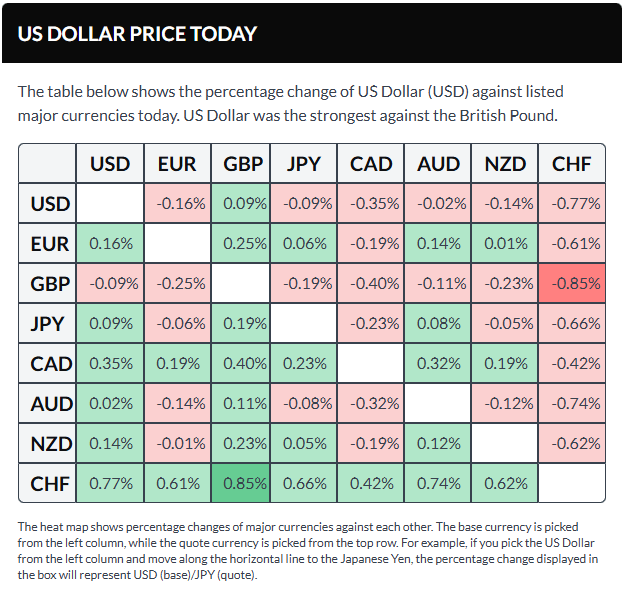

The U.S. dollar weakened this week amid ongoing geopolitical tensions and renewed uncertainty over U.S. trade policy. The setback followed a ruling by the Supreme Court of the United States declaring the Trump administration’s tariffs illegal, prompting President Donald Trump to announce a fresh round of levies. Even stronger-than-expected Producer Price Index (PPI) data failed to revive the greenback.

The U.S. Dollar Index (DXY) hovered near the 97.60 area, down about 0.20% on the day and ending the week modestly lower, as traders remained cautious amid trade and geopolitical uncertainty.

EUR/USD traded around 1.1810, edging higher during the U.S. session after Germany’s flash Harmonized Index of Consumer Prices (HICP) for February came in softer than expected at 2% year-on-year (vs. 2.1% forecast) and 0.4% month-on-month (vs. 0.5%). Investors also evaluated testimony from Christine Lagarde, President of the European Central Bank, before the European Parliament. Lagarde reiterated that inflation is gradually returning to the 2% target and said she intends to complete her term, dismissing speculation about an early departure.

GBP/USD hovered near 1.3470, rebounding after nearly revisiting a one-month low earlier in February. Meanwhile, Andrew Bailey, Governor of the Bank of England, indicated there is room for rate cuts as inflation is expected to move back toward the 2% target.

USD/JPY traded near 156.00, stabilizing after recouping most of its intraday losses. Tokyo’s February CPI rose 1.6% year-on-year, with the core measure excluding fresh food falling below the Bank of Japan’s 2% target for the first time since 2024.

AUD/USD climbed back toward 0.7120, turning positive after reversing earlier declines. Attention now shifts to Australia’s TD-MI Inflation Gauge, due Monday.

USD/CAD hovered around 1.3630, marking nearly a two-week low, as markets assessed economic data from both sides of the border. According to Statistics Canada, Canada’s GDP contracted at an annualized 0.6% rate in the fourth quarter, following a revised 2.4% expansion in Q3.

Gold traded near $5,260, reaching a one-month high amid persistent geopolitical uncertainty. The precious metal is attempting to retest its all-time high of $5,598 set earlier this year.

Anticipating economic perspectives: Key voices in focus

Sunday, March 1

Joachim Nagel – European Central Bank

Monday, March 2

Frank Elderson – European Central Bank

Joachim Nagel – European Central Bank

Christine Lagarde – European Central Bank

Dave Ramsden – Bank of England

Michele Bullock – Reserve Bank of Australia

Tuesday, March 3

Kazuo Ueda – Bank of Japan

John C. Williams – Federal Reserve

Olaf Sleijpen – European Central Bank

Martin Kocher – European Central Bank

Neel Kashkari – Federal Reserve

Wednesday, March 4

Piero Cipollone – European Central Bank

Tiff Macklem – Bank of Canada

Luis de Guindos – European Central Bank

Thursday, March 5

Luis de Guindos – European Central Bank

Martin Kocher – European Central Bank

Christine Lagarde – European Central Bank

Friday, March 6

Piero Cipollone – European Central Bank

Mary Daly – Federal Reserve

Beth Hammack – Federal Reserve

Scott Paulson – Federal Reserve

Central bank meetings and key data releases set to steer monetary policy outlook

Monday, March 2

Australia: TD-MI Inflation Gauge

China: February RatingDog Manufacturing PMI

Germany: January Retail Sales

Switzerland: January Real Retail Sales

Spain: February HCOB Manufacturing PMI

Italy: February HCOB Manufacturing PMI

Germany: February HCOB Manufacturing PMI

Canada: February S&P Global Manufacturing PMI

U.S.: February ISM Manufacturing Employment Index

U.S.: February ISM Manufacturing New Orders Index

U.S.: February ISM Manufacturing PMI

U.S.: February ISM Manufacturing Prices Paid

New Zealand: January Building Permits (s.a.)

Japan: January Unemployment Rate

Tuesday, March 3

Australia: January Building Permits

Eurozone: HICP (Harmonized Index of Consumer Prices)

The U.S. dollar steadied on Thursday, recovering from earlier declines after upbeat earnings from AI heavyweight Nvidia, as investors looked ahead to further clarity on upcoming U.S. tariff measures.

As of 03:00 ET (08:00 GMT), the US Dollar Index, which measures the greenback against six major peers, was up 0.1% at 97.650. Despite the modest rebound, the index remained on course for a weekly drop of roughly 0.2%.

Dollar Holds Steady Following Strong Results from Nvidia

The dollar steadied after starting the session under pressure, as stronger-than-expected earnings from Nvidia lifted investor sentiment and reduced demand for the traditional safe-haven currency.

The world’s most valuable company reported January-quarter revenue that topped analyst forecasts and projected current-quarter sales above market expectations, reinforcing optimism around the AI theme.

“Improved sentiment has weighed on the dollar over the past 24 hours, with only the yen faring worse among G10 currencies yesterday,” analysts at ING Group noted.

Markets are also watching how the Trump administration responds to the February 20 Supreme Court decision that invalidated the president’s emergency tariffs. Meanwhile, U.S. Trade Representative Jamieson Greer said Wednesday that tariff rates for certain countries will increase to 15% or more from the newly introduced 10%, though he did not specify which trading partners would be affected.

In addition, U.S. and Iranian officials are set to meet in Geneva to discuss a potential nuclear agreement, with Donald Trump warning that “bad things” could occur if meaningful progress is not made.

According to ING, any escalation in tensions could serve as the most credible trigger for a broader dollar rally, particularly given the supportive backdrop from Nvidia’s results and the absence of major economic data releases. Overall, while the dollar may find some near-term stability, downside risks persist as the positive spillover from Nvidia’s earnings keeps investors leaning away from defensive currencies for now.

Euro edges lower

In Europe, EUR/USD slipped 0.1% to 1.1798 ahead of the latest Eurozone consumer confidence data due later in the session.

Still, both these figures and Friday’s inflation release are unlikely to move the needle much for the single currency, as the European Central Bank is widely expected to leave interest rates unchanged for the foreseeable future.

“For now, the EUR/USD short-term rate differential remains unsupportive for the pair, but we haven’t seen a sufficient rebound in dollar confidence to call for a significant downside break. We continue to view 1.1750 as solid support, absent a major escalation involving Iran,” analysts at ING Group said.

Meanwhile, GBP/USD declined 0.3% to 1.3523, with sterling failing to gain traction despite improved sentiment data from the UK’s business and professional services sector.

The latest quarterly survey from the Confederation of British Industry showed optimism in the sector rebounded sharply to -3 in February from -50 in November — its strongest reading since August 2024.

Yen Strengthens Following Interview with Kazuo Ueda

In Asia, USD/JPY slipped 0.3% to 156.01 after Kazuo Ueda, governor of the Bank of Japan, told the Yomiuri Shimbun that policymakers will внимательно assess incoming data at their March and April meetings, keeping the door open to another rate hike if inflation and wage growth remain solid.

His comments bolstered expectations that Japan will stay on a gradual path toward policy normalization.

The yen had weakened the previous day following reports that Prime Minister Sanae Takaichi adopted a cautious stance on additional rate increases, alongside news that two dovish-leaning nominees were selected for the BOJ board.

Meanwhile, USD/CNY declined 0.4% to 6.8392, hitting a fresh 34-month low amid anticipation of supportive measures ahead of China’s annual legislative gathering, the National People’s Congress. Investors are looking for growth targets and potential fiscal stimulus signals from the meeting, which typically outlines Beijing’s economic agenda for the year.

Elsewhere, AUD/USD eased 0.1% to 0.7114, while NZD/USD fell 0.2% to 0.5988.

The U.S. dollar weakened on Monday as investors assessed the implications of the Supreme Court of the United States decision to strike down tariffs introduced by Donald Trump, along with the administration’s subsequent response.

Traders were also monitoring renewed nuclear negotiations between Washington and Tehran.

As of 14:12 ET (19:12 GMT), the Dollar Index — which measures the greenback against a basket of six major currencies — was down 0.2% at 97.65. The currency had posted a gain of roughly 1% last week, marking its strongest weekly advance in more than four months.

Dollar pressured by mounting trade uncertainty

The Supreme Court of the United States ruled on Friday that sweeping tariffs introduced by Donald Trump exceeded his authority. In response, Trump criticized the court and unveiled a blanket 15% levy on imports.

The new duties are set to remain in place for 150 days, but it remains unclear whether the U.S. government must reimburse importers for tariffs already collected, as the Court did not address that issue.

The uncertainty could trigger prolonged legal battles and further confusion as Trump explores alternative mechanisms to reinstate broad-based global tariffs on a more permanent footing.

Thierry Wizman, global FX and rates strategist at Macquarie, said the firm’s bearish U.S. dollar outlook for 2026 was based on the view that tariffs signal U.S. “disengagement” from the rules-based order underpinning free trade. He added that tariff conflicts themselves generate uncertainty centered on the United States — a negative for the dollar.

“In that sense, while the Supreme Court ruling may have strengthened institutional checks, it also heightens uncertainty, as Trump is likely to revive the tariff war through different — and more legally grounded — channels that have yet to be detailed. We see no reason to revise our broader expectation for a weaker USD in 2026,” Wizman said.

Beyond trade policy, investors are also watching a U.S. military buildup in the Middle East aimed at pressuring Iran to abandon its nuclear ambitions, with further talks between Washington and Tehran expected later this week.

Euro advances as confidence in Europe strengthens

In Europe, EUR/USD rose 0.2% to 1.1799, with the single currency drawing support from trade-driven weakness in the dollar.

Growing confidence in the region’s economic outlook also underpinned the euro, following data on Friday showing eurozone business activity expanded faster than expected this month, as manufacturing returned to growth for the first time since October.

Momentum was reinforced on Monday as Germany’s Ifo business climate index climbed to 88.6 from 87.6 the previous month, signaling improving sentiment in Europe’s largest economy.

Meanwhile, GBP/USD added 0.1% to 1.3497, with sterling firming ahead of key event risks this week — including testimony before the Treasury Committee by Andrew Bailey, governor of the Bank of England, and Thursday’s UK by-election in Gorton and Denton.

Yen edges higher

In Asia, USD/JPY fell 0.4% to 154.48, with the Japanese yen supported by its traditional safe-haven appeal as investors remained cautious about the economic impact of higher U.S. tariffs. Trading volumes were thinner due to a public holiday in Japan.

