The United Nations is considering a global tax framework that would tie oil and gas industry profits to climate compensation, though deep divisions among member states leave the outcome uncertain. Attempts to hold major energy producers financially accountable for climate change are not new. However, as the costs of the energy transition mount and legal efforts deliver mixed results, taxation is increasingly being viewed as an alternative policy instrument.

The United Nations is currently weighing the creation of a new international tax cooperation framework that could, among other objectives, channel funds from the oil and gas industry toward climate-related compensation. While the proposal reflects a familiar ambition to hold the industry financially accountable for climate change, its prospects remain uncertain.

The initiative falls under the Framework Convention on International Tax Cooperation, which is being negotiated at UN headquarters in New York. The broader goal is to strengthen global tax collection mechanisms and increase taxation on the world’s wealthiest entities and individuals. Sustainability features prominently in the discussions, with many countries—particularly those experiencing frequent climate-related disasters—supporting efforts to make major oil producers contribute financially. At the same time, resistance remains strong among other member states that oppose assigning climate liability to the energy sector or implementing a global wealth tax.

Recent proposals have suggested linking oil and gas profits directly to climate compensation payments. However, critics argue that these ideas lack sufficient clarity and enforcement power, limiting their viability. Supporters note that such measures could have generated as much as $1 trillion in additional revenue since the 2015 Paris Agreement, highlighting the scale of the opportunity lost if no agreement is reached.

Any move to formally tax Big Oil for its alleged role in man-made climate change would almost certainly provoke a strong response from the industry, likely through legal challenges. This would build on an already extensive record of climate-related litigation, where activist groups have achieved mixed results.

In the United States, California launched a lawsuit against major oil companies in 2024, accusing them of downplaying the climate risks associated with fossil fuels. The case targets companies including Exxon Mobil, Chevron, BP, and ConocoPhillips. State Attorney General Rob Bonta later strengthened the case by adding a provision aimed at forcing companies to surrender profits derived from alleged wrongful conduct. However, the lawsuit’s progress remains unclear, and California officials have recently softened their rhetoric toward oil companies in an effort to keep refineries operating and prevent fuel price spikes.

Maine has pursued a similar legal path, filing a “climate deception” lawsuit against several oil majors and the American Petroleum Institute. A federal judge allowed the case to proceed last year, with plaintiffs alleging that the defendants concealed information about the environmental and economic consequences of fossil fuel use.

This wave of so-called climate lawfare has become a favored strategy among activists seeking to penalize the fossil fuel industry. Yet given the uncertain outcomes of court cases, taxation is increasingly viewed as a more reliable alternative. The energy transition has proven far more expensive than initially anticipated, and governments are searching for sustainable funding sources.

Big Oil remains an obvious target due to its substantial profits from essential energy commodities that are widely blamed for climate change. Whether the UN negotiations ultimately result in a binding global tax remains to be seen. Even if they do, governments hoping for swift revenue may need patience—because the oil and gas industry is unlikely to accept such measures without a prolonged fight.

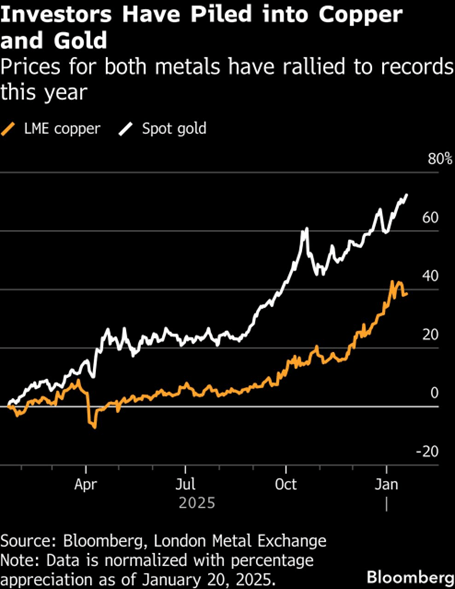

Over the past year, market focus has largely centered on gold and silver, with investors weighing safe-haven demand, central bank purchases, and inflation concerns. Meanwhile, copper has been quietly revaluing. So far this year, copper is up about 4%, following a roughly 40% surge in 2025. Analysts increasingly warn that copper demand could exceed supply within the next decade.

Introduction

When Thomas Edison brought electricity to cities in the late 1800s, copper was essential for carrying power from generating stations to homes, factories, and public lighting. Over time, it has become a cornerstone of modern economies, deeply integrated into energy networks, industrial activity, transportation, and communications. Today, its role is more critical than ever.

