Oil prices declined for a second consecutive day on Wednesday as expectations grew that peace talks between the U.S. and Iran could resume, potentially restoring supply from the Middle East that has been disrupted by the closure of the Strait of Hormuz.

Brent crude slipped 0.55% to $94.27 per barrel after a sharp 4.6% drop in the previous session, while U.S. West Texas Intermediate fell 1.1% to $90.24 following an even steeper 7.9% decline earlier.

Investor sentiment improved after President Donald Trump suggested that negotiations to end the conflict involving the U.S., Israel, and Iran could restart in Pakistan within days. The earlier breakdown in talks had led Washington to impose a blockade on Iranian ports, but renewed diplomatic hopes are raising expectations that oil and fuel flows could eventually resume.

The conflict has effectively shut down the Strait of Hormuz, a crucial route for transporting crude and refined products from the Gulf to global markets, particularly in Asia and Europe. Although a ceasefire has been in place for two weeks, shipping activity remains severely limited, with vessel traffic far below pre-war levels.

On Tuesday, a U.S. warship reportedly prevented two oil tankers from departing Iran, underscoring ongoing disruptions. Analysts at the Schork Group noted that while diplomatic developments hint at easing restrictions, actual conditions on the ground remain unstable, leaving markets focused on the risk of supply disruptions rather than a full recovery.

Further tightening supply concerns, U.S. officials indicated that sanctions waivers on Iranian oil shipments will not be renewed, and a similar waiver for Russian oil has already expired.

Later in the day, attention will turn to U.S. inventory data from the Energy Information Administration. Expectations are for a modest increase in crude stockpiles, alongside declines in gasoline and distillate inventories. Meanwhile, preliminary data from the American Petroleum Institute suggested that crude inventories rose for a third straight week.

The U.S. dollar declined on Tuesday as investors moved away from the safe-haven currency and shifted toward riskier equities, supported by optimism over potential ceasefire progress between the U.S. and Iran, despite the ongoing naval blockade in the Persian Gulf.

Risk sentiment was further strengthened by a much weaker-than-expected U.S. producer inflation report, easing concerns that the Iran-related energy shock could fuel inflation—especially after a recent surge in consumer prices.

By 17:20 ET (21:20 GMT), the U.S. Dollar Index, which measures the greenback against six major currencies, had dropped 0.3% to 98.12.

The Hormuz blockade continued into its second day, even as Donald Trump signaled that potential negotiations could be on the horizon.

The blockade of the Strait of Hormuz entered its second day even as President Donald Trump highlighted the possibility of renewed negotiations.

The U.S. dollar, which had initially strengthened as a safe-haven asset following the outbreak of the Iran conflict in late February, has recently weakened amid growing optimism that tensions could ease.

This optimism increased on Tuesday after Trump told the New York Post that additional talks “could take place within the next two days” in Pakistan. According to earlier reports, the U.S. and Iran have remained in contact and made some progress toward a lasting ceasefire agreement.

Trump also stated that Iranian officials had reached out to the White House expressing interest in striking a deal, while reiterating that Iran would not be allowed to develop nuclear weapons. The U.S. is reportedly insisting that Iran halt uranium enrichment for 20 years, a key step in nuclear weapons development.

At the same time, the U.S. naval blockade of vessels entering and leaving Iranian ports continued into its second day. The U.S. Central Command said the operation involves over 10,000 personnel, more than a dozen warships, and dozens of aircraft to enforce the restrictions.

CENTCOM reported that within the first 24 hours, no ships managed to pass through the blockade, and six commercial vessels complied with U.S. directives to turn back toward ports in the Gulf of Oman.

British maritime authorities also confirmed that access has been limited for ships attempting to enter or exit Iranian ports, as well as in nearby waters including the Persian Gulf, Gulf of Oman, and parts of the Arabian Sea.

Trump noted that the blockade began on Monday after weekend ceasefire negotiations failed to produce immediate results. The move risks further disrupting already reduced oil flows through the Strait of Hormuz, a critical route that carries about one-fifth of the world’s oil supply.

U.S. producer inflation came in weaker than expected.

U.S. producer inflation came in less severe than expected, drawing significant market attention on Tuesday. The March producer price index (PPI) rose 0.5% month-on-month and 4.0% year-on-year, falling short of forecasts of 1.1% and 4.6%. Meanwhile, core PPI increased by 0.1% over the month and 3.8% compared to a year earlier.

Despite the softer-than-expected overall figures, the annual rise in headline PPI marked the largest increase since February 2023, largely driven by a sharp 8.5% monthly surge in energy prices for final demand.

Even so, the weaker headline data helped ease investor concerns.

Guy LeBas, chief fixed income strategist at Janney, noted on X that expectations had been elevated due to fears of rising energy input costs, which were not fully reflected in the data.

He added that although gas prices are clearly higher, these cost increases may take several months to filter through the economy rather than appearing all at once. This gradual pass-through could complicate monetary policy, as it may delay the Federal Reserve’s confidence that inflation pressures are not spreading beyond the energy sector.

The euro and British pound strengthened, while the yen also gained despite weak economic data.

Among major currencies, both the euro (EUR/USD) and the British pound (GBP/USD) moved higher, supported by the softer U.S. dollar. The euro rose 0.2% to $1.1795, while the pound gained 0.4% to $1.3567.

The Japanese yen also strengthened, with USD/JPY slipping 0.3% to 158.80, despite data showing Japan’s industrial production fell 2% month-on-month in February after a 4.3% increase in January.

In other markets, the Australian dollar (AUD/USD) increased 0.3% to $0.7122, even though economic indicators were weak. According to National Australia Bank, business confidence dropped sharply in March following the Iran conflict, while the Westpac–Melbourne Institute survey showed a steep decline in consumer sentiment in April.

U.S. President Donald Trump said Sunday evening that he was unconcerned about whether Iran would return to negotiations after ceasefire talks over the weekend failed to produce an agreement.

He also confirmed that the United States intends to impose a blockade on the Strait of Hormuz starting Monday morning, accusing Iran of failing to honor its commitment to reopen the vital shipping route. Speaking to reporters at Joint Base Andrews, Trump stated that the U.S. would be fine even if Iran chose not to resume talks.

His remarks followed a report indicating that several countries are attempting to restart diplomatic efforts after lengthy discussions in Islamabad ended without a deal. Despite the breakdown, sources suggested that further negotiations could take place within days, while regional governments are working with Washington to extend a fragile two-week ceasefire.

The Islamabad meeting represented the highest-level direct engagement between U.S. and Iranian officials since 1979, with 21 hours of talks concluding without progress. Vice President JD Vance said the U.S. had clearly outlined its conditions, but Iran declined to accept them.

U.S. demands reportedly included ending uranium enrichment entirely, dismantling key nuclear facilities, surrendering enriched materials, reopening the Strait of Hormuz without fees, promoting broader regional stability, and ceasing support for groups such as Hezbollah and the Houthis. Iran, however, proposed limited enrichment or reducing its stockpile, but the two sides failed to reach a compromise.

In response to Trump’s blockade announcement, Iranian Parliament Speaker Mohammad Bagher Qalibaf warned that Iran would not back down under pressure, stating that any confrontation would be met with force.

The U.S. plans to enforce the blockade on all vessels entering or leaving Iranian ports from 10 a.m. ET on April 13, covering areas along the Arabian Gulf and Gulf of Oman. It remains unclear whether U.S. allies will participate. Trump also criticized NATO for its lack of involvement and said Washington is reassessing its relationship with the alliance.

Oil prices rose on Friday amid renewed concerns over supply disruptions from Saudi Arabia and continued minimal tanker movement through the strategically vital Strait of Hormuz.

Despite the gains, crude was still on track for a weekly decline as market fears eased slightly following a fragile two-week ceasefire between the United States and Iran. At the same time, Israel indicated a possible diplomatic shift, expressing readiness to start direct negotiations with Lebanon soon.

Brent crude increased by $0.96, or 1%, to $96.88 per barrel at 0604 GMT, while West Texas Intermediate (WTI) gained $0.78, or 0.80%, reaching $98.65 per barrel.

Both benchmarks are down roughly 11% so far this week, marking their steepest weekly drop since June 2025, when earlier Israeli-U.S. strikes on Iran were paused.

According to Saudi Arabia’s state news agency SPA, citing the Ministry of Energy, attacks on key energy infrastructure have reduced the kingdom’s oil output capacity by about 600,000 barrels per day and cut throughput on the East-West Pipeline by approximately 700,000 barrels per day.

Analysts at ANZ noted that these developments have intensified concerns about further supply disruptions.

