HSBC Asset Management said gold and silver posted dramatic price swings in 2025, fueled by geopolitical risks and worries about the Federal Reserve’s independence, before evolving into a retail-driven speculative phase. Analysts caution that leveraged selling could increase their correlation with equities, but note that central bank de-dollarisation efforts and crisis-related demand continue to support the long-term structural case for precious metals.

Safe-haven demand weighed against speculative flows

“This year’s moves in gold and silver have been extraordinary. Sparked by geopolitical tensions and concerns over the Federal Reserve’s independence, the 2025 rally morphed into a retail-driven speculative surge, making a correction increasingly probable.

So where does that leave investors who rely on gold as a portfolio diversifier? Although retail inflows lifted returns, they also brought equity-like volatility — at odds with gold’s traditional safe-haven role.

That said, recent turbulence shows that no safe haven is perfect, reinforcing the case for ‘diversifying the diversifiers’: taking an active, multi-asset approach to seek uncorrelated returns across a wide range of assets.”

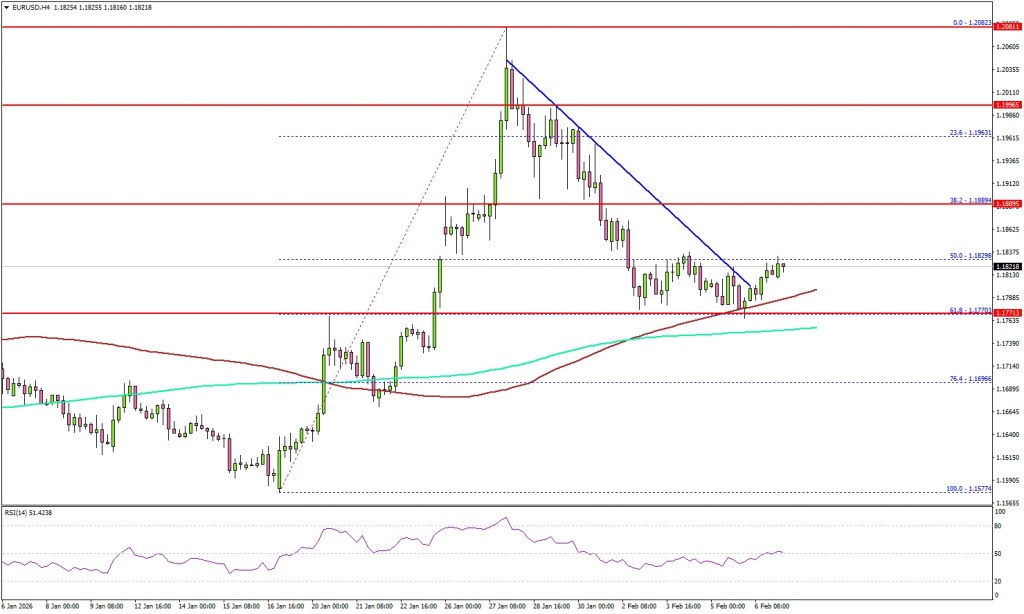

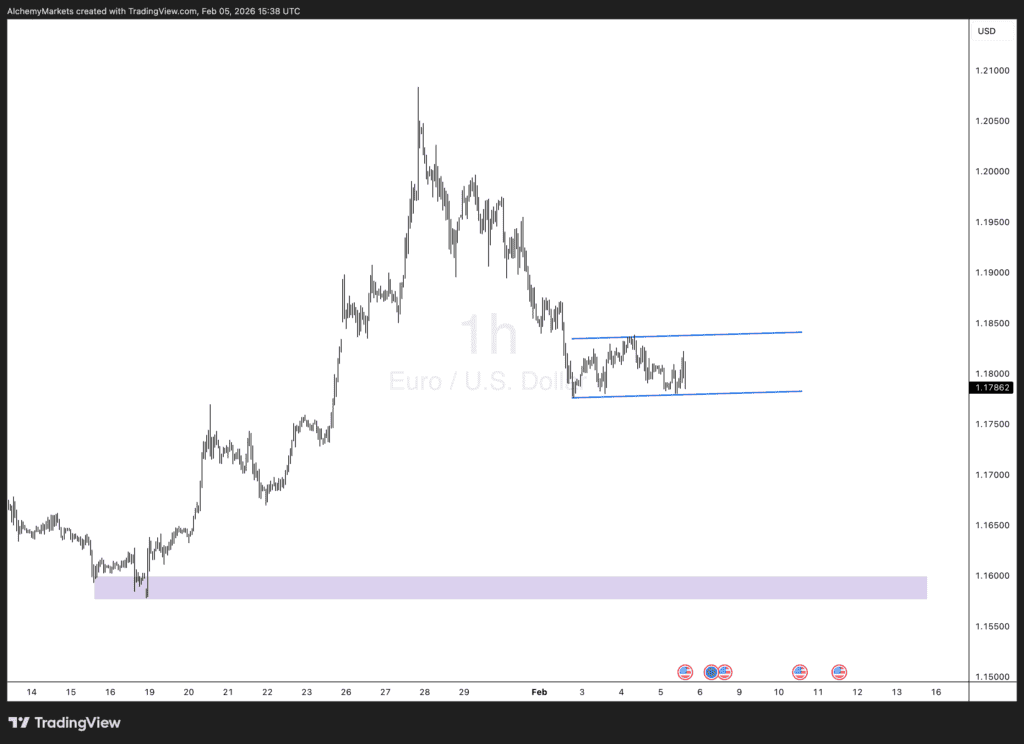

EUR/USD slipped below 1.1900 and tested support near 1.1780.

The pair broke above a key bearish trend line, previously acting as resistance around 1.1810 on the 4-hour chart.

EUR/USD technical analysis

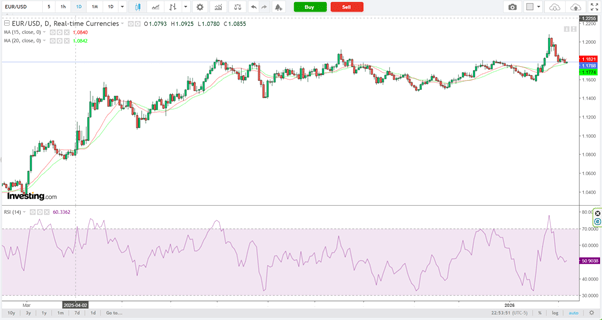

On the 4-hour chart, EUR/USD tested the 61.8% Fibonacci retracement of the advance from the 1.1577 swing low to the 1.2082 peak. The pair has held above both the 100-period (red) and 200-period (green) simple moving averages, signaling underlying support.

The pair is stabilizing above 1.1780 and has recently cleared the bearish trend line near 1.1810. On the upside, initial resistance is seen around 1.1850, followed by 1.1890. A sustained close above 1.1890 could pave the way for further gains toward 1.1920, with a potential extension toward the 1.2000 handle.

On the downside, immediate support remains at 1.1780. A deeper pullback could test the 1.1720 area, while the key support level lies at 1.1700. A break below this zone would likely shift momentum in favor of the bears and could expose the 1.1650 region.

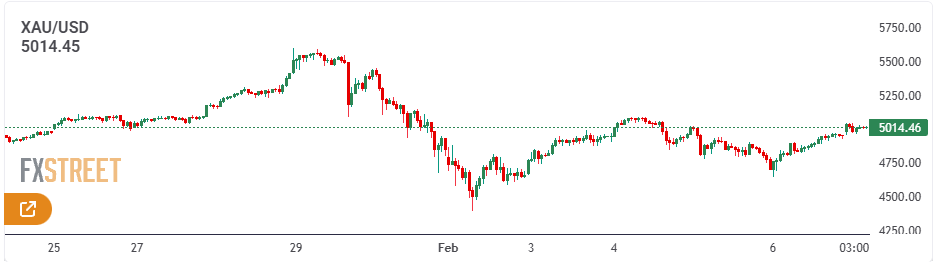

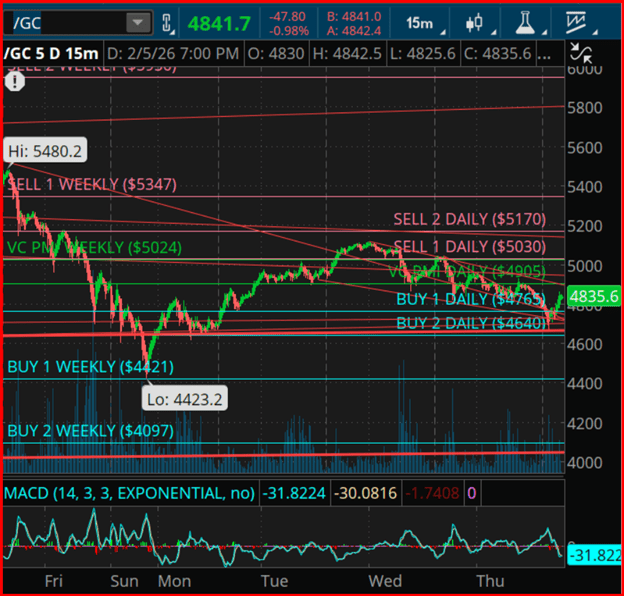

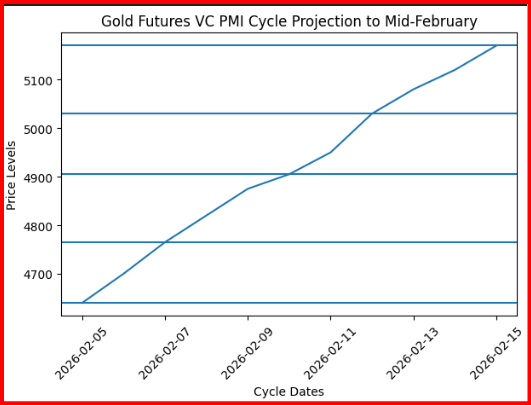

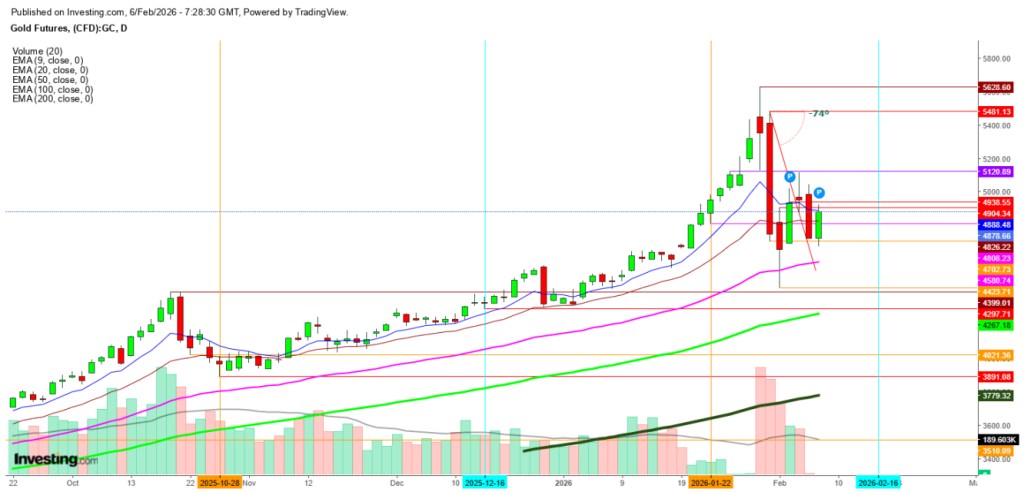

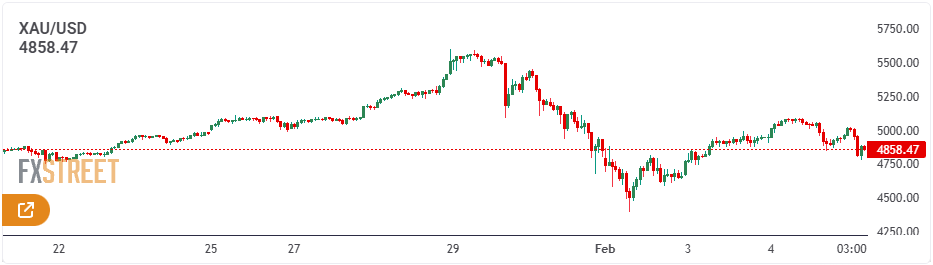

Gold is consolidating recent gains around the $5,000 level, with buyers gradually building momentum for a potential sustained uptrend as a pivotal week gets underway. Market attention is firmly on the delayed U.S. Nonfarm Payrolls report due Wednesday and the Consumer Price Index data scheduled for release on Friday.

Fundamental Analysis

As the new, data-heavy week begins, dovish sentiment surrounding the U.S. Federal Reserve is setting the tone, with renewed reflation trades helping gold extend Friday’s strong rebound from the $4,650 area.

After last week’s weak U.S. labor data, markets have continued to price in the first Fed interest-rate cut as early as June, even as investors remain divided over the likely policy stance of Fed chair nominee Kevin Warsh.

