GBP/USD extended its advance for a fourth straight session, hovering near 1.3510 in Wednesday’s Asian trading. The pair is benefiting from continued softness in the US Dollar after US President Donald Trump delivered the first State of the Union address of his second term before a joint session of Congress.

Technical Analysis

GBP/USD continues to draw support near the 200-period Simple Moving Average (SMA) on the four-hour chart, around the 1.3550 area, which now serves as an important short-term pivot. The MACD histogram remains in negative territory, reflecting that the MACD line is still below the Signal line near the zero threshold. Meanwhile, the RSI stands at 40 — leaning neutral-to-bearish — after bouncing from earlier lows, indicating that upside moves may lack strong conviction.

As long as price holds above the upward-sloping 200-period SMA, the near-term bias remains constructive. However, a decisive break back below this level would tilt momentum in favor of sellers. A turn of the MACD histogram into positive territory would signal easing bearish pressure. For a stronger recovery outlook, the RSI would need to climb back above 50; remaining below that mark would likely keep rallies contained and shift focus toward consolidation rather than a sustained advance.

Fundamental Analysis

The GBP/USD pair edges lower for a second consecutive session on Tuesday, sliding to its weakest level in over a week — around the mid-1.3500s — during early European trading after the release of the UK labor market data.

Figures from the UK Office for National Statistics showed the ILO unemployment rate rose to 5.2% in the three months to December, up from 5.1% previously and marking the highest reading since early 2021. Meanwhile, jobless claims increased by 28.8K in January, signaling further softening in the labor market at the start of 2026.

Wage growth also cooled notably. Average Earnings Excluding Bonus rose 4.2% in the three months to December, easing from 4.6% in the prior quarter and hitting the slowest pace in nearly four years. Earnings Including Bonuses likewise slowed to 4.2% from 4.6%. Unless UK inflation data due Wednesday delivers an upside surprise, the latest employment figures reinforce expectations that the Bank of England could cut rates as soon as March, adding pressure on the British Pound.

At the same time, the US Dollar strengthens to a one-week high, further weighing on GBP/USD. However, the greenback’s upside appears limited by dovish Federal Reserve expectations. Following softer US inflation data last Friday, markets increased bets that the Fed may begin easing policy in June. Current pricing suggests at least two rate cuts in 2026, and lingering concerns about the Fed’s independence also restrain bullish USD momentum.

With traders hesitant to take aggressive positions ahead of clearer guidance on the Fed’s path, attention now shifts to the FOMC Minutes on Wednesday and the US Personal Consumption Expenditure (PCE) Price Index on Friday. These releases will be pivotal for shaping expectations around US monetary policy and, in turn, the direction of the dollar. Additionally, Wednesday’s UK CPI report could inject fresh volatility into GBP/USD as the week progresses.

Macro uncertainty is intensifying just as EUR/USD and GBP/USD test pivotal technical zones. With interest-rate expectations shifting and tail risks mounting, the next directional move may depend more on macro catalysts than chart patterns.

Both pairs are hovering near critical support and resistance levels, while a dense lineup of U.S. and European data raises the prospect of increased volatility. The dollar continues to trade in close correlation with Treasury yields and evolving Federal Reserve rate pricing, reinforcing the macro-driven backdrop.

At the same time, tariff developments and geopolitical tensions are injecting additional tail risk ahead of the weekend, leaving markets vulnerable to sharp, sentiment-driven swings.

Summary

As the week moves into its final stretch, both Europe and the United States face a heavy slate of economic releases—and this is unlikely to be mere background noise for markets. Recent price action has already underscored how reactive EUR/USD and GBP/USD are to changes in relative rate expectations across the U.S., U.K., and euro area.

With both currency pairs now positioned near critical technical thresholds, the incoming data flow carries the potential to do more than simply inject volatility. It may ultimately determine whether the latest directional moves gain traction—or begin to lose momentum and reverse.

Heavy Data Calendar Lifts Volatility Threat

Flash PMIs rarely fail to generate movement in EUR/USD and GBP/USD, largely because European participants tend to respond far more decisively to the releases than traders elsewhere. In the euro area, the focus is likely to center on price components and new orders, especially in light of the recent resilience in the single currency. In the UK, attention may gravitate toward price pressures, employment trends, and overall activity, reflecting the economy’s persistent softness.