Shipping activity through the Strait of Hormuz remained below 10% of normal levels on Thursday, despite the ceasefire, as Iran asserted control by instructing vessels to stay within its territorial waters.

Although Iran and the U.S. agreed to a two-week ceasefire mediated by Pakistan, clashes reportedly continued afterward.

Experts suggest Pakistan may attempt to broker a longer-term agreement, but its ability to enforce the reopening of the waterway remains limited.

A Tehran official also told Reuters that Iran is seeking to impose transit fees on ships passing through the Strait under any peace arrangement, an idea opposed by Western governments and the U.N. shipping agency.

The conflict, which began on February 28 following U.S. and Israeli airstrikes on Iran, has effectively disrupted one of the world’s most important energy corridors.

Energy consultant John Paisie of Stratas Advisors warned that Brent crude could surge to $190 per barrel if current shipping constraints persist, though prices would be more contained if flows improve, albeit still above pre-war levels.

Mukesh Sahdev, CEO of XAnalysts, emphasized that the critical issue is not whether the Strait of Hormuz reopens, but how quickly normal oil flows can resume.

Meanwhile, JPMorgan estimated that around 50 energy infrastructure sites across the Gulf have been damaged by drone and missile attacks since the conflict began, with approximately 2.4 million barrels per day of refining capacity taken offline.

The dollar stayed fragile on Thursday following broad losses, as investors closely watched whether the uneasy ceasefire between the U.S. and Iran would hold. The truce appeared uncertain, with Israel continuing its conflict with Hezbollah in Lebanon and Tehran accusing both Washington and Tel Aviv of breaching the agreement, calling further peace talks unreasonable. Meanwhile, the Strait of Hormuz remained restricted, with ships requiring permits to pass, prompting higher oil prices as traders awaited clearer conditions.

U.S. President Donald Trump said American military forces would remain deployed around Iran until the terms of the deal were fully met. Analysts noted growing skepticism over whether the ceasefire could last or even be finalized. The dollar index was largely unchanged at 99.07, while the euro dipped slightly, sterling edged higher, and the yen weakened after giving back earlier gains.

The prolonged Middle East tensions have fueled expectations of more expansionary fiscal policy, contributing to yen weakness. Markets are currently pricing in a moderate chance of a Bank of Japan rate hike later this month, though this outlook could shift if the ceasefire collapses. Japan’s weakening consumer confidence and ongoing economic concerns tied to the conflict further complicate the central bank’s decision.

BOJ Governor Kazuo Ueda reiterated that real interest rates remain negative, keeping financial conditions loose. The dollar has benefited overall from the conflict, partly because the U.S. is a net energy exporter, unlike many oil-importing economies such as Japan and parts of Europe.

The five-week conflict has disrupted global energy supplies significantly, and despite the ceasefire, Iran retains increased influence over shipping through the Strait of Hormuz. Upcoming U.S. economic data, including personal spending and inflation measures, could influence the dollar’s direction, with strong figures potentially supporting a rebound.

Elsewhere, the Australian dollar edged lower, the New Zealand dollar gained slightly, and cryptocurrencies declined, with bitcoin and Ethereum both posting losses.

Markets have rebounded strongly after President Donald Trump chose to halt military action against Iran, but improved risk sentiment doesn’t change the bigger picture—oil prices are likely to stay elevated.

A clear relief rally is underway. US equity futures jumped almost immediately following the announcement of a two-week pause, with the Dow, S&P 500, and Nasdaq-100 all moving sharply higher. Meanwhile, oil prices, which had surged on fears of supply disruptions in the Strait of Hormuz, retreated as traders quickly unwound worst-case positions.

The speed of the reaction highlights how markets had been positioned for escalation. Defensive strategies were widespread, volatility was high, and crude prices had already priced in a significant geopolitical premium. Removing even part of that risk triggered a rapid reversal.

This strong rally also reflects how stretched investor sentiment had become. Markets were preparing for a scenario where a substantial share of global oil supply could be disrupted. Even a temporary easing of those fears prompted a swift shift back into equities.

Equity markets had already hinted at a possible de-escalation. Despite increasingly aggressive rhetoric, indices had begun to stabilize, suggesting investors anticipated some form of pause. The confirmation has now accelerated the move back into risk assets.

Technology stocks are expected to lead the recovery. The sector had been hit hardest by rising yields and risk aversion, but slightly lower oil prices help ease inflation concerns, supporting valuations—especially for large-cap and AI-driven companies.

Consumer sectors should also benefit quickly. Lower oil prices reduce fuel costs, boosting household purchasing power. Airlines, travel firms, and retailers are particularly well positioned to gain from improved sentiment and lower input expenses.

Financial stocks are also likely to rise. Greater stability encourages deal-making, strengthens capital markets activity, and eases pressure on credit conditions. Banks typically perform better when uncertainty declines and risk appetite increases.

Energy stocks, however, face a more mixed outlook. In the short term, falling crude prices may weigh on them. But underlying supply constraints remain unresolved, inventories are still tight, and geopolitical fragmentation continues to influence energy flows.

There’s a reason oil prices remain significantly higher this year. The risks go beyond the current conflict. Even if shipping through Hormuz resumes, it only provides temporary relief and does not fix deeper vulnerabilities in global energy supply chains.

As a result, oil is unlikely to fall back to previous lows anytime soon. A geopolitical premium is now built into prices, and traders will continue to factor in the risk of renewed disruptions.

Attention now turns to whether the two-week pause will hold. Temporary ceasefires often come with uncertainty, effectively starting a countdown. Markets will be watching closely to see if diplomacy can turn this into a longer-term solution.

Key factors include compliance with the pause, coordination over shipping routes, and the tone of ongoing negotiations. Meaningful progress could extend the rally further, lifting industrials, cyclical sectors, and emerging markets.

However, if diplomacy fails, sentiment could reverse quickly. Oil prices would likely surge again, volatility would return, and recent equity gains could be erased.

For now, investors are navigating a narrow path between opportunity and risk. The current rally is driven by reduced immediate fear, but underlying tensions remain unresolved—and energy markets continue to reflect that uncertainty.

Positioning for short-term gains may be reasonable, but any sustained upside will depend entirely on whether diplomatic efforts lead to lasting progress.

Bitcoin edged higher on Tuesday, recovering from earlier losses as risk appetite improved after Pakistan urged President Donald Trump to extend his deadline for Iran to reopen the vital Strait of Hormuz.

Market sentiment had previously been weighed down by stalled U.S.-Iran negotiations and Trump’s warning that Iran could face severe consequences if no agreement was reached by his deadline.

The world’s largest cryptocurrency was last trading 0.5% higher at $69,845.4 as of 17:43 ET (21:43 GMT).

Pakistan calls for a deadline extension and proposes a two-week ceasefire.

Pakistan, now a key intermediary between the U.S. and Iran, said diplomatic efforts to end the Middle East conflict are advancing steadily and could yield meaningful results in the near term.

Prime Minister Shehbaz Sharif urged President Trump to extend his deadline by two weeks to give negotiations more time, while also calling on Iran to reopen the Strait of Hormuz for the same period as a goodwill gesture. He further appealed to all sides to observe a two-week ceasefire to create space for diplomacy and work toward a lasting resolution.

According to Reuters, Tehran is responding positively to the proposal, while Axios reported that Trump has been informed of Pakistan’s initiative, citing the White House press secretary.

Trump’s Tuesday night deadline approaches.

Earlier on Tuesday, Trump warned that “a whole civilization will die tonight,” while expressing reluctance but suggesting the outcome seemed likely. He had already threatened to strike Iran’s bridges and power infrastructure if no deal was reached by his 20:00 ET deadline.

He also insisted that any ceasefire must include Iran reopening the Strait of Hormuz, which has effectively been closed since the conflict began, pushing global oil prices higher.

Reuters reported that Iran denied any negotiations with the U.S., accusing Washington of seeking surrender under pressure. Meanwhile, Iran’s Tasnim news agency said Tehran could target additional oil facilities, including those linked to Saudi Aramco, if U.S. attacks on energy infrastructure proceed.

An analyst at Nexo Dispatch noted that markets remain cautious rather than panicked, with investors waiting for the deadline to pass before taking a clearer stance.

Inflation data due later this week is in focus.

Bitcoin has increasingly moved in line with overall risk sentiment, as geopolitical tensions overshadow earlier optimism about diplomatic progress.

Attention is now shifting to upcoming U.S. economic data, particularly the March consumer price index due Friday. Rising energy costs tied to the Middle East conflict are expected to lift inflation, which could strengthen expectations that interest rates will stay higher for longer.

