytics, even media and advertising adjacencies. If AI does the work, who gets paid for it? That is the question markets are stress-testing in real time.

For years, software earned its margins by controlling workflow—owning the screen, the process, the friction. Humans did the thinking; software rented them the tools and charged a recurring toll. Predictable. Scalable. Defensible. That doctrine is now under review.

Bitcoin and gold sliding alongside tech is telling. When risk sentiment turns, speculative layers lose sponsorship first. It is not ideology—it is mechanics. When leverage gets pulled back, froth goes first.

This does not mean tech is finished. It means tech is being tested.

Every cycle follows the same arc: markets fall in love with innovation, price it as destiny, then recoil when destiny arrives with disruption and bills. AI is no longer just a growth story—it is a competitive weapon. That creates winners and losers, not a rising tide. The trade is shifting from owning the theme to owning the survivors.

This is what a regime change looks like within a sector. Euphoria gives way to scrutiny. Momentum yields to forensic analysis. Markets stop paying for possibility and start paying for proof.

Ironically, the most technologically advanced firms often feel the shock first—they sit closest to the blast radius. If your business automates knowledge work and a universal automation engine shows up, you do not get to pretend the rules stayed the same.

Panic, of course, is rarely precise. Markets swing the hammer before identifying the nail. These moments tend to overshoot because fear moves faster than analysis.

This looks less like the end of AI and more like a narrative reckoning. The market is re-evaluating who captures value, who loses the toll booth, and who gets displaced.

AI is not killing tech. It is forcing tech to prove it has a moat—not just a story.

When markets stop buying dreams, they start auditing business models.

UK grocery inflation slowed to 4.0% in the four weeks ending January 25, marking its lowest level since April last year, according to figures released Tuesday by market researcher Worldpanel by Numerator.

The reading eased from the 4.3% inflation rate reported in Worldpanel’s previous update, offering modest relief to households grappling with elevated food prices.

The data also serves as an early signal of price pressures ahead of the UK’s official inflation release scheduled for February 18.

Despite the moderation in inflation, Worldpanel noted that UK grocery sales increased 3.8% year on year in value terms over the four-week period. Adjusted for inflation, however, this translates into a decline in volumes, indicating that consumers are buying less even as overall spending rises.

The Reserve Bank of Australia raised its policy rate by 25 basis points on Tuesday, in line with expectations, and cautioned that inflation is likely to stay above target in the months ahead.

The unanimous decision lifted the cash rate target to 3.85% from 3.65%, following a renewed uptick in inflation late last year that pushed underlying price pressures back above the RBA’s 2%–3% target range.

The central bank said private demand remained resilient and domestic capacity constraints persisted, factors it expects will keep inflation elevated for some time. While some of the recent rise in inflation reflects temporary influences, the RBA noted that demand has been expanding faster than anticipated, capacity pressures are stronger than previously assessed, and labour market conditions remain tight.

The RBA stopped short of signalling further rate increases, instead reaffirming its commitment to maintaining price stability and full employment, and said it would take whatever action it deems necessary to achieve those objectives.

JPMorgan has lifted its year-end 2026 gold price forecast to $6,300 an ounce, pointing to sustained and strengthening demand from central banks and investors despite the recent bout of sharp price volatility.

Gold and silver both saw steep pullbacks late last week after rapid rallies left prices overstretched, with the move partly driven by a rebound in the U.S. dollar. Even so, JPMorgan analysts said the broader environment continues to favor gold, arguing that the “longer-term rally momentum will remain intact” and that they remain “firmly bullish” over the medium term, supported by a structural diversification trend.

A key factor behind the higher forecast is stronger-than-expected buying from the official sector. Central banks purchased around 230 tonnes of gold in the fourth quarter, taking total buying for 2025 to roughly 863 tonnes, even as prices moved above $4,000 an ounce. JPMorgan now expects about 800 tonnes of central bank demand in 2026, citing ongoing reserve diversification that still has room to run.

Investor demand has also picked up, with analysts highlighting rising ETF holdings, solid physical bar and coin purchases, and broader portfolio allocations to gold as a hedge against macroeconomic and geopolitical risks.

“Gold remains a dynamic, multi-faceted portfolio hedge, and investor demand has continued to exceed our previous expectations,” analysts led by Gregory Shearer wrote. “As a result, we now see sufficient demand from central banks and investors to push gold prices to $6,300 per ounce by the end of 2026.”