Risk appetite has also been supported by a resurgence in reflationary trades, sparked by Japan’s ruling Liberal Democratic Party securing a decisive majority in snap elections. The outcome has reinforced expectations of debt-funded fiscal stimulus, further underpinning the broader reflation theme.

Adding to gold’s support, the U.S. dollar has softened amid renewed weakness in USD/JPY following strong verbal intervention from Japanese authorities. The resulting dollar pressure has helped keep the precious metal buoyant.

That said, gold’s recovery momentum appears somewhat constrained as overall risk sentiment remains upbeat on expectations of expansionary fiscal policies in Japan. Japanese equity markets have surged to record highs, lifting broader Asian stocks and reducing demand for traditional safe havens.

Looking ahead, it remains uncertain whether gold can sustain its rebound, as traders may grow more cautious and adjust positions ahead of Wednesday’s closely watched U.S. January jobs report.

XAU/USD Technical Overview

On the daily chart, XAU/USD is trading around $5,023.88, with the technical structure firmly tilted to the upside. The 21-day Simple Moving Average (SMA) has crossed above the 50-, 100-, and 200-day SMAs, and all are sloping higher, highlighting a strong and well-established bullish trend. Prices remain comfortably above these moving averages, keeping buyers in control.

Momentum indicators also support the constructive outlook. The Relative Strength Index (RSI) is at 57.72, holding above the neutral 50 level and well below overbought territory, suggesting steady positive momentum without signs of exhaustion. Immediate dynamic support is provided by the rising 21-day SMA at $4,873.06.

This bullish alignment implies that any pullbacks are likely to be limited as long as prices stay above the faster moving average. A daily close below the 21-day SMA would signal a deeper corrective move, potentially exposing the 50-day SMA near $4,563.97. For now, the continued rise in medium- and long-term SMAs favors a buy-on-dips approach and keeps the broader trend firmly pointed higher.

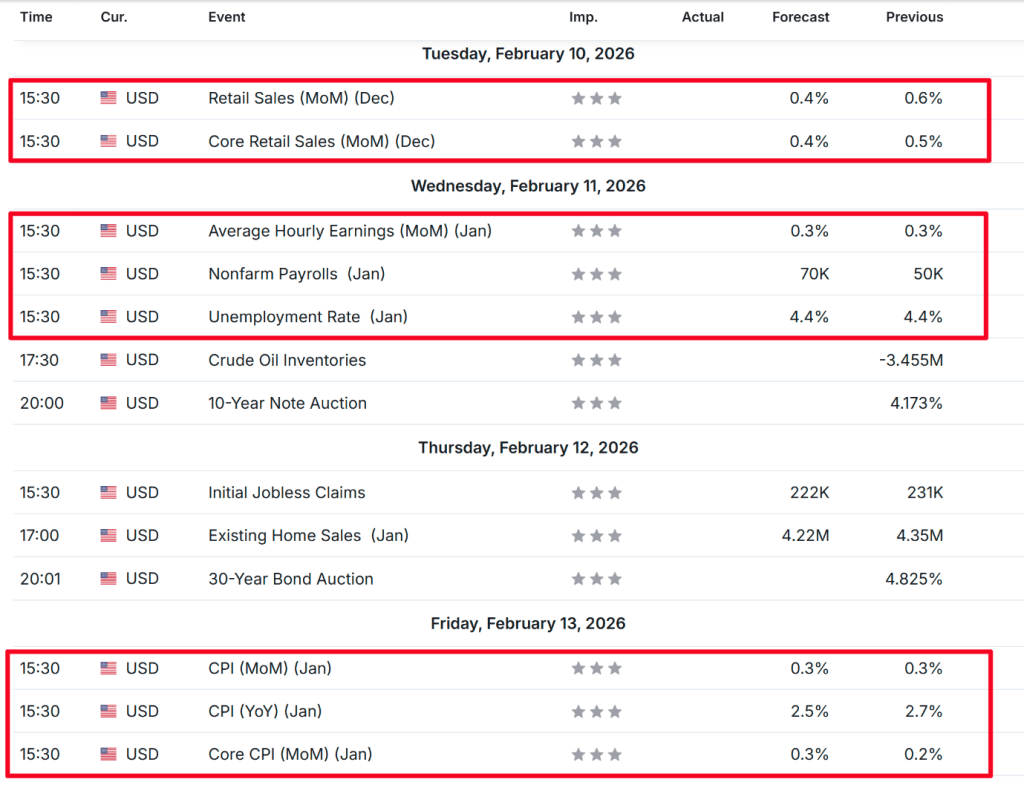

Key U.S. economic data—including the jobs report, CPI inflation, retail sales—and another round of corporate earnings will be in focus this week.

Cisco is expected to post strong earnings along with upbeat guidance, positioning the stock as a high-conviction potential outperformer in the near term.

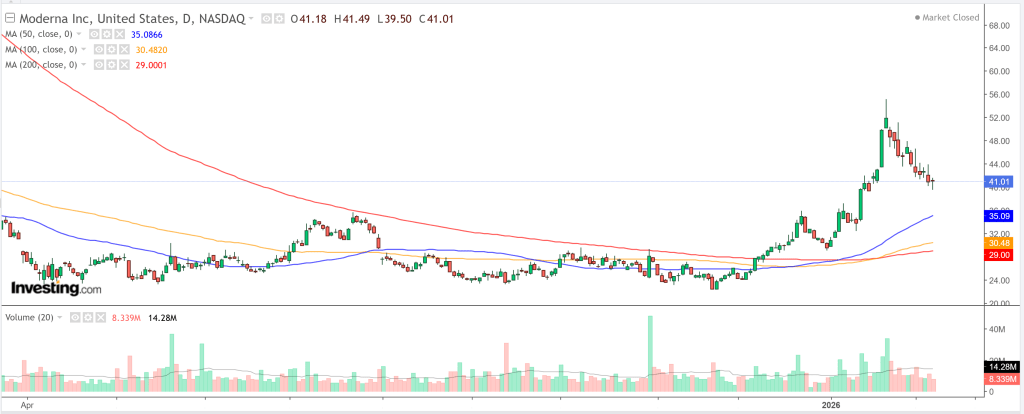

By contrast, Moderna faces pressure from declining revenue and anticipated losses, leaving the stock vulnerable to downside risk this week.

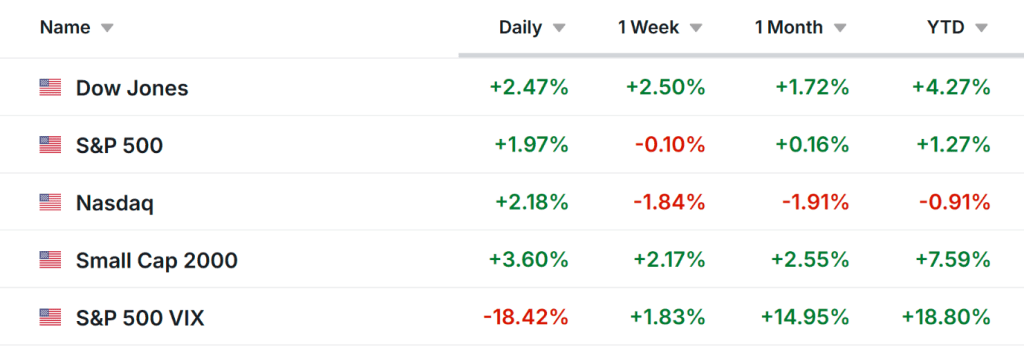

Wall Street stocks surged on Friday, posting their strongest gains in months as the Dow Jones Industrial Average finished above the landmark 50,000 level for the first time.

The rally came after three consecutive sessions of declines driven by artificial intelligence-related concerns, with software stocks particularly pressured on fears that AI could intensify competition across the sector.

For the week, the benchmark S&P 500 and the tech-heavy Nasdaq Composite edged lower by 0.1% and 1.8%, respectively, while the 30-stock Dow Jones Industrial Average gained 2.5% and the small-cap Russell 2000 advanced 1.8%.

Volatility may remain elevated in the days ahead as investors weigh the outlook for economic growth, inflation, interest rates, and corporate earnings.

On the economic front, delayed December retail sales data is set for release on Tuesday. However, Wednesday’s postponed January U.S. jobs report could prove more influential amid mounting concerns over labor-market conditions. January CPI inflation data due on Friday will also be closely watched for further evidence on whether price pressures are truly easing.

Earnings season also rolls on, with a busy slate of high-profile results due in the coming days. Notable reports include Coca-Cola, McDonald’s, Ford, Cisco, Robinhood, Coinbase, and Arista Networks, alongside key software names such as AppLovin, Shopify, and Datadog.

Regardless of broader market direction, below I highlight one stock that is likely to attract buying interest and another that could face renewed downside pressure. Note that this view is strictly short term, covering the week ahead from Monday, February 9 through Friday, February 13.

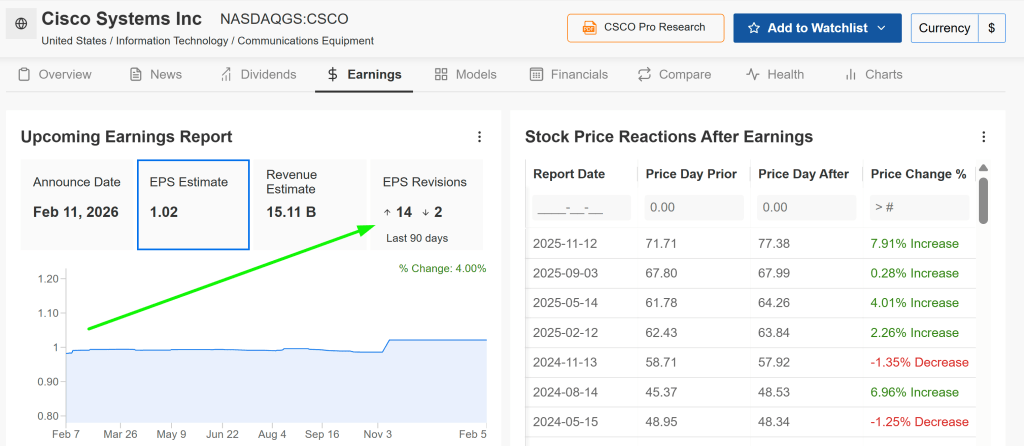

Stock To Buy: Cisco

Cisco’s upcoming earnings report is the key catalyst for the stock this week, with the risk–reward profile appearing skewed to the upside. CSCO is set to report fiscal second-quarter results after the market closes on Wednesday at 4:05 p.m. ET.

Market expectations remain relatively modest, suggesting that even a small beat on revenue and earnings per share, coupled with steady or slightly optimistic guidance, could be enough to spark a post-earnings rally.

Analyst sentiment has been notably constructive heading into the release. According to InvestingPro data, 14 of the last 16 EPS revisions have been upward, underscoring growing confidence in Cisco’s ongoing expansion.

As a leading player in networking hardware, cybersecurity, and an increasingly important provider of AI infrastructure, Cisco is well positioned to capitalize on multiple tailwinds that could support a strong quarterly performance despite a mixed macroeconomic backdrop.

Consensus forecasts call for adjusted earnings per share of $1.02, representing a 9% increase from a year earlier. Revenue is expected to rise 8% year over year to $15.1 billion, supported by AI-driven demand and solid product sales.

Analysts see potential for longer-term upside from Cisco’s partnership with Nvidia to develop AI networking solutions for the enterprise market. Meanwhile, Cisco’s security segment underperformed in fiscal first quarter results despite the acquisition of Splunk, and investors will be watching closely for signs of a rebound in that business.

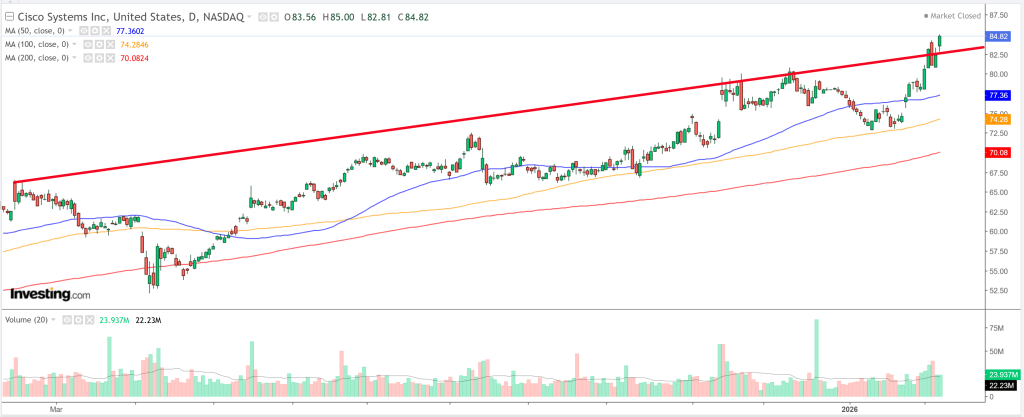

Cisco’s shares have been on a strong run, notching a string of fresh 52-week highs in recent sessions. The stock closed at $84.82 on Friday, underscoring solid momentum heading into the earnings release.

