Silver faced a difficult week as the U.S. dollar strengthened for much of the period, though it’s important to remember that its recent collapse wiped out many retail trading accounts.

That said, this is a market worth monitoring closely because the $80 level represents an important support area and sits near the center of the broader consolidation range.

If the price breaks below this week’s candlestick, it could open the door for silver to decline toward the $70 level, where I also expect support to emerge.

Overall, the market has been quite volatile and choppy, and that pattern is likely to persist. Because of this, careful position sizing will be essential.

S&P 500

The S&P market declined quite sharply over the week, testing the 5,000 level. This level is a major round number with strong psychological importance, so it’s an area many investors are watching closely.

If the market breaks below 5,000, it could pave the way for a drop toward 4,800, with the possibility of quickly moving further down to around 4,600.

From a longer-term perspective, the 5,000 level may continue to act as a price magnet for the market.

If that remains the case, we could see extended sideways movement around this zone, although my broader outlook still leans bullish over the long run.

USD/CAD

The US dollar first strengthened against the Canadian dollar, rising to test the 1.3750 level, but then reversed and began showing signs of weakness. Meanwhile, the 1.35 level below stands as an important support area that many market participants are closely monitoring.

It is also worth noting that the Canadian dollar has been gaining some strength on the back of rising oil prices. Whether that trend will continue is uncertain, but if oil fails to maintain its momentum, a reversal could follow.

For now, the market remains within the same consolidation range that it has revisited repeatedly.

USD/MXN

The US dollar surged sharply against the Mexican peso during the week, but in reality a pullback had been due. The key question now is whether the 18-peso level will act as strong enough resistance to reverse the move.

If it does, it could present a solid opportunity to take short positions. However, if the market manages a daily close above the 18-peso level, it may signal that the recent trend is coming to an end.

All things considered, this is a market where traders may look for signs of exhaustion to sell into, as the interest rate differential still generally favors Mexico.

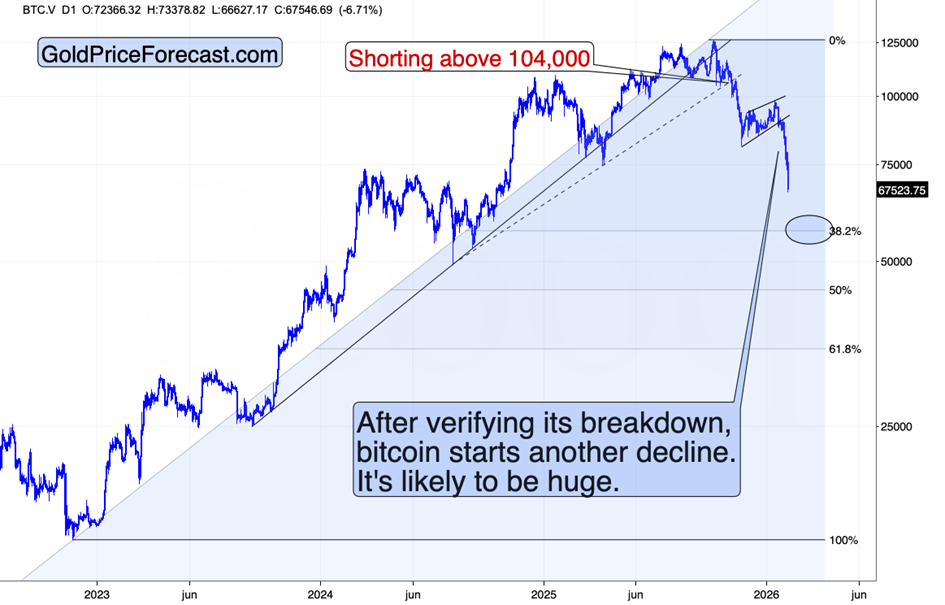

Bitcoin

The Bitcoin market has been quite volatile during the week, but it did manage to break above the $72,000 level. This is notable given the overwhelmingly negative headlines around the world at the moment, and it’s a market I’ll be monitoring very closely.

If the market can close above the weekly high and continue moving higher, Bitcoin could begin to rally strongly. There may still be debate about what Bitcoin truly represents, but one thing seems clear—it appears to be heavily oversold.

The key question now is whether buyers will step back in. On the other hand, if the price drops below the $60,000 level, it could trigger a sharp and widespread sell-off.

Nasdaq 100

The Nasdaq 100 has been volatile but has continued to show resilience. This is a pattern that appears repeatedly in the US stock market, even when there have been plenty of reasons for it to break down. In itself, that persistence likely says a lot about the underlying strength of the market.

What I think it tells you is that given enough time, the US stock market, and in this case the Nasdaq 100, will find buyers on any pullback and selling just does not seem to be working out.

EUR/USD

The euro weakened significantly during the week. Much of this appears to be driven by expectations that energy costs in the European Union will rise sharply, which could heavily influence the options available to the European Central Bank.

Keep a close eye on the 1.15 level. If the market breaks below that point, the euro could decline sharply.

For now, the market remains within the same consolidation range it has been trading in for some time. I do not expect significant movement at the moment, but the 1.15 level will be important to watch.

USD/JPY

The US dollar continues to signal the possibility of a major breakout against the Japanese yen, although it has not achieved it yet. The ¥158 level marks the start of a strong resistance zone that extends up to the ¥160 level.

If the market manages to break above that area, it is likely to move significantly higher. In the short term, pullbacks could present buying opportunities as traders look to pick up the dollar at lower prices.

Over the longer term, I expect an eventual breakout to the upside. However, the current situation makes it challenging to short the market, while buying directly at this resistance zone is also difficult. It may be best to wait for better value and take advantage of opportunities when they appear.

Bitcoin edged higher on Thursday, stabilizing after a wave of regulatory optimism and improving market sentiment fueled recent gains in the world’s largest cryptocurrency, though concerns linked to the Iran conflict continued to weigh on markets. The digital asset rose 1.5% to $72,620 by 09:37 ET (14:37 GMT), after reaching a one-month peak of $73,243 on Wednesday.

However, some gains were pared back as U.S. stock index futures turned negative Thursday morning, with ongoing tensions between the U.S., Israel, and Iran keeping investors cautious. Rising oil prices also intensified worries about the conflict’s potential inflationary effects.

Bitcoin had surged on Wednesday, extending earlier weekly gains as a strong performance on Wall Street boosted risk appetite. Bargain buying also contributed to the rally following the cryptocurrency’s sharp losses in February. The market was further supported after U.S. President Donald Trump urged lawmakers to quickly pass a long-delayed crypto market framework bill and criticized major U.S. banking groups for opposing yield payments on stablecoins.

His remarks fueled expectations that the industry could receive more favorable regulation in the U.S., although progress on the CLARITY Act—designed to establish a clear market structure for crypto—remains limited. Earlier optimism was also driven by reports suggesting Iran was seeking talks with Washington, raising hopes for de-escalation. However, Iran denied those reports and launched missile strikes on Israel early Thursday, dampening risk sentiment.

Meanwhile, billionaire hedge fund manager Ray Dalio renewed his criticism of Bitcoin, arguing it should not be compared with gold because it lacks central bank backing, offers limited privacy, and could be vulnerable to advances in quantum computing. Speaking on a podcast, the Bridgewater Associates founder said Bitcoin remains small relative to gold as a monetary asset and questioned its reliability as a safe haven.

Despite his skepticism, Dalio noted in 2025 that he maintains a 1% allocation to Bitcoin in his portfolio and previously suggested investors consider holding around 15% in either Bitcoin or gold amid concerns about the U.S. debt situation.

In corporate news, Intercontinental Exchange—the owner of the New York Stock Exchange—acquired a minority stake in crypto exchange OKX in a deal valuing the platform at roughly $25 billion. As part of the agreement, ICE will license OKX’s spot crypto pricing data and intends to launch U.S.-regulated futures contracts tied to those prices.

Subject to regulatory approval, ICE’s U.S. futures products and tokenized NYSE-listed equities could also become available on OKX’s platform. Financial terms of the investment were not disclosed, though ICE will receive a seat on OKX’s board.

Across the broader crypto market, prices moved slightly higher on Thursday, following Bitcoin’s gains as the sector recovered part of last month’s losses. Ether rose about 2% to $2,123.34, while XRP gained more than 1% to $1.43. Solana, Cardano, and BNB also recorded modest increases. Among memecoins, Dogecoin traded flat, while the $TRUMP token declined around 2%.

Bitcoin was little changed on Wednesday, drawing modest support after Donald Trump called for stronger regulatory backing of the crypto sector.

Still, lingering concerns over the escalating U.S.-Iran conflict—and its potential inflationary fallout—kept broader digital asset markets under pressure, capping what had been a brief rebound earlier in the week.

Bitcoin was flat at $68,147.8 as of 01:30 ET (06:30 GMT). The token had briefly climbed back toward $69,000 earlier this week before surrendering part of those gains.

Trump targets banks over crypto legislation

In a Tuesday evening social media post, Trump accused major U.S. banks of attempting to weaken the GENIUS Act—legislation regulating stablecoins—by delaying progress on the CLARITY Act in the Senate. The latter bill aims to establish a broader regulatory framework for crypto markets.

Trump argued that record bank profits should not come at the expense of the administration’s crypto agenda, warning that failure to pass the CLARITY Act could drive innovation overseas. He urged banks to support, rather than obstruct, efforts to formalize rules for the industry.

According to reports, Trump met privately with Brian Armstrong, CEO of Coinbase, shortly before issuing his remarks. Armstrong has opposed a full ban on yield payments for stablecoins.

The GENIUS Act, passed in June 2025, prohibits issuers such as Tether from directly paying yields to holders. However, third-party platforms like exchanges may still offer such returns—an arrangement banking groups argue creates a regulatory loophole.

The CLARITY Act, approved by the House in July but still awaiting Senate passage, has faced delays largely due to disagreements over whether stablecoin yield payments should be regulated similarly to bank interest payments.

Altcoins muted amid geopolitical strain

Broader crypto markets traded within a narrow range on Wednesday. While optimism over potential U.S. regulatory clarity provided some support, investor sentiment remained constrained by ongoing tensions in the Middle East.

With the U.S., Israel, and Iran conflict entering its fifth day, fears of supply disruptions—particularly in global oil markets—have fueled inflation concerns. Persistent price pressures could prompt major central banks to maintain a hawkish stance, dampening appetite for risk assets, including cryptocurrencies.

Among major tokens, Ethereum fell 1% to $1,979.99, while XRP slipped 0.2% to $1.3594. Solana and BNB were little changed, while Cardano declined 3%. In the meme coin segment, Dogecoin dropped 2.6%, and TRUMP slid 3.4%.

Bitcoin rebounded on Monday, recovering from losses triggered by U.S. strikes on Iran over the weekend. The cryptocurrency’s advance mirrored a broader recovery in equity markets.

The world’s largest digital asset was up 5.7% at $69,428.4 as of 16:40 ET (21:40 GMT).

Bitcoin rebounds after weekend selloff

Bitcoin had dropped sharply after coordinated U.S. and Israeli military operations in Iran reportedly resulted in the death of Supreme Leader Ayatollah Ali Khamenei, marking one of the most severe regional escalations in recent years.

Iran responded with several waves of missile attacks targeting Israeli and U.S. military facilities.

Following the initial strikes, Bitcoin tumbled to around $63,000 before stabilizing and beginning to recover.

According to Dessislava Ianeva, analyst at Nexo Dispatch, Bitcoin held relatively steady as markets evaluated the evolving U.S.–Iran situation. While prediction markets remain split on the likelihood of further escalation, the limited price reaction indicates investors currently see the conflict as a contained, short-term risk rather than the beginning of a sustained downturn.

President Donald Trump stated Monday that the military operation had four key goals: dismantling Iran’s missile capabilities, destroying its navy, preventing the country from acquiring nuclear weapons, and stopping Tehran from supporting and directing terrorist activities.

“We’re already well ahead of schedule, but whatever time is required, that’s fine. We’ll do whatever it takes,” Trump said, adding that although initial projections suggested four to five weeks, the U.S. has the capacity to extend operations significantly if necessary.

Strategy adds $204 million in Bitcoin

Michael Saylor’s company Strategy expanded its Bitcoin holdings last week, purchasing 3,015 BTC valued at approximately $204.1 million, at an average price of about $67,700 per coin.

Following the acquisition, Strategy’s total Bitcoin holdings increased to 720,737 BTC, accumulated at a total cost of roughly $54.77 billion — averaging about $75,985 per Bitcoin.

Strategy remains the largest publicly traded corporate holder of Bitcoin, having steadily built one of the most substantial corporate crypto treasuries.

Altcoins track Bitcoin higher

Most major altcoins also moved higher alongside Bitcoin.

Ethereum, the second-largest cryptocurrency, climbed 6% to $2,045.01. XRP gained 2.9% to $1.3936, while Solana and Cardano rose 5.7% and 2.2%, respectively.

The U.S. dollar initially strengthened against the Canadian dollar over the course of the week, but has since pulled back and is now showing signs of indecision. This isn’t particularly surprising, given that the pair has been fluctuating within the same range for the past five weeks. Notably, the 1.3550 level continues to serve as solid support, while the 1.3750 area above remains a key resistance zone.

For longer-term traders, the prudent approach is likely to wait for a decisive breakout in either direction. In the meantime, short-term participants may keep trading the range, especially as the interest rate differential between the two currencies continues to narrow, encouraging back-and-forth price action.