USD/CNY was little changed at 6.9087, with Chinese markets shut for New Year holidays. Elsewhere, AUD/USD declined 0.3% to 0.7060, while NZD/USD also dropped 0.3% to 0.5961.

Thierry Wizman of Macquarie said that while the dollar could remain under pressure amid persistent U.S.-driven uncertainty, some currencies — such as the yuan and the euro — may outperform, whereas others, including the Canadian and Mexican pesos, could lag. He added that even in the face of potential credit rating actions, long-term U.S. Treasury yields might rise due to uncertainty over revenue replacement, and equities could come under strain if higher yields lead to valuation compression.

Oil prices edged higher during Asian trade on Tuesday, remaining just under the seven-month peaks reached in the prior session, as markets looked ahead to upcoming U.S.–Iran discussions later this week. Ongoing uncertainty surrounding trade tariffs continued to temper investor sentiment.

At 22:22 ET (03:22 GMT), Brent crude futures climbed 0.8% to $72.04 per barrel, while U.S. West Texas Intermediate (WTI) crude futures also advanced 0.8% to $66.81 per barrel.

Both benchmarks had approached seven-month highs in the previous session before ending slightly lower.

Market participants are holding back ahead of US – Iran talks scheduled for later this week.

Markets stayed tense ahead of a third round of nuclear talks between Washington and Tehran set for Thursday in Geneva. Strains have persisted since last week amid indications that the situation could escalate. The U.S. pulled some non-essential embassy staff from Beirut, underscoring concerns that diplomacy might collapse and spark conflict.

President Donald Trump warned in a social media post on Monday that it would be a “very bad day” for Iran if no agreement is reached.

“In the event of a deal, we would likely see a significant unwinding of the risk premium currently built into prices — though securing such an agreement is far from straightforward,” analysts at ING noted.

A failure in negotiations could heighten worries about stricter sanctions enforcement or potential disruptions in the Strait of Hormuz, a crucial corridor for global crude shipments. Fears of a possible military clash contributed to a 6% surge in oil prices last week.

Tariff tensions under Donald Trump weigh on demand outlook

Oil markets are also contending with wider macro uncertainty after the Supreme Court of the United States invalidated an earlier round of tariffs introduced under emergency powers.

Donald Trump has since sought to reinstate duties of up to 15% using alternative legal provisions and cautioned that countries that “play games” in trade negotiations with the U.S. could be hit with steeper tariffs.

The risk of renewed trade tensions has darkened the global growth and fuel demand outlook, limiting oil’s advance even as geopolitical concerns continue to lend support to prices.

The Australian government has pledged to “consider every possible response” after President Donald Trump raised the standard import tariff to 15%. The abrupt increase came just a day after an initial 10% rate was announced, surprising global markets.

Trade Minister Don Farrell described the decision as “unjustified” and suggested it could strain relations between the long-standing strategic partners. The move follows a U.S. Supreme Court ruling that invalidated the administration’s earlier targeted tariff system as unlawful.

In reaction, the President shifted to a universal global tariff. The first 10% duty is scheduled to take effect at 12:01 a.m. EST on February 24, but the implementation date for the additional 5% remains uncertain, leaving exporters with goods already in transit facing heightened uncertainty.

Economic repercussions and Australia’s reaction

For Australia, the implications are significant. As a leading exporter of iron ore, LNG, and agricultural commodities, a 15% tariff could erode the competitiveness of Australian products in the U.S. market. Trade Minister Don Farrell confirmed that officials are coordinating closely with Australia’s embassy in Washington to evaluate the potential impact.

Analysts note that keeping “all options on the table” may involve filing a formal complaint with the World Trade Organization (WTO) or imposing reciprocal, tit-for-tat duties on American imports. Such action would represent an unusual trade clash between AUKUS allies.

The across-the-board 15% tariff reflects a broad, uniform policy that overlooks customary bilateral arrangements. Should Canberra proceed with countermeasures, it could affect multi-billion-dollar energy and defense agreements that are currently being negotiated.

Market turbulence and the investor outlook

Investors are already responding to the uncertainty. The Australian Dollar (AUD) came under immediate pressure as traders assessed the potential blow to the nation’s trade balance, while mining and energy shares adopted a more cautious tone.

Should the full 15% tariff be implemented without carve-outs, Australian exporters may have to accelerate their shift toward Asian markets, potentially deepening the divide between Western trading partners.

Attention is now fixed on the February 24 deadline. If the White House does not clarify whether allies will receive exemptions, the risk of a formal trade conflict increases. Analysts caution that much of the added cost could ultimately be passed on to American consumers, heightening concerns about renewed inflation.

For more than a year, Donald Trump has operated in Washington with sweeping confidence, exercising power in ways critics said resembled monarchical authority. On Friday, however, the Supreme Court of the United States sharply redirected that momentum.

By invalidating his administration’s cornerstone economic policy, the court handed down a rare and highly visible rebuke, signaling that even a dominant president faces constitutional limits. The 6–3 ruling, written by Chief Justice John Roberts, rejected Trump’s expansive claim that he could impose broad tariffs under emergency powers to safeguard U.S. economic security.

Trump reacted swiftly and angrily. According to Delaware Governor Matt Meyer, the president told governors at the White House that he was “seething” and needed to respond to the courts. Later, speaking to reporters, he criticized the justices who ruled against him — including two he had appointed — calling them weak and an embarrassment. Still, he maintained that the decision ultimately clarified his authority and insisted he could pursue even higher tariffs through alternative legal avenues.

Few issues have defined Trump’s second term more than tariffs, which he has frequently described as his “favorite word.” He used them not only as trade tools but as leverage in disputes over agriculture, foreign investment, narcotics trafficking, prescription drug pricing, and industrial policy. While Congress holds constitutional authority over taxation, the Republican-controlled legislature largely refrained from challenging his approach, and the conservative-leaning court had often bolstered executive power in prior rulings.

This decision, however, marked a boundary. Historians and legal scholars described it as a direct blow to Trump’s broad interpretation of emergency authority under the International Emergency Economic Powers Act. Although the president suggested he could rely on other statutes — and even impose a temporary global tariff — such paths would likely involve stricter procedural requirements and time constraints.

Legal experts noted that no previous president had used the disputed law as aggressively. As University of Virginia scholar Saikrishna Prakash put it, the ruling leaves the presidency “definitely weaker,” underscoring that even assertive executive power remains subject to judicial review.

The U.S. Supreme Court’s decision on Friday to overturn trade tariffs introduced by President Donald Trump last year could ease financial pressure on certain oil producers and drilling firms, though analysts say it is unlikely to significantly reshape global energy trade flows in the near term.

By striking down the tariffs, the Supreme Court of the United States may lower the cost of constructing LNG facilities and other major energy projects that depend on foreign-made modules and components. For instance, Venture Global assembles parts of its LNG plants in Italy before shipping them to the U.S. for completion — a process that had become more expensive under the tariff regime. U.S. crude producers and oilfield service firms also faced higher costs for imported equipment and materials, with some absorbing the impact and others attempting to pass it along to customers.

Cam Hewell, CEO of Premium Oilfield Technologies, said his company had expected to pay $5–6 million in tariff-related taxes in 2026 — a figure that may now decline. He noted that most of the added costs had been absorbed internally, meaning customer pricing would see little change, but improved cash flow could support research, employee compensation, and shareholder returns.

Kirk Edwards, president of Latigo Petroleum in Texas, added that the ruling could improve budgeting clarity and cost visibility for drilling projects.

However, the decision does not eliminate the 50% tariffs on steel and aluminum imposed last year, and some executives remain cautious that the administration could pursue alternative measures to maintain similar trade barriers. Trump himself indicated he may introduce a 10% global tariff for 150 days, signaling that policy uncertainty remains.

Despite the potential cost relief for LNG infrastructure, experts believe global LNG trade patterns are unlikely to shift materially. Ira Joseph of Columbia University’s Center on Global Energy Policy said China has stronger economic incentives to continue redirecting U.S. LNG cargoes to Europe for arbitrage or to import cheaper oil-indexed LNG from the Middle East.

Alex Munton of Rapidan Energy added that Beijing increasingly views LNG purchases as strategic leverage in its relationship with Washington, making new buying commitments unlikely even if tariff pressures ease. Samantha Santa Maria-Hartke of Vortexa echoed that view, suggesting China — which halted U.S. crude and LNG imports after imposing retaliatory tariffs — is unlikely to reverse course in the near term.

Oil prices advanced in Asian trading on Wednesday as investors monitored developments in U.S.-Iran relations and looked ahead to travel demand during an upcoming major holiday in China.

Crude rebounded from part of the previous session’s losses, supported by a softer U.S. dollar ahead of key economic data releases.

By 21:04 ET (02:04 GMT), April Brent futures climbed 0.6% to $69.18 a barrel, while WTI crude futures also gained 0.6% to $64.19 a barrel.

Oil prices rise amid US-Iran tensions over potential supply disruptions.

On Tuesday, Iranian officials stated that recent nuclear discussions with the United States helped Tehran assess Washington’s intentions, adding that diplomatic engagement between the two nations would continue.

The remarks followed talks held last week regarding Iran’s nuclear program, which came after U.S. President Donald Trump sent several warships to the Middle East.

Although both sides indicated some progress from their weekend negotiations, attention shifted after the U.S. issued a maritime warning for vessels passing through the Strait of Hormuz.

Media reports also suggested that Trump was weighing the deployment of a second aircraft carrier near Iran—a step that could significantly heighten regional tensions.

Amid the uncertainty, oil markets incorporated a risk premium, as traders grew concerned that potential military action might disrupt Iranian oil supplies.

China’s Lunar New Year travel surge draws attention as CPI data falls short of expectations.

Oil prices found some support on expectations of stronger Chinese fuel consumption during the upcoming Lunar New Year holiday.

This year’s Lunar New Year, marking the Year of the Horse in the Chinese zodiac, falls on February 17 and will be observed with an extended nine-day public holiday from February 15 to 23.

The festive period typically drives higher consumer spending in China, particularly in travel. Authorities project a record 9.5 billion passenger journeys during the spring holiday travel rush.

International travel is set to include several favored destinations across Southeast Asia, though flights to Japan have reportedly declined sharply amid escalating diplomatic tensions between Beijing and Tokyo.

Meanwhile, recent economic data signaled that deflationary pressures persist in China, as consumer price index figures came in below expectations and producer prices continued to contract.