While acknowledging the speed of the rally, the analysts dismissed concerns that prices are nearing unsustainable levels, noting that demand remains well above the historical threshold needed to keep the market tightening. “While the air gets thinner at higher price levels, we are not yet close to a point where the structural gold rally risks collapsing under its own weight,” they added.

On silver, JPMorgan struck a more cautious tone following the metal’s sharp surge and subsequent pullback. Without central banks acting as consistent dip buyers, the analysts said they are “somewhat apprehensive” about the risk of a deeper near-term correction in silver relative to gold.

Even so, they see a higher average price floor of around $75 to $80 an ounce, arguing that silver is unlikely to fully give up its recent gains. Over the longer term, JPMorgan expects higher prices to reshape fundamentals, gradually easing the supply-demand imbalance that underpinned silver’s recent rally.

Morgan Stanley said the recent pullback in Nvidia shares appears disconnected from the company’s strong near-term fundamentals, noting that investors remain puzzled by the stock’s underperformance despite a “very robust AI environment.”

Analyst Joseph Moore said his team was “somewhat surprised” by Nvidia’s year-to-date weakness following a soft finish to 2025. He added that investors frequently ask what factors drove the decline and how those pressures could dissipate in 2026.

Moore said business checks remain “very strong and getting stronger,” while market optimism around upcoming earnings is building. He noted growing discussion of Nvidia’s earnings power exceeding $9 per share this year, well above the consensus estimate of $7.75, which he believes makes near-term upside “highly likely.”

In his view, several concerns weighing on sentiment are exaggerated. Moore said AI beneficiaries are expanding as demand accelerates and supply constraints spread across the industry. He also addressed investor focus on financing risks tied to frontier AI model developers and Nvidia’s involvement, saying this will require some recalibration in how the market assesses the risk.

Concerns about rising competition from custom ASICs and AMD persist, but Moore described them as overblown. Looking ahead, he highlighted Nvidia’s upcoming Vera Rubin platform as a key catalyst that should reinforce the company’s technology leadership and help alleviate momentum concerns.

“Ultimately, we expect the stock to outperform from here,” Moore wrote, adding that while Nvidia still faces a “wall of worry,” it appears well positioned to move past it.

Lynx warns Apple margins under renewed pressure as NAND prices jump

Lynx Equity Strategy warned that Apple could be facing a deeper profitability squeeze than investors currently expect, arguing there is “further downside” to the stock even after its roughly 10% decline this year.

The brokerage said channel checks point to rising memory costs, with Apple confronting a sharp increase in NAND flash prices after talks with long-time supplier Kioxia broke down. Lynx said tensions emerged after Apple secured lower long-term pricing that created a margin gap for Kioxia, potentially leading the supplier to ship below Apple’s projected demand.

As a result, Apple has reportedly turned to Samsung to cover the shortfall. Without long-term supply agreements, Lynx said Samsung can charge prevailing market rates, which may be significantly higher. A Taiwan report cited by the firm suggested Samsung may have lifted NAND prices by as much as 100%, with Apple likely among the affected customers.

Lynx also highlighted technical risks, noting that Apple’s flash controller is optimized for Kioxia’s NAND process and may not perform as effectively with Samsung’s chips, increasing the possibility of performance issues or product returns.

“The Street is underestimating the impact,” Lynx said, warning that both Apple’s margins and its share price could remain under pressure in the coming period.

Barclays upgrades ASML on record orders, sees further upside

ASML shares moved higher earlier in the week after Barclays upgraded the stock to Overweight, pointing to record order growth, accelerating AI-driven demand and upside potential that it says the market has yet to fully reflect.

Analyst Simon Coles said expectations were already elevated going into the results, but those hopes were exceeded as orders hit record levels, prompting significant upward revisions to forecasts. Barclays raised its price target to €1,500 from €1,200, arguing there is still “room for further upside” given what it views as conservative guidance despite improving fundamentals.

ASML reported record order intake of €13.2 billion, almost double last year’s figure and well above market expectations. The company also increased its 2026 revenue outlook to a range of €34 billion to €39 billion, surpassing consensus estimates and improving on its prior outlook for largely flat growth versus 2025.

In addition to the strong demand outlook, ASML announced plans to reduce its workforce by around 1,700 roles as part of a broader restructuring effort aimed at simplifying management structures while increasing investment in engineering capacity.

