- The U.S. dollar weakened on Monday as investors assessed the implications of the Supreme Court of the United States decision to strike down tariffs introduced by Donald Trump, along with the administration’s subsequent response.

- Traders were also monitoring renewed nuclear negotiations between Washington and Tehran.

- As of 14:12 ET (19:12 GMT), the Dollar Index — which measures the greenback against a basket of six major currencies — was down 0.2% at 97.65. The currency had posted a gain of roughly 1% last week, marking its strongest weekly advance in more than four months.

Dollar pressured by mounting trade uncertainty

The Supreme Court of the United States ruled on Friday that sweeping tariffs introduced by Donald Trump exceeded his authority. In response, Trump criticized the court and unveiled a blanket 15% levy on imports.

The new duties are set to remain in place for 150 days, but it remains unclear whether the U.S. government must reimburse importers for tariffs already collected, as the Court did not address that issue.

The uncertainty could trigger prolonged legal battles and further confusion as Trump explores alternative mechanisms to reinstate broad-based global tariffs on a more permanent footing.

Thierry Wizman, global FX and rates strategist at Macquarie, said the firm’s bearish U.S. dollar outlook for 2026 was based on the view that tariffs signal U.S. “disengagement” from the rules-based order underpinning free trade. He added that tariff conflicts themselves generate uncertainty centered on the United States — a negative for the dollar.

“In that sense, while the Supreme Court ruling may have strengthened institutional checks, it also heightens uncertainty, as Trump is likely to revive the tariff war through different — and more legally grounded — channels that have yet to be detailed. We see no reason to revise our broader expectation for a weaker USD in 2026,” Wizman said.

Beyond trade policy, investors are also watching a U.S. military buildup in the Middle East aimed at pressuring Iran to abandon its nuclear ambitions, with further talks between Washington and Tehran expected later this week.

Euro advances as confidence in Europe strengthens

In Europe, EUR/USD rose 0.2% to 1.1799, with the single currency drawing support from trade-driven weakness in the dollar.

Growing confidence in the region’s economic outlook also underpinned the euro, following data on Friday showing eurozone business activity expanded faster than expected this month, as manufacturing returned to growth for the first time since October.

Momentum was reinforced on Monday as Germany’s Ifo business climate index climbed to 88.6 from 87.6 the previous month, signaling improving sentiment in Europe’s largest economy.

Meanwhile, GBP/USD added 0.1% to 1.3497, with sterling firming ahead of key event risks this week — including testimony before the Treasury Committee by Andrew Bailey, governor of the Bank of England, and Thursday’s UK by-election in Gorton and Denton.

Yen edges higher

In Asia, USD/JPY fell 0.4% to 154.48, with the Japanese yen supported by its traditional safe-haven appeal as investors remained cautious about the economic impact of higher U.S. tariffs. Trading volumes were thinner due to a public holiday in Japan.

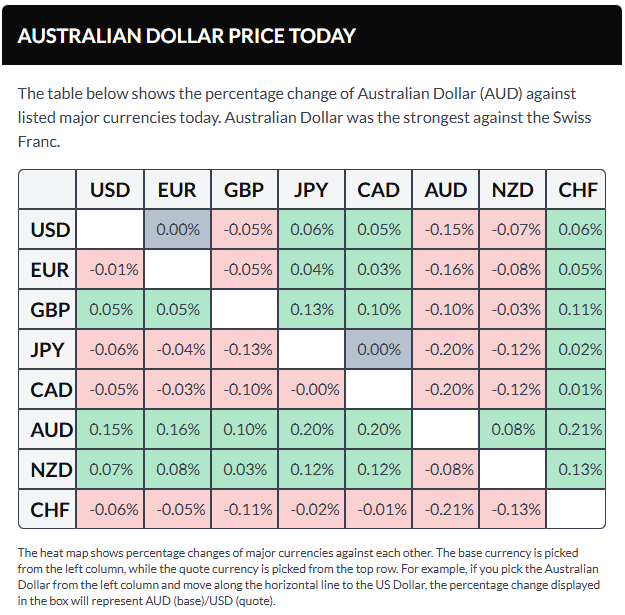

USD/CNY was little changed at 6.9087, with Chinese markets shut for New Year holidays. Elsewhere, AUD/USD declined 0.3% to 0.7060, while NZD/USD also dropped 0.3% to 0.5961.

Thierry Wizman of Macquarie said that while the dollar could remain under pressure amid persistent U.S.-driven uncertainty, some currencies — such as the yuan and the euro — may outperform, whereas others, including the Canadian and Mexican pesos, could lag. He added that even in the face of potential credit rating actions, long-term U.S. Treasury yields might rise due to uncertainty over revenue replacement, and equities could come under strain if higher yields lead to valuation compression.

Sources: Peter Nurse