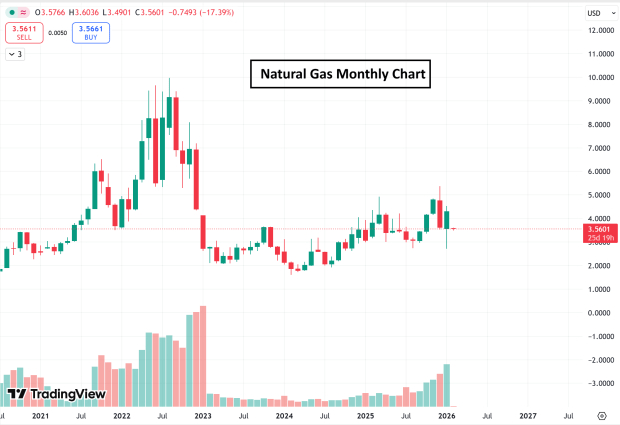

Following a sharp and prolonged rally triggered by the outbreak of the Russia–Ukraine war in 2022, natural gas prices have since collapsed. The downturn has been driven by record U.S. output, warmer-than-expected winters, and improvements in drilling technology, all of which have contributed to a significant supply–demand imbalance.

Over the past five years, natural gas—and related instruments such as the US Natural Gas Fund ETF (NYSE: UNG)—has dropped nearly 60%, reinforcing its long-standing reputation as the “widow maker.”

However, following a sharp cold-weather-driven spike, warmer February forecasts have dampened near-term demand expectations, triggering a roughly 15% selloff in natural gas prices on Sunday evening.

Even so, a number of bullish catalysts are coming into focus that could pave the way for a powerful, 2022-style rally in natural gas. Below are three key reasons to maintain a bullish outlook, including:

Rising Energy Demand From Data Centers

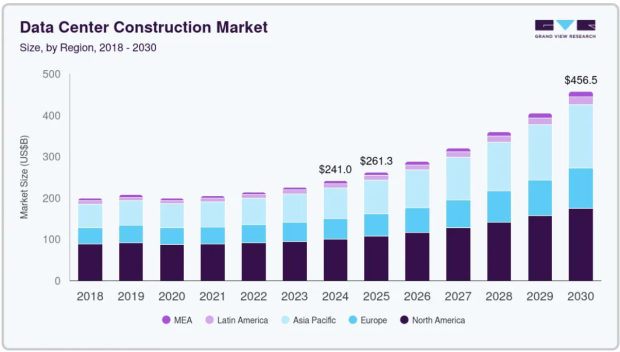

Already, the buildout of AI-focused data centers represents the largest infrastructure expansion in history. Data from Grand View Research shows that the data center construction market surpassed $250 billion in 2025, as hyperscalers such as Alphabet (NASDAQ: GOOGL) and Microsoft (NASDAQ: MSFT) race to secure leadership in artificial intelligence. Looking ahead, spending on AI data center construction is projected to surge to $450 billion by the end of the decade.

Recent remarks from Nvidia’s (NASDAQ: NVDA) influential CEO, Jensen Huang, reinforce this view. Speaking at the World Economic Forum (WEF) 2026 in Davos, Switzerland, Huang pushed back against concerns of an AI bubble, pointing to rising spot prices—even for older GPUs—and the scarcity of available units for rent. He also suggested that trillions of dollars of capital are poised to flow into the development of increasingly powerful AI models.

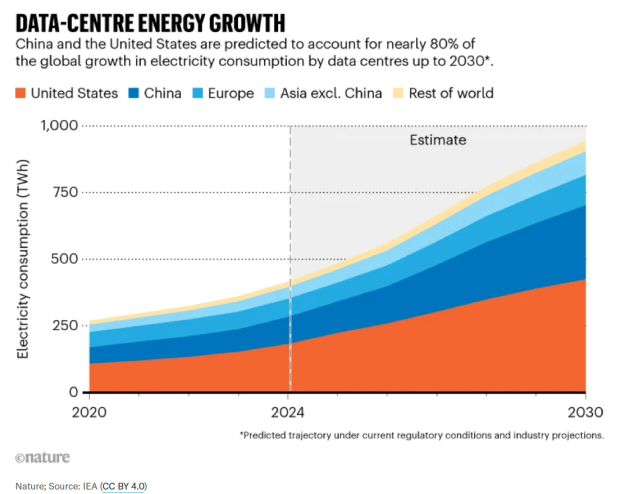

That said, hyperscalers face a significant constraint: energy. Power costs are climbing as electricity demand from AI data centers is projected to double by the end of the decade.

While renewable and nuclear energy continue to dominate Wall Street’s narrative, both come with relatively high upfront costs. In the near term, natural gas remains the most reliable, scalable, and cost-effective source of power for meeting large-scale electricity demand.

U.S. LNG Producers Capitalize on Global Demand

Several major liquefied natural gas (LNG) export terminals are set to come online in 2026, expanding U.S. producers’ ability to supply Europe and other global markets. With U.S. natural gas prices well below those in Europe, exporters are incentivized to ship more volumes overseas. This dynamic is expected to absorb excess domestic supply, helping establish a solid price floor for U.S. natural gas.

In addition, the Trump administration has emphasized an “American Energy Dominance” strategy, securing multiple long-term LNG supply agreements with countries such as Japan and Qatar. These deals underpin durable, long-term demand for U.S. LNG exports.

Natural Gas Poised to Replace Coal

According to the U.S. Energy Information Administration (EIA), U.S. coal production declined 11.3% year over year, with the number of active coal mines dropping from 560 to 524. Although many countries are transitioning toward renewable sources such as solar, these alternatives are currently insufficient to fully replace coal-fired generation. In the near term, natural gas offers the most viable solution, given its scalability, cost efficiency, and significantly lower emissions—producing roughly half the CO₂ of coal.

Technical Outlook for Natural Gas

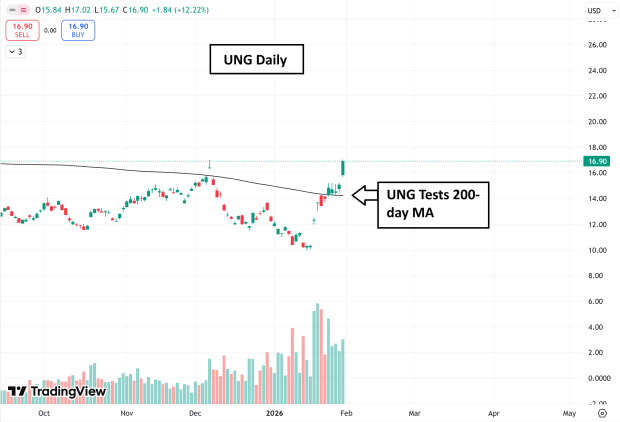

Over the past several weeks, UNG has surged from roughly $10 to $16.90. However, warmer-than-expected weather forecasts suggest the ETF may pull back to test its 200-day moving average. Bulls will be watching closely this week to see whether that key support level holds.

Bottom Line

While natural gas is well known for its short-term volatility and weather-driven swings, the underlying fundamentals are increasingly pointing toward a bullish long-term trajectory. Rising energy demand from AI data centers, combined with expanding U.S. export capacity, is expected to drive sustained growth in demand over time.

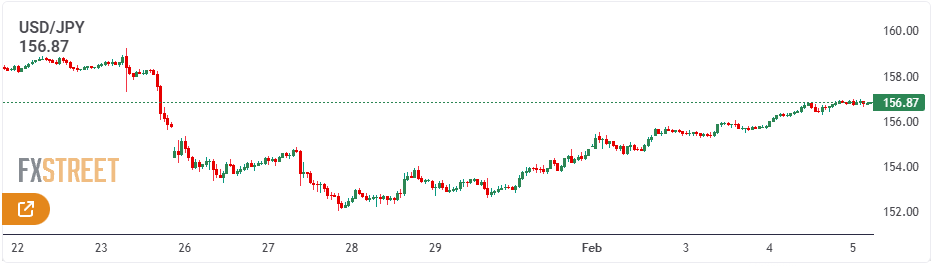

USD/JPY paused its advance near the 157.00 mark during Thursday’s Asian session, as a renewed bout of risk aversion revived safe-haven demand for the Japanese yen.

That said, the yen remains on fragile footing amid ongoing concerns over Japan’s fiscal position under Prime Minister Sanae Takaichi’s expansionary spending agenda, helping to limit downside pressure on the pair.

Looking ahead, the U.S. JOLTS Job Openings report could provide fresh impetus for near-term trading.

USD/JPY Technical Analysis

The Japanese yen emerged as the weakest-performing G8 currency on Wednesday. Its sharp underperformance has lifted USD/JPY above the 156.80 level at the time of writing, putting the pair on course for a roughly 3% rebound from last week’s lows.

Fundamental Analysis

Investors are offloading the yen broadly ahead of this weekend’s snap election. Rising support for Prime Minister Takaichi has fuelled concerns that a stronger electoral mandate would allow her to extend tax cuts and expand stimulus spending, heightening fears of fiscal strain.

Markets Brush Aside Intervention Concerns

Tokyo authorities have warned of possible intervention to curb excessive yen volatility, but those concerns have been largely brushed aside. Comments from Prime Minister Takaichi highlighting the benefits of a weaker yen, along with the U.S. Treasury Secretary’s denial of any coordinated effort to stabilise the currency, have instead driven the yen sharply lower across the board.

The U.S. dollar, however, is not especially strong on Wednesday. While markets continue to react positively to the nomination of Kevin Warsh as the next Federal Reserve Chair and to the end of the brief partial government shutdown, the recent rally in the U.S. Dollar Index appears to be losing momentum.

Attention now turns to upcoming U.S. data, including the Services PMI and the ADP Employment Change report. The latter could be particularly influential, as the government shutdown has delayed Friday’s official nonfarm payrolls release, leaving private-sector jobs data as a key guide for markets.

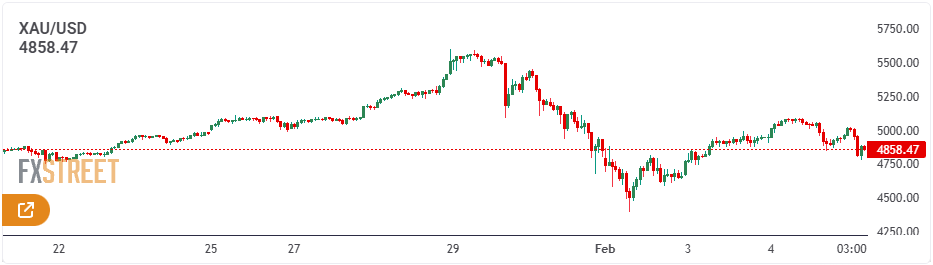

Gold saw choppy price action during Thursday’s Asian session, oscillating within a roughly $200 range. Traders are now looking to the U.S. JOLTS Job Openings report and developments on the geopolitical front—particularly U.S.–Iran tensions—for clearer directional cues.

XAU/USD Technical Analysis

The 21-, 50-, 100- and 200-day SMAs are all sloping higher, with the 21-day positioned above the longer-term averages, highlighting a well-established bullish structure. Prices remain above these indicators, confirming that buyers retain control. Initial support is seen at the 21-day SMA near $4,827.45, followed by the 50-day SMA at $4,532.68. The 14-day RSI has eased to a neutral 52.58, suggesting momentum is consolidating after retreating from overbought levels.

The positive alignment of the moving averages favours a buy-on-dips approach while prices hold above the short-term average. A more pronounced correction would bring the 100-day SMA at $4,271.21 into focus, with the 200-day SMA at $3,821.77 reinforcing the broader uptrend. As long as the RSI remains above the 50 midpoint, the bullish bias stays intact, while a sustained break below it could signal scope for a deeper retracement.

Fundamental Analysis

Gold ended Wednesday little changed near $4,950 after choppy two-way trading. The metal initially rebounded sharply, testing the $5,100 area amid uncertainty surrounding the Federal Reserve’s future policy direction under Kevin Warsh, which weighed broadly on the U.S. dollar.

Renewed geopolitical tensions in the Middle East and between Russia and Ukraine also lent support to gold prices, alongside concerns about potential economic data disruptions stemming from the U.S. partial government shutdown that concluded on Tuesday.

Sentiment shifted during the U.S. session after the ISM Services PMI signalled firmer inflation pressures, prompting a rebound in the dollar. At the same time, an intensifying tech-sector sell-off on Wall Street unsettled markets, driving demand for the greenback as a safe haven.

Additional USD strength came from renewed weakness in the Japanese yen amid rising fiscal and political concerns, which pushed USD/JPY higher and further supported the dollar.

The USD rebound triggered a sharp pullback in gold, although buyers stepped back in near the key $4,950 psychological support level.

Early Thursday, gold remains under pressure after once again failing above the $5,000 resistance zone. The U.S. dollar continues to advance, hitting fresh two-week highs against its major peers as risk sentiment deteriorates amid a global technology sell-off.

The decline in global data analytics, professional services, and software stocks followed Anthropic’s launch of plug-ins for its Claude Cowork agent, which raised fresh concerns about AI-driven disruption across these industries, according to Reuters.

Looking ahead, the delayed U.S. JOLTS Job Openings report could offer gold some relief, particularly if it reinforces expectations for two Federal Reserve rate cuts this year. Conversely, an extended sell-off in the Japanese yen could spark another wave of heavy selling pressure in gold.

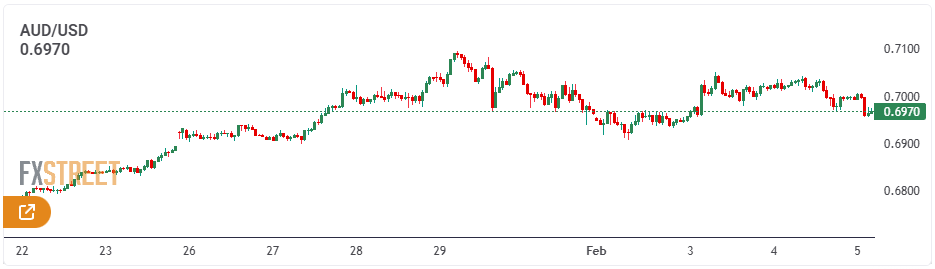

AUD/USD is trading lower below the key 0.7000 psychological level during Thursday’s Asian session, pressured by mixed Australian trade data. The pair is also weighed down by a firm U.S. dollar, which is hovering near a two-week high. With limited domestic catalysts, traders are now turning their attention to the upcoming U.S. JOLTS job openings data for fresh direction.

