The U.S. housing market is currently facing a pronounced imbalance between supply and demand. Housing starts have climbed to their highest level in a year, even as existing home inventory remains limited and home prices continue to face upward pressure.

At the same time, new inflationary risks are emerging. A 15% global tariff and rising energy costs tied to the conflict in Iran threaten to weaken consumer purchasing power and potentially disrupt expectations for a housing market recovery in 2026.

Ongoing inflation has also forced the Federal Reserve to maintain a defensive “higher for longer” interest-rate stance. Market expectations now suggest the first potential rate cut may not arrive until October 2026.

This week, the U.S. housing sector has been in focus as a wave of economic data coincides with an important earnings release from homebuilder Lennar. Investors are closely monitoring the interaction between limited housing supply, evolving inflation pressures, and geopolitical developments that could reshape the economic outlook for 2026.

The Inventory Challenge: Existing Home Sales and Construction Activity

The week began with a reminder of the housing market’s supply-demand imbalance. On Tuesday, the National Association of Realtors reported that existing home sales for February rose 1.7% from January to a seasonally adjusted annual rate of 4.09 million units. Although the monthly increase suggests some stabilization, sales remain down 1.4% compared with the same period last year.

NAR Chief Economist Lawrence Yun noted that while housing inventory is gradually increasing, supply growth remains slow. As the spring buying season approaches, a key concern is that if demand strengthens faster than inventory expands, home prices could climb further, worsening affordability challenges for first-time buyers.

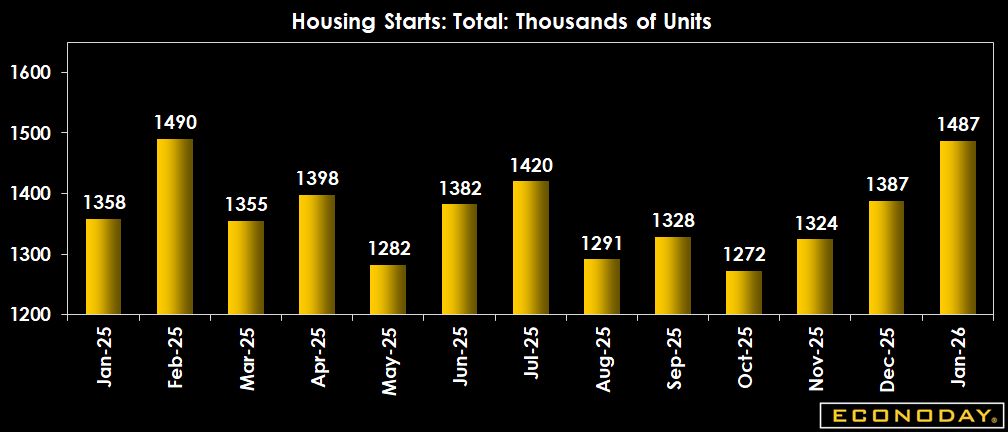

However, more encouraging news emerged today from the United States Census Bureau. The latest housing starts report showed that residential construction activity rose for the third straight month, reaching its fastest pace since February 2025. Housing starts increased 7.2% in January to an annualized rate of 1.49 million units.

The rise was largely driven by a sharp 29.1% increase in multifamily construction, while single-family building activity continued to lag. This development offers some support for homebuilders—particularly Lennar Corporation, which is scheduled to report earnings later today.

Despite the improvement in construction activity, sentiment across homebuilding stocks has remained cautious, as investors continue to worry about housing affordability and elevated construction costs.

Spotlight on Homebuilders: Lennar Earnings in Focus

With many homeowners locked into ultra-low mortgage rates from previous years, the responsibility for adding new housing supply has increasingly shifted to publicly traded homebuilders. Lennar is scheduled to report its Q1 2026 earnings later today, offering investors an important gauge of the industry’s current health.

Market participants will be paying close attention to several key issues:

Construction Outlook: Whether Lennar plans to accelerate new housing starts despite ongoing economic uncertainty.

Mortgage Rate Buy-Down Programs: The extent to which the company continues subsidizing buyer mortgage rates—an approach that has helped sustain sales activity but is beginning to weigh on profitability. Analysts expect gross margins to ease toward the 15–16% range this quarter.