Valuation and sentiment also remain supportive. Cisco continues to trade at a reasonable earnings multiple relative to both the broader technology sector and its own historical averages, while offering an appealing dividend yield underpinned by robust free cash flow.

Trade setup:

Entry: Near current levels (~$84–85)

Target: $90–$95 (potential upside of ~5.8%–10.8%)

Stop-loss: $80 (downside risk of ~5.8%)

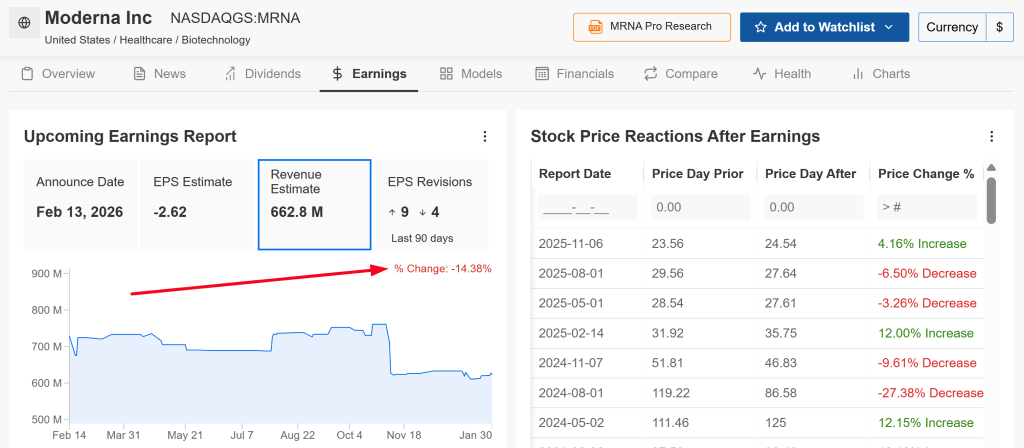

Stock To Sell: Moderna

Moderna, meanwhile, faces a tougher setup this week as it heads into its fourth-quarter earnings release scheduled for before Friday’s opening bell at 6:35 a.m. ET. Options markets are pricing in a sharp post-earnings swing of around ±16%, underscoring the heightened risk of a downside surprise.

After its blockbuster pandemic-era success with the mRNA COVID-19 vaccine, the biotech company has struggled with the transition from reliance on a single product to a broader—yet still largely unproven—development pipeline.

Analyst sentiment has turned increasingly cautious ahead of the report, with consensus sales estimates cut by roughly 14%, reflecting growing concerns over Moderna’s near-term revenue outlook.

Consensus expectations point to a sizable loss, with earnings per share projected at around –$2.62 on revenue of $662.8 million, representing a steep year-over-year decline of more than 30% from sales of $966 million.

Moderna is grappling with slowing revenue growth and a lack of near-term catalysts to counter weakening demand, as vaccine sales continue to fade.

At the same time, the company must maintain elevated spending on research, development, and manufacturing to advance a broad pipeline spanning respiratory viruses, oncology, and other therapeutic areas. This combination is weighing on near-term profitability and increasing pressure on cash burn.

Moderna’s share price has started to lose momentum after a strong recent rally, ending Friday at $41.01. While the stock remains up 67.1% over the past three months and 21.1% in the last month, last week’s 7% decline points to waning upside traction.

In a market increasingly favoring growth and AI-linked themes, high-beta biotech stocks like Moderna are vulnerable to rotation, particularly if earnings fall short or forward guidance disappoints.

Trade setup:

Entry: Near current levels (~$40–41)

Target: $35 (potential gain of ~15%)

Stop-loss: $45 (risk of ~12.5%)

Whether you’re a newer investor or an experienced trader, tools like InvestingPro can help uncover opportunities while managing risk in a challenging and fast-moving market environment.

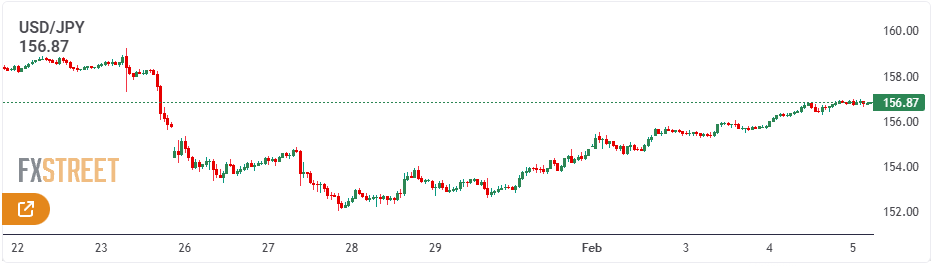

The Japanese yen slid to a fresh two-week low as Sanae Takaichi’s landslide victory reignited concerns over Japan’s fiscal outlook. However, warnings of possible currency intervention sparked some intraday short covering in the yen, aided by broader U.S. dollar weakness.

Still, downside momentum in the yen was partly limited after data showed a decline in Japan’s real wages, which reduced expectations for an immediate interest rate hike by the Bank of Japan and helped cap further moves in the currency.

The Japanese yen began the new week on a softer footing after Prime Minister Sanae Takaichi’s landslide victory in Sunday’s election raised expectations of additional fiscal stimulus. That initial weakness proved short-lived, however, as Finance Minister Satsuki Katayama reiterated warnings over excessive currency moves and confirmed close coordination with the United States to counter disorderly FX fluctuations. Combined with continued U.S. dollar selling, the comments prompted an intraday reversal of nearly 150 pips in USD/JPY from the Asian session peak near 157.65.

Meanwhile, data released earlier showed Japan’s real wages fell in December for a 12th straight month, with nominal pay growth slightly lagging cooling consumer inflation. This reinforces expectations that the Bank of Japan will proceed cautiously after lifting interest rates to a three-decade high in December. In addition, a more upbeat risk environment, supported by signs of easing tensions in the Middle East, limited further safe-haven demand for the yen, allowing USD/JPY to find support and stall its pullback around the 156.20 area.

Yen bulls stay cautious as fiscal concerns and delayed BoJ hike bets offset intervention talk

Japan’s ruling Liberal Democratic Party, led by Prime Minister Sanae Takaichi, secured a decisive victory in Sunday’s election, comfortably surpassing the 233-seat threshold needed for a lower-house majority. The result clears the path for proposed tax cuts and increased defense spending, bringing renewed attention to Japan’s already stretched public finances.

Finance Minister Satsuki Katayama said on Monday that she stands ready to communicate with markets if necessary to help stabilize the yen. She reiterated that Japan remains in close coordination with U.S. Treasury Secretary Scott Bessent and emphasized Tokyo’s right to intervene if currency moves stray from economic fundamentals.

Meanwhile, data from the labor ministry showed nominal wages rose 2.4% year-on-year in December 2025, accelerating from a revised 1.7% gain previously but still missing market expectations. Adjusted for inflation, real wages fell 0.1% from a year earlier, extending their decline to a 12th consecutive month.

The figures have dampened expectations for an imminent Bank of Japan rate hike, as policymakers have stressed that further tightening hinges on sustained and broad-based wage growth. Together with a generally positive global equity backdrop, this has limited the yen’s rebound from a more than two-week low.

Risk sentiment was further supported by indirect U.S.–Iran talks on Tehran’s nuclear program, which concluded on Friday with agreement to keep diplomatic channels open. The development eased fears of a military escalation in the Middle East and encouraged demand for risk assets at the start of the week, despite new U.S. sanctions on Iran.

The U.S. dollar weakened for a second straight session amid growing bets that the Federal Reserve could cut interest rates twice more in 2026. This contrasts with expectations that the BoJ will continue its gradual policy normalization, helping to cap gains in USD/JPY and urging caution among bullish traders.

Attention now turns to key U.S. data later this week, including the closely watched nonfarm payrolls report due Wednesday and consumer inflation figures on Friday, both of which are likely to shape dollar direction and drive fresh moves in USD/JPY.

USD/JPY holds steady below 100-hour SMA as technical signals remain mixed

The USD/JPY pair is showing modest resilience around the 100-hour Simple Moving Average (SMA), with its intraday pullback stalling near the 156.20 area, which now stands out as a key pivot for short-term traders. Momentum indicators, however, paint a mixed picture. The Moving Average Convergence Divergence (MACD) has formed a bearish crossover near the zero line, signaling rising downside pressure, while the Relative Strength Index (RSI) is hovering around 46, below the neutral 50 level, pointing to subdued momentum.

At the same time, USD/JPY remains above the 100-hour SMA, currently located around the 156.55–156.50 zone, which preserves a mildly constructive near-term bias and provides dynamic support. A move by the MACD back into positive territory alongside an RSI break above 50 would strengthen the bullish case and open the door to further gains. On the other hand, a clear break and close below the 100-hour SMA would undermine the setup and increase the risk of a deeper corrective move.

U.S. stock futures ticked higher on Sunday evening after Wall Street mounted a strong rebound late last week, even as investors remained cautious ahead of delayed U.S. employment and inflation data scheduled for release in the coming days.

S&P 500 futures rose 0.4% to 6,978.75 points, while Nasdaq 100 futures advanced 0.6% to 25,319.0 points by 19:12 ET (00:12 GMT). Dow Jones futures were up 0.2% at 50,327.0 points.

Wall Street bounced back late last week as AI disruption fears eased

Wall Street’s major indexes surged on Friday after several days of losses, as investors stepped in to scoop up beaten-down technology stocks and found reassurance in easing bond yields.

The S&P 500 advanced 2%, while the Nasdaq Composite climbed 2.2%. The Dow Jones Industrial Average rose 2.5%, notching its first close above the 50,000-point mark.

Gains were led by chipmakers and AI-linked stocks, which had faced intense selling pressure amid concerns over technology disruption and lofty valuations.

Earlier in the week, the technology sector had suffered sharp declines as investors rotated away from high-growth names, worried that rapid advances in artificial intelligence could upend software business models and squeeze profit margins.

For the week as a whole, the Dow gained roughly 2.5%, supported by strength in industrial and financial stocks. The S&P 500 slipped 0.1%, while the Nasdaq fell about 2%, underscoring the sector’s pronounced weakness.

Jobs, inflation data in focus with major earnings ahead

Market attention is shifting toward key U.S. economic data releases that were postponed due to the partial government shutdown.

The closely watched January employment report, originally due last week, is now scheduled for release on Wednesday. A private-sector jobs report published last week showed weaker-than-expected hiring, sparking concerns that labor market momentum may be starting to cool after months of strength.

Focus will then turn to January consumer price index data, set for release on Friday following the shutdown-related delay. The inflation report will be closely examined for indications that price pressures are easing enough to give the Federal Reserve scope to consider interest rate cuts later this year.

Corporate earnings may also influence markets in the days ahead, with companies such as Coca-Cola Co (NYSE:KO) and Ford Motor Company (NYSE:F) among the notable firms due to report quarterly results this week.