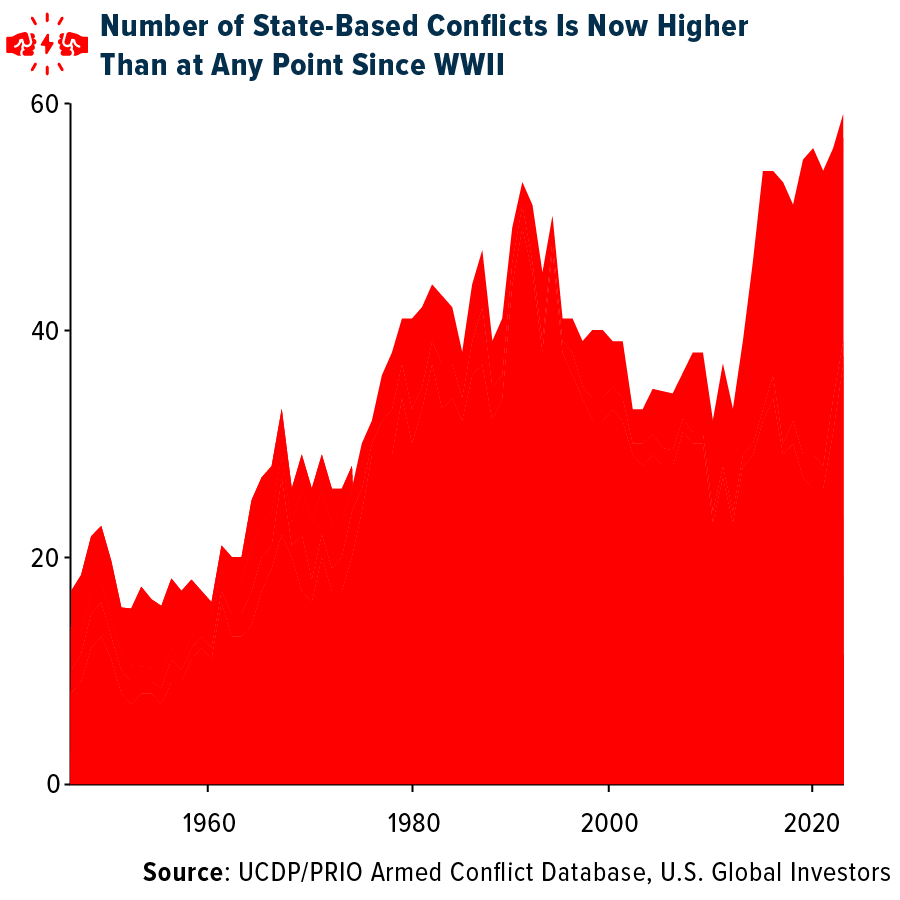

Last week, I attended the 2026 Harvard Presidents’ Seminar with leading executives and thinkers, where Ambassador Kevin Rudd, former Australian prime minister, stood out. He warned that the post–World War II rules-based global order is likely fading, giving way to a more 19th-century style world defined by power politics and spheres of influence. Rudd, a realist rather than an alarmist, argued that a strong U.S. remains essential for global stability, while a weakened U.S. risks creating power vacuums that China and Russia are ready to exploit.

A Fracturing Global Order?

For roughly eight decades after World War II, the United States played a central role in shaping the global order—promoting open markets, free trade, democratic expansion, and the U.S. dollar as the world’s reserve currency—underpinning a period of relative stability.

According to Rudd, that chapter may now be closing. Democratic governance is weakening worldwide, while the number of armed conflicts has climbed to its highest level since World War II.

China and Russia are making their ambitions increasingly explicit. Just last week, Xi Jinping and Vladimir Putin reaffirmed their deepening partnership, pledging mutual support across economic, military, and ideological fronts. With the New START treaty expiring this month, the final pillar of nuclear arms control between the United States and Russia has now fallen away.

Redrawing the Global Playbook

Rudd, who has written two major books on Xi Jinping, cautioned that China’s current leader is far from a pragmatist in the mold of Deng Xiaoping, whose market-oriented reforms in the 1970s set China on its path to global prominence. Instead, Xi is best understood as a Marxist-Leninist nationalist.

Under his leadership, China has moved beyond simply operating within existing global rules to actively reshaping them. The Chinese Communist Party is pursuing an all-encompassing strategy that spans nearly every sphere—military modernization, industrial leadership, energy self-sufficiency, and more. As I noted back in October, I see China’s expansive Belt and Road Initiative as a Trojan horse.

For Xi’s government, economic strength and national security are inseparable, a reality most evident in its approach to energy and technology.

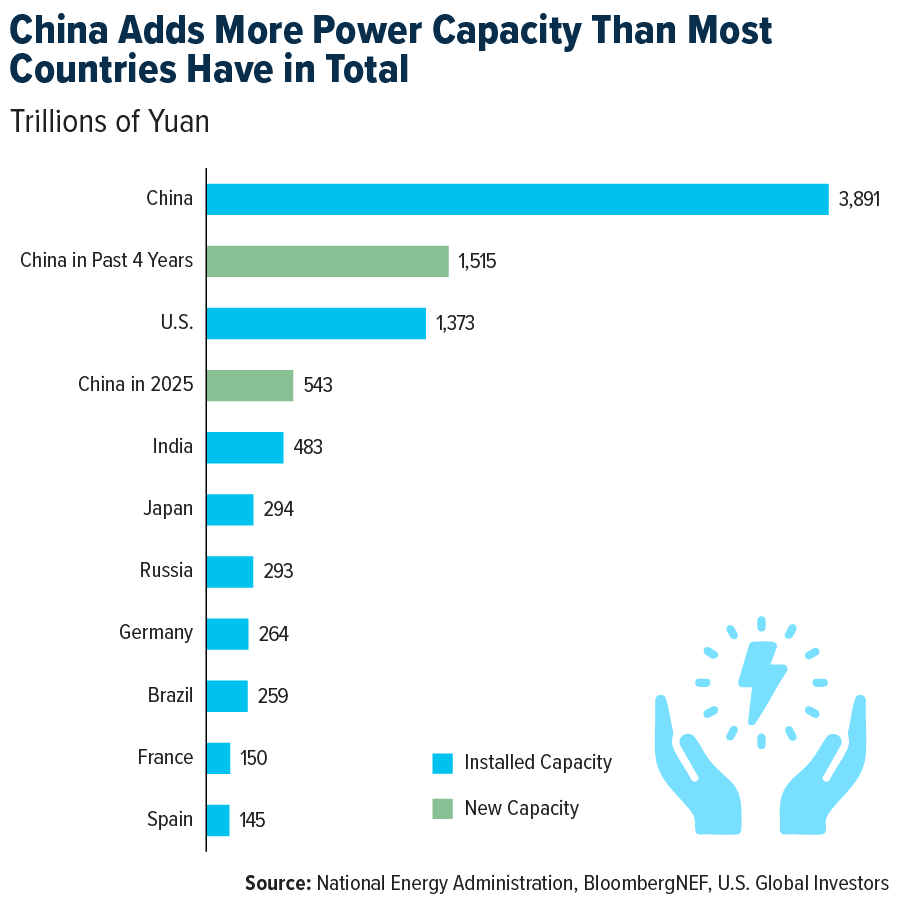

China’s Sweeping Energy Expansion

As the U.S. continues to oscillate on energy policy, China has been pressing ahead at full speed. Since 2021, it has added more power-generating capacity than the United States has built over its entire 250-year history—an astonishing feat achieved in just four years.

In 2025 alone, China brought online 543 gigawatts of new capacity across solar, wind, coal, nuclear, and gas. Looking ahead, BloombergNEF projects an additional 3.4 terawatts over the next five years—nearly six times what the U.S. is expected to add. The objective is clear: to ensure that China’s next wave of industries, including AI, robotics, and advanced manufacturing, is never constrained by energy shortages.

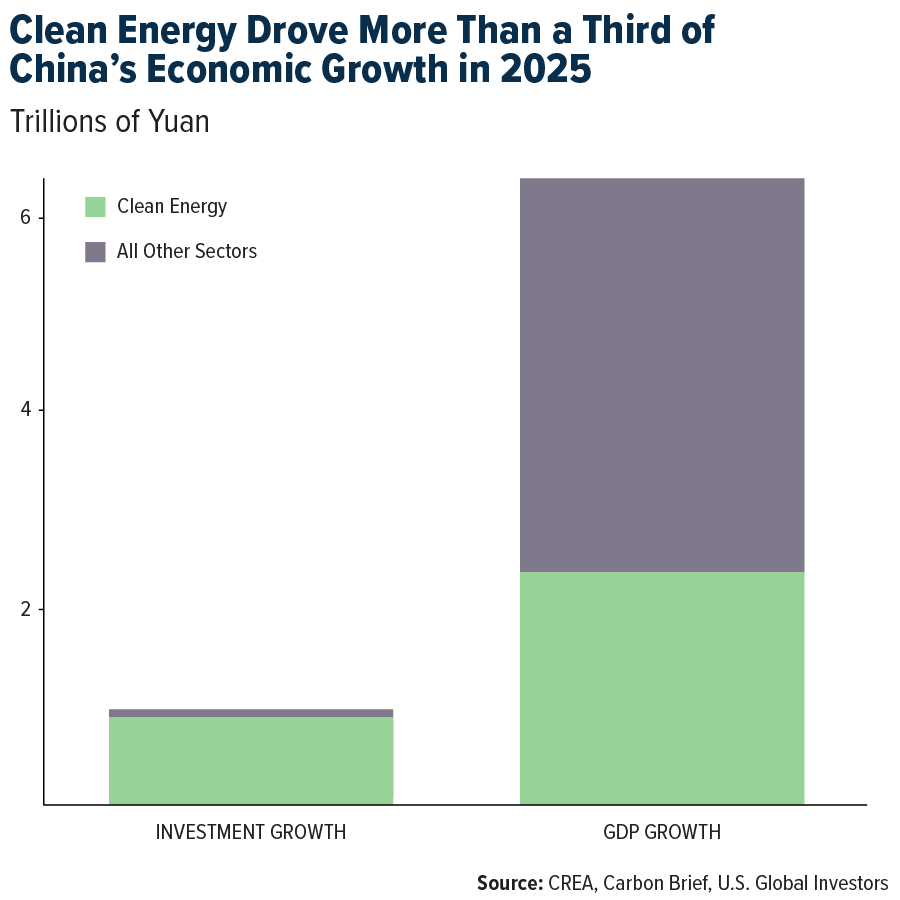

Clean Energy Emerges as the Next Growth Engine

As I’ve noted before, both Elon Musk and NVIDIA CEO Jensen Huang have warned that China’s enormous power surplus could give it a decisive edge in AI computing—and the data backs that up.

In 2025, clean energy accounted for more than a third of China’s GDP growth and over 90% of new investment. Industries such as solar, electric vehicles, and battery technology generated more than $2.1 trillion in economic output, roughly on par with the GDP of Canada or Brazil. Viewed on its own, China’s clean energy sector would rank as the world’s eighth-largest economy.

Meanwhile, in Washington, progress remains stalled by politics.

By contrast, the United States has struggled to execute large-scale energy buildouts amid political gridlock and partisan divides. While China plans decades ahead, U.S. policymakers too often remain focused on the next election cycle.

According to a recent report from the Information Technology and Innovation Foundation (ITIF), China is on course to overtake the U.S. across a wide range of what it terms “national power industries.” These span military sectors such as guided missiles and tanks, dual-use industries like electronic displays and semiconductors, and enabling industries including automobiles and heavy construction equipment.

That said, the U.S. continues to commit heavily to defense spending. Congress recently approved an $839 billion defense bill—$8 billion more than requested by the Pentagon—with funding directed toward key systems such as the F-35, the B-21 bomber, and the Sentinel intercontinental ballistic missile program. More than $13 billion is also allocated to space and missile defense under President Trump’s Golden Dome initiative.

What This Means for Investors

Equity markets may already be signaling the start of a new investment cycle. In January, leadership shifted toward small-cap, domestically oriented stocks. While the S&P 500 hit new highs with a gain of about 1.4%, the Russell 2000 jumped 5.4%, markedly outperforming large caps. Small caps also logged a 15-day streak of outperformance versus the S&P—the longest since May 1996.

This strength does not appear to be a one-off. Since the beginning of Trump’s second term, the Russell 2000 has edged ahead of the S&P 500, rising roughly 17% versus 15% as of Friday, February 6. Some small-cap companies, though not all, tend to be less exposed to tariffs and could benefit over time in a less globalized world.

That said, careful stock selection is critical. Around 40% of Russell 2000 constituents are currently unprofitable.

Finally, with precious metals retreating from recent highs, investors may want to consider buying the dip. A 10% allocation to gold—split evenly between physical bullion and high-quality mining stocks—can help diversify portfolios, with regular rebalancing remaining essential.