Such a backdrop may weigh on Bitcoin, as the asset typically underperforms in a high-rate environment.

According to Nexo’s Kalchev, ongoing energy-driven price pressures mean each inflation reading this week carries outsized importance for crypto—cooler data could revive hopes for rate cuts, while stronger figures would reinforce the higher-for-longer outlook.

Bitcoin ETFs record their largest daily inflows since February.

Bitcoin exchange-traded funds (ETFs) recorded their largest daily inflows since late February on Monday, as investors positioned ahead of the Iran deadline.

The funds saw a total of $471.3 million in inflows, led by BlackRock’s IBIT with $181.9 million. Fidelity’s FBTC and ARKB followed, attracting $147.3 million and $118.8 million, respectively, according to SoSoValue. Notably, no ETF reported any outflows during the session.

Most altcoins also rebounded on Tuesday, moving in line with Bitcoin’s gains.

Ethereum edged up 0.1% to $2,141.62, while XRP rose slightly by 0.1% to $1.3366. Solana gained 1.7%, and Cardano increased 0.4%. Among meme tokens, Dogecoin advanced 1.6%.

Bitcoin slipped below $69,000 on Tuesday as risk sentiment weakened ahead of a deadline set by U.S. President Donald Trump for Iran to reopen the Strait of Hormuz or risk military action.

The cryptocurrency was last down 0.8% at $68,525.1 as of 03:06 ET (07:06 GMT).

It had briefly climbed above $70,000 on Monday on hopes of a ceasefire, but was unable to sustain the gains.

Traders on edge as Trump’s deadline for Iran draws near, stoking fears of U.S. strikes and market volatility.

Markets are bracing for possible U.S. strikes on Iran as a deadline set by President Donald Trump approaches.

Sentiment worsened after Iran rejected a U.S.-backed ceasefire plan, instead calling for broader terms, increasing fears of escalation.

Trump has warned Iran could be “taken out” if it fails to comply by his 8 p.m. ET deadline, including potential strikes on critical infrastructure such as power plants and bridges.

The standoff has rattled global markets, pushing oil above $110 per barrel as concerns grow over disruptions in the Strait of Hormuz, a key route for global crude supply.

Rising energy prices have intensified inflation worries and boosted demand for safe-haven assets like the U.S. dollar.

Bitcoin has been trading more closely with overall risk sentiment, with geopolitical tensions outweighing earlier hopes for diplomatic progress.

Attention is now shifting to upcoming U.S. inflation data, especially Friday’s CPI report, which is expected to show upward pressure from higher energy costs—potentially keeping interest rates elevated for longer, a backdrop that could weigh further on Bitcoin.

Most altcoins extended losses on Tuesday as risk-off sentiment persisted in crypto markets.

Ethereum, the second-largest cryptocurrency, fell 1.5% to $2,103.92, while XRP dropped 2.4% to $1.31.

Solana and Polygon each declined about 3%, and Cardano lost more than 4%.

Gold prices dipped in Asian trade on Tuesday, marking a third consecutive day of losses, as investors grappled with inflation and interest-rate concerns ahead of U.S. President Donald Trump’s looming deadline on Iran. Spot gold eased about 0.2% to roughly $4,640 an ounce by early U.S. trading, while U.S. gold futures also retreated. Markets had closed lower on Monday after a volatile session.

Trump’s warning to Iran fuels concerns about rising inflation.

Trump’s escalating rhetoric on Iran added to inflation concerns, even as geopolitical tensions intensified. He warned that Iran could face severe consequences if it failed to reopen the Strait of Hormuz by his Tuesday 8 p.m. ET deadline, increasing fears of a wider conflict in the Middle East.

The standoff has already disrupted global energy supplies and driven oil prices higher, further fueling inflation expectations and clouding the outlook for monetary policy.

Although gold is usually supported by geopolitical uncertainty, it has instead weakened as rising oil prices feed inflation worries and reduce the likelihood of near-term interest rate cuts by the U.S. Federal Reserve.

Higher interest rates tend to weigh on non-yielding assets like gold, while a stronger dollar has also added pressure on bullion prices.

Iran has turned down a U.S. proposal for a ceasefire.

Diplomatic efforts to ease the conflict have made limited headway. Iran has rejected a U.S.-backed proposal for a 45-day ceasefire and a phased reopening of the Strait of Hormuz.

Instead, Tehran is pushing for a comprehensive settlement that includes sanctions relief, security assurances, and compensation for damages.

The absence of any breakthrough has increased uncertainty in financial markets, with investors closely monitoring developments ahead of Trump’s deadline.

Market participants are also awaiting key U.S. inflation figures due on Friday, which are expected to offer further signals on the Federal Reserve’s interest rate path.

In other precious metals, silver declined 0.9% to $72.16 per ounce, while platinum fell 1% to $1,963.60 per ounce. Meanwhile, copper prices moved higher, with benchmark London Metal Exchange futures rising 0.7% to $12,422.5 a ton, and U.S. copper futures edging up 0.3% to $5.62 per pound.

Iran has prepared its reply to the proposed ceasefire terms, according to a foreign ministry spokesperson.

Iran has outlined its positions and demands in response to recent ceasefire proposals delivered through intermediaries, a foreign ministry spokesperson said Monday, stressing that negotiations cannot proceed under ultimatums or threats of war crimes.

Spokesperson Esmaeil Baghaei noted that Tehran’s requirements—based on national interests—have already been communicated via intermediary channels, while earlier U.S. proposals, including a 15-point plan, were rejected as excessive.

He emphasized that clearly stating Iran’s legitimate demands should not be seen as compromise, but as confidence in defending its stance. Baghaei added that Iran has prepared its responses and will disclose further details in due course.

US and Iran consider a peace proposal as Trump warns of severe retaliation if the Strait remains closed.

The United States and Iran have received an outline for ending the conflict, but Tehran has refused to immediately reopen the Strait of Hormuz, even after Donald Trump warned of severe consequences if no deal is reached by Tuesday.

According to a source, the proposal follows a two-stage plan: an immediate ceasefire, followed by a broader agreement to be finalized within 15–20 days. Pakistan’s army chief, Asim Munir, has reportedly been in continuous contact with U.S. Vice President JD Vance, envoy Steve Witkoff, and Iran’s foreign minister Abbas Araqchi.

Iran, however, has rejected reopening the Strait under a temporary truce and dismissed imposed deadlines, while also expressing doubts about Washington’s commitment to a lasting ceasefire.

Earlier, Axios reported that the U.S., Iran, and regional mediators were exploring a potential 45-day ceasefire as part of a phased deal toward ending the war.

Trump, posting on Truth Social, issued a deadline of Tuesday evening, threatening further strikes on Iran’s infrastructure if the Strait remains closed.

Meanwhile, airstrikes continued across the region, more than five weeks into the conflict involving the U.S., Israel, and Iran. Tehran has responded by effectively shutting the Strait—through which about 20% of global oil and gas flows—and launching attacks on Israel, U.S. bases, and energy sites in the Gulf.

Officials in the UAE emphasized that any agreement must ensure free passage through the Strait, warning that failing to curb Iran’s nuclear and missile capabilities could lead to greater regional instability.

Despite repeated U.S. claims of weakening Iran’s military capacity, recent Iranian strikes on petrochemical facilities and vessels in Kuwait, Bahrain, and the UAE highlight its continued ability to retaliate.

The conflict has caused heavy casualties: thousands have died in Iran, including many civilians, while Israel and Lebanon have also suffered significant losses as fighting spreads, including clashes with Iran-backed Hezbollah forces.

Gold prices declined in Asian trading on Thursday, ending a four-session rally as markets responded to renewed escalation signals from U.S. President Donald Trump regarding the Iran conflict.

Spot gold was last down 1.4% at $4,693.12 per ounce as of 22:21 ET (02:21 GMT), after briefly reaching an intraday high of $4,800.58. U.S. gold futures also fell nearly 2% to $4,721.80 per ounce.

Market sentiment shifted after Trump stated in a televised address that the U.S. would intensify military action against Iran over the next “two to three weeks,” reaffirming Washington’s position on blocking Iran from acquiring nuclear weapons. He added, “We’re going to hit them extremely hard over the next two to three weeks. We’re going to bring them back to the Stone Ages where they belong.”

The comments contrasted with earlier remarks this week suggesting the U.S. could withdraw from the conflict within a similar timeframe, even without a formal agreement.

Financial markets have remained highly reactive to changing rhetoric on the conflict as investors reassess geopolitical risk. Oil prices rebounded following Trump’s remarks, raising concerns about inflationary pressures that could keep interest rates higher for longer and reduce demand for non-yielding assets like gold.

