U.S. stock index futures slipped modestly on Tuesday night as a fragile rebound in technology shares showed signs of strain, with investors remaining cautious ahead of a wave of economic data and Federal Reserve signals.

Futures pulled back following a mildly upbeat session on Wall Street, where tech stocks attempted to bounce from recent declines. The recovery, however, was uneven, as lingering concerns over AI-driven disruptions continued to cloud sentiment in the sector.

By 19:55 ET (00:55 GMT), S&P 500 futures were down 0.1% at 6,851.50, Nasdaq 100 futures fell 0.2% to 24,721.0, and Dow Jones futures slipped 0.1% to 49,553.0.

Economic data, Fed minutes in focus

Attention now turns to several key economic releases and the minutes from the Fed’s January meeting, due Wednesday afternoon. Investors are looking for greater clarity on the central bank’s interest rate outlook after policymakers kept rates steady last month and signaled ongoing caution over persistent inflation and softening labor market conditions.

January industrial production figures are scheduled for Wednesday, followed by December’s PCE price index on Friday — the Fed’s preferred inflation measure and a key input into its longer-term rate projections.

Uncertainty surrounding the Fed has weighed on markets in recent weeks, particularly after President Donald Trump’s nomination of Kevin Warsh as the next Fed Chair was interpreted as a less dovish shift in leadership.

Nvidia, Meta pare gains; AMD cuts losses

NVIDIA and Meta Platforms gave back some after-hours gains but still rose about 0.6% each after announcing a multi-year partnership to expand AI infrastructure, with Nvidia set to supply millions of chips to Meta.

Rival AMD, which had dropped as much as 4% following the announcement, reduced its losses to trade roughly 2% lower.

Technology stocks remain sensitive after weeks of declines fueled by concerns about AI-related disruption — especially within software — as well as skepticism over elevated AI spending and the sector’s long-term growth outlook.

Wall Street posts modest gains

Major indexes ended Tuesday slightly higher, supported by a patchy tech rebound and strength in financial stocks. The S&P 500 rose 0.1% to 6,843.22, the Nasdaq Composite added 0.1% to 22,578.38, and the Dow Jones Industrial Average gained 0.07% to 49,533.19.

While some dip-buying helped tech shares recover modestly, heavyweight names including Microsoft, Tesla, Alphabet, and Oracle extended last week’s declines.

Markets also drew limited support from reports of progress in U.S.-Iran nuclear discussions, easing some concerns about escalating geopolitical tensions in the Middle East.

Austan Goolsbee said in a Friday interview with Yahoo Finance that while interest rates are likely to decline further, any additional cuts will depend on continued progress in bringing down services inflation.

He described the latest CPI report as mixed, with both positive signals and lingering concerns, noting that services inflation remains elevated and above target. Goolsbee expressed hope that the peak effects of tariffs have passed and pointed to strong January employment data as evidence of a broadly stable labor market with only modest cooling. Although he believes rates could be reduced further, he stressed the need for clearer improvement in inflation before accelerating cuts, warning that persistently high services inflation is a risk.

He added that the U.S. consumer remains the economy’s strongest pillar and should stay resilient if the job market holds steady and inflation eases. If inflation returns to 2%, he said, the Fed would have room to implement several more rate cuts.

U.S. equity futures moved slightly higher Tuesday night following a modest decline in the regular trading session, as investors assessed softer retail sales figures and looked ahead to a series of postponed U.S. economic reports due later in the week.

By 20:11 ET (01:11 GMT), S&P 500 futures rose 0.2% to 6,978.25, Nasdaq 100 futures advanced 0.3% to 25,291.75, and Dow Jones futures added 0.2% to 50,385.0.

Wall Street declined ahead of the upcoming jobs report, while the Dow posted a fresh record closing high.

During Tuesday’s regular session, the S&P 500 declined 0.3% and the Nasdaq Composite dropped 0.6%, pressured by losses in technology and other growth-oriented stocks.

In contrast, the Dow Jones Industrial Average managed a slight advance, closing above the 50,000 mark at a new record high for the third consecutive session.

Earlier, investors reacted to U.S. retail sales figures showing flat monthly consumer spending, missing expectations. The softer data fueled worries that elevated borrowing costs may be starting to curb household demand, despite broader signs of economic resilience. This strengthened expectations that the Federal Reserve could move toward rate cuts later this year if growth continues to ease.

Attention now shifts to the delayed monthly employment report, set for release Wednesday following the recent government shutdown. The data will offer the first detailed snapshot of labor market conditions in weeks, as policymakers monitor for indications of cooling.

Markets are also awaiting the postponed U.S. consumer price index report on Friday, which could play a pivotal role in shaping near-term market sentiment.

Robinhood and Lyft slide in after-hours trading.

In company-specific developments, Robinhood Markets (NASDAQ: HOOD) fell 7.5% in after-hours trading after posting earnings that came in below expectations, as weaker-than-anticipated revenue and user figures pressured the stock.

Shares of Lyft (NASDAQ: LYFT) plunged more than 17% in extended trading after the ride-hailing firm reported results that missed forecasts, further weighing on consumer-focused tech stocks.

Meanwhile, Ford Motor Company (NYSE: F) delivered quarterly earnings that fell short of Wall Street estimates, citing costs related to its electric vehicle operations and ongoing supply chain challenges. Despite the miss, the automaker projected improved earnings in 2026. Ford shares rose 0.5% in after-hours trading.

European stocks dropped sharply on Monday after U.S. President Donald Trump threatened to impose economic sanctions on several countries in the region if they resist his plans to acquire Greenland.

By 03:05 ET (08:05 GMT), Germany’s DAX was down 1.3%, France’s CAC 40 fell 1.6% and Britain’s FTSE 100 slipped 0.4%.

Tariff threats dampen market sentiment

President Donald Trump said over the weekend that he plans to impose tariffs on exports to the United States from eight European countries that have opposed his proposal for the U.S. to acquire Greenland. The countries affected include France, Germany and the United Kingdom, along with several Nordic and northern European nations.

Trump said an initial 10% tariff would be introduced on Feb. 1, rising to 25% in June if no agreement is reached allowing the United States to take control of Greenland, the semi-autonomous territory of Denmark.

The European Union has already suspended ratification of a U.S.–EU trade agreement, and media reports indicate the bloc may revive a €93 billion tariff package targeting U.S. goods. Such a move could sharply escalate tensions and increase the risk of a wider transatlantic trade conflict.

According to IG market analyst Tony Sycamore, the latest dispute has intensified fears of NATO fragmentation and the breakdown of last year’s trade accords with European partners, pushing investors toward risk-off positioning in equities while boosting demand for safe havens such as gold and silver.