AUD/USD Technical Outlook

Should bullish momentum intensify, AUD/USD is likely to encounter its next resistance at the 2026 peak of 0.7093 (Jan 29), followed by the 2023 high at 0.7157 (Feb 2).

On the downside, a break below the February low at 0.6908 (Feb 2) may trigger a deeper pullback toward the interim 55-day SMA at 0.6693, ahead of the 2026 trough at 0.6663 (Jan 9). Additional downside support is seen at the 100-day SMA at 0.6628, with stronger support at the 200-day SMA at 0.6563 and the November low at 0.6421 (Nov 21).

Momentum indicators remain constructive and point to further upside potential, although the pair’s overbought readings suggest the risk of a near-term correction. The RSI hovers near 72, while the ADX around 50 continues to signal a strong underlying trend.

Bottom line

AUD/USD continues to be heavily influenced by global risk appetite and developments in China’s economy. A sustained move above the 0.7000 handle would reinforce a more credible bullish outlook.

For the time being, a weaker U.S. dollar, stable—though not particularly strong—domestic data, a still-hawkish tilt from the RBA, and modest backing from China leave the balance of risks skewed toward further upside rather than a pronounced pullback.

Fundamental Analysis

AUD/USD remains entrenched in its broader uptrend despite renewed selling pressure emerging on Wednesday. Any near-term pullbacks are expected to attract buying interest, as the Reserve Bank of Australia continues to project a clearly hawkish stance following its latest rate decision.

The Australian Dollar is struggling to extend Tuesday’s advance, easing back and once again testing the psychologically significant 0.7000 mark.

The retreat comes as the U.S. Dollar regains some traction, with markets having largely absorbed the RBA’s hawkish hike and refocusing attention on U.S. economic and monetary policy developments.

Australia: Growth Is Cooling, Not Collapsing

Recent Australian data have been underwhelming rather than alarming, reinforcing a well-established narrative. Economic activity is slowing, but in a controlled manner, with momentum easing rather than breaking down—supporting the soft-landing view.

January PMI surveys align with this assessment, as both Manufacturing and Services strengthened and remained firmly in expansion territory, at 52.3 and 56.3 respectively. Retail sales continue to show resilience, and although the trade surplus narrowed to A$2.936 billion in November, it remains solidly positive.

Growth is moderating only gradually, following a 0.4% quarter-on-quarter rise in GDP in Q3. On an annual basis, output expanded by 2.1%, matching the RBA’s projections.

The labour market remains a standout performer. Employment jumped by 65.2K in December, while the unemployment rate unexpectedly edged down to 4.1% from 4.3%.

Inflation, however, continues to be the key challenge. December CPI surprised to the upside, with headline inflation accelerating to 3.8% year-on-year from 3.4%. The trimmed mean rose to 3.3%, in line with market expectations but slightly above the RBA’s 3.2% forecast. On a quarterly basis, trimmed mean inflation increased to 3.4% in the year to Q4, marking the highest level since Q3 2024.

China: A Backdrop of Support, Not a Catalyst

China continues to offer a generally supportive backdrop for the Australian dollar, though without the momentum needed to drive a sustained upswing.

Economic growth ran at an annualised 4.5% in the October–December quarter, with quarter-on-quarter expansion at 1.2%. Retail sales rose 0.9% year-on-year in December—respectable, but not particularly compelling.

More recent indicators point to a renewed loss of momentum. Both the NBS Manufacturing PMI and the Non-Manufacturing PMI slipped back into contraction territory in January, at 49.3 and 49.4 respectively.

By contrast, the Caixin surveys painted a slightly brighter picture, with the Manufacturing PMI edging up to 50.3 to remain in expansion, while the Services PMI increased to 52.3.

Trade stood out as a relative bright spot, as the surplus widened sharply to $114.1 billion in December, supported by nearly 7% growth in exports and a solid 5.7% rise in imports.

Inflation signals remain mixed. Consumer prices were unchanged at 0.8% year-on-year in December, while producer prices stayed firmly negative at -1.9%, underscoring that deflationary pressures have yet to fully fade.

For now, the People’s Bank of China is maintaining a cautious stance. Loan Prime Rates were left unchanged in January at 3.00% for the one-year and 3.50% for the five-year, reinforcing expectations that policy support will remain gradual rather than aggressive.

RBA: Leaning Hawkish, In No Hurry to Ease

The RBA raised the cash rate to 3.85% in a decisively hawkish move that largely met expectations. Upward revisions to both growth and inflation forecasts signal firmer economic momentum and increasingly broad-based price pressures. Core inflation is now projected to remain above the 2–3% target band for much of the forecast horizon, reinforcing the case for a restrictive policy stance.

The central message is that inflation is becoming more demand-driven. The RBA cited stronger-than-expected private demand as a key justification for tighter policy, even as productivity growth remains subdued. While Governor Bullock described the move as an “adjustment” rather than the beginning of a renewed hiking cycle, the signal was clear: policymakers are uneasy with the upward drift in inflation.

For markets, this implies interest rates are likely to stay higher for longer, limiting the scope for near-term easing. From an FX perspective, this provides marginal support for the Australian dollar—particularly against low-yielding peers—even as the RBA’s emphasis on full employment tempers the likelihood of an aggressive tightening phase.

In the wake of the decision, markets are now pricing in nearly 40 basis points of additional tightening by year-end.

Positioning: Shifting Sentiment Toward the AUD

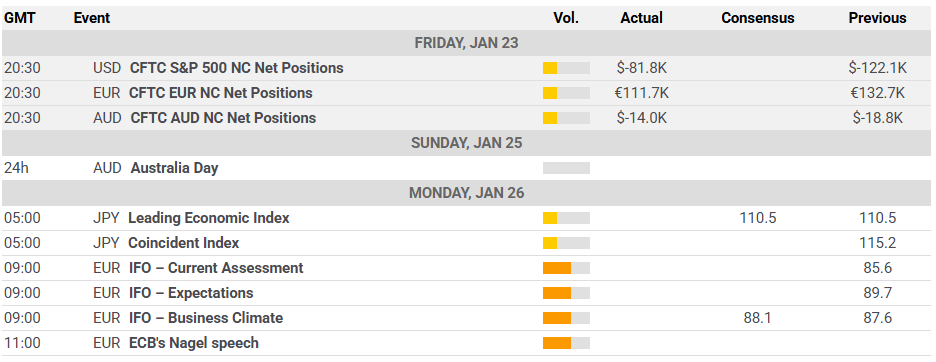

The latest positioning data suggest the worst of the bearish sentiment toward the Australian dollar may have passed. CFTC figures show that non-commercial traders have returned to a net long stance for the first time since early December 2024, although the position remains modest at just over 7.1K contracts in the week ending January 27.

Open interest has also climbed to its highest level in several weeks, exceeding 252K contracts, indicating that traders are beginning to re-engage with the market. That said, the move appears tentative rather than a strong conviction call on a sustained appreciation in the AUD, at least for now.

Key Drivers Ahead

Near term: Market attention is shifting back toward the United States. Incoming economic data, tariff-related developments, and ongoing geopolitical headlines are likely to drive movements in the U.S. dollar. For the Australian dollar, the key swing factors remain domestic labour market and inflation data, and how these shape expectations for the RBA’s next policy decision.

Risks: The AUD remains highly sensitive to global risk sentiment. A sharp deterioration in risk appetite, renewed concerns over China’s outlook, or an unexpected resurgence in the U.S. dollar could quickly unwind recent gains.

Gold’s most recent move was sharp, chaotic, and relentless. With volatility running high and prices stretched, managing risk is just as critical as getting the direction right.

Gold shows capitulation-like price behavior

Volatility jumps to multi-year highs

Prices look stretched after a rapid upside surge

Position sizing and risk management become paramount

Gold shows meme-stock–like trading behavior

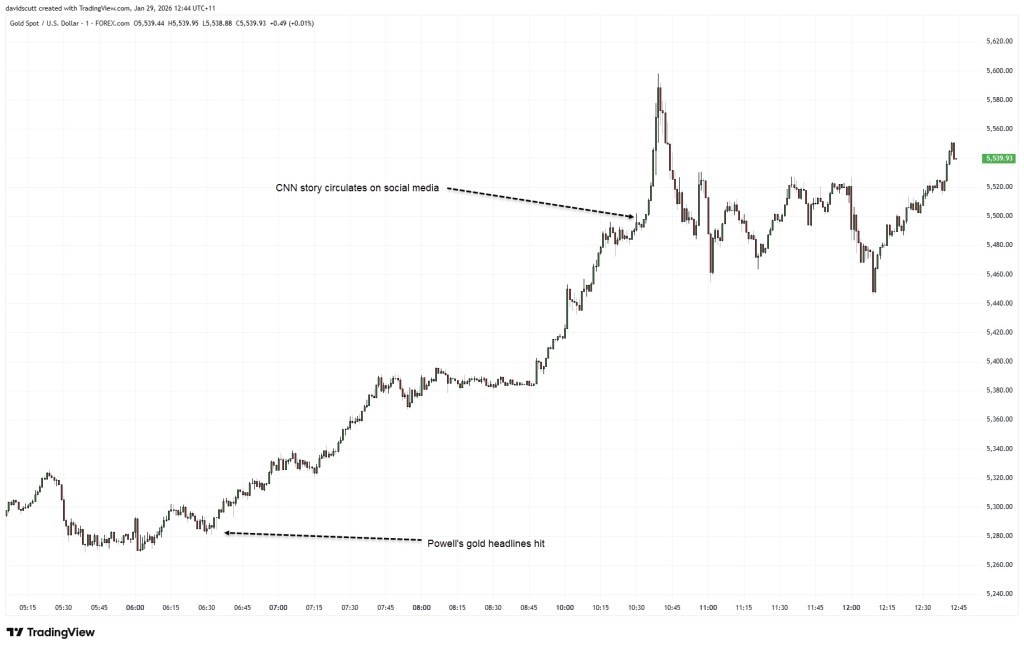

Gold behaved less like a classic safe haven and more like a meme stock on Thursday, surging nearly $100 within minutes during early Asian trading. Prices briefly spiked toward $5,600 before reversing just as quickly. The sheer speed and magnitude of the move felt like capitulation in real time, likely exacerbated by thin liquidity during the transition from North American to Asian market hours.

Although the price surge began around the same time, a CNN report later surfaced indicating that the U.S. was considering new military strikes against Iran. However, given that geopolitical tensions have been elevated for weeks rather than emerging suddenly, much of that risk was likely already priced in. In that sense, the headline appears more like a catalyst than the underlying cause of the move.

Some traders also cited comments from Fed Chair Jerome Powell after the January FOMC meeting, in which he downplayed any macroeconomic signal from gold’s record highs. Still, those remarks seem to have played only a minor role, coming several hours before the most volatile phase of the price action unfolded.

Volatility jumps sharply higher

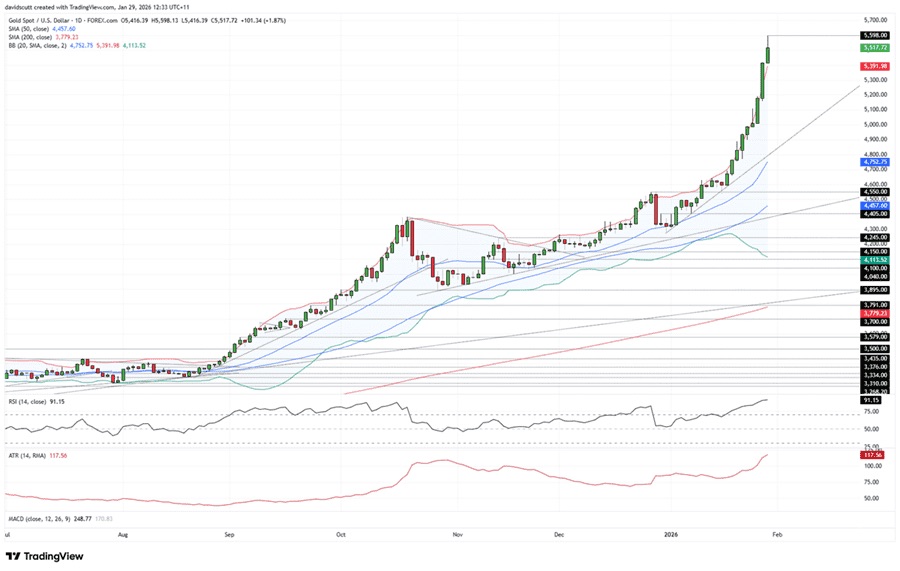

While today’s spike has understandably drawn attention, it is not an isolated event, instead forming part of a broader and accelerating expansion in volatility across the gold market.

As illustrated above, the Gold Volatility Index (GVZ) has climbed to its highest level since the early days of the COVID-19 lockdowns in 2020, highlighting just how extreme price action in the traditional safe haven has become. GVZ measures implied volatility in gold options, offering insight into the magnitude of price swings the options market is anticipating. The surge suggests the market has entered a markedly different volatility regime, one in which unusually large moves are occurring with increasing frequency.

The broader volatility environment is also clearly visible on the daily chart. Gold is trading well above its upper Bollinger Band, highlighting the speed and magnitude of the recent acceleration relative to prior conditions. Daily trading ranges have expanded sharply, with the 14-day ATR elevated at 117.56—making $100-plus moves routine rather than exceptional. Meanwhile, the 14-day RSI sits deep in overbought territory at 91.15, reinforcing that while the broader uptrend remains intact, price action is increasingly stretched and unstable.

Risk management takes center stage

In short, this is an exceptionally high-volatility environment where price behavior is far from normal. Gold has surged rapidly, leaving prices highly extended and vulnerable to sharp moves in both directions, even as the broader uptrend remains in place. In such conditions, traditional technical signals often lose reliability, making risk management and position sizing especially critical—particularly with mean-reversion risks running high.

The S&P 500 ended the session largely unchanged ahead of a largely uneventful Federal Reserve meeting, which offered little new information beyond reaffirming that the U.S. economy remains in fairly solid condition. The tone of Chair Jay Powell’s press conference also suggested that, at least while he remains at the helm, there are likely to be few—if any—interest-rate cuts in the near term.

Earnings released after the close were mixed. Microsoft (NASDAQ: MSFT) fell roughly 6.5%, while Meta Platforms (NASDAQ: META) surged about 7.5%. From an options standpoint, both stocks had bearish setups heading into earnings, with elevated implied volatility and heavy call-delta positioning at higher strike levels. Following the results, implied volatility declined, causing higher-strike calls to lose value and prompting the unwinding of hedges.