EUR/USD

The euro has traded in a choppy, sideways manner throughout the week, much like the U.S. dollar against the Canadian dollar. The interest rate differential between the euro and the dollar is relatively modest, with the European Central Bank expected to hold rates steady while the Federal Reserve may move toward cutting them.

In this kind of environment, traders are searching for a catalyst to drive price in either direction. At the moment, the 1.18 level appears to be acting as a magnet, drawing price back toward it as the market struggles to establish a clear trend.

USD/MXN

The U.S. dollar moved higher against the Mexican peso over the week, which isn’t particularly surprising given how sharply it had declined beforehand. If the pair continues to rebound, the 17.50 level is likely to attract selling pressure, making it a potential area to consider short positions.

A sustained break above 18.00 would be needed before entertaining the idea of a broader trend reversal. For now, the interest rate differential continues to favor the downside, so the pair is often used to collect positive swap. I rarely look to buy this market, though sharp upside moves can occur and prove highly profitable—typically driven by strong momentum or bouts of risk aversion, which tend to override the yield advantage.

BTC/USD

Bitcoin has been highly volatile throughout the week, with price action continuing to revolve around the $60,000 level. This area is drawing significant attention, as a decisive break below it could pave the way for a swift move toward the $50,000 region.

A break above the $72,000 level would open the door for a potential rally toward $84,000. However, at this stage, the more likely scenario appears to be continued sideways consolidation. In fact, the longer Bitcoin trades within a range and builds a base, the healthier the overall structure becomes, potentially setting the stage for a more sustainable move higher later on.

USD/JPY

The U.S. dollar edged higher against the Japanese yen over the week, though the ¥158 level continues to act as resistance. At this point, traders seem to be searching for a catalyst strong enough to push the pair beyond the key ¥160 threshold.

A sustained move above ¥160 could trigger a significant rally, as that area marks the major swing high dating back to 1990. In the meantime, short-term pullbacks are likely to be viewed as buying opportunities, supported by the wide interest rate differential and Japan’s heavy debt burden, which limits the scope for materially higher domestic rates.

DAX

The German equity market has been somewhat erratic, with the DAX moving back and forth, though overall activity has been relatively subdued. The 25,000-euro level remains a key focus, as it represents a major round number with strong psychological significance. In the near term, minor pullbacks are likely to be viewed as buying opportunities.

There is also the potential for a push above the 25,400 level. A decisive breakout there could pave the way for a move toward the 27,000-euro region. At this stage, I have no interest in shorting the DAX, as the German economy appears to be supported by substantial government stimulus measures.

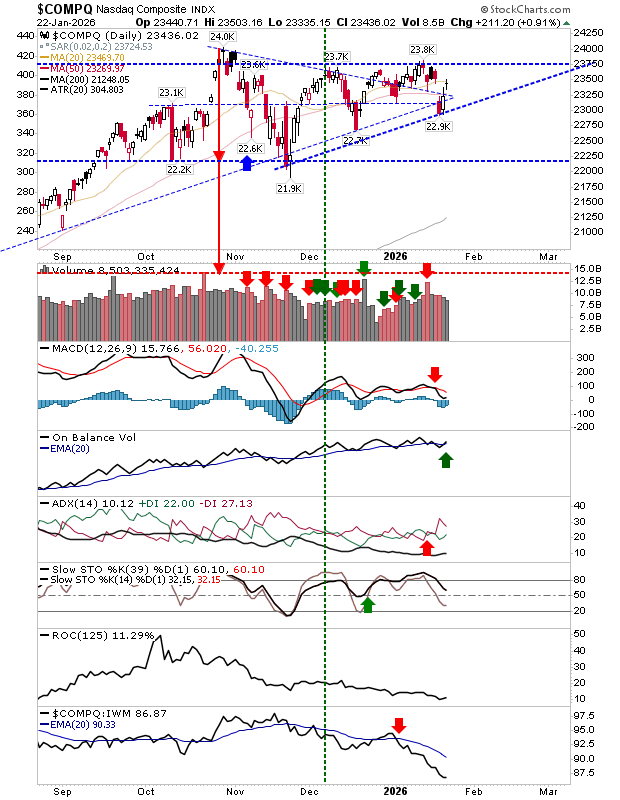

NASDAQ 100

The Nasdaq 100 has experienced significant volatility throughout the week. Despite ongoing challenges and heavy selling pressure in major stocks such as Nvidia, the index is set to close the week in relatively steady shape. The 25,000 level remains a key focus, as it represents a major psychological milestone.

A decisive move above 25,000 could open the door to the 25,500 area, which may act as the next resistance barrier. Overall, the broader outlook remains constructive, with short-term pullbacks likely presenting buying opportunities.

Meanwhile, the U.S. dollar has continued to weaken against the Swiss franc over the past week, making this currency pair one to monitor closely.

USD/CHF

The U.S. dollar has edged lower against the Swiss franc over the past week, making the pair particularly important to monitor. Swiss officials have expressed concern about the franc’s strength, which adds another layer of sensitivity to current price movements.

The 0.76 level appears to be providing near-term support, and the market will be watching closely to see whether it holds. A breakdown below that area could open the way toward the 0.75 level. Over the longer term, there is a strong possibility that the Swiss National Bank may step in to curb further franc appreciation, though any intervention would more likely begin in the euro–Swiss franc pair rather than in USD/CHF itself.

Bitcoin (BitfinexUSD) is rebounding from its weekend slide, trading above the $67,000 mark as investors process a dramatic shift in Middle Eastern geopolitics.

The bounce comes after intense volatility sparked by coordinated U.S. and Israeli strikes on Iran. President Donald Trump stated that the operation led to the death of Supreme Leader Ayatollah Ali Khamenei. Although Tehran initially rejected the reports, Iranian state media later confirmed his death, triggering sharp reactions across global financial markets.

As highlighted in Saturday’s analysis, Bitcoin has a consistent pattern of sharply dropping on unexpected geopolitical shocks before stabilizing. That pattern appears to be unfolding again. After falling to nearly $63,000 yesterday, the cryptocurrency has gradually attracted renewed capital flows as the initial wave of panic selling eases.

Ethereum and XRP are also participating in the broader recovery. ETH/USD has moved back toward the $2,000 level, while XRP is trading near $1.40, with investors anticipating a key March 1 deadline that could bring greater regulatory clarity in the United States.

Regime change dynamics and shifting sentiment

Khamenei’s death was a decisive and largely unforeseen development. The swift return of buyers into Bitcoin reflects a growing belief among traders that the most severe phase of military escalation may have already passed.

At the same time, optimism is tempered by uncertainty surrounding the power vacuum in Tehran. As Iran’s highest authority for decades, Khamenei’s absence leaves open questions about the country’s leadership transition and broader regional stability.

President Trump’s remarks encouraging Iranians to “reclaim their country” indicate that Washington may be aiming for structural regime change. For crypto investors, the coming days represent a critical period of observation. If Iran manages a controlled leadership transition without broadening the conflict, Bitcoin’s rebound could remain intact. However, a drawn-out internal or regional confrontation could quickly pressure the $67,000 support level once more.

Escalation risks and Bitcoin’s “safe haven” debate

Despite the recovery, the possibility of a wider regional conflict persists. Iran’s Revolutionary Guards have reportedly carried out strikes against neighboring states hosting U.S. forces, and casualties have been reported following retaliatory action involving Israel. This ongoing cycle of retaliation continues to unsettle institutional crypto participants.

The central issue now is whether Bitcoin can genuinely function as a “digital gold” hedge during geopolitical crises — or whether it will keep behaving like a high-beta technology asset that reacts sharply to shifts in global risk sentiment.

Indices: Tech Drags as Futures Edge Lower Before PPI

U.S. equity futures slip slightly after a weak session led by semiconductor losses. The tech-heavy Nasdaq 100 (-1.2% to 25,034) paced declines, followed by the S&P 500 (-0.5% to 6,908), while the Dow 30 (flat at 49,499) avoided closing in the red. Treasury yields eased across the curve, with the 10-year hovering near the 4% threshold, as investors await January PPI data. CME FedWatch pricing still points to rate cuts in July and October as the base case.

Stocks: Chip Selloff; Media Takeover Saga Nears Conclusion

Nvidia (-5.5%) slid despite beating earnings and revenue expectations, dragging the broader semiconductor space lower, including AMD (-3.4%), Intel (-3%), and ASML (-4.1%).

The contest for Warner Bros Discovery (-1.7% AH) appears to be wrapping up, with Netflix (+8.5% extended) stepping aside after Paramount Skydance (+10% close; +6.2% AH) presented a stronger bid.

Block (+23.6%) surged in extended trading after earnings and announcing plans to cut over 4,000 jobs.

IonQ (+21.7%) rallied on upbeat revenue guidance, with Morgan Stanley lifting its price target.

Meta (-0.7% AH) dipped after reports its in-house chip project faced hurdles and that it struck a deal to lease Google TPUs for AI development.

PayPal (-3.7%) declined after denying talks of a potential sale.

Meme stock movers included Beyond Meat (+2.9%), GoPro (+3.3%), Krispy Kreme (+27.8%), Opendoor (+8.6%), and BlackBerry (+2.6%).

Earnings Highlights:

Dell Technologies beat on both earnings and revenue; shares rose 11.6% after hours.

Zscaler missed on deferred revenue and billings; shares fell 9.5% AH.

Synopsys disappointed with full-year guidance; shares dropped 5.2%.

Rolls-Royce beat expectations, raised its profit outlook, and announced £2.5bn in buybacks; shares closed up 5.2%.

Baidu missed revenue forecasts; shares slid 5.7%.

Commodities:

Gold volatility eased as prices hovered near $5,200 but failed to sustain gains above that level, amid geopolitical uncertainty and a firmer dollar. Silver reclaimed $90, narrowing the gold/silver ratio below 58. The World Gold Council flagged stretched valuations.

WTI crude steadied around $65 after elevated intraday swings, with attention on Geneva talks and lingering U.S. military rhetoric. Traders are also focused on Sunday’s OPEC+ meeting amid speculation of a possible April output increase.

FX / Central Banks / Crypto:

Bitcoin retreated toward $68K, while Ether remained above $2K.

The U.S. Dollar Index firmed back into the 97 area, reversing prior losses on stronger labor data and reduced expectations for near-term Fed easing.

Fed officials offered mixed signals: Miran backed four quarter-point cuts this year, while Goolsbee cautioned against easing too quickly before inflation cools.

ECB President Lagarde reiterated inflation is expected to return to the 2% target over the medium term, emphasizing a data-dependent approach and monitoring — not targeting — FX markets.

Data: Stronger-Than-Expected Labor Figures

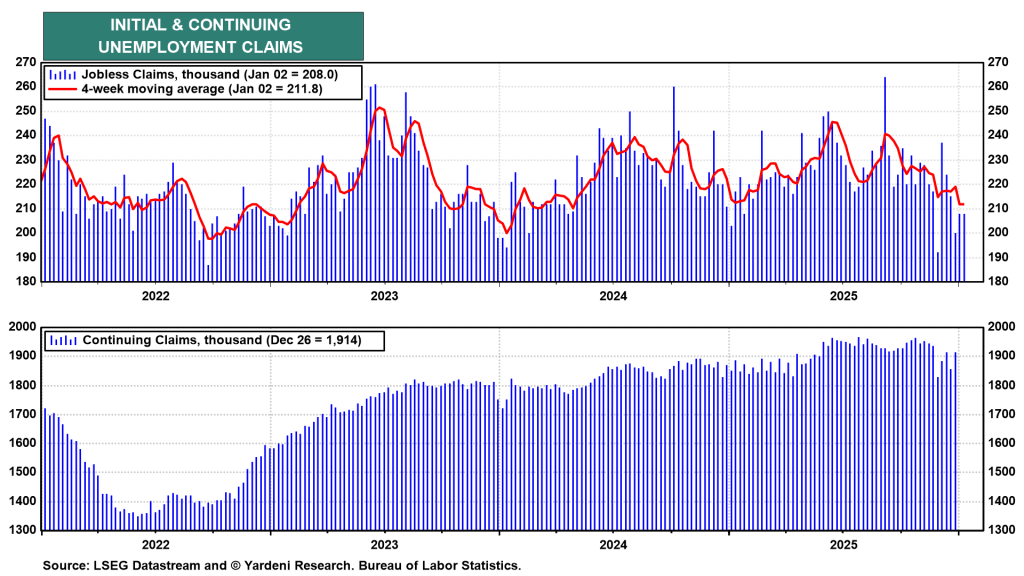

U.S. initial jobless claims came in at 212K (vs. 217K forecast), with continuing claims falling to 1.833m. Kansas Fed manufacturing improved sharply to 10 from -2.

Tokyo headline CPI rose to 1.6% y/y, though core measures eased. Retail sales rebounded 1.8% y/y, while industrial production disappointed at 2.2% growth (vs. 5.3% expected).

Ahead:

U.S. PPI, Chicago PMI, and Baker Hughes rig count data due later today.

In Europe, German preliminary CPI, import prices, and labor data.

Saturday: Earnings from Berkshire Hathaway.

Sunday: OPEC+ meeting to determine April output levels.

Bitcoin declined on Friday, halting a recovery from its midweek lows as investor risk appetite stayed weak. The world’s largest cryptocurrency is now on track for a fifth straight month of significant losses.

The broader crypto market moved largely in line with Bitcoin and is also poised for steep losses in February, as both retail and institutional investors continued to avoid the sector.

By 00:48 ET (05:48 GMT), Bitcoin was down nearly 1% at $67,788.0.