Barclays said lithography demand linked to large-scale data center construction remains a key growth driver for ASML, while further upside could emerge from consumer AI adoption, humanoid robotics and a more resilient memory spending cycle.

The bank also highlighted intensifying foundry competition as a particularly supportive factor. Analyst Simon Coles said increased rivalry is likely to spur higher capital investment, creating upside risk that should benefit ASML and the broader semiconductor capital equipment sector through 2027.

Concerns around China were described as overstated. Coles noted that ASML’s guidance already assumes China revenue declines of more than 10% year over year at the start of 2026, but recent strength in imports suggests demand remains robust.

Barclays now forecasts low-teens revenue growth for ASML in both 2026 and 2027, translating into mid- to high-teens earnings upgrades, with additional upside possible if AI investment and foundry spending accelerate beyond current expectations.

Mizuho lifts Applied Materials on strengthening chip equipment demand

Applied Materials was upgraded to Outperform from Neutral by Mizuho, which cited a sharp rebound in semiconductor capital spending and improving demand from foundry and logic customers.

Analyst Vijay Rakesh raised the firm’s price target to $370 from $275, saying Applied Materials is positioned to benefit from a “meaningful acceleration” in wafer fab equipment (WFE) spending through 2027. Mizuho now forecasts WFE growth of 13% year over year in 2026, followed by 12% growth in 2027, marking a notable step-up from its prior outlook.

With roughly 65% of revenue exposed to foundry and logic customers, Rakesh highlighted rising capital expenditures from TSMC and improving tool spending at Intel as key growth drivers. TSMC’s capital spending from 2026 to 2028 is expected to be significantly higher than in the 2023–25 period, with 2026 outlays alone projected to climb 32% to about $54 billion.

Memory demand is also seen as supportive, with DRAM tied to high-bandwidth memory accounting for roughly 30% of Applied Materials’ revenue base. While China remains a headwind, with revenue from the region expected to decline 4% this year, Rakesh said growth elsewhere — representing about 70% of sales — is accelerating more rapidly.

He added that AI-driven investment is pushing leading-edge development below the 2-nanometer node, and said the broader recovery in global WFE spending is creating “strong tailwinds” for equipment suppliers, underpinning the upgrade and higher earnings estimates for 2026 and 2027.

BofA reiterates Snowflake as top software pick, says AI to accelerate growth

Bank of America said Snowflake remains “one of the fastest-growing stories in software,” reaffirming its Buy rating and keeping the stock as a top pick within infrastructure software.

Analyst Koji Ikeda said Snowflake is well positioned to benefit from accelerating enterprise investment in data analytics and artificial intelligence, given its role as a core cloud data platform. He said the key investor debate is whether Snowflake can sustain product revenue growth in the high-20% year over year range or even reaccelerate into the 30s — an outcome he believes is achievable.

Ikeda pointed to Snowflake’s expanding product portfolio, strong AI-related demand and rising customer consumption as key growth drivers. “The blizzard is just starting to form around broad AI adoption, and we believe Snowflake will play a foundational role,” he wrote.

BofA expects Snowflake’s growth to remain top-tier within infrastructure software, far outpacing peers growing at around 10%. The bank also raised its price target to $275, reflecting an updated valuation framework incorporating its revised growth outlook, risk assessment and peer multiple trends.

Ikeda described Snowflake as increasingly becoming the “king of enterprise data in the cloud,” highlighting its OLAP data lakehouse architecture, which enables customers to scale compute and storage independently to optimize performance and costs.

While acknowledging that the shares are not inexpensive — trading at a roughly 123% premium to peers — Ikeda said the valuation appears more reasonable on a growth-adjusted basis, where Snowflake trades in line with its peer group.

Canada’s opposition Conservative Party has voted by a wide margin to keep Pierre Poilievre as leader following a mandatory leadership review triggered by its loss in the last federal election.

At a party convention in Calgary on Saturday, Conservatives backed Poilievre with 87.4% of the vote, reaffirming his leadership after the party was defeated by the Liberals under Prime Minister Mark Carney in April.

The result comes after a sharp political reversal. In January, the Conservatives were polling more than 20 points ahead of the Liberals, but momentum shifted after repeated remarks by U.S. President Donald Trump about Canada becoming the 51st U.S. state helped rally voters around Carney.

Although Poilievre lost his own parliamentary seat in the election, he returned to the House of Commons after winning a by-election in August.