This has put the World Economic Forum, which gets under way later in the session in Davos, squarely in focus as global leaders convene, including a large U.S. delegation led by President Trump.

Euro zone inflation data due

Monday’s key economic event is the release of December eurozone inflation data, particularly with U.S. markets closed for the Martin Luther King Jr. holiday. Annual eurozone CPI is expected to come in at 2.0% in December, matching the European Central Bank’s target for the first time since mid-2025, down from 2.1% in November.

The ECB has left interest rates unchanged since ending its rate-cut cycle in June and signalled last month that it is under no immediate pressure to adjust policy, as inflation concerns have eased and growth surprised on the upside toward the end of 2025. The ECB’s next policy meeting is scheduled for early February.

Earlier data showed China’s economic growth slowed to a three-year low in the fourth quarter, with GDP expanding 4.5% year on year, compared with 4.8% in the previous quarter.

U.S. tech giants in focus

The European corporate earnings calendar is thin, though UK building products group Marshalls reported full-year 2025 adjusted profit before tax in line with market expectations despite ongoing uncertainty in its end markets.

U.S. technology heavyweights listed in Europe will also be in focus, as they could become targets of retaliatory measures by European authorities if President Trump follows through on tariff threats against European countries until the U.S. is permitted to acquire Greenland.

Crude slips lower

Oil prices edged lower on Monday, giving back part of the previous week’s gains as markets weighed the growing risk of a trade dispute linked to Greenland. Brent crude slipped 0.1% to $59.74 a barrel, while U.S. West Texas Intermediate fell 0.1% to $55.95.

Prices had climbed early last week on concerns that unrest in Iran could threaten oil supplies from the Middle East, a region that represents a large share of global production. However, much of that risk premium faded after President Trump said there would be no immediate U.S. military action, triggering a pullback before prices stabilized later in the week.

Oil prices remained mostly steady during Asian trading on Monday as investors balanced concerns over potential supply disruptions due to escalating unrest in Iran against the likelihood of more Venezuelan crude returning to the market.

As of 22:23 ET (03:23 GMT), March Brent crude futures rose slightly by 0.1% to $63.39 per barrel, while West Texas Intermediate (WTI) futures also increased by 0.1% to $59.15 per barrel. Both benchmarks had gained over 3% last week amid heightened geopolitical tensions.

Iran’s lethal protests raise fears of oil supply disruption

Markets have been closely monitoring Iran, a major oil producer in the Middle East, where widespread anti-government protests have escalated in recent days. According to rights organizations, over 500 people have died amid the unrest.

Iranian authorities have warned that U.S. military bases in the region would be targeted if Washington intervenes in support of the protesters. This threat has intensified concerns about a wider regional conflict that could disrupt oil shipments passing through the Strait of Hormuz, a critical artery for global energy supplies.

U.S. President Donald Trump adopted a tougher stance on Iran last week, declaring that the U.S. would not remain passive if Iranian forces continue harsh crackdowns on demonstrators.

“Iran, as the fourth-largest OPEC member, produces about 3.2 million barrels per day of crude oil, which represents a significant supply risk for the market,” ING analysts noted in a recent report.

Resumption of Venezuelan oil exports limits upside in oil prices

However, gains were limited by news from Venezuela, where U.S. officials indicated they might ease restrictions on the country’s oil sector. U.S. Treasury Secretary Scott Bessent said additional sanctions could be lifted as early as next week to help facilitate the sale of Venezuelan crude and support oil exports.

President Donald Trump also revealed plans for Venezuela to turn over up to 30 – 50 million barrels of previously sanctioned oil to the United States.

Despite the prospects of renewed output, major oil companies are cautious about re-entering the Venezuelan market without substantial legal and political reforms. ExxonMobil has described the country as “uninvestable” without major changes, and analysts note that firms whose assets were nationalised previously may be reluctant to return without adequate compensation.

Asian currencies remained largely steady on Monday, while the U.S. dollar weakened following the announcement of a criminal investigation involving Federal Reserve Chair Jerome Powell, casting uncertainty over the central bank’s independence.

The U.S. Dollar Index, which tracks the greenback against a basket of major currencies, declined 0.2% from its one-month peak. Meanwhile, U.S. Dollar Index futures were also down 0.2% as of 04:27 GMT.

Fed Chair Powell faces threat of indictment

Investor confidence was rattled after Powell revealed that the administration had threatened the Federal Reserve with a potential criminal indictment related to his Senate testimony about cost overruns in the Fed’s headquarters renovation.

This development weakened trust in U.S. institutions and prompted a cautious mood across global markets, dampening risk appetite in Asia.

In this environment, most regional currencies showed little movement.

The Japanese yen’s USD/JPY pair edged up 0.2%, while the Singapore dollar’s USD/SGD remained flat.

The South Korean won stood out, rising 0.7% on Monday.

In China, the onshore yuan’s USD/CNY pair was mostly unchanged, whereas the offshore yuan’s USD/CNH dipped slightly by 0.1%.

The Indian rupee’s USD/INR pair saw minimal change.

Meanwhile, the Australian dollar’s AUD/USD pair rose modestly by 0.2%.

US jobs data bolster expectations for Fed rate cuts

Investor sentiment was also shaped by U.S. economic data released last Friday, which revealed that nonfarm payroll growth in December slowed more than anticipated.

The weaker-than-expected hiring numbers have heightened expectations that the Federal Reserve may implement interest rate cuts later this year.

Market pricing now factors in at least one additional Fed rate cut in 2026, with some traders anticipating two reductions.

Attention is now turning to the U.S. consumer price index for December, due Tuesday, a key economic indicator ahead of the Fed’s upcoming policy meeting later this month.

Ankur Banerjee provides a preview of the day ahead in European and global markets. Investors remain focused on the escalating conflict between U.S. President Donald Trump and Federal Reserve Chair Jerome Powell, who is pushing back against attempts to exert political control over the Fed and its interest rate decisions.

Meanwhile, growing turmoil in Iran—where over 500 people have reportedly been killed, according to human rights groups—adds to the geopolitical uncertainties shaping market sentiment at the start of 2026, supporting demand for safe-haven assets.

Markets opened Monday with shocking news that the Trump administration had threatened to indict Powell over his Congressional testimony last summer concerning a Fed building renovation. Powell described this as a “pretext” aimed at increasing political influence over monetary policy.

“This issue centers on whether the Fed can continue setting interest rates based on data and economic realities, or if monetary policy will instead be shaped by political pressure and intimidation,” Powell stated.

The initial market reaction saw the dollar weaken and stock futures decline, although the impact on interest rate policy remains unclear. Gold prices surged past $4,600 per ounce as investors sought refuge.