Bitcoin on track for fifth straight monthly decline

Bitcoin was down nearly 14% in February, as the risk-off sentiment in the crypto market showed little sign of easing throughout the month.

Rising geopolitical tensions worldwide, uncertainty surrounding major global economies, and concerns over further disruptions from U.S. trade tariffs kept investors cautious and away from speculative assets like cryptocurrencies.

The digital asset dropped as much as 50% from its October record high earlier this month, though it has since staged a modest recovery from those lows.

Bitcoin has remained in a sustained downtrend since October, with purchases by major corporate holder Strategy doing little to stem the losses.

Strategy has also reportedly slowed its pace of Bitcoin acquisitions in recent months, amid mounting concerns that continued price declines could force the company to sell part of its holdings to service its debt.

MARA Holdings jumps as AI deal eclipses weak Q4 results

Shares of MARA Holdings — previously known as Marathon Digital (NASDAQ: MARA) — surged Thursday evening after the Bitcoin mining company revealed a partnership with Starwood Capital to repurpose several of its mining facilities into artificial intelligence data centers. The stock climbed as much as 17% in after-hours trading.

The announcement helped eclipse a steep $1.7 billion loss in the fourth quarter, driven by an extended slump in Bitcoin prices that severely pressured the firm’s mining profitability. Revenue also came in below expectations.

Amid continued weakness in Bitcoin and growing investor enthusiasm around AI, MARA has recently been shifting strategy, aiming to redeploy its computing infrastructure toward AI data center operations rather than focusing solely on cryptocurrency mining.

Crypto prices today: Altcoin recovery fades, February losses loom

Crypto markets retreated on Friday, giving back much of this week’s brief rebound, with most tokens on track to post steep declines for February.

The world’s second-largest cryptocurrency, Ethereum, slipped 1.2% to $2,038.21 and was heading for a monthly drop of nearly 17%. The token faced additional pressure after co-founder Vitalik Buterin sold more of his holdings, reinforcing cautious sentiment across the market.

XRP fell 2.3% and was poised to lose around 15% in February, while BNB held steady on Friday but remained down close to 20% for the month.

Solana was also nursing losses of roughly 17% in February, whereas Cardano traded largely unchanged. In the meme coin segment, Dogecoin declined 5.4% for the month, while Official Trump tumbled about 20% over the same period.

Bitcoin’s latest decline is unfolding amid mounting macroeconomic headwinds and crypto-specific pressures, fueling fears that the downtrend could deepen, with some analysts eyeing a potential floor near $45,000.

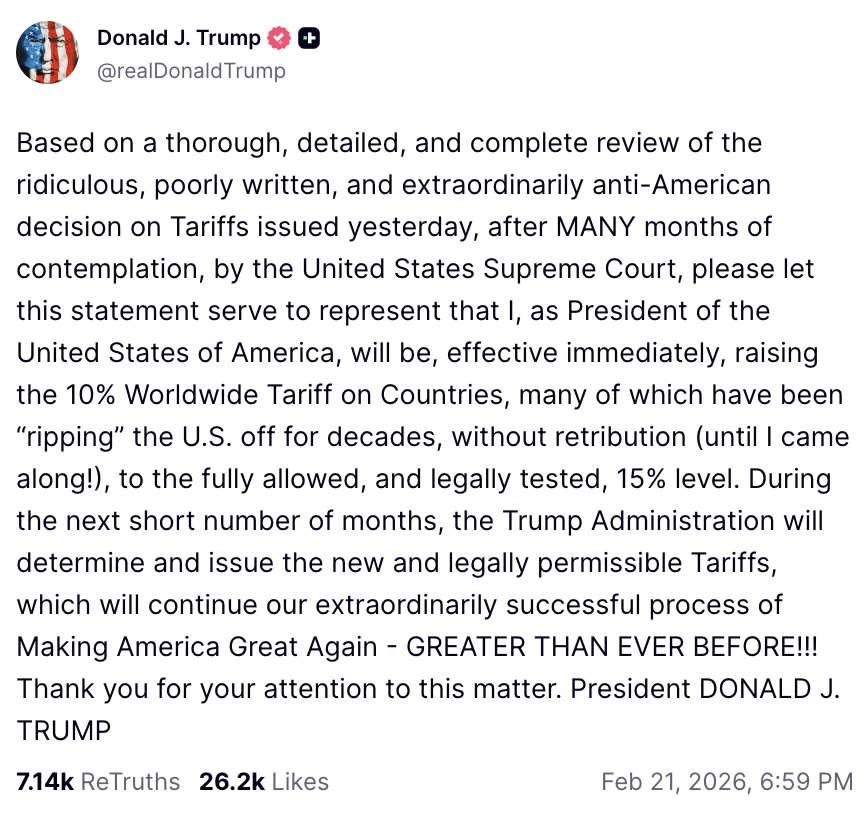

Trump’s 15% Global Tariff Weighs on BTC

On Saturday, February 21, US President Donald Trump unveiled a 15% blanket tariff on imports, jolting global financial markets — cryptocurrencies included. The move followed a decision by the US Supreme Court to overturn his earlier sweeping tariff measures. The revised levy, initially proposed at 10% before being lifted to 15%, officially comes into force today, February 24, 2026.

Activated under Section 122 of the Trade Act of 1974, the new tariff covers the majority of imported goods for an initial 150-day period, with any extension subject to congressional approval. Although intended to narrow trade imbalances, the measure has heightened economic uncertainty, triggering a widespread retreat from risk-sensitive assets.

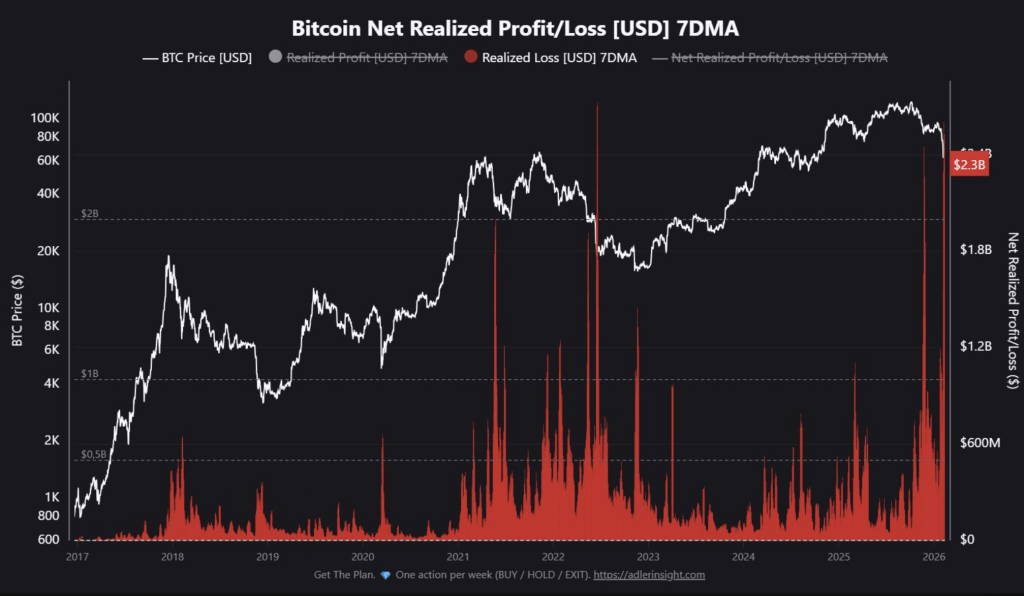

Within the crypto market, the development has reinforced a risk-off mood, as investors rotate out of volatile positions into safer havens. Bitcoin holders are increasingly realizing losses, with on-chain figures indicating more than $2.3 billion in realized losses over the past week.

Crypto analyst IT Tech described the move as one of the most significant capitulation phases in Bitcoin’s history, comparing it to the 2021 market crash, the 2022 Luna/FTX collapse, and the mid-2024 correction. In a post on X, he noted that the scale of losses ranks among the top three to five worst drawdowns ever recorded, adding that only a few moments in Bitcoin’s history have witnessed such intense capitulation.

The reaction reflects mounting concerns that higher import costs could reignite inflationary pressures, potentially forcing the Federal Reserve to delay rate cuts and keeping financial conditions tighter for longer.

Markets sold off swiftly following the announcement, with Bitcoin sliding intraday to below the $63,000 mark.

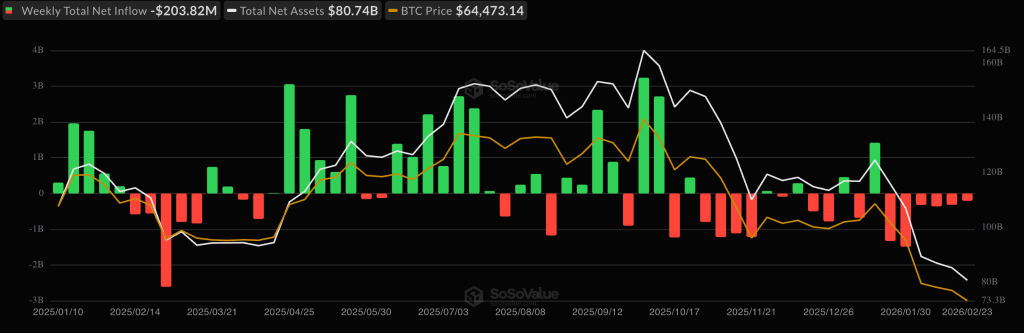

Spot Bitcoin ETFs Extend Outflow Streak to Five Weeks

Adding to the tariff-driven volatility, U.S.-listed spot Bitcoin ETFs have now recorded five consecutive weeks of net outflows — the longest stretch of withdrawals since February 2025.

Data from SoSoValue shows that nearly $3.8 billion has exited these funds over the five-week period, including $316 million in redemptions last week alone.

BlackRock’s iShares Bitcoin Trust (IBIT) accounted for the largest share of the withdrawals, losing roughly $2.1 billion during the streak. Fidelity Investments’ Fidelity Wise Origin Bitcoin Fund (FBTC) and several other products also saw notable outflows.

The sharp reversal from the strong inflows seen in late 2024 highlights a cooling in institutional appetite, as portfolio managers trim crypto exposure amid heightened macro uncertainty and broader market turbulence.

The persistent ETF withdrawals are intensifying sell-side pressure on Bitcoin, as fund managers are forced to offload underlying BTC holdings to satisfy investor redemptions.

With total net outflows reaching $4.5 billion so far in 2026, much of the earlier inflow momentum has been erased. Analysts describe the environment as a “risk-off stress test,” where macro headwinds — including tariffs and geopolitical tensions — are discouraging fresh allocations into crypto.

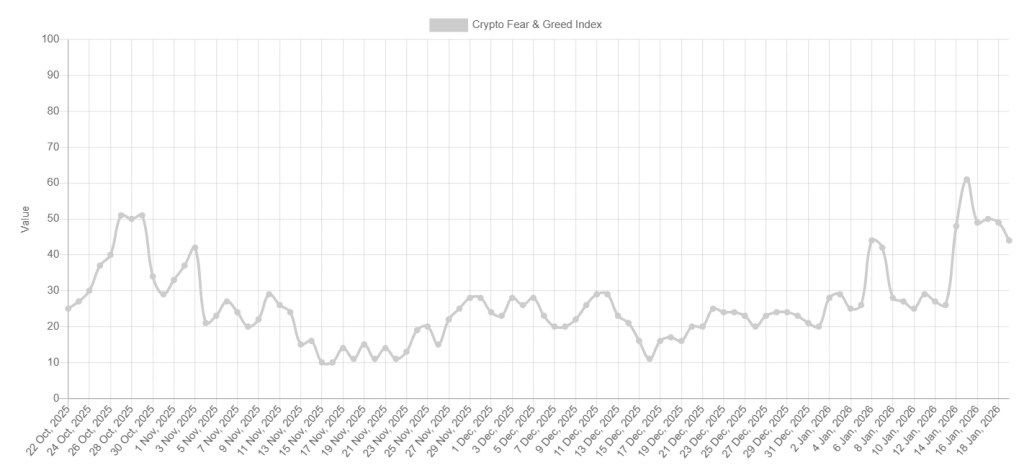

Sentiment indicators reflect the strain. The Crypto Fear & Greed Index has plunged to one of its most extreme fear readings on record, reinforcing the ongoing wave of liquidation. Unless ETF flows stabilize or reverse, downside momentum may continue, particularly if institutional distribution remains dominant.

