The Elliott Wave (EW) framework seeks to measure and interpret investor sentiment, which unfolds in recognizable wave patterns. These waves can span extremely short periods—such as minutes—or stretch across decades and even centuries. At its core, the pattern reflects a “three steps forward, two steps back” progression. Because this structure repeats across multiple timeframes, it is considered fractal in nature.

Given that markets are non-linear, stochastic, and probabilistic, Elliott Wave analysis does not predict certainties but instead identifies the most probable path forward—so long as key price levels remain intact. If those levels are breached—such as a downside break signaling a potential top—the outlook shifts, providing a clear framework for adjusting positions to protect profits or limit losses.

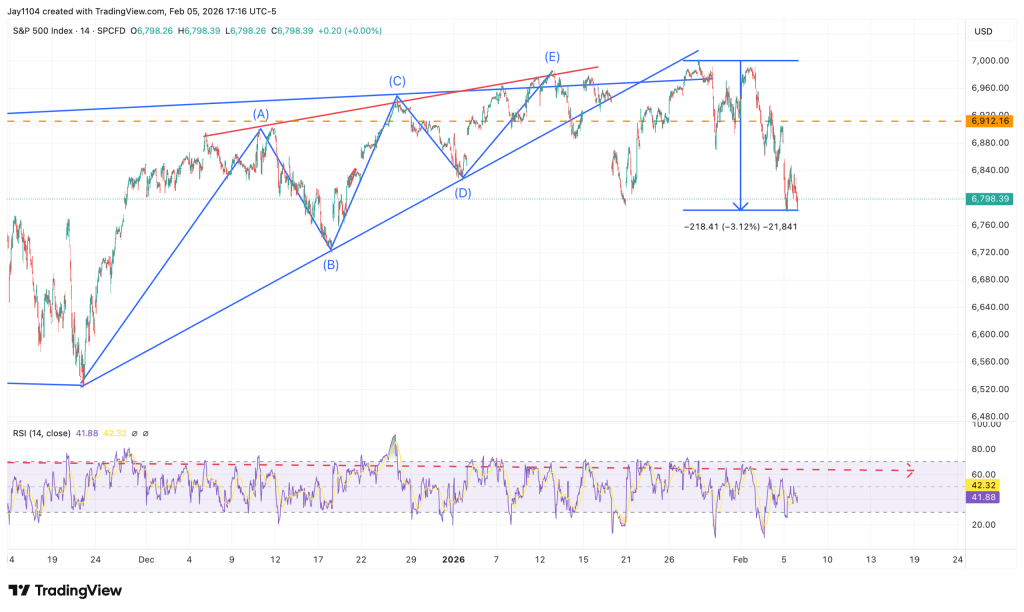

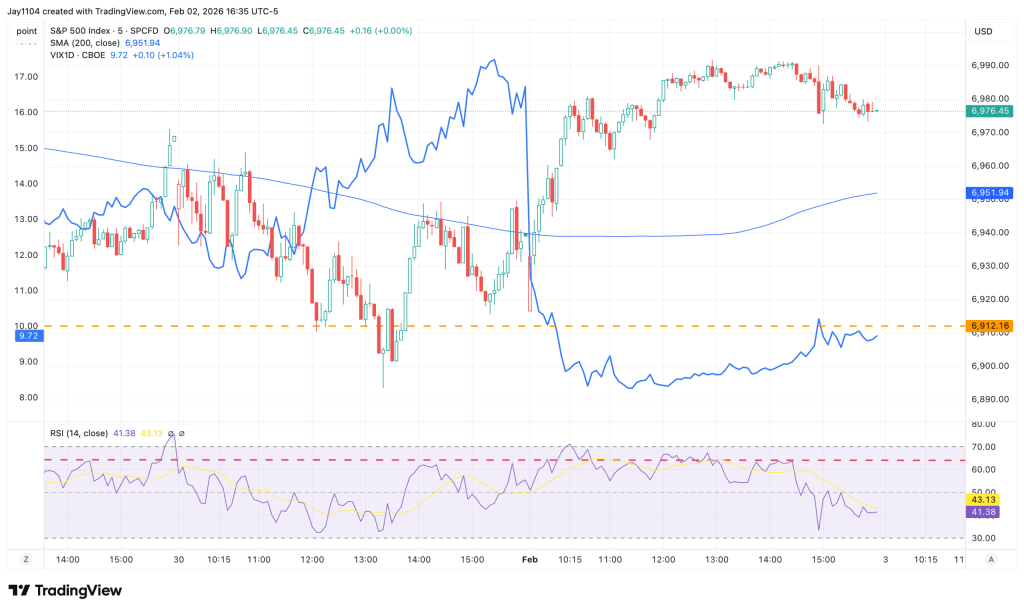

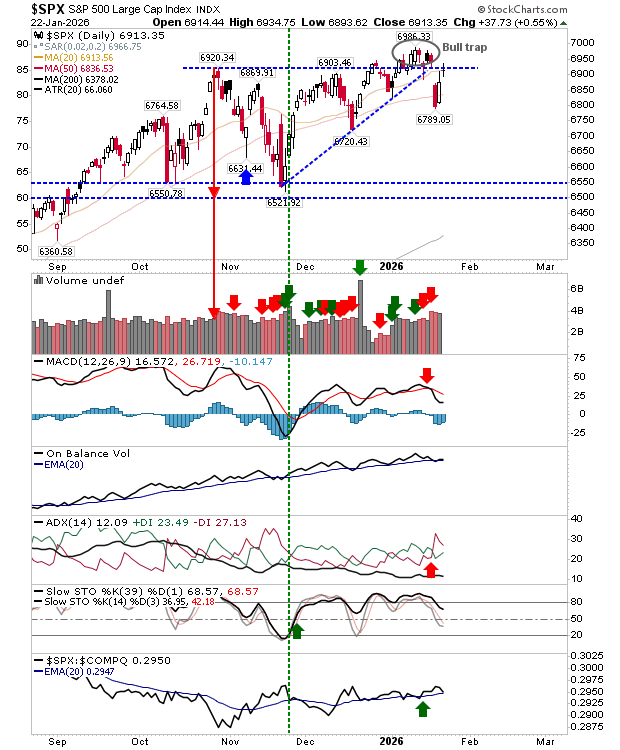

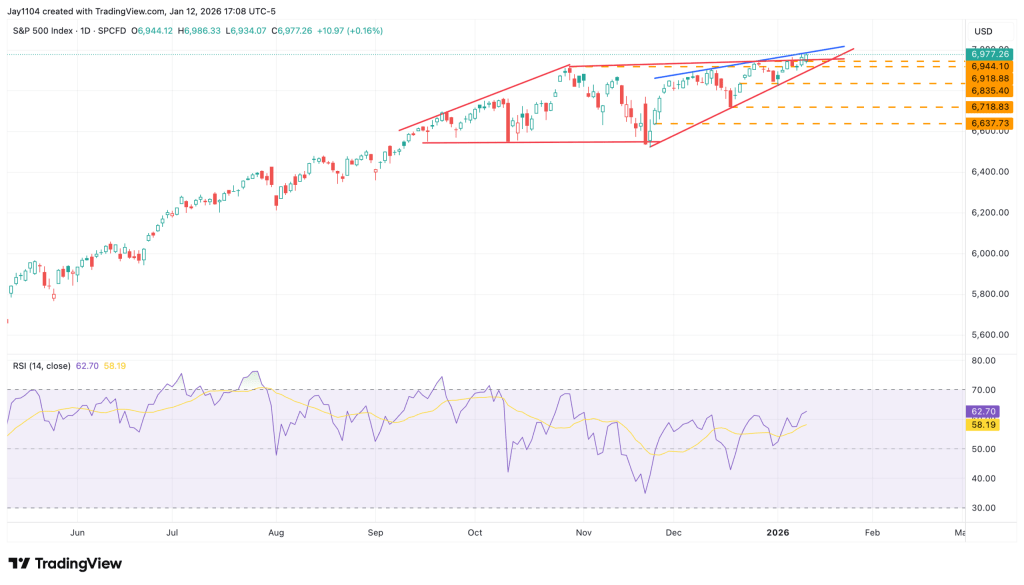

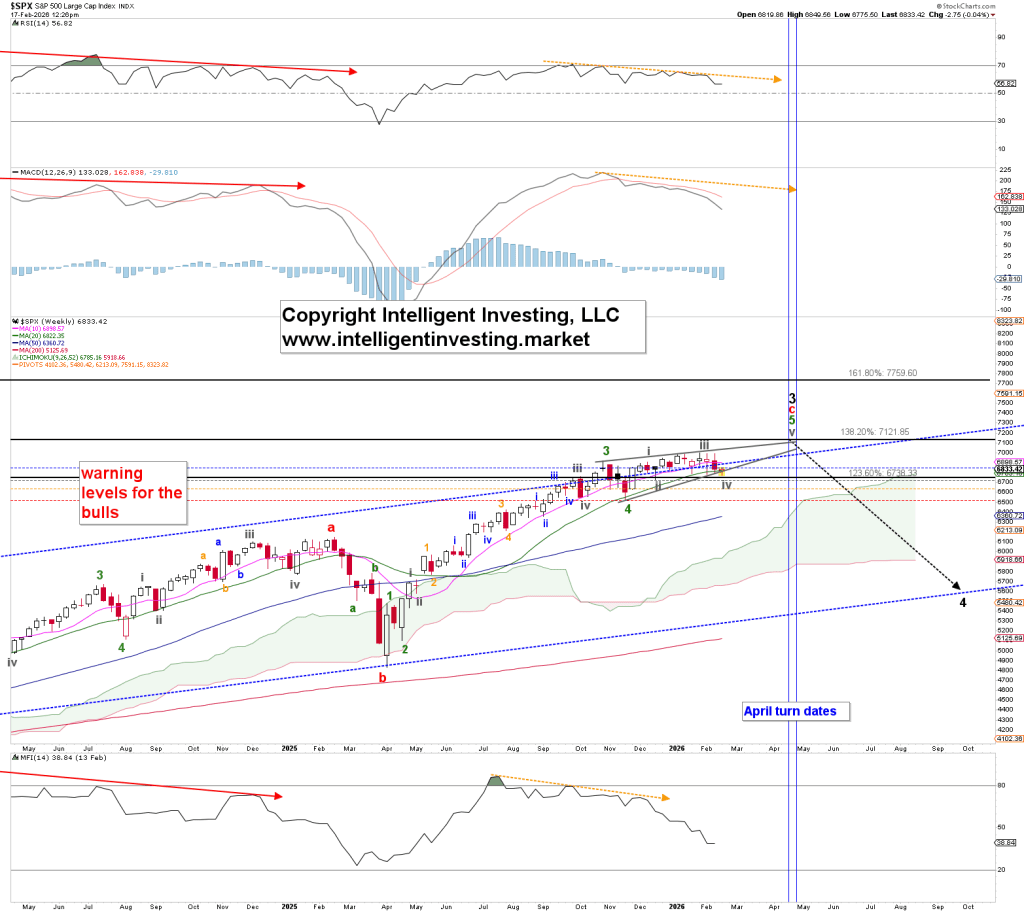

Turning to the S&P 500, we have been monitoring an advance labeled green Wave 5, forming what appears to be an overlapping ending diagonal (ED) since the November 2025 low (green Wave 4). As illustrated in Figure 1, we first identified this developing structure in mid-December and have been tracking its progression closely to assess how the pattern ultimately resolves.

Figure 1. Intermediate-term Elliott Wave count for the S&P 500 (SPX).

An ending diagonal is made up of five overlapping waves—here labeled gray Wave i through v. Importantly, each of those gray waves unfolds as its own three-wave structure. Three-wave patterns are notoriously difficult to forecast, and the current sideways action in the index reflects that overlapping, indecisive character. (See Figure 2.)