For Meta, the key technical level was $700, which the stock managed to break through, at least initially. Revenue guidance significantly exceeded expectations, leading the market to overlook higher-than-expected capital expenditures for now. The key question will be whether Meta can hold above the $700 level once regular trading resumes.

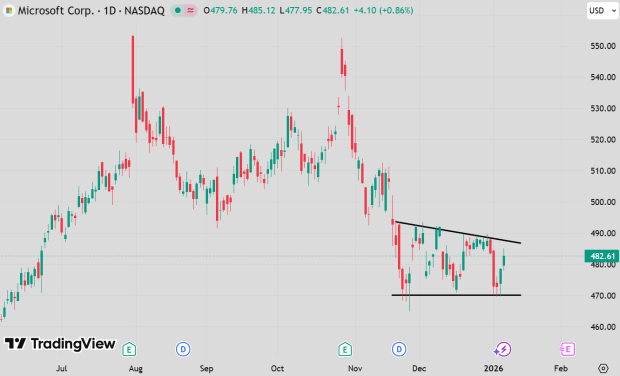

For Microsoft, the key level was $500, which the stock failed to break despite reporting better-than-expected results. Investor sentiment was weighed down by weaker-than-expected growth in its Azure cloud business.

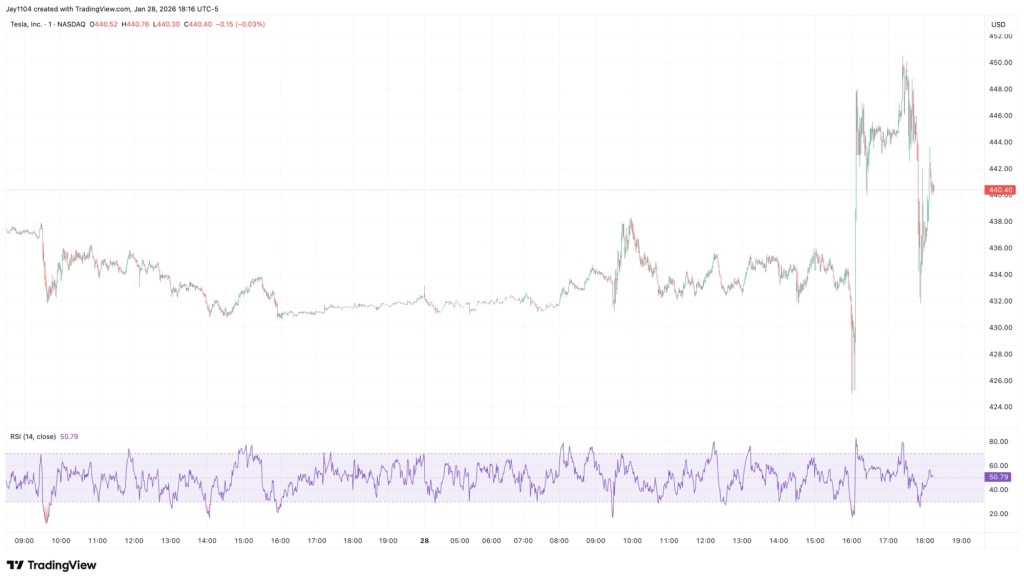

For Tesla (NASDAQ: TSLA), the setup ahead of earnings was more mixed, but $450 clearly stood out as the key level to break. So far, the stock has tested that threshold but has been unable to hold above it.

After-hours moves can be unpredictable, which is why it often makes sense to wait and see how price action develops during regular trading hours. How the CDS market trades tomorrow may be even more telling, potentially offering a clearer read on the true implications of the earnings reports.

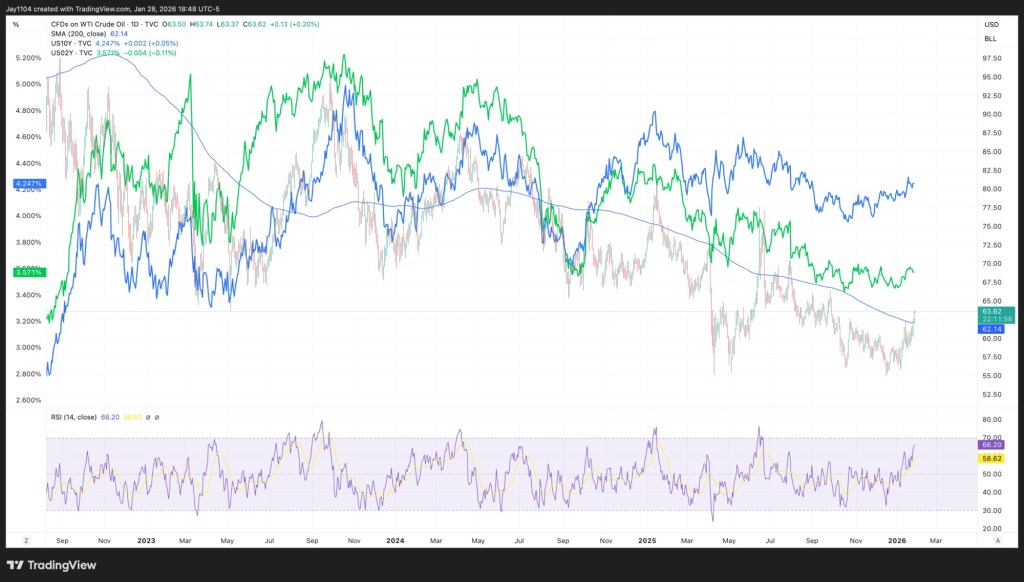

For now, near-term rate expectations appear more closely tied to oil than to any other factor. Crude has broken out and moved above its 200-day moving average, a technical development that could set the stage for a rally toward $65 in the near term.

Whether looking at the 2-year or 10-year Treasury yield, the correlation with oil prices since late 2022 has been remarkably strong. As a result, if oil continues to move higher, it would likely put upward pressure on interest rates as well. In that sense, oil may have been the final missing link in the case for higher rates.

EUR/USD extended Monday’s positive momentum, pushing closer to the key 1.2000 level and reaching highs not seen since June 2021. The latest advance reflects continued selling pressure on the U.S. dollar, supported by a constructive risk backdrop and renewed investor focus on potential tariff-related risks stemming from the White House.

Macro & Fundamental Overview

EUR/USD’s bullish momentum remains firmly intact, closely mirroring persistent selling pressure on the U.S. dollar, which continues to be weighed down by concerns over trade policy, questions surrounding the Federal Reserve’s independence, and renewed shutdown risks.

The pair extended its advance for a fourth straight session on Tuesday, edging closer to the pivotal 1.2000 level for the first time since June 2021.

The latest leg higher reflects a further deterioration in the dollar’s outlook amid revived trade tensions and geopolitical uncertainty, all ahead of the Federal Reserve’s interest rate decision due on Wednesday.

Meanwhile, sentiment surrounding U.S.–European Union trade relations has improved after President Donald Trump softened his rhetoric last week regarding potential tariffs tied to the Greenland dispute. Markets have interpreted this shift positively, boosting risk appetite and lending support to the euro alongside other risk-sensitive currencies.

By contrast, the U.S. dollar continues to underperform. The Dollar Index (DXY) remains under heavy pressure, extending its decline toward the 96.00 area — levels last seen in late February 2022.

The FED: Rates on hold, politics in focus

The Federal Reserve delivered its widely anticipated December rate cut, but the key signal came from its messaging rather than the policy action itself. A divided vote and Chair Jerome Powell’s measured language suggested that additional easing is far from assured.

The Fed begins its two-day policy meeting today, with markets largely expecting rates to remain unchanged when the decision is released on Wednesday.

However, monetary policy may not be the primary focus this time. Market attention has increasingly turned to questions surrounding the Fed’s independence after reports earlier this month of a Justice Department investigation involving Chair Powell.

Compounding the uncertainty, President Trump has indicated that an announcement on his nominee for the next Fed Chair could be imminent, keeping scrutiny on the central bank well beyond the outcome of this week’s meeting.

ECB urges patience, not complacency

The European Central Bank left interest rates unchanged at its December 18 meeting, adopting a more measured and patient tone that has pushed expectations for near-term rate cuts further into the future. Modest upward revisions to growth and inflation projections helped underpin this approach.

Minutes from the meeting, released last week, showed policymakers saw little immediate need to adjust policy. With inflation hovering near target, the ECB has room to remain patient, while still retaining flexibility should risks materialize.

Governing Council members emphasized that patience does not equate to complacency. Monetary policy is viewed as appropriately calibrated for now, but not on autopilot. Markets appear to have absorbed this message, currently pricing in just over 4 basis points of easing over the coming year.

Positioning remains constructive, but confidence has softened

Speculative positioning remains tilted toward the euro, although bullish conviction appears to be easing.

CFTC data for the week ended January 20 show non-commercial net long positions declining to a seven-week low of around 111.7K contracts. At the same time, institutional participants also reduced short positions, which now stand near 155.6K contracts.

Meanwhile, open interest slipped to approximately 881K contracts, breaking a three-week streak of increases and suggesting that market participation may be thinning alongside fading confidence.

Key Events Ahead

Near term: The FOMC meeting is set to keep attention firmly on the U.S. dollar, while flash inflation data from Germany and preliminary GDP readings for the euro area will dominate the regional data calendar later in the week.

Risk: A more hawkish-than-expected outcome from the Fed could quickly tilt momentum back in favor of the dollar. In addition, a clear break below the 200-day simple moving average would increase the risk of a deeper medium-term correction.

EUR/USD Technical Outlook

EUR/USD continues to exhibit a firm bullish bias, trading at levels last seen in mid-2021 while gradually shifting focus toward the key 1.2000 psychological handle.

On the downside, initial support is located at the 2026 low of 1.1576 (January 19), reinforced by the closely watched 200-day simple moving average. A more pronounced correction could open the door to the November 2025 trough at 1.1468, followed by the August base at 1.1391.

Momentum indicators remain broadly supportive of further gains, although elevated conditions may challenge the immediate upside. The Relative Strength Index is hovering near 75, pointing to overbought territory, while an Average Directional Index reading above 26 confirms the presence of a well-established trend.

Bottom Line

For the time being, EUR/USD continues to be influenced primarily by U.S.-centric developments rather than euro area dynamics.

Absent clearer signals from the Federal Reserve on the extent of potential policy easing, or a more compelling cyclical recovery in the eurozone, any additional upside is likely to unfold in a steady, incremental manner rather than marking the beginning of a decisive breakout.

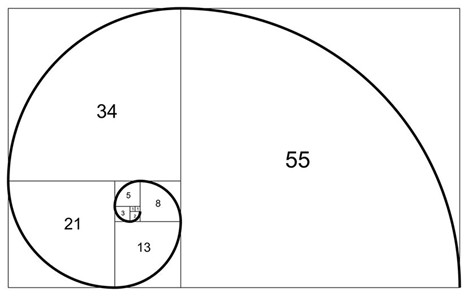

Did you know that a form of technical analysis shares structural patterns with hurricanes, nautilus shells, sunflowers, music, and even human proportions? These phenomena—along with countless others—adhere to ratios derived from a numerical sequence: 0, 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89… Known as the Fibonacci sequence, these numbers generate ratios that are widely used as a technical framework for analyzing and managing financial markets.

Before it sounds like we’re turning to biology—or worse, mysticism—to forecast stock prices, let’s explain how this concept is applied in a practical, market-driven way.

Fibonacci Patterns Are Everywhere

As shown in the diagram, drawing quarter-circle arcs across adjacent squares whose side lengths follow the Fibonacci sequence (1, 1, 2, 3, 5, 8, 13, 21, and so on) creates an expanding spiral that closely resembles the shape of a nautilus shell.

Each number in the sequence is the sum of the two numbers before it. Importantly, the ratios between consecutive Fibonacci numbers converge toward the golden ratio, 1.618, often referred to as Phi. Its inverse—obtained by dividing the smaller number by the larger—approaches 0.618, a relationship that underpins many Fibonacci-based applications in both nature and financial markets.

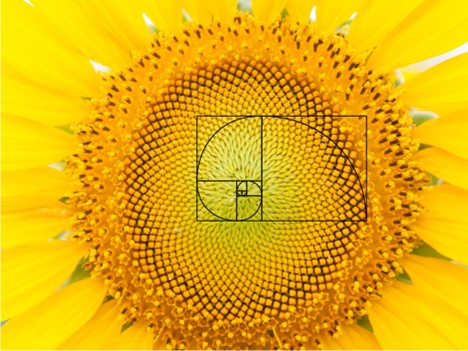

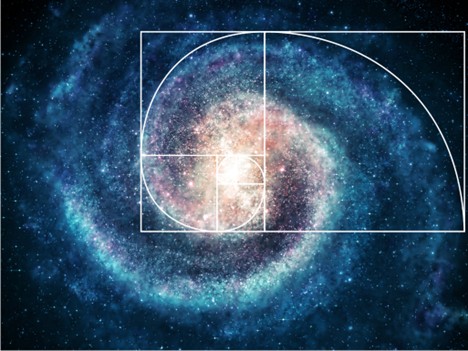

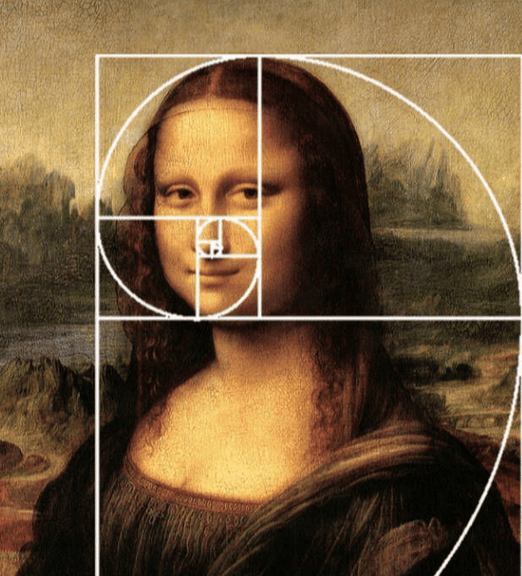

Below are several examples of natural and human-made phenomena that reflect the Fibonacci sequence and the golden ratio:

Spiral Galaxies: The arms of some galaxies expand outward in patterns that closely resemble a Fibonacci spiral.

Sunflowers: The arrangement of seeds often forms intersecting spirals—commonly 34 in one direction and 55 in the other, or sometimes 55 and 89—consistent with Fibonacci numbers.

Cauliflower: The spiraling florets frequently appear in counts such as five, eight, or thirteen per cluster, reflecting Fibonacci-based growth patterns.