The U.S. dollar also strengthened after two consecutive losing sessions, further weighing on gold by making it more expensive for foreign buyers.

Investors are now focused on upcoming U.S. jobs data due Friday for signals on the Federal Reserve’s policy direction, a key driver for precious metals.

Elsewhere in metals, silver dropped 3.2% to $72.77 per ounce, while platinum slipped 1.7% to $1,934.60 per ounce.

Oil jumped over 4% on escalation fears.

Oil prices surged by more than $4 on Thursday after U.S. President Donald Trump said the United States would continue military strikes against Iran, including energy and oil infrastructure, over the coming weeks, while offering no clear timeline for ending the conflict.

Brent crude futures jumped $4.88, or 4.8%, to $106.04 per barrel at 0200 GMT, while U.S. West Texas Intermediate (WTI) crude rose $4.17, or 4.2%, to $104.29 per barrel.

The rally followed earlier weakness, as both benchmarks had dropped by more than $1 earlier in the session ahead of Trump’s address and closed lower in the prior trading day.

In his televised national speech, Trump said U.S. forces had nearly achieved their objectives in the conflict with Iran and that the war was approaching its conclusion, though he did not specify a timeframe. “We are going to finish the job, and we’re going to finish it very fast. We’re getting very close,” he said.

Geopolitical risks in the region have escalated, with threats to maritime shipping increasing. On Wednesday, an oil tanker chartered by QatarEnergy was struck by an Iranian cruise missile in Qatari waters, according to the country’s defence ministry.

Meanwhile, the head of the International Energy Agency warned that supply disruptions are beginning to affect Europe’s economy, with the region having previously relied on pre-war contracted oil shipments.

The U.S. dollar fell on Wednesday, touching a one-week low, as expectations of a possible de-escalation in the Middle East conflict reduced demand for the currency’s safe-haven appeal.

At 17:10 ET (21:10 GMT), the U.S. Dollar Index—which measures the dollar against a basket of six major currencies—was down 0.4% at 99.65.

Trump says Iran has requested a cease-fire and hints at a possible U.S. withdrawal, but ties any pause in fighting to conditions on the ground.

On Wednesday, Trump stated on Truth Social that Iran’s newly installed president had requested a ceasefire, describing him as “less radical and more intelligent” than his predecessors. He claimed the United States would only consider the request once the Strait of Hormuz is fully reopened and secure, adding that U.S. forces would continue striking Iran until then.

He also said that if Iran’s request is confirmed, it could signal a further step toward de-escalation, though uncertainty remains over the status of the Strait of Hormuz, a key global energy route that carries roughly one-fifth of the world’s oil and gas supply and has reportedly been disrupted since the conflict began, contributing to higher oil prices.

In earlier remarks from the Oval Office, Trump suggested the U.S. could begin withdrawing forces within two to three weeks, arguing that the objective of eliminating Iran’s nuclear threat had already been achieved and that no formal agreement would be necessary to end the conflict.

The White House also announced that Trump is scheduled to address the nation at 21:00 ET (01:00 GMT) with an “important update on Iran.”

The dollar posts its strongest monthly performance since July 2025.

The greenback ended Tuesday, closing out March with its strongest monthly performance since July last year.

Rising oil prices, driven by supply disruptions following the closure of the Strait of Hormuz, have raised concerns about a potential inflation shock. This has prompted investors to reassess expectations for central bank rate cuts and, in some cases, price in a higher likelihood of rate hikes.

A “higher-for-longer” interest rate outlook typically supports the U.S. dollar, enhancing its appeal as a safe-haven asset amid ongoing Middle East tensions. The currency has also benefited from the U.S. position as a net energy exporter, as well as a broader shift toward cash holdings.

According to David Morrison, senior market analyst at Trade Nation, the Dollar Index has been a key beneficiary of regional instability. He noted that the dollar surged last month as investors moved into the currency in a classic flight to safety, at the expense of traditional havens such as precious metals, U.S. Treasuries, and currencies like the Japanese yen and Swiss franc.

Morrison added that the index appeared to have broken above long-term resistance near the 100 level, suggesting a potential bottom after a weak year. However, he cautioned that momentum may now be stalling, implying that dollar bulls may need to wait for clearer signals before expecting further sustained gains.

Euro, yen, and sterling end the month lower.

The euro (EUR/USD), sterling (GBP/USD), and Japanese yen (USD/JPY) were largely unchanged on Wednesday.

However, developed market currencies underperformed the U.S. dollar over March. The euro and British pound recorded their weakest monthly results since July and October 2025, respectively, while the yen also posted its worst month since October.

Europe and Japan, both heavily dependent on Middle Eastern supplies of liquefied natural gas and fuel, have been more exposed to the impact of rising oil prices than the United States.

The inflationary pressure from higher oil costs linked to the Iran conflict is already beginning to appear in economic data. Preliminary Eurostat figures showed eurozone inflation is expected to rise to 2.5% in March from 1.9% in February. Energy prices are projected to be the main driver, with annual energy inflation accelerating to 4.9% after a 3.1% decline in the previous month.

In the UK, which is experiencing its fifth oil supply shock in roughly a decade, concerns are growing that rising energy costs could tip the economy toward recession, according to Deutsche Bank economist Sanjay Raja.

A massive oil tanker near Dubai was struck by an Iranian attack following the latest threats from Trump.

Iran struck and set fire to a fully laden crude tanker near Dubai on Monday, as President Donald Trump warned Washington would destroy Iran’s energy infrastructure if Tehran failed to reopen the Strait of Hormuz. The targeted vessel, the Kuwait-flagged Al-Salmi, is the latest in a series of attacks on commercial shipping using missiles and drone strikes in the Gulf since U.S. and Israeli forces hit Iran on February 28.

The conflict, now a month old, has expanded across the Middle East, causing heavy casualties, disrupting energy flows, and raising fears of a global economic downturn. Oil prices briefly surged again following the attack on the tanker, which has a capacity of roughly 2 million barrels valued at over $200 million. Its owner, Kuwait Petroleum Corp, said the strike occurred early Tuesday, igniting a fire and damaging the hull, though no injuries were reported. Dubai authorities later confirmed the blaze had been contained after what they described as a drone strike.

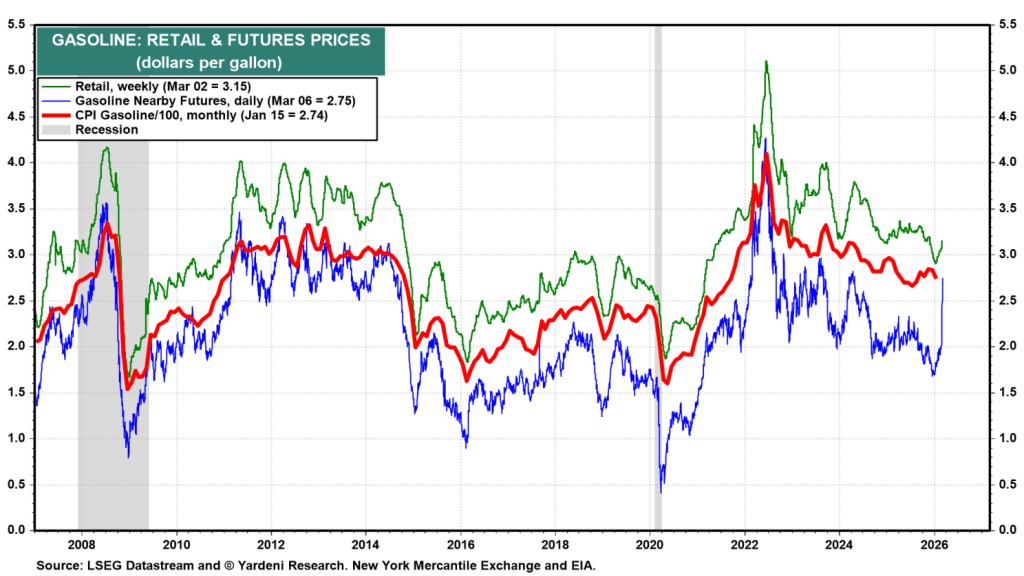

Rising oil and fuel costs are beginning to strain U.S. households and pose a political challenge for Trump and Republicans ahead of November’s midterm elections, particularly after pledges to cut energy prices and boost domestic production. Gasoline prices in the U.S. climbed above $4 per gallon for the first time in more than three years, according to GasBuddy, as tighter global supply pushed crude above $101 per barrel.