Here is what you need to know on Friday, January 30:

Markets were driven early Friday by the latest political and geopolitical developments linked to US President Donald Trump, as investors focused on the announcement of his pick for Federal Reserve Chair. Bloomberg reported that the Trump administration is preparing to nominate former Fed Governor Kevin Warsh for the role as early as Friday morning in the US.

At the same time, the Wall Street Journal noted that President Trump and Senate Democrats have reached an agreement to avoid a government shutdown.

Together with profit-taking and the Federal Reserve’s recent decision to keep interest rates unchanged, these developments helped revive demand for the US Dollar (USD), pushing it up from four-year lows against its major counterparts.

Despite the rebound, the US Dollar remains on course for a second consecutive weekly decline, weighed down by concerns over President Trump’s unpredictable foreign policy stance and repeated challenges to the Federal Reserve’s independence.

On Thursday, Trump threatened to levy a 50% tariff on all aircraft exported from Canada to the United States, accusing Ottawa of unfairly restricting the certification of Gulfstream business jets.

Reuters also reported that Trump plans to hold talks with Iran, even as the Pentagon readies for potential military action and the US steps up its naval presence in the Middle East.

In addition, the White House confirmed that Trump signed an executive order authorizing tariffs on countries that supply oil to Cuba.

Looking ahead, market attention remains firmly on Trump’s nomination of the next Fed Chair, along with the upcoming US Producer Price Index (PPI) release, which could shape the Dollar’s next move.

Before that, preliminary fourth-quarter 2025 GDP data from Germany and the Eurozone are expected to draw investor interest.

In G10 currencies, AUD/USD remains under heavy pressure below the 0.7000 mark amid profit-taking ahead of a likely Reserve Bank of Australia (RBA) rate hike next week. USD/JPY hovers near 154.00, with the Japanese Yen staying weak after softer Tokyo CPI data reduced expectations for an early Bank of Japan (BoJ) rate increase.

EUR/USD pares losses to reclaim the 1.1900 level, though downside risks persist ahead of key German and Eurozone GDP releases. GBP/USD continues to consolidate around 1.3750, weighed down by the ongoing recovery in the US Dollar.

In commodities, Gold slides nearly 4% to trade around $5,200 in early European hours after briefly testing the $5,100 level during the Asian session. Meanwhile, WTI crude oil extends its retreat from five-month highs near $66.25, trading close to $64 as Trump signals openness to talks with Iran.

President Donald Trump once again surprised markets by announcing an increase in tariffs on South Korea to 25% from 15%, citing Seoul’s failure to implement a trade agreement reached last July. The move targets sectors such as autos, lumber, and pharmaceuticals, yet South Korean equities ended up surging 2% to fresh record highs. The KOSPI initially slid more than 1%, but the dip quickly attracted buyers seeking exposure to Asia’s strongest-performing equity market of 2025.

With South Korea’s industry minister set to travel to Washington, investors appear to be betting on a negotiated climbdown, reviving the popular “TACO” trade—Trump Always Chickens Out. Few are surprised that Seoul has been reluctant to commit massive U.S. investments while the risk of abrupt tariff threats remains a defining feature of the administration.

Tariff uncertainty also boosted demand for precious metals, pushing gold and silver back toward record levels. Gold rose 1% to $5,063 an ounce, while silver jumped 5% to $109 an ounce.

Asian equities were broadly firmer, supported by optimism that blockbuster earnings from the U.S. “Magnificent Seven,” beginning with Meta, Microsoft and Tesla later this week, will help sustain the global equity rally into 2026. MSCI’s Asia-Pacific index excluding Japan climbed 1% to a new high, while Japan’s Nikkei added 0.7%, even as the yen hovered near a two-month peak—normally a headwind for exporters.

European equities are poised for a firmer open, with EURO STOXX 50 futures up 0.3%. U.S. futures are also higher, as Nasdaq futures climb nearly 0.6% and S&P 500 futures rise 0.3%. The global economic calendar remains relatively quiet ahead of Wednesday’s Federal Reserve policy decision, at which interest rates are widely expected to be left unchanged. Nevertheless, the meeting is likely to be dominated by the Justice Department’s investigation into Fed Chair Jerome Powell, adding extra scrutiny to his post-meeting press conference. Any indication that Powell may choose to remain on the Fed’s board after his term ends in May—a move permitted under Fed rules—could provoke an unpredictable reaction from President Trump.

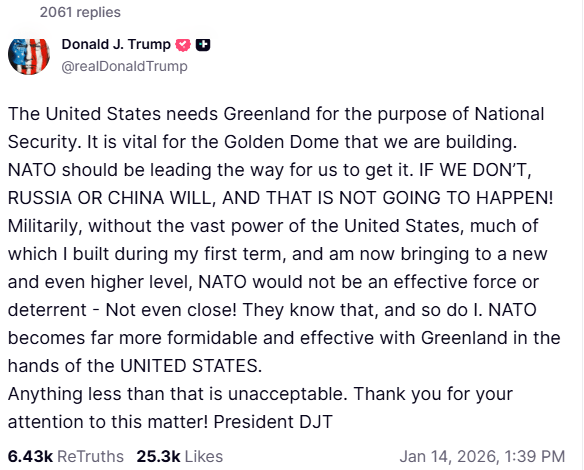

Geopolitical tensions are rising as President Trump moves ahead with threats to levy tariffs on eight NATO allies while continuing his push regarding Greenland. Although overall markets have weakened, these frictions may spur higher defense budgets, accelerated resource reshoring, and expanded infrastructure investment. Below, we identify five U.S.-based companies that stand to gain from the intensifying U.S.–NATO standoff.

As tensions between the U.S. and NATO escalate over fresh tariffs and Greenland’s strategic resource base, defense, mining, and industrial shares appear well positioned for a strong upswing. Against this backdrop, five companies stand out—Lockheed Martin (NYSE:LMT), RTX (NYSE:RTX), Critical Metals (NASDAQ:CRML), Teck Resources (NYSE:TECK), and Caterpillar (NYSE:CAT). Each is set to benefit from increased U.S. defense spending, intensifying competition for Arctic resources, and ongoing efforts to shift supply chains away from Europe and China.

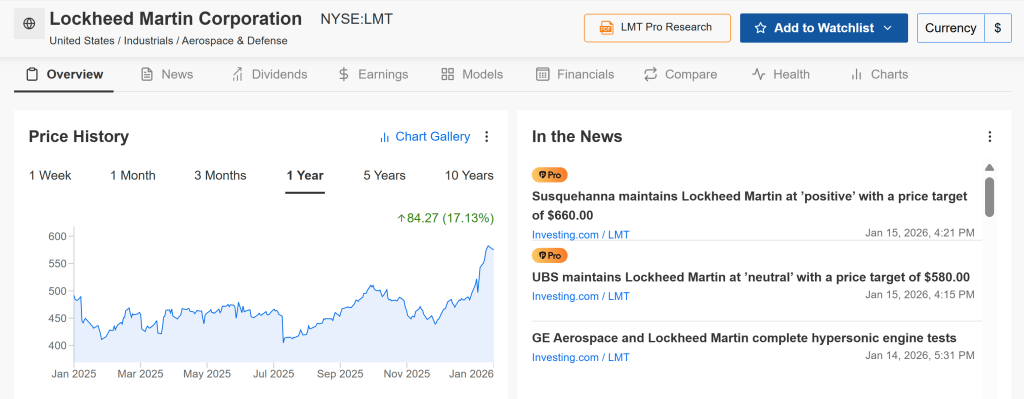

Lockheed Martin: A Leader in Arctic Defense Capabilities

Lockheed Martin appears to be among the primary beneficiaries of rising U.S.–NATO tensions, particularly as Greenland’s strategic value elevates the need for enhanced Arctic defense capabilities. The company’s advanced military platforms and surveillance systems are well suited to the region’s demanding operational environment.

Its F-35 fighter aircraft, along with missile defense and radar solutions such as the “Golden Dome,” play a central role in Arctic security, where Greenland’s geographic position strengthens U.S. monitoring capacity and deterrence against potential Russian and Chinese advances.

So far in 2026, Lockheed Martin’s shares are up roughly 19% year to date, supported by President Trump’s proposed $1.5 trillion defense budget for 2027, which points to expanded procurement activity. In periods of sustained geopolitical strain, investors typically favor companies with stable revenues and long-term contracts. Against this backdrop, Lockheed’s robust order backlog, strong free cash flow generation, and reliable dividend profile position it as a traditional “geopolitical hedge” stock.

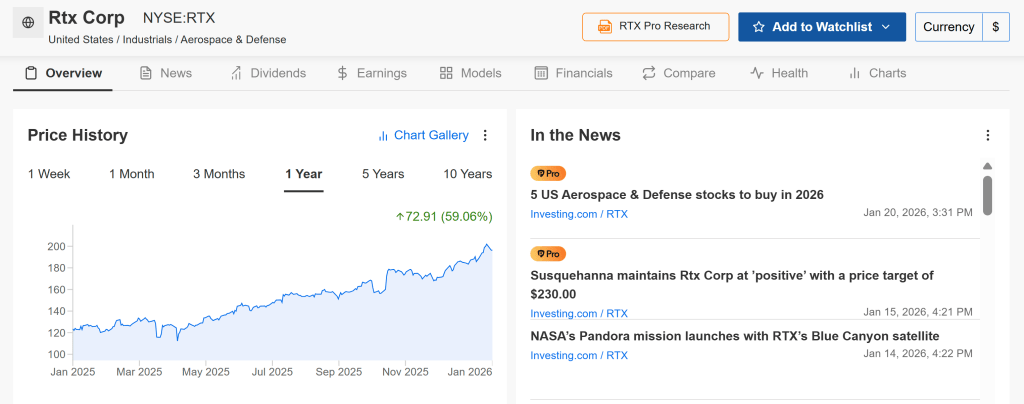

RTX: Rising Demand Across Aerospace and Missile Systems

RTX, formerly known as Raytheon, stands out as a key beneficiary due to its broad defense technology portfolio tailored to the demanding requirements of Arctic environments. The company’s missile defense and advanced radar solutions are central to securing and monitoring strategically vital regions such as Greenland.

In particular, RTX’s Patriot missile defense system is regaining prominence as governments prioritize battle-tested platforms capable of operating in extreme climates while defending against increasingly sophisticated threats.

RTX shares are up about 7% year to date in 2026, following a strong 60% advance in 2025, with a record backlog of $251 billion underpinning continued momentum.

Looking ahead through the rest of 2026, RTX remains attractive amid rising orders from the Middle East, its inclusion in leading defense-focused ETFs, and expectations for roughly 20% earnings growth.