The more consequential headline risk, however, lies in the United States. The advance Q4 GDP print stands out. While backward-looking and heavily estimate-based, it still carries the potential to influence how the dollar closes the week. An upside surprise would reinforce the narrative of U.S. exceptionalism. A downside miss, on the other hand, could reignite expectations for Federal Reserve rate cuts—expectations that have recently been scaled back after generally firm data and relatively hawkish FOMC minutes.

December’s core PCE deflator rarely delivers genuine surprises these days. Enhanced data mapping has largely diminished its shock factor, shifting attention toward the consumption and income components instead. Markets will scrutinize the consumption data for signs that recent weakness in goods demand has spilled into services, while income figures should provide a clearer indication of households’ capacity to sustain spending.

US flash PMIs, meanwhile, have produced inconsistent market reactions and are often overshadowed when more significant releases land on the same day. Broadly speaking, they have tended to exaggerate the signal seen in ISM surveys. As a result, a stronger market response may emerge if there are clear signs of softening—particularly within the services sector.

Weekend Risk Premium Builds

Beyond the dense data schedule, traders also face mounting tail risks heading into the weekend. A ruling from the Supreme Court of the United States on the legality of tariffs imposed under the International Emergency Economic Powers Act (IEEPA) could arrive around 10 a.m. U.S. time, although there is no certainty a decision will be issued today. Even the possibility is sufficient to keep markets cautious, given the potential implications for Treasury yields and overall risk sentiment.

At the same time, Donald Trump has set a 10-day deadline for Iran to reach a deal or face potential military action. Considering the risks to global energy supply—and the United States’ position as a major energy producer—any pre-emptive strike would likely support the dollar against European currencies, particularly if it sparks a renewed wave of risk aversion.

Regarding tariffs, the market reaction may remain relatively muted regardless of the court’s decision—unless investors begin to question whether any shortfall in government revenues can be covered through alternative channels. Should doubts arise on that front, both the dollar and longer-dated Treasuries could face meaningful downside pressure as fiscal concerns move to the forefront.

Dollar Catalysts Return to Center Stage

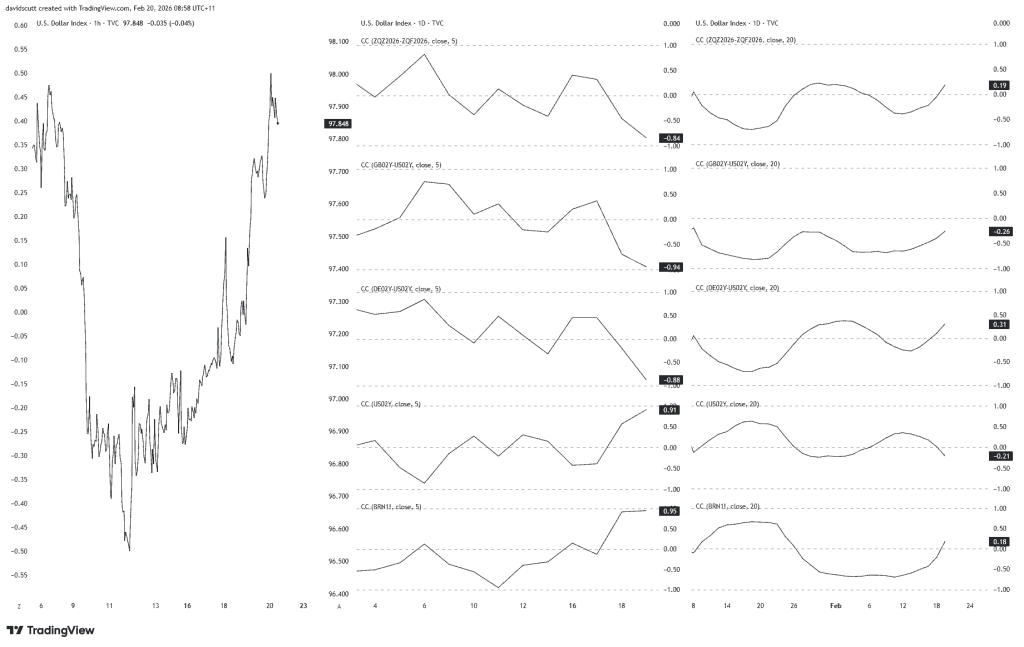

Underscoring the significance of the upcoming data and event risk, the US Dollar Index (DXY) has shown a notably tight correlation over the past week with Fed rate-cut expectations, front-end yield differentials, US two-year Treasury yields, and even Brent crude, as illustrated in the middle panel of the chart above. In practical terms, the dollar has reverted to trading primarily as a rates-and-yields narrative, with an added layer of sensitivity to energy prices.