Ahead of the vote, Ashton Arsenault, a former aide in Stephen Harper’s Conservative government, said Poilievre needed at least 75% support to clearly demonstrate confidence in his leadership. The final result exceeded that threshold comfortably, signaling unity within the party heading into the next election cycle.

Meanwhile, public opinion remains mixed. Pollster Angus Reid reports Carney’s approval rating has climbed to 60%, the highest since he became Liberal leader. While about 80% of Conservative supporters back Poilievre, broader public sentiment is less favorable, with 58% of Canadians viewing him negatively.

The U.K. economy is at risk of a “significant recession,” a scenario that could force the Bank of England into a far more aggressive easing cycle, according to BCA Research.

In a research note, analysts led by Robert Timper said key indicators of U.K. economic growth continue to show weakness, with business sentiment and labor market data sending what they described as recession-like signals.

They noted that although layoffs remain relatively contained for now, slowing profit growth increases the risk of deeper job cuts ahead.

“The bottom line is that the U.K. labor market is deteriorating at a concerning pace and, in many respects, already appears recessionary,” the analysts wrote. “If incoming data fails to improve, labor market conditions could tip the U.K. economy into recession.”

At the same time, wage growth has moderated and price pressures in the services sector have normalized, reinforcing expectations that underlying inflation will ease toward the Bank of England’s 2% target later this year.

Against this backdrop, the BoE is expected to deliver rate cuts broadly in line with market pricing, totaling around 41 basis points this year. The central bank cut interest rates by 100 basis points in 2025.

From an investment perspective, BCA Research said U.K. equities remain appealing despite domestic economic softness, supported by the prospect of lower borrowing costs, a weaker pound, and strong overseas revenue exposure. The firm favors U.K. stocks over Eurozone equities over the next three to six months.

The analysts said U.K. equities remain attractively valued and have yet to show signs of being overbought.

They added that energy markets could again provide support, noting that a potential collapse of Iran’s ruling regime could trigger what they described as a historic shock to global oil supply.

Given the heavy weighting of oil and gas companies in major U.K. indexes, they said the broader U.K. market has historically outperformed Eurozone equities during periods of rising oil prices.

The euro’s recent surge has brought renewed attention to the European Central Bank, though economists argue it is unlikely to prompt any near-term policy action.

Last week, the single currency climbed to $1.20 against the U.S. dollar for the first time since mid-2021, marking an unusually swift move by historical standards. According to Capital Economics, the euro has strengthened by a similar scale over a 10-day period only a few times in the past decade, while its trade-weighted exchange rate has reached a record high.

Even so, analysts expect the inflationary impact across the euro zone to remain modest. Capital Economics cited ECB sensitivity analysis showing that if the euro stabilizes at current levels, headline inflation next year would be roughly 0.1 percentage points lower than projected in the ECB’s December forecasts.

While this slightly increases downside risks to inflation, the brokerage said it falls far short of the threshold that would justify foreign-exchange intervention on price-stability grounds.

The ECB is likely to address the euro’s strength at its meeting next week, but concrete action appears improbable. Although the central bank has the authority to intervene in currency markets to prevent disorderly moves that could threaten price stability, Capital Economics noted that the euro would need to rise much further before such measures were considered. Even then, intervention through dollar purchases is viewed as highly unlikely.

Historically, the ECB has stepped into currency markets only twice—once in late 2000 and again in March 2011—both times to support, rather than weaken, the euro. Those interventions were coordinated with other major central banks. Capital Economics added that a coordinated effort to push the euro lower now looks extremely unlikely, particularly given the U.S. administration’s preference for a weaker dollar.

ECB officials have so far played down the recent appreciation. Vice President Luis de Guindos has previously described levels above $1.20 as “complicated,” while also calling the level itself “perfectly acceptable.” Meanwhile, Austria’s central bank governor has characterized the latest rise as “modest.”

Capital Economics expects ECB President Christine Lagarde to reiterate that policymakers are closely monitoring exchange-rate developments, but not to actively try to talk the currency down.

Although intervention is unlikely in the near term, prolonged euro strength could influence policy over time. Capital Economics said ECB analysis suggests that if the euro were to appreciate gradually to between $1.25 and $1.30 over the next three years, headline inflation in 2028 would be about 0.3 percentage points lower.

Under such conditions, policymakers would be more inclined to respond through stronger verbal guidance and lower interest rates rather than direct currency market intervention.