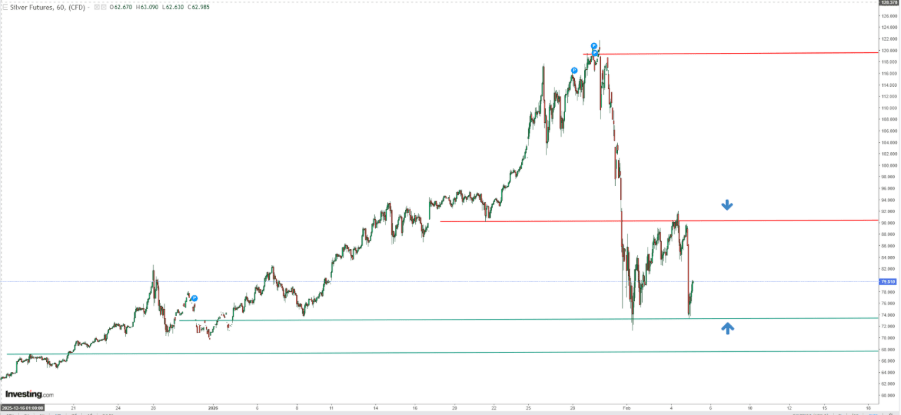

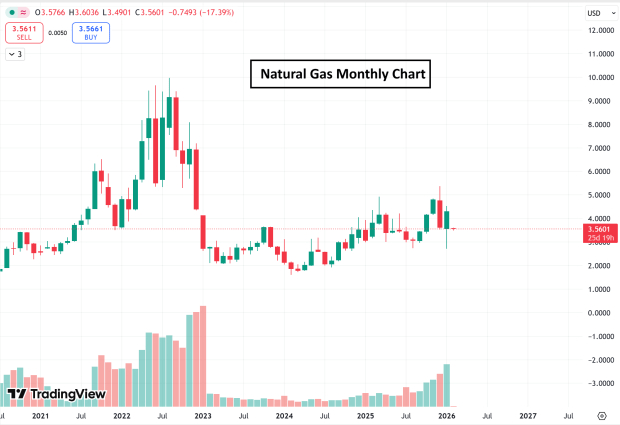

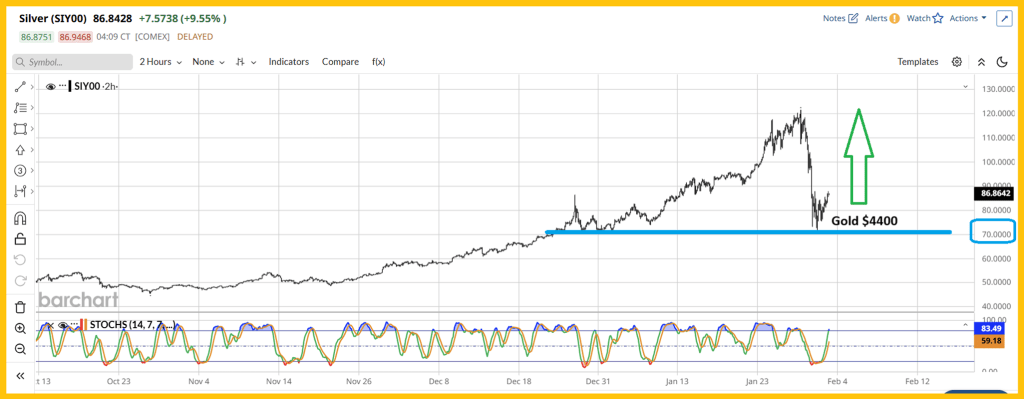

Gold prices climbed in Asian trading on Monday, with silver also advancing after precious metal markets experienced sharp volatility last week amid weaker safe-haven demand, profit-taking, and heightened uncertainty over U.S. monetary policy.

This week’s focus is on a series of key U.S. economic releases—most notably nonfarm payrolls and consumer price index inflation data—which are expected to offer fresh signals on the outlook for the world’s largest economy. Demand for haven assets eased as the United States and Iran showed signs of progress in weekend talks, with both sides agreeing to continue negotiations over Tehran’s nuclear program.

Spot gold rose 0.7% to $4,996.47 an ounce by 20:49 ET (01:49 GMT), after briefly touching an intraday high of $5,046.79. April gold futures gained 0.8% to $5,016.21 an ounce.

Spot silver jumped 3.3% to $80.5330 an ounce, extending its rebound from lows near $60 an ounce seen last week. Platinum underperformed, slipping 2.3% to $2,068.45 an ounce.

Precious metals saw sharp swings last week as investors weighed the outlook for U.S. monetary policy under President Donald Trump’s nominee for Federal Reserve chair, Kevin Warsh. His nomination boosted the dollar, triggering broad selling across metal markets as traders also took profits after strong recent gains in gold and silver.

So far in 2026, gold and silver remain up about 15% and 5%, respectively, despite both metals retreating sharply from record highs reached in early February.

Oil prices slipped in Asian trading on Monday as the United States and Iran indicated they would continue negotiations over Tehran’s nuclear program, easing concerns about heightened tensions in the Middle East.

Crude prices were also weighed down by a firmer U.S. dollar ahead of a busy week of key U.S. economic data, extending losses after a roughly 2% decline last week. Investors are additionally awaiting major economic releases from China, the world’s largest oil importer.

Brent crude futures for April dropped 0.7% to $67.57 a barrel by 21:17 ET (02:17 GMT), while West Texas Intermediate futures also fell 0.7% to $63.12 a barrel.

U.S. and Iran agree to press ahead with nuclear negotiations

Washington and Tehran said over the weekend that indirect nuclear negotiations will continue following what both sides described as constructive talks in Oman on Friday.

The statements helped ease fears of an imminent military confrontation in the Middle East, particularly after the United States had earlier deployed several warships to the region.

Concerns over a potential conflict had previously pushed traders to build a higher risk premium into oil prices, with former President Donald Trump also issuing threats of military action against Iran.

However, the likelihood of a full-scale war in the region now appears reduced, even as Tehran indicated it will continue advancing its nuclear enrichment activities.

Markets await key U.S. and China economic data

Attention this week is also on a slate of major economic data from the world’s largest oil-consuming economies.

In the United States, January nonfarm payrolls figures are due on Wednesday, followed by CPI inflation data on Friday. These releases will be closely scrutinized for further signals on the interest-rate outlook, as markets continue to assess the direction of monetary policy under Warsh.

In China, January CPI data is also scheduled for release on Friday, providing fresh insight into conditions in the world’s biggest oil importer.

The data arrives just ahead of China’s week-long Lunar New Year holiday, which is expected to boost fuel demand across the country.

Most Asian markets climbed sharply on Monday, tracking Wall Street’s tech-led rebound, while Japanese shares jumped to record highs after Prime Minister Sanae Takaichi’s coalition won a decisive lower-house victory. Risk sentiment improved across the region following Friday’s strong U.S. rebound from AI-driven losses, with U.S. stock futures also edging higher in Asian trade.

Nikkei tops 57,000 following Takaichi’s election victory

Japan’s Nikkei 225 jumped as much as 5.6% to a new record of 57,337.07, supported by improved political certainty after Prime Minister Sanae Takaichi’s coalition won a commanding majority in Sunday’s lower-house election. The broader TOPIX index also surged 3.4% to an all-time high of 3,825.67.

Analysts said the decisive victory gives Takaichi greater latitude to push through policy initiatives, with markets anticipating higher public spending, tax incentives, and measures to lift wages and corporate investment, alongside continued backing for key sectors such as technology, defense, and energy. While the outcome is seen as positive for Japanese equities, it is expected to pressure government bonds and the yen.

Asian tech stocks jump, with South Korea’s KOSPI surging nearly 5%

Asian tech stocks rallied at the start of the week, supported by gains in U.S. chipmakers and AI-linked shares. South Korea’s KOSPI surged nearly 5%, rebounding from sharp losses, as Samsung Electronics jumped more than 5% on reports it will begin mass production of HBM4 chips later this month, while SK Hynix also climbed over 5%.

Elsewhere, Hong Kong’s Hang Seng rose 2% with the tech subindex up 1.5%, while China’s CSI 300 and Shanghai Composite gained 1.3% each. Australia’s ASX 200 advanced 2%, Singapore’s STI added 1%, and India’s Nifty 50 futures edged higher. Despite the rebound, investors remain cautious amid recent volatility in tech stocks and ahead of key U.S. jobs and inflation data due later this week.

Most Asian currencies traded in narrow ranges on Monday, while the yen edged higher after Japan’s finance ministry stepped up intervention warnings. However, the yen remained under pressure from concerns over heavy fiscal spending, which are expected to persist following Prime Minister Sanae Takaichi’s landslide election win. Elsewhere, Asian currencies stayed subdued after recent dollar strength, with markets now focused on key economic data due from the U.S. and China.

Yen buoyed by intervention warnings following Takaichi’s victory

The USD/JPY slipped 0.2% to 156.87 on Monday after earlier dropping as much as 0.5%, with the yen finding modest support from renewed intervention warnings by Japanese officials. While the currency remained broadly weak against the dollar, comments from Finance Minister Satsuki Katayama about close coordination with U.S. Treasury officials lent temporary relief.

However, the yen continues to face pressure following Prime Minister Sanae Takaichi’s decisive election victory, which gives her coalition a supermajority in the lower house and a clearer path to expansionary fiscal plans. Concerns over stretched government spending have weighed heavily on the yen and previously triggered a sharp sell-off in Japanese government bonds. Analysts at OCBC noted that while a looser fiscal stance could further pressure the yen, the risk of official pushback is likely to rise as USD/JPY nears the 160 level.

Dollar rebound eases as Asian FX trades quietly

The dollar eased slightly in Asian trade, extending its pullback from last week’s near-98 highs, as traders stayed cautious ahead of key U.S. data, including nonfarm payrolls on Wednesday and CPI inflation on Friday. The releases are expected to shape expectations for U.S. interest rates under potential Fed leadership changes.

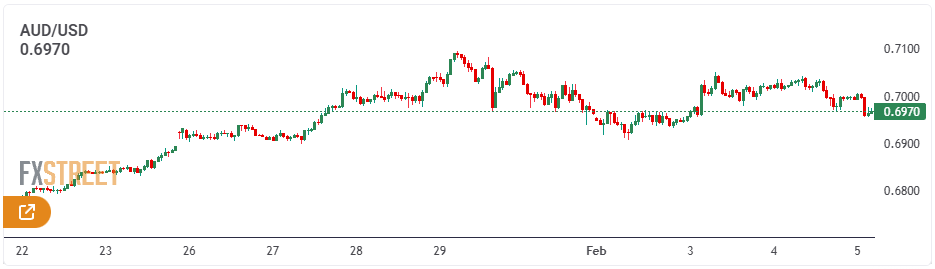

Asian currencies were mostly rangebound. The Chinese yuan edged up, with USD/CNY down 0.1% and hovering near mid-2023 lows, supported by firm PBOC fixings ahead of Friday’s CPI data and the Lunar New Year. The Australian dollar rose 0.2% above $0.70 on bets of further RBA rate hikes after a hawkish move last week.

Elsewhere, the Singapore dollar was flat, the Korean won weakened slightly, and the Indian rupee stayed above 90 per dollar following the RBI’s steady policy stance and upgraded forecasts.

Google plans to increase capital expenditures to as much as $185 billion this year, significantly exceeding market expectations of around $120 billion. Robust growth in search advertising and Google Cloud has provided Alphabet with the financial flexibility to pursue this aggressive investment strategy. According to Morgan Stanley analysts, the sharp rise in spending signals that AI is driving higher engagement and improved monetisation across Google’s core businesses, with search revenue climbing 17% and cloud revenue surging 48% in the most recent quarter.

Meta conveyed a similar message after projecting annual capital expenditures of $135 billion, supported by evidence that AI is enhancing advertising effectiveness. However, not all technology giants have been able to convince investors that rising capital spending is justified. Microsoft, for example, saw its shares fall sharply—erasing more than $350 billion in market value—after its cloud performance disappointed, even as its own capital investment ramped up.

Amazon is also under pressure to sustain strong growth at AWS while continuing to expand data-center capacity. In contrast, Alphabet’s sharply rising cloud backlog highlights growing demand for AI infrastructure and tools, lending credibility to its aggressive spending plans.

The trade-off, however, is immediate. Morgan Stanley estimates that Alphabet’s free cash flow per share could decline by 58% in 2026 and by as much as 80% in 2027 as higher capital expenditures flow through the business. In effect, the company is sacrificing near-term cash returns in exchange for longer-term strategic positioning.

Alphabet now stands at a crossroads. Strong advertising and cloud growth point to early benefits from AI investments, but the sheer scale of spending increases execution risk. If the added capacity delivers sustained revenue growth, the strategy will appear well-timed. If growth slows, Alphabet could face a thinner cash buffer and heightened expectations. For now, the company is betting that leading with investment is essential to staying ahead—and the market will be watching closely to see whether returns keep pace.

After closing the prior week comfortably above the 65.000 level, WTI Crude Oil began this past Monday with a sharp selloff, dropping to nearly 63.300. From there, price action largely revolved around that area throughout the week, with technical levels guiding the back-and-forth movement.

Heading into the weekend, WTI is trading near 63.490 and is likely to open with early momentum when markets reopen on Monday. Overall, crude appears to have formed a central pricing zone, reflecting a higher equilibrium that remains reluctant to drift too far from lower levels. Resistance seems to be forming near 65.500, while the 61.000 area is acting as a key support floor—though, of course, there is no guarantee prices will remain confined within this range.

Short-Term Outlook and Retrospective Analysis

While some market participants attribute higher WTI crude prices to geopolitical concerns in the Middle East—particularly surrounding Iran and the buildup of U.S. military forces in the region—another factor may be the recent stretch of record cold temperatures across the United States. Notably, WTI crude had been trading with support near the 59.000 level up until January 22.

The challenge with any of these explanations is the possibility that WTI crude is simply trading higher due to speculative forces, even though broader factors are clearly influencing market sentiment. The combined impact of geopolitical tensions involving Iran and unusually cold weather in the U.S. may be shaping positioning decisions among large market participants. At the same time, WTI has returned to a price range that was already tested back in August 2025, underscoring that this valuation zone is not unfamiliar territory for the commodity.

Support and Resistance Levels in Focus This Week

Broader financial markets continue to display signs of unease, with many large traders and institutions positioning defensively and expressing limited confidence in signals coming from other asset classes.

By contrast, WTI crude oil has continued to grind along within a familiar and well-defined range, potentially creating opportunities for speculative positioning. The opening price action on Monday will be worth watching, especially given that the prior week began with a sharp selloff at the open. A repeat of that move appears less likely this time, as market anxiety seems to have eased somewhat compared with last week. If WTI opens in a more orderly fashion, it could present attractive opportunities to engage around key technical levels.