Yet the 20-day correlation metrics shown on the right paint a much less compelling picture. Over the past month, these relationships have been weak and statistically insignificant, serving as a reminder that the recent alignment may prove temporary rather than structural.

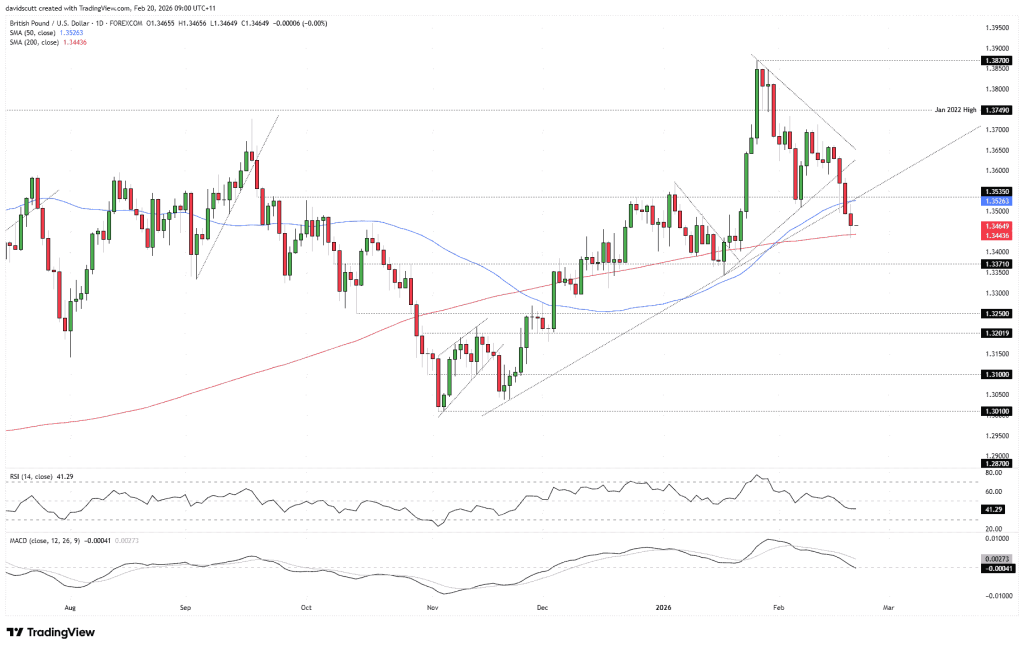

GBP/USD Faces Growing Downside Pressure

As discussed in earlier analysis this week, the release of key UK labour market and inflation figures acted as the catalyst that pushed GBP/USD out of its consolidation phase. Combined with firm U.S. data, the move triggered a decisive break below multiple technical markers, including the November uptrend and the 50-day moving average, before finding support at the 200-day moving average. Whether assessed through pure price action or momentum indicators, the bias now tilts toward increasing downside risk.

The 14-period RSI continues to trend lower below the 50 mark, while MACD has crossed beneath its signal line and moved into negative territory—both reinforcing the build-up of bearish momentum. As a result, selling rallies appears more favorable than buying dips. That said, the pair’s proximity to the 200DMA provides a clearly defined reference point for structuring trades as incoming data and headlines shape sentiment.

A sustained break below the 200DMA would strengthen the bearish case, opening the door for short positions with stops placed just above the average. Initial downside targets would sit at 1.3371, followed by 1.3300 and 1.3250. Conversely, if price manages to hold above the 200DMA, the setup could shift tactically. Long positions above the level, with stops placed beneath, would target 1.3535—a zone where several technical indicators, including the 50DMA, currently converge. A reclaim of that area would undermine the newly established bearish bias and shift directional risks back toward a sideways-to-higher outlook.