Despite the unsettling news, market responses were measured, with no signs of panic selling as investors await further clarity on the Fed’s independence and the future path of interest rates.

WASHINGTON, DC – DECEMBER 13: U.S. Federal Reserve Board Chairman Jerome Powell speaks during a news conference at the headquarters of the Federal Reserve on December 13, 2023 in Washington, DC. The Federal Reserve announced today that interest rates will remain unchanged. (Photo by Win McNamee/Getty Images)

Markets may now generally anticipate that the Federal Reserve will yield to Trump’s influence and ease interest rates freely once a new Fed chair takes over after Powell’s term ends in May. Futures pricing currently reflects expectations of two rate cuts this year.

With Japanese markets closed on Monday, no cash trading occurred in Treasuries during Asian hours. Attention will shift to the Treasury market when London trading begins.

Key events that could impact markets on Monday include: Germany’s November current account balance and the euro zone Sentix investor confidence index for January.

TASIILAQ, GREENLAND — For decades, oil executives have eyed the Arctic as a potential source for vast petroleum reserves. U.S. government studies estimate that the region north of the Arctic Circle may contain up to 90 billion barrels of oil and nearly 1,700 trillion cubic feet of natural gas.

The amount of oil alone could meet global demand for almost three years if all other drilling activities worldwide stopped immediately.

At the heart of these ambitions lies Greenland, where some of the planet’s most extreme conditions safeguard vast reserves that have attracted prospectors hoping to find another giant oil field like Alaska’s Prudhoe Bay.

One company, March GL—set to be renamed Greenland Energy Company upon going public this year—is aiming to become a major player in the industry by tapping into billions of barrels of oil located on Jameson Land, a peninsula on Greenland’s eastern coast. This oil has the potential to significantly impact U.S. and European markets by introducing a large new supply, which could help reduce Europe’s reliance on Russian oil, currently constrained by strict sanctions due to the ongoing war in Ukraine.

In late October, Yahoo Finance joined March GL CEO and experienced oilman Robert Price, along with the company’s lead petroleum engineer, in the town of Tasiilaq on Greenland’s eastern coast. There, March GL’s contractors were preparing to store a range of heavy machinery for the winter season.

Price had planned to transport the earthmoving equipment by barge to Jameson Land, where the company intends to build a three-mile road from the coast to its inland drilling site for the initial wells. However, rough seas along the island’s eastern coast prevented the tugboat assigned to move the equipment from making the trip. By late autumn, the ice-free window for such a journey was closing too fast to wait for a replacement vessel.

As a result, March GL’s team will keep much of the machinery in Tasiilaq until spring or summer, when thawing ice will allow movement. This delay underscores the challenging and unpredictable operating conditions in Greenland.

Since that trip, the challenges around Price’s ambitions in Greenland have only grown more complex.

After Venezuelan leader Nicolás Maduro was captured and removed from power in early January, President Trump intensified his focus on Greenland. At a Jan. 4 press briefing, Trump said the United States “needs Greenland” to secure its national security interests in the Arctic, drawing strong criticism from both the Greenlandic and Danish governments.

At a White House meeting with more than a dozen major oil executives, Trump insisted that owning Greenland would be essential for defense, saying that defending leased territory is not the same as defending territory the U.S. owns. He added that the U.S. would take action on Greenland “whether they like it or not.”

In a Jan. 6 briefing to Congress, Secretary of State Marco Rubio confirmed that the U.S. was actively pursuing the option of purchasing Greenland from Denmark, and Louisiana Governor Jeff Landry—who Trump named as a special envoy to Greenland—said he intends to work toward making the territory part of the United States.

These moves have heightened diplomatic tensions, with Greenland’s leaders and Denmark pushing back against U.S. efforts and stressing that the island’s future should be decided by its people and legal processes.

Meanwhile, China and Russia have been expanding their military and maritime activities across the Arctic, putting pressure on the U.S. and Europe to boost their own defense readiness and elevating Greenland’s strategic importance. In January, a subsidiary of Russia’s state nuclear corporation shared a video on Telegram showing an icebreaker navigating the “Northern Sea Route,” which passes near Greenland and offers a significantly faster shipping route between Europe and Asia compared to the Suez Canal.

If March GL succeeds, Price’s company could establish a significant American energy foothold in the High North at a time when territorial control has become a top priority for the White House. That, however, was not originally part of Price’s plan.

Oil companies seeking to take part in newly approved exports of Venezuelan crude to the United States after the removal of President Nicolás Maduro are holding urgent talks to secure tankers and organize operations to safely transfer oil from ships and deteriorating Venezuelan ports, according to four sources familiar with the matter.

Trading firms and energy companies such as Chevron, Vitol, and Trafigura are vying for U.S. government contracts to export Venezuelan crude, the sources said, after President Donald Trump announced that Venezuela could deliver up to 50 million barrels of previously sanctioned oil to the United States.

Trafigura told the White House in a meeting on Friday that its first vessel is expected to load within the coming week.

After months under a U.S. blockade, Venezuela has been storing crude aboard tankers and has nearly exhausted its onshore storage capacity. Many of these vessels are aging, poorly maintained, and subject to sanctions. Due to insurance and liability restrictions, other ships cannot directly interact with sanctioned tankers—even if U.S. licenses are granted—sources added.

Onshore storage facilities have also suffered years of neglect, creating additional risks for companies attempting to load the oil.

Shipping firms including Maersk Tankers and American Eagle Tankers are among those seeking to expand ship-to-ship transfer operations in Venezuela, according to three of the sources.

According to one source, Maersk Tankers could reuse the ship-to-shore-to-ship logistics model it previously employed in Venezuela’s Amuay Bay. The company already operates in nearby Aruba and Curaçao, whose waters are frequently used for transferring Venezuelan oil. However, while such transfers are feasible in Aruba and at U.S. ports, they come at a higher cost.

In a statement, Maersk said its presence in Venezuela remains limited, with only 17 employees in the country. The company confirmed that all staff are safe and accounted for, and that there have been no changes to its ocean services. Operations are continuing with only minor delays, and the situation is being closely monitored.

Another shipping source noted that transfer operations will be further complicated by a shortage of smaller vessels needed to move oil from storage tankers to piers, where it can then be transferred to other ships, as well as by poorly maintained machinery and equipment.

American Eagle Tankers (AET), which already facilitates Chevron’s shipments of Venezuelan crude to the United States, is being contacted by potential customers seeking to expand its capacity in the region, two sources said.

Neither AET nor Chevron immediately responded to requests for comment.

Sources added that while exports could potentially return to the roughly 500,000 barrels per day that Venezuela shipped to the United States before sanctions—allowing stockpiles to be drawn down within 90 to 120 days—reaching that level will be difficult if crude must be sourced from both offshore tankers and onshore storage facilities.