WTI Crude Oil Weekly Market Outlook

If WTI crude oil moves higher at the start of Monday’s session and approaches the 64.000 level, traders may look to target slightly higher price zones. That said, day traders should avoid becoming overly aggressive, as the 64.500 area could present stiff resistance unless upside momentum is firmly maintained. For now, a sharp acceleration to higher levels appears unlikely, with a decisive breakout probably requiring fresh catalysts—such as escalating developments involving Iran—to overcome established resistance.

Conversely, if WTI opens lower on Monday, the early reaction around the 63.000 support level will be key. A successful hold there would suggest larger participants are comfortable maintaining the current price equilibrium. However, a sustained break below 63.000 lasting several hours could indicate reduced concern among major oil players, potentially opening the door to further downside movement.

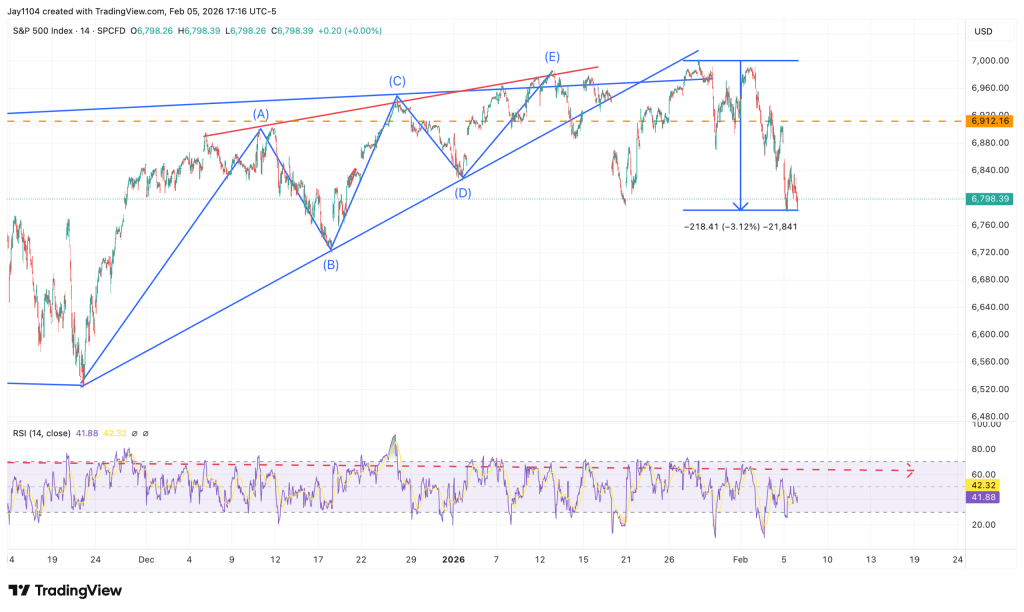

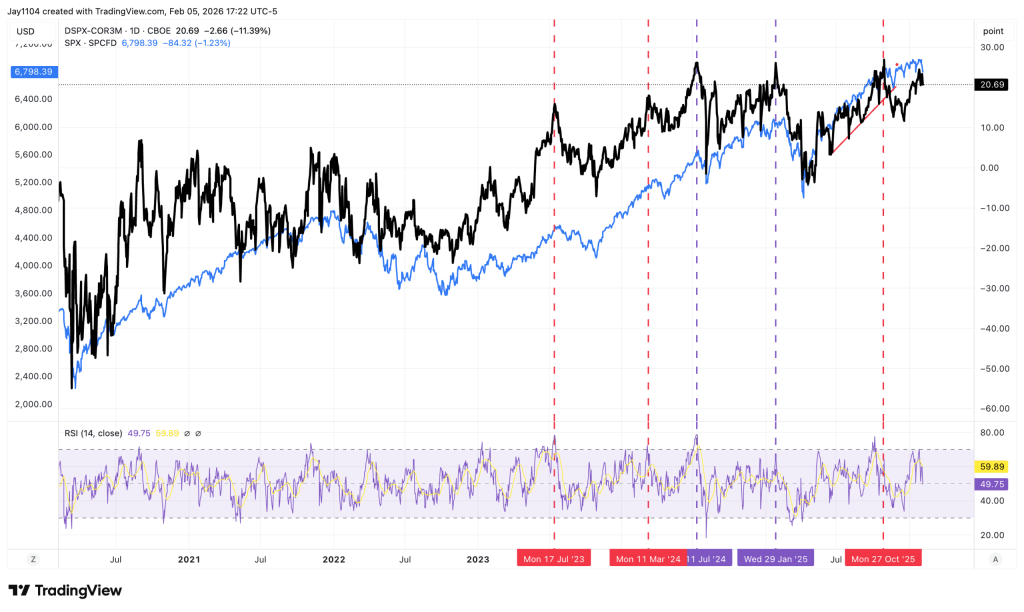

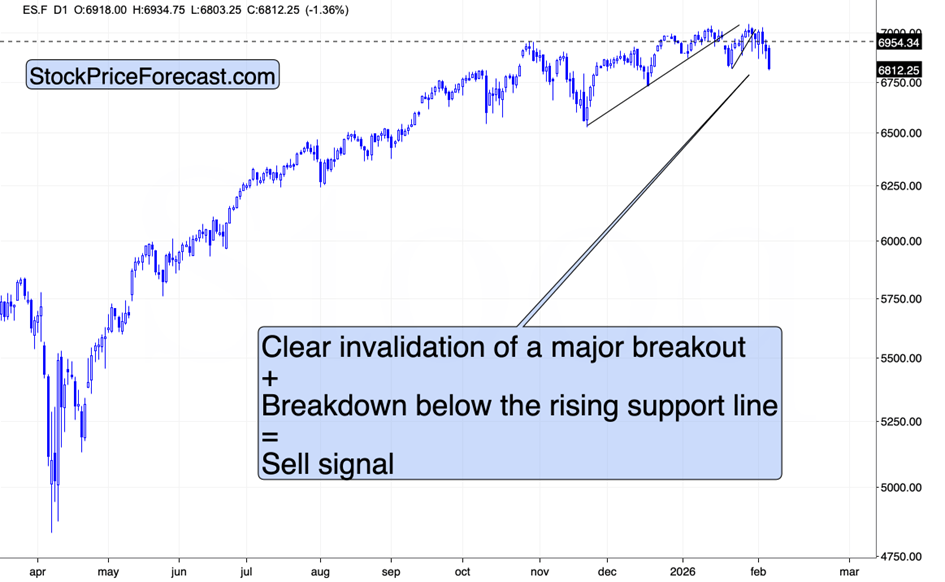

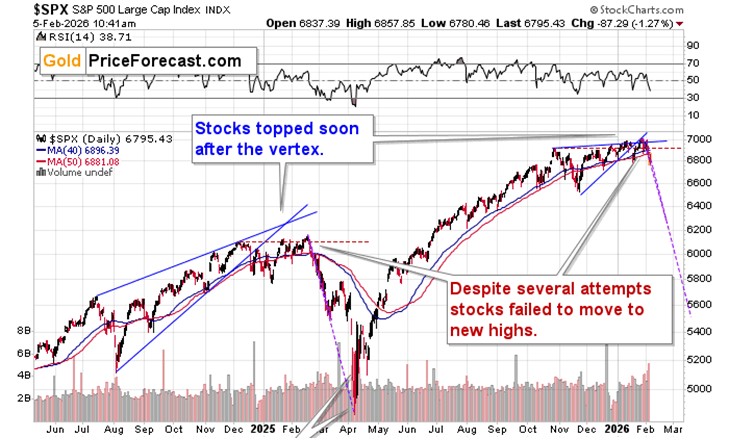

The S&P 500 remains highly volatile, with last week seeing the index test the 7,000 mark and briefly dip below 6,800 before rebounding. Overall, the price action suggests the market is still trying to determine its next direction, which is understandable given that earnings season is underway.

For now, the index continues to favor a buy-the-dip dynamic, with rebounds likely fueling further FOMO. A decisive move above 7,000 would likely open the door to further upside, although short-term choppiness is still to be expected.

EUR/USD

The euro traded in a choppy manner throughout the week as it tested the 1.18 level, an area that had previously acted as resistance. Last week’s price action formed a particularly ugly shooting star, leaving uncertainty about whether the euro has enough momentum to sustain an upside breakout.

A move below the low of last week’s candle could open the door for a pullback toward the 1.16 level, effectively returning the pair to its prior consolidation range. While short-term price action is likely to remain noisy, the broader outlook is clouded by ongoing uncertainty around ECB policy and whether the Federal Reserve will move quickly enough on rate cuts to satisfy market expectations. Overall, I remain neutral on this pair.

USD/CAD

The US dollar strengthened against the Canadian dollar but once again ran into resistance near the 1.37 level. Price is hovering around the 200-week EMA, and last week’s hammer candle suggests buyers may attempt to drive the pair higher, though confirmation is still needed.

From a technical perspective, this zone appears attractive for potential long positions, with the interest rate differential continuing to favor the US dollar. That said, this setup is better suited for short-term traders, as large or sustained moves are unlikely in the near term given the pair’s typically range-bound behavior.

USD/CHF

The US dollar has edged higher against the Swiss franc, pushing above the 0.78 level, a key psychological round number that many traders are closely monitoring. This pair is especially noteworthy given last week’s hammer formation and ongoing comments from the Swiss National Bank expressing discomfort with a strong franc.

Should the SNB maintain this stance, intervention remains a possibility, which would likely weaken the franc and lift USD/CHF along with other CHF-denominated pairs. While the positive swap favors long positions, the move higher is likely to be uneven and challenging, so traders should be mindful of potential volatility.

USD/MXN

The US dollar has been highly volatile against the Mexican peso, with the 17.50 level continuing to act as resistance. For now, the 17.00 area below appears to be the most likely short-term target.

From a longer-term perspective, there is substantial support beneath current levels, making a deeper breakdown uncertain. At the same time, the pair still offers an attractive carry trade, particularly for short-term participants. Given recent price action, this week is likely to remain as choppy as the last two, and significant moves seem unlikely.

DAX

The German DAX has maintained a bullish tone for most of the week but continues to face resistance near the 25,000 level. A decisive break above 25,000—ideally confirmed by a daily, if not weekly, close—would likely clear the way for further upside in the index.

A Global Search for Support

Over time, I expect that breakout to occur. This is not a market that lends itself well to short positions, as it is likely to receive ongoing support from the German government, which continues to inject significant spending into the economy. As a result, buying pullbacks in the DAX remains an attractive strategy.

USD/JPY

The US dollar has held up well against the Japanese yen this week, even in the wake of recent intervention efforts. The 158 level remains a major reference point on long-term charts, an area of significance that dates back to May 1990 and deserves close attention.

Looking further ahead, a sustained break above the 163 level—where the monthly chart shows a substantial resistance zone—could eventually open the door to much higher levels, potentially even toward 250 yen over the longer term. While such a move is not expected in the near future, it reflects the broader outlook for the yen unless there is a meaningful shift in underlying conditions.

GBP/USD

The British pound was highly volatile throughout the week, with the 1.3750 level once again acting as notable resistance. A break below 1.35 would be a strongly bearish signal for GBP/USD and could potentially open the door for a move toward the 1.30 area.

While it remains unclear whether the US dollar has definitively bottomed, it is beginning to show signs of attempting a base. If that proves to be the case, it could leave many traders positioned on the wrong side of the market.

Concerns that the U.S. dollar is heading into a phase of rapid debasement look exaggerated, despite ongoing longer-term headwinds. Although the currency has been volatile recently and briefly hit multi-year lows—reviving “Sell America” narratives—Bank of America says market evidence does not yet point to a structural shift away from U.S. assets.

While BofA remains bearish on the dollar over the long run, it expects any depreciation to play out gradually through 2026 and 2027 rather than through an abrupt decline. Investor positioning and capital flow data show little sign of a coordinated move out of U.S. assets. Dollar risk premia have risen only modestly, and options markets indicate that short-dollar positioning is not meaningfully larger than it was three months ago.

Cross-asset flows reinforce this view, with equity and bond data showing no substantial foreign capital flight from the U.S. Notably, there has been just one session this year in which both the dollar and U.S. equities sold off sharply at the same time—an outcome inconsistent with a broad debasement scenario.

Instead, BofA suggests that increased currency hedging is the more likely adjustment. European investors may hedge their U.S. exposure more actively, which could place steady, incremental pressure on the dollar without triggering a disorderly selloff.

Macro indicators also fail to signal rising debasement risks. Inflation expectations remain well anchored, and although fiscal concerns are widely discussed, they have not produced market stress indicative of eroding confidence in the dollar. Part of the expected dollar weakness may simply reflect improving conditions elsewhere, particularly in Europe, where stronger growth prospects, German fiscal stimulus, potential spillovers from Chinese stimulus, and longer-term structural factors such as higher defense spending and trade agreements could support the euro and other non-U.S. assets.