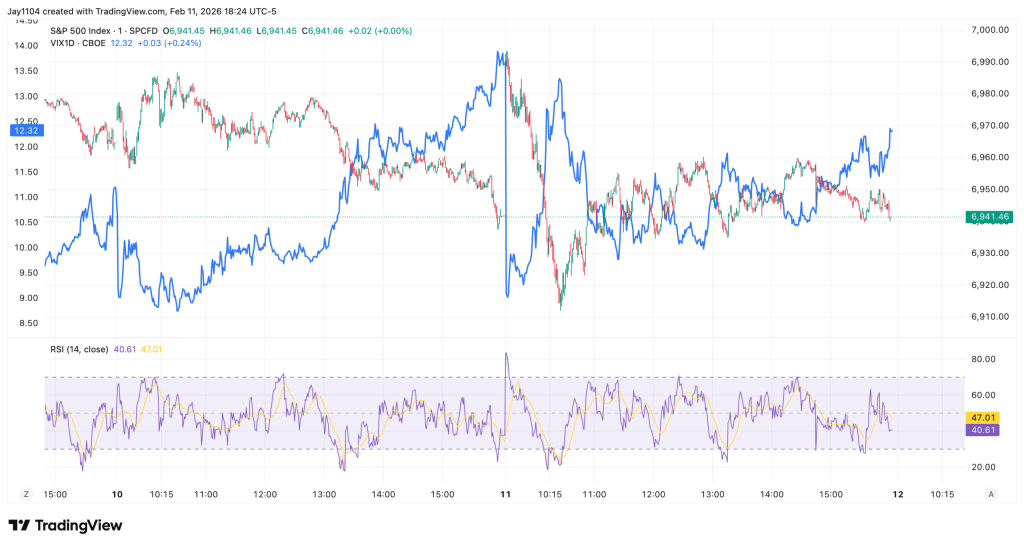

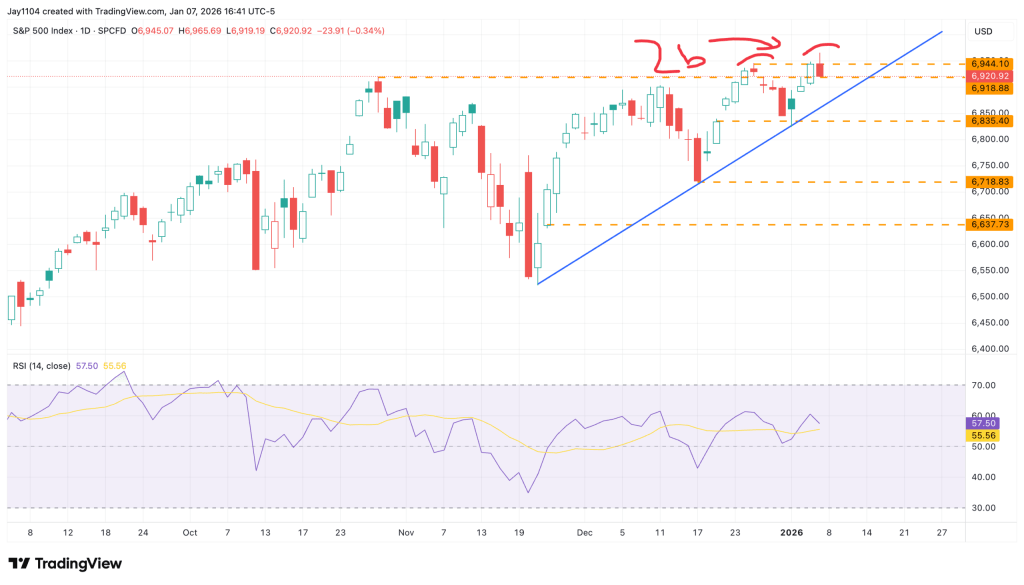

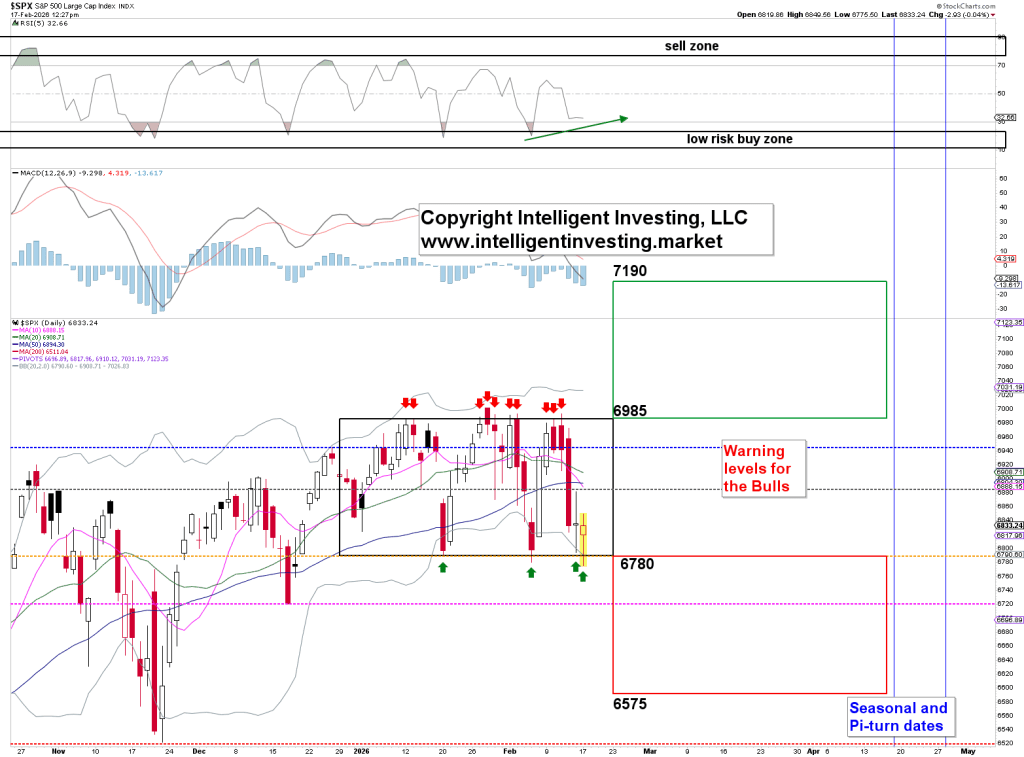

At present, the S&P 500 is trading near the same levels seen in late October. The 6,985 area has been tested ten times (red arrows), while support around 6,780 has held on four occasions (green arrows). This repeated interaction with resistance and support suggests a developing range.

Range-bound conditions tend to frustrate traders because the absence of a clear directional trend makes forecasting more challenging. From a symmetry standpoint, an upside breakout projects toward approximately 7,190 (6,985 + 6,985 − 6,780), highlighted by the green box. Conversely, a breakdown below support would imply a downside target near 6,575 (6,780 − 6,985 + 6,780), marked by the red box.

With today’s price action, the bulls appear to be on the brink. However, if the index manages to close higher, a positive divergence could form on the daily RSI(5) (green arrow), signaling that downside momentum may be fading and giving way to emerging upside strength.

Figure 2. The S&P 500 since October 2025 has largely traded within a defined range.

As noted earlier, Elliott Wave analysis outlines the most probable path forward—provided key price levels remain intact. Once those levels are breached, the outlook shifts, giving traders a clear signal to protect gains or limit losses.

In this case, the pivotal level is the November low at 6,521. A decisive break beneath that threshold would signal that the ending diagonal has completed and that a larger corrective phase—black Wave 4 in Figure 1—is underway, with a preferred target zone between 5,500 and 6,125, ideally toward the upper end of that range.

For now, the focus remains on 6,780. If the bulls can defend that level—our third warning threshold—we can still allow for a final gray Wave v advance toward roughly 7,120–7,190, potentially extending into the April turn window. However, a daily close below 6,780 raises the probability to about 60% that the broader uptrend has already topped.

Should support fail, attention quickly shifts to 6,575 as the next downside level to monitor.

Sources: Arnout ter Schure