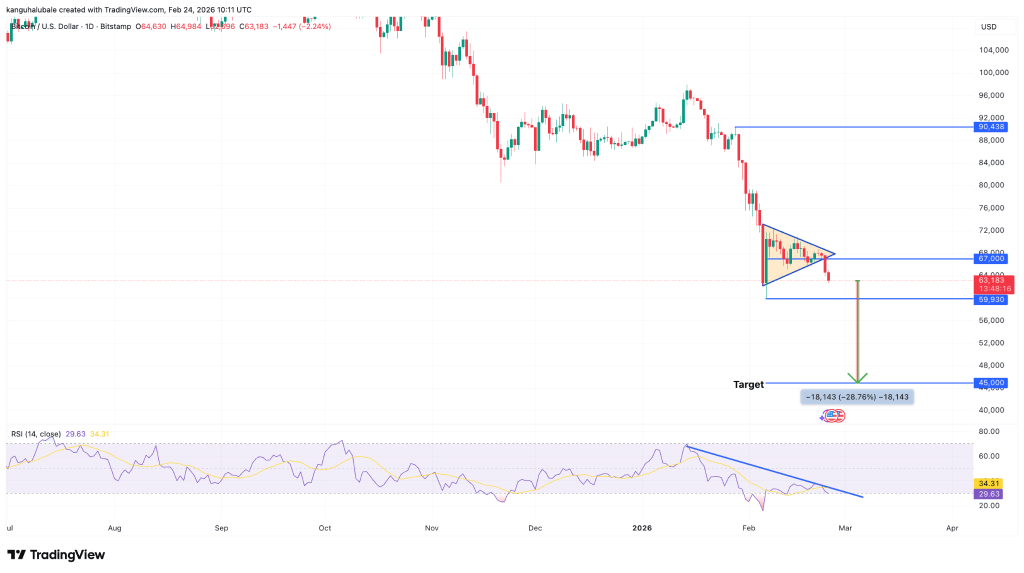

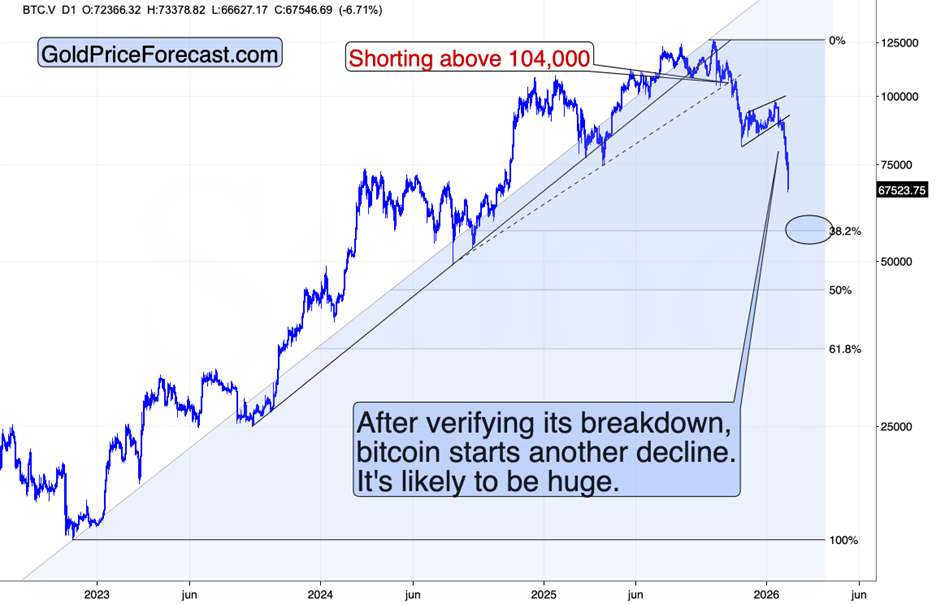

Bear Pennant Signals $45K Target for Bitcoin

From a technical perspective, Bitcoin’s chart structure remains bearish, with a well-defined bear pennant forming on the daily timeframe.

A bear pennant is a continuation pattern that follows a steep decline (the flagpole), then consolidates within a tightening symmetrical triangle before typically breaking lower.

The BTC/USD pair fell below a major support level at $80,117 — its November 2025 low — and slid to $60,000 on February 6, forming the flagpole. A rebound toward $72,000 followed, before price retreated again to around $63,100.

The pattern confirmed on Monday when Bitcoin broke beneath the pennant’s lower trendline near $67,000. Based on the measured-move technique — projecting the height of the flagpole from the breakout point — the downside target falls in the $45,000–$50,000 range.

A drop toward $45,000 would imply roughly a 28% decline from current levels, underscoring the risk of further capitulation if macro and flow dynamics fail to improve.

The bearish outlook is reinforced by strengthening downside momentum, with the RSI sliding from overbought territory near 70 on January 15 to around 29 currently — signaling growing selling pressure and near-oversold conditions.

Bitcoin continues to trade below key moving averages, keeping the broader technical structure fragile. A decisive break beneath the $60,000 threshold could intensify losses, opening the door toward the $52,450 realized price level — a historically significant support area.

On the other hand, a sustained move above $72,700 would invalidate the bear pennant setup and could shift momentum back in favor of the bulls, paving the way for a broader recovery.

Bitcoin fell again on Tuesday, deepening its recent slide and now trading roughly 50% below its October record high, as uncertainty surrounding U.S. tariff policy dampened risk appetite for digital assets.

The world’s largest cryptocurrency slipped 0.9% to $64,169.6 by 17:35 ET (22:35 GMT), after touching an intraday low of $62,650.1.

Broader crypto markets also remained under pressure, with both institutional and retail investors continuing to reduce exposure. Escalating geopolitical tensions involving Iran, along with an AI-driven selloff on Wall Street, further weighed on sentiment.

Bitcoin down 50% from peak

With Tuesday’s losses, Bitcoin is now trading about half below its early-October all-time high of $126,186.

The cryptocurrency has been in a sustained downturn since that peak, as fresh U.S. regulatory measures and ongoing purchases by major corporate holder Strategy failed to meaningfully support prices.

On Monday, Strategy revealed it had acquired an additional 592 Bitcoin. However, the firm is currently facing significant unrealized losses, as Bitcoin trades below its reported average purchase price of $76,020.

On-chain data from CryptoQuant and Coinglass indicated that large holders—commonly known as “whales”—continued transferring substantial amounts of Bitcoin to exchanges, suggesting further selling pressure.

Meanwhile, major buyers appear scarce. Data from Glassnode showed institutional investors recorded a fifth straight week of net outflows from U.S. spot Bitcoin ETFs as of Monday.

Iliya Kalchev of Nexo Dispatch noted that U.S. spot Bitcoin ETFs saw around $203 million in net outflows on Monday alone. At the same time, derivatives markets still show demand for downside hedging, while long-term holders have not signaled broad capitulation—leaving Bitcoin in what he described as a fragile balance between visible pressure and underlying structural conviction.

He highlighted the $60,000–$72,000 range as the key near-term zone. If ETF flows stabilize and macro volatility subsides, the range could form a base. But if outflows continue, focus may shift toward the realized price area near $55,000 as the next major reference point.

Tariff uncertainty adds pressure

Bitcoin’s latest weakness was largely driven by renewed uncertainty over U.S. trade policy after the Supreme Court struck down much of President Donald Trump’s tariff framework.

In response, Trump announced new universal tariffs of 15% under a different legal authority, though the initial rate implemented at midnight Tuesday was 10%. The president now faces additional legal hurdles in expanding tariffs but has shown little intention of retreating from his trade agenda, even warning that countries seeking to renegotiate trade deals could face higher duties.

Although cryptocurrencies are not directly tied to trade flows, they are highly sensitive to shifts in global risk sentiment. The uncertainty surrounding U.S. tariffs has triggered broader risk aversion across financial markets, spilling over into digital assets.

Altcoins follow Bitcoin lower

Most altcoins tracked Bitcoin’s decline, with the broader market showing little sign of relief from the ongoing downturn.

Ethereum slipped 0.1% to $1,857.78, hovering near early-February lows. XRP and BNB fell 0.2% and 1.9%, respectively, while Cardano declined 1.4%. Solana bucked the trend, rising 0.9%.

Among meme tokens, Dogecoin dropped 1.1%, while TRUMP gained 1.3%.

Bitcoin Cash slipped below the $500 mark on Tuesday, extending losses after plunging 13% in the previous session.

Hyperliquid fell another 1% on Tuesday, marking its fourth straight day of declines following Monday’s sharp 9% drop.

Pump.fun also came under pressure, sliding beneath a key psychological support level after tumbling 11% on Monday.

Altcoins such as Bitcoin Cash (BCH), Hyperliquid (HYPE), and Pump.fun (PUMP) have led declines over the past 24 hours as Bitcoin slipped below the $64,000 level on Tuesday. Technical indicators for BCH, HYPE, and PUMP point to further downside risks amid broad-based market selling.

The wider cryptocurrency market remains under strain as Donald Trump explores new legal avenues, citing national security concerns, to introduce additional tariffs. Meanwhile, U.S. equities ended Monday’s session in negative territory, adding to the cautious tone across risk assets.

CoinMarketCap’s Fear and Greed Index has dropped to 11, signaling extreme fear in the market and underscoring that sellers remain firmly in control.

Bitcoin Cash slips beneath the $500 mark

Bitcoin Cash was trading below the $500 level on Tuesday, extending losses after plunging 13% in the prior session. The altcoin has slipped beneath its 200-day Exponential Moving Average (EMA) at $544, while the 50-day EMA — now trending lower at $555 — is approaching a potential death cross formation.

Technically, the path of least resistance appears tilted to the downside, with the next key support seen around $443, corresponding to the October 17 low.

Daily chart indicators reinforce the bearish momentum shift. The Relative Strength Index (RSI) has dropped to 36, edging closer to oversold territory as selling pressure intensifies. Meanwhile, the Moving Average Convergence Divergence (MACD) has crossed below its signal line, signaling a bearish crossover.

BCH/USDT

If Bitcoin Cash reclaims the $500 psychological barrier with a strong daily close above it, selling pressure could begin to fade, potentially paving the way for a rebound toward the 200-day EMA near $544.

Hyperliquid was trading below $26 on Tuesday, extending losses after falling 9% in the previous session. The HYPE token has now declined for a fourth straight day and remains well under both its 50-day EMA at $29.08 and 200-day EMA at $32.37, reinforcing a bearish outlook.

On the daily chart, the Relative Strength Index (RSI) stands at 38 and continues to trend lower, with further room before entering oversold territory. Meanwhile, the Moving Average Convergence Divergence (MACD) and its signal line are steadily declining, with widening bearish histogram bars signaling strengthening downside momentum.

Immediate support levels are seen at $23.58, marking the December 21 low, followed by $20.82, the October 10 low.

HYPE/USDT

On the upside, Hyperliquid would need to break back above its 50-day EMA at $29.08 to revive short-term bullish momentum and signal the start of a potential recovery.

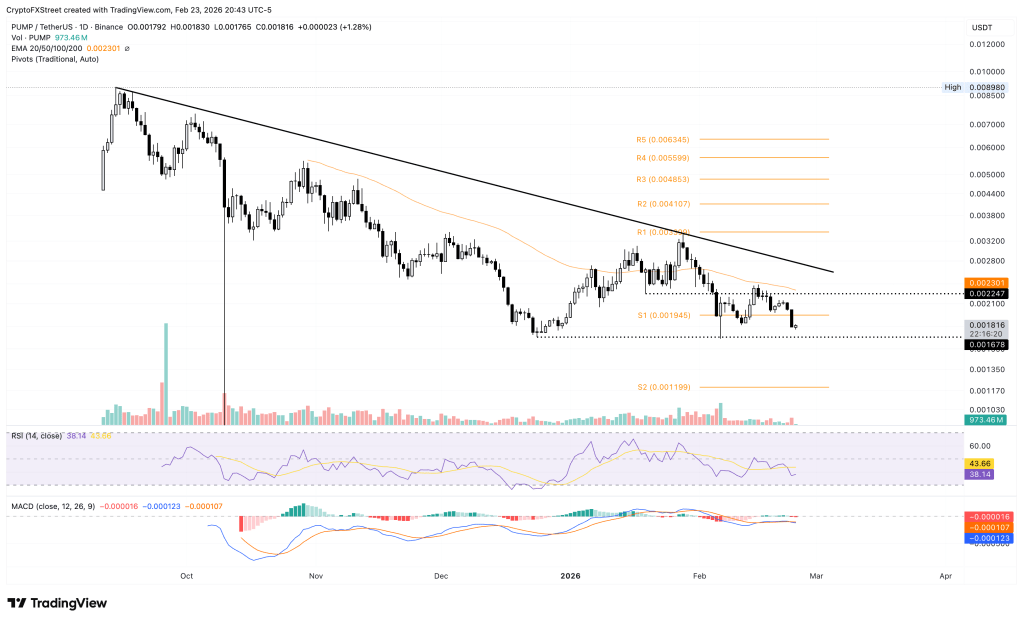

Pump.fun slides toward all-time low amid heavy selling

Pump.fun was trading around $0.001800 at the time of writing on Tuesday, after tumbling 11% in the previous session. The meme-coin launchpad token has continued its broader downtrend since late September and is now eyeing support at $0.001678 — a level that previously sparked a rebound on February 6.

A firm break and close below this support could open the door to further losses toward the S2 pivot at $0.001199.

Momentum indicators point to mounting downside pressure. The Relative Strength Index (RSI) sits at 37, hovering just above oversold territory and reflecting persistent selling interest. Meanwhile, the Moving Average Convergence Divergence (MACD) and its signal line have resumed a downward trajectory following a bearish crossover on Monday, indicating renewed negative momentum.

PUMP/USDT

If Pump.fun climbs back above the S1 pivot at $0.001945, it may pave the way for a move toward the 50-day EMA near $0.002300, potentially easing near-term bearish pressure.

