Inflation came in cooler than anticipated in January, though markets still largely expect the Federal Reserve to hold its benchmark rate steady until June. However, the bond market appears ready to test that timeline, increasingly factoring in the possibility of a rate cut arriving sooner.

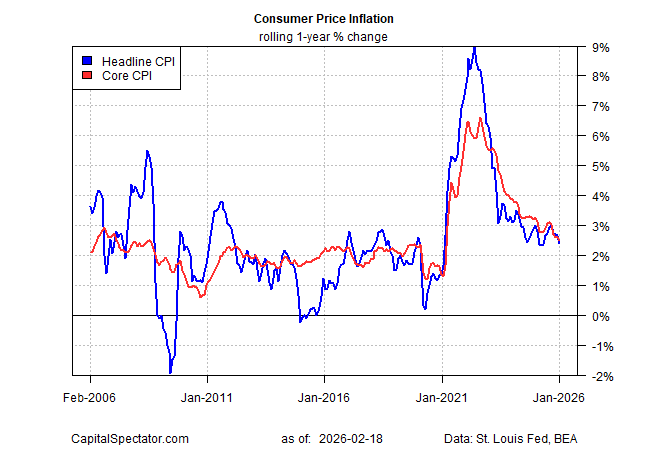

According to government data released Friday, the Consumer Price Index (CPI) rose 2.4% year over year in January, down from 2.7% in December and marking the lowest reading in eight months. Core CPI—which excludes volatile food and energy prices and is considered a clearer gauge of underlying inflation—also eased to 2.5% annually, its slowest pace since 2021.

While the slowdown in headline inflation is a welcome development, a deeper dive into the data suggests it may be premature to relax concerns about where prices are headed next. Persistent increases in tariff-sensitive goods remain one pressure point. Food prices are another, climbing 2.9% year over year—elevated by historical standards.

Energy costs rose even more sharply, and both homeowners’ and renters’ insurance premiums continued to increase. Moreover, inflation is still running above the Federal Reserve’s 2% target, reinforcing the likelihood that policymakers will proceed carefully.

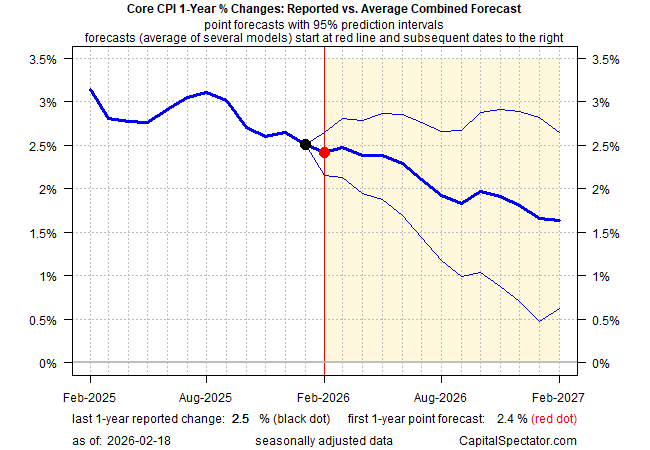

Although it’s too soon to claim inflation has been fully tamed, the broader trend of moderating price growth strengthens the argument that the worst may be behind us. The Capital Spectator’s ensemble forecast has long projected continued disinflation in core CPI, a view that has so far aligned reasonably well with actual data. The model still anticipates further easing, with core CPI’s 12-month rate expected to edge down to around 2.4% in the upcoming February report.

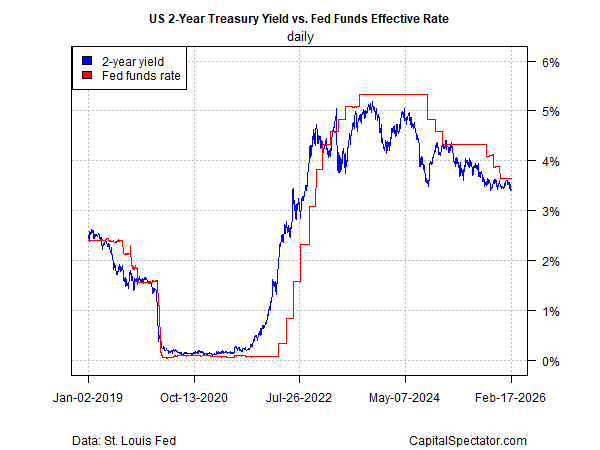

Fed funds futures continue to indicate that the first rate cut won’t arrive until the June meeting. In contrast, the Treasury market appears to be probing the possibility of an earlier move. The policy-sensitive 2-year Treasury yield has fallen to about 3.45%—near its lowest level since 2022—and now sits below the Federal Reserve’s current target range of 3.50% to 3.75%, signaling that bond investors may be anticipating a faster shift in policy.