Companies are also fiercely competing for loading slots at Venezuela’s main Jose oil terminal, where both capacity and operating speed are constrained. Chevron, a major joint-venture partner in the country, is working aggressively to maintain its preferential access to Venezuelan terminals while preparing its vessel fleet, according to one source.

Meanwhile, oil firms including Chevron, Vitol, and Trafigura are already securing supplies of much-needed naphtha, a Venezuelan industry source said. Naphtha is commonly blended with heavy Venezuelan crude to reduce its density, making it easier to transport and refine.

Oil prices advanced during Asian trading on Friday, extending the previous session’s rebound as investors focused on possible supply disruptions in Russia and Iran amid geopolitical risks.

At the same time, fears of an immediate rise in Venezuelan oil output subsided after the U.S. Senate approved a measure requiring congressional authorization for further military action by President Trump.

Analysts said oil production in the country is unlikely to increase sharply in the near term, even with U.S. intervention.

Brent crude futures for March rose 0.7% to $62.44 a barrel, while WTI futures gained 0.7% to $58.03 by 21:04 ET (02:04 GMT). Both benchmarks rebounded to levels seen before last week’s U.S. military action in Venezuela after posting more than 4% gains on Thursday.

Oil prices were supported by positive inflation data from China, the world’s top oil importer, signaling a tentative economic recovery. However, gains were limited as traders remained cautious ahead of key U.S. nonfarm payrolls data that could affect interest rate expectations.

Markets focus on potential supply disruptions in Russia and Iran

Concerns about possible supply disruptions in Russia and the Middle East lent support to oil prices this week.

The conflict between Russia and Ukraine showed little sign of resolution, with ongoing military actions. A drone strike on a tanker headed to Russia in the Black Sea heightened fears of further interruptions to Russian crude supplies.

Compounding these concerns, reports indicated that U.S. President Donald Trump plans to endorse a bipartisan bill imposing even tougher restrictions on countries trading with Russia, aiming to increase pressure on Moscow to seek a ceasefire.

Meanwhile, Iraq’s government approved a move to nationalize operations at the West Qurna 2 oilfield—one of the world’s largest—in an effort to avoid supply disruptions stemming from U.S. sanctions on Russia.

In Iran, escalating nationwide anti-government protests have raised worries about potential impacts on oil production. The government responded with a countrywide internet blackout as demonstrations spread across major cities protesting the Nezam regime.

Market concerns over Venezuelan oil supply ease

Oil prices benefited from easing worries that a U.S. intervention in Venezuela would lead to a significant near-term surge in global crude supply.

Earlier this week, Trump stated that Caracas could deliver up to $3 billion worth of oil to the U.S. and indicated plans for long-term U.S. influence over the country.

However, Congress has advanced legislation that may restrict U.S. military involvement in Venezuela.

Many analysts noted that while U.S. involvement could eventually help boost Venezuelan oil production, persistent political turmoil and deteriorated infrastructure make any near‑term surge in output unlikely.

Oil prices initially plunged after the U.S. detained Venezuelan President Nicolás Maduro and signaled control over the country’s oil industry, but prices had fully recovered by Friday as markets judged immediate changes to supply to be limited.

Still, crude prices were experiencing their steepest annual decline in five years in 2025, weighed down by concerns over a widening supply glut and sluggish demand growth—an outlook echoed by major global institutions forecasting continued oversupply into 2026.

Oil prices weakened yesterday after President Trump said Venezuela would supply large volumes of sanctioned crude to the United States.

Energy

Developments in Venezuela remain in the spotlight, adding further downside pressure to oil prices. President Trump said Venezuela is prepared to sell up to 50 million barrels of sanctioned crude to the United States, a move that could also immediately weigh on Canadian crude exports to the U.S.

Such a deal would effectively open a release channel for Venezuelan oil, which has struggled to reach global markets due to a U.S. blockade on sanctioned tankers entering and leaving the country. Redirecting these barrels to the U.S. could ease storage constraints and reduce the need for Venezuela to curb production.

The U.S. Department of Energy confirmed that Venezuelan crude is already being marketed internationally, while Trump’s energy secretary stated that Washington intends to maintain long-term control over future Venezuelan oil sales. This strategy is reinforced by the continued tanker blockade, with two additional vessels reportedly seized yesterday.

Washington’s growing influence over Venezuela’s oil sector also raises uncertainty about the country’s future role within OPEC.

Meanwhile, Energy Information Administration (EIA) data showed U.S. crude inventories fell by 3.83 million barrels last week, the sharpest draw since late October. However, product balances were more bearish, as gasoline stocks rose by 7.7 million barrels and distillate inventories increased by 5.6 million barrels.

These inventory builds point to refinery utilization remaining firm, while implied demand for both products softened somewhat over the past week.

European gas prices moved higher yesterday, with TTF closing more than 2.5% up on the day. Colder conditions across parts of Europe, along with forecasts for below-average temperatures in the days ahead, are supporting the market. The current cold spell has also accelerated storage drawdowns, with EU gas inventories now at 58% of capacity, compared with a five-year average of 72%.

The latest positioning data show that investment funds cut their net short exposure in TTF for a third straight week. Funds purchased 6.2 TWh during the latest reporting period, reducing their net short position to 72.4 TWh.

The ISM service index suggests potential positive revisions for fourth-quarter GDP growth. On Wednesday, the Institute for Supply Management (ISM) reported that its non-manufacturing service sector index increased to 54.4 in December from 52.6 in November, marking the third consecutive month of expansion and the fastest pace of growth in over a year.

The new orders sub-index rose sharply to 57.9 from 52.9, while business activity climbed to 56 from 54.5. Additionally, new export orders improved to 54.2, up from 48.7 in November. Out of 16 surveyed service industries, 11 showed expansion in December.

Conversely, the ISM manufacturing index fell to 47.9 in December from 48.2 the prior month, continuing its contractionary trend for the tenth straight month (a reading below 50 indicates contraction). Only 2 of 17 manufacturing industries—Electrical Equipment, Appliances & Components, and Computer & Electronic Products—reported growth, likely supported by strong data center demand.

ADP’s December report showed private payrolls increasing by 41,000, missing economists’ expectation of 48,000. This follows a loss of 29,000 private jobs in November, meaning just 12,000 private jobs were created over the last two months. Manufacturing shed 5,000 jobs in December, while education and health services added 39,000, and leisure and hospitality gained 24,000 jobs. Regionally, the West lost 61,000 private sector jobs, while the South led with a gain of 54,000.

