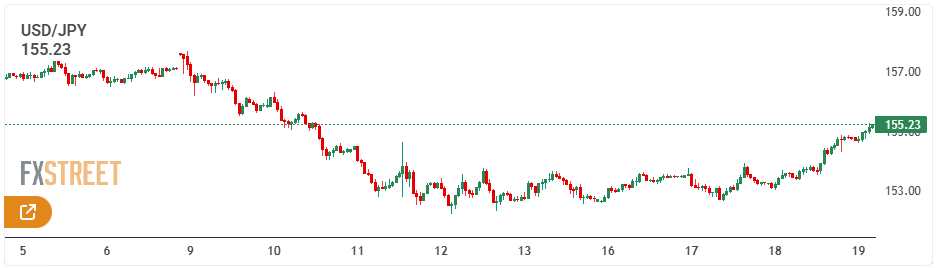

USD/JPY is consolidating Wednesday’s strong advance, hovering near the 155.00 mark early Thursday. The bullish bias remains intact as concerns over Japan’s fiscal outlook and a generally positive market sentiment continue to weigh on the safe-haven Japanese Yen.

At the same time, the latest FOMC Minutes revealed divisions among Fed officials regarding the need and timing of additional rate cuts amid lingering inflation risks. This uncertainty lends support to the US Dollar, providing an added tailwind for the pair.

USD/JPY Technical Overview

The US Dollar (USD) is trading with a mild bullish bias against the Japanese Yen (JPY) this week, hovering near the top of the 153.00 range. However, the pair remains confined within its weekly boundaries, as resistance around 154.00 continues to cap upside attempts ahead of the release of the minutes from the US Federal Reserve’s latest meeting.

Fundamental Overview

The Federal Reserve kept its benchmark rate unchanged at 3.5%–3.75% and signaled that policy is likely to remain steady in the near term. The meeting minutes are expected to underscore divisions within the committee—differences that are drawing added attention after last week’s softer U.S. inflation data and disappointing jobs report.

On Tuesday, Chicago Fed President Aistan Goolsbee pointed to those internal splits, noting that if inflation continues to ease, the central bank could lower rates multiple times this year.

In Japan, weak fourth-quarter GDP data released Monday have renewed worries about the country’s economic prospects, reinforcing Prime Minister Sanae Takaichi’s push for substantial fiscal stimulus and tax cuts.

Meanwhile, the International Monetary Fund cautioned that reducing the consumption tax could strain public finances and urged the Bank of Japan to tighten monetary policy further to keep inflation in check. As a result, the yen’s recent bullish momentum has faded somewhat, offering relief to the previously pressured U.S. dollar.

If you’ve been tracking currency markets, you’ve likely seen the Japanese yen advance for three straight sessions, trading near the 153 JPY/USD level. This move isn’t random—it reflects deeper shifts in forex positioning and strategic reallocations by Japanese investment funds.

Despite stronger-than-expected U.S. employment data, the yen has gained ground. The key driver appears to be a rotation in positioning: Japanese hedge funds and institutional investors have closed out prior bearish bets on the yen and are now positioning for further appreciation. This shift highlights a broader change in sentiment and confidence within the currency market.

What’s Fueling the Move?

The primary catalyst is renewed buying interest from Japanese funds. After unwinding short-yen trades, they are now building long positions, anticipating continued strength. Market perceptions of the Japanese government and the Bank of Japan’s commitment to currency stability are also contributing to this shift.

While U.S. macroeconomic indicators—such as payroll data—often dominate headlines, this episode shows that capital flows and institutional positioning can at times outweigh even strong economic releases.

Authorities Remain Vigilant

Japan’s top foreign exchange official, Junichi Mimura, has emphasized that authorities are closely monitoring currency developments and maintaining active communication with U.S. counterparts. This ongoing dialogue signals a commitment to orderly market conditions.

For traders and investors, this reinforces an important point: currency movements are shaped not only by data, but also by policy signals, market psychology, and cross-border coordination.

Sentiment and USD/JPY Positioning

Recent trends indicate softer demand for USD/JPY hedging, suggesting rising confidence in the yen’s near-term outlook. Shifts in options activity often provide insight into market expectations and potential support or resistance zones.

Whether you’re a short-term trader or a longer-term investor, staying attuned to these sentiment indicators can help refine entry points and risk management strategies.