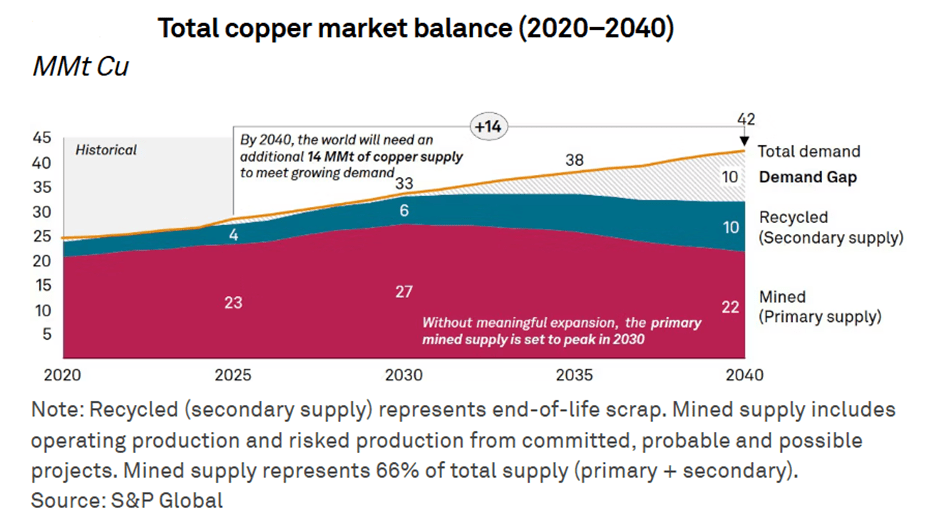

Copper now underpins electrification, AI infrastructure, electric vehicles, and defence systems. Yet the pace and scale of this shift are pushing the limits of global supply. According to S&P Global, without substantial new investment, the world could face a copper deficit of roughly 10 million metric tons by 2040.

Copper’s record-high prices point to a fundamental shift in demand dynamics.

At the start of the year, copper prices reached new record highs on the London Metal Exchange (LME), climbing to $13,407 per metric ton. So far this year, copper is up about 3%, building on a strong rally of roughly 40% in 2025.

Historically, copper has behaved as a cyclical commodity, moving in step with global economic growth, especially construction and manufacturing. In past upswings, prices typically weakened once growth cooled or inventories were replenished. This time, though, the forces supporting demand look wider in scope and more enduring.

A growing proportion of copper use is now tied to long-term electrification trends that are far less sensitive to short-term economic cycles.

From the demand side, copper is indispensable as an electrical conductor. It allows efficient power transmission, resists corrosion, has inherent antimicrobial properties, and can be recycled repeatedly without losing performance. Viable substitutes are scarce. Aluminium is often mentioned as an alternative, but with only about 60% of copper’s conductivity, it requires thicker cables to deliver the same current and typically needs extra insulation because it dissipates heat less effectively.

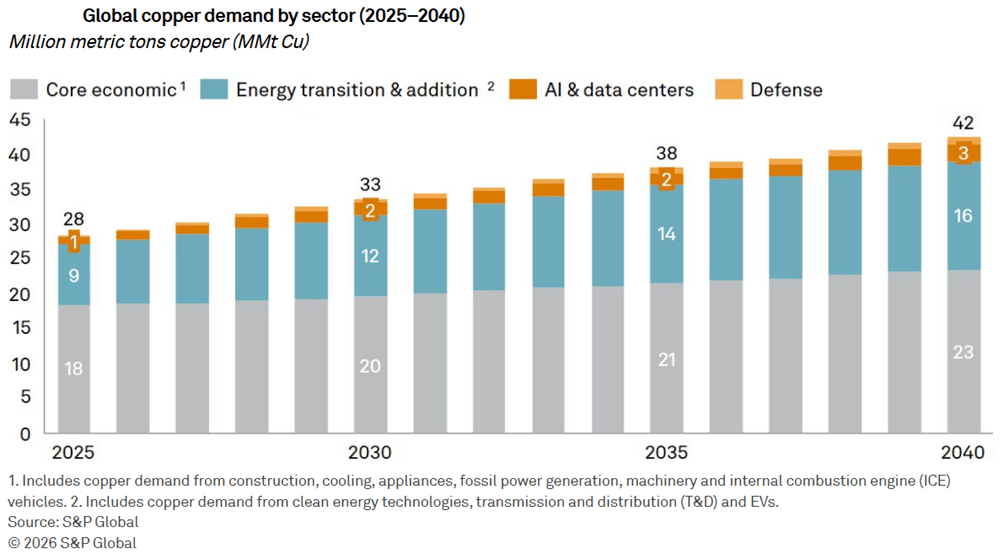

S&P Global projects that global copper demand will rise by roughly 50% by 2040, increasing from about 28 million metric tons today to around 42 million. This expansion is being driven by four key forces: baseline economic demand, the energy transition and new capacity build-out, AI and data centres, and defence modernisation.