Piano Keys: A standard octave contains 13 keys—8 white and 5 black—with the black keys grouped in sets of two and three.

The Mona Lisa: As noted by Math Central, the painting contains multiple golden rectangles. When a rectangle is drawn around the subject’s face, its proportions closely align with the golden ratio. Dividing this rectangle at eye level creates another golden rectangle, and similar proportions can be observed from her neck to the top of her hands.

It is widely believed that the Fibonacci sequence and the golden ratio underpin aspects of the brain’s structure and cognitive processes.

According to Professor Adrian Bejan of Duke University, as cited in The Atlantic:

“This represents the most efficient flow of visual information from the eye to the brain, which is why it so often appears in human-made designs that seem to be intentionally structured around the golden ratio.”

Market Prices and Fibonacci Relationships

Human brains are naturally inclined to search for, recognize, and react to patterns. As a result, we subconsciously gravitate toward Fibonacci relationships and the golden ratio. This tendency helps explain why many works of art, music, and poetry incorporate Fibonacci structures. It also sheds light on why Fibonacci-based tools can be effective for market technicians in identifying support and resistance levels, as well as projecting potential breakout targets.

Retracements/Support

Fibonacci sequences—particularly the golden ratio—are commonly used by technicians to identify potential support and resistance levels within a defined price range.

In the example shown, the selected range starts from the early April 2025 lows and extends to the highs formed in October and December. Once this range is established, Fibonacci retracement levels are applied to identify likely areas of support. The percentages referenced represent the portion of the total price range where Fibonacci-based support is expected to emerge.

78.6% – Derived from the square root of the golden ratio (61.8%). While not part of the Fibonacci sequence itself, this level is widely used in Fibonacci analysis.

61.8% – The golden ratio, calculated from the relationship between 55 and 34 (34 ÷ 55).

50% – Not a true Fibonacci retracement, but the midpoint of a range is a key psychological level and is commonly included in Fibonacci studies.

38.2% – A two-step retracement from 55 to 21 (21 ÷ 55), often viewed as a secondary support or resistance level.

23.6% – A three-step retracement from 55 to 13 (13 ÷ 55), typically representing shallow pullbacks within strong trends.

In the example above, the S&P 500 (SPY) is expected to find initial support near 640.34, which represents the first Fibonacci retracement level. The next key support area lies around 609.99, aligning with the 61.8% golden ratio retracement.

The Fibonacci chart referenced above was generated using SimpleVisor’s charting platform.

Fibonacci Extension/Profit Targets

Fibonacci analysis can also be used to project potential resistance levels once prices move to new highs. The main limitation of this approach is that it requires estimating where the trend is likely to peak, making it less reliable than the prior resistance analysis discussed earlier.

As illustrated in the chart, the same Fibonacci ratios are applied by extending the bullish trend from the recent high toward the 800 level.

Summary

You should never depend on a single form of technical analysis. The most effective insights come from combining multiple patterns and indicators. No method is infallible, but when several approaches point to the same conclusion, the probability of a favorable outcome increases.

Although skeptics argue that Fibonacci analysis is simply pattern recognition, its widespread use across financial markets highlights its lasting value as a tool that sits at the intersection of mathematics, investor psychology, and market behavior.

The year ahead offers a clear divide between bullish and bearish outcomes for investors. Will 2026 deliver another period of above-average returns, or mark a turning point toward disappointment? Optimists contend that the foundations for a sustained rally remain intact. A robust technology cycle, heavy corporate investment, and supportive policy settings all suggest further upside. Pessimists, however, warn that key growth drivers are losing momentum, market leadership has become uncomfortably narrow, and underlying economic stress is increasingly evident.

After a strong 2025, investors are entering a shifting market environment. Liquidity is still plentiful, but concerns over stretched valuations, labor-market pressure, and consumer resilience are mounting. Much hinges on how long optimism can outweigh economic realities, and whether expected gains from artificial intelligence and capital spending arrive quickly enough to counteract the drag from debt burdens, interest costs, and widening inequality.

Sentiment remains broadly constructive, though far from unanimous. Equity strategists are split, while bond markets reflect expectations of rate cuts alongside rising recession risk. Fiscal stimulus may postpone a downturn, but it also exacerbates longer-term imbalances. For investors, the central challenge is maintaining objectivity. Both the bullish and bearish narratives are credible, and timing will be decisive. In fact, 2026 could validate elements of both cases, making adaptability the most valuable strategy.

Below, we examine the bullish and bearish scenarios for 2026 in detail, assessing the macroeconomic and market forces behind each view. By translating these dynamics into practical portfolio considerations, investors can prepare for either outcome. Ultimately, success in 2026 will hinge less on forecasting accuracy and more on disciplined risk management.

The Bullish Case

The bullish thesis rests on several core pillars: a fresh surge in technology-led investment, accommodative fiscal policy, improving liquidity conditions, and the ongoing strength of both corporate balance sheets and consumer activity. Together, these forces have propelled markets higher, and proponents argue they will continue to support gains through 2026.

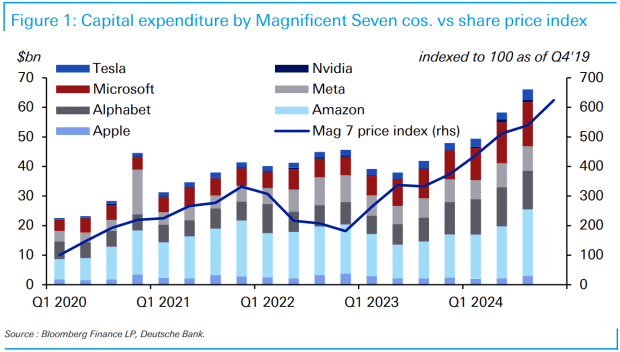

Central to the bull case is the rise of a potentially transformative technology cycle driven by artificial intelligence and large-scale infrastructure upgrades. Unlike earlier tech booms fueled primarily by optimism, this cycle is already translating into substantial capital spending. The so-called “Magnificent Seven” have collectively pledged over $600 billion toward data centers, semiconductor capacity, and AI-related services. This investment is rippling across software, energy, and industrial supply chains. Should the anticipated productivity improvements materialize, corporate earnings could accelerate, providing fundamental support for elevated valuations.

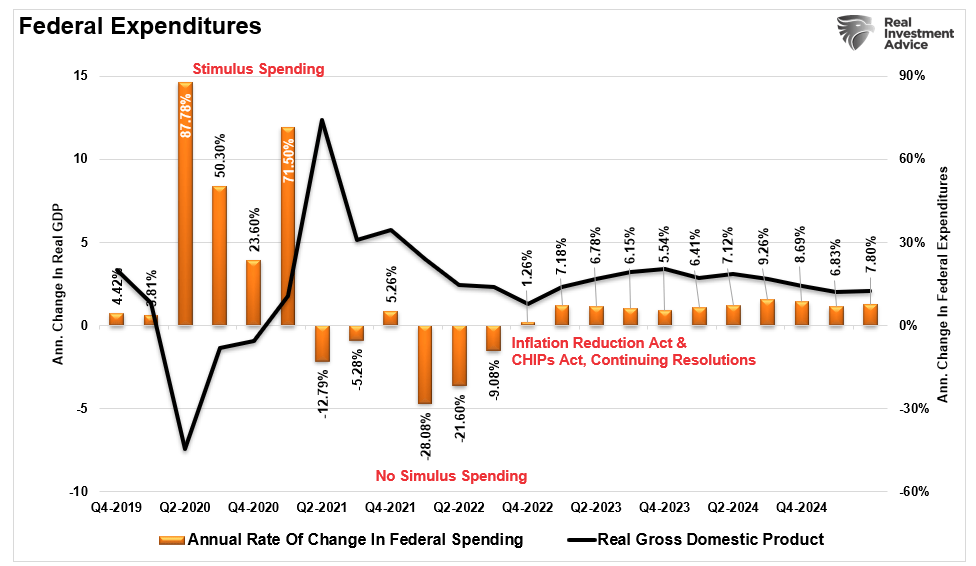

Fiscal policy is also positioned to support growth. Under a Trump-led administration, proposed tax cuts and direct transfers are expected to bolster both corporate activity and consumer spending. While $2,000 stimulus checks may not appear dramatic on their own, they can meaningfully lift short-term consumption and provide relief to small businesses. When paired with income tax reductions, these initiatives create a favorable backdrop for GDP growth and market sentiment. As recent history shows, following the 2022 market correction and widespread recession concerns, ongoing fiscal support has continued to play a stabilizing role in economic expansion.

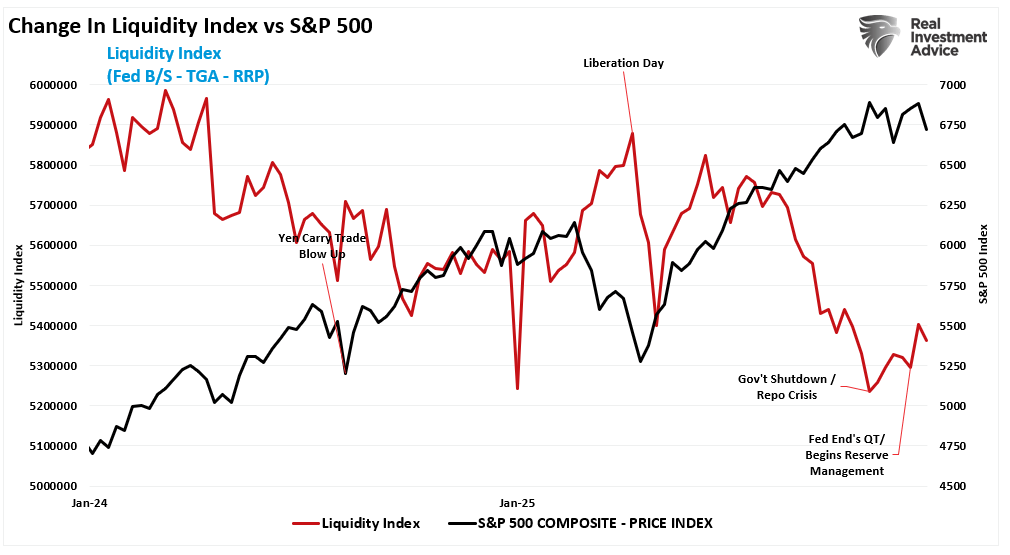

The monetary environment is also turning more supportive for bulls. Quantitative tightening concluded in December 2025, and the Federal Reserve has since shifted toward what many describe as “QE Lite,” combining rate cuts with monthly purchases of roughly $40 billion in short-term Treasuries. Officially framed as “reserve management,” the objective is to maintain ample liquidity within the financial system. As interest rates decline, credit conditions are likely to loosen, providing a favorable backdrop for risk assets. Rising liquidity has historically supported higher equity valuations, with technology and growth stocks typically benefiting the most from this dynamic.

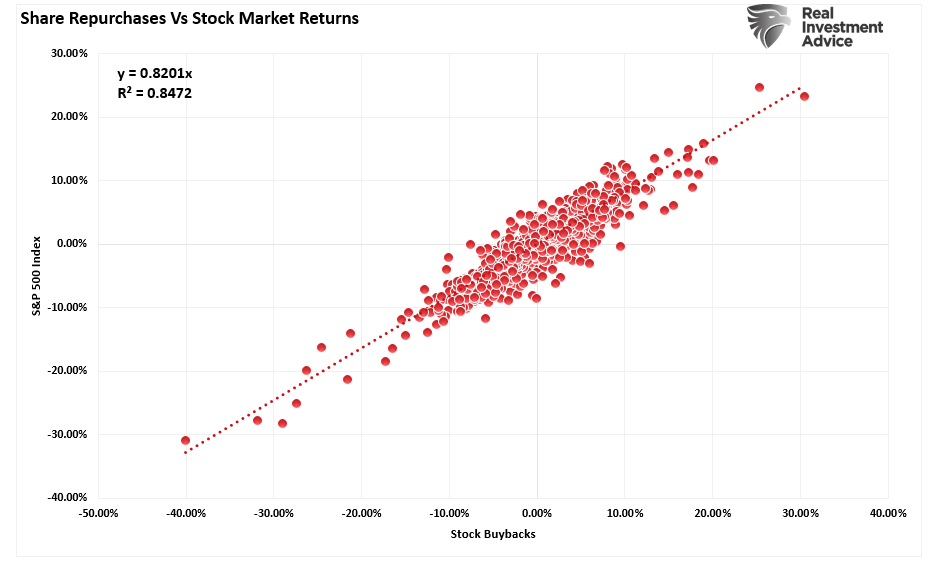

Corporate actions further reinforce the bullish narrative. Share buyback authorizations are projected to reach a new record of more than $1.2 trillion in 2026. Although often framed as a “capital return strategy”—a characterization that misses the point—buybacks have shown a strong correlation with equity market performance. Notably, since 2000, corporate repurchases have accounted for nearly all net equity demand, underscoring their outsized influence on stock prices.

Importantly, the notion that buybacks signal management’s confidence in future earnings is misleading. In practice, repurchases are frequently used as a form of financial engineering to boost per-share results and beat Wall Street expectations. This dynamic is likely to intensify in 2026, further supporting reported earnings growth and reinforcing the bullish case.

Finally, deregulation tied to the so-called “Big Beautiful Bill” is expected to relax capital requirements for banks, enabling them to hold a greater amount of collateral. While this should support the Treasury market, it also expands overall lending capacity. Much of that capacity is likely to flow into leverage for hedge funds and Wall Street trading desks, as looser regulatory constraints encourage greater risk-taking.

The bullish thesis ultimately rests on a reinforcing feedback loop: innovation spurs capital investment, rising investment lifts earnings, policy measures inject liquidity, and investors respond by increasing risk exposure. As long as each link in this chain remains intact, the upward trend can persist.

The Bearish Case

The bearish case starts with a key observation: many of the forces that powered the 2025 rally are now fading or already fully reflected in prices. Elevated valuations, softening economic data, and rising speculative excesses suggest that current market momentum may be masking deeper structural vulnerabilities. With that in mind, it is worth examining several of these risks more closely.