How to Navigate Yen Volatility

Monitor official communication: Watch statements from Japanese policymakers and central bank officials.

Apply technical analysis: Pay attention to key levels around 153 JPY/USD for potential breakout or reversal signals.

Control risk exposure: Use stop-loss strategies to guard against sharp counter-moves.

Diversify allocations: Avoid overexposure to a single currency pair by balancing across assets.

Why It Matters

The yen’s recent strength reflects more than price action—it represents shifting expectations, institutional flows, and evolving policy narratives. Understanding these dynamics can sharpen your broader market perspective and improve decision-making.

In forex, staying informed is a competitive advantage. By tracking positioning trends, official commentary, and sentiment signals, you can better anticipate market turns and respond with confidence.

The Japanese yen slid to a fresh two-week low as Sanae Takaichi’s landslide victory reignited concerns over Japan’s fiscal outlook. However, warnings of possible currency intervention sparked some intraday short covering in the yen, aided by broader U.S. dollar weakness.

Still, downside momentum in the yen was partly limited after data showed a decline in Japan’s real wages, which reduced expectations for an immediate interest rate hike by the Bank of Japan and helped cap further moves in the currency.

The Japanese yen began the new week on a softer footing after Prime Minister Sanae Takaichi’s landslide victory in Sunday’s election raised expectations of additional fiscal stimulus. That initial weakness proved short-lived, however, as Finance Minister Satsuki Katayama reiterated warnings over excessive currency moves and confirmed close coordination with the United States to counter disorderly FX fluctuations. Combined with continued U.S. dollar selling, the comments prompted an intraday reversal of nearly 150 pips in USD/JPY from the Asian session peak near 157.65.

Meanwhile, data released earlier showed Japan’s real wages fell in December for a 12th straight month, with nominal pay growth slightly lagging cooling consumer inflation. This reinforces expectations that the Bank of Japan will proceed cautiously after lifting interest rates to a three-decade high in December. In addition, a more upbeat risk environment, supported by signs of easing tensions in the Middle East, limited further safe-haven demand for the yen, allowing USD/JPY to find support and stall its pullback around the 156.20 area.

Yen bulls stay cautious as fiscal concerns and delayed BoJ hike bets offset intervention talk

Japan’s ruling Liberal Democratic Party, led by Prime Minister Sanae Takaichi, secured a decisive victory in Sunday’s election, comfortably surpassing the 233-seat threshold needed for a lower-house majority. The result clears the path for proposed tax cuts and increased defense spending, bringing renewed attention to Japan’s already stretched public finances.

Finance Minister Satsuki Katayama said on Monday that she stands ready to communicate with markets if necessary to help stabilize the yen. She reiterated that Japan remains in close coordination with U.S. Treasury Secretary Scott Bessent and emphasized Tokyo’s right to intervene if currency moves stray from economic fundamentals.

Meanwhile, data from the labor ministry showed nominal wages rose 2.4% year-on-year in December 2025, accelerating from a revised 1.7% gain previously but still missing market expectations. Adjusted for inflation, real wages fell 0.1% from a year earlier, extending their decline to a 12th consecutive month.

The figures have dampened expectations for an imminent Bank of Japan rate hike, as policymakers have stressed that further tightening hinges on sustained and broad-based wage growth. Together with a generally positive global equity backdrop, this has limited the yen’s rebound from a more than two-week low.

Risk sentiment was further supported by indirect U.S.–Iran talks on Tehran’s nuclear program, which concluded on Friday with agreement to keep diplomatic channels open. The development eased fears of a military escalation in the Middle East and encouraged demand for risk assets at the start of the week, despite new U.S. sanctions on Iran.

The U.S. dollar weakened for a second straight session amid growing bets that the Federal Reserve could cut interest rates twice more in 2026. This contrasts with expectations that the BoJ will continue its gradual policy normalization, helping to cap gains in USD/JPY and urging caution among bullish traders.

Attention now turns to key U.S. data later this week, including the closely watched nonfarm payrolls report due Wednesday and consumer inflation figures on Friday, both of which are likely to shape dollar direction and drive fresh moves in USD/JPY.