While traditional economic uses and energy-transition applications are expected to remain the dominant sources of growth, Asia is likely to account for around 60% of the additional demand.

Around three-quarters of global copper demand comes from electrical uses, including power generation, transmission and distribution, electronics, and electrical equipment. Construction remains the largest single end-market, with copper heavily used in building wiring, plumbing, heating and cooling systems, and renovation projects. This provides a relatively stable foundation for demand, even when economic growth slows.

The energy transition adds another powerful layer of demand. As transport and power systems become increasingly electrified, copper usage is rising across the economy. Electric vehicles are a key driver of this shift, as they contain nearly three times as much copper as internal combustion engine vehicles—about 2.9 times more—reflecting the added requirements for wiring, batteries, power electronics, and electric motors.

More recently, AI and data centres have become a rapidly expanding source of copper demand. S&P Global estimates that copper consumption from data centres could increase from about 1.1 million metric tons in 2025 to roughly 2.5 million metric tons by 2040. Much of this growth reflects the copper needed for internal power distribution, cooling infrastructure, and the grid connections that supply these facilities. By the end of the decade, AI training data centres alone are expected to represent more than half of total data-centre-related copper demand.

Beyond these established drivers, emerging technologies may provide additional upside. Humanoid robotics is still in its early stages, but it is relatively copper-intensive. A single humanoid robot typically contains between 4 and 8 kilograms of copper, used across motors, actuators, wiring, sensors, batteries, and semiconductors. Even modest adoption scenarios could therefore have a meaningful impact on demand.

Defence is another area where copper consumption is set to rise. Heightened geopolitical tensions and the modernisation of military capabilities are leading to higher defence spending and quicker deployment of advanced technologies. Copper is extensively used in military equipment and infrastructure due to its conductivity, durability, and reliability in electrical systems, communications, and propulsion.

Given copper’s strategic role, much of this investment is relatively insensitive to price. At the 2025 NATO summit in The Hague, member states committed to lifting defence spending to 5% of GDP. As a result, annual copper demand from defence applications is expected to approach 1 million metric tons by 2040—around three times current levels.

A Constrained and Rigid Supply Landscape

While global demand continues to rise, supply is expected to stay tight as existing mining assets age. Without substantial additions to capacity, the market could face a shortfall of roughly 10 million metric tons by 2040.

Bridging this gap will be one of the major challenges of the coming decades, as the supply response is both complex and structurally limited. Substitution offers little relief, given copper’s unmatched conductivity, durability, and recyclability.

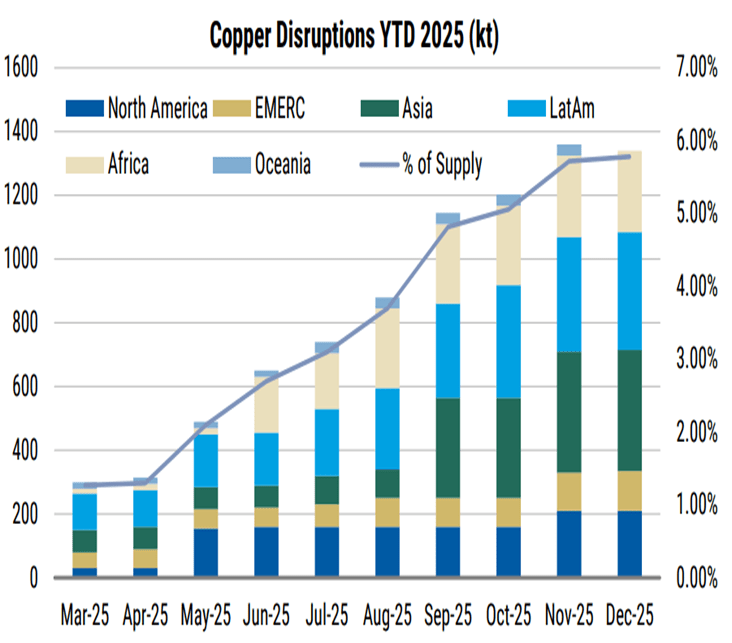

Over time, mine depletion has made copper extraction more technically difficult and more expensive, while producers are also contending with tighter regulation and rising environmental and social opposition from local communities.