Meanwhile, hostilities show no sign of easing, with concerns mounting over a broader regional war. Iran-aligned Houthi forces have launched missiles and drones at Israel, while Turkey reported intercepting a ballistic missile from Iran that briefly entered its airspace. Israel has carried out strikes on targets in Tehran and Hezbollah-linked sites in Beirut, with explosions reported across parts of the Iranian capital and power outages affecting some districts.

The Israeli military said four of its soldiers were killed in southern Lebanon, where recent incidents have also claimed the lives of UN peacekeepers. Iran’s military stated its latest wave of attacks targeted U.S. bases and Israeli positions across the region.

The U.S. has begun deploying thousands of troops from the 82nd Airborne Division to the Middle East, signaling potential escalation even as diplomatic efforts continue. The White House said Trump aims to secure a deal with Iran before an April 6 deadline to reopen the Strait of Hormuz, a key route for roughly one-fifth of global oil and LNG shipments.

While U.S. officials say talks are progressing, Iran has dismissed proposed terms as unrealistic, insisting it is focused on defense amid ongoing attacks. Trump reiterated both optimism for a deal and a renewed threat to destroy Iran’s energy facilities if no agreement is reached, though reports suggest he may be open to ending military operations even if the strait remains partially closed.

Oil prices later eased and equities recovered on hopes of de-escalation. Still, the administration is weighing further steps, including seeking financial contributions from Arab allies, as it requests an additional $200 billion in war funding—an effort likely to face resistance in Congress.

Oil and war fears dominate markets heading into an uncertain Q2.

Financial markets enter the second quarter on shaky ground, highly sensitive to war-related headlines. This environment raises the risk of deeper equity declines, while the sharp selloff in bonds may start to attract buyers.

Even if the conflict eases soon, investors believe lasting damage to Middle East energy infrastructure and persistently high oil prices will weigh on growth and keep inflation elevated. That combination could further pressure stocks, though if growth fears begin to outweigh inflation concerns, bonds may stage a recovery.

Seema Shah, chief global strategist at Principal Asset Management, noted that uncertainty dominates: it’s hard for investors to see beyond the constant flow of geopolitical news. While diversification into international equities remains appealing, she emphasized that U.S. exposure still plays an important role.

The Middle East conflict caps a volatile first quarter also shaped by U.S. geopolitical moves and rapid AI-driven disruption. Oil has been the standout performer, surging about 90% to above $100 a barrel, which has shaken bond markets and pushed expectations for higher interest rates.

Analysts surveyed by Reuters see oil ranging from $100 to $190 if supply disruptions persist, with an average forecast around $134. Meanwhile, prediction platform Polymarket assigns roughly a one-third chance of the war ending by mid-May and a 60% likelihood by late June.

Echoing the inflation surge of 2022, short-term borrowing costs in countries like Britain and Italy have jumped sharply, with notable moves also seen in U.S., German, and Japanese bonds. According to Societe Generale strategist Manish Kabra, the key factors for markets are how long the oil shock lasts and how central banks respond.

Since the war began, expectations for U.S. rate cuts this year have largely disappeared. In Europe and the UK, investors now anticipate rate hikes instead of easing, while hopes for monetary loosening in emerging markets have faded.

Kabra highlighted the upcoming U.S. Memorial Day weekend as a potential pressure point, as rising travel demand could intensify public and political focus on energy prices. Reflecting this backdrop, he has increased exposure to commodities in portfolios.

Bond markets have taken a hit, with yields rising sharply, but some investors see value emerging. Amundi, for instance, has added short-term eurozone government bonds and maintained positions in U.S. Treasuries, expecting central banks to look past short-term inflation spikes once the crisis stabilizes.

Similarly, Russell Investments sees bonds as more attractive than a few months ago and expects the dollar’s recent strength—up over 2% in March—to fade over time. Before the conflict, investors had been rotating away from U.S. assets, a trend that could resume if tensions ease.

Gold has slipped about 4% in March, as investors sell profitable positions to offset losses elsewhere, despite its usual role as an inflation hedge.

Equities, while initially resilient thanks to strong earnings and the tech sector, are now under pressure. The S&P 500 and Europe’s STOXX 600 have fallen roughly 9–10% from recent highs, and Japan’s Nikkei has dropped nearly 13% from its February peak.

Zurich Insurance strategist Guy Miller said his firm has shifted to an underweight position in equities as the economic outlook deteriorates. Data already points to weakening momentum, with U.S. consumer sentiment declining, German investor confidence dropping sharply, and business activity indicators hitting multi-month lows.

Although the U.S. benefits from a relatively strong economy and its status as an energy exporter, it is not immune. Prolonged high energy prices would still weigh on growth. The OECD has already warned that the global economy has been knocked off a stronger growth trajectory.

Miller concluded that this conflict differs from recent geopolitical shocks, which had limited market impact—this time, the implications for earnings, margins, and valuations are far more significant.

The U.S. dollar is on track for its strongest monthly performance since July, solidifying its position as the dominant safe-haven asset as escalating conflict in the Middle East drives oil prices higher and fuels concerns about a global economic slowdown.

The greenback extended its broad rally overnight, with the notable exception of the Japanese yen, where renewed intervention warnings from Tokyo have made traders cautious about pushing the currency much beyond the 160-per-dollar level.

After hitting its weakest level since July 2024 a day earlier, the yen traded at 159.81 in Tuesday’s Asian session, marking a roughly 2.4% monthly decline, largely due to Japan’s heavy reliance on imported energy. It showed little reaction to data indicating a slight easing in Tokyo inflation.

Meanwhile, the euro dropped 0.3% overnight and is set for a monthly loss of around 3%, while both the Australian and New Zealand dollars fell to multi-month lows. The Australian dollar, which had remained relatively resilient for most of the month, has recently come under pressure as market concerns shift from inflation toward slowing global growth. It slipped to a two-month low of $0.6834 before stabilizing slightly, while the New Zealand dollar hit a four-month low near $0.5716.

Elsewhere, South Korea’s won weakened to its lowest level since 2009. The U.S. dollar index climbed to 100.61 on Monday—its highest since last May—and is up 2.9% in March, marking its sharpest monthly gain since July.

Geopolitical tensions intensified after U.S. President Donald Trump warned that the U.S. could target Iran’s energy infrastructure if Tehran fails to reopen the Strait of Hormuz, following Iran’s dismissal of U.S. peace proposals and continued missile strikes on Israel. Reports of an Iranian attack on a Kuwaiti oil tanker near Dubai further lifted oil prices.

According to ING’s global head of markets, Chris Turner, the dollar is unlikely to give up its gains without clear signs of de-escalation from Iran.

On the monetary policy front, Federal Reserve Chair Jerome Powell signaled a cautious stance, downplaying the likelihood of near-term rate hikes and emphasizing a wait-and-see approach as inflation expectations remain stable in the longer term. Although this pushed short-term bond yields lower and reduced expectations for rate hikes this year, it did little to weaken the dollar, which continues to benefit from safe-haven demand amid global uncertainty.

Other traditional safe havens have underperformed since the conflict began. Bonds and gold have struggled, while the yen has remained weak and the Swiss franc has been pressured by signals from the Swiss National Bank that it may act to curb currency strength. The dollar has gained nearly 4% against the franc this month, reaching around 0.80 francs.

Looking ahead, investors are watching for upcoming European inflation data and China’s PMI figures later in the session.

Gold prices edged up slightly as attention remains on the escalating Iran conflict.

Gold edged higher in Asian trading on Monday, recovering modestly after a volatile week, as investors continued to watch the risk of escalation in the U.S.–Israel conflict with Iran.

Spot gold gained 0.4% to $4,509.51 an ounce, with futures rising similarly to $4,537.40. Prices had swung sharply last week, dropping to around $4,000 before rebounding close to $4,500 by Friday.

Other precious metals were mixed, with silver slipping 0.9% while platinum advanced 1.8%.

Analysts at OCBC said the recent rebound in gold appears largely technical, following a steep decline of about 20% since the conflict began. While bearish pressure is easing and momentum indicators are improving, they cautioned that the recovery may struggle to hold unless prices break above key resistance levels at $4,624, $4,670, and $4,850 per ounce.

They also warned that persistently high energy prices could keep inflation elevated, potentially pushing Treasury yields higher and creating a less favorable environment for gold in the near term.

Meanwhile, geopolitical tensions remained high after Iran-backed Houthi forces in Yemen launched attacks on Israel over the weekend, raising fears of a broader conflict. Iran signaled readiness for a possible U.S. ground invasion, amid reports that Washington is deploying additional troops to the Middle East.