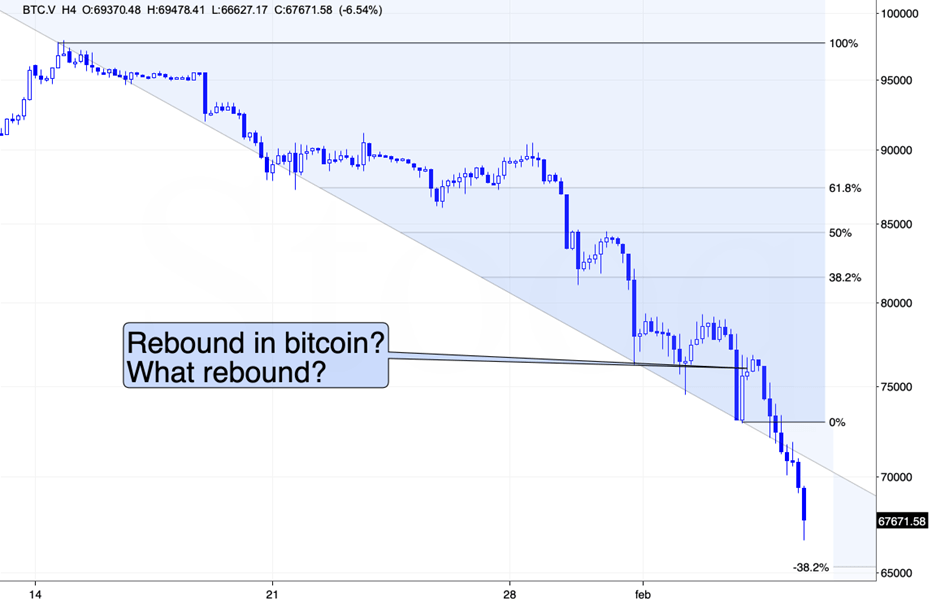

Bitcoin falls beneath the lower boundary of its consolidation range on Monday, and a decisive close below this level could open the door to a more pronounced correction.

Ethereum drops under $1,900, marking a continuation of its six-week decline.

XRP dips below $1.40, unable to hold support at the lower edge of its trendline channel.

Bitcoin (BTC), Ethereum (ETH), and Ripple (XRP) continue to weaken on Monday after posting modest losses last week. BTC has slipped beneath the $65,000 consolidation floor, while ETH has fallen under $1,900, both marking a sixth consecutive week of declines. Meanwhile, XRP drops below $1.40, failing to hold support at its lower trendline — collectively signaling the risk of a deeper correction across the top three cryptocurrencies.

Bitcoin breaks below consolidation support

Bitcoin had been trading within a sideways range between $65,729 and $71,746 since February 7. On Monday, BTC moved below the lower boundary of this range, changing hands near $64,700.

A confirmed daily close beneath $65,729 would strengthen the bearish case and could open the path toward the next major support around $60,000.

On the daily chart, the RSI stands at 31, hovering close to oversold territory and reflecting strong downside momentum. Meanwhile, the MACD lines are tightening, suggesting growing indecision in the market.

BTC/USDT

However, if BTC manages to reclaim and hold above the $65,729 level, a rebound toward the upper boundary of the range at $71,746 remains possible.

Ethereum extends its correction

Ethereum continued to edge lower last week, prolonging its slide that began in mid-January. As of Monday, ETH is down 4.77%, trading around $1,864.

A daily close beneath the lower consolidation boundary at $1,747 would reinforce the bearish outlook and could drive prices toward the next key support at $1,669.

Similar to Bitcoin, Ethereum’s RSI points to strengthening downside momentum, while the MACD lines are narrowing, reflecting growing uncertainty among market participants.

ETH/USDT

On the flip side, a recovery from current levels could see ETH rebound toward the upper end of its consolidation range near $2,149.

XRP deepens its pullback after breaking below key lower trendline support.

XRP is hovering below $1.40 on Monday after slipping beneath the lower boundary of a falling wedge pattern.

Should the pullback persist, the token may slide further toward the weekly support around $1.30.

Similar to Bitcoin and Ethereum, XRP’s RSI points to building bearish pressure, while the MACD lines are tightening, signaling trader uncertainty.

XRP/USDT

On the other hand, if price manages to reclaim and hold the lower trendline as support, a rebound toward the psychological $1.50 level could follow.

The US dollar at one stage surged sharply against the Mexican peso, but by week’s end it had given back some of those gains. The 17.00 area below continues to act as a key support zone, and a decisive break beneath it could open the door for a move toward 16.50.

While short-term bounces are possible, the broader setup suggests selling into strength. The 17.50 region remains a significant resistance barrier, and the wide interest rate differential still strongly favors the Mexican peso.

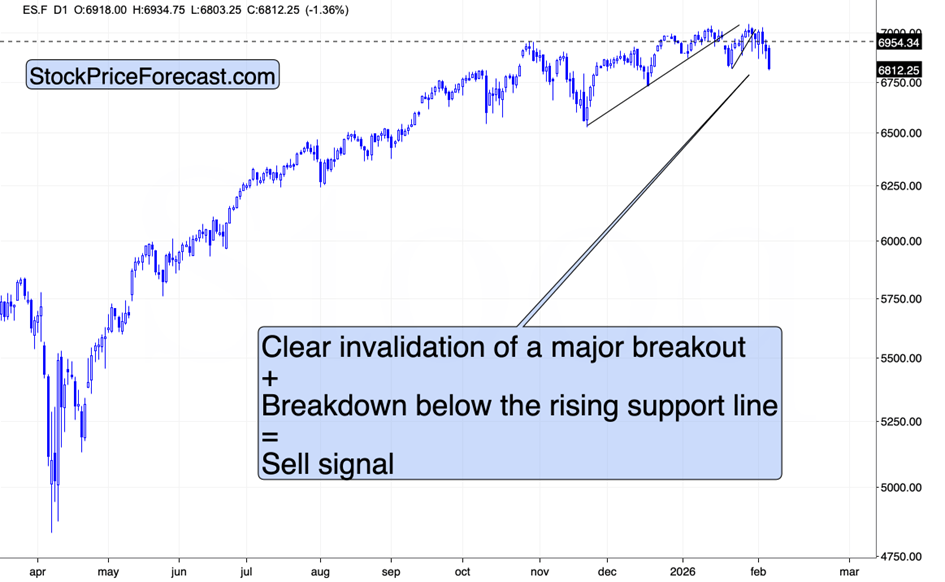

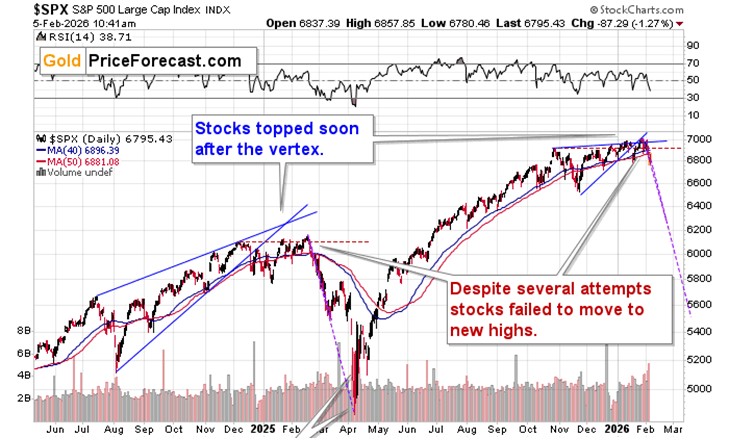

S&P 500

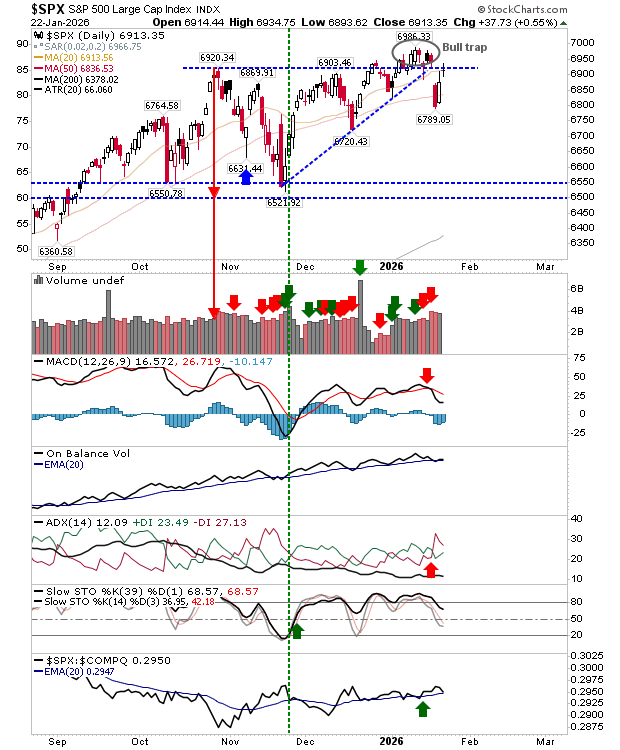

The S&P 500 pulled back early in the week but appears to be stabilizing as it continues to trade within a broader consolidation range. Since early December, price action has been confined between 6,800 and 7,000, suggesting a market building momentum for its next major move.

The bias still leans to the upside. A decisive daily close above 7,000 could trigger a stronger breakout and accelerate gains. On the other hand, a breakdown below 6,800 would signal a shift in tone and mark a more bearish development.

EUR/USD

The euro declined notably over the course of the week, but it continues to find buyers near the 1.18 level, making that area especially important to watch. Given the current structure, caution is warranted when trading this pair.

Price action appears largely range-bound, with 1.18 acting as a central pivot or magnet. Resistance stands near 1.1850, while solid support can be found around 1.1750, reinforcing the broader sideways pattern.

USD/CAD

The US dollar has advanced against the Canadian dollar, but price action remains choppy around the 1.3750 zone — an area that has repeatedly proven significant. The pair appears to be oscillating as traders assess whether momentum can build for a sustained move higher.

A decisive push and hold above 1.3750 would signal renewed strength for the US dollar. Conversely, a breakdown below 1.35 would represent a notably bearish shift in sentiment.

Major Technical Support and Resistance Levels

Gold (XAU/USD)

Gold remains choppy, initially easing back during the week, yet buyers continue to emerge on dips, stepping in whenever prices soften. The 4,800 level appears to be firm support, while the 5,000 mark is likely to act as a psychological magnet for price action.

The broader bias still favors buying pullbacks, with the expectation of an eventual move higher. However, volatility may persist after the sharp turbulence seen in recent weeks, following what had previously been a near one-way surge. Over the longer term, a retest of the highs seems plausible, though it will likely require patience amid ongoing fluctuations.

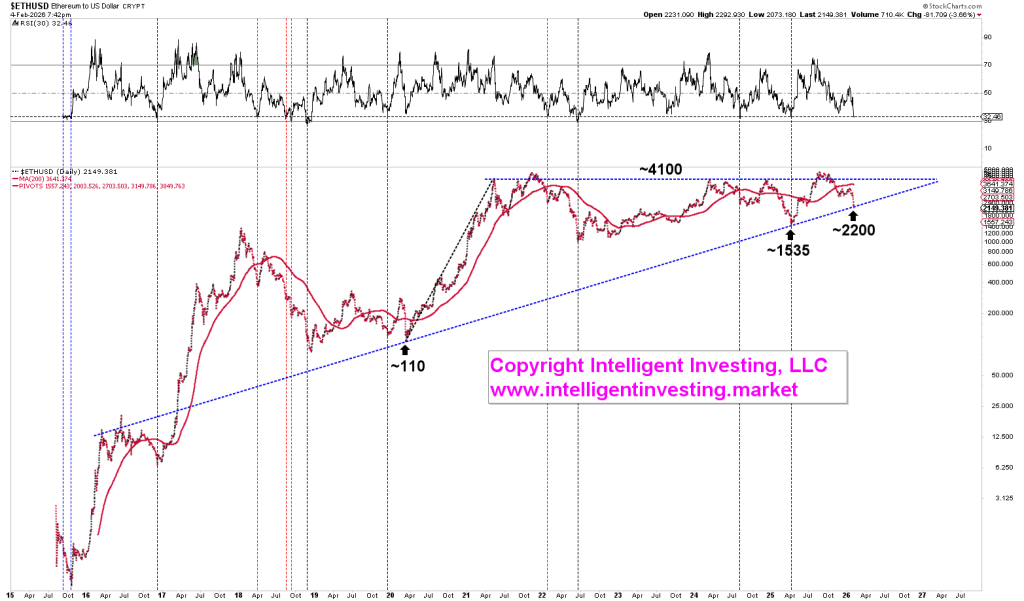

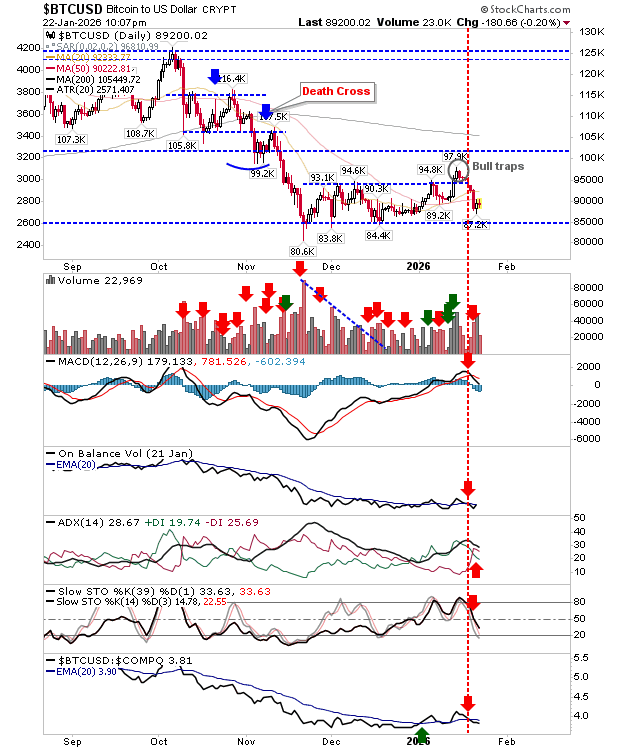

Bitcoin (BTC)

The Bitcoin market is still searching for renewed upside momentum, but the encouraging development is that price action has at least stabilized. Given the prolonged weakness seen in recent periods, simple stability is a constructive step forward for the market.