USD/JPY holds steady below 100-hour SMA as technical signals remain mixed

The USD/JPY pair is showing modest resilience around the 100-hour Simple Moving Average (SMA), with its intraday pullback stalling near the 156.20 area, which now stands out as a key pivot for short-term traders. Momentum indicators, however, paint a mixed picture. The Moving Average Convergence Divergence (MACD) has formed a bearish crossover near the zero line, signaling rising downside pressure, while the Relative Strength Index (RSI) is hovering around 46, below the neutral 50 level, pointing to subdued momentum.

At the same time, USD/JPY remains above the 100-hour SMA, currently located around the 156.55–156.50 zone, which preserves a mildly constructive near-term bias and provides dynamic support. A move by the MACD back into positive territory alongside an RSI break above 50 would strengthen the bullish case and open the door to further gains. On the other hand, a clear break and close below the 100-hour SMA would undermine the setup and increase the risk of a deeper corrective move.

Japanese yen bears trimmed positions ahead of Japan’s snap election on Sunday, allowing the currency to recover modestly. Growing speculation of an imminent Bank of Japan rate hike, combined with a broader risk-off mood, has also supported the safe-haven yen. Meanwhile, the U.S. dollar paused its recent rebound from a four-year low, adding further downside pressure on USD/JPY.

The Japanese yen attracted modest buying during Asian trading on Friday, appearing to snap a five-day losing streak against the U.S. dollar after touching a two-week low in the previous session. Traders remain alert to the possibility of coordinated Japan–U.S. intervention to curb further yen weakness, while a shift in global risk sentiment and elevated market volatility have boosted demand for the currency’s safe-haven appeal. Expectations for a more hawkish Bank of Japan have also provided underlying support to the yen.

Data released earlier showed Japan’s household spending fell sharply in December, highlighting the impact of higher prices on consumer activity and reinforcing expectations that the BoJ could move toward a rate hike sooner rather than later. That said, concerns about Japan’s fiscal position and ongoing political uncertainty may limit aggressive bullish positioning in the yen. In addition, the U.S. dollar’s recent recovery from a four-year low could help cap further declines in USD/JPY as markets look ahead to Japan’s snap lower house election on February 8.

Yen finds support from hawkish BoJ outlook and improving risk sentiment

Data released earlier on Friday showed that Japan’s Household Spending fell 2.6% YoY in December 2025, reversing a 2.9% increase in the previous month. The sharp contraction highlights the drag from elevated living costs on consumption and reinforces the Bank of Japan’s resolve to tackle inflation, strengthening the case for an earlier interest rate hike.

This view is supported by the Summary of Opinions from the BoJ’s January meeting, which revealed that policymakers discussed rising price pressures stemming from a weak Japanese Yen and agreed that further rate hikes would be appropriate over time. These factors helped the JPY attract modest buying during the Asian session.

The Yen also benefited from a risk-off impulse, as Asian equities extended losses for a second straight day following a deepening selloff in global tech stocks. Meanwhile, the US Dollar paused its recent advance to a two-week high, prompting traders to trim USD/JPY long positions ahead of Japan’s snap lower house election on Sunday, February 8.

Japan’s Prime Minister Sanae Takaichi’s Liberal Democratic Party (LDP) is widely expected to secure a decisive victory, which would strengthen her control over parliament and provide greater scope to pursue aggressive pro-stimulus policies. However, markets remain concerned that expansionary fiscal plans could further strain Japan’s already fragile public finances, limiting the Yen’s upside.

From the US, data released Thursday showed that Initial Jobless Claims rose to 231K for the week ending January 31, up from 209K and above expectations of 212K, adding to weak private-sector employment data released earlier in the week. Further evidence of labor market softening came from the JOLTS report, which showed job openings falling to 6.542 million in December from a downwardly revised 6.928 million previously.

The softer labor backdrop has reinforced expectations for additional Federal Reserve easing, with markets currently pricing in two more rate cuts in 2026. This has capped the US Dollar’s rebound from a four-year low and contributed to USD/JPY pulling back modestly from the two-week high above the 157.00 level touched on Thursday.

Traders now await the preliminary Michigan Consumer Sentiment Index and inflation expectations, along with remarks from key FOMC members, for fresh directional cues later in the North American session. However, market reactions are likely to remain subdued ahead of Japan’s closely watched political event.

USD/JPY buyers remain in control after breaking above the 200-period SMA resistance on the H4 chart.