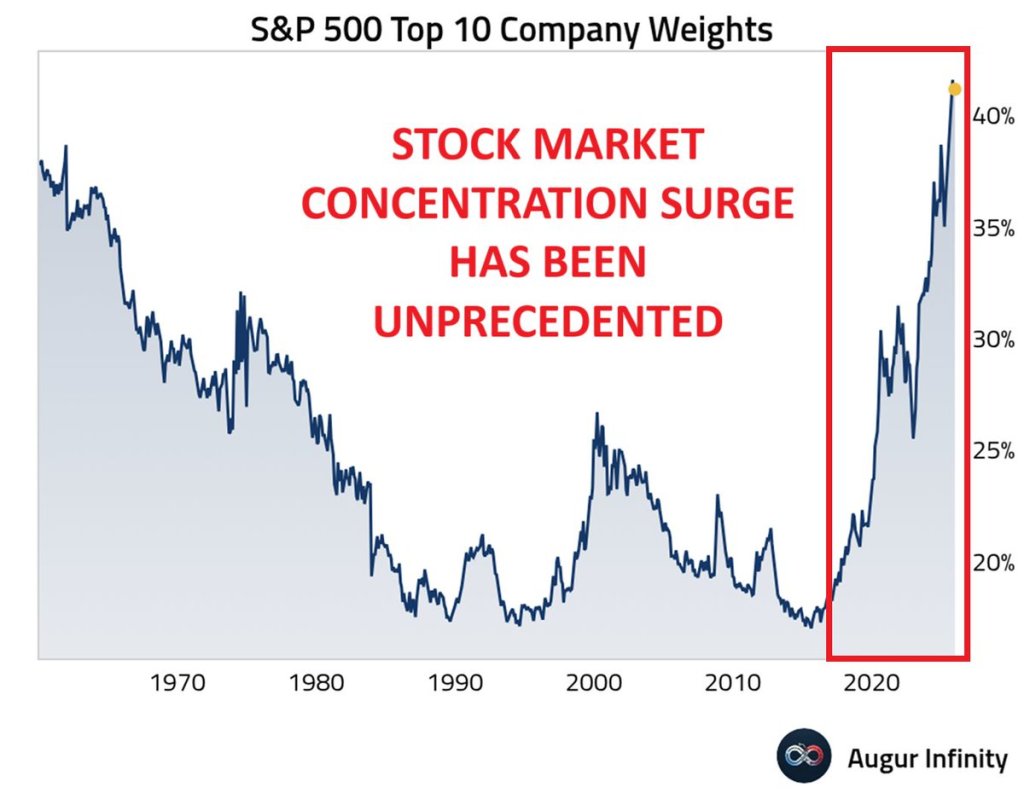

One of the most visible concerns is market concentration. In 2025, the bulk of equity gains came from just 10 companies on a market-capitalization-weighted basis, a dynamic amplified by the continued shift into passive ETF investing.

Passive investing has evolved from a niche approach into the dominant force shaping equity markets. Index funds and ETFs now represent more than half of U.S. equity ownership. Because these vehicles allocate capital according to market capitalization rather than valuation, fundamentals, or business quality, the largest companies attract a disproportionate share of inflows. This has created a powerful feedback loop in which rising prices draw in more capital, and those inflows, in turn, push prices even higher.

This narrow leadership is inherently fragile. Should investor flows into ETFs reverse, a disproportionate share of selling—roughly 40%—would be concentrated in the same 10 stocks. History shows that when market performance depends on a small handful of names, volatility tends to increase and drawdowns can be sharp.

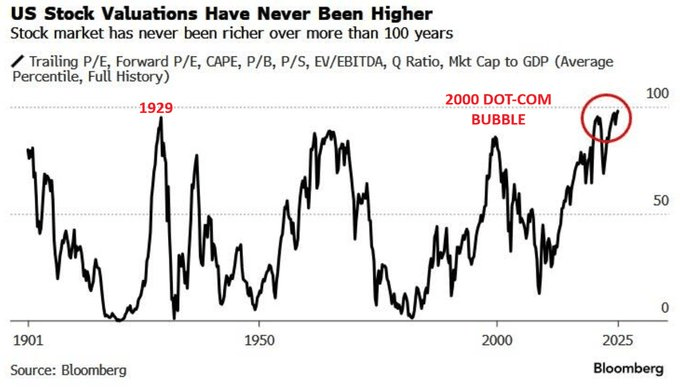

Valuations present another clear risk. Price-to-earnings multiples on the S&P 500 remain near cycle peaks, leaving little room for error. Growth assumptions are ambitious, and even modest earnings disappointments could trigger a meaningful repricing. While enthusiasm around AI has driven a surge in investment, much of this spending is circular—companies are investing in AI largely to produce and sell AI-related products. That dynamic may prove self-limiting over time, particularly if end demand weakens or costs begin to outstrip returns.

A significant portion of the current investment cycle is also being financed with debt, as companies borrow to fund capital spending, repurchase shares, and sustain dividend payouts. If interest rates remain high or credit conditions deteriorate, rising debt-servicing costs could quickly erode earnings gains.

The broader economic risk is that the reallocation of capital toward technology and automation could sideline large segments of the workforce. While the buildout of data centers may employ thousands during construction, only a fraction of those jobs—perhaps a few hundred—remain once operations begin. Over time, this dynamic could weigh on employment growth, increase the risk of demand destruction, and may already be showing early warning signs.

This dynamic underpins the concept of a “K-shaped economy.” While high-income households and asset owners continue to prosper, lower-income consumers are facing increasing strain. Consumption patterns are diverging as financially pressured households cut back, leaving the top 20% of earners responsible for nearly half of total consumer spending. Signs of stress are already emerging, with rising auto loan and credit card delinquencies, stagnant real wages for many workers, and persistently high costs for housing and essential goods.

At the same time, risks within the credit system—particularly in private markets—are growing. Private credit has expanded rapidly in recent years, yet limited transparency makes it difficult to fully assess systemic vulnerabilities. Regulators have begun to pay closer attention, and default rates in middle-market lending are climbing. Should these stresses intensify, the fallout could extend across banks, hedge funds, and pension portfolios.

The bearish argument is not one of an imminent crash, but of growing fragility. Beneath the headline gains, the market appears increasingly exposed to earnings disappointments, tighter credit conditions, and weakening consumer demand.

The key takeaway is that 2026 may validate elements of both the bullish and bearish narratives. Preparation, rather than prediction, will be essential.

Navigating Whatever Comes Our Way

Investors should treat 2026 as a year in which both the bullish and bearish narratives may ultimately be validated. In the first half, bullish momentum is likely to persist, supported by strong sentiment, ample liquidity, and continued growth in corporate investment. Optimism around AI, fiscal support, and a potential pause in monetary tightening could propel equity indexes higher.

By the second half, however, underlying vulnerabilities may begin to surface. Elevated valuations increase sensitivity to earnings disappointments, while widening economic inequality could weigh on the outlook for consumer demand and corporate revenues. Should these pressures intensify, market sentiment could shift rapidly.

Navigating such a divided year will require a tactical approach—participating in early upside while avoiding excessive exposure to risks that may materialize later in the year.

Early 2026: Participate in Momentum, but Manage Exposure

Overweight sectors poised to benefit from capital spending and ample liquidity, including technology, industrials, and energy.

Prioritize high-quality growth companies with durable earnings and strong cash-flow generation, rather than momentum-driven narratives.

Implement trailing stop-loss strategies to protect gains if market sentiment shifts.

Use periods of volatility to add selectively, while scaling back position sizes as valuations become more stretched.

Avoid excessive concentration in AI-related stocks, even during strong rallies, as crowding increases dispersion and downside risk.

Mid-to-Late 2026: Emphasize Defense and Cash-Flow Stability

Gradually rotate toward defensive, value-oriented sectors such as healthcare, consumer staples, and utilities.

Increase exposure to dividend-paying companies with strong balance sheets and resilient cash flows.

Raise cash allocations or shift into short-duration Treasuries to preserve flexibility.

Allocate selectively to high-quality credit while reducing exposure to private credit and high-yield debt.

Monitor consumer credit conditions, labor-market trends, and bank earnings for early signs of financial stress.

Throughout the Year: Maintain Discipline and Objectivity

Adhere to valuation discipline regardless of shifts in market narratives.

Keep portfolios well diversified to withstand both volatility and sector rotation.

Let data—not headlines—drive allocation decisions.

Rebalance regularly, particularly if strong first-half performance leads to excessive concentration in certain sectors.

In 2026, tactical flexibility, risk awareness, and discipline are likely to matter more than adopting a purely bullish or bearish stance. It is a year in which both camps could be partially wrong. Markets rarely move in straight lines, but a sound investment process should remain consistent throughout.

The year ahead is likely to test investors with heightened volatility, as both the bullish and bearish arguments carry real weight. A new technology cycle may generate genuine economic momentum, yet it also introduces risks tied to elevated valuations, debt-fueled growth, and widening inequality. With markets effectively pricing in near-perfection, history suggests outcomes often fall short of expectations.

Whether 2026 delivers further gains or a sharp correction, performance will hinge on effective risk management. Avoid anchoring to any single narrative. Let data guide decisions, respect your signals, and remain willing to adjust as conditions evolve.

Ultimately, the objective is not to chase short-term returns, but to endure—and compound—across full market cycles.

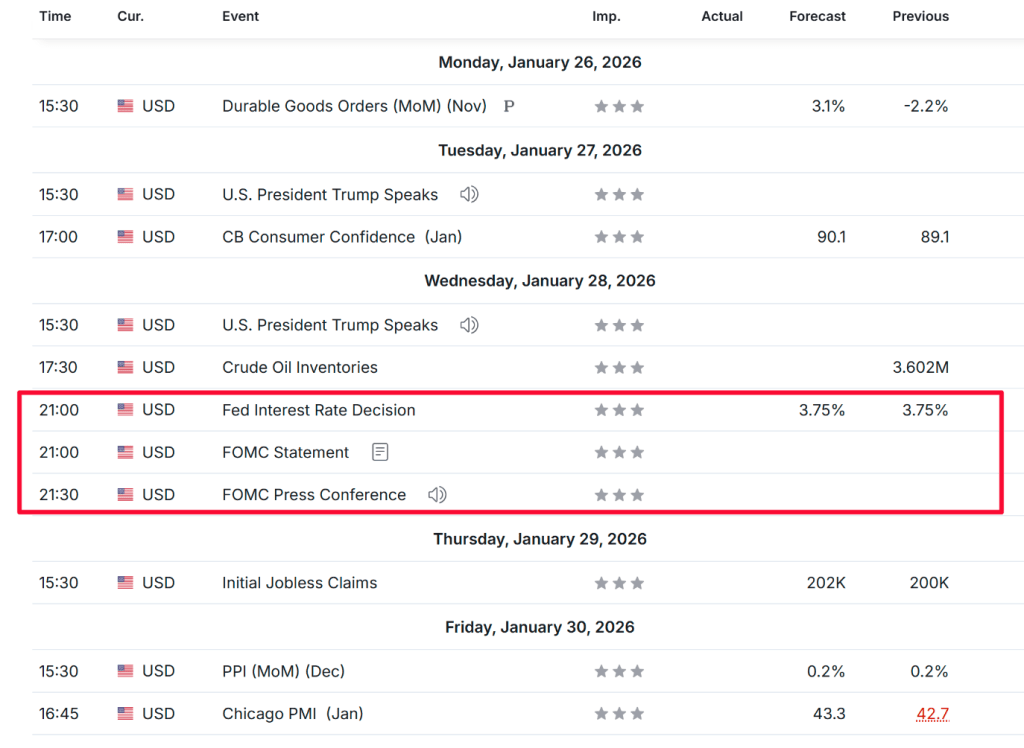

This week’s spotlight will be on the Fed’s FOMC meeting, Chair Powell’s press conference, major Big Tech earnings, and the looming U.S. government shutdown deadline. Apple is set to report earnings after Thursday’s close, with expectations rising for a beat-and-raise quarter. Meanwhile, Starbucks looks like a sell, as profit growth continues to slow and a weaker outlook is anticipated.

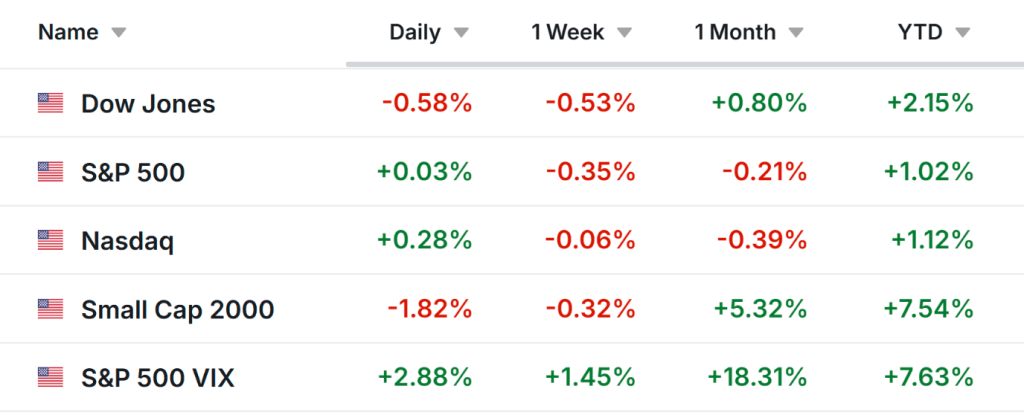

The stock market finished Friday on a mixed note, as both the S&P 500 and Nasdaq Composite recorded their second consecutive weekly declines.

The Dow Jones Industrial Average slipped 0.5% for the week, while the S&P 500 edged down about 0.4%. The tech-heavy Nasdaq fell by less than 0.1%, and the small-cap Russell 2000 lost 0.3%.

Looking ahead, the coming week is set to be a blockbuster, packed with potential market catalysts. Investors will be watching a crucial Federal Reserve policy meeting alongside a wave of earnings from major technology companies.

The Fed is widely expected to hold interest rates steady on Wednesday, though markets could see volatility as Chair Jerome Powell addresses the media in his post-meeting press conference.

Other key economic releases on the calendar include durable goods orders on Monday and The Conference Board’s Consumer Confidence Index for January on Tuesday. Friday will also bring the release of the December producer price index.