These vulnerabilities have already led to repeated supply disruptions. Freeport-McMoRan has declared force majeure at its Grasberg mine—the world’s second-largest copper operation, accounting for roughly 4% of global output—with a full recovery not expected until 2027. Disruptions are also set to continue this month following strikes at Capstone Copper’s Mantoverde mine in Chile.

Source: Morgan Stanley

Bringing new copper projects online is a lengthy process, typically taking close to two decades—around 17 years—from initial discovery to first production, reflecting regulatory, environmental, political, and cost hurdles. Even so, today’s price levels do not provide strong enough incentives to develop major new deposits by 2040. Most high-quality, easily accessible resources have already been exhausted or are currently in production.

This underscores the importance of maximising output from existing mines, improving operational efficiency, and simplifying permitting processes and incentive structures for new developments. Future supply growth will increasingly rely on deeper exploration, which is both more expensive and technically challenging. Although several deposits have been identified that could theoretically help meet future demand, many are unlikely to be developed because they are not viable under current prices or with existing technologies.

Secondary supply from recycling offers an important supplementary source but cannot fully bridge the gap. Unlike many other metals, copper retains its key properties when recycled, making recycled material virtually indistinguishable from newly mined copper. As copper use expands across the economy, more scrap will become available as equipment and infrastructure reach the end of their life cycles.

End-of-life copper waste is expected to grow by about 4% annually, surpassing 15 million metric tons by 2040. S&P Global estimates that if recycling rates increase from 50% in 2025 to 66% by 2040, recycled copper from end-of-life sources could add roughly 6 million metric tons to total supply.

The expansion of recycling hinges on more efficient collection and processing systems. While scrap supply is more flexible than mined output, policy support will be critical to scaling recycling globally. Regions such as the United States, the European Union, and China have already implemented measures to set recycling targets or invest in supporting infrastructure.

These initiatives are designed to boost secondary copper supply while lowering environmental impacts. Even with significant gains in processing efficiency, recycling is expected to account for at least one-third of total copper supply by 2040.

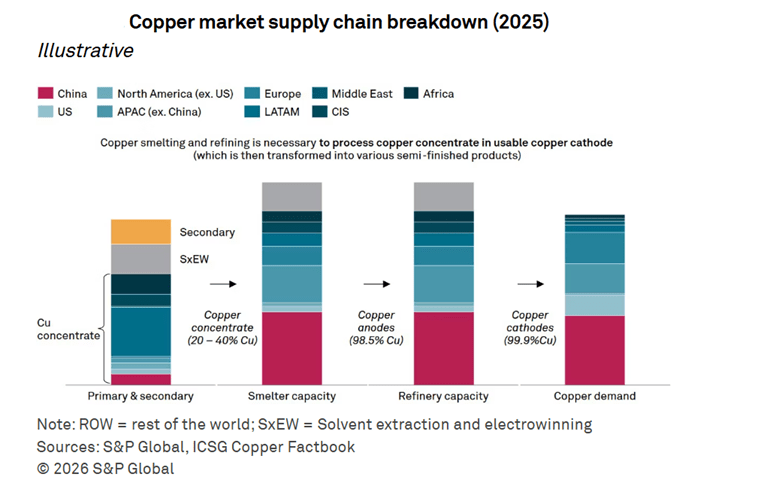

Meanwhile, smelting and refining are heavily concentrated in China, making them a strategic chokepoint in the global supply chain. China controls a large share of global smelting capacity—around 12 out of 29 million metric tons worldwide—and continues to expand this position, further increasing industry concentration.

Processing margins are coming under growing pressure as treatment and refining charges decline, while costs and regulatory burdens vary widely by region. At the same time, the high concentration of capacity—estimated at around 40–50% of the global total—adds to systemic fragility and increases exposure to geopolitical disruptions.

For these reasons, governments increasingly view mineral supply chains as strategically vital. New models of international cooperation, along with greater participation by sovereign wealth funds, are emerging as alternative ways to strengthen and diversify access to critical minerals and reduce reliance on China-centric supply chains.

Conclusion: A Global Race for Critical Metals

The global economy is entering a phase of exceptional expansion in renewable energy, electric vehicles, artificial intelligence, data centres, and defence, all of which are driving a sharp increase in copper demand—the cornerstone metal of electrification. New technologies, ranging from electrified military systems to advanced robotics, are likely to intensify this trend further. The pace of electrification is now running ahead of the growth in copper supply.

This race extends beyond geological availability to the downstream stages that determine mineral quality and value. China’s dominance in copper refining and magnet production represents a major vulnerability for global supply chains, prompting advanced economies such as the European Union to launch initiatives aimed at securing alternative sources and accelerating the development of domestic capabilities.