In short, Treasury market sentiment is tilting toward the idea that a rate cut could come sooner than previously anticipated. Other market-based indicators are reinforcing that view by assigning higher odds to continued disinflation.

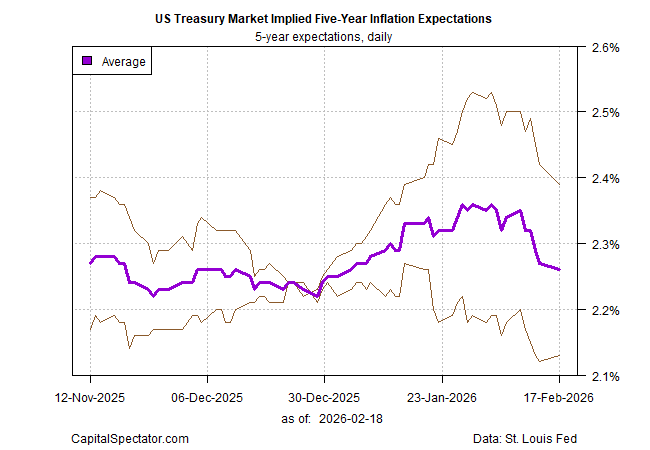

The average of two Treasury-derived inflation gauges now projects five-year inflation in the low 2% range—the mildest reading in a month and not far from the Federal Reserve’s 2% objective. The surge in inflation expectations seen in January has since unwound, signaling that investors have grown less worried about upside inflation risks in recent weeks.

Markets are not infallible, but it would likely require a meaningful upside surprise in the economic data—pointing to renewed inflationary pressure—to overturn the prevailing disinflation narrative. For now, investors show little appetite for betting on a reflationary turn.

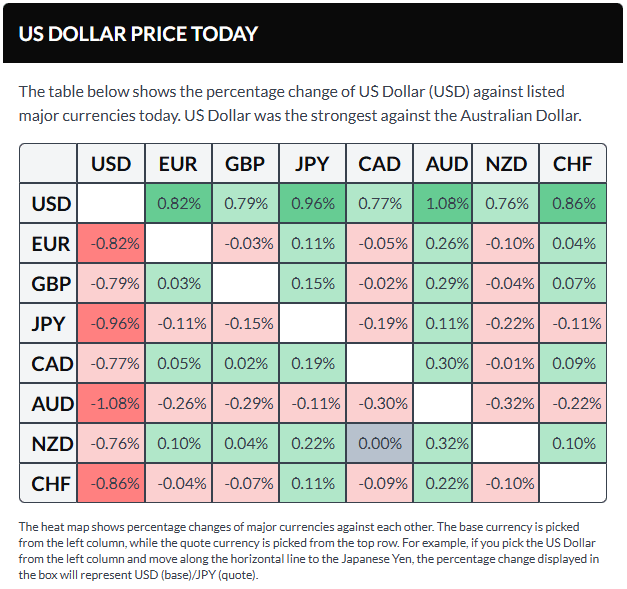

The US Federal Reserve experienced an eventful week. On Monday, it contacted New York–based banks to assess their USD/JPY exposure, sparking speculation that Washington could be coordinating with Japan to address the Japanese Yen’s weakness. This development prompted a sharp sell-off in the US Dollar early in the week.

The Fed’s midweek policy meeting resulted in no change to the federal funds rate, which was kept within the 3.50%–3.75% range, in line with expectations. During his press conference, Chair Jerome Powell avoided questions related to politics, his tenure, and the subpoena. However, he pointed to improving economic momentum and reduced risks to both inflation and the labor market.

The US Dollar Index (DXY) has since rebounded toward the 96.90 level, recovering most of its weekly losses after President Donald Trump nominated former Fed Governor Kevin Warsh as the next Fed Chair on Friday. The nomination now awaits Senate approval. Looking ahead, the US is set to release several key data points next week, including the ISM Manufacturing PMI for January, MBA mortgage applications, Challenger job cuts, and weekly initial jobless claims.