Stifel downgrades Microsoft to Hold, says it’s “time to pause”

Microsoft (NASDAQ: MSFT) saw a rare Wall Street downgrade this week as Stifel analyst Brad Reback lowered the stock to Hold from Buy, cautioning that expectations for fiscal and calendar 2027 appear overly optimistic. He cited ongoing cloud capacity constraints, rising capital intensity, and intensifying AI competition as key concerns.

Reback cut Stifel’s price target to $392 from $540, saying the stock may need a breather after its strong run. Persistent limitations in Azure capacity remain a major headwind. Given well-known supply issues, along with strong results from Google’s GCP and Gemini platforms and increasing momentum at Anthropic, Reback believes meaningful near-term acceleration at Azure is unlikely.

He also noted that revenue tailwinds from overlapping product cycles that benefited fiscal 2026 should fade, limiting upside in subsequent years. Meanwhile, investment spending is expected to surge. Stifel raised its fiscal 2027 capex estimate to roughly $200 billion, about 40% growth and well above the Street’s $160 billion forecast. As a result, Reback lowered his FY27 gross margin outlook to around 63%, versus a consensus near 67%.

Operationally, Microsoft is entering what Reback described as a new — though still efficient — phase of elevated spending as it builds and monetizes proprietary AI platforms, a shift likely to weigh on operating margin leverage. While Stifel remains positive on Microsoft’s long-term strategic position, Reback said near-term visibility has become less clear, arguing the stock is unlikely to re-rate until capital spending moderates relative to Azure growth or cloud demand reaccelerates meaningfully.

DA Davidson cuts Amazon as AWS cedes cloud leadership

DA Davidson downgraded Amazon (NASDAQ: AMZN) to Neutral from Buy, warning that the company is losing its leadership position in cloud computing and showing early strategic strain in an AI-driven retail landscape. The firm lowered its price target to $175, arguing Amazon is now playing catch-up through increasingly aggressive investment.

Analyst Gil Luria said AWS continues to trail Microsoft Azure and Google Cloud. While AWS posted 24% year-over-year growth, Google Cloud accelerated to 48%, and Azure grew 39% despite capacity constraints. Luria highlighted Amazon’s lack of a frontier AI research lab and the absence of a flagship partnership like Microsoft’s alliance with OpenAI as factors driving customer preference toward rivals.

Falling behind, he warned, is forcing Amazon into heavier spending, pointing to more than $200 billion in projected capex. Luria suggested Amazon may ultimately need to pursue a $50 billion OpenAI investment to remain competitive in frontier AI models. He also raised concerns that Amazon’s retail business could face a structural disadvantage in a chat-centric internet dominated by Gemini and ChatGPT, where merchants embedded directly in leading AI platforms may gain superior traffic and advertising leverage.

Wolfe sees massive long-term upside in Tesla robotaxis, but near-term pressure

Wolfe Research said Tesla’s (NASDAQ: TSLA) robotaxi platform could become a major long-term growth engine, estimating the business could scale to $250 billion in annual revenue by 2035 as autonomous adoption expands. Analyst Emmanuel Rosner described 2026 as a catalyst-heavy year, with investor focus on robotaxi rollout, Optimus production, and the launch of unsupervised full self-driving.

Wolfe’s model assumes 30% autonomous penetration, a 50% market share for Tesla, and pricing of $1 per mile, which could support roughly $2.75 trillion in equity value, or about $900 billion on a discounted basis. Additional upside could come from Optimus and FSD licensing.

Despite the long-term optimism, Rosner remains cautious on near-term fundamentals, sitting below consensus earnings estimates for 2026 and 2027. He expects margin pressure from higher costs, pricing dynamics, and changes in FSD monetization, along with heavy AI-related investment weighing on earnings. Still, strong momentum in Tesla’s energy storage business provides some offset, and Wolfe remains tactically constructive given the steady flow of upcoming catalysts.

Truist tells investors to “buy the dip” in AMD

Truist Securities reiterated a bullish long-term view on AMD (NASDAQ: AMD), urging investors to buy the weakness after the stock fell more than 14% over the past week to its lowest level since October 2025. Analyst William Stein said AMD continues to compound earnings at roughly a 45% CAGR through 2030, while trading at just 11x estimated 2030 EPS.

Although fourth-quarter results benefited from a one-off China-related dynamic, AMD still reaffirmed its outlook for 60% data-center growth and 35% overall sales growth, which management believes could drive more than $20 in EPS by 2030. Stein cited strong customer engagement, accelerating adoption of Instinct MI350 GPUs, and solid demand for fifth-generation EPYC processors as key drivers. Truist raised its 2027 EPS forecast and lifted its price target to $283, arguing long-term fundamentals outweigh short-term noise.

Jefferies warns Palantir valuation still has room to fall

Jefferies said Palantir Technologies (NASDAQ: PLTR) remains vulnerable to further downside despite a steep year-to-date decline of roughly 27%. Analyst Brent Thill emphasized that the call is based on valuation rather than fundamentals, noting that even after compressing from 73x to about 31x forward revenue, Palantir still trades at nearly double the valuation of other large-cap software peers.

While acknowledging improving fundamentals, expanding addressable markets, and strengthening competitive positioning, Thill argued that valuation risk outweighs operational progress. The stock’s premium leaves it highly sensitive to shifts in AI sentiment and broader software sector trends. Jefferies believes cooling enthusiasm could push Palantir toward more sustainable valuation levels, reiterating its Underperform rating and $70 price target, even after strong quarterly results failed to justify the stock’s elevated multiple.

On Monday, JPMorgan downgraded Best Buy (NYSE: BBY) to Neutral with a $76 price target.

TL;DR

JPMorgan turns cautious on BBY. Seller pressure remains heavy, upside is capped, and the stock struggles to break out — “Run, Forrest, run.”

The full story

JPMorgan cut BBY to Neutral from Overweight and set a December 2026 price target of $76, based on 12x P/E and 5.5x EV/EBITDA using its 2026 estimates.

The firm expects a tough 4Q25, with punishing year-over-year comparisons in 2Q and 3Q that mute any consumer recovery rally. Computing faces meaningful pressure just as macro tailwinds fade. While tax stimulus could briefly lift demand, JPM sees limited durability: a short-lived boost from the Nintendo Switch 2 (adding ~2.3 points of comp in 2Q) and the October Windows 10 end-of-support event fail to change the bigger picture.

Rising memory prices — potentially doubling — threaten computing, which makes up over 35% of sales, undercutting what had been mid-single-digit growth from replacement demand. Meanwhile, housing remains weak, while TVs (20%+ of revenue) and appliances (11%) continue to struggle amid aggressive pricing and limited feature-driven upgrades.

Crowded short positioning and stimulus optimism could push shares back into the $70s, but JPM sees this as a classic “can’t see the forest for the trees” setup. With sellers positioned higher, the firm steps aside.

SoFi (SOFI)

What happened?

On Tuesday, JPMorgan upgraded SoFi (NASDAQ: SOFI) to Overweight and lifted its price target to $31.

TL;DR

Momentum is real, and the recent pullback looks like a gift — not a red flag. Happy New Year.

The full story

SoFi shares are down about 10% since the company’s Q4 earnings call on January 30, even as the S&P 500 has barely moved. JPMorgan views the selloff as disconnected from fundamentals, coming on the heels of record quarterly results and 2026 adjusted EBITDA guidance that surpassed expectations.

The firm points to strong and accelerating momentum across the business. SoFi continues to add members and deposits at record levels, standing out as many competing fintechs face outflows or stalled growth. Elevated marketing spend through 2025 and into the first half of 2026 is seen as a strategic advantage, helping attract and retain higher-quality customers.

With a nearly $40 billion loan portfolio now producing meaningful GAAP earnings — even excluding non-cash fair-value adjustments — alongside growing fee revenue from the Tech Platform and expanding products like SoFi Plus, JPM argues the company has reached real scale. That combination, in its view, supports a premium valuation and underpins the upgrade.

Booking Holdings (BKNG)

What happened?

On Wednesday, Mizuho upgraded Booking Holdings (NASDAQ: BKNG) to Outperform and reiterated its $6,000 price target.

TL;DR

Mizuho turns bullish on BKNG. Buy the fear — roughly 30% upside ahead.

The full story

Mizuho raised BKNG to Outperform from Neutral while holding its $6,000 price target, implying about 30% upside and a compelling 2.7x bull/bear skew.

Shares are down 16% since the recent selloff, underperforming peers (Expedia +6%, Airbnb -1%) and the broader market (Nasdaq +2%), even as 2027 EPS estimates have risen roughly 4%. The firm dismisses concerns that generative AI will bypass online travel agencies and drive consumers directly to hotels, characterizing the narrative as exaggerated market fear rather than a structural threat.

Valuation has become increasingly attractive. BKNG now trades at 17.8x next-twelve-month consensus P/E, a full standard deviation below its three-year average of 20.6x, and around 16x projected 2027 GAAP EPS.

For investors who missed the November selloff, Mizuho frames the current setup as another clear opportunity: sentiment has overshot fundamentals, and fear is once again creating an entry point.

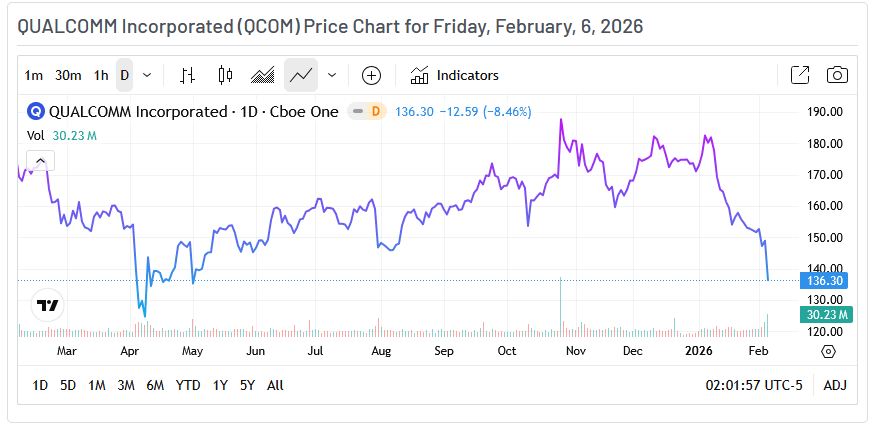

Qualcomm (QCOM)

What happened?

On Thursday, Bank of America downgraded Qualcomm (NASDAQ: QCOM) to Neutral and cut its price target to $155.

TL;DR

Handset demand is collapsing, QCT is in trouble, and near-term catalysts are nowhere to be found. BofA looks elsewhere.

The full story

BofA downgraded QCOM from Buy to Neutral and slashed its price target from $215 to $155, lowering its valuation multiple to 13.5x FY27E P/E, down from 17x previously.

The call centers on worsening handset fundamentals. Smartphones account for roughly 74% of QCT revenue, and unit volumes are now expected to fall about 15% this year, a sharp deterioration from prior expectations of a modest 2% decline. Memory pricing volatility continues to pressure the ecosystem, weighing on demand across the supply chain, with even ARM and MediaTek feeling the strain.

Competitive dynamics add to the pain. Samsung has taken roughly 25% share, Apple is expected to reduce reliance on Qualcomm later this year, and China demand is fading following a holiday-driven surge. As a result, BofA forecasts QCT revenue to decline 1.5% in FY26.

While Qualcomm trades at a seemingly cheap ~12x FY27E earnings, the firm sees little reason for multiple expansion. With no clear near-term catalysts and both cyclical and structural headwinds building, BofA steps to the sidelines.

Amazon (AMZN)

What happened?

On Friday, DA Davidson downgraded Amazon (NASDAQ: AMZN) to Neutral and cut its price target to $175.

TL;DR

AWS is losing momentum versus faster-moving rivals, AI leadership gaps are widening, and rising capex clouds the risk/reward. DA Davidson steps back.

The full story

DA Davidson downgraded Amazon from Buy to Neutral, arguing that AWS’s dominance is beginning to erode under competitive pressure. While AWS is growing at roughly 24%, rivals are accelerating faster—Google Cloud at 48% and Azure at 39%—driven by stronger AI ecosystems, frontier-model partnerships, and perceived leadership rather than arguments around scale.

The firm highlights growing concerns around AWS’s AI stack. Trainium continues to lag Google’s TPUs, and customers appear increasingly willing to shift workloads accordingly. In retail, DA Davidson sees strategic risk from limited deep integration with leading conversational AI platforms such as Gemini or ChatGPT, potentially allowing competing commerce platforms to capture merchant traffic and advertising dollars. Internal efforts, including Rufus and broader “horizontal model” initiatives, are viewed as slow to gain traction. Even Amazon’s early investment in Anthropic is seen as less differentiating as competition intensifies.