Residential investment acted as a 5.1% drag on GDP growth during the second and third quarters. Strengthening GDP going forward will depend largely on stabilizing the residential real estate market, which remains sluggish due to high mortgage rates, rising insurance costs, and an oversupply in several key areas. According to the Intercontinental Exchange, prices for U.S. condominiums dropped 1.9% in September and October, with high homeowners association (HOA) fees and insurance expenses cited as major factors. In nine major metropolitan regions, over 25% of condominiums have fallen below their original sale prices. While multiple Federal Reserve rate cuts could help support home prices, the current weakness is fueling deflationary concerns that the Fed needs to address.

If deflation emerges from (1) weak housing and rental prices, (2) low crude oil prices, and (3) deflation imported from China and other struggling global economies, the Fed may need to implement rapid interest rate cuts totaling around 100 basis points. With President Trump expected to nominate a new Fed Chair soon, current Chair Jerome Powell is likely to become a lame duck. Minutes from the December Federal Open Market Committee (FOMC) meeting indicated at least one more 0.25% rate cut is probable, but any further deflationary signals could prompt the Fed to enact much larger reductions in key rates in the coming months.

President Trump is expected to nominate a new Federal Reserve Chair in January who will likely reverse the Fed’s current restrictive policies and adopt a more pro-business stance. Should Kevin Hassett, the current Chair of the Council of Economic Advisors, be appointed, the Fed would gain a strong economic advocate, a development that many find promising and exciting.

Oil prices climbed during Asian trading on Thursday, regaining some losses after sharp declines triggered by worries over rising Venezuelan crude supplies.

Additionally, stronger-than-anticipated weekly declines in U.S. oil inventories supported the price recovery. Ongoing conflict between Russia and Ukraine also contributed to maintaining a risk premium in the market.

March Brent crude futures increased by 0.7% to reach $60.38 per barrel, while West Texas Intermediate (WTI) futures also gained 0.7%, settling at $56.28 per barrel as of 20:25 ET (01:25 GMT). Both benchmarks had fallen more than 1% over the previous two sessions.

Attention turns to US – Venezuela oil agreement after Trump highlights up to $3 billion in planned crude sales

Oil markets are closely watching the impact of a new agreement between the U.S. and Venezuela on global oil supplies.

U.S. President Donald Trump announced on Tuesday that Venezuela will deliver between 30 million and 50 million barrels of oil to the U.S., valued at up to $3 billion, shortly after U.S. forces detained Venezuelan President Nicolás Maduro.

Trump also appeared to encourage multiple U.S. oil companies to expand production activities in Venezuela, with Chevron Corp (NYSE: CVX) leading these efforts. According to Reuters, Chevron is negotiating to broaden its license to operate in the country.

Currently, Chevron is the only major U.S. oil company active in Venezuela, benefiting from special government exemptions that shield it from stringent sanctions imposed on the nation.

Markets are worried that a significant rise in Venezuelan oil output could further swell global supplies, adding to prevailing fears of an oil glut in 2026. Traders are already pricing in ample supply conditions, with expectations that any additional barrels from Venezuela might weigh on crude prices.

However, analysts caution that any meaningful increase in Venezuelan production is unlikely to happen quickly, given the country’s deep political instability and the extensive investment needed to rebuild its dilapidated oil infrastructure after recent upheavals.

A Financial Times report also noted that U.S. oil firms are seeking strong legal and financial guarantees from the U.S. government before committing to major investments in Venezuela’s oil sector, reflecting industry hesitancy amid uncertain policy and market conditions.

U.S. crude stockpiles decline beyond forecasts

Government data released Wednesday revealed that U.S. oil inventories fell by 3.8 million barrels in the week ending January 2, significantly exceeding expectations of a 1.2 million barrel decline.

This reduction was almost double the 1.9 million barrel draw reported the previous week, bolstering confidence that demand remains robust in the world’s largest fuel consumer.

Attention this week centers on several key U.S. economic reports, especially the December nonfarm payrolls data set to be released on Friday, which is expected to influence interest rate forecasts.

U.S. stock index futures were mostly flat on Wednesday evening, after Wall Street’s major benchmarks ended the session broadly lower from record highs, as investors looked ahead to key U.S. employment data due later this week.

S&P 500 futures edged up 0.1% to 6,967.0, while Nasdaq 100 futures were little changed at 25,837.25 by 20:03 ET (01:03 GMT). Dow Jones futures also added 0.1% to 49,263.0.

Wall Street Pulls Back From Record Highs Ahead of U.S. Jobs Data

During the session, the S&P 500 declined 0.3%, while the Dow Jones Industrial Average dropped 0.9%. In contrast, the Nasdaq Composite added 0.2%, supported by selective gains among large-cap technology stocks that helped offset broader market weakness.

Both the S&P 500 and the Dow had reached record highs in the previous session, and the mixed performance pointed to some profit-taking after the recent rally.

Figures from payroll processor ADP showed that private-sector job growth in December came in below expectations, signaling a slowdown in hiring momentum toward year-end.

Although the ADP report is often seen as volatile and not always a reliable guide to official government data, it added to evidence that the labor market may be gradually cooling.

Focus now shifts to Friday’s highly anticipated nonfarm payrolls report, which is expected to offer clearer insight into employment trends and wage growth. The data will be closely watched by markets evaluating the probability and timing of potential Federal Reserve rate cuts in the months ahead. Weaker-than-expected job growth could reinforce expectations that the Fed may begin easing policy earlier in 2026.

Attention on rising tensions between the US and Venezuela

Geopolitical strains continued to run high after U.S. forces apprehended Venezuelan President Nicolás Maduro, yet financial markets have so far exhibited only limited, short‑lived reactions to the dramatic turn of events. Investors appear to be largely unfazed by the heightened political risk, although the episode has introduced fresh uncertainty into the outlook for energy markets. U.S. President Donald Trump stated that Venezuela’s interim leadership would transfer up to 50 million barrels of crude oil to the United States.

After months of rising tensions, the United States launched a major military operation in Venezuela on 3 January 2026, resulting in the capture of President Nicolás Maduro and his wife, Cilia Flores. U.S. President Donald Trump confirmed the operation, saying Washington would administer Venezuela until a stable transition government could be established. This marks one of the most dramatic U.S. interventions in Latin America in decades, with Maduro removed from power and taken into U.S. custody.

Maduro, long a focal point of U.S. sanctions and foreign policy pressure, was transported to the United States to face federal charges—such as narco‑terrorism and drug trafficking—filed in the Southern District of New York.

Venezuela holds the world’s largest proven oil reserves, and the sudden change in leadership carries significant geopolitical and economic implications well beyond its borders.

Why Did the US Capture Maduro?