The overnight move above the 156.50 barrier, which aligns with the 200-period SMA on the 4-hour chart, marked an important catalyst for USD/JPY bulls. The gently rising SMA reflects a stable underlying uptrend, and prices remaining above it preserve a bullish tone. However, the MACD has dipped below its Signal line around the zero level, with the histogram turning negative and widening, pointing to a loss of upside momentum. Meanwhile, the RSI has retreated to 63 from overbought territory, highlighting a more tempered momentum backdrop.

As long as USD/JPY holds above the rising 200-period SMA, upside risks remain favored. A sustained break below this level would shift the focus toward a corrective pullback. From a momentum perspective, continued expansion of the negative MACD histogram would strengthen downside risks, while a swift move back above zero would negate the bearish crossover. The RSI staying above 50 continues to support the bullish case, whereas a slide toward that level would signal weakening buying interest.

USD/JPY paused its advance near the 157.00 mark during Thursday’s Asian session, as a renewed bout of risk aversion revived safe-haven demand for the Japanese yen.

That said, the yen remains on fragile footing amid ongoing concerns over Japan’s fiscal position under Prime Minister Sanae Takaichi’s expansionary spending agenda, helping to limit downside pressure on the pair.

Looking ahead, the U.S. JOLTS Job Openings report could provide fresh impetus for near-term trading.

USD/JPY Technical Analysis

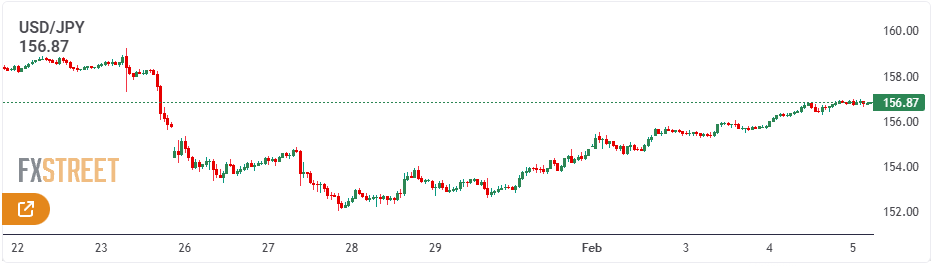

The Japanese yen emerged as the weakest-performing G8 currency on Wednesday. Its sharp underperformance has lifted USD/JPY above the 156.80 level at the time of writing, putting the pair on course for a roughly 3% rebound from last week’s lows.

Fundamental Analysis

Investors are offloading the yen broadly ahead of this weekend’s snap election. Rising support for Prime Minister Takaichi has fuelled concerns that a stronger electoral mandate would allow her to extend tax cuts and expand stimulus spending, heightening fears of fiscal strain.

Markets Brush Aside Intervention Concerns

Tokyo authorities have warned of possible intervention to curb excessive yen volatility, but those concerns have been largely brushed aside. Comments from Prime Minister Takaichi highlighting the benefits of a weaker yen, along with the U.S. Treasury Secretary’s denial of any coordinated effort to stabilise the currency, have instead driven the yen sharply lower across the board.

The U.S. dollar, however, is not especially strong on Wednesday. While markets continue to react positively to the nomination of Kevin Warsh as the next Federal Reserve Chair and to the end of the brief partial government shutdown, the recent rally in the U.S. Dollar Index appears to be losing momentum.

Attention now turns to upcoming U.S. data, including the Services PMI and the ADP Employment Change report. The latter could be particularly influential, as the government shutdown has delayed Friday’s official nonfarm payrolls release, leaving private-sector jobs data as a key guide for markets.

The Japanese yen edged lower after softer-than-expected Tokyo CPI data dampened expectations for an imminent Bank of Japan rate hike.

Persistent fiscal challenges and political uncertainty continued to pressure the currency, although fears of official intervention helped limit losses.

Meanwhile, concerns over the Federal Reserve’s independence could restrain any rebound in the U.S. dollar and cap gains in the USD/JPY pair.