The $60,000 level remains a crucial support zone and a major psychological benchmark. Holding above this area is essential if Bitcoin is to maintain any realistic prospect of a sustained recovery.

USD/JPY

The US dollar posted solid gains against the Japanese yen over the week, with the ¥152 level continuing to provide strong support. The 50-week EMA is positioned just beneath that area, reinforcing the floor and encouraging dip-buying as the interest rate differential remains in favor of the US dollar.

With the Bank of Japan maintaining its current policy stance, there appears to be little immediate catalyst for a structural shift. As a result, the pair may be entering a consolidation range between ¥152 on the downside and ¥158 on the upside. A decisive move above ¥160 would represent a significant breakout, clearing a resistance zone that has been in place since 1990.

GBP/USD

The British pound declined sharply during the week, dropping to test the 1.35 level — a large, round psychological threshold that has proven important on multiple occasions. The fact that buyers are attempting to defend this area is at least a constructive short-term signal.

However, recent UK economic data has been somewhat underwhelming. As a result, sterling may currently be one of the weaker major currencies against the US dollar. This pair deserves close monitoring, as broader dollar strength could translate into pronounced downside pressure here, potentially making GBP/USD particularly vulnerable.

Cryptocurrency markets moved within a tight range late in the week as traders remained cautious ahead of important U.S. inflation and growth releases. According to Nexo analyst Iliya Kalchev, broader macro uncertainty continues to guide investor sentiment.

Bitcoin held just above the $68,000 mark, while Ethereum struggled to push past $2,000, signaling selective positioning rather than a broad return to risk appetite. A more guarded macro tone has emerged in recent days, with hawkish cues from the Federal Reserve’s January meeting minutes pressuring risk assets and strengthening the view that interest rate cuts may come later than previously anticipated.

Geopolitical concerns have further shaped market behavior. Heightened tensions involving the U.S. and Iran have driven demand for traditional safe havens such as the U.S. dollar and gold, while capping gains in liquidity-driven assets like cryptocurrencies.

Kalchev highlighted that U.S.-listed Bitcoin ETFs posted around $165 million in net outflows, and Ethereum ETFs saw roughly $130 million withdrawn. These flows reflect a broader sense of institutional caution as investors recalibrate exposure amid persistent macro volatility.

Bitcoin remains in a consolidation phase following its early-February pullback, even as underlying network metrics improve. Mining difficulty has risen notably, and hashrate levels have recovered, pointing to structural strength despite muted price action. Still, analysts note that the asset remains highly responsive to macro signals—particularly inflation data that could influence Federal Reserve policy expectations.

Outside of crypto, financial markets have displayed uneven risk appetite. Gold is trading near record highs, and the dollar is on course for a strong weekly advance as investors hedge against geopolitical instability and interest rate uncertainty.

Looking ahead, market participants are closely watching upcoming U.S. Core PCE inflation data and GDP figures. These releases could determine whether digital assets break out of their current consolidation range or continue moving sideways. While regulatory progress on stablecoin legislation may serve as a longer-term structural driver, Kalchev emphasized that near-term price movements will likely remain tied to macro developments and investor positioning.

Bitcoin edged higher on Friday, drawing some support from dip-buying after recent losses, though overall sentiment toward cryptocurrencies remained weighed down by uncertainty over U.S. interest rates and rising geopolitical tensions.

The world’s largest digital asset was still on track for a weekly decline, as a short-lived rebound from last week quickly lost momentum. Bitcoin has also fallen roughly 25% so far in 2026.

Bitcoin climbed to $67,843.1 by 01:21 ET (06:21 GMT). Despite the modest uptick, it was down 2.8% for the week and poised to register losses in five of the past seven weeks.

Rate uncertainty intensifies ahead of PCE, GDP data

Bitcoin and the broader crypto market extended declines this week as demand for speculative assets weakened amid growing doubts about the U.S. rate outlook.

Concerns escalated after minutes from the Federal Reserve’s January meeting revealed that several policymakers supported keeping the door open to further rate hikes to counter inflation risks — a backdrop that typically pressures high-risk assets.

A string of mixed inflation and labor market reports has further clouded expectations for monetary policy. Cryptocurrencies are particularly sensitive to higher interest rates, as they tend to perform better in environments flush with liquidity.

Investors are now awaiting December’s Personal Consumption Expenditures (PCE) price index — the Fed’s preferred inflation measure — due later Friday, along with fourth-quarter gross domestic product data, both of which could shape longer-term rate expectations.

Iran tensions dent risk appetite

Risk sentiment was also dampened by escalating geopolitical strains between the U.S. and Iran. President Donald Trump reiterated threats of military action if Tehran fails to agree to a nuclear deal, while multiple reports indicated Washington is weighing several military options and has increased its regional presence.

The heightened tensions curbed appetite for riskier assets such as Bitcoin, prompting some traders to favor traditional safe havens including the U.S. dollar and gold.

Altcoins head for weekly losses

Broader crypto markets traded in a narrow range on Friday, with most major altcoins also facing another week of declines.

The second-largest cryptocurrency, Ethereum, slipped 1.5% to $1,954.09 and was set for a 6.2% weekly drop.

XRP and BNB were down around 6% and 3% for the week, respectively, while Cardano and Solana were on track for losses of roughly 5% to 7%.

Among meme tokens, Dogecoin was headed for an 11% weekly decline.

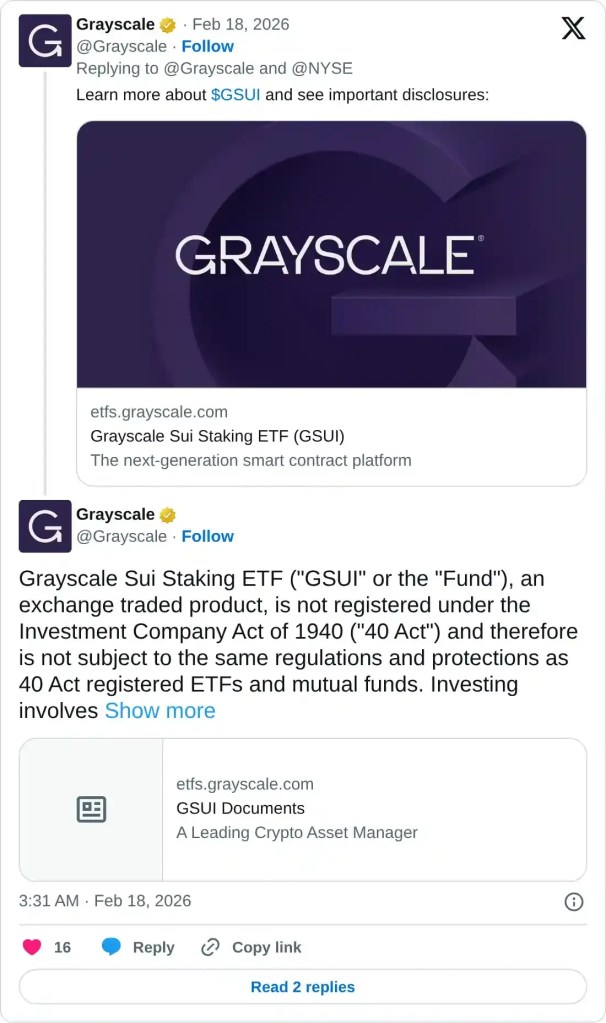

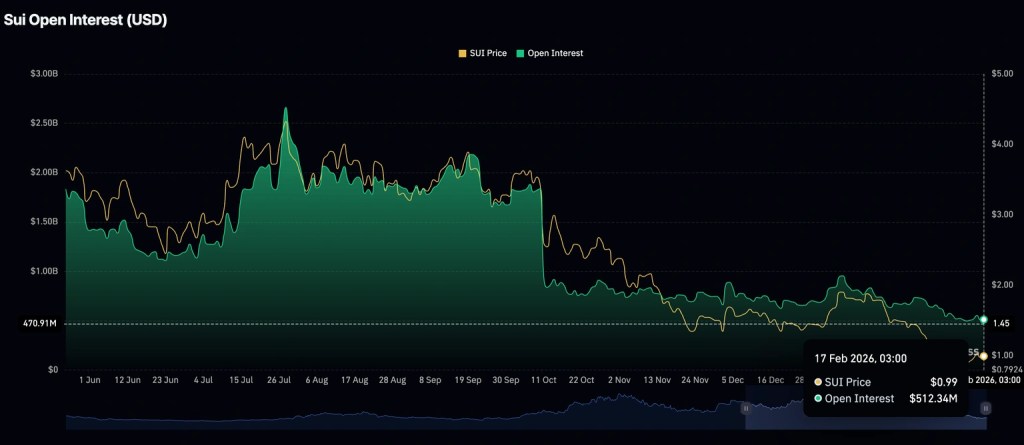

Sui remains under pressure near $0.96 as its technical outlook continues to weaken. The upcoming launch of the Grayscale Sui Staking ETF on Wednesday will give investors exposure to the Sui Network’s native token. However, subdued retail participation — with futures Open Interest hovering just above $500 million — could restrain any meaningful breakout attempt.

Sui (SUI) has extended its decline for a second straight session, trading around $0.95 at the time of writing on Wednesday. The Layer-1 token has dropped more than 16% in February and is down roughly 34% year-to-date, mirroring the broader bearish tone across the crypto market.

Technically, Sui risks prolonging its downtrend amid weak retail engagement. While support at $0.87 remains intact for now, a decisive break below this level could open the door for a pullback toward the $0.79 demand zone.

Grayscale’s Sui Staking ETF begins trading

Grayscale Investments has confirmed the launch of its Sui Staking Exchange-Traded Fund (ETF), set to start trading Wednesday. The fund is listed on NYSE Arca under the ticker GSUI, following the conversion of the former Grayscale Sui Trust. The ETF is expected to hold SUI tokens and incorporate staking.

According to Grayscale, while purchasing shares does not constitute direct ownership of SUI, the product is structured to offer a cost-efficient and accessible way for investors to gain exposure to the token.

The Bank of New York Mellon will act as the trust’s transfer agent and administrator. Coinbase, Inc. will serve as prime broker, while Coinbase Custody Trust Company will function as custodian.

Investors can purchase shares only in creation blocks of 10,000 units or more.

Despite the ETF debut, retail demand for Sui remains muted. Futures Open Interest has slipped to $512 million on Wednesday from $554 million on Sunday, signaling limited appetite for new positions. The stagnation suggests traders remain unconvinced about the token’s ability to sustain a meaningful recovery, opting instead to scale back exposure.

Technical outlook: Sui’s downtrend remains intact

Sui is trading around $0.95, still capped below the declining 50-day Exponential Moving Average (EMA) at $1.28, maintaining a bearish medium-term outlook. The 100-day EMA at $1.58 and the 200-day EMA at $2.02 are also trending lower, continuing to limit recovery attempts.

On the daily chart, the Relative Strength Index (RSI) sits at 36, below the neutral 50 level, signaling persistent weakness. A sustained pickup in buying pressure could help improve momentum. However, if the RSI drifts further into oversold territory, the decline may accelerate toward support near $0.78 — in line with the February 6 low.

A decisive break above descending trendline resistance would create scope for a move toward the 100-day EMA at $1.58. Conversely, failure to extend any rebound would leave the broader downtrend firmly in control.

Meanwhile, the Moving Average Convergence Divergence (MACD) histogram has turned positive and is gradually expanding, showing the MACD line above the signal line near the zero threshold — an early sign of strengthening momentum. The Parabolic SAR, positioned at $0.86 below the current price, also suggests a tentative stabilization attempt.