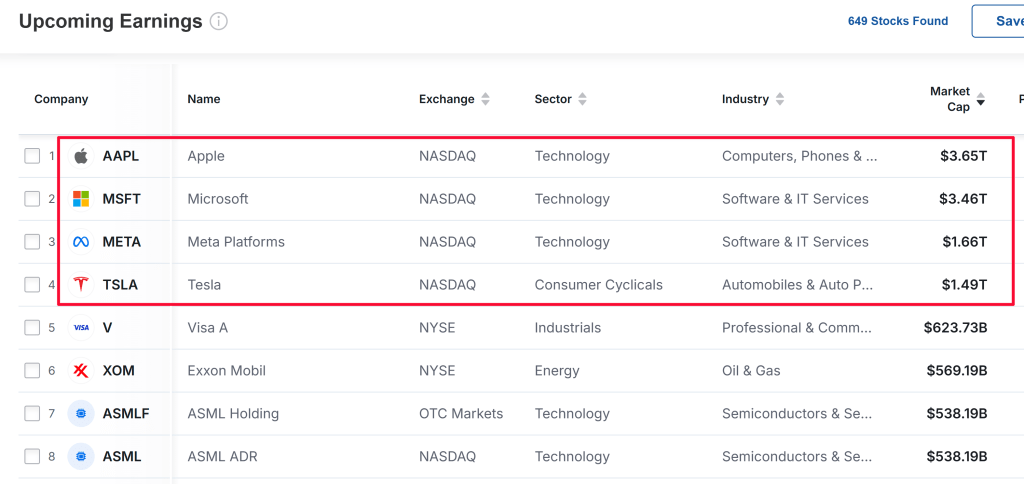

At the same time, earnings season ramps up sharply, with four members of the “Magnificent Seven” set to report this week. Microsoft (NASDAQ:MSFT), Tesla (NASDAQ:TSLA), and Meta Platforms (NASDAQ:META) are scheduled to announce results Wednesday evening, followed by Apple (NASDAQ:AAPL) after the close on Thursday.

These mega-cap names will be joined by a long list of other major companies, including IBM (NYSE:IBM), ASML (NASDAQ:ASML), SanDisk, Exxon Mobil (NYSE:XOM), Chevron (NYSE:CVX), Visa (NYSE:V), Mastercard (NYSE:MA), American Express (NYSE:AXP), SoFi Technologies (NASDAQ:SOFI), UnitedHealth Group (NYSE:UNH), Boeing (NYSE:BA), UPS (NYSE:UPS), Caterpillar (NYSE:CAT), General Motors (NYSE:GM), Verizon (NYSE:VZ), AT&T (NYSE:T), Starbucks (NASDAQ:SBUX), American Airlines (NASDAQ:AAL), RTX (NYSE:RTX), and Lockheed Martin (NYSE:LMT).

Adding to the uncertainty, Congress faces a Friday deadline to fund the government once again, with the risk of a prolonged shutdown looming.

No matter how markets ultimately move, I outline below one stock that could attract strong buying interest and another that may face renewed downside pressure. Keep in mind, this outlook is strictly for the week ahead, from Monday, January 26 through Friday, January 30.

Stock to Buy: Apple

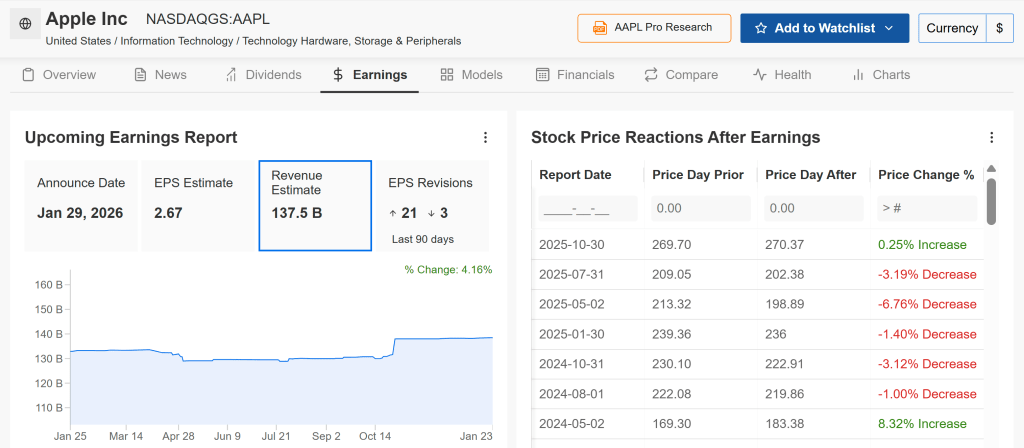

Apple is scheduled to report earnings after the market closes on Thursday, with conditions lining up for a possible upside surprise. Wall Street is increasingly calling for a beat-and-raise quarter, as consensus forecasts point to double-digit revenue growth fueled by steady iPhone demand and continued expansion in services.

Options markets are pricing in a post-earnings move of roughly plus or minus 4%. Meanwhile, earnings expectations have turned more optimistic, with profit estimates revised higher 21 times in recent weeks versus just three downward revisions, according to InvestingPro data—underscoring the growing bullish sentiment surrounding Apple’s results.

Apple is expected to post adjusted earnings of $2.67 per share, representing an 11.2% increase from a year ago, while revenue is projected to climb 10.6% year over year to $137.5 billion. Analysts are looking to the iPhone and Services segments to lead the charge, pointing to double-digit growth and a strong pipeline of upcoming products, including a foldable iPhone and an AI-enhanced Siri.

With sentiment leaning bullish, the market appears positioned for a positive surprise. Price targets reaching as high as $350—implying roughly 41% upside—suggest that even a modest earnings beat could be enough to trigger a rebound in the stock.

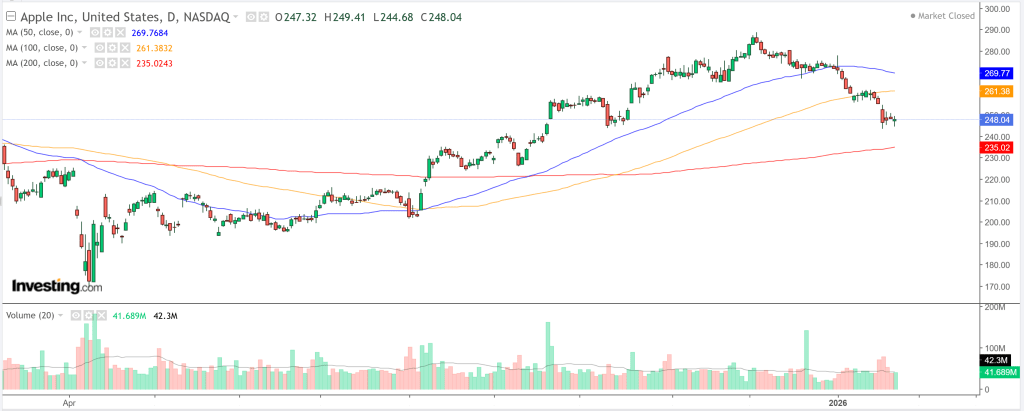

So far in 2026, Apple shares have struggled, falling roughly 9% year to date to finish Friday at $248.04. The decline has mirrored broader volatility across the tech sector, alongside investor concerns that Apple’s AI strategy may be lagging rivals such as Alphabet.

That said, the recent pullback is shaping up as a potential buying opportunity. The stock is trading in deeply oversold territory, and while daily technical indicators still signal a “Strong Sell,” key support sits near $247.53 (pivot S1). A decisive move above resistance at $248.87 could open the door to a rebound toward $260 or higher, particularly if earnings guidance exceeds expectations.

Trade Setup:

Entry: $248 (pre-earnings)

Target: $265 (gain ~7%)

Stop-Loss: $240 (risk ~3%)

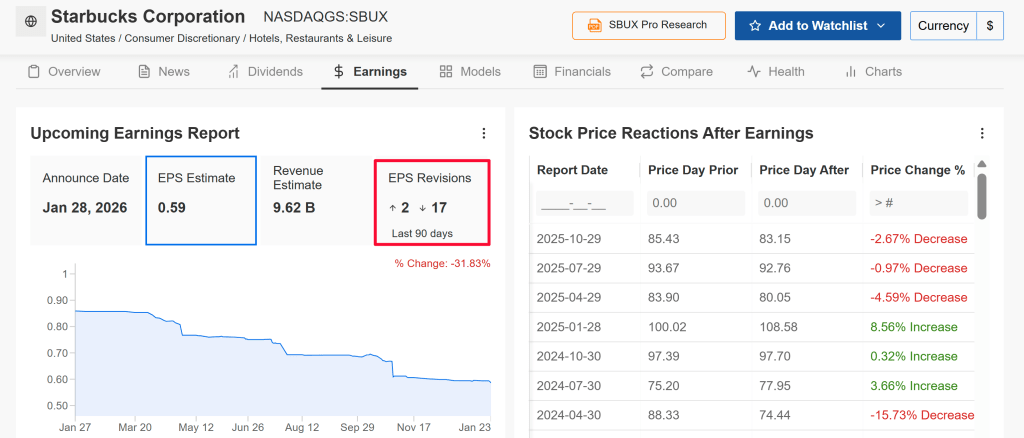

Stock to Sell: Starbucks

Starbucks is set to report earnings Wednesday morning, but unlike Apple, it heads into the week on much shakier footing. The coffee chain is grappling with slowing same-store sales in core markets, intensifying competition, changing consumer spending habits, and persistent cost pressures from labor and commodities.

Options markets are pricing in a post-earnings move of about plus or minus 6.4%, highlighting elevated downside risk. Sentiment has also turned notably bearish, with 17 of the 19 analysts tracked by InvestingPro cutting their EPS forecasts over the past three months ahead of the report.

Wall Street is bracing for a difficult quarter, with earnings per share projected to fall 15.9% year over year to $0.59, even as revenue is expected to edge up 2.5% to $9.62 billion.

Starbucks is also contending with intensifying competition from value-focused fast-food chains such as McDonald’s and Dunkin’, alongside pressure from local coffee shops. At the same time, its China growth narrative—once a major upside driver—has increasingly become a source of investor concern.

Looking ahead, expectations are building that CEO Brian Niccol may caution about continued near-term weakness, citing softer customer traffic, higher operating costs, and lingering uncertainty around the company’s turnaround efforts.

So far in 2026, Starbucks has been one of the stronger performers, climbing roughly 16% year to date and closing Friday at $97.62. However, the technical setup suggests the stock may be overextended heading into earnings.

Key pivot support lies near $96.25, with resistance around $97.84. A downside break below support could open the door to a pullback toward the $90 level if earnings or guidance disappoint.

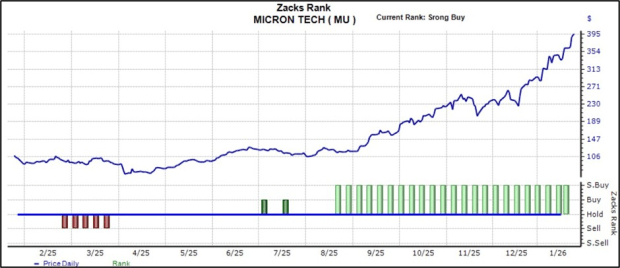

Micron (MU) is a global leader in advanced memory and storage technologies, playing a critical role in converting data into actionable intelligence. The stock has surged amid the AI-driven rally, as Micron’s products have become an essential component of AI infrastructure, particularly in addressing persistent memory bottlenecks.

The shares also highlight the effectiveness of the Zacks Rank framework. In August of last year, Micron was upgraded to the highly sought-after Zacks Rank #1 (Strong Buy) following upward revisions to earnings estimates, a shift that has since been accompanied by a strong and sustained rally in the stock price.

As illustrated above, the Zacks Rank may also have helped mitigate downside risk last March.

Why Micron Shouldn’t Be Overlooked

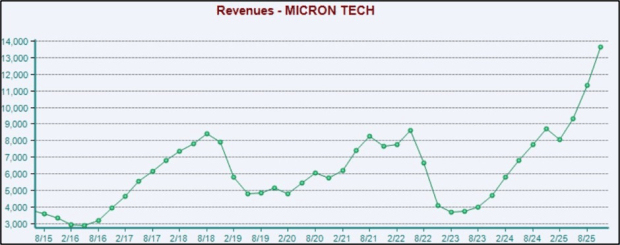

Micron delivered outstanding results in its latest earnings report, surpassing consensus expectations on both revenue and earnings, driven by rapidly accelerating demand tied to AI workloads. Revenue surged more than 55% year-over-year to a record high, while adjusted EPS jumped an impressive 185%.

The company’s cash-generation profile also strengthened significantly amid the favorable demand backdrop. Operating cash flow reached a record $8.4 billion during the period, sharply exceeding the $5.7 billion generated in the same period last year.

The positive momentum appears set to continue, with Micron’s Q2 guidance pointing to new records across revenue, margins, earnings, and free cash flow. In short, Micron plays a critical role in enabling the AI boom, as memory capacity remains a key bottleneck in advanced systems. This strategic positioning places the company in a strong overall stance and helps shield it from concerns about being an AI “also-ran” or laggard.

As illustrated below, Micron’s revenue has surged sharply in recent periods, reinforcing the strength of the current demand environment. The company’s top-line trajectory mirrors that of NVIDIA (NVDA – Research Report), widely regarded as the flagship beneficiary of the broader AI trade.

Micron vs. NVIDIA

While many AI-linked companies are likely to come under increased scrutiny in 2026, Micron represents a far more straightforward beneficiary of the broader infrastructure buildout. Memory remains a key bottleneck in AI systems, and MU has been capitalizing meaningfully on this constraint. The company recently announced its exit from the consumer memory segment, further underscoring its strategic focus on maximizing revenue from large-scale enterprise and data-center customers.

Micron noted that “AI-driven growth in the data center has led to a sharp increase in demand for memory and storage,” adding that the decision to wind down its Crucial consumer business was made to improve supply allocation and support for larger, strategic customers in faster-growing markets.

Overall, Micron stands out as one of the most compelling AI-related investment opportunities, drawing a clear parallel with NVIDIA. While NVIDIA dominates the GPU side of AI computing, Micron plays an equally critical role by supplying the high-performance memory required for those GPUs to operate efficiently.

Turning to NVIDIA, the company once again delivered a double beat versus consensus in its latest, record-setting earnings report. Revenue reached $57 billion, up 62% year-over-year, alongside a 67% surge in earnings per share. Data Center revenue climbed to $51.2 billion, representing a robust 66% annual increase and comfortably exceeding consensus expectations of $49.1 billion.

For investors looking to capitalize on the AI infrastructure buildout, both Micron (MU – Research Report) and NVIDIA (NVDA) stand out as premier choices, with each currently holding the highly sought-after Zacks Rank #1 (Strong Buy).

GBP/USD is extending its strong weekly rally and is edging closer to the 1.3600 handle on Friday, marking fresh four-month highs. The pair’s upside momentum is being fueled by a deepening decline in the US Dollar, while supportive UK economic data further reinforces the bullish trend.