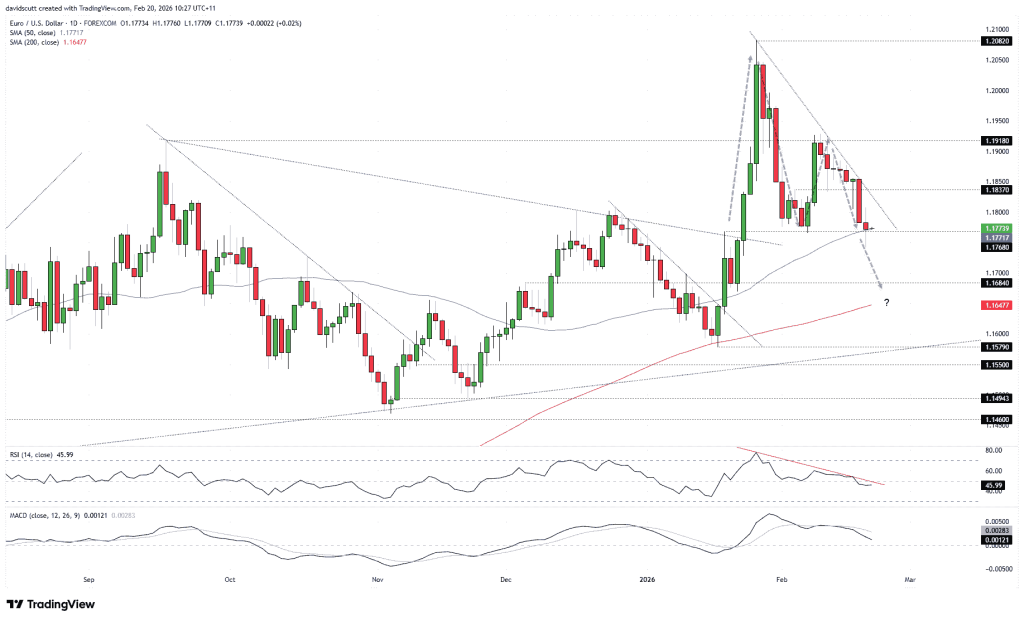

Triangle Formation Brings Breakout Levels Into View

With EUR/USD coiling within a descending triangle and momentum indicators drifting lower, downside risks appear to be gradually building. A decisive break beneath the confluence of the 50-day moving average and horizontal support at 1.1768 may prove pivotal in unlocking further weakness. Thursday’s doji candle aligns with that narrative, highlighting a degree of indecision among market participants at a technically sensitive juncture.

While the bearish case in GBP/USD looks more straightforward—given recent UK data and the repricing of Bank of England rate expectations—the outlook for the euro is less clear-cut. That ambiguity reinforces the importance of upcoming data and headlines in shaping near-term direction. RSI (14) has slipped just below 50, offering a neutral-to-soft signal, while MACD has rolled over but remains marginally above zero, underscoring the lack of decisive momentum so far.

The descending triangle structure keeps the downside break scenario firmly in focus, but confirmation is still required. A sustained break and close below the 50DMA/1.1768 area would strengthen the bearish case, with short positions targeting 1.1684 initially, followed by the 200-day moving average. Stops could be placed just above the broken support zone for protection.

Conversely, if the pair manages to hold this confluence area, a tactical long setup may be considered with tight stops below, initially targeting the January downtrend line. Should price test but fail to clear that trendline convincingly, it may favor squaring positions or re-establishing shorts with stops above, aiming for a retest of the 50DMA/1.1768 region. A clean upside breakout, however, would alter the landscape, opening scope toward 1.1837 and potentially 1.1918, shifting directional risks back toward a sideways-to-higher bias.

The United Kingdom is set to release its preliminary February Purchasing Managers’ Index (PMI) figures, with the data scheduled to be published by S&P Global on Friday at 09:30 GMT.

The Services PMI is forecast at 53.6, slightly lower than January’s reading of 54.0, signaling a modest slowdown in services sector growth.

Potential Impact on GBP/USD

If the Services PMI prints in line with expectations, GBP/USD could face pressure, as a softer services reading may counterbalance the recent strength seen in UK Retail Sales.