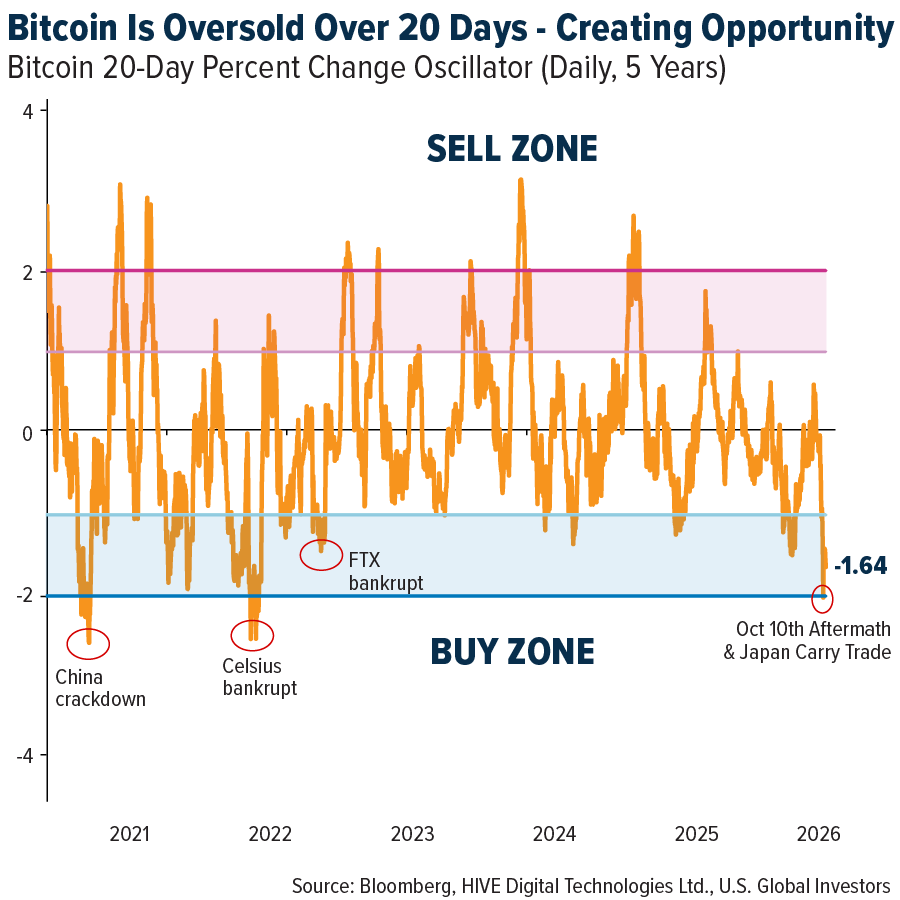

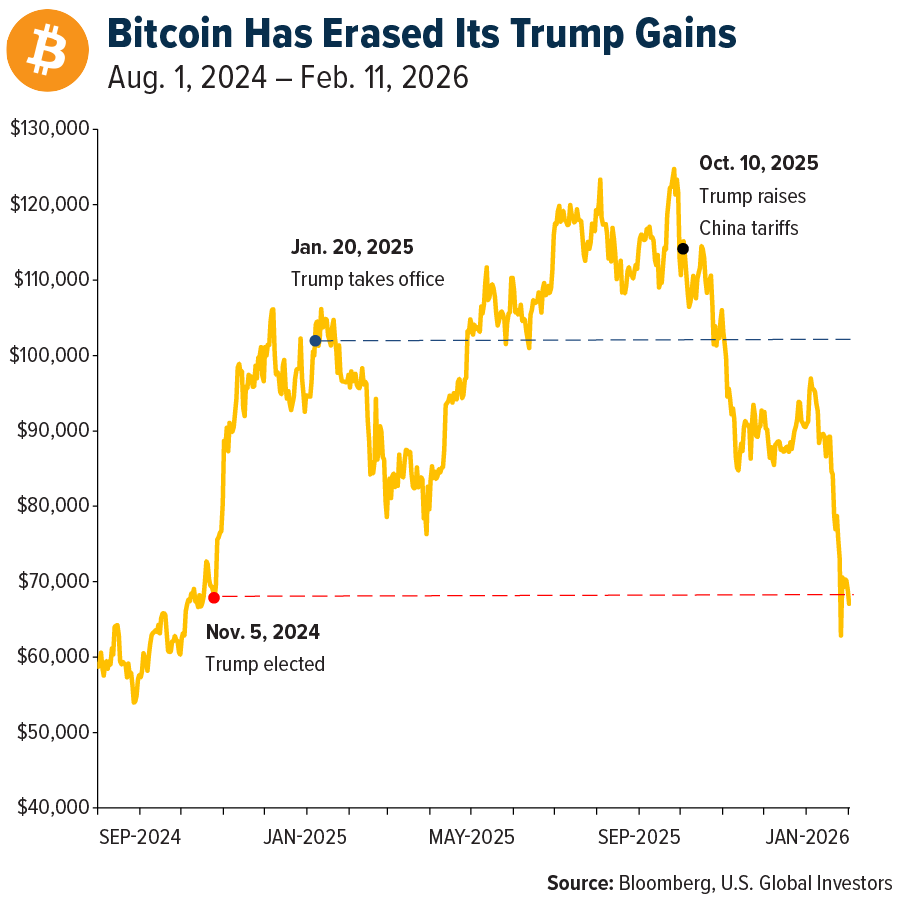

Four months ago, the digital asset market experienced what I consider its most significant liquidation event to date. On October 10, 2025, more than $19 billion in leveraged positions were erased within a matter of hours. Bitcoin tumbled from around $122,000 to $105,000, and over 1.6 million trader accounts were forced into liquidation.

The so-called “10/10” crypto crash did more than shake prices—it reshaped the psychological backdrop of crypto investing.

As I mentioned on PreMarket Prep last week, from a technical perspective Bitcoin is currently trading about two standard deviations below its 20-day average—a condition that has appeared only three times in the past five years. Historically, such stretched readings have tended to precede short-term rebounds over the following 20 trading sessions.

The unwinding of the Japanese carry trade—estimated at roughly $500 billion—likely added to the weakness seen in January and again this month. Still, I believe much of that pressure has now run its course.

With Bitcoin still trading below $70,000—about 45% off its all-time high—some investors may be asking whether the events of October 10 are the reason the downturn has lingered.

The short answer is yes. But the deeper explanation is more complex—and, in my view, more relevant for portfolio positioning going forward.

What Really Happened

To put it in context, the 10/10 crash surpassed the FTX collapse in absolute dollar losses. It effectively overshadowed the failure of what had been the world’s second-largest crypto exchange. Binance alone reportedly drew $188 million from its insurance fund to cover bad debt, while several other trading platforms faced comparable strains.

As for the catalyst, many point to President Donald Trump’s announcement of a 100% tariff on Chinese imports, layered on top of an existing 30% levy.

That geopolitical jolt rattled global markets. But in crypto—where leverage is deeply embedded in the system—it transformed what might have been a routine correction into a cascading liquidation event.

The crash laid bare deep structural flaws in how exchanges were managing risk, with one platform in particular drawing scrutiny.

The Binance Factor

Star Xu, founder and CEO of OKX, recently posted a detailed breakdown on X outlining his view of how the 10/10 meltdown unfolded.

According to Xu, Binance rolled out an aggressive user acquisition push offering 12% APY on USDe, a synthetic dollar built on Ethereum. At the same time, the exchange permitted USDe to be posted as collateral under the same terms as established stablecoins such as Tether (USDT) and USD Coin (USDC).

Xu argues this created a distorted incentive structure. Users were enticed to swap USDT and USDC for USDe in pursuit of higher yields, often without fully appreciating the added risk profile.

A leverage loop soon followed. Traders converted USDT into USDe, pledged USDe as collateral to borrow more USDT, then recycled the borrowed funds back into USDe—repeating the process. Xu claims this dynamic drove advertised yields as high as 24%, 36%, and even above 70%.

When volatility surged, USDe quickly lost its peg, unleashing cascading liquidations. The market entered a classic doom loop: forced selling triggered margin calls, which in turn sparked further forced selling.

For its part, Binance has denied responsibility. Speaking at a crypto conference last week, co-CEO Richard Teng attributed the turmoil entirely to President Donald Trump’s tariff announcement. Still, allowing heavily leveraged positions in a market where stop-losses can be gamed and safeguards are thin creates systemic fragility. In such an environment, even a minor shock can ignite a chain reaction.

The Psychological Fallout

October 10 erased more than leveraged trades—it shattered investor confidence. The event coincided with Bitcoin peaking near $126,000 and sparked a wave of fear that continues to weigh on sentiment.

In the weeks that followed, ETFs saw meaningful outflows. Retail traders—many of whom had piled into futures and margin positions as Bitcoin hit record highs—were hit hardest. More than 1.6 million accounts were liquidated, a large share belonging to smaller participants.

This month’s follow-on decline, which marked Bitcoin’s largest realized loss on record as prices slid from $70,000 to $60,000, was described by one analyst as a “textbook capitulation.” The drop was swift, volume-heavy, and flushed out holders with the weakest conviction.

Why I’m Still Constructive

Despite persistent volatility, I remain long-term bullish because the underlying fundamentals remain intact.

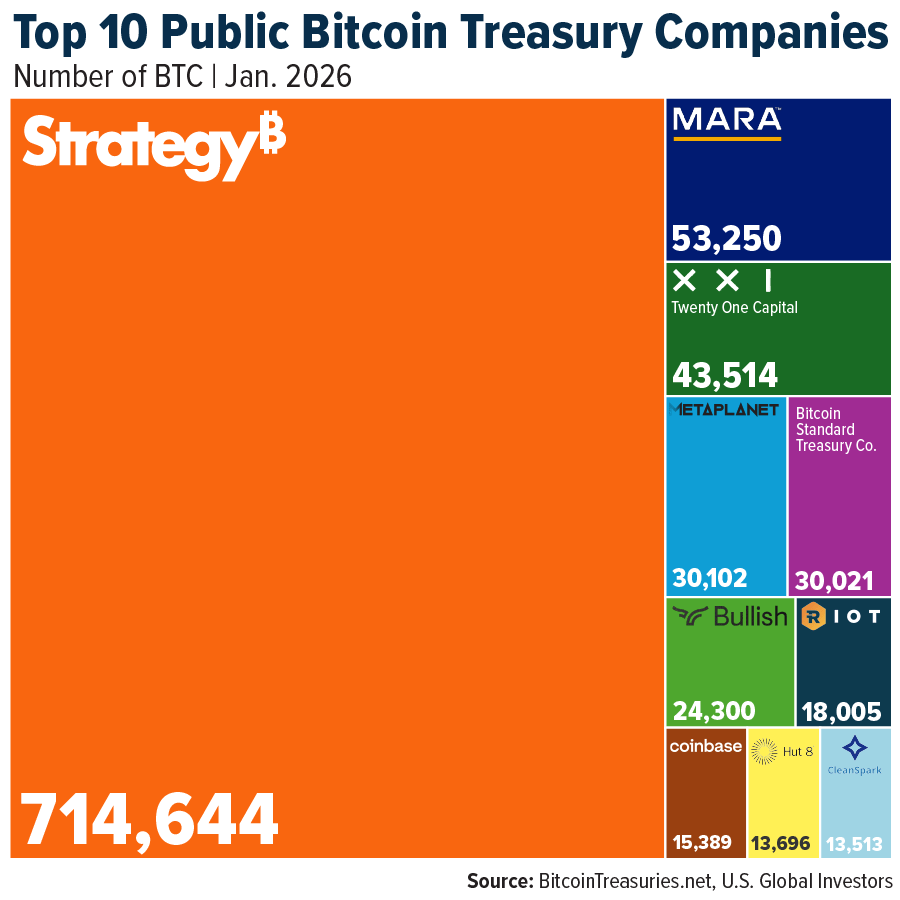

Institutional participation continues to expand. Corporate Bitcoin treasuries—often referred to as Digital Asset Treasury (DAT) firms—now collectively control more than 1.1 million BTC, about 5.7% of total supply, valued near $90 billion. MicroStrategy (now operating as Strategy) alone holds roughly 3.5% of Bitcoin’s circulating supply.

Notably, institutions added around 43,000 BTC in January, even amid adverse price conditions—suggesting that long-term capital remains engaged despite the market’s recent turbulence.

The U.S. Strategic Bitcoin Reserve now reportedly holds more than 325,000 BTC—about 1.6% of total supply—making it the largest sovereign holder globally. At the same time, other nation-states are building positions, much as they do with gold, and major corporations continue to add to their allocations.

The Bottom Line

I’ve long described Bitcoin as “digital gold,” but I don’t believe it has fully evolved into a true safe-haven asset. For now, institutions largely categorize it as a risk-on asset rather than risk-off. That suggests it is still carving out its place within diversified portfolios.

Was October 10 the root cause of Bitcoin’s prolonged weakness? In my view, yes. The event delivered a structural shock that obliterated leveraged positions and forced a sweeping—if painful—deleveraging across the digital asset ecosystem.

Did aggressive marketing and flawed incentive structures at certain platforms worsen the fallout? Again, I would argue yes. Encouraging investors to treat what was effectively a tokenized hedge strategy as if it were a stablecoin—while layering on substantial leverage—inevitably magnified systemic risk.

As severe as the collapse was, it may ultimately prove constructive. Excess leverage often needs to be purged before a sustainable advance can resume. My sense is that we are nearing the final phase of that cleansing process.

Bitcoin declined on Monday, deepening its downturn after crypto markets posted four consecutive weeks of heavy losses, as interest-rate uncertainty continued to dampen appetite for riskier assets.

The largest cryptocurrency briefly touched $70,000 over the weekend before retreating. By 00:58 ET (05:58 GMT), Bitcoin was down 2.7% at $68,409.7.

Strategy says liquidation unlikely unless Bitcoin drops to $8,000

Strategy Inc (NASDAQ:MSTR), the biggest corporate holder of Bitcoin, said Sunday it can meet its debt obligations even if Bitcoin tumbles to $8,000. In a social media update, the company stated it could “withstand a drawdown in $BTC price to $8K and still have sufficient assets to fully cover our debt.”

The firm owns 714,644 Bitcoins, financed through a combination of equity issuance and long-term borrowing. Led by prominent Bitcoin advocate Michael Saylor, Strategy has continued accumulating coins in recent weeks despite the broader market slide.

Bitcoin has now erased about half its value since peaking near $126,000 in October, leading declines across speculative assets as traders grew cautious amid U.S. rate uncertainty.

Extended losses had fueled speculation that Strategy might be forced to sell part of its holdings to service debt, though Saylor has repeatedly downplayed such concerns. Earlier this month, the company reported a $12.4 billion loss for the December quarter, compared with a $670.8 million loss a year earlier. Aside from its substantial Bitcoin position, Strategy generates relatively limited operating revenue.