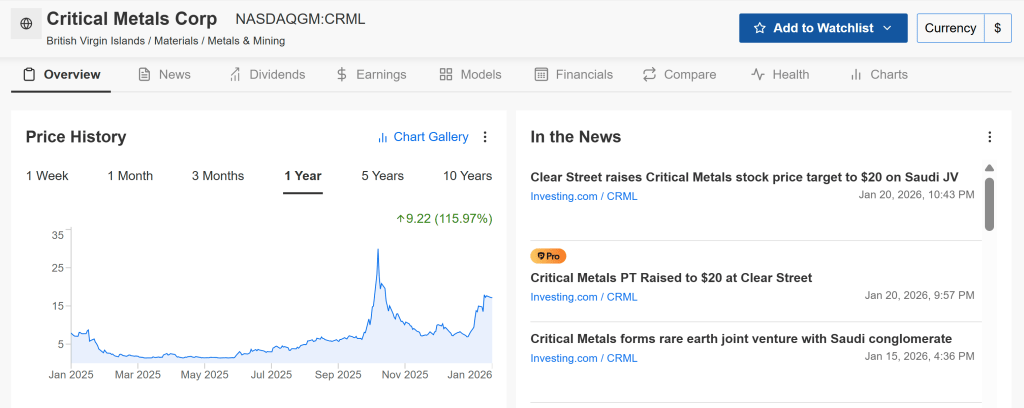

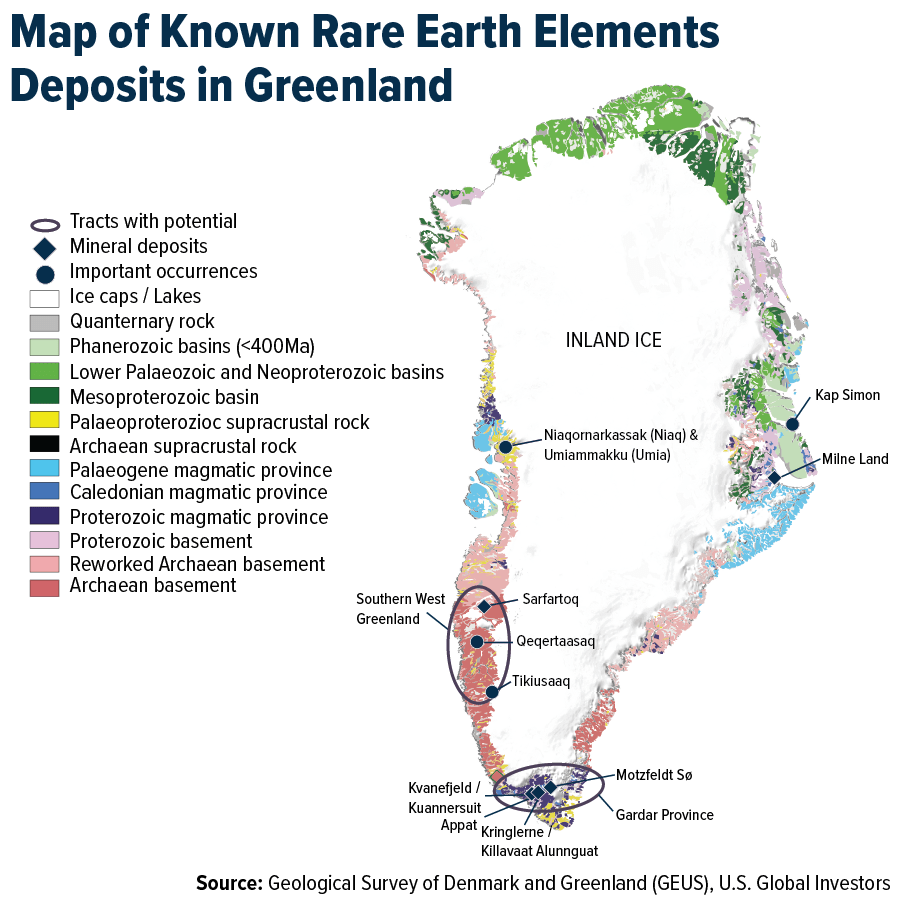

Critical Metals controls the Tanbreez project in Greenland, the largest non-Chinese rare earth deposit globally, directly linking the company to U.S. strategic resource objectives. Heightened geopolitical tensions could accelerate Washington’s push to secure access to these materials, which are essential for defense systems, missile technologies, and electric vehicles—reducing reliance on China and enhancing CRML’s strategic importance.

In addition, the company’s proprietary rare earth processing capabilities and its focus on North American operations position it to benefit from government initiatives aimed at strengthening domestic critical-materials supply chains and expanding strategic mineral stockpiles.

CRML shares have surged nearly 150% so far in 2026, propelled by strong high-grade drilling results and regulatory approval for its pilot processing plant in Greenland.

While the stock carries elevated risk, it offers substantial upside potential this year, with the possibility of capturing up to 50% of the Western rare earth supply. Despite ongoing volatility, secured offtake agreements and heightened U.S. national security priorities support the bullish case, with the stock still trading at an estimated 22% discount to net present value.

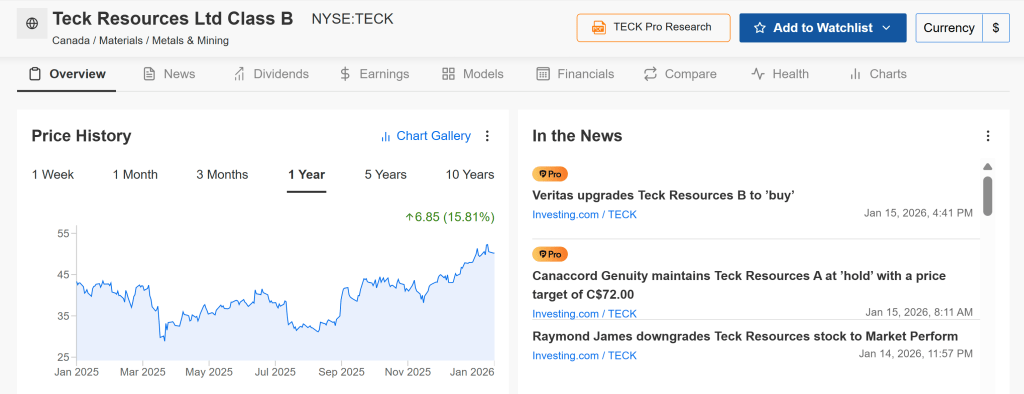

Teck Resources: A Global Metals and Mining Leader

Teck Resources is a leading diversified mining company with significant exposure to steelmaking coal, copper, zinc, and other essential industrial metals. While its operations are not exclusively Arctic-centric, Teck’s asset base firmly places it within the strategic raw materials space that underpins infrastructure development, defense manufacturing, and the global energy transition.

Should 2026 be marked by robust commodity demand, sustained decarbonization spending, and intensifying geopolitical rivalry, diversified miners such as Teck are well positioned to benefit from favorable pricing dynamics and rising shipment volumes.

TECK shares are up roughly 5% year to date, notching fresh 52-week highs as copper prices rally and investors rotate into the materials sector.

Looking ahead, Teck presents a compelling copper-focused opportunity, with its merger with Anglo American set to create a top-five global producer, unlock an estimated $800 million in synergies, and benefit from AI-driven demand growth. Analyst price targets in the $80–90 range are underpinned by structural supply constraints and sustained long-term commodity demand.

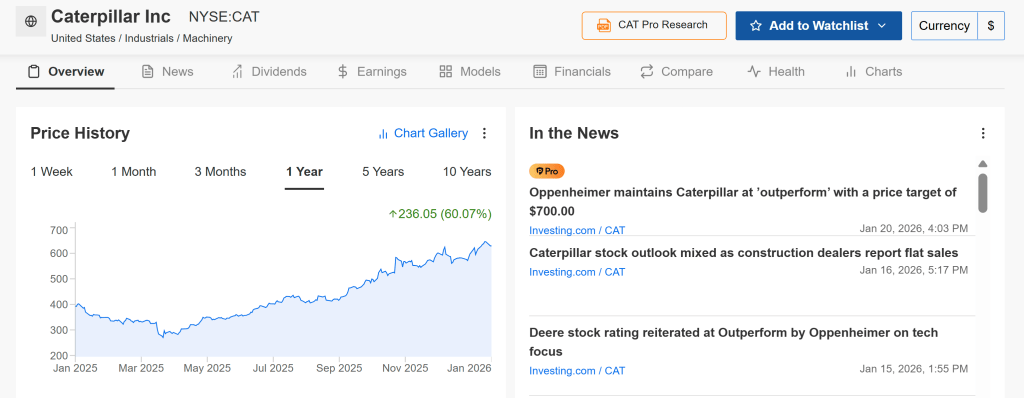

Caterpillar – Infrastructure & Arctic Expansion

Caterpillar stands out as a key beneficiary through its portfolio of heavy machinery and construction equipment critical to Arctic infrastructure expansion, including military installations, transportation networks, and mining projects.

Its specialized cold-weather and Arctic-rated equipment gives Caterpillar a distinct advantage in supporting development across Greenland and other high-latitude regions that gain strategic relevance amid heightened geopolitical tensions.

CAT shares are up roughly 10% year to date in 2026, building on a strong 58% gain in 2025, supported by a record backlog of $39.9 billion.

Looking ahead, Caterpillar remains a solid hold for 2026, with earnings per share projected to grow about 20.5%, aided by continued spending under the U.S. Infrastructure Act and expanding construction tied to AI-driven data center development.

Roughly $700 billion is the price tag now being discussed for a potential acquisition of Greenland, according to recent reports.

Skepticism is warranted. A transaction of that magnitude seems highly unlikely, particularly given that it would exceed half of the U.S. Defense Department’s entire 2024 budget. Public sentiment also appears far from supportive, despite President Donald Trump’s assertion that “anything less than full U.S. control of Greenland is unacceptable.”

Polling suggests little domestic support in the United States for the idea, whether pursued diplomatically or by force. A recent YouGov survey found that just 13% of Americans support compensating Greenland’s residents to join the U.S., while only 8% favor acquiring the island through military means.

Sentiment in Greenland is similarly resistant, with an overwhelming majority unwilling to leave the Danish realm, and opposition across Europe—particularly in Denmark—remains firm.

That said, dismissing Greenland’s significance altogether would be a mistake.

Why Greenland Matters—Even Without a Sale

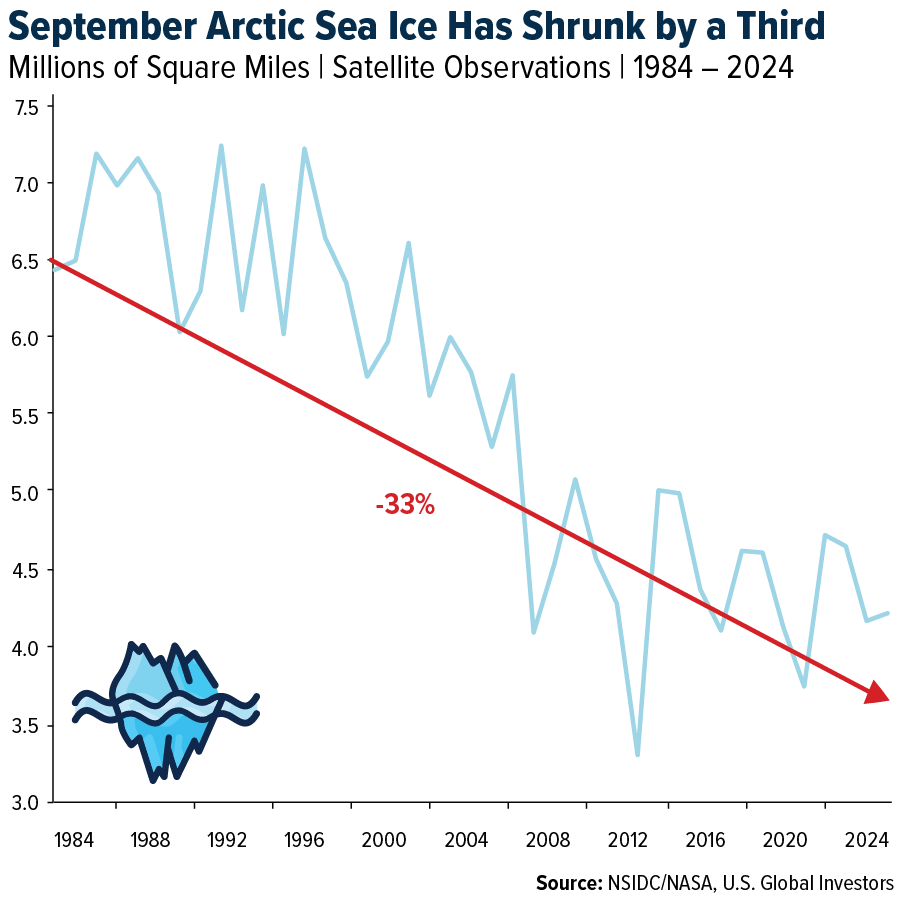

Positioned between North America, Europe, and Russia, Greenland hosts the Pituffik Space Base, a critical site where the U.S. Space Force monitors potential threats traversing the Arctic and the North Pole.