EUR/USD is hovering around the 1.1880 area after the US Dollar rebounded and recovered nearly all of its weekly losses. In the coming week, Hamburg Commercial Bank (HCOB) will release Manufacturing, Services, and Composite PMIs for both Germany and the Eurozone. Additional Eurozone data include the ECB Bank Lending Survey and December Producer Price Index (PPI), while Germany will publish December Factory Orders and Industrial Production figures.

GBP/USD is trading near 1.3600 ahead of the Bank of England’s monetary policy announcement on Thursday. Governor Andrew Bailey’s subsequent press conference is expected to shed further light on the central bank’s outlook for interest rates. UK data releases include the final January S&P Global PMIs and the Halifax House Price Index.

USD/JPY is holding close to the 154.50 level, paring earlier gains after Tokyo CPI data indicated easing inflation in January. Headline inflation slowed to 1.5% year-over-year from 2% in December, while core measures eased to 2%, undershooting forecasts. The softer inflation profile reduces pressure on the Bank of Japan to tighten policy.

USD/CAD is trading around 1.3580, with the Canadian Dollar maintaining a slight edge against the greenback despite data showing economic stagnation in November. Monthly GDP was flat following a 0.3% contraction in the prior month and fell short of expectations for modest growth. Upcoming Canadian releases include January S&P Global PMIs and the Ivey PMI.

Gold is trading near the $4,880 area after surrendering all weekly gains. Prices retreated from a record high of $5,598 as profit-taking emerged and the US Dollar strengthened sharply.

Looking ahead: Emerging views on the economic outlook

Scheduled central bank speakers for the week:

Monday, February 2: – Bank of England’s Breeden – Federal Reserve’s Bostic

Tuesday, February 3: – Federal Reserve’s Barkin

Wednesday, February 4: – Federal Reserve’s Cook

Thursday, February 5: – Bank of England Governor Andrew Bailey – Federal Reserve’s Bostic – Bank of Canada Governor Tiff Macklem

Friday, February 6: – European Central Bank’s Cipollone – European Central Bank’s Kocher – Bank of England’s Pill – Federal Reserve’s Jefferson

Central bank meetings and upcoming data set to influence monetary policy decisions

Key economic data and policy events for the week:

Monday, February 2: – Germany’s December Retail Sales – US ISM Manufacturing PMI

Tuesday, February 3: – Reserve Bank of Australia monetary policy decision – US December JOLTS job openings

Wednesday, February 4: – Eurozone January Harmonized Index of Consumer Prices (HICP) – US January ADP employment report

Thursday, February 5: – Australia’s December trade balance – Eurozone December retail sales – Bank of England monetary policy decision – European Central Bank monetary policy decision

Friday, February 6: – Canada’s January employment change – US January nonfarm payrolls – US February Michigan consumer sentiment

Last week, we kicked off a broad review of the key macro forces shaping the stock market, focusing on the health of the economy and earnings expectations. The takeaway was clear: the economy appears to be in solid shape, and consensus forecasts for earnings growth this year are not just positive, but notably strong.

Admittedly, there has been no shortage of headlines and market volatility since then. It would be reasonable to dive into geopolitical developments, market breadth, or the current state of the AI trade. However, at least for now, none of these factors have altered the market’s primary trend. With that in mind, it makes sense to continue our top-down assessment of the major macro drivers.

Having already examined the economy and earnings, the remaining areas to address are inflation, Federal Reserve policy and interest rates, and market valuations. Let’s turn to those next.

What Is Inflation?

The Federal Reserve defines inflation as a sustained rise in the prices of goods and services over time, reflecting a general increase in the overall price level across the economy. Similarly, Investopedia and standard economics textbooks describe inflation as a gradual erosion of purchasing power, manifested through a broad-based increase in the prices of goods and services over time. The International Monetary Fund frames inflation as the pace at which prices rise over a given period, indicating how much more costly a representative basket of goods and services has become.

Or, as I was taught in my very first economics class many years ago, inflation can be summed up as “too much money chasing too few goods.”

In Focus

There is little doubt that inflation has dominated the attention of the Federal Reserve, policymakers, consumers, and financial markets for several years. Unless one has been completely disconnected from events, it is well known that inflation surged in the aftermath of the COVID crisis, driven by trillions of dollars in government stimulus flowing into household bank accounts and severe disruptions across global supply chains.