Nicolás Maduro rose through the Venezuelan political system under socialist leader Hugo Chávez and became president in 2013. His time in power was widely criticized domestically and internationally, with opponents accusing him of suppressing dissent, restricting freedoms, and holding elections that lacked credibility.

Relations with Washington deteriorated sharply, especially under the Trump administration. U.S. officials accused Maduro’s government of involvement in drug trafficking and creating conditions that fueled migration toward the United States. They also branded elements of his regime—including the Cartel of the Suns—as a terrorist organization.

Tensions escalated in 2025 when the U.S. increased the bounty for Maduro’s arrest to $50 million and expanded military pressure in the region, including strikes on vessels the U.S. claimed were tied to drug smuggling.

On 3 January 2026, after months of military buildup and diplomatic pressure, U.S. forces launched a major operation in Venezuela—code‑named Operation Absolute Resolve—that resulted in the capture of Maduro and his wife. The U.S. government framed the intervention as a law‑enforcement action tied to longstanding criminal charges against Maduro, including narcoterrorism.

The United States claims that Venezuelan officials were engaged in government‑backed drug trafficking, asserting links with the so‑called Cartel of the Suns, which Washington has designated as a terrorist organization—a claim Maduro vehemently rejects. He argues that U.S. actions were aimed at forcing regime change and securing control over Venezuela’s vast oil riches.

Only hours before his detention, Maduro made his final public appearance as president when he hosted China’s special envoy, Qiu Xiaoqi, at the Miraflores Palace to discuss bilateral relations—an event that highlighted Caracas’s reliance on foreign partnerships for political support. Shortly after that meeting, explosions were reported across Caracas.

The event went beyond a simple arrest; it sent a broader strategic message, particularly to countries like China and Iran, undermining the belief that the U.S. would refrain from acting against governments supported by foreign adversaries.

Drill, Baby, Drill

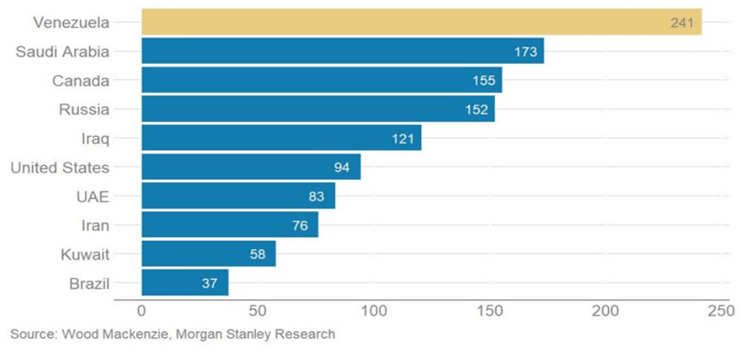

A major strategic factor behind U.S. actions in Venezuela appears to be securing access to its vast energy resources. Venezuela sits on the largest proven oil reserves on the planet, with estimates from Wood Mackenzie suggesting roughly 241 billion barrels of recoverable crude, making it a uniquely significant player in global oil markets.

Top Countries by Proven Oil Reserves (Billion Barrels)

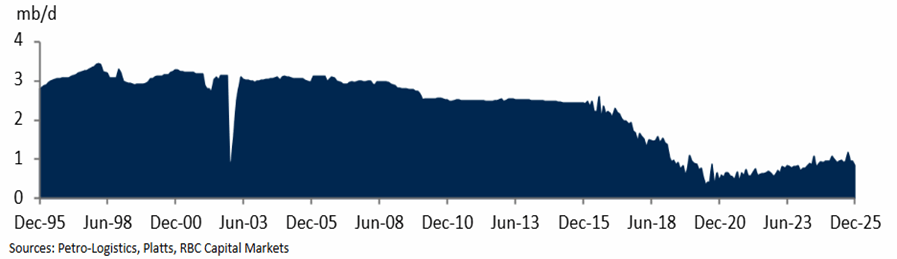

However, Venezuela’s track record of oil output underscores just how challenging it has been to tap into its vast reserves. In the late 1990s and early 2000s, the nation was capable of producing close to 3 million barrels per day—a level that made it one of the world’s top crude exporters. But political turmoil, labor strikes, and the restructuring of the oil sector under Hugo Chávez triggered a prolonged decline. The downturn was steepened further by U.S. sanctions starting in 2017, which restricted investment, technology, and exports, driving production down sharply. After bottoming out around 374,000–500,000 bpd during the worst of the crisis, output has only modestly recovered in recent years and remains in the range of approximately 800,000–900,000 bpd.

Historical Total Venezuelan Supply

Expectations that Venezuelan oil output could quickly rebound may overstate what’s realistically achievable. History shows that even after major disruptions, rebuilding oil production takes many years and vast investment. For example, Iraq needed almost a decade and well over $200 billion in capital to restore its output after the Iraq War, while Libya still has not returned to its pre‑2011 production levels.

Venezuela’s challenges are even more severe. Most of its reserves are extra‑heavy crude that demands upgrading and blending with diluents before it can be transported and refined, a costly and technical process. Years of underinvestment, international sanctions, the erosion of PDVSA’s workforce, and the deterioration of infrastructure have compounded these production hurdles. Pipelines, upgraders, and refineries have been left in poor condition, and limited access to modern technology continues to restrict any rapid recovery.

While PDVSA has claimed that facilities were not physically damaged in recent events—suggesting limited short‑term disruption—oil markets appear capable of absorbing this uncertainty for now. Inventories remain ample, and OPEC+ has signalled that its voluntary cuts of around 1.65 million bpd could be reversed if necessary to balance markets.

In a scenario where a pro‑U.S. government enables sanctions relief and attracts foreign investment, Venezuelan exports could gradually recover. But bringing production back to around 3 million bpd would take many years and substantial infrastructure upgrades. U.S. leadership has indicated that American oil companies would play a role in operating and developing Venezuela’s oil sector, though analysts note that the heavy crude’s technical challenges and investment risks remain significant.