This role has grown increasingly significant as Arctic ice continues to recede. Satellite data show that summer sea ice has been declining by more than 12% per decade—roughly 33% since 1984—opening new shipping routes and reshaping both military and commercial dynamics. As I noted last year, the Arctic is becoming not only more accessible, but also more investable.

Denmark clearly recognizes Greenland’s growing importance. The kingdom has pledged more than $4 billion toward Arctic and North Atlantic defense through 2033, coordinating closely with NATO allies. Danish and allied air, naval, and ground forces are increasing their presence on and around the island, with exercises focused on protecting critical infrastructure and conducting fighter operations in Arctic conditions. At the same time, Denmark’s Chief of Army Command, Peter Boysen, has openly discussed the need for a stronger boots-on-the-ground posture.

The Tough Realities of Developing Greenland

Greenland’s resource base adds another layer of significance. The island holds substantial deposits of iron ore, copper, zinc, graphite, tungsten, and other minerals.

Most attention, however, centers on rare earth elements (REEs)—critical materials used in technologies ranging from smartphones and fighter jets to missile guidance systems. According to the Center for Strategic and International Studies (CSIS), Greenland currently ranks eighth worldwide in proven rare earth reserves, with the potential to climb higher as exploration continues.

From a miner’s perspective, the resource potential looks compelling. In reality, however, development would be slow, complex, and highly capital-intensive.

Greenland spans an area roughly three times the size of Texas, yet it has fewer than 100 miles of roads—and none connect one town to another. Energy infrastructure is sparse, transportation costs are steep, and many mineral deposits are associated with uranium, which Greenland prohibited from mining in 2021 following strong local opposition.

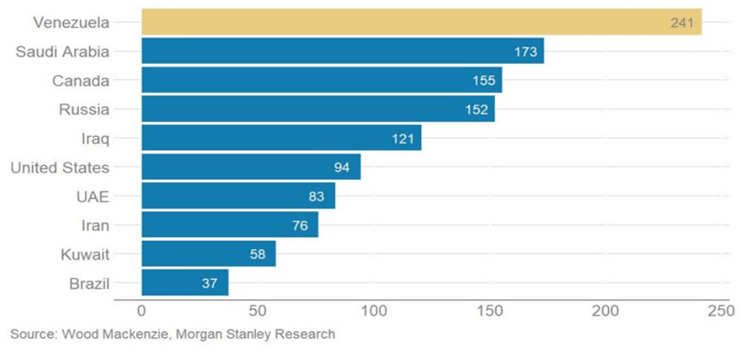

In this sense, Greenland is often mischaracterized in much the same way as Venezuela. Both are portrayed as resource-rich prizes ready for rapid exploitation—rare earths in Greenland’s case, oil in Venezuela’s—but the reality is that unlocking these assets would require billions of dollars and many years of sustained investment. Illustrating the challenge, Wood Mackenzie notes that only 25 hydrocarbon exploration wells have ever been drilled in Greenland, none of which have resulted in commercial success. Neither region should be viewed as a quick path to easy riches.

China’s Efforts to Establish a Presence in Greenland Have Fallen Short

China is well aware of Greenland’s strategic and resource significance. Over the past decade, Beijing has sought to establish a presence through airport construction proposals, infrastructure investments, scientific research initiatives, and other channels.

Most of these efforts, however, have been blocked on national security grounds by either Denmark or the United States. In 2016, for example, a Chinese mining firm’s attempt to purchase a former U.S. naval base in Greenland was stopped. Two years later, China’s state-owned China Communications Construction Company (CCCC) pursued a $550 million contract to expand several Greenlandic airports, but then–U.S. Secretary of Defense James Mattis successfully urged Denmark to withdraw the bid.

So What’s Driving Trump’s Interest in Greenland?

Having said all that, why does President Trump want Greenland so badly (other than as retribution for not being awarded the Nobel Peace Prize)?

He insists it’s for national security, but, as I mentioned earlier, the U.S. military already has broad access to the island, as spelled out in the 1951 agreement signed by the U.S. and Denmark.

Further, Greenland is under the protection of NATO, of which the U.S. is a member. If Russia or China tried to attack it, Article 5 of the treaty would be triggered, activating NATO forces.

Recent reporting suggests that some of Trump’s wealthiest backers see Greenland not as a military outpost or mining play, but as a blank slate. According to Reuters, influential tech investors—including Peter Thiel and Marc Andreessen—have pitched the idea of turning parts of Greenland into a so-called “freedom city,” offering a low-regulation, quasi-autonomous hub for next-gen technologies.

Another explanation? Trump’s reaffirmation of the Monroe Doctrine, which the White House has dubbed the “Trump Corollary” or “Donroe” Doctrine. As stated in the president’s December 2 proclamation, the “American people—not foreign nations nor globalist institutions—will always control their own destiny” in the Western Hemisphere. Denmark, notably, sits in the Eastern Hemisphere.

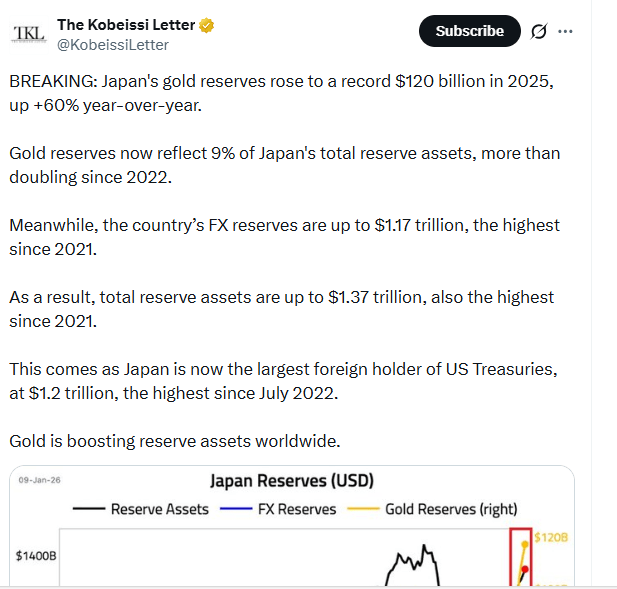

Japan’s Gold Reserves Reach a New Record High

To conclude, central banks worldwide continue to accumulate gold as a means of supporting their currencies and reducing reliance on the U.S. dollar.

While emerging markets have driven the bulk of gold purchases over the past decade, several advanced economies have also increased their holdings. According to The Kobeissi Letter, Japan’s gold reserves reached a new record in 2025, rising to approximately $120 billion—an increase of roughly 60% compared with the previous year.

According to data from the World Gold Council (WGC), Japan now holds the world’s ninth-largest gold reserves, excluding the International Monetary Fund.

As I’ve noted previously, the actions of major institutions underscore a clear recognition of the value of hard assets like gold. For that reason, I continue to advocate allocating around 10% of a portfolio to gold, divided evenly between physical bullion and high-quality gold mining equities, with positions rebalanced annually.

All views expressed and information provided are subject to change without prior notice and may not be suitable for all investors. Links provided may direct you to third-party websites; U.S. Global Investors does not endorse and is not responsible for the accuracy or content of these external sources.

I’m not concerned about a negative market reaction at the open tied to headlines about President Trump’s interest in Greenland, as my exposure to gold stocks provides protection. Gold is surging today as a classic safe haven, offering an oasis amid uncertainty. There are always opportunities in the market, and some assets move counter to broader market swings—gold being a prime example. Among the gold names I favor are Kinross Gold, Agnico Eagle Mines, Alamos Gold, Coeur Mining, Caledonia Mining, Eldorado Gold, Idaho Strategic Resources, New Gold, OR Royalties, and SSR Mining.

I also view any pullback in high-quality technology stocks—particularly those linked to data centers and semiconductors—as a buying opportunity. Investors should not be distracted by short-term volatility or headline noise, as the U.S is simply reaffirming its global leadership position. Preferred names in the semiconductor and data center space include Bloom Energy, Power Solutions International, Comfort Systems, Vertiv Holdings, EMCOR Group, GE Vernova, and Ubiquiti.

Meanwhile, rising geopolitical uncertainty has given so-called bond vigilantes an opening to push global bond yields higher. Japan, the UK, and France remain especially vulnerable due to demographic headwinds that could constrain their ability to service government debt. U.S. Treasury yields have also moved higher, but for fundamentally stronger reasons: higher real rates, solid economic growth, and more favorable demographics relative to other developed economies. As global markets adjust to the reality of President Trump’s long-term ambitions, I expect the U.S dollar to strengthen and the 10-year Treasury yield to retreat toward 3.5% from its recent level near 4.3%.

The World Economic Forum is getting underway this week in Davos, Switzerland, with BlackRock CEO Larry Fink serving as an interim co-chair. Given BlackRock’s recent shift away from ESG and other themes long promoted at Davos, it remains to be seen whether Fink will face criticism from fellow participants. President Trump is scheduled to address the forum on Wednesday, where he is expected to outline his vision for global peace and prosperity, while also stressing the need for the U.S. to confront what he describes as destabilizing forces, including the Iranian regime.

California Governor Gavin Newsom is also expected to speak in Davos, where he plans to argue that President Trump’s economic agenda has underperformed—an argument that may prove difficult amid reports of roughly 5% GDP growth.

Heightened controversy surrounding the U.S. push to purchase Greenland from Denmark has effectively turned Davos into an emergency diplomatic gathering, with President Trump set to hold meetings with NATO allies. Italian Prime Minister Giorgia Meloni has offered to help mediate the Greenland discussions. Meanwhile, Trump has publicly criticized French President Emmanuel Macron and reportedly disclosed private communications in an attempt to highlight France’s handling of Syria. Known for his confrontational negotiating style, President Trump’s approach is likely to draw close scrutiny as European leaders assess how to respond.

WTI crude prices edged lower to around $59.25 in early European trading on Tuesday.

Tensions surrounding Iran have eased in recent days following earlier speculation about a potential U.S. attack.

Market attention is now turning to developments around Greenland after President Trump threatened to escalate tariffs on eight European countries.

West Texas Intermediate (WTI), the U.S. crude oil benchmark, was trading near $59.25 during early European hours on Tuesday. Prices edged lower as concerns over supply disruptions from Iran eased, while traders continued to assess the implications of the U.S. push to take control of Greenland.

There were no signs of escalating tensions in Iran over the weekend, although Supreme Leader Ayatollah Ali Khamenei said that 5,000 people were killed in anti-government protests this month, according to Reuters. The easing of tensions has reduced the risk of a potential U.S. attack that could disrupt supplies from a major OPEC producer, weighing on WTI prices.

Traders are turning their focus to the Greenland crisis after U.S. President Donald Trump said on Saturday that Washington would impose an additional 10% import tariff from February 1 on goods from Denmark, Norway, Sweden, France, Germany, the Netherlands, Finland and the United Kingdom until the U.S. is permitted to purchase Greenland.