Meanwhile, capital expenditures are surging beyond $200 billion, raising questions about return on investment and whether Amazon may need to pursue costly external AI partnerships simply to remain competitive. Although revenue growth remains solid at around 13% and backlog continues to build, the firm believes the balance of risk has shifted.

DA Davidson concludes that Amazon’s scale no longer guarantees leadership, and that caution—not blind confidence—is warranted at current levels.

The opening weeks of the year have underscored how rapidly investor sentiment can change. In early 2026, markets saw a clear rotation into consumer staples, a sector traditionally favored for its defensive characteristics. As technology stocks came under pressure from elevated valuations and growing doubts about the durability of the AI-driven rally, consumer staples emerged as a relative safe haven.

The Consumer Staples Select Sector SPDR Fund (XLP), a widely followed benchmark, climbed roughly 13% year-to-date through early February—one of its strongest starts in more than ten years. By contrast, technology shares fell by about 3% over the same period, reflecting a classic shift toward lower-risk assets.

Why Investors Are Seeking Safety

The drivers behind this rotation are varied but grounded in clear logic. After years of leadership fueled by AI enthusiasm and an extended period of low interest rates, technology entered 2026 with lofty expectations. Rising concerns over escalating AI capital expenditures, potential regulatory pressure, and a more normalized rate environment triggered a wave of profit-taking.

At the same time, broader macro signals—including softening labor market conditions, pockets of persistent inflation, and heightened geopolitical risks—pushed investors toward more stable areas of the market. Consumer staples fit that role well. Demand for everyday necessities such as food, beverages, household goods, and tobacco alternatives remains steady, supporting reliable earnings, consistent dividend payouts, and lower overall volatility.

This shift mirrors historical patterns in which periods of uncertainty or market broadening drive capital away from high-growth, cyclical sectors and into defensive ones. Amid broader market pullbacks this year, consumer staples have stood out as one of the few areas of relative strength, drawing significant inflows as investors reduce risk. The sector’s limited sensitivity to economic cycles—consumers continue to buy essentials like toothpaste, soap, and snacks regardless of conditions—offers a cushion when discretionary spending weakens.

Consumer Staples Stocks Reaching Yearly Highs

Established industry leaders have been at the forefront of this move, combining defensive stability with incremental growth drivers. Philip Morris International (NYSE: PM) has been a notable example, with shares posting solid gains in early 2026 following a strong fourth-quarter 2025 earnings report. The company’s ongoing shift toward smoke-free alternatives—such as IQOS heated tobacco products and Zyn nicotine pouches—has delivered robust volume growth, more than offsetting declines in traditional cigarette sales.

Philip Morris exceeded Q4 expectations, reporting adjusted earnings per share of $1.70, up 9.7% year over year, alongside revenue growth of 6.8%. The stock currently holds a Zacks Rank #3 (Hold), reflecting stable near-term expectations. Consensus forecasts call for full-year 2026 EPS of roughly $8.34, representing nearly 11% annual growth, supported by strong pricing power and continued momentum in emerging markets.

Coca-Cola (NYSE: KO) completes the list of standout performers, benefiting from its unmatched global brand presence in beverages. Continued volume growth in emerging markets, along with broader diversification into non-carbonated offerings, has helped sustain the company’s momentum. Coca-Cola’s attractive dividend yield and dependable payout profile make the stock particularly appealing in income-focused environments. Currently holding a Zacks Rank #3 (Hold), consensus estimates suggest a steady, incremental improvement in earnings per share.

Bottom Line

These sector leaders highlight the core appeal of consumer staples: dependable, recurring revenue from essential products; strong balance sheets that support consistent dividends—often in the 3–4% yield range; and modest growth driven by innovation or international expansion. Valuations across the sector remain reasonable relative to growth prospects, with many names trading at forward price-to-earnings multiples in the high teens to low 20s, well below the elevated valuations seen in much of the technology space.

As recession concerns quietly build amid a softening labor market, consumer staples offer credible downside protection without materially compromising long-term total returns. For well-diversified portfolios, the sector serves as a stabilizing anchor—delivering steady performance in increasingly uncertain market conditions.

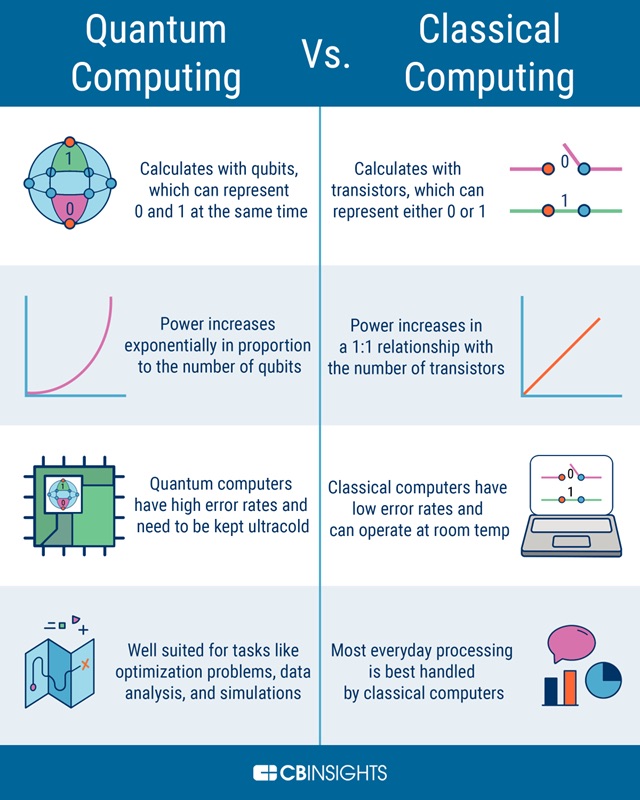

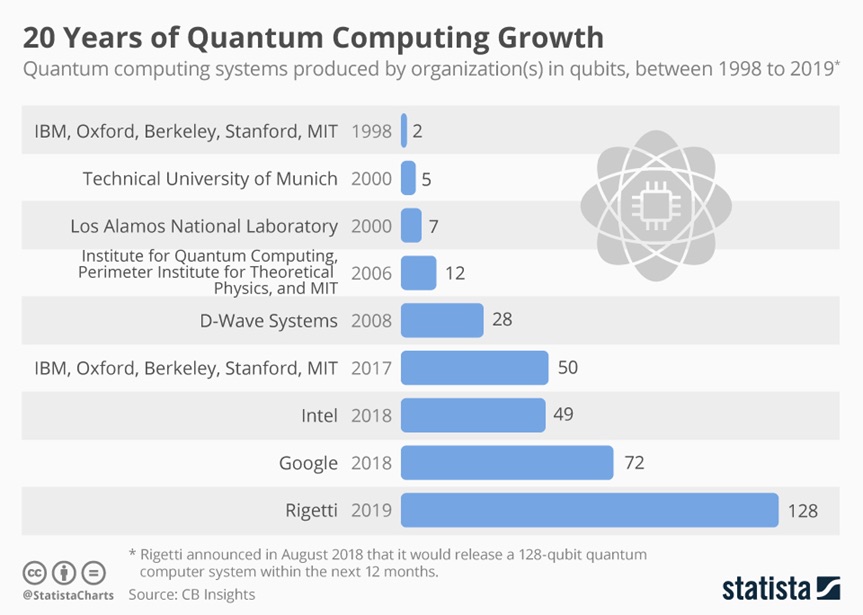

Over the past year, market attention has largely centered on bitcoin’s price volatility and shifting investor sentiment. Headlines were dominated by discussions around regulation, adoption, and inflation. Meanwhile, a more subtle but potentially significant risk has been developing in the background: advances in quantum computing. Bitcoin has recently come under pressure as investors begin to factor in these concerns, prompting renewed debate over the cryptocurrency’s long-term security and durability.

Introduction

Rapid progress in quantum computing is raising fresh questions about the future security of blockchain-based systems. Bitcoin’s network depends on cryptographic algorithms to protect transactions and verify ownership, and researchers are increasingly examining whether sufficiently powerful quantum computers could one day compromise these safeguards.

These worries are no longer confined to academic circles. Christopher Wood, Jefferies’ global head of equity strategy, recently removed bitcoin from his model portfolio, citing the risk that breakthroughs in quantum computing could erode the cryptographic foundations underpinning the asset. He cautioned that any successful attack would call into question bitcoin’s credibility as a long-term store of value.

The Quantum Computing Threat

Quantum computing is widely viewed as the next major leap in computational technology. Traditional computers process information using binary bits—either a 0 or a 1. Quantum computers, by contrast, rely on quantum bits, or qubits, which can exist in multiple states simultaneously due to a phenomenon known as superposition. When combined with other quantum effects such as entanglement and interference, this capability allows quantum systems to solve certain classes of problems far more efficiently than classical machines.

Timothy Hollebeek, Industry Standards Strategist at DigiCert, offers a helpful analogy: classical computing is like navigating a maze by testing one route at a time, while a quantum computer can explore all possible paths simultaneously. This parallelism is what makes quantum computers especially powerful for tasks involving complex mathematics, including factoring large numbers and uncovering patterns within massive datasets.

Recent breakthroughs highlight the promise of quantum technology. Google’s quantum processor, Willow, reportedly completed a specialized computation in under five minutes—an exercise that would take classical supercomputers an impractically long time to finish. The chip is estimated to be roughly 13,000 times faster than the world’s most powerful traditional systems for that task. Achievements like this help explain why quantum computing is drawing growing interest across sectors such as healthcare, logistics, and materials research.

Still, despite the enthusiasm, quantum computing remains in its early developmental phase. Current systems face significant technical limitations. Qubits are highly fragile, must operate at temperatures close to absolute zero, and are extremely sensitive to environmental noise, which can introduce errors. Even in tightly controlled settings, sustaining a stable quantum state for more than a short duration remains challenging. For instance, Google’s Willow chip uses 105 qubits, whereas practical, fault-tolerant quantum computers would likely require thousands of reliably connected and stable qubits.

The rapid progress of quantum computing has prompted renewed scrutiny of the long-term security of cryptography-dependent digital systems, including cryptocurrencies. Because bitcoin’s architecture rests on assumptions about the limits of computational power, any transformative advance in computing naturally warrants closer evaluation.

The Real Threats That Could Undermine Bitcoin’s Value

“Quantum computers are not a matter of if, but when,” said Timothy Hollebeek, Industry Standards Strategist at DigiCert—a sentiment that helps explain why quantum advancements are increasingly viewed as a potential long-term risk to bitcoin’s security and valuation.

The most significant risk centers on Shor’s algorithm, a quantum method capable of compromising the elliptic curve digital signature algorithm (ECDSA) that bitcoin relies on to verify ownership of funds. Under today’s classical computing constraints, deriving a private key from a public key is computationally infeasible. However, in a future with sufficiently powerful quantum computers, this assumption may no longer hold. In theory, an attacker could extract a private key from its corresponding public key in a relatively short period, enabling unauthorized transfers of funds.

The quantum risk is not evenly spread across the bitcoin network. Roughly 25% of all bitcoins—more than 5 million BTC—are held in so-called “vulnerable” addresses, including early P2PK addresses and reused P2PKH addresses. This category also encompasses the estimated 1.1 million BTC attributed to Satoshi Nakamoto. These holdings are more exposed because their public keys are already visible on the blockchain, making them potential targets for quantum-enabled attacks. If even a fraction of these coins were moved by a quantum adversary, the resulting supply shock could be severe, shaking confidence in bitcoin’s ownership framework and placing significant downward pressure on prices.

Even newer address formats are not entirely risk-free under extreme assumptions. One commonly cited theoretical vulnerability involves transactions sitting in the mempool—the queue of unconfirmed transactions shared across network nodes. In this scenario, a sufficiently advanced quantum computer could detect a transaction before it is confirmed, derive the corresponding private key in real time, and submit a competing transaction that redirects the funds. Although highly speculative, this example illustrates how execution speed could become as critical as raw computational power.

Beyond outright theft, quantum computing could also erode trust in bitcoin’s neutrality and privacy. Through Grover’s algorithm, quantum-capable miners could gain a disproportionate advantage in proof-of-work mining, increasing the risk of mining centralization. If a single entity accumulated enough influence, it could censor transactions or reorganize blocks, undermining bitcoin’s decentralised ethos.

Another frequently cited risk is the concept of “harvest now, decrypt later,” where encrypted blockchain data is collected today with the expectation that future quantum computers could decrypt it. While this would not alter historical transactions, it could reveal identities behind pseudonymous wallets or expose past activity, weakening perceived privacy guarantees.

These technical risks are increasingly showing up in market behavior. By early 2026, quantum-related concerns had moved beyond abstract theory and begun to affect investor positioning. Bitcoin, for instance, lagged gold by roughly 6.5% year-to-date, while gold advanced about 55% over the same period. As a result, the bitcoin-to-gold ratio fell to around 19 BTC per ounce, signaling a more cautious stance toward bitcoin among investors.