UK Retail Sales rose 1.8% month-over-month in January, well above December’s 0.4% gain and surpassing the 0.2% market forecast. Core Retail Sales increased 2.0% over the same period, improving from a 0.3% rise previously and exceeding expectations for a 0.2% uptick.

However, the pair may remain under strain as the US Dollar stays firm following the release of the January meeting minutes from the Federal Open Market Committee. The minutes revived speculation that the Federal Reserve could consider further rate hikes if inflation proves persistent. Although most officials favored holding rates steady, only a minority supported a cut, and policymakers suggested easing could be appropriate if inflation slows as projected.

From a technical standpoint, GBP/USD has stabilized after rebounding from daily losses, hovering near 1.3460 at the time of writing. Daily chart analysis points to a developing bearish tone, with the pair trading below an ascending channel formation. Immediate support is located near the two-month high of 1.3344. On the upside, resistance is seen at the 50-day EMA around 1.3524, followed by the nine-day EMA near 1.3548.

The Bank of England held its policy rate at 3.75%, but the decision revealed a notably divided committee, with four of the nine members voting in favor of another cut. This close split has reinforced expectations for a rate reduction as soon as March, particularly as inflation continues to ease and wage growth shows signs of cooling.

The BoE now estimates that wage growth consistent with its 2% inflation target is roughly 3.25%, only slightly below current private-sector pay growth of about 3.6%. With inflation projected to fall toward 1.8% by April, the central bank appears increasingly comfortable with the prospect of further policy easing.

Governor Andrew Bailey remains a pivotal swing vote, and if upcoming data confirms a softer labor market and moderating pay growth, he is widely expected to back a rate cut at the next meeting. Markets are already pricing in additional easing through the summer months.

GBP/USD Technical Perspective

GBP/USD has been trending lower, reflecting expectations of Bank of England rate cuts and a broadly dovish policy outlook.

On the four-hour chart, the pair continues to trade within a well-defined descending channel, currently hovering around 1.3536. This structure indicates that sellers remain in control for the time being.

That said, a notable support zone sits near 1.34, aligning with a previous accumulation area. A break lower within the channel could see price gravitate toward that level.

Conversely, a move above the upper boundary of the channel would signal a shift in momentum and could open the door to a rebound toward the 1.37–1.38 area in the near term.

Summary:

Trend: Bearish, within a descending channel

Support: 1.34

Resistance: 1.37–1.38

Key Catalyst: March Bank of England policy meeting

ECB Remains Comfortably on Hold

The European Central Bank left interest rates unchanged, signaling confidence that the eurozone economy remains in a solid position. Inflation is tracking close to the 2% target, growth is stable, and there is little immediate need to either tighten or ease policy.

That said, past experience suggests the ECB is willing to resume rate cuts after extended pauses if conditions evolve. A meaningful appreciation in the euro or a dip in inflation below target could prompt policymakers to consider a modest “insurance cut” later in the year to guard against undershooting inflation.

For now, however, the ECB appears comfortable remaining on hold, a stance that has translated into relatively calm market conditions.

EUR/USD Technical Perspective

EUR/USD continues to consolidate in a narrow range between 1.1780 and 1.1840, reflecting the ECB’s steady policy stance and a broader lack of directional conviction. Volatility remains subdued, underscoring ongoing market indecision.

A renewed move lower could develop if expectations build around further ECB easing, or if euro strength becomes a concern for policymakers. Until a clear catalyst emerges, price action is likely to remain range-bound, with consolidation dominating near-term trading.

Summary:

Trend: Sideways / range-bound

Range: 1.1780–1.1840

Downside risk: A decisive break below 1.1780 would expose a move toward 1.1700

Catalyst: Shift in ECB tone or renewed concerns over excessive euro strength

In short:

The BoE’s dovish stance is pressuring the pound, leaving GBP/USD biased lower.

The ECB’s steady, wait-and-see approach is keeping the euro supported, though excessive euro strength could revive rate-cut speculation.

With both central banks leaning dovish, the next meaningful FX moves are likely to be driven by shifts in rate expectations, not policy surprises.

UK retail sales increased by 0.4% month-on-month in December, rebounding from a 0.1% decline in November, according to data released Friday by the Office for National Statistics.