Trump is expected to discuss Greenland at the World Economic Forum in Davos, Switzerland, on Wednesday, while European Union leaders are set to hold an emergency summit in Brussels on Thursday. Concerns that tensions could escalate into a broader U.S.–EU trade war have weighed on market sentiment and may add selling pressure to oil prices.

“With fears around Iran easing in recent days following rumors of a U.S. attack, market attention has shifted to the Greenland issue and the potential depth of any fallout between the U.S. and Europe, as an expanded trade conflict could weigh on demand,” said Janiv Shah, an analyst at Rystad.

Meanwhile, the American Petroleum Institute’s (API) crude inventory report is due later on Tuesday. A larger-than-expected draw could signal stronger demand and support WTI prices, while a bigger-than-forecast build would point to weaker demand or oversupply, potentially pressuring prices lower.

Few analysts had a U.S. invasion of Greenland anywhere near the top of their 2026 market outlooks. President Trump’s surprise weekend tariff move has triggered a classic risk-off reaction, with gold rallying around 2%, equities down 1.0–1.5%, and the dollar coming under modest pressure. This week’s World Economic Forum in Davos is now set to become a focal point for U.S.–European diplomacy, with elevated FX volatility likely.

USD: Too Early to Embrace the ‘Sell America’ Narrative

Washington escalated its pursuit of Greenland over the weekend, with the threat of 10% tariffs—potentially rising to 25%—on eight European countries appearing consistent with a broader “maximum pressure” strategy to force a deal. Political commentary in Europe suggests this could mark the end of the EU’s long-standing policy of accommodation toward the U.S., with France emerging as a key advocate for deploying the EU’s Anti-Coercion Instrument, which allows for retaliatory measures spanning tariffs, taxation, and investment restrictions against coercive trade actions.

The issue, alongside growing concerns about strains within NATO, is set to dominate the policy agenda in a week that might otherwise have focused on Ukraine. President Donald Trump is scheduled to speak at the World Economic Forum in Davos on Wednesday, followed by an EU leaders’ meeting on Thursday. A central question is whether Europe adopts China’s approach from last year—matching U.S. tariffs one-for-one—to ultimately force a de-escalation from Washington.

Initial market reactions have been cautious but telling: gold has gapped roughly 2% higher, German DAX futures are down around 1.5%, and the U.S. dollar is marginally weaker. While U.S. cash markets are closed for the Martin Luther King Jr. holiday, S&P 500 futures are indicating losses of about 0.8%. Still, it may be premature to revive the “Sell America” narrative. As with last April’s near-50% “Liberation Day” tariff threats, investors appear reluctant to chase what often proves to be aggressive rhetoric that ultimately gives way to diplomatic negotiation.

Nonetheless, these developments are likely to inject a degree of volatility into what has otherwise been a relatively calm investment environment. On the broader “Sell America” theme, we noted on Friday that there was little concrete evidence of meaningful de-dollarisation last year. Even in a scenario where geopolitical tensions were to escalate materially, it appears unlikely that the dollar would experience a sell-off on the scale of last year’s near-10% decline, particularly given that the buy-side was then unusually under-hedged in U.S. dollar exposure.

Beyond the Greenland issue, this week may also bring clarity on the future leadership of the Federal Reserve. President Trump could announce his nominee to succeed Jerome Powell as Fed Chair. The dollar rallied on Friday after reports suggested Trump wants Kevin Hassett to remain at the National Economic Council, with Kevin Warsh now viewed as the leading candidate—an outcome that would be modestly supportive for the dollar if confirmed.

Overall, U.S. economic data are likely to take a back seat to political developments in the coming days. In the near term, the dollar may probe lower levels. For DXY, gap resistance around 99.35 could cap upside, while a corrective move toward the 98.80–98.85 zone remains the mild tactical bias.

EUR: Unwelcome Developments

The renewed tensions surrounding Greenland and the prospect of fresh tariffs are particularly negative for European industry. This comes just as industrial confidence had begun to recover, with firms appearing to have adapted to last year’s tariff-related volatility. The latest developments are likely to sharpen the focus among European policymakers on boosting domestic demand and may even add momentum to long-delayed reforms such as the Savings and Investment Union, aimed at strengthening Europe’s capital markets and enhancing their competitiveness relative to the U.S.

In FX markets, EUR/USD has established support just below 1.1600. Initial intraday resistance is seen near 1.1650, with scope for a move toward the 1.1690–1.1700 area if that level is cleared. Short-dated implied volatility for EUR/USD, both one-week and one-month, has edged higher, reflecting the elevated uncertainty surrounding the week ahead.

GBP: Poised for Relative Outperformance This Week

We believe this week’s U.K. data — November employment figures and December CPI — may offer modest support to sterling, potentially extending the short-covering rally that has been underway since late November. While EUR/GBP was initially seen as the more vulnerable cross, with downside risks toward 0.8600, early-week dollar softness could shift the bulk of the move into GBP/USD. A sustained break above the 1.3415–1.3420 zone would open scope for a move toward 1.3450–1.3460.

That said, sterling historically underperforms during pronounced risk-off phases, and the current environment remains fluid with multiple cross-currents at play.

Futures tied to major U.S. stock indexes fell after President Donald Trump raised the prospect of imposing tariffs as part of his push to acquire Greenland. European leaders discussed possible retaliation against the measures, which they described as a form of blackmail. Gold climbed to a fresh record high, while oil prices edged lower as traders assessed Trump’s remarks and the EU’s response. Elsewhere, China’s economic growth slowed in the fourth quarter but still met Beijing’s 2025 target.

U.S. futures and global stocks decline

U.S. stock futures pointed lower on Monday as investors weighed President Donald Trump’s threat to impose tariffs on several European countries until the United States is allowed to acquire Greenland.

By 03:05 ET (08:05 GMT), Dow futures were down 404 points, or 0.8%, S&P 500 futures had fallen 66 points, or 1.0%, and Nasdaq 100 futures were off 336 points, or 1.3%.

With U.S. cash markets closed for the Martin Luther King Jr. Day holiday, the immediate reaction to Trump’s latest tariff threat will be delayed. Risk-off sentiment has spread globally, dragging equities lower across Europe and Asia.

ING analysts said Trump’s comments, following last year’s sweeping global tariffs, have pushed trade tensions into “an entirely new dimension,” driven less by economic considerations and more by political motives. They added that while past experience suggests caution in reacting to dramatic announcements, some of Trump’s threats over the past year have ultimately been carried out.

Focus on Trump’s Greenland tariffs

European leaders agreed on Sunday to intensify efforts to counter President Donald Trump’s tariff threats, with reports suggesting EU officials are considering strong retaliatory measures if the levies are imposed.

On Saturday, Trump said he would introduce 10% tariffs on exports from eight European countries—Denmark, Sweden, France, Germany, the Netherlands, Finland, Norway and the United Kingdom—until the United States is able to acquire Greenland. He added that the tariffs would be raised to 25% if the purchase of the semi-autonomous Danish territory does not go ahead. Trump has framed the move as a national security necessity, a claim European governments have rejected, describing it as blackmail.

Ahead of an emergency EU summit in Brussels on Thursday, member states are expected to debate a range of responses, including a potential €93 billion tariff package on U.S. imports and the possible use of the bloc’s “Anti-Coercion Instrument,” which could restrict U.S. access to investment, banking and services markets. Reuters, citing an EU source, reported that the tariff package currently has broader backing.

Trump’s latest tariff threat has also cast doubt over the future of a U.S.–EU trade agreement reached last year, with EU officials saying they cannot approve the deal while Washington pursues control of Greenland. ING analysts said that while the outcome of the dispute remains uncertain, it underscores the lack of predictability in global trade and tariff policy.

Gold reaches record high

Gold prices climbed to record highs in Asian trade on Monday, nearing $4,700 an ounce, as investors rushed into safe-haven assets following President Trump’s latest tariff threat.

Spot gold rose 1.6% to $4,667.33 an ounce by 02:26 ET (07:26 GMT), after earlier touching a record $4,690.75. U.S. gold futures also hit a new peak at $4,697.71 an ounce.

Silver prices surged more than 4% to a fresh all-time high of $94.03 an ounce, supported by safe-haven demand as well as its role as an industrial metal.

Oil prices edge lower

Oil prices edged lower, giving back part of last week’s gains as markets weighed the growing risk of a trade dispute linked to Greenland. Brent crude slipped 0.1% to $59.74 a barrel, while U.S. West Texas Intermediate fell 0.1% to $55.95.

Crude had rallied early last week on concerns that unrest in Iran could threaten oil supplies from the Middle East, a region that accounts for a significant share of global output. Much of that risk premium faded after President Trump ruled out immediate U.S. military action, leading prices to pull back before stabilizing toward the end of the week.

China’s economy meets 2025 growth target

China’s economy grew slightly more than expected in the fourth quarter of 2025, data released on Monday showed, as policy stimulus and a pickup in consumption helped the country meet its annual growth target.

Gross domestic product rose 4.5% year on year in the October–December period, in line with forecasts but down from 4.8% in the previous quarter, marking the slowest pace in three years. On a quarter-on-quarter basis, GDP expanded 1.2%, marginally above expectations of 1.1%.

The result brought full-year 2025 growth to 5%, meeting Beijing’s target. The government is widely expected to set a similar 5% growth goal again, as it continues to face heightened U.S. trade tensions, weak consumer demand and a prolonged property sector downturn.

European stocks dropped sharply on Monday after U.S. President Donald Trump threatened to impose economic sanctions on several countries in the region if they resist his plans to acquire Greenland.

By 03:05 ET (08:05 GMT), Germany’s DAX was down 1.3%, France’s CAC 40 fell 1.6% and Britain’s FTSE 100 slipped 0.4%.

Tariff threats dampen market sentiment

President Donald Trump said over the weekend that he plans to impose tariffs on exports to the United States from eight European countries that have opposed his proposal for the U.S. to acquire Greenland. The countries affected include France, Germany and the United Kingdom, along with several Nordic and northern European nations.

Trump said an initial 10% tariff would be introduced on Feb. 1, rising to 25% in June if no agreement is reached allowing the United States to take control of Greenland, the semi-autonomous territory of Denmark.

The European Union has already suspended ratification of a U.S.–EU trade agreement, and media reports indicate the bloc may revive a €93 billion tariff package targeting U.S. goods. Such a move could sharply escalate tensions and increase the risk of a wider transatlantic trade conflict.

According to IG market analyst Tony Sycamore, the latest dispute has intensified fears of NATO fragmentation and the breakdown of last year’s trade accords with European partners, pushing investors toward risk-off positioning in equities while boosting demand for safe havens such as gold and silver.

This has put the World Economic Forum, which gets under way later in the session in Davos, squarely in focus as global leaders convene, including a large U.S. delegation led by President Trump.

Euro zone inflation data due

Monday’s key economic event is the release of December eurozone inflation data, particularly with U.S. markets closed for the Martin Luther King Jr. holiday. Annual eurozone CPI is expected to come in at 2.0% in December, matching the European Central Bank’s target for the first time since mid-2025, down from 2.1% in November.

The ECB has left interest rates unchanged since ending its rate-cut cycle in June and signalled last month that it is under no immediate pressure to adjust policy, as inflation concerns have eased and growth surprised on the upside toward the end of 2025. The ECB’s next policy meeting is scheduled for early February.

Earlier data showed China’s economic growth slowed to a three-year low in the fourth quarter, with GDP expanding 4.5% year on year, compared with 4.8% in the previous quarter.