This surge fueled fears that the United States was heading back toward the inflationary turmoil of the 1970s—a period the Fed ultimately subdued, but only at significant cost to the economy. With the Consumer Price Index approaching double-digit territory in early 2022, such concerns were understandable.

As the pandemic faded and supply chains normalized, inflationary pressures also began to ease. By early 2024, CPI readings had fallen back near pre-pandemic levels, when face coverings were not yet a cultural norm. The key question now is whether the inflation spike has been fully brought under control.

While corporate pricing strategies and consumer behavior—both central drivers of inflation—are inherently difficult to forecast, it remains possible to analyze the components of the CPI and examine the historical forces that have shaped inflation trends.

A Framework for Understanding Inflation

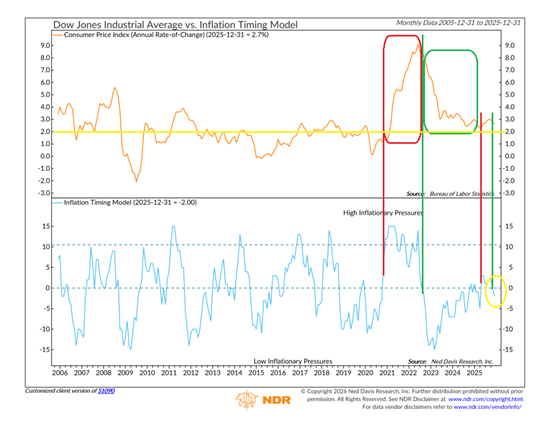

Unsurprisingly, the team at Ned Davis Research Group has already taken this step. In short, there is indeed a model that addresses this—shown below.

The upper chart shows the Consumer Price Index, which represents the inflation rate, while the lower chart displays NDR’s Inflation Timing Model. Reading the model is fairly intuitive. When the blue line rises above zero, it signals that inflation pressures are likely increasing. Historically, readings above 10 have coincided with periods when inflation was significantly above normal levels.

The red box highlights the CPI period from late 2020 through early 2022. During that phase, the model effectively flagged the acceleration in inflation and warned that conditions were set to deteriorate. The model also performed well in the opposite direction in the fall of 2022. While widespread concern about inflation persisted, the model correctly indicated that inflation was poised to ease—and it did.

That downtrend continued until late 2024 or early 2025, when the model briefly suggested inflation was no longer moving in the right direction. However, the signal proved temporary, as the model dropped back below the zero line by the end of 2025. Encouragingly, recent data has validated the model’s current reading, with price pressures generally moderating and the inflation rate falling back below 3%.

Is 3% Becoming the New Inflation Norm?

Inflation skeptics are quick to push back against my relatively calm view, pointing out that inflation remains well above the Federal Reserve’s stated 2% target. From that perspective, they argue the Fed is unlikely to turn accommodative anytime soon. While this logic is understandable, it overlooks two important points: first, the Fed operates under a dual mandate, and second, its preferred inflation gauge—core PCE—differs from the inflation measures most often highlighted in the media.

Crucially, inflation is not the Fed’s sole concern. Maintaining a healthy labor market is equally central to its mission. As a result, the Federal Open Market Committee must carefully balance inflation pressures against broader economic conditions.

This helps explain why the Fed has been cutting interest rates even as inflation remains above target. The labor market has shown signs of weakening, prompting policymakers to act. Equity bulls have welcomed these moves, mindful of the long-standing adage that it rarely pays to fight the Fed. With rates coming down, investors have largely aligned with the bullish camp.

That said, it’s important to recognize that the Fed is not engaged in an aggressive stimulus campaign. Chair Jerome Powell and his colleagues are not attempting to jump-start the economy. Instead, they are seeking to bring interest rates back toward a more neutral, “normal” level—one that balances inflation with labor market stability.

In this context, the prevailing view is that the Fed is willing to tolerate inflation running somewhat above its 2% target while it works to shore up employment conditions. From that standpoint, an inflation rate around 3% may be acceptable—for the time being.

In Summary

The encouraging takeaway is that history suggests a modest amount of inflation can actually be beneficial—supporting stock prices, home values, and corporate earnings. From that perspective, inflation does not appear to be a headwind for equities at present. While this may not be a classic “don’t fight the Fed” environment, the central bank is also not acting as an adversary. As a result, my view is that investors can remain on the bullish path—for now.