U.S. President Donald Trump said negotiations with Iran were progressing and a deal could be near, though he provided no clear timeline and warned that further strikes on Tehran remain possible. He also recently extended a deadline for potential attacks on Iran’s energy infrastructure into early April.

Oil prices jumped above $115 per barrel after Yemen’s Houthi forces launched an attack on Israel.

Oil prices surged in early Monday trading after Yemen’s Houthi group launched attacks on Israel, raising fears of a wider Middle East conflict.

Brent crude jumped 2.2% to $115.08 a barrel, after briefly spiking as high as $116.43.

The Iran-backed Houthis said they had fired multiple missiles at Israel and warned of further strikes, heightening concerns about escalation—especially given their ability to target vessels in the Red Sea.

Tensions remained elevated as Israeli forces struck targets in Tehran, while the U.S. deployed 3,500 troops to the region aboard the USS Tripoli. Iran also signaled readiness for a potential U.S. ground operation.

Oil prices have rallied sharply in March, with Brent up nearly 60%, driven by severe supply disruptions. Iran’s effective blockade of the Strait of Hormuz—a route carrying about 20% of global oil supply—has intensified market fears.

While Pakistan has offered to host talks between Washington and Tehran following a U.S. ceasefire proposal, Iran has largely rejected direct negotiations and accused the U.S. of preparing for a ground invasion.

Donald Trump said the United States and Iran have been engaging both directly and through intermediaries, describing Iran’s new leadership as “very reasonable,” even as additional U.S. troops deployed to the region and Tehran warned it would not accept humiliation.

His comments came after Pakistan announced it was preparing to host potential talks between Washington and Tehran aimed at ending the month-long conflict. Trump expressed confidence a deal could be reached, though he acknowledged uncertainty.

He also suggested that recent strikes, including one that killed Ali Khamenei, had effectively resulted in regime change, noting that the new leadership appears more pragmatic.

The conflict, which began with an Israeli strike on February 28, has spread across the Middle East, causing heavy casualties, disrupting global energy supplies, and weighing on the world economy.

Pakistan’s Foreign Minister Ishaq Dar said regional discussions had focused on ending the war and possibly hosting U.S.-Iran negotiations in Islamabad, though it remains unclear if both sides will attend.

Meanwhile, Iran’s parliamentary speaker Mohammad Baqer Qalibaf accused the U.S. of signaling negotiations while preparing for a potential ground invasion, warning that Iran would resist any attempt at forced submission.

The Pentagon has sent thousands of additional troops to the region, giving Washington the option of launching a ground offensive, while Israel has indicated it will continue strikes against Iranian military targets regardless of diplomatic efforts.

Recent Israeli airstrikes have targeted missile facilities and infrastructure across Iran, while Iranian retaliation has struck sites in Israel. The conflict has also disrupted key shipping routes, including the Strait of Hormuz, driving oil prices sharply higher and rattling global markets.

As tensions escalate, the arrival of more U.S. forces and the possibility of broader regional involvement—including attacks linked to Yemen’s Houthi forces—raise the risk of a prolonged and wider war.

The U.S. dollar rose on Friday, positioning itself for its strongest monthly performance since July, as investors turned to the currency as a safe haven amid uncertainty surrounding the Iran conflict.

By 17:28 ET (21:28 GMT), the U.S. Dollar Index—which measures the greenback against six major currencies—had increased by 0.3% to 100.18.

The U.S. dollar is on track for its strongest monthly performance since July 2025.

The U.S. dollar is on track for its strongest monthly gain since July 2025, with the Dollar Index rising 2.6% in March—its biggest increase since a 3.2% climb last July.

This strength has been driven by growing safe-haven demand amid geopolitical tensions, along with expectations that interest rates will stay higher for longer due to inflation pressures from rising energy prices. Markets have largely abandoned bets on Federal Reserve rate cuts this year, and are even starting to price in potential rate hikes.

At the same time, investors have been selling off bonds, pushing U.S. Treasury yields sharply higher, with the 10-year yield reaching its highest level since July.

According to Macquarie strategist Thierry Wizman, while safe-haven flows have played a role, the dollar’s strength is more fundamentally driven—particularly by the U.S.’s lower reliance on imported oil compared to other regions. He noted that unlike past periods of uncertainty, the current environment may have a less severe impact on U.S. incomes, helping support the dollar despite global economic disruptions.

Trump pushed back a critical deadline, while Iran reported that its infrastructure had been struck.

Risk assets fell sharply on Friday as tensions in the Middle East intensified, while oil prices surged past $110 per barrel. Although President Donald Trump extended a deadline for Iran to reopen the Strait of Hormuz, the move did little to reassure markets.

Iran’s foreign minister, Abbas Araghchi, stated that Israeli strikes had already hit key infrastructure, including steel plants, a power station, and civilian nuclear facilities, calling the attacks inconsistent with Trump’s extended timeline.

Earlier, Trump had warned Iran to unblock the strategic waterway—through which about 20% of global oil supply passes—or face U.S. strikes on its energy infrastructure. He later delayed potential action until Friday following what he described as “very strong” talks with Iran. However, Tehran has denied that any negotiations with Washington are taking place.

The euro and British pound weakened, while the yen surged to 160 against the dollar.

The euro and British pound weakened against the U.S. dollar, with EUR/USD falling 0.2% to 1.1510 and GBP/USD dropping 0.5% to 1.3259, as Europe continues to face energy supply disruptions—especially in natural gas—linked to the Iran conflict.

G7 diplomats met in France, where U.S. Secretary of State Marco Rubio highlighted the Strait of Hormuz as a key issue, warning that any attempt by Iran to impose tolls on the passage would be unacceptable.

Meanwhile, the Japanese yen slid further, with USD/JPY rising 0.4% to 160.25. Reports suggest that breaching the 160 level could prompt intervention by Japanese authorities. The Australian dollar, often seen as a risk-sensitive currency, remained broadly stable after earlier falling to a two-month low.

Analysts at MUFG expect the U.S.–Iran conflict to be relatively short-lived, with geopolitical risk premiums eventually easing. However, they caution that a prolonged conflict could keep energy prices elevated, putting additional pressure on currencies in Asia that rely heavily on energy imports—particularly the South Korean won and the Japanese yen.

Cuba seeks Vatican help to ease the U.S. oil embargo, the Washington Post reports.

Cuban officials have asked the Vatican to help convince the administration of U.S. President Donald Trump to relax its oil embargo, raising the issue in high-level meetings with Vatican representatives, including Pope Leo, the Washington Post reported Friday, citing sources familiar with the discussions.

Reuters said it could not immediately confirm the report, and the Vatican, the White House, and the Cuban government did not respond to requests for comment.

Havana and Washington began talks earlier this month as the embargo intensifies economic pressures on the Communist-led country, with some reports indicating the Trump administration may be aiming to remove President Miguel Díaz-Canel from power.

Oil edges higher but is still on track for its first weekly drop since the Iran conflict began.

Oil prices rose on Friday but were still set for their first weekly decline since February 9, after U.S. President Donald Trump extended a pause on strikes against Iran’s energy facilities. Despite the temporary restraint, investors remain cautious about the chances of a ceasefire in the month-long conflict.

Brent crude climbed $1.87 (1.73%) to $109.88 a barrel, while U.S. West Texas Intermediate (WTI) gained $1.57 (1.66%) to $96.05. Even so, both benchmarks were down on the week, with Brent slipping 2.1% and WTI losing 2.3%, though they have surged sharply since the conflict began.

Analysts noted that oil markets are being driven more by the potential duration of the war than short-term headlines, warning that any damage to infrastructure or prolonged fighting could push prices significantly higher. Trump has extended a deadline to April 6 for Iran to reopen the Strait of Hormuz or face further action, while the U.S. continues to build up military presence in the region and considers targeting key Iranian oil assets.

Iran has rejected a U.S. proposal relayed via Pakistan, calling it unfair. Meanwhile, the conflict has removed around 11 million barrels per day from global supply, worsening an already tight market. Analysts say prices could fall quickly if tensions ease, but remain elevated overall—or even spike to $200—if the war drags on into late June, as countries increasingly draw on reserves and adjust demand.

Oil prices inched up as Iran considers the U.S. plan to end the conflict.

Oil prices in Asia inched up on Thursday as mixed signals over Middle East de-escalation kept markets cautious, while Iran considered a U.S. proposal to end the conflict.

By 20:31 ET (00:31 GMT), May Brent crude rose 0.8% to $103.02 per barrel and WTI crude gained 1% to $91.20, after both benchmarks dropped more than 2% in the previous session.