The Japanese yen (JPY) came under renewed selling pressure during Asian trading on Friday after data showed consumer inflation in Tokyo, Japan’s capital, slid sharply to a near four-year low in January. The weaker inflation reading reduces urgency for the Bank of Japan (BoJ) to move toward near-term rate hikes. In addition, concerns over Japan’s fiscal outlook, linked to Prime Minister Sanae Takaichi’s reflationary agenda, along with political uncertainty ahead of the February 8 snap election, continue to weigh on the currency. Coupled with modest U.S. dollar (USD) strength, these factors pushed USD/JPY toward the 154.00 level and the key 100-day Simple Moving Average (SMA) resistance.

That said, expectations of coordinated intervention by U.S. and Japanese authorities to support the yen may discourage aggressive bearish positioning. At the same time, lingering trade uncertainty stemming from President Donald Trump’s tariff threats and broader geopolitical risks is tempering risk appetite, as reflected in the cautious tone across equity markets, which could help limit downside in the safe-haven JPY. Meanwhile, the USD may struggle to gain sustained traction amid expectations of further Federal Reserve rate cuts and ongoing concerns over the central bank’s independence, potentially capping further upside in USD/JPY.

Japanese yen comes under pressure from soft Tokyo CPI, fiscal concerns and political uncertainty

A government report released earlier on Friday showed that Tokyo’s headline Consumer Price Index (CPI) fell to 1.5% in January from 2.0% previously, marking its lowest level since February 2022. Core inflation, which strips out fresh food prices, also softened to 2.0% from 2.3% in December, while a broader measure excluding both food and energy eased to 2.4% from 2.6% the month before.

The data signals easing demand-driven inflation pressures and diminishes the urgency for further monetary tightening by the Bank of Japan, following its December rate hike that lifted the policy rate to 0.75%, the highest level in three decades.

Meanwhile, concerns over Japan’s fiscal outlook persist as Prime Minister Sanae Takaichi has anchored her snap election campaign on expanded stimulus measures and pledged to suspend the consumption tax on food, raising questions about fiscal sustainability.

Adding another layer of complexity, reports of an unusual rate check by the New York Federal Reserve last Friday, following a similar move by Japan’s Ministry of Finance, have fueled speculation about potential coordinated U.S.-Japan intervention to curb yen weakness.

On the geopolitical front, U.S. President Donald Trump announced plans on Thursday to decertify all Canada-made aircraft and threatened to impose 50% tariffs unless U.S.-built Gulfstream jets receive certification in Canada. The move marks a fresh escalation in U.S.-Canada trade tensions.

These developments, alongside rising U.S.-Iran frictions and the prolonged Russia-Ukraine conflict, could help limit downside pressure on the safe-haven yen. The United States continues to deploy warships and fighter jets across the Middle East, while Secretary of War Pete Hegseth stated that Washington stands ready to act decisively under President Trump’s directives.

Russia has also reiterated its invitation for Ukrainian President Volodymyr Zelensky to travel to Moscow for peace talks, although prospects for a deal remain slim amid deep divisions between the two sides.

Meanwhile, the U.S. dollar received a modest boost amid speculation that Kevin Warsh may be appointed as the next Federal Reserve chair, lending additional support to the USD/JPY pair. President Trump is expected to announce his choice for Fed chair on Friday morning.

Looking ahead, traders will take further cues from the release of the U.S. Producer Price Index (PPI), which, alongside comments from Federal Reserve officials, is likely to influence dollar demand and provide direction for USD/JPY into the weekend.

USD/JPY bulls look for a sustained break above the 100-day SMA before adding new positions

The 100-day Simple Moving Average (SMA) continues to trend higher and is currently located near 153.98, with USD/JPY trading just below this level. This keeps near-term sentiment on the heavy side, despite the broader uptrend suggested by the rising trend filter. A sustained move back above this dynamic resistance would help steady the short-term outlook.

Momentum indicators show tentative signs of stabilization. The Moving Average Convergence Divergence (MACD) remains in negative territory, although its recent narrowing points to fading downside pressure. Meanwhile, the Relative Strength Index (RSI) stands at 37.81, below the neutral 50 mark but rebounding from oversold levels, indicating that bearish momentum is beginning to ease.

On the upside, the 38.2% Fibonacci retracement of the 159.13–152.07 decline, located at 154.77, is likely to act as initial resistance. A daily close above this level would enhance the recovery setup and open the door to further gains as momentum improves. Conversely, failure to break above this barrier would keep rebounds limited and reinforce a cautious near-term bias.