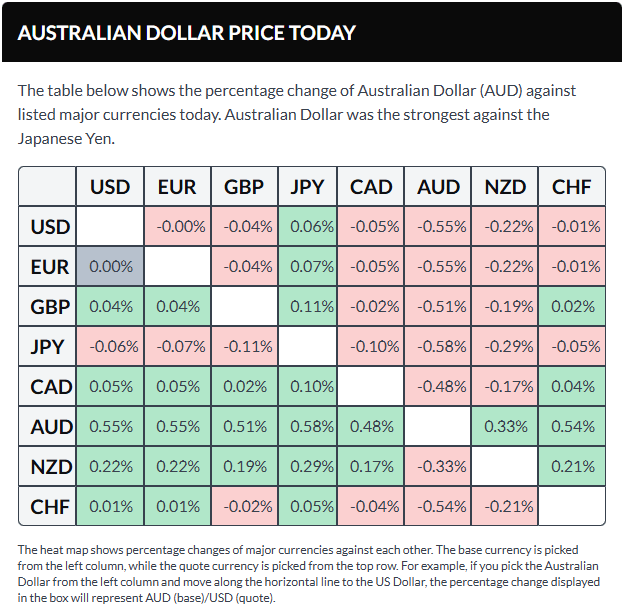

The Australian dollar moved higher after stronger-than-expected employment data reinforced expectations of a tighter policy stance from the Reserve Bank of Australia. Seasonally adjusted employment in Australia increased by 65.2K in December, while the unemployment rate declined to 4.1%. Meanwhile, the U.S. dollar firmed after Bloomberg reported that President Trump would pause tariffs on European countries opposing his push over Greenland.

The Australian dollar strengthened against the U.S. dollar on Thursday after seasonally adjusted employment data from Australia reinforced expectations of a tighter monetary policy stance by the Reserve Bank of Australia. Data from the Australian Bureau of Statistics showed employment rose by 65.2K in December, reversing a revised loss of 28.7K jobs in November and well above the market forecast of a 30K increase. Meanwhile, the unemployment rate fell to 4.1% from 4.3%, beating expectations of 4.4%.

Sean Crick, head of labour statistics at the ABS, noted that a rise in employment among people aged 15–24 helped lift overall employment levels and contributed to the drop in the unemployment rate. Meanwhile, the International Monetary Fund has called on the RBA to proceed cautiously, pointing out that inflation has remained above the Bank’s 2%–3% target range for an extended period, despite headline CPI easing faster than expected in November.

U.S. dollar rises as Trump eases tariff threats against Europe

The U.S. Dollar Index (DXY), which tracks the greenback against six major currencies, was steady after posting modest gains in the previous session, trading around 98.80 at the time of writing. The dollar found support after Bloomberg reported on Wednesday that President Donald Trump said he would step back from imposing tariffs on goods from European countries opposing his bid to take control of Greenland. Earlier, Trump had insisted there was “no going back” on his ambitions for Greenland and had threatened to impose new 10% tariffs on eight European Union nations.

Trump also stated that the United States and NATO had “established the framework of a future deal on Greenland,” though he provided no details, leaving the scope and substance of the proposed agreement unclear.

U.S. labor market data has pushed expectations for further Federal Reserve rate cuts back to June, with Fed officials signaling little urgency to ease policy until there is clearer evidence that inflation is moving sustainably toward the 2% target. Morgan Stanley analysts revised their 2026 outlook, now projecting one rate cut in June and another in September, compared with their earlier expectations for cuts in January and April.

In Asia, the People’s Bank of China announced on Tuesday that it would keep its Loan Prime Rates unchanged, with the one-year and five-year LPRs remaining at 3.00% and 3.50%, respectively. Developments in China remain important for the Australian dollar, given the close trade relationship between the two economies.

China’s industrial production grew 5.2% year-on-year in December, accelerating from 4.8% in November, supported by resilient export-led manufacturing. However, retail sales increased just 0.9% year-on-year, falling short of expectations of 1.2% and slowing from November’s 1.3%.

In Australia, the TD-MI Inflation Gauge rose to 3.5% year-on-year in December from 3.2%, while monthly inflation jumped 1.0%, the fastest pace since December 2023 and a sharp acceleration from 0.3% in the previous two months.