Fundamental Analysis Overview

The latest PMI data signaled a strong expansion in overall business activity, driven by a notable pickup in both manufacturing and services. The Composite PMI surged to 53.9 in January from 51.4 in December, comfortably surpassing market expectations of 51.7.

The Services PMI climbed to 54.3, exceeding both the forecast of 51.7 and the previous reading of 51.4, while the Manufacturing PMI also improved markedly, rising to 51.6 from 50.6.

In addition, UK Retail Sales rebounded in December after two consecutive monthly declines. Data from the Office for National Statistics (ONS) showed that Retail Sales, a key gauge of consumer spending, increased by 0.4% month-over-month, defying expectations for a 0.1% contraction.

On a year-on-year basis, consumer spending rose sharply by 2.5%, well above the consensus forecast of 1% and up from a revised 1.8% in November (previously reported at 0.6%).

The stronger-than-expected Retail Sales figures are likely to reduce market expectations for near-term interest rate cuts by the Bank of England (BoE).

Looking ahead, the UK economic calendar is relatively light next week, leaving broader market sentiment and expectations surrounding the BoE’s February policy decision as the primary drivers of Pound Sterling performance.

GBP/USD Technical Outlook

GBP/USD is trading around 1.3437 at the time of writing. The 20-day Exponential Moving Average is hovering near 1.3439, with price currently testing this dynamic resistance. A daily close above the moving average would strengthen near-term momentum. The Relative Strength Index (RSI) stands at 52, edging higher but still signaling broadly neutral momentum.

Using the move from the 1.3780 peak to the 1.3006 trough, the 50% Fibonacci retracement at 1.3393 continues to act as a hurdle on rebounds, while the 61.8% retracement at 1.3485 limits upside potential. A decisive break above the latter would suggest the broader bearish bias is losing strength and could pave the way for a deeper recovery, whereas rejection at that level would likely keep the pair confined to a range.

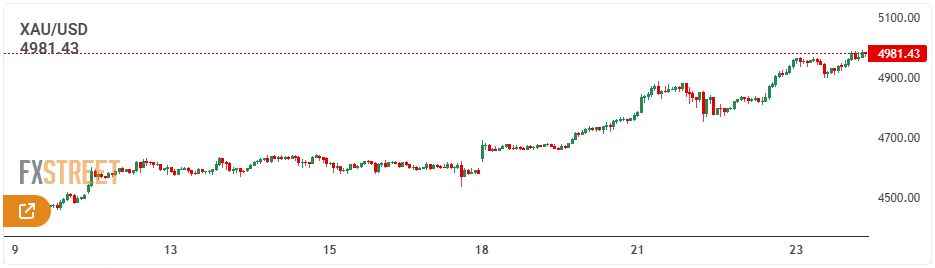

Gold prices remain firmly in an uptrend and are poised to test the key $5,000 per troy ounce level on Friday. The precious metal’s strong rally accelerates amid mounting US Dollar weakness and mixed US Treasury yields across the curve.

Fundamental Analysis Overview

Expectations of additional monetary easing by the US Federal Reserve (Fed) continue to support demand for the non-yielding yellow metal, even as geopolitical risks have eased following US President Donald Trump’s reversal on Greenland. The bullish momentum also appears largely undeterred by extremely overbought short-term technical conditions, reinforcing the view that Gold’s path of least resistance remains upward.

On Wednesday, Trump announced the cancellation of planned tariffs on European allies related to US control over Greenland, after reaching a preliminary framework with NATO leaders on future Arctic security cooperation. He also dismissed the possibility of taking Greenland by force, encouraging risk appetite. However, the positive market response proved short-lived, as dovish Fed expectations dominated, outweighing Thursday’s US economic data and pushing the US Dollar (USD) back toward its lowest level since January 6, last seen earlier this week.

Data from the US Bureau of Economic Analysis showed that final third-quarter GDP growth came in at 4.4%, marginally above the previous estimate of 4.3% and notably stronger than the 3.8% expansion recorded in the prior quarter. Meanwhile, the Core Personal Consumption Expenditures (PCE) Price Index — the Fed’s preferred inflation measure — rose 2.8% year-on-year in November, up from 2.7%, while the monthly increase remained steady at 0.2%.

Further weighing on the USD, the US Department of Labor reported that initial jobless claims edged up by 1,000 to 200,000 for the week ending January 17, below market expectations of 212,000. Despite the better-than-expected figure, the data failed to offer meaningful support to the greenback amid the broader de-dollarization trend. Investors now turn their attention to upcoming flash PMI releases for insight into global economic conditions, which could influence risk sentiment and shape Gold’s trajectory as it heads toward solid weekly gains.

XAU/USD Technical Analysis

The broader uptrend remains supported by an ascending channel originating from $3,805.69, with XAU/USD now having decisively broken above the channel’s upper boundary around $4,742.80. The Moving Average Convergence Divergence (MACD) remains firmly above the zero line and continues to trend higher, indicating strengthening bullish momentum. Meanwhile, the Relative Strength Index (RSI) stands at 81.25, deep in overbought territory, which may limit immediate upside as momentum becomes stretched.

That said, a sustained hold above the former channel ceiling opens the door for a continuation of the rally toward new highs. On the downside, initial support is seen near the ascending channel’s lower boundary at $4,437.79 should prices consolidate. A flattening MACD would point to fading upside momentum at elevated levels, while a pullback in RSI toward the 70 mark would help ease overbought conditions and reinforce trend stability. A failure to defend the breakout zone could trigger a move back into the previous range, whereas continued momentum would keep bullish control intact.

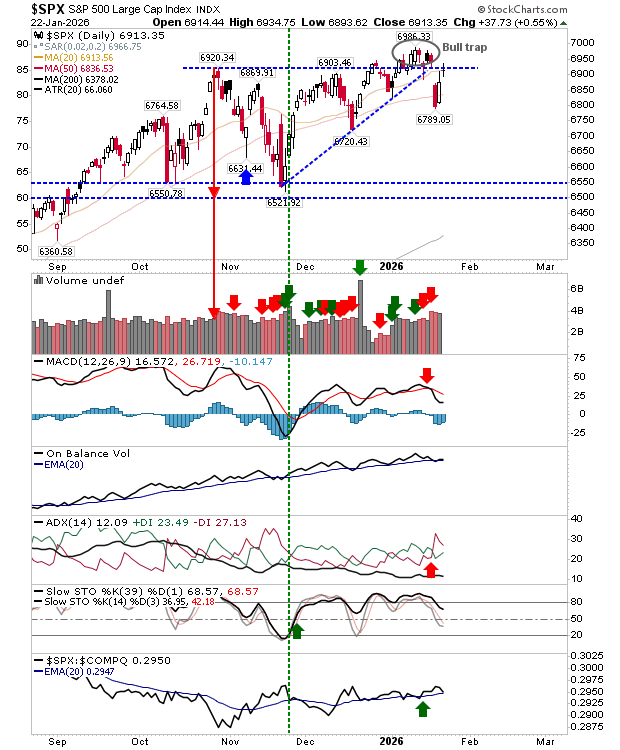

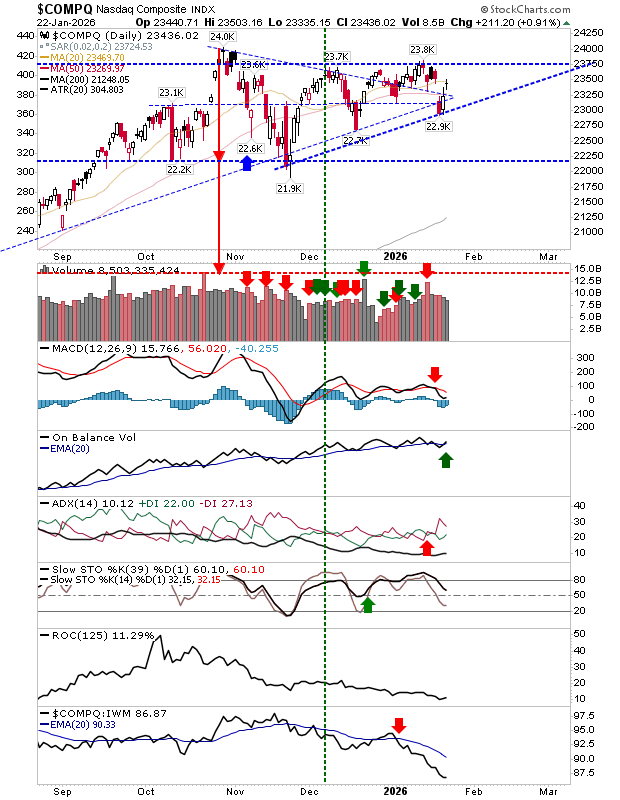

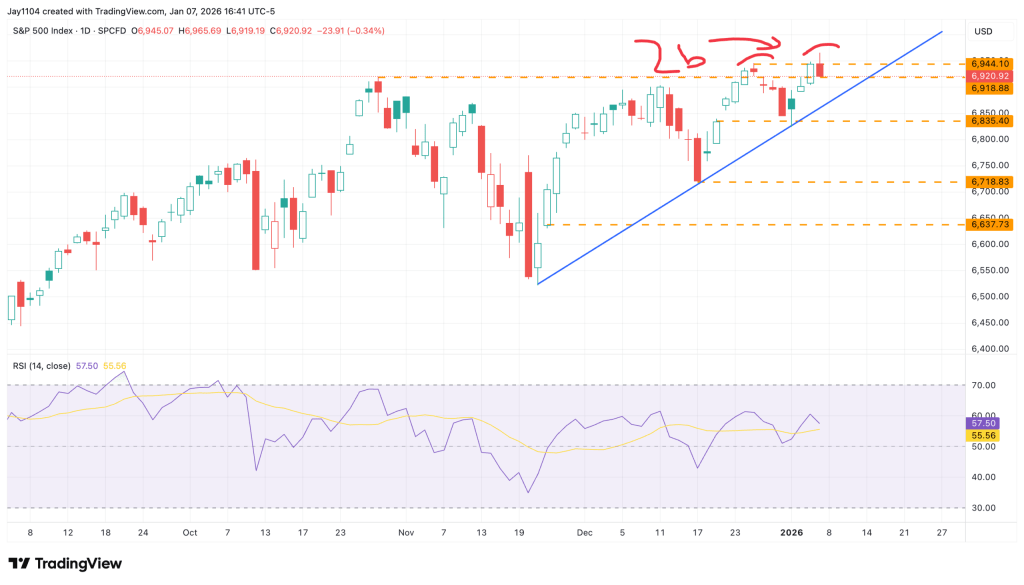

Markets managed to rebound after Tuesday’s sell-off, but the bounce—despite attracting attention—fell short of fully recouping the earlier losses. More importantly, a significant “bull trap” remains in place for the S&P 500. Technical signals for the index continue to be mixed, with momentum indicators such as stochastics failing to move back into overbought territory—a key condition needed to support a sustained rally.

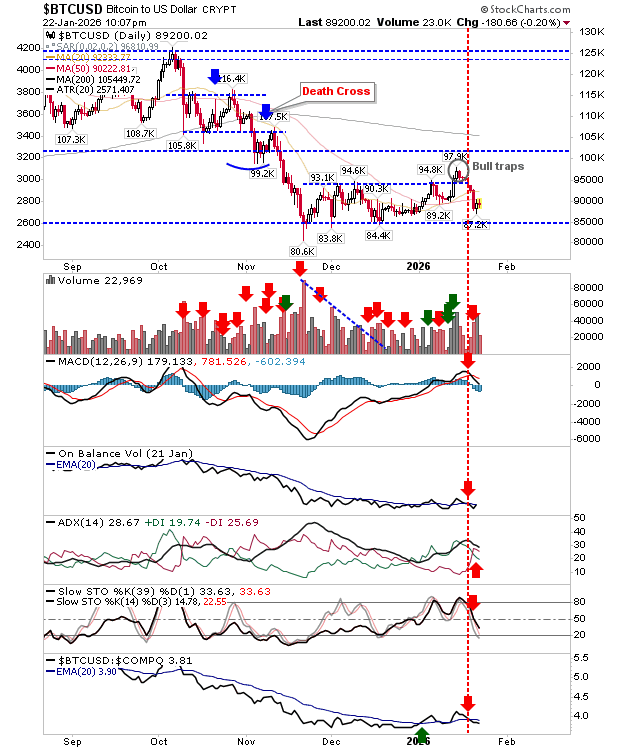

Bitcoin faces more significant challenges. Yesterday’s rise alone is far from sufficient to undo what was beginning to resemble the formation of a right-hand base. That said, this still appears to be the early stages of building a new base and could represent an attractive buying opportunity for investors willing to hold through what may be a year-long process, potentially targeting a move toward $125K. For now, technical indicators remain net bearish, and a break below $85K would invalidate any bullish outlook.

The Nasdaq has mounted a counter-trend bounce following the breakdown, but the symmetrical triangle pattern has already resolved, meaning attention now shifts to identifying new support and resistance levels. There is still a potential bullish scenario if price action evolves into a bullish ascending triangle.

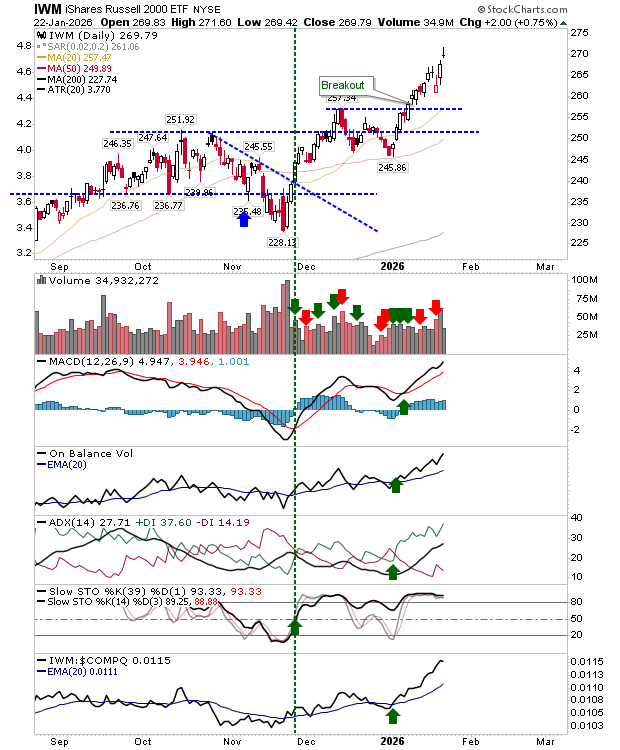

On the other hand, the Russell 2000 shows the potential to form a bearish “evening star” pattern, though this would require a gap lower today. Setting that possibility aside, the index remains firmly in rally mode and is far from any “bull trap” conditions. Overall, technical indicators are net bullish.