Yesterday, the US CPI came in weaker than anticipated, supporting our prediction of a Fed rate cut in March. However, we expect the market to take a few more weeks before fully embracing this outlook. The US dollar could recover more than its recent losses, possibly driven by a hawkish stance following the Powell criminal investigation. In the meantime, we’ll continue to watch the Japanese yen closely today, along with developments in the Greenland discussions.

USD: We Maintain a Short-Term Optimistic Outlook

US inflation came in softer than consensus and well below our expected 0.4% month-on-month core reading. Yet, yesterday’s market reaction actually reinforced our short-term positive outlook on the dollar: despite the weak CPI data, Fed rate expectations barely shifted, and the dollar quickly regained strength.

This may partly be due to market caution in over-interpreting the CPI figures amid ongoing shutdown-related distortions. It also indicates that concerns about the Fed’s independence are diminishing, helped by expectations that the criminal probe into Chair Powell may not advance much further and opposition from some GOP lawmakers. We believe there’s a fair chance the dollar will ultimately come out stronger from this situation, as Powell might adopt a more firmly hawkish stance to assert Fed independence.

Additionally, the key message from yesterday’s CPI report is the continued softness in goods prices, highlighting how limited the tariff effects on inflation have been. Several tariff-sensitive categories remained weak, including appliances (-4.3% MoM), furniture (-0.4%), new vehicles (0.0%), and video and audio equipment (-0.4%). This clear trend suggests US retailers are still squeezing their margins. Overall, this strengthens our confidence in a Fed rate cut in March, although it may take time for markets to fully accept this outlook.

Today, focus shifts to November’s PPI, with core PPI expected to rise by 0.2% month-on-month, and retail sales, which are anticipated to remain fairly strong. A busy lineup of Fed speakers—including Paulson, Miran, Kashkari, Bostic, and Williams—will be closely watched for any subtle hawkish signals in support of Powell and the Fed’s independence.

Additionally, the Supreme Court is expected to issue a ruling on tariffs today, likely unfavorable. If that happens, significant noise from the Trump administration is expected, though markets are unlikely to be caught off guard. Our baseline expectation is for a mildly positive reaction in the dollar.

EUR: Greenland Discussions Likely to Have Limited Market Impact

A US delegation, including JD Vance and Marco Rubio, is scheduled to meet today with officials from Denmark and Greenland. So far, US threats related to Greenland have had minimal impact on markets—limited mostly to some movements in EUR/DKK forwards—meaning there’s little risk premium to be unwound even if the talks lead to a cooperative outcome. Nevertheless, any progress could help eliminate a lingering geopolitical “black swan” risk for European currencies.

There seems to be potential for an agreement, likely based on the US abandoning any claims of “ownership” over Greenland—a stance firmly rejected by both Denmark and Greenland—in exchange for enhanced economic partnerships and a greater US military presence.

Positive headlines from the talks might ease the EUR/USD’s recent decline slightly, but we still expect the pair to approach 1.1600 in the near term.

JPY: Approaching the 160 Level for a Key Test

The USD/JPY rally shows no signs of slowing. Rising speculation about snap elections is bringing back a political risk premium, giving another push to test Japan’s currency tolerance band. Meanwhile, ongoing diplomatic tensions between Japan and China are adding more momentum to the move.

On Monday, we viewed 160 as a key upside target. While intervention concerns may slow the rally near that level, it increasingly looks like 160 will eventually be tested. Recall that in July 2024, Japan allowed the pair to surpass 160 and only intervened when it neared 162. Pinpointing the exact intervention level is tricky, but since the BoJ hasn’t acted sooner, it’s reasonable to expect they’ll wait until the pair exceeds 160.

For context, the first intervention on July 11, 2024, led to a 1.8% drop in USD/JPY. Interestingly, back then, CFTC net non-commercial positions on the yen were at -52% of open interest, whereas now they are 3% net-long, despite spot price action suggesting otherwise.

The crucial question is whether FX interventions alone can sustain a USD/JPY recovery. Historically, they haven’t. In 2024, interventions curtailed short-term gains but the subsequent USD/JPY decline was driven mainly by a sharp 50bp drop in US 2-year swap rates over the next month. That scenario seems unlikely now, and with snap election risks ongoing, markets remain hesitant to price in a BoJ rate hike before summer.