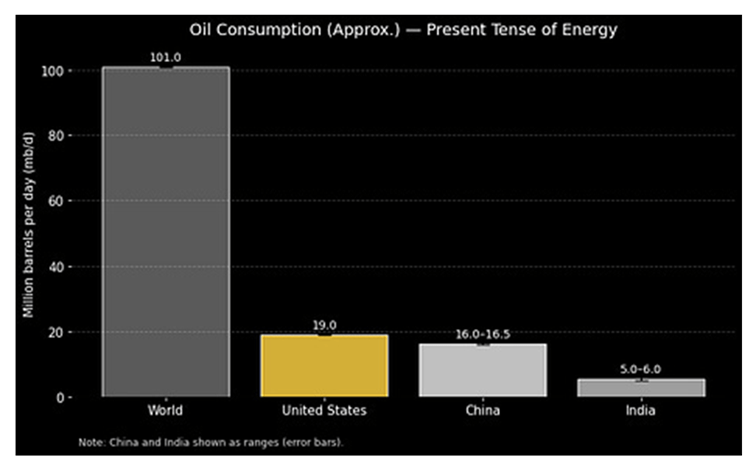

Meanwhile, global oil markets are structurally tightening, with world consumption exceeding 101 million bpd driven by demand growth in the U.S., China, and India. Any short‑term impact on supply may show up as a modest increase in geopolitical risk premiums, but over time, the sidelined Venezuelan barrels—currently producing around 800,000–900,000 bpd—could eventually add supply and influence prices if output scales up gradually.

In addition to oil, Venezuela sits on a wealth of mineral resources. Large deposits of iron ore, bauxite, gold, nickel, copper, zinc and other metallic minerals are concentrated mainly in the southern Guayana Shield region. The country also ranks among Latin America’s largest holders of gold, and geological assessments identify significant iron and bauxite resources alongside reserves of coal, antimony, molybdenum and other base metals.

Despite this geological potential, commercial mining activity remains very limited. Most non‑oil mineral sectors contribute only a tiny fraction of Venezuela’s economic output, and substantial foreign investment has largely been absent, meaning much of the nation’s mineral wealth has yet to be developed into large‑scale production.

The Ongoing Economic Battle Between the United States and China

Competition between modern empires today is no longer about direct confrontation but about control over key inputs. Energy, metals, and critical materials form the foundation of the modern world. When leaders signal a willingness to secure these resources directly, markets should interpret this not as mere rhetoric, but as a concrete resource strategy.

The rivalry between the United States and China is fundamentally structural rather than ideological. The U.S. is rich in energy but dependent on imported metals and rare earths. China dominates metals processing but imports around 70% of its crude oil. Each side is strong where the other is vulnerable, and both seek to turn this imbalance into strategic advantage.

Control over energy flows also carries monetary implications. Influence over Venezuelan oil is not only about supply, but also about reinforcing the petrodollar and preventing the rise of the petroyuan.

There is also a regional dimension to this rivalry. China has steadily increased its presence in Latin America through infrastructure projects and commodity-backed financing. Recent U.S. moves indicate an effort to reassert dominance in the Western Hemisphere, compelling Beijing to compete on less advantageous terms. The Trump administration’s 2025 National Security Strategy elevated the region to a core priority, effectively reviving the logic of the Monroe Doctrine—rebranded as the “Donroe Doctrine.” The aim is to bring strategically important natural resources, especially critical minerals and rare earths, under U.S.-aligned corporate control while building a hemisphere-wide supply chain that reduces dependence on China.

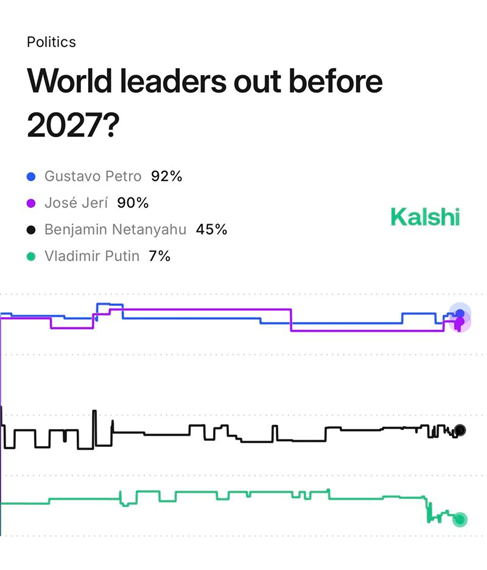

Across much of South America, governments are edging closer to Washington, leaving Brazil increasingly isolated. This is significant given President Lula’s openly left-leaning stance and his consistent alignment with Russia, China, and Iran. Following Trump’s capture of Maduro, betting markets on Kalshi assign a 90% probability that the presidents of Colombia and Peru will be out of office before 2027. At the same time, President Trump has again stated that Greenland should become part of the United States, reinforcing a broader strategy centered on securing critical assets.

Which Assets Could Gain from “Nation Building” in Venezuela?

A political transition in Venezuela would most directly benefit assets tied to sovereign debt restructuring, energy infrastructure, and the oil supply chain.

Venezuelan bonds are currently priced at roughly 25–35 cents on the dollar, reflecting the impact of sanctions and ongoing legal uncertainty. Under a regime-change scenario, several analysts project potential recoveries in the 30–55 cent range, supported by the prospects of debt restructuring and the easing or removal of sanctions.

Ashmore continues to rank among the largest institutional holders of Venezuelan sovereign debt. Advisory firms such as Houlihan Lokey—financial adviser to the Venezuela Creditor Committee—and Lazard, a veteran of major sovereign restructurings (including Greece and Ukraine), would likely stand to gain from the sheer scale and complexity of any debt workout. In such processes, advisers typically earn success-based fees and function as the “picks and shovels” of restructuring. Venezuela’s debt structure is widely regarded as one of the most intricate ever assembled.

Reviving Venezuela’s oil industry would demand swift rehabilitation of aging infrastructure. Technip, which historically designed much of the country’s core oil facilities, is well placed to play a leading role given its proprietary expertise—particularly if emergency repairs are fast-tracked through sole-source or no-bid contracts. Graham Corporation, a supplier of vacuum ejector systems used in heavy-oil upgrading and refining, could also benefit, since Venezuela’s crude requires vacuum distillation to prevent it from solidifying into coke.

Before exports can meaningfully increase, Venezuela will need to import substantial volumes of diluent (such as naphtha or natural gasoline) to transport its heavy crude through pipelines. Targa Resources, operator of the Galena Park Marine Terminal in Houston—a major LPG and naphtha export hub—would be a natural beneficiary if Venezuela pivots back to U.S. diluent supplies, replacing current inflows from Iran.

The clearest corporate beneficiary of regime change and nation-building in Venezuela is Chevron (NYSE: CVX). Unlike other U.S. energy majors that exited the country, Chevron has maintained an on-the-ground presence. It retains the workforce, regulatory approvals (through OFAC), and operational assets—most notably Petroboscan and Petropiar—that position it to scale up production quickly. Exxon Mobil (NYSE: XOM) and ConocoPhillips (NYSE: COP), both of which hold legacy claims and arbitration awards stemming from past expropriations, could also regain market access or pursue compensation under a revised legal and political framework.

