Thursday’s headline from the United States Department of Commerce showed the U.S. trade deficit widening sharply to $70.3 billion in December and reaching $901.5 billion for full-year 2025. December imports jumped 3.6% to $357.6 billion, while exports fell 1.7% to $287.3 billion. Economists had projected a $55.8 billion gap, making the release a significant downside surprise that prompted many to cut fourth-quarter GDP forecasts. Following the data, the Federal Reserve Bank of Atlanta lowered its Q4 GDP estimate to 3% from 3.6%.

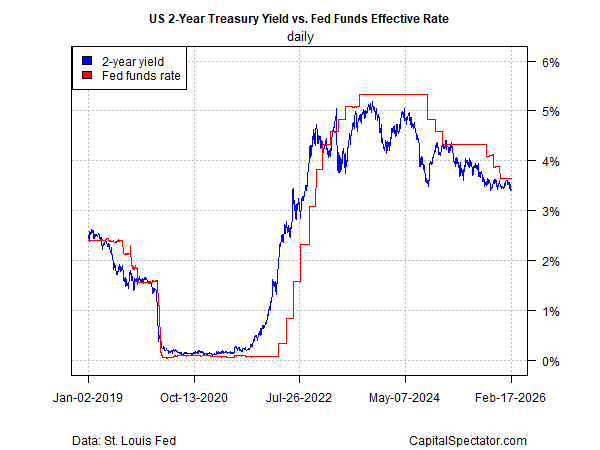

The Commerce Department’s preliminary report showed the economy expanded at just a 1.4% annualized pace in Q4, well below the 2.8% consensus estimate. Federal government spending dropped 16.6% during the quarter — largely due to the shutdown — subtracting roughly one percentage point from growth. The wider trade deficit further weighed on output. For all of 2025, GDP rose 2.2%. Treasury yields drifted lower after the report, increasing expectations that the Federal Reserve may move toward another rate cut.

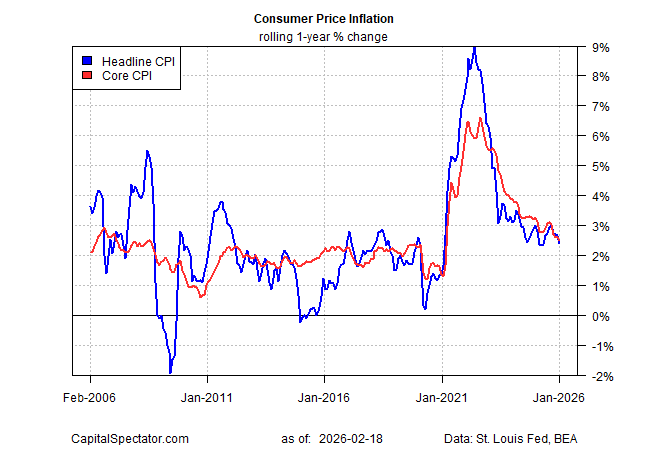

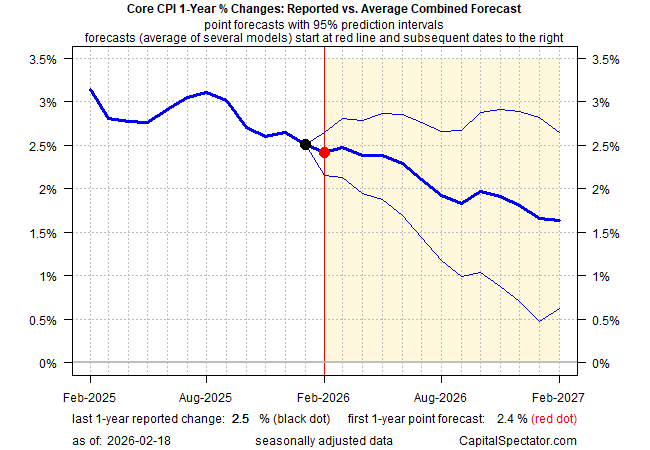

One potential obstacle to near-term easing is inflation. The Personal Consumption Expenditures (PCE) index rose 0.4% in December and 2.9% year-over-year. Core PCE, excluding food and energy, also climbed 0.4% on the month and 3% annually. On a positive note, consumer spending advanced 0.4% in December, offering some support for future growth momentum.

In financial markets, private credit came under scrutiny after Blue Owl Capital permanently restricted redemptions from one of its retail vehicles, Blue Owl Capital Corp II. The move triggered declines in alternative asset managers including Ares Management, Apollo Global Management, KKR, Blackstone, and TPG. Adding to concerns, BlackRock recently marked down portions of its private credit portfolio. Former PIMCO CEO Mohamed El-Erian publicly questioned whether this could signal a broader stress point for the sector.

In a separate development, The Wall Street Journal reported that President Donald Trump ordered the release of government files related to UFOs and unidentified aerial phenomena following heightened public interest. The directive reportedly came after comments by former President Barack Obama referencing extraterrestrial topics. Christopher Mellon, who previously helped publicize the “Tic Tac” military footage, suggested the move could have far-reaching implications.

Taken together, the combination of a widening trade deficit, softer GDP growth, persistent inflation, and emerging private credit strains presents a complex macro backdrop — one that leaves markets balancing expectations of further rate cuts against lingering structural risks.

Sources: Louis Navellier