For today, bulls may want to focus on Bitcoin, while bears should monitor the Russell 2000 for signs that a bearish “evening star” pattern could emerge.

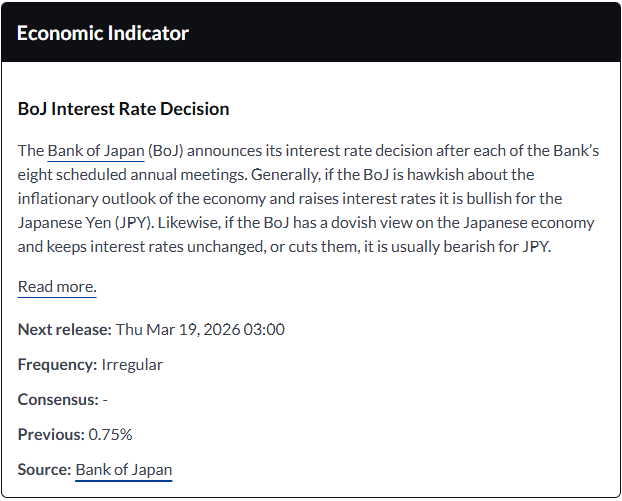

Bank of Japan (BoJ) Governor Kazuo Ueda is speaking at a press conference, outlining the rationale for keeping the benchmark interest rate unchanged at 0.75% at the January policy meeting.

Key takeaways from the BoJ press conference

Japan’s economy is showing a moderate recovery and is expected to continue growing at a steady pace.

The government’s economic stimulus package has improved the overall outlook.

Underlying inflation is projected to rise gradually and move closer to the 2% target.

Board members Takata and Tamura suggested revisions to the outlook report.

The BoJ will continue to raise interest rates if economic and price projections are realized.

Lending rates tied to the BoJ’s policy rate are already trending higher.

Financial conditions remain accommodative despite the December rate hike.

Foreign exchange movements are influenced by multiple factors.

The governor refrained from commenting on specific yen levels but emphasized close monitoring of FX developments.

Government bond yields are increasing at a rapid pace.

The BoJ stands ready to conduct bond-buying operations flexibly in exceptional circumstances.

Measures may be taken to support stable yield formation when necessary.

Currency movements, particularly the yen, may be having a stronger impact on prices.

Greater attention will be paid to foreign exchange trends going forward.

The rise in long-term yields is partly influenced by end-of-fiscal-year factors.

Price developments in April will be an important consideration when assessing the timing of future rate hikes.

The section below was published at 3:35 GMT on January 23 to cover the Bank of Japan’s monetary policy announcement and the initial market reaction.

The Bank of Japan (BoJ) board voted to keep the short-term policy rate unchanged at 0.75% at the conclusion of its two-day monetary policy meeting on Friday, a move that was widely expected.

As a result, borrowing costs remain at their highest level in roughly three decades.

Key takeaways from the BoJ’s policy statement

Japan’s economy is expected to continue a moderate recovery.

Consumer inflation is likely to pick up gradually.

The virtuous cycle in which wage growth and inflation reinforce each other is expected to be sustained.

The output gap is projected to improve over time and expand at a moderate pace.

Medium- to long-term inflation expectations are seen rising gradually.

No major imbalances are observed in Japan’s financial activity.

The overall financial system remains stable.

Firms’ moves to pass higher wages on to selling prices could strengthen more than previously anticipated.

The recent increase in food prices, including rice, mainly reflects temporary supply-side factors.

Significant uncertainty surrounds the global economic outlook, particularly due to trade policies that could push up import prices through supply-side channels.

Trade measures announced so far may weigh on global economic growth.

Regarding the US economy, close attention is needed on how tariffs could affect employment and income via weaker corporate profits.

High uncertainty persists around China’s economic outlook, especially the future pace of growth.

A sharp rise in import prices could further reinforce households’ cautious stance on spending.

Current trade policies could lead to a shift in the long-term trend of globalisation.

The Board raised its median real GDP growth forecast for fiscal 2025 to +0.9% from +0.7% in October.

The fiscal 2026 median growth forecast was revised up to +1.0% from +0.7%.

The fiscal 2027 median growth forecast was lowered to +0.8% from +1.0%.

BoJ’s Quarterly Outlook Report: Key Highlights

The Board kept its median core consumer price index forecast for fiscal 2025 unchanged at +2.7%, the same as in October.

The median real GDP growth forecast for fiscal 2025 was revised up to +0.9% from +0.7% in October.

Real interest rates remain at significantly low levels.

Risks to the economic outlook are assessed as roughly balanced.

The impact of foreign exchange volatility on prices has become more pronounced than in the past, as firms are more willing to raise prices and wages.

Core consumer inflation is expected to slow to below 2% during the first half of this year.

Companies’ efforts to pass higher wages on to selling prices could strengthen more than anticipated.

Japan’s economy is projected to continue a moderate recovery.

Market reaction following the BoJ policy announcements

USD/JPY climbed further toward 158.60 in an immediate reaction to the Bank of Japan’s (BoJ) decision to keep interest rates unchanged, rising 0.11% on the day.

The section below was published at 23:00 GMT on January 22 as a preview of the Bank of Japan’s interest rate decision.

The Bank of Japan is widely expected to leave interest rates unchanged at 0.75% on Friday.

The central bank is likely to wait and assess the effects of December’s rate hike before considering further tightening.

February’s general elections introduce an additional layer of uncertainty to the BoJ’s monetary policy outlook.

The Bank of Japan (BoJ) is widely expected to keep its benchmark interest rate unchanged at 0.75% following the conclusion of its two-day monetary policy meeting next Friday.

The Japanese central bank raised interest rates to their highest level in three decades in December and is now likely to keep policy unchanged on Friday to better evaluate the economic impact of earlier hikes.

BoJ Governor Kazuo Ueda is expected to reaffirm the bank’s commitment to continued policy normalisation. As a result, investors will closely scrutinise his press conference for clues on the timing and extent of the next phase of the tightening cycle.

What to anticipate from the Bank of Japan’s interest rate decision?

The Bank of Japan is broadly expected to leave interest rates unchanged in January while signaling the possibility of further tightening if economic conditions unfold as projected.

In December, the BoJ raised rates by 25 basis points to 0.75%, and the meeting minutes showed that some policymakers favor additional tightening, noting that real interest rates remain sharply negative once inflation is taken into account.

Markets, however, have ruled out consecutive rate hikes, especially following Prime Minister Sanae Takaichi’s surprise call for snap elections and her proposal to suspend food and beverage taxes for two years to ease the burden on households amid rising inflation.

While the implications of these political developments for monetary policy remain uncertain, the BoJ has emphasized a cautious, gradual normalization of policy, aiming to withdraw stimulus without undermining economic growth. As a result, the central bank is likely to wait for greater political clarity and for the effects of past rate increases to become clearer before moving again.

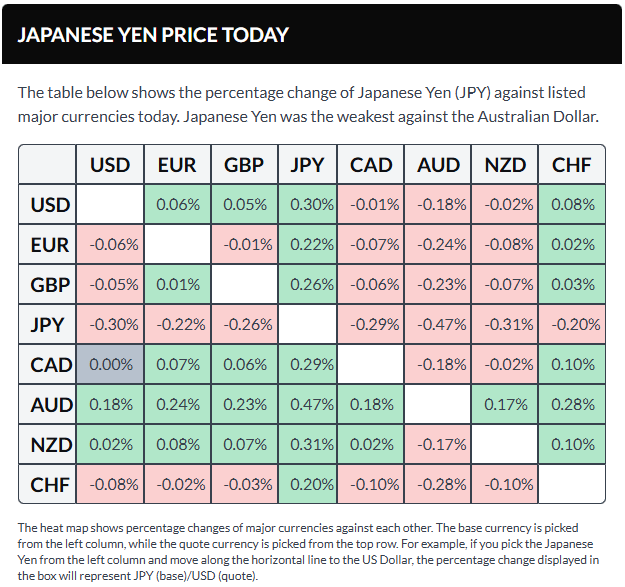

Meanwhile, the yen has weakened steadily amid speculation surrounding the snap election. This raises the question of whether the currency’s depreciation will push the BoJ to adopt a firmer stance on monetary tightening.

How might the Bank of Japan’s monetary policy decision influence the USD/JPY exchange rate?

Markets have fully priced in a Bank of Japan rate pause on Friday, but the central bank will need to clearly signal further monetary tightening to curb the Yen’s ongoing weakness.

Yen sellers have eased off in recent days, helped by broad US Dollar softness linked to the EU–US trade dispute following President Donald Trump’s threats over Greenland. Even so, USD/JPY is still up roughly 0.7% year to date and remains close to last week’s 18-month peak around 159.50.

Investors are also concerned that Prime Minister Takaichi could secure stronger parliamentary backing after the elections, allowing her to push ahead with expansionary fiscal policies such as higher spending and tax cuts. This has heightened worries about Japan’s already stretched public finances, driving the Yen lower and pushing long-term government bond yields to record highs amid fears of a potential fiscal crisis.

Meanwhile, recent remarks from BoJ Governor Ueda have reinforced the bank’s cautious tightening stance, suggesting Japan is transitioning toward a more sustainable inflation environment where wages and prices rise together. For the Yen’s recent, still-fragile rebound to continue, markets will need clearer evidence that interest rate hikes are on the horizon.

USD/JPY 4-Hour Chart

From a technical standpoint, FXStreet analyst Guillermo Alcalá views USD/JPY as undergoing a bearish correction, with an important support zone just above 157.40. He notes that while the pair has pulled back from recent highs, Yen buyers would need to push it below the 157.40–157.60 support area to invalidate the short-term bullish structure and open the door to a move toward the early-January lows near 156.20.

A cautious or non-committal message from the BoJ would likely disappoint markets and weaken the Yen. In that scenario, Alcalá expects USD/JPY to climb to new long-term highs. He points out that technical signals are improving, with the 4-hour RSI rebounding from the 50 level, indicating strengthening bullish momentum. At the time of writing, the pair is challenging resistance around 158.70 (the January 16 high), which stands as the final hurdle before the 18-month peak close to 159.50.

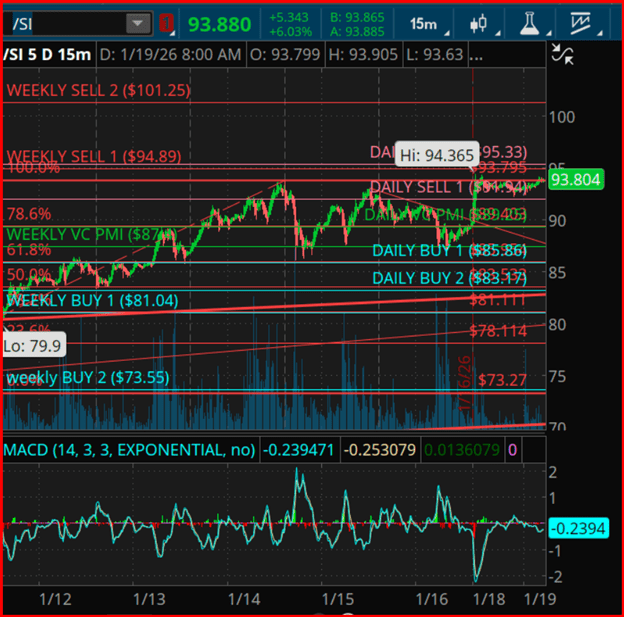

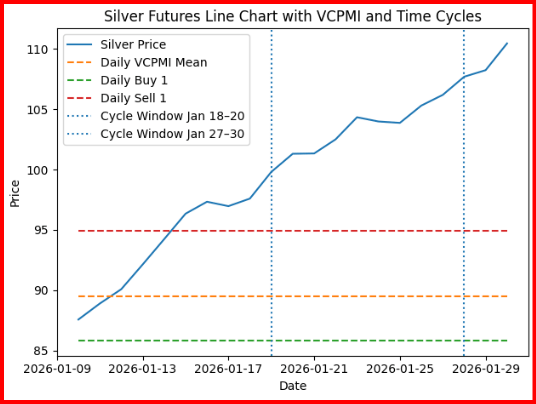

Silver remains in a high-momentum price-discovery phase, holding above the Daily VCPMI mean in the upper $89–$90 area, signaling sustained bullish momentum across both short- and intermediate-term timeframes.

The current structure points to strong participation on corrective pullbacks, increasing the likelihood that dips remain brief as buyers continue to defend the Daily Buy 1 and Weekly VCPMI support zones between $85 and $87.

From a time-cycle standpoint, the dominant 30-, 60-, and 90-day harmonic cycles remain in alignment with the broader expansion phase that began in early Q4. The market is now entering a near-term inflection window projected for January 18–20, a period that historically aligns with volatility compression and subsequent directional resolution. Should price sustain closes above the Daily Sell 1 level, the probability outlook shifts toward trend continuation, with upside targets extending to the Weekly Sell 1 and Weekly Sell 2 zones.

Square of 9 price geometry identifies $93.75, $94.80, and $95.40 as key harmonic resistance levels—rotational nodes where trend acceleration or rejection is most likely to occur. A sustained acceptance above this zone would open the technical pathway toward the $98–$101 range, aligning with the upper Weekly Sell 2 projection and longer-term cycle expansion targets.

Conversely, failure to rotate higher through this resistance band would favor a mean-reversion move back toward the Daily VCPMI mean and the Weekly Buy 1 support zone near $81–$83.

From a structural perspective, silver’s resilience amid elevated volatility and margin pressure continues to validate a supported trend environment, with accumulation behavior dominating corrective phases. Rising open interest and consistent closes above the Weekly VCPMI further support the view that the broader market remains positioned for higher price discovery rather than distribution.

Looking ahead, the secondary momentum window from January 27–30 marks the next key timing convergence, where the interplay between Square of 9 resistance and cyclical factors could drive either a decisive breakout or a rotational pullback.

Traders applying the VC PMI framework should maintain discipline, executing systematically at predefined probability levels while separating emotional bias from structured risk and money management.

Pi Network rebounded about 1% on Tuesday from a key support level after falling roughly 4% on Monday.

Data from PiScan showed more than 4 million PI tokens were withdrawn over the past 24 hours, signaling retail efforts to hedge against further downside.

From a technical perspective, PI remains under heavy selling pressure, with momentum turning bearish and leaving the token vulnerable to additional losses.