Refiners along the U.S. Gulf Coast—such as Valero Energy (NYSE: VLO), Phillips 66 (NYSE: PSX), and Marathon Petroleum (NYSE: MPC)—were purpose-built to handle heavy, sour crude like that produced in Venezuela. Since the imposition of sanctions, these companies have had to rely on costlier substitute feedstocks. A resumption of Venezuelan supply would reduce input costs and support refining margins, assuming end-product demand remains stable.

At the sector level, a significant increase in Venezuelan output would likely weigh on oil prices, which would be negative for crude producers but positive for consumer-oriented equities. Lower energy prices are inherently deflationary and could translate into lower bond yields—conditions that are generally supportive of risk assets, all else equal.

Note: This section is for analytical purposes only and does not constitute investment advice.

Venezuela: What Comes Next for the Economy and Markets?

In a characteristically Trump-like approach, President Trump initially stated that the United States would “administer” Venezuela during the transition period. U.S. officials later confirmed that approximately 15,000 troops would remain stationed in the Caribbean, with the option of further intervention if the interim authorities in Caracas failed to comply with Washington’s demands.

Venezuela’s Supreme Court subsequently named Vice President Delcy Rodríguez as interim president. A close ally of Maduro since 2018, Rodríguez previously oversaw much of the oil-dependent economy and the country’s intelligence structures, placing her firmly within the existing power framework. She signaled a willingness “to cooperate” with the Trump administration, hinting at a potentially dramatic reset in relations between the two long-hostile governments.

International observers, including the United Nations and the Carter Center, have concluded that Venezuela’s 2024 elections lacked legitimacy and fell short of international standards. Independently verified tally sheets reviewed by analysts indicated that opposition candidate Edmundo González secured around 67% of the vote, compared with roughly 30% for Maduro.

At the same time, María Corina Machado—Nobel Peace Prize laureate and a leading figure in Venezuela’s opposition—is expected to return to the country later this month and has said the opposition is ready to take power. President Trump, however, has publicly cast doubt on the breadth of her support among the Venezuelan population.

In this context, three potential scenarios appear likely, as outlined by Gavekal Research:

“Soft” Military Rule

In the near term, the most probable outcome is the continuation of the current power structure under Rodríguez and the armed forces. For this arrangement to endure, it would likely require a pragmatic shift toward U.S. priorities—embracing a more business-friendly approach and loosening ties with traditional partners such as Russia, China, and Iran. Washington may be willing to accept this scenario if it ensures political stability and reliable access to energy supplies.

Democratic Transition

A negotiated move toward civilian governance would hinge largely on how new elections are structured. Allowing participation from the Venezuelan diaspora could significantly reshape the results, whereas restricting voting to residents inside the country would be more likely to benefit factions linked to the existing regime.

“Libya Redux” (State Breakdown)

The most destabilizing scenario would involve the collapse of central authority, triggering internal military conflict and the proliferation of armed groups. Such an outcome would heighten the risk of civil strife, renewed migration pressures, and severe disruptions to oil production and global energy markets.

Oil prices tumbled in Asian trading on Wednesday after U.S. President Donald Trump said Venezuela would deliver tens of millions of barrels of crude to the United States, a development expected to significantly increase global supply. Prices were already under pressure earlier in the week, as Washington’s takeover of Venezuela fueled expectations of a broad easing of sanctions on the country’s oil sector—potentially releasing tens of millions of barrels back onto the market.

Despite elevated geopolitical risks adding a modest risk premium, oil prices stayed under pressure as markets grew increasingly concerned about a potential supply glut in 2026. Crude was already on track for its steepest annual decline in five years in 2025. Brent futures for March slid 1% to $60.11 a barrel at 20:13 ET (01:13 GMT), while U.S. benchmark WTI dropped 1.1% to $56.29 a barrel.

Venezuela to send 30–50 million barrels of crude to the United States, Trump says

In a post on social media, Trump said Venezuela would transfer between 30 and 50 million barrels of oil to the United States, with Washington planning to sell the crude at prevailing market prices. He added that the proceeds from the sales would be managed by him as U.S. president, stating that the funds would be used to serve the interests of both Venezuela and the United States.

The announcement follows just days after U.S. forces detained Venezuelan President Nicolas Maduro, when Trump said Washington was taking control of the country and planned to open up its oil sector. Oil prices initially fell after Maduro’s capture, as markets anticipated that a potential easing of U.S. sanctions on Venezuela could unleash large volumes of crude onto global markets. Trump’s actions since then suggest that this outcome is increasingly likely.

However, analysts cautioned that any reopening of Venezuela’s energy industry could take longer than expected, citing risks of political instability and the constraints of the nation’s aging infrastructure. Data from maritime analytics firm Kpler also indicated that a near-term increase in Venezuelan output is unlikely due to limited domestic storage capacity.

Russia-Ukraine ceasefire draws attention as U.S. backs security guarantees for Kyiv

Oil markets were also tracking any fresh developments in talks on a Russia–Ukraine ceasefire after the United States on Tuesday endorsed a largely European-led coalition that pledged to provide security guarantees for Kyiv.

The U.S. commitment was made at a Paris summit aimed at reassuring Ukraine in the event of a truce with Moscow. Washington also said it was prepared to help monitor and verify any ceasefire should an agreement be reached. However, Russia has so far shown limited willingness to engage in a ceasefire, with fighting between the two sides continuing as the war moves toward its fifth consecutive year.

Even so, any prospective ceasefire between Russia and Ukraine could ultimately lead to a rollback of U.S. sanctions on Moscow, allowing additional Russian oil to return to the market. Such a development would also reduce the geopolitical risk premium embedded in crude prices.

U.S. President Donald Trump said on Tuesday night that Venezuela’s interim government would transfer tens of millions of barrels of oil to the United States, with the proceeds from sales to be managed by Washington. In a social media post, Trump said Caracas would hand over between “30 and 50 million barrels of high-quality, sanctioned oil,” which would be sold at market prices. He added that the revenue would be overseen by him as president to ensure it benefits both the Venezuelan and U.S. people, and noted that he had directed Energy Secretary Chris Wright to implement the plan immediately.

The proposed arrangement could redirect Venezuelan oil exports away from China while helping state-run PDVSA avoid deeper production cuts, following reports that Washington and Caracas were in talks over a supply agreement. The announcement comes days after U.S. forces captured President Nicolas Maduro, heightening political uncertainty in Venezuela. Maduro’s vice president, Delcy Rodriguez, was sworn in as interim leader this week and has signaled her willingness to cooperate with Washington.

Trump said the United States would oversee Venezuela until a permanent leader is elected and would also assume control of the country’s aging oil sector. Following the announcement, oil prices fell, as a U.S. takeover could bring large volumes of crude to market and boost supply. March Brent futures dropped 2%.