Markets had expected retail sales to fall by 0.1% during the month. Core retail sales, which exclude auto fuel, rose 0.3% month-on-month in December, reversing a revised 0.4% decline previously reported. The reading exceeded market expectations for a 0.2% fall.

On an annual basis, UK retail sales increased 2.5% in December, up from a revised 1.8% previously and above the consensus forecast of 1.0%. Annual core retail sales also strengthened, climbing 3.1% compared with a revised 2.6% gain earlier, outperforming expectations of a 1.4% rise.

Market response to the UK Retail Sales data

The positive UK Retail Sales report has failed to lift the Pound Sterling, with GBP/USD down 0.06% on the day, trading at 1.3488 at the time of writing.

The following section was published on January 23 at 5:11 GMT as a preview of the UK Retail Sales report.

Overview of UK Retail Sales

The UK calendar features the release of the December Retail Sales figures from the Office for National Statistics (ONS) on Friday at 07:00 GMT.

Retail Sales are forecast to edge down by 0.1% month-on-month in December, following an identical 0.1% decline in November. On a yearly basis, sales are expected to increase by 1%, slightly higher than the previous 0.6% rise.

Core Retail Sales, which exclude motor fuel, are also projected to slip by 0.2% MoM, in line with the prior reading, while annual growth is anticipated to improve to 1.4% from 1.2% in November.

How might UK retail sales influence the GBP/USD exchange rate?

The GBP/USD pair could show little reaction even if UK Retail Sales for December exceed expectations, as markets largely anticipate the Bank of England to maintain a cautious, gradual easing stance despite stronger price pressures seen in December. Attention is likely to shift instead to the preliminary January S&P Global PMI readings from both the UK and the US, scheduled for release later in the day.

Sterling may find support if the US Dollar weakens amid rising risk aversion linked to geopolitical tensions. Earlier, US President Donald Trump threatened tariffs on European nations opposing his Greenland initiative, but later eased his stance after reaching a NATO framework agreement that opened the door to a potential deal.

From a technical perspective, GBP/USD is holding firm after climbing more than 0.5% in the previous session, hovering near the 1.3500 level at the time of writing. The pair could aim for the three-month peak at 1.3562 as the next resistance. On the downside, initial support is seen at the nine-day EMA around 1.3451, followed by the 50-day EMA near 1.3398.

GBP/USD inched up to around 1.3430 during Monday’s early European session.

The market remains cautious as federal prosecutors launch a criminal investigation into Fed Chair Powell.

With the RSI lingering near the midline, further consolidation is possible in the short term.

Key support to watch is at 1.3358, while immediate resistance is seen near 1.3458.

The GBP/USD pair found some buying interest around 1.3430 during Monday’s early European trading session. The US Dollar weakened against the British Pound following Federal Reserve Chair Jerome Powell’s revelation that President Donald Trump threatened him with a criminal indictment, sparking concerns about the Fed’s independence.

The US Justice Department issued subpoenas and threatened criminal charges linked to Powell’s Senate testimony regarding renovations at Federal Reserve buildings. Powell described the investigation as “unprecedented” and suggested it was motivated by Trump’s frustration over his refusal to lower interest rates despite the president’s repeated public pressure.

Ray Attrill, head of currency strategy at National Australia Bank, commented, “This open conflict between the Fed and the U.S. administration clearly doesn’t bode well for the U.S. dollar.”

Traders will be paying close attention to UK jobs data due Tuesday, as the results could provide insights into market expectations for the Bank of England’s monetary policy. Weaker-than-expected figures might put short-term pressure on the British Pound (Cable).

GBP/USD Technical Analysis

On the daily chart, the 100-day EMA is trending upward, offering support at 1.3358, with the price maintaining above this key moving average to sustain the broader bullish outlook. The RSI at 51.90 is neutral but trending slightly higher, indicating momentum is stabilizing following a recent pullback. Holding above the EMA could set the stage for a retest of resistance at 1.3458, preserving the recovery trend.

The price currently trades just below the Bollinger Bands’ middle line at 1.3458, with the bands narrowing, signaling lower volatility and a consolidation phase. The RSI near 52 confirms a range-bound environment. A decisive move above the mid-band would increase upward momentum, potentially targeting the upper band at 1.3552. Conversely, a drop toward 1.3365 would bring the lower band into focus, risking a deeper correction.