Broader digital assets also moved lower Monday in line with Bitcoin’s sustained slump. Ethereum fell 6.1% to $1,958.63, while XRP dropped 7.7% to $1.4575.

BNB declined about 4%, with Solana and Cardano sliding 5.4% and 6.2%, respectively.

Among meme tokens, Dogecoin tumbled 11.4%, while TRUMP slipped 2.4%.

Crypto sentiment has remained fragile since October, as both retail and institutional inflows slowed sharply. Meanwhile, a surge in gold prices amid speculative enthusiasm in precious metals has drawn attention away from Bitcoin, with investors favoring tangible assets.

Bitcoin snapped a four-session slide on Friday, climbing nearly 4%, though it remained on course for its first four-week losing streak since November 2025. The leading cryptocurrency was up 3.7% at $68,776.1 by 17:15 ET (22:15 GMT), after dropping close to $65,000 in the prior session.

Bitcoin pressured by tech slump as U.S. inflation eases.

While Friday’s rebound trimmed some weekly losses, Bitcoin was still headed for a roughly 0.6% decline, struggling to build lasting upside momentum after bouncing from earlier lows and drifting back toward last week’s $60,000 support zone.

Risk appetite has been fragile amid a prolonged selloff in technology stocks, driven by renewed concerns that artificial intelligence could disrupt traditional software and office-service business models. Those fears resurfaced on Thursday as investors questioned how automation and emerging AI tools might erode established revenue streams.

At the same time, fresh U.S. inflation data showed price pressures eased more than anticipated in January. According to the U.S. Bureau of Labor Statistics, headline CPI rose 2.4% year-over-year, down from 2.7% in December, while core CPI increased 2.5%, matching forecasts.

On a monthly basis, headline CPI gained 0.2% and core CPI 0.3%, with the softer headline figure boosting expectations that the Federal Reserve could move toward policy easing. However, strong labor market data earlier in the week—highlighting solid payroll growth and a lower unemployment rate—had dampened hopes for near-term rate cuts.

Dessislava Ianeva of Nexo Dispatch noted that crypto markets appear to be stabilizing after the softer CPI reading, even as ETF outflows continue, with positioning data suggesting lower leverage and consolidation rather than a fresh directional breakout.

Crypto leaders appointed to CFTC Innovation Advisory Committee.

Separately, the U.S. Commodity Futures Trading Commission appointed several prominent crypto executives to its new Innovation Advisory Committee, including Brian Armstrong of Coinbase, Brad Garlinghouse of Ripple, Vladimir Tenev of Robinhood, and Hayden Adams of Uniswap Labs.

The committee will advise on emerging technologies such as blockchain and AI in derivatives and crypto markets, as regulators clarify oversight of digital assets, with the CFTC expected to take a leading role.

Elsewhere in the market, altcoins also advanced. Ethereum jumped 5.4% to $2,049.07, XRP rose 2.8% to $1.40, Solana surged 8.3%, Cardano gained 4.1%, and Dogecoin added 4.7%.

Bitcoin has fallen roughly 50% from its October 2025 peak near $126,000 and is now trading around $65,000, marking a far deeper retracement than a routine correction. This downturn reflects not just price volatility but a broader shift in the macro backdrop and crypto’s structural dynamics.

Macro Pressures Reshape the Cycle

As institutional participation has increased, Bitcoin has become more tightly linked to global financial conditions. Rather than acting as “digital gold,” it has moved in closer correlation with U.S. equities—especially technology stocks. Ongoing uncertainty about the pace of disinflation, combined with renewed tariff measures from the Trump Administration targeting Europe and Asia, has strengthened the U.S. dollar and dampened overall risk appetite. Concerns that the artificial intelligence boom may be maturing have further pressured growth assets, including crypto.

Miner Stress and Institutional Retreat

On-chain and industry data reveal mounting supply-side pressure. With the estimated average mining cost around $87,000, many miners are operating below breakeven at current price levels. To stay solvent, some have been liquidating reserves, adding persistent sell-side pressure to the market.

Institutional flows tell a similar story. Roughly $5 billion has exited Bitcoin ETFs in recent weeks, signaling a rotation into safer assets. Meanwhile, reports of operational pauses at certain established crypto platforms have revived memories of the 2022 bankruptcy wave, further unsettling sentiment.

The Crypto Fear and Greed Index remains entrenched in the 5–8 range—classified as “extreme fear”—highlighting the depth of caution across the market.

The Technical Road Ahead

For sentiment to meaningfully reset, Bitcoin must reclaim the $70,000–$78,000 zone, which now represents a critical resistance band. A sustained move above that range would signal renewed confidence and potentially mark the beginning of a recovery phase. Until then, macro headwinds, miner capitulation risks, and fragile investor psychology are likely to continue defining the tone of this cycle.

Bitcoin Technical Outlook

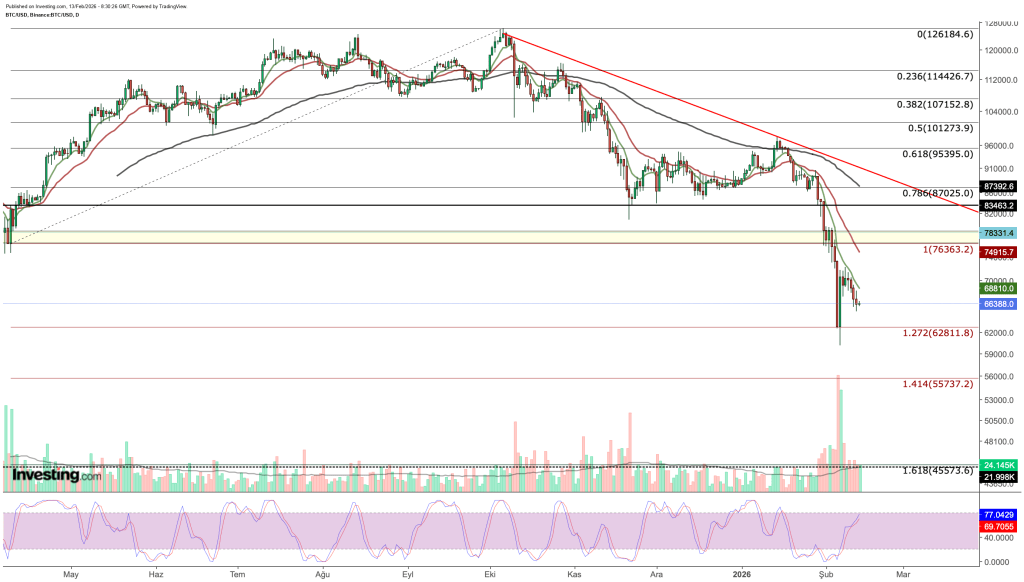

On the daily chart, Bitcoin is attempting to stabilize in a critical technical zone. After sliding to roughly $60,000 last week, price rebounded, but the recovery stalled near $70,000 as sellers re-emerged. Over the past week, Bitcoin has remained below its 8-day EMA, signaling short-term weakness and keeping the broader technical bias cautious.

The $62,800 area—aligned with the Fibonacci 1.272 extension—now stands out as key support. The earlier bounce from $60,000 suggests buyers are active in this region and view it as a potential base. However, a daily close below that level could accelerate downside pressure, exposing the next major support near $55,000, around the Fibonacci 1.414 extension.

One constructive signal comes from momentum indicators. On the daily timeframe, the Stochastic RSI is showing positive divergence: while price has continued to drift lower, the indicator has turned upward from oversold territory. This often signals waning downside momentum and can precede sharp countertrend rallies, including short squeezes or bear traps. Still, for a rebound to evolve into a durable recovery, Bitcoin must reclaim key resistance levels and short-term moving averages. Until then, the market remains delicately balanced between support and renewed selling.

Critical Resistance Levels for a Trend Reversal

A sustained recovery would first require a decisive break above the psychological $70,000 level, ideally accompanied by strong trading volume. Without volume confirmation, upside moves may lack conviction.

A more robust trend reversal signal would come from breaking the descending trendline and reclaiming the Fibonacci 1.0 level near $76,350. The broader $76,000–$78,000 band represents a major technical barrier. Unless Bitcoin can firmly establish itself above this zone, rallies are likely to remain corrective within a broader medium-term downtrend.

Is a Short Squeeze Setup Building?

Bitcoin futures funding rates are hovering around -0.006%, indicating short positioning dominates. When leverage becomes skewed heavily to one side, sharp counter-moves often follow as liquidity is cleared. Combined with the positive Stochastic RSI divergence, this creates the potential for a swift spike toward $70,000.

Zooming out, Bitcoin appears to be navigating a capitulation phase marked by ETF outflows, miner pressure, and macro uncertainty. At the same time, some technical signals hint at a cleansing process that could reset positioning.

A conservative stance would wait for weekly closes above $78,000 before declaring a structural recovery. More tactical traders may view the Stoch RSI divergence as an opportunity for a move toward $70,000, with $62,800 serving as a clear risk threshold.

As the crypto sector enters what looks like a period of corporate restructuring in early 2026, the $55,000 region could eventually be seen as a longer-term base—if stabilization holds. Until stronger confirmation emerges, disciplined risk management remains critical: reduced leverage, smaller position sizing, and strict stop-loss levels are essential in this highly volatile environment.

Total Bitcoin futures open interest has fallen to $34 billion as of Thursday, marking a 28% drop over the past month. However, this decline appears largely driven by price effects rather than a reduction in leverage. When measured in Bitcoin terms, open interest remains broadly unchanged at 502,450 BTC, indicating that underlying demand for leveraged exposure is still intact.

Over the past two weeks, forced liquidations have reached $5.2 billion, contributing significantly to the contraction in nominal dollar terms. Meanwhile, options markets show a 22% bearish skew, and funding rates continue to stay below the 12% threshold, suggesting that sentiment remains cautious but not excessively overheated.

Bitcoin Diverges from Traditional Markets

Bitcoin has declined 28% over the past month, even as gold surged back above the $5,000 psychological threshold and the S&P 500 remains just 1% shy of its record high. This growing divergence has prompted investors to question what is driving crypto’s relative weakness. One possible explanation lies in softer US labor data, with the economy adding only 181,000 jobs in 2025—falling short of expectations.

In derivatives markets, sentiment remains cautious. The annualized funding rate on Bitcoin futures has stayed below the neutral 12% benchmark for four straight months, reflecting persistent risk aversion. Options markets show even stronger defensive positioning, as the delta skew on Deribit climbed to 22%. This suggests traders are paying a notable premium for protective put options. Under typical conditions, the skew fluctuates between -6% and +6%, signaling more balanced sentiment.

Despite the bearish tone in derivatives, institutional participation appears steady. US-listed Bitcoin ETFs are recording average daily trading volumes of $5.4 billion, challenging narratives of fading institutional interest. Ultimately, Bitcoin’s near-term rebound may hinge on clearer signals about the direction of the US labor market and broader macroeconomic stability.

Bitcoin remained under pressure on Thursday as investors stayed cautious and its divergence from the rallying stock market widened. The BTC/USD pair slipped below 68,000, a sharp decline from its year-to-date peak of 126,300.

The pullback came even as US equities extended their strong advance, with the Dow Jones reaching a record high. The decline followed the release of solid US labor market data. According to the Bureau of Labor Statistics, the economy added more than 130,000 jobs, while the unemployment rate eased to 4.3%. However, some analysts cautioned that the figures could be revised lower, as has happened previously.

Indeed, revisions to last year’s employment data revealed that job growth averaged 15,000 per month, significantly below the initially reported 49,000 average.

Bitcoin also weakened amid a continued drop in futures open interest, which has fallen to $45 billion from last year’s peak of over $95 billion—an indication that market participation and demand have cooled.

Additional pressure followed warnings from the Congressional Budget Office (CBO) about the US government’s unsustainable fiscal trajectory. The deficit is projected to rise by $4.7 trillion over the next decade. Increased immigration-related spending, estimated at more than $500 billion, is cited as one contributing factor, while Trump’s tariffs are expected to generate approximately $3 trillion in revenue.

BTC/USD Technical Analysis

On the daily chart, BTC/USD remains in a pronounced downtrend, sliding from its October high of 126,300 to around 67,665. The decline persists despite continued accumulation by large holders.

Technically, Bitcoin is trading below both the 50-day and 100-day Exponential Moving Averages, as well as the Supertrend indicator, reinforcing the bearish bias. The MACD has crossed below the zero line, while the Relative Strength Index hovers near 30, suggesting weak momentum and near-oversold conditions.

The most probable scenario is a continued decline toward the key support level at 60,000. Conversely, a break above the major resistance at 72,000 would negate the bearish outlook and signal the potential for renewed upside momentum.

Bitcoin hovered around $67,000 during Thursday’s Asian session, showing little movement as investors weighed stronger-than-expected U.S. jobs data that reduced hopes for an imminent Federal Reserve rate cut. The leading cryptocurrency edged up 0.4% to $67,102.8 but remained below the crucial $70,000 threshold, with trading subdued amid thinner liquidity conditions.

After bouncing back from a steep drop toward $60,000 earlier this month, Bitcoin has struggled to rebuild bullish momentum.

Robust U.S. jobs data tempers rate-cut expectations; CPI in focus

Figures released Wednesday showed U.S. nonfarm payrolls rose more than anticipated in January, highlighting ongoing strength in the labor market. The unemployment rate stayed near multi-month lows, and wage growth remained solid—reinforcing expectations that the Fed may keep interest rates elevated for longer.