For now, economists say the euro’s rise largely reflects U.S. dollar weakness rather than stronger euro zone fundamentals, reducing the need for an immediate response. As a result, the ECB is expected to remain on the sidelines unless the appreciation becomes substantially larger and more persistent, according to Capital Economics.

Japanese Prime Minister Sanae Takaichi highlighted the advantages of a weaker yen during a campaign speech, striking a note that contrasted with her finance ministry’s stance, which has kept all measures on the table to address excessive currency volatility.

She later walked back her remarks, clarifying that she holds no particular preference regarding the yen’s direction.

“Many people argue that the weak yen is a negative at the moment, but for exporters it represents a significant opportunity,” Takaichi said on Saturday, ahead of the snap election scheduled for February 8.

“Whether in food exports or automobile sales, even with U.S. tariffs in place, the weaker yen has acted as a cushion. That support has been extremely valuable,” she added.

Takaichi also said she aims to strengthen Japan’s economy against currency swings by encouraging greater domestic investment.

FILE PHOTO: Japan’s Internal Affairs Minister Sanae Takaichi attends a news conference at Prime Minister Shinzo Abe’s official residence in Tokyo, Japan September 11, 2019. REUTERS/Issei Kato/File Photo

The yen has been trading near 18-month lows against the U.S. dollar, fuelling inflation and raising expectations of potential interest-rate increases by the central bank. Finance Minister Satsuki Katayama has repeatedly stated that authorities are prepared to step in to stabilise the currency if needed — comments widely interpreted by markets as a signal of possible intervention.

In a post on X on Sunday, Takaichi reiterated that she does not support either a strong or weak yen.

“I did not state that one is better or worse,” she wrote, adding that the government is closely watching financial markets and that, as prime minister, she will avoid making specific remarks on exchange-rate levels.

“My intention was simply to say that we want to build an economic framework capable of withstanding exchange-rate volatility, not — as some reports have implied — to promote the advantages of a weak yen.”

Former prime minister and finance minister Yoshihiko Noda, who co-leads the largest and newly formed opposition group, the Centrist Reform Alliance, said a weak yen is hurting households, according to Nikkei on Sunday.

“Amid an excessive depreciation of the yen, no one feels comfortable when they look at their household finances,” Noda was quoted as saying. “The viewpoint of ordinary citizens is absent, which once again raises serious concerns for me.”

The yen jumped after reports that the New York Federal Reserve had joined Japanese authorities in contacting banks to inquire about exchange rates for potential yen purchases — a move traders often view as a signal that intervention could be imminent.

The currency’s prolonged slide, alongside a recent surge in Japanese government bond yields to record levels, underscores investor unease over the country’s stretched fiscal position.

Takaichi is seeking voter approval for her push to revive inflation and reflate the economy.

During and in the aftermath of 9/11, Nassim Taleb—a Lebanese-born former options trader and quantitative analyst—published Fooled by Randomness. He later refined and formalized the idea in his 2007 book The Black Swan, drawing on the metaphor of the rare black swan, an anomaly among typically white birds.

Taleb defined a Black Swan as an event that meets three criteria: first, it is an extreme outlier, often without historical precedent; second, it carries an immediate and profound impact; and third, it becomes explainable only in hindsight, after the event has occurred.

Forty years ago tomorrow, on the morning of Tuesday, January 28, 1986, tens of millions of Americans watched live as the Space Shuttle Challenger lifted off—only to explode 73 seconds into flight, killing all seven crew members, including the widely admired teacher-astronaut Christa McAuliffe.

The tragedy met all of Nassim Taleb’s criteria for a Black Swan event. First, it was unprecedented, marking the first fatal in-flight disaster involving a US spacecraft. Second, its impact was immediate: President Ronald Reagan postponed his State of the Union address scheduled for that evening. Third, the cause was only fully understood after the fact, when physicist Richard Feynman explained during televised hearings that the disaster resulted from O-ring failure in unusually cold conditions.