Traders assessed tentative diplomatic developments from Tehran, where authorities are said to be reviewing a U.S.-supported plan to stop the fighting. Although Iran has yet to accept the proposal, it has not rejected it outright, fueling guarded optimism for easing tensions.

However, uncertainty remains high. Tehran has denied direct talks with Washington and signaled that major disagreements persist, leaving markets uneasy and price moves relatively muted.

Crude has seen sharp swings in recent weeks as the conflict disrupted supply flows from the Gulf, a key global oil hub. Earlier this month, Brent surged past $119 per barrel on concerns over potential supply outages.

The Strait of Hormuz—through which about one-fifth of global oil passes—remains a critical risk point, with any disruption likely to drive prices higher.

On Wednesday, prices fell as reports of possible negotiations eased some geopolitical risk premium. Meanwhile, investors are monitoring Washington’s stance, as officials warn of tougher action if Iran fails to engage, adding further uncertainty to the outlook.

Gold holds steady as markets weigh conflicting signals over potential de-escalation between the U.S. and Iran.

Gold prices were mostly stable in Asian trading on Thursday as investors navigated mixed signals surrounding the Iran conflict, while Tehran continued to assess a U.S. proposal to end the war.

Spot gold edged up 0.1% to $4,509.06 an ounce by 22:57 ET (02:57 GMT), while U.S. gold futures declined 1.1% to $4,536.10.

Bullion had recovered earlier in the week, climbing back above $4,500 after a sharp pullback, supported by a weaker dollar and cautious optimism over potential U.S.-Iran diplomacy.

Still, gains were limited as uncertainty persisted. Iran is reviewing a U.S.-backed plan to halt hostilities, but unclear signals on whether talks will advance have kept investors wary.

Although Tehran has not formally accepted the proposal, it has avoided rejecting it outright, fueling guarded hopes for de-escalation. At the same time, Iran has denied direct negotiations with Washington and emphasized that key differences remain unresolved, leaving markets uneasy.

The U.S. has also warned of tougher action if Iran fails to engage constructively, adding another layer of tension.

Gold—traditionally a safe-haven asset—has shown unusual volatility in recent weeks. Prices dropped sharply earlier this month despite rising geopolitical risks, as expectations of prolonged high interest rates and a stronger dollar weighed on demand.

Movements in oil prices have also influenced sentiment. Rising crude has heightened inflation concerns, reinforcing expectations that central banks may keep rates elevated, which tends to pressure non-yielding assets like gold.

Wider financial markets reflected a cautious tone, with investors seeking clearer direction on both geopolitical developments and global monetary policy.

Among other precious metals, silver gained 0.1% to $71.32 an ounce, while platinum slipped 0.6% to $1,918.60.

The U.S. dollar rose slightly on Wednesday, rebounding from earlier losses as hopes for Middle East de-escalation faded after Iran rejected a U.S. ceasefire proposal.

At 17:45 ET (21:45 GMT), the U.S. Dollar Index—tracking the greenback against six major currencies—gained 0.2% to 99.62.

The United States has put forward a ceasefire proposal.

While there is some optimism that Washington and Tehran may be exploring ways to end the conflict, markets remain cautious as both sides continue to offer conflicting accounts of how negotiations are progressing.

Reportedly eager to find an exit from the war, President Donald Trump has backed a U.S. proposal outlining a 15-point peace plan to Iran. The plan not only calls for Tehran to dismantle its primary nuclear facilities but also urges the reopening of the Strait of Hormuz — a critical shipping route south of Iran that has been largely shut to tanker traffic in recent weeks. This disruption has pushed energy prices higher and raised concerns about global inflation.

According to Thierry Wizman, global FX and rates strategist at Macquarie, investor optimism was revived by news that the U.S. had presented concrete terms to Iran. However, he cautioned that a ceasefire is unlikely in the near term. Instead, the U.S. may escalate military pressure over the next couple of weeks to push Iran toward meaningful concessions, with major combat potentially reaching a turning point by mid-April. He described the situation as entering a third phase — one defined by both negotiation and conflict, rather than purely one or the other.

Wizman added that the possibility of renewed negotiations signals a more critical stage in the U.S.-Iran conflict. Initially driven by diplomacy, then by direct confrontation, the situation may now evolve into a blend of both. While this dual-track approach could help stabilize market sentiment compared to outright war, it also carries the risk of sharper downside if it fails to deliver lasting stability and security.

Iran has pushed back against the proposal.

On Wednesday morning, the Fars News Agency reported that Tehran does not accept a ceasefire, emphasizing that it seeks a complete end to the conflict rather than a temporary halt in fighting.

Later, Press TV stated that Iran would not allow the United States to dictate when the war should end, citing a senior political figure. According to the report, the official outlined five key demands from Tehran, including a full cessation of attacks as well as international recognition and guarantees of Iran’s authority over the Strait of Hormuz.

However, Axios later cited a U.S. official saying Washington had not received any formal communication from Iran rejecting the ceasefire plan.

Iranian Foreign Minister Abbas Araghchi also denied that negotiations with the U.S. were taking place, according to Reuters. While acknowledging that messages were being passed through intermediaries, he stressed that such exchanges should not be interpreted as formal talks.

In the energy market, Brent crude — the global benchmark — briefly dipped below $100 per barrel on Wednesday, though it remains significantly higher than the roughly $70 level seen before the conflict began in late February.

Rising concerns over energy-driven inflation have strengthened expectations that central banks worldwide may need to adopt a more hawkish policy stance. In Germany, ECB President Christine Lagarde indicated that further tightening could be justified even if the inflation spike proves temporary.

The euro and yen edged higher on Wednesday, while sterling drew attention following the latest UK inflation figures.

The euro saw a slight uptick, with EUR/USD hovering around 1.1560. At the same time, the Japanese yen strengthened, pushing USD/JPY down to 159.33.

Sterling remained largely flat, trading near 1.3365 against the dollar, but came into focus after the release of new consumer inflation data. The UK’s consumer price index rose 3% year-on-year in March, unchanged from February. Notably, the data does not yet reflect the impact of rising oil prices triggered by the Middle East conflict.

According to Sanjay Raja, chief UK economist at Deutsche Bank, the UK’s disinflation trend may be approaching a pause. He noted that February’s inflation reading is already outdated, as households and businesses are beginning to feel the effects of the Iran conflict, particularly through higher fuel costs. Further increases in fuel prices are expected, and even if the conflict ends quickly, energy bills — including electricity and gas — could still climb by double digits over the summer.

Gold rises on softer dollar, lower oil after U.S. proposal.

Gold surged more than 2% during Asian trading on Wednesday, driven by falling oil prices and a softer U.S. dollar. Hopes of a potential Middle East ceasefire eased inflation concerns, increasing the appeal of the metal.

Spot gold rose 2.3% to $4,577.55 per ounce, while U.S. gold futures climbed 4% to $4,611.70.

The move came as reports emerged that the United States had proposed a 15-point plan to Iran aimed at ending the conflict. President Donald Trump said negotiations were ongoing and noted that Iran appeared willing to reach a deal. However, Iranian officials denied any talks, underscoring continued uncertainty.

Oil prices dropped sharply after earlier gains fueled by supply disruption fears, with Brent crude slipping below $100 per barrel. This decline helped ease inflation expectations, reducing pressure on central banks to maintain high interest rates.

Lower energy prices also weighed on bond yields and the dollar—factors that typically support gold, which does not yield interest. The U.S. Dollar Index slipped 0.2% in early trading.

Gold had recently been under pressure due to rising oil prices and bond yields, which strengthened the dollar and triggered a broader selloff in precious metals.

Despite the rebound, analysts warned that volatility is likely to continue, as markets remain highly sensitive to developments in the Middle East.

Elsewhere, silver jumped 3.3% to $73.60 per ounce, and platinum rose 2.2% to $1,977.60.

Oil drops on Middle East ceasefire hopes.

Oil prices dropped about 4% on Wednesday as hopes of a potential ceasefire in the Middle East raised expectations that supply disruptions from the region could ease. The decline followed reports that the U.S. had delivered a 15-point proposal to Iran aimed at ending the conflict.

Brent crude fell $4.89 (4.7%) to $99.60 per barrel, after hitting a low of $97.57. U.S. West Texas Intermediate (WTI) slipped $3.54 (3.8%) to $88.81, touching as low as $86.72. This came after both benchmarks had surged nearly 5% in the previous session before trimming gains amid volatile trading.

Analysts said growing optimism over a ceasefire, along with profit-taking, pressured prices. However, uncertainty over whether negotiations will succeed continues to limit further declines.

U.S. President Donald Trump stated that progress was being made in talks with Iran, while sources confirmed Washington had sent a detailed settlement plan. Reports also suggested the U.S. is pushing for a temporary ceasefire to facilitate discussions, including measures such as curbing Iran’s nuclear program and reopening the Strait of Hormuz.

Despite this, some analysts remain cautious, warning that Middle East developments will continue to drive price swings in the near term.

The conflict has severely disrupted oil and LNG shipments through the Strait of Hormuz—responsible for roughly one-fifth of global supply—creating what the International Energy Agency has described as an unprecedented supply shock.

Even if a ceasefire is reached and flows resume, experts say it is unclear how quickly production will fully recover, especially without confidence in a lasting agreement.

Meanwhile, diplomatic efforts continue, with Pakistan offering to host negotiations, and Iran indicating that non-hostile vessels may pass through the Strait if coordinated with its authorities. Still, military activity in the region persists, and the U.S. is reportedly preparing to deploy additional troops.

To offset disruptions, Saudi Arabia has ramped up exports via its Red Sea Yanbu port to nearly 4 million barrels per day.

In the U.S., inventory data added further pressure to prices, with crude stocks rising by 2.35 million barrels, gasoline up 528,000 barrels, and distillates increasing by 1.39 million barrels last week, according to industry estimates.

The dollar climbed on Tuesday, recovering from the previous session’s decline as uncertainty surrounding U.S.–Iran peace negotiations dampened sentiment and boosted demand for safe-haven assets.

The greenback showed little response to an unverified media report released after the Wall Street close, which suggested a potential ceasefire between the two countries.

As of 17:49 ET (21:49 GMT), the U.S. Dollar Index—measuring the currency against a basket of six major peers—rose 0.3% to 99.23.

Dollar rebounds amid persistent uncertainty

The dollar regained ground as uncertainty continued to dominate market sentiment. On Monday, Donald Trump stated that he would postpone potential strikes on Iran’s energy facilities for five days following what he described as “very positive and productive” discussions aimed at ending the nearly month-long conflict. His remarks initially pressured the dollar, pushing it to its lowest level in almost two weeks.

However, sentiment shifted on Tuesday as conflicting media reports emerged regarding developments in the Middle East. Iran’s parliamentary speaker dismissed Trump’s claims, accusing him of fabricating the talks to calm volatile financial markets.

Later, Trump told reporters that negotiations were still underway and asserted that Iran had agreed to forgo developing nuclear weapons. He also noted that U.S. Secretary of State Marco Rubio and Vice President JD Vance were involved in the discussions.

Following the close of Wall Street, Israel’s Channel 12 reported that U.S. Middle East envoy Steve Witkoff and businessman Jared Kushner were working on a framework to establish a ceasefire and initiate negotiations based on a 15-point plan. Meanwhile, The New York Times reported that the U.S. had already delivered a proposal to Iran aimed at ending the conflict.

Despite these developments, hostilities in the Middle East continue, with the Strait of Hormuz—a crucial passage south of Iran through which roughly 20% of global oil supply flows—effectively closed. The strait remains a major flashpoint, as the risk of Iranian attacks on vessels threatens to disrupt vital energy shipments, particularly to key Asian importers.

Analysts at ING noted that the dollar remains highly sensitive to evolving headlines surrounding the conflict. They added that markets are closely watching for signals—especially from Iran—on whether meaningful ceasefire negotiations could begin. Until clearer progress emerges, any sustained rally in risk assets or significant decline in the dollar is likely to remain limited.

Euro and sterling steady; yen in spotlight after Japan inflation data

The euro and British pound remained largely stable on Tuesday, with EUR/USD edging slightly higher to 1.1607 and GBP/USD ticking up to 1.3409.

Meanwhile, the dollar posted modest gains against the Japanese yen after fresh data showed Japan’s inflation slowed more than expected in February. Core inflation dropped below the central bank’s target for the first time in four years, reinforcing expectations that the Bank of Japan may adopt a more cautious approach toward further monetary tightening.

Analysts at ING noted that the central bank is likely to look past the recent slowdown in inflation and instead focus on potential upside risks to prices.

They added that strong wage negotiation outcomes and firmer-than-expected PMI readings could still support the case for an interest rate hike as early as April. However, the exact timing remains uncertain and may depend on evolving geopolitical developments, particularly in the Middle East.

Bitcoin surged on Monday as investor appetite for risk improved amid hopes of easing tensions in the Middle East.

Donald Trump highlighted “productive” discussions with Iran and announced that the U.S. would delay planned strikes on Iranian energy facilities for five days. Following these remarks, Bitcoin climbed 4.5% to $70,947.6 after previously trading lower.

However, Iran’s Fars News Agency denied any form of communication with the U.S., stating that no direct or indirect talks had taken place. The report also suggested that Washington’s decision to postpone strikes came after Iran warned it would retaliate by targeting energy infrastructure across West Asia.

Donald Trump highlights “productive” talks, raising hopes for a potential end to the conflict.

Donald Trump claimed that the U.S. had held “productive” discussions with Iran, suggesting a potential path toward ending the conflict. In a social media post, he said both sides had made progress toward a “complete and total resolution” and announced a five-day delay in planned strikes on Iran’s energy infrastructure.

However, officials in Tehran denied that any talks had taken place. Iran’s foreign ministry reiterated that its stance on the Strait of Hormuz and the conditions for ending the conflict remain unchanged.

Reports from The Wall Street Journal, citing Fars News Agency, also stated there had been no direct or indirect communication between the two sides. According to Fars, the U.S. decision to hold off on strikes came after Iran warned it would retaliate by targeting similar infrastructure across West Asia.

Trump later told reporters that the discussions had gone very well and that there was a strong possibility of reaching an agreement, though he emphasized that no outcome was guaranteed.

Meanwhile, Justin Wolfers from the University of Michigan highlighted the uncertainty facing financial markets—whether to trust U.S. statements about negotiations or Iran’s denials.

Earlier, Trump had warned that Iran must reopen the Strait of Hormuz within 48 hours or face military action. In response, Tehran threatened to shut down the waterway entirely and target key energy and water infrastructure in Gulf countries if attacked.

Bitcoin outperforms gold as geopolitical tensions and interest rate concerns weigh more heavily on the precious metal.

Bitcoin has outperformed gold and other precious metals this month since the conflict began, with bullion attracting limited demand despite rising geopolitical tensions.

Bitcoin has gained nearly 6% in March, while spot gold has dropped around 17%. The precious metal came under pressure after hitting a record high in late January, triggering profit-taking and a broader unwinding of long positions.

Even with the escalation involving Iran, gold failed to see strong safe-haven inflows, as concerns over persistent inflation and higher interest rates outweighed its appeal. In contrast, Bitcoin benefited from improving U.S. regulatory sentiment and renewed buying interest after previously falling as much as 50% from its October peak.

However, on a year-to-date basis, gold still leads, rising about 2% compared to Bitcoin’s roughly 19% decline.

Across the broader crypto market, gains followed Bitcoin’s move higher after Donald Trump’s announcement. Ethereum climbed 5.6%, while XRP rose 4.3%. Other major tokens including BNB, Solana, and Cardano also posted gains, alongside memecoins like Dogecoin.

The U.S. dollar declined on Monday, giving up earlier gains as investors reacted to President Donald Trump’s remarks about “productive” discussions with Iran. By 17:15 ET (21:15 GMT), the dollar index—measuring the greenback against six major currencies—had dropped 0.5% to 99.13.

Optimism over easing tensions spreads across global markets.

Hopes of easing tensions spread across global markets. Wall Street posted strong gains, while oil prices plunged after Trump decided to delay missile strikes on key Iranian infrastructure, citing progress in talks with Tehran. In a social media update, he said discussions aimed at achieving a “complete and total resolution” to the conflict.

Trump noted that, based on the positive tone of the talks—which are expected to continue—he had ordered the Pentagon to postpone any military action against Iranian energy facilities for five days. However, Iranian state media denied that any direct negotiations had taken place with the U.S. Officials in Tehran maintained their stance on the Strait of Hormuz and reiterated that their conditions for ending the conflict remain unchanged.

Reports from the The Wall Street Journal, citing Iran’s Fars news agency, also indicated there had been no communication between the two sides. According to Fars, the U.S. decision to step back from targeting Iranian energy sites followed warnings from Iran about potential retaliation across West Asia.

Speaking to reporters, Trump said the talks had gone “very well” and suggested there was a serious chance of reaching an agreement, though he stopped short of making any guarantees.