Upcoming Homebuilder Earnings to Watch

- Lennar (LEN) – March 12, 2026

- KB Home (KBH) – March 24, 2026

- D.R. Horton (DHI) – April 21, 2026

- PulteGroup (PHM) – April 23, 2026

- Toll Brothers (TOL) – May 19, 2026

*Estimated based on historical reporting schedules.

The Inflation Shock: Tariffs and the Iran Conflict

The housing outlook is becoming more complex as the U.S. economy faces a sudden two-pronged inflation shock. Although February’s Consumer Price Index (CPI) showed a relatively moderate 2.4% year-over-year increase, that figure is now considered outdated because it was recorded before two major inflationary developments.

Global Tariffs: After a ruling by the Supreme Court of the United States, the administration introduced a 10% global tariff on February 24, which was quickly raised to 15% in early March. These tariffs are expected to increase the cost of imported construction materials. Perhaps more importantly, they could further strain household finances, making prospective buyers even more hesitant to enter the housing market.

Conflict in Iran: Shortly after the tariff announcement, military strikes by Israel and the United States targeted multiple locations across Iran, triggering sharp reactions in global energy markets. Oil prices surged in the aftermath, and the impact is already being felt by consumers. U.S. gasoline prices have climbed roughly 20% in under two weeks, pushing the national average to $3.58 per gallon.

Despite the International Energy Agency releasing 400 million barrels from strategic reserves, energy markets remain skeptical that this supply will be sufficient to offset potential disruptions from the Middle East if the conflict persists. Concerns intensified after reports that Iran intends to keep the Strait of Hormuz closed, a move that threatens a critical global oil transit route.

The Fed’s Dilemma: March FOMC Meeting

Later this week, the Bureau of Economic Analysis will publish the Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve’s preferred gauge of inflation. Under normal circumstances, this would be the most significant economic release of the week.

However, due to the 2025 government shutdown, the agency is still working through a backlog of delayed reports. As a result, Friday’s release will reflect January data, meaning it predates both the newly implemented tariffs and the outbreak of the Iran conflict.

Attention is also turning to the upcoming meeting of the Federal Open Market Committee scheduled for March 17–18. Earlier in the year, markets anticipated that the Federal Reserve might begin easing policy relatively soon. Now, however, expectations have shifted. According to the CME FedWatch Tool, policymakers are widely expected to hold interest rates steady, with current market pricing suggesting the first—and possibly only—rate cut of 2026 could arrive in October.

Consumer Impact: Windfalls vs. Headwinds

As the U.S. tax season progresses, many households are receiving larger tax refunds. Consumers often treat these refunds as a temporary financial windfall, typically using them to pay down credit card balances accumulated during the holiday season or to make major purchases such as vehicles or household appliances.

However, this extra liquidity is unlikely to trigger a surge in housing demand. Instead, it may simply help households cope with rising living costs. Higher gasoline prices, in particular, function like a stealth tax by reducing discretionary income. Rather than saving for a home down payment, many consumers may find themselves allocating more of their budgets toward essential expenses.

Recent data from the Internal Revenue Service shows that the average tax refund has increased by 10.6% compared with last year, based on figures from the first four weeks of the filing season.

The Bottom Line

The U.S. housing market currently finds itself caught between an urgent need for additional supply and an increasingly challenging macroeconomic backdrop. While major homebuilders such as Lennar represent the sector’s strongest source of new housing inventory, they are confronting a difficult environment marked by higher construction costs from tariffs and cautious consumers strained by persistent inflation.

At the same time, the Federal Reserve appears poised to maintain its “higher for longer” interest-rate policy as it works to contain renewed inflationary pressures. If that stance persists, borrowing costs are likely to remain elevated, limiting housing affordability and slowing demand.

As a result, the much-anticipated housing market recovery expected in 2026 could face delays, particularly if geopolitical tensions and trade disruptions continue to weigh on inflation and consumer confidence. Until those uncertainties begin to ease, the path toward a sustained housing rebound may remain uneven.

Sources: Christine Short