U.S. tech giants in focus

The European corporate earnings calendar is thin, though UK building products group Marshalls reported full-year 2025 adjusted profit before tax in line with market expectations despite ongoing uncertainty in its end markets.

U.S. technology heavyweights listed in Europe will also be in focus, as they could become targets of retaliatory measures by European authorities if President Trump follows through on tariff threats against European countries until the U.S. is permitted to acquire Greenland.

Crude slips lower

Oil prices edged lower on Monday, giving back part of the previous week’s gains as markets weighed the growing risk of a trade dispute linked to Greenland. Brent crude slipped 0.1% to $59.74 a barrel, while U.S. West Texas Intermediate fell 0.1% to $55.95.

Prices had climbed early last week on concerns that unrest in Iran could threaten oil supplies from the Middle East, a region that represents a large share of global production. However, much of that risk premium faded after President Trump said there would be no immediate U.S. military action, triggering a pullback before prices stabilized later in the week.

EUR/USD edges higher toward the 1.1625 area in early European trading on Monday, as the euro finds support from signs that Europe is prepared to respond to U.S. tariff measures.

The move follows President Donald Trump’s announcement of a 10% tariff on goods from several European countries, prompting pushback from European leaders.

Meanwhile, expectations that the Federal Reserve will keep interest rates unchanged at its January meeting—amid a resilient labor market and still-elevated inflation—have weighed on the U.S. dollar, providing additional support for the pair.

The EUR/USD pair advances to around 1.1625 in early European trading on Monday, snapping a four-day losing streak. The U.S. dollar comes under modest pressure against the euro after President Donald Trump threatened to escalate tariffs on eight European nations opposing his proposal for the United States to acquire Greenland.

U.S. markets are closed on Monday in observance of Martin Luther King Jr. Day.

Over the weekend, Trump announced a 10% tariff on goods from Denmark, Norway, Sweden, France, Germany, the Netherlands, Finland, and the United Kingdom, set to take effect on February 1. He added that the levy would rise to 25% in June unless an agreement is reached allowing the U.S. to purchase Greenland.

Europe is set to respond after President Donald Trump imposed additional tariffs on key allies, with European leaders expected to convene an emergency meeting in the coming days to consider potential retaliation. Renewed concerns over a trade war and the longer-term implications of Trump’s latest move have weighed on the U.S. dollar, providing support for the EUR/USD pair.

“While one could argue the tariffs are a threat to Europe, it is actually the dollar that is absorbing most of the impact, as markets appear to be pricing in a higher political risk premium for the U.S. currency,” said Khoon Goh, head of Asia research at ANZ.

That said, stronger-than-expected U.S. labor market data released last week have delayed expectations for further Federal Reserve rate cuts until June, which could help cap downside pressure on the dollar. According to the CME FedWatch tool, markets are pricing in nearly a 95% probability that the Federal Open Market Committee will leave rates unchanged at its January 27–28, 2026 meeting.

EUR/JPY moved higher as the euro drew support from EU efforts to push back against potential U.S. tariffs on European allies.

President Donald Trump said tariffs would be imposed on eight European countries that have opposed his proposal involving Greenland.

Meanwhile, Japan’s industrial production dropped 2.7% month-on-month in November, marking its sharpest fall since January 2024.

EUR/JPY rebounded after three consecutive sessions of losses, trading near 183.60 during Asian hours on Monday. The cross found support as the euro was buoyed by reports that European Union ambassadors agreed on Sunday to intensify efforts to deter U.S. President Donald Trump from imposing tariffs on European allies, while also preparing retaliatory measures if the duties go ahead, according to diplomats.

On Saturday, Trump said he would impose tariffs on eight European countries opposing his proposal for the United States to acquire Greenland. He said a 10% levy would be applied from Feb. 1 on goods from Denmark, Sweden, France, Germany, the Netherlands and Finland, as well as Britain and Norway, until Washington is allowed to purchase Greenland, Bloomberg reported.

FILE – This July 31, 2012 file photo shows the euro sculpture in front of the headquarters of the European Central Bank, ECB, in Frankfurt, Germany. The eurozone economy has finally recouped all the ground lost in the recessions of the past eight years after official figures Friday April 29, 2016. showed that the 19-country single currency bloc expanded by a quarterly rate of 0.6 percent in the first three months of the year. (AP Photo/Michael Probst, File) ORG XMIT: LON101

Japan’s industrial production fell 2.7% month-on-month in November 2025, slightly worse than the preliminary estimate of a 2.6% decline, reversing October’s 1.5% rise and marking the steepest contraction since January 2024.

Gains in EUR/JPY could be limited as the yen finds support from expectations of Bank of Japan rate hikes and the prospect of increased fiscal spending under Prime Minister Sanae Takaichi.The BoJ is widely expected to keep its policy rate unchanged at 0.75% this week, although markets are watching for a potential move as early as June.

Last week, BoJ Governor Kazuo Ueda reiterated that the central bank stands ready to tighten policy if economic and inflation trends develop in line with its projections.

Meanwhile, Finance Minister Satsuki Katayama signaled the possibility of coordinated intervention with the United States, stressing on Friday that all options—including direct market action—remain on the table to address the yen’s recent weakness.

Most Asian currencies were little changed on Monday as fresh U.S. tariff threats against Europe dampened risk appetite, while markets also absorbed China’s slightly better-than-expected growth figures.

The U.S. Dollar Index slipped 0.2% from a seven-week peak during Asian trading, while Dollar Index futures were down 0.3% as of 03:58 GMT.

Yuan rises to a 32-month peak following China’s Q4 GDP release

China helped temper the broader risk-off sentiment after data showed the world’s second-largest economy expanded slightly faster than expected in the fourth quarter.

The GDP reading enabled China to achieve its official 5% growth target for 2025, providing some comfort on regional economic momentum despite ongoing worries about subdued domestic demand and stress in the property sector.The onshore yuan pair USD/CNY slipped 0.1% to its weakest level since May 2023.

Asia FX little changed as Trump renews Greenland tariff threats

Risk appetite weakened after U.S. President Donald Trump said he would impose tariffs on eight European countries that have opposed his proposal to acquire Greenland.

Trump said the duties would start at 10% from Feb. 1 and increase to 25% in June if no deal is reached, reigniting concerns about escalating transatlantic trade tensions and possible spillover effects on global markets.

Media reports indicated the European Union is considering suspending progress on an EU-U.S. trade agreement and may revive a previously proposed 93 billion euro tariff package on U.S. goods.

France has called on the bloc to consider deploying its anti-coercion instrument against the United States, a tool designed to respond to economic pressure from external partners.

Asian currencies mostly moved sideways, with traders remaining cautious and refraining from bold bets.

USD/KRW ticked up 0.1%, while USD/SGD slipped 0.2%.USD/INR was little changed.AUD/USD added 0.1%.

Japanese snap elections come into focus

The Japanese yen strengthened against the dollar, with USD/JPY slipping 0.2% to a 10-day low, supported by safe-haven demand amid global trade uncertainty.Domestic political developments also remained in focus after reports said Prime Minister Sanae Takaichi is weighing a snap election in the coming weeks to bolster her mandate.

“For now, the yen continues to face headwinds from election-related uncertainty, and greater clarity is unlikely before February,” MUFG analysts said in a note.

“Over the medium term, our global team still sees the yen as having been relatively weak, and we maintain a bias for USD/JPY to trend lower, subject to election outcomes,” they added.

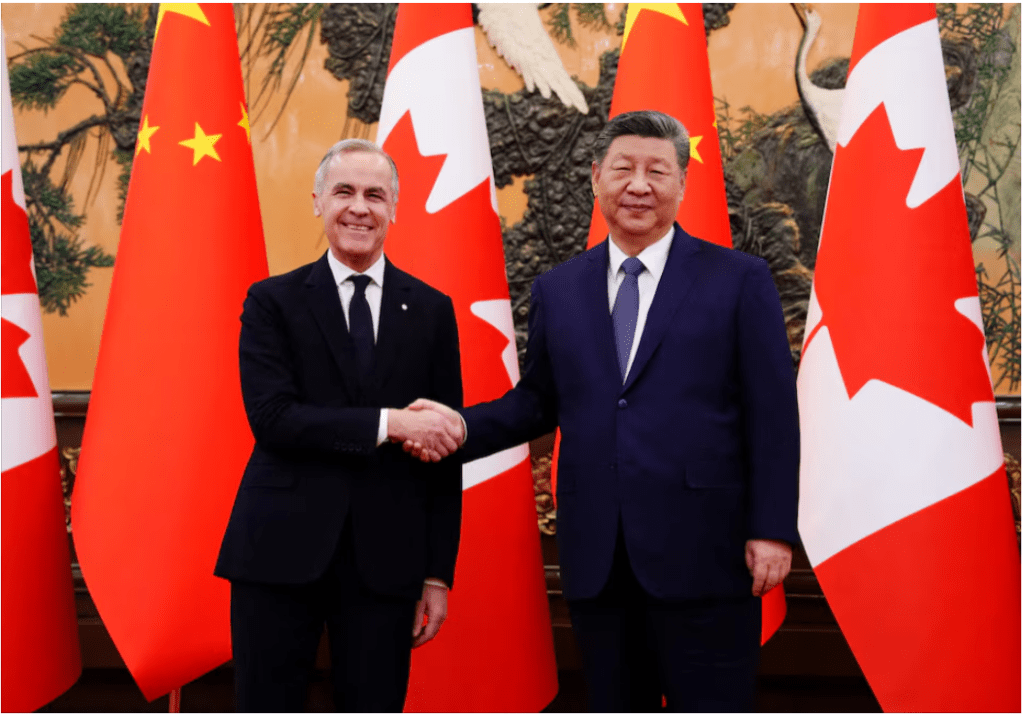

Canada and China reached a preliminary trade agreement on Friday to sharply reduce tariffs on electric vehicles and canola, pledging to dismantle trade barriers and deepen strategic cooperation during Prime Minister Mark Carney’s visit.

On his first trip to China since 2017 by a Canadian prime minister, Carney aims to repair relations with Canada’s second-largest trading partner after the United States, following months of diplomatic outreach.

Canada will initially permit imports of up to 49,000 Chinese electric vehicles at a 6.1% most-favoured-nation tariff, Prime Minister Mark Carney said following talks with Chinese leaders, including President Xi Jinping.

The move marks a sharp reversal from the 100% tariff imposed on Chinese EVs in 2024 under former Prime Minister Justin Trudeau, in line with similar measures taken by the United States. China shipped 41,678 electric vehicles to Canada in 2023.

“This restores access to levels seen before the recent trade disputes, but within a framework that offers significantly more benefits for Canadians,” Carney said, adding that the import quota would be expanded gradually to around 70,000 vehicles over the next five years.

“To build a globally competitive electric vehicle industry, Canada must learn from innovative partners, gain access to their supply chains, and stimulate domestic demand,” Carney said, distancing himself from former prime minister Justin Trudeau’s view that tariffs were necessary to shield local manufacturers from subsidised Chinese competitors.

Canada’s decision to ease EV tariffs runs counter to U.S. policy, drawing criticism from some members of President Donald Trump’s cabinet ahead of a planned review of the U.S.–Canada–Mexico trade agreement. However, Trump himself voiced support for Carney’s approach.

“That’s exactly what he should be doing. Signing trade deals is good for him. If you can strike a deal with China, you should take it,” Trump said at the White House.

AGRI-FOOD PARTNERSHIP: Ontario Premier Doug Ford denounces the deal.

“The federal government is effectively opening the door to a surge of low-cost Chinese-made electric vehicles without firm assurances of comparable or timely investment in Canada’s economy, auto industry, or supply chains,” Ford said in a post on X.