Bitcoin Relative to Gold

How Bitcoin Could Be Compromised—and Why It Remains Resilient

At present, Bitcoin depends on elliptic curve cryptography (ECC)—specifically the secp256k1 curve—to generate public and private keys. Transactions are authenticated using ECDSA signatures, a system that is secure against classical computers but could be vulnerable to sufficiently advanced quantum machines. If that were to happen, both fund ownership and transaction integrity could be at risk.

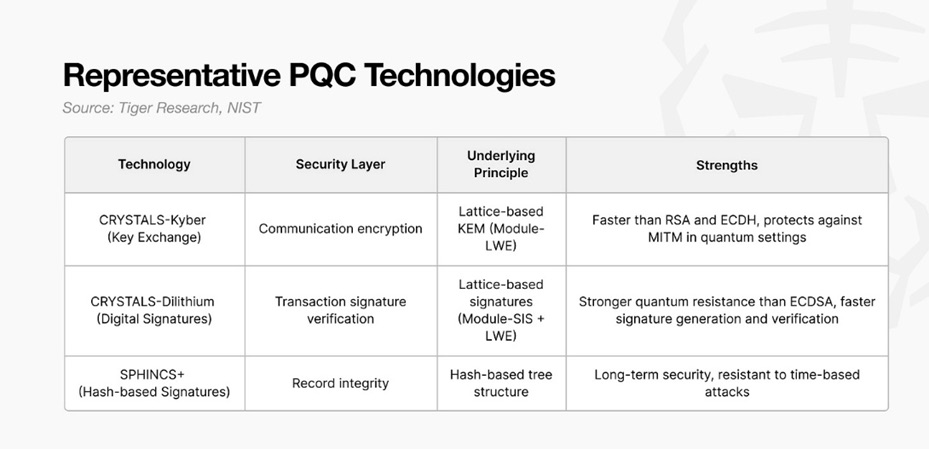

One practical solution is the adoption of post-quantum cryptography (PQC), which is designed to withstand quantum attacks. Rather than requiring a complete overhaul of the network, PQC could be introduced incrementally, allowing vulnerable cryptographic components to be replaced over time.

Under a PQC framework, security would be reinforced through a three-layer defense. Kyber would protect communications between nodes and wallets, preventing interception or eavesdropping. Dilithium would handle transaction verification and safeguard private keys against quantum-enabled attacks. SPHINCS+ would ensure the integrity of transaction records, effectively giving each transaction a unique, tamper-resistant cryptographic fingerprint.

Bitcoin is not a static system. In January 2026, the first “Bitcoin Quantum” testnets began experimenting with post-quantum cryptography using NIST-standardised algorithms such as ML-DSA (formerly Dilithium). These trials demonstrated that quantum-resistant upgrades can be tested safely before any network-wide rollout. Such technologies strengthen transaction validation, data transmission, and record integrity, helping ensure bitcoin’s durability in a future shaped by quantum computing. Previous upgrades—including SegWit and Taproot—illustrate that bitcoin can evolve without disrupting network operations.

Resilience is not purely technical; it is also economic and social. A visible quantum-related attack would pose an immediate threat to bitcoin’s value, creating strong incentives for miners, developers, exchanges, and large holders to coordinate a rapid response. Historically, the network has shown an ability to converge quickly on practical solutions when facing systemic risks. Moreover, quantum computing is advancing incrementally, giving bitcoin ample time to prepare, test, and deploy defensive measures before the threat becomes acute. In this context, resilience is about managing technological change carefully rather than attempting to stop it outright.

Bitcoin’s robustness is rooted in both its architecture and its incentives. The network has no central authority, physical headquarters, or kill switch. Its ledger is maintained by thousands of independent nodes globally, eliminating single points of failure. A fixed supply cap of 21 million coins guards against monetary inflation, while the proof-of-work mechanism—secured by vast computational resources—makes large-scale attacks prohibitively expensive.

Widespread adoption further reinforces this resilience. By 2024, an estimated 500 million people held bitcoin or other cryptocurrencies, while institutional participation expanded through ETFs, hedge funds, pension funds, and even sovereign entities. As bitcoin becomes increasingly embedded in the global financial system, the economic and political costs of attempting to disrupt it continue to rise. Major stakeholders now have strong incentives to preserve long-term stability rather than undermine it.

Some observers, including Michael Saylor, have argued that a shift to quantum-resistant addresses could materially affect bitcoin’s market dynamics. If the network were to establish a migration deadline, coins held in legacy addresses—whose owners have lost access or passed away—could become permanently inaccessible. This would effectively remove millions of bitcoins from circulation, tightening supply and increasing scarcity. While the timing and market response remain uncertain, such a transition underscores the intricate relationship between technological evolution and bitcoin’s economic framework.

Conclusion

Quantum computing poses challenges that extend well beyond bitcoin, as many digital platforms and internet communications depend on the same public-key cryptographic systems that could eventually be vulnerable to quantum attacks. Nvidia CEO Jensen Huang has suggested that truly practical quantum computers may still be 15 to 30 years away, providing a meaningful window for industries to prepare and adapt.

In the meantime, leading technology firms are already moving to address these risks. Microsoft, for instance, is incorporating post-quantum cryptography (PQC) into its core software libraries and working alongside global standards organizations to develop quantum-resistant protocols for secure communications.

Together, these initiatives indicate that both the broader technology sector and the cryptocurrency ecosystem are actively planning for a post-quantum future, testing and deploying safeguards well ahead of the arrival of commercially viable quantum computers.

The U.S. and Iran are holding talks in Oman today focused on dismantling Iran’s nuclear program. Washington is pushing Tehran to halt uranium enrichment, scale back its ballistic missile development, and withdraw support for regional proxy groups that contribute to instability in the Middle East. Iran, however, has stated it is only prepared to negotiate on nuclear-related issues. If discussions collapse, the risk of renewed U.S. military action rises, underscored by the significant U.S. naval presence in the region. That said, Iran recently seized two oil tankers ahead of the talks and later described the discussions as “positive.”

Following the meeting, Iranian Foreign Minister Abbas Araghchi said on state television that both sides could reach a framework for future negotiations if talks continue along the same lines. He emphasized that the dialogue remains limited strictly to nuclear matters, with no broader issues under consideration. Given Iran’s history of prolonging negotiations and the U.S. military buildup aimed at Iranian nuclear and defense assets, it remains to be seen how long Washington will tolerate a narrow scope of engagement.

Meanwhile, despite some concerns on Wall Street about OpenAI’s momentum, activity in the data center sector continues to accelerate. Super Micro Computer (SMCI) reported a 123% year-over-year jump in fourth-quarter revenue to $12.7 billion, while earnings climbed to $0.69 per share. The company delivered a 22.1% revenue beat and a 40.8% earnings surprise, along with upbeat forward guidance. As one of Nvidia’s largest customers, Super Micro’s results suggest Nvidia could also deliver a strong upside surprise, even as analysts forecast robust growth of 66.7% in sales and 71.1% in earnings.

AI-driven productivity gains are expected to continue supporting stronger GDP growth. The data center expansion shows no signs of slowing, underscoring the durability of the AI revolution. Nvidia’s upcoming Vera Rubin GPU—offering five times the performance and ten times the energy efficiency of the Blackwell architecture—is likely to trigger a multi-year AI hardware replacement cycle. At the same time, pricing for advanced chips and memory remains resilient, allowing AI demand to sustain strong profitability across the semiconductor ecosystem, including Nvidia (NVDA), Micron (MU), and Seagate Technology (STX).

The U.S. economy is experiencing a powerful growth phase, with annual GDP growth of 5% potentially driven by an estimated $20 trillion in onshoring investments across data centers, semiconductors, pharmaceuticals, and automotive manufacturing. Energy independence gives the U.S. a structural advantage over global peers, as manufacturers can avoid tariffs by relocating production domestically. In addition, U.S. support for increased crude oil output in Venezuela should help keep global oil prices contained over the medium term.

Overall, the U.S. continues to outperform globally in domestic growth. With Kevin Warsh nominated as the next Federal Reserve Chair, the U.S. dollar is expected to strengthen further. While AI is clearly enhancing productivity, it is also contributing to job displacement across corporate America. As a result, the Federal Reserve is likely to cut policy rates at least three times this year amid ongoing labor market concerns. These rate cuts should, in turn, help lift consumer confidence in the months ahead.

Amazon.com (NASDAQ: AMZN) reported quarterly revenue that topped expectations on Thursday, but markets focused on the company’s 2026 capital expenditure forecast of roughly $200 billion—far above what analysts had anticipated.

Shares ended Friday down 5.55%, though they pared earlier losses as a broad rally on Wall Street boosted risk assets.

The results arrive amid a notable rotation out of technology stocks into other sectors. Investor sentiment has shifted from viewing the tech sector broadly as an AI beneficiary to a more selective approach, with clear winners and losers emerging. Software firms have been singled out as laggards, with weakness spreading to chipmakers and the wider tech space.

Concerns around stretched valuations and aggressive spending plans have also weighed on sentiment. Amazon’s projected $200 billion in 2026 capex significantly exceeded the consensus estimate of $146.11 billion.

Despite those concerns, Morgan Stanley analyst Brian Nowak struck an optimistic tone, noting that AWS is gaining momentum with stronger growth ahead, while Amazon’s retail business continues to improve efficiency. Although the company is ramping up investment across AWS, Retail, and its low-Earth-orbit initiatives, Nowak highlighted Amazon’s solid history of delivering returns on invested capital, keeping the firm bullish on what it views as an underappreciated GenAI leader.

Amazon’s guidance followed closely on the heels of Alphabet (NASDAQ: GOOGL), which also surprised investors earlier in the week with plans to spend as much as $185 billion in capital expenditures in 2026.

On the earnings front, Amazon narrowly missed profit expectations, posting earnings of $1.95 per share—one cent below forecasts—on revenue of $213.39 billion for Q4 2025, representing a 13.6% year-over-year increase. Revenue exceeded the consensus estimate of $211.27 billion.

Emarketer principal analyst Sky Canaves described the results as slightly mixed, citing strong overall revenue growth and a notable acceleration in the cloud business, which had been closely watched by investors.

Looking ahead, Amazon forecast first-quarter 2026 revenue in the range of $173.5 billion to $178.5 billion, compared with analyst expectations of $175.2 billion.

CEO Andy Jassy said the company plans to invest heavily in areas such as AI, custom chips, robotics, and low-Earth-orbit satellites, adding that Amazon expects these investments to generate strong long-term returns on invested capital despite the elevated spending outlook.

An overview of AWS

For Amazon, one of the Magnificent Seven, Amazon Web Services (AWS) sits at the core of its AI strategy and remains its fastest-expanding business. AWS generated $35.58 billion in revenue in Q4, marking a 23.6% year-over-year increase. Beyond cloud services, the unit includes Amazon’s AI development platforms and infrastructure—such as Bedrock—as well as products like Alexa and Polly.

According to Emarketer analyst Canaves, AWS delivered an uncommon performance in Q4 by outpacing the advertising segment’s growth while also improving operating margins. Amazon has also deepened its exposure to AI through a substantial investment in Anthropic, the startup behind the Claude AI models.

Amazon revealed in October that it had added 3.8 gigawatts of cloud computing capacity over the past year—more than any rival provider. CEO Andy Jassy noted during the earnings call that AWS’s power capacity has doubled since 2022 and is expected to double again by 2027.

UBS has argued that the market is not fully accounting for the implications of Amazon’s aggressive capital expenditure plans. The bank raised its combined CapEx forecast for 4Q25–4Q27 to $344 billion from $300 billion, including an increase in AWS investment estimates from $225 billion to $260 billion.

UBS analysts Stephen Ju and Vanessa Fong believe Amazon shares remain undervalued, as neither they nor broader markets are factoring in the possibility that AWS revenue could double by 2028. They estimate this scenario could generate an additional $20 billion in free cash flow that year.

Despite these growth drivers, Amazon’s stock has lagged its Magnificent Seven peers. Shares rose just 5.2% in 2024—the weakest performance among the group—and trailed the S&P 500’s 16.4% gain. Performance in the current year has also been modest, with Amazon up 0.9% year-to-date, compared with the S&P 500’s 0.5% increase.

While AI continues to attract attention, Amazon’s core business is still its e-commerce, retail, and subscription services—primarily housed in its North America segment. This division posted Q4 revenue of $127.08 billion, up 9.9% year over year.

Consumer spending faced increasing pressure last year amid economic challenges. The National Retail Federation projects 2025 holiday sales growth of 4.1%, down from 4.3% in 2024, while consumer confidence has recently dropped to its lowest level since May 2014.

Even so, Amazon’s retail operations showed resilience during the critical holiday season. Canaves noted that profitability in North America improved due to stronger fulfillment efficiency, despite faster delivery rollouts. Meanwhile, Amazon’s AI shopping assistant, Rufus, is gaining adoption and contributing to higher sales among users.

Macquarie has updated its 2026 outlook for gold and silver, pointing to extreme volatility and recent geopolitical and policy-driven shocks as the main catalysts.