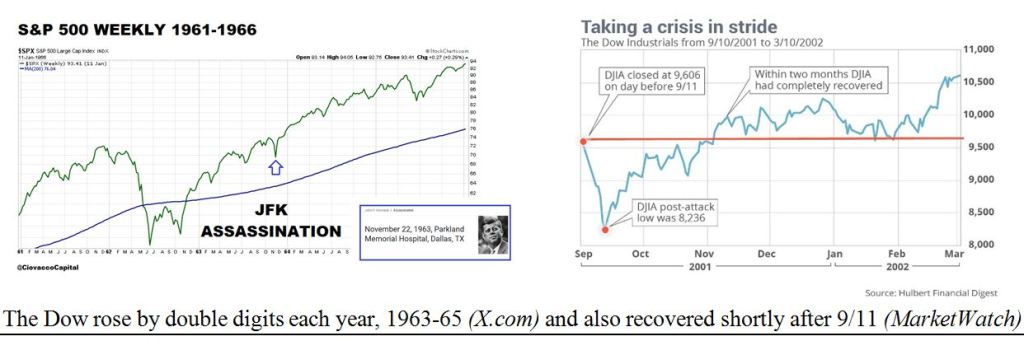

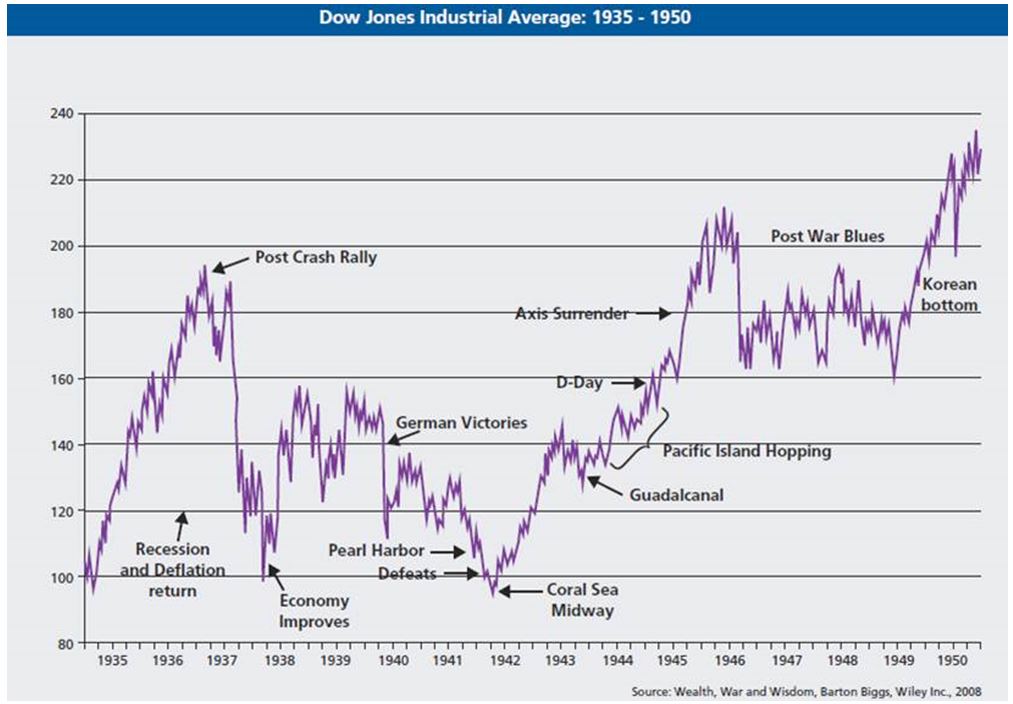

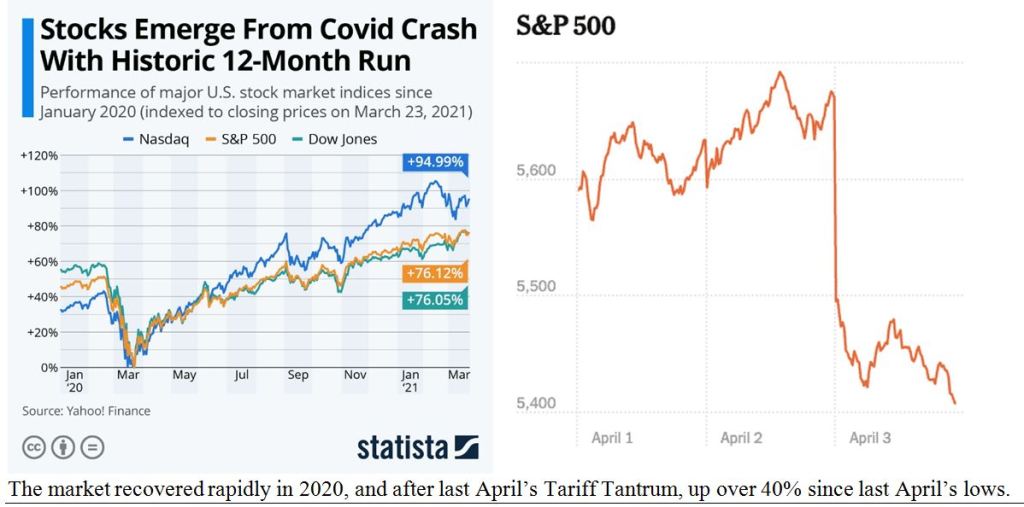

One response that did not occur—then or in most Black Swan events—was a meaningful stock market selloff. Markets were largely indifferent. The S&P 500 rose on the day of the explosion and continued higher, gaining 2.6% for the week and 16.8% over the remainder of 1986. The Dow Jones Industrial Average also advanced, rising 1.2% on the day, 2.7% for the week, and 22.6% for the year.

Another Black Swan touched Great Britain exactly fifty years earlier, when global stock markets closed on January 28, 1936, to mark the funeral of King George V. He was succeeded by Edward VIII, whose relationship with an American divorcée triggered a constitutional crisis that lasted much of the year. The turmoil ended with Edward’s abdication in favor of his younger brother, who became King George VI and later passed the crown to his daughter, Elizabeth II—the longest-reigning and arguably most popular British monarch—suggesting the succession ultimately resolved smoothly.

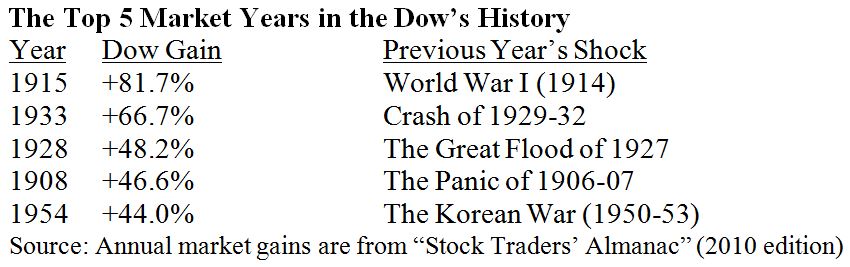

Despite the political uncertainty, 1936 proved to be a strong year for markets during an otherwise bleak Depression-era decade, with the Dow Jones Industrial Average rising 25%.

Across the past century, several other major Black Swan events have reshaped history, including the outbreak of World War I following the assassination in Sarajevo on June 28, 1914; Japan’s attack on Pearl Harbor on December 7, 1941; the assassination of President John F. Kennedy on November 22, 1963; and the September 11, 2001 attacks.