RBA policymakers acknowledged that inflation has eased significantly from its 2022 peak, but recent data points to renewed upward pressure. Headline CPI slowed to 3.4% year-on-year in November, the lowest level since August, yet remains above the RBA’s 2–3% target range. Trimmed mean CPI edged down to 3.2% from 3.3% in October.

The RBA assessed that inflation risks have modestly tilted to the upside, while downside risks—particularly from global factors—have eased. Policymakers expect only one additional rate cut this year, with underlying inflation projected to stay above 3% in the near term before easing toward around 2.6% by 2027.

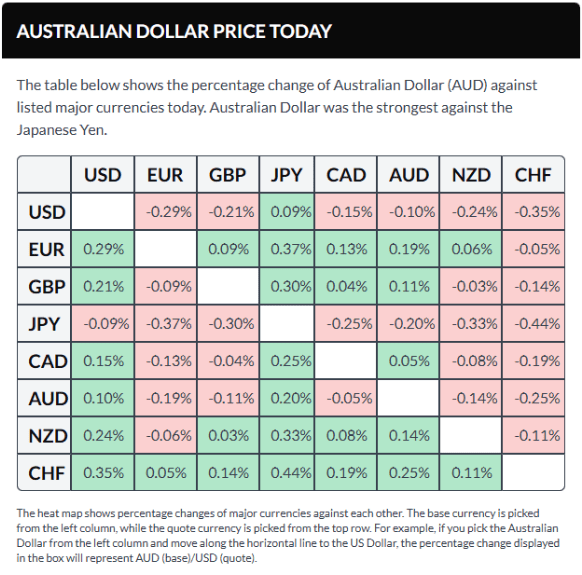

Australian dollar tests the 0.6800 level near the top of its ascending channel

AUD/USD was trading near 0.6790 on Thursday. Daily chart signals show the pair continuing to climb within an ascending channel, reflecting a sustained bullish bias. The nine-day exponential moving average remains above the 50-day EMA, with prices holding above both indicators, reinforcing the positive momentum and keeping upside pressure intact. Meanwhile, the 14-day Relative Strength Index stands at 69.93, close to overbought territory, suggesting momentum is becoming stretched.

The pair is currently challenging immediate resistance at the psychological 0.6800 level, followed by the upper boundary of the ascending channel near 0.6810. A decisive break above the channel could open the door to 0.6942, marking the highest level since February 2023.

On the downside, initial support is seen at the nine-day EMA around 0.6732. A move below this short-term support would undermine bullish momentum, bringing the lower boundary of the ascending channel near 0.6680 into focus, ahead of the 50-day EMA at 0.6656.

Jerome Powell’s eight-year leadership at the Federal Reserve is ending amid significant challenges for the U.S. central bank and divided opinions among policymakers about the right approach to monetary policy. So, what might Powell’s last moves as Chair look like in this environment?

The labor market is still slightly weaker than full employment. Private sector job growth has stalled recently, and although the unemployment rate dropped a bit in December, it remains above what most economists consider the long-term natural rate.

On the inflation front, recent data are more promising. Core CPI inflation fell to 2.6% year-over-year in December from 3.1% in August. Some temporary shutdown effects may be lowering this figure by about 0.1 percentage points, and the Fed’s preferred inflation gauge, the PCE deflator, likely hasn’t improved as much. However, the overall trend for core inflation entering 2026 is clearly downward.

Given this, the Federal Open Market Committee (FOMC) likely has room to continue guiding the federal funds rate toward a neutral level in the near term. The forecast remains two quarter-point rate cuts in March and June, with the rate then holding steady at 3.00%-3.25%.

However, the opportunity for further rate reductions is narrowing. Fiscal stimulus from the recent One Big Beautiful Bill Act is expected to start boosting the economy by spring or summer. Additionally, tariff risks seem to be declining, which could also spur faster growth later in the year. The recent 75 basis points of rate cuts over the past three months will likely provide some support as well.

If labor market and inflation indicators show signs of overheating in the coming months, Powell and the FOMC might opt to pause policy adjustments and leave things steady for the next Chair. This successor could face skepticism from a committee under pressure from the Trump administration. The expectation of stronger economic growth in spring and summer further supports holding rates steady.

For now, the current forecast stands, but there is growing risk that rate cuts may be delayed or reduