Google plans to increase capital expenditures to as much as $185 billion this year, significantly exceeding market expectations of around $120 billion. Robust growth in search advertising and Google Cloud has provided Alphabet with the financial flexibility to pursue this aggressive investment strategy. According to Morgan Stanley analysts, the sharp rise in spending signals that AI is driving higher engagement and improved monetisation across Google’s core businesses, with search revenue climbing 17% and cloud revenue surging 48% in the most recent quarter.

Meta conveyed a similar message after projecting annual capital expenditures of $135 billion, supported by evidence that AI is enhancing advertising effectiveness. However, not all technology giants have been able to convince investors that rising capital spending is justified. Microsoft, for example, saw its shares fall sharply—erasing more than $350 billion in market value—after its cloud performance disappointed, even as its own capital investment ramped up.

Amazon is also under pressure to sustain strong growth at AWS while continuing to expand data-center capacity. In contrast, Alphabet’s sharply rising cloud backlog highlights growing demand for AI infrastructure and tools, lending credibility to its aggressive spending plans.

The trade-off, however, is immediate. Morgan Stanley estimates that Alphabet’s free cash flow per share could decline by 58% in 2026 and by as much as 80% in 2027 as higher capital expenditures flow through the business. In effect, the company is sacrificing near-term cash returns in exchange for longer-term strategic positioning.

Alphabet now stands at a crossroads. Strong advertising and cloud growth point to early benefits from AI investments, but the sheer scale of spending increases execution risk. If the added capacity delivers sustained revenue growth, the strategy will appear well-timed. If growth slows, Alphabet could face a thinner cash buffer and heightened expectations. For now, the company is betting that leading with investment is essential to staying ahead—and the market will be watching closely to see whether returns keep pace.

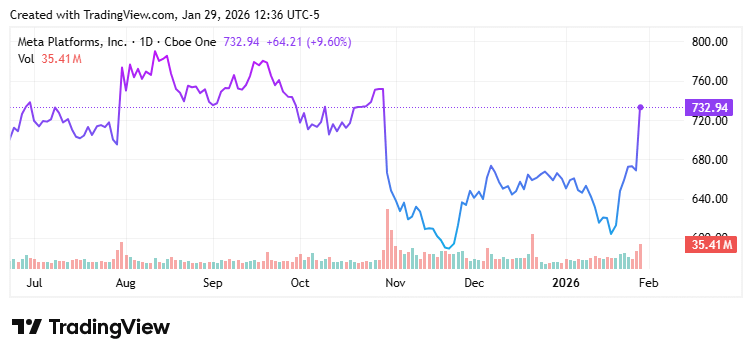

After spending months in the doldrums, Meta Platforms appears to have reshaped the narrative around its business. The Magnificent Seven stock slumped 11% in October following its third-quarter earnings release, as investors grew increasingly concerned about runaway spending on artificial intelligence.

That skepticism now looks to be fading after Meta’s fourth-quarter 2025 earnings report, released on Jan. 28. Shares climbed roughly 8% in after-hours trading by 7:00 p.m. ET, prompting investors to rethink the company’s outlook, with growth prospects increasingly overshadowing prior worries about spending.

Meta delivers strong earnings beat and upbeat guidance

In the fourth quarter, Meta reported revenue of $59.9 billion, representing growth of about 24% and comfortably exceeding expectations of $58.3 billion, or 21% growth. Adjusted earnings per share (EPS) came in at an impressive $8.88, up nearly 11% year over year and well above the consensus estimate of $8.16.

The standout highlight, however, was Meta’s guidance for the first quarter of fiscal 2026. At the midpoint, the company forecasts revenue of $55 billion, far surpassing analysts’ expectations of $51.3 billion.

This outlook implies quarterly revenue growth of roughly 30%, which would mark Meta’s fastest expansion rate since the third quarter of 2021. Such an acceleration is precisely what investors had been hoping for and offers further confirmation that the company’s investments in artificial intelligence are beginning to pay off.

Among Meta’s underlying performance metrics, growth in ad impressions delivered was particularly notable. The measure, which tracks the number of ads shown across Meta’s platforms, rose 18% during the quarter—its strongest pace in nearly two years. Chief Financial Officer Susan Li attributed this performance to robust user engagement and growth, highlighting that watch time on Instagram Reels increased 30% year over year, signaling a meaningful rise in platform engagement.

Stronger engagement is an encouraging signal for Meta, indicating that its AI-driven recommendation and ranking algorithms—responsible for determining what content users see and when—are becoming more effective. As these systems improve, users spend more time across Meta’s platforms, enabling the company to serve a greater volume of advertisements.

Markets shrug off higher-than-expected spending outlook

Expectations of sharply higher capital spending have been the key drag on Meta’s shares in recent months. Against that backdrop, the company’s latest CapEx guidance came in well above even elevated market expectations.

Meta now projects capital expenditures of $115 billion to $135 billion in 2026, compared with Wall Street estimates of roughly $110 billion. At the midpoint, this implies a 73% jump from 2025 CapEx of $72.2 billion.

In addition, Meta guided for total expenses of $162 billion to $169 billion in 2026, materially higher than consensus forecasts of around $150 billion.

Reading between the lines, however, reveals a crucial detail in Meta’s 2026 outlook. Management stated that “despite the meaningful step up in infrastructure investment, in 2026, we expect to deliver operating income that is above 2025 operating income.”

Since revenue equals operating income plus total expenses, this guidance allows for an implied revenue estimate. Meta generated $83.3 billion in operating income in 2025, and using the upper end of its 2026 expense guidance at $169 billion implies potential full-year revenue of roughly $252.3 billion.

That figure would represent about 25.5% growth from Meta’s 2025 revenue of $201 billion—well above the approximately 18.3% growth rate analysts had been projecting for 2026.

Growth eclipses spending concerns as Meta’s AI strategy gains traction

Although Meta’s expense guidance initially appeared to be the primary concern for investors, the company ultimately rose above those figures with exceptionally strong growth projections. While critics continue to argue that Meta has yet to produce a best-in-class general-purpose AI model, the company’s financial performance tells a compelling story.

Meta’s AI strategy is proving effective, driving faster growth in its core business of social media advertising. After a challenging stretch, Meta Platforms appears to have delivered precisely what was needed to restore investor confidence.