History also shows a striking pattern in which US presidents elected in seven consecutive election years, spaced 20 years apart, died in office: William Henry Harrison (1840), Abraham Lincoln (1860), James Garfield (1880), William McKinley (1900), Warren Harding (1920), Franklin Roosevelt (1940), and John F. Kennedy (1960). One might argue that this grim sequence made the outcome seem almost “predictable.” The streak ended two decades later, when Ronald Reagan survived an assassination attempt in March 1981, with John Hinckley’s bullet narrowly missing his heart.

Following the survival of Reagan—and Pope John Paul II six weeks later—three major Black Swan events marked the late 1980s. The first was the 1986 Challenger explosion, followed by the 1987 Black Monday market crash, which shocked investors far more than the general public. The decade closed with the fall of the Berlin Wall in 1989, a swan-like event, even though many had anticipated the eventual collapse of Gorbachev’s Soviet Union.

The stock market shrugs off most Black Swan events

The stock market posted an unexpected rally in the week and year following President Kennedy’s assassination and rebounded swiftly after the September 11, 2001 attacks. These Black Swan events appeared to have little lasting effect on Wall Street, as traders largely focused on other—primarily financial—developments and trends.

Markets also tended to rise during many 20th-century wars, most of which began with surprise attacks. The abrupt onset of World Wars I and II, the unexpected outbreak of the Korean War, and the August 1964 Gulf of Tonkin escalation of the Vietnam War all triggered initial sell-offs that were followed by strong market recoveries.

The accompanying diagram illustrates the market’s detailed reaction after the attack on Pearl Harbor in late 1941 and following the North Korean invasion in June 1950. These two episodes were separated by a period of post-war, largely “Swan-less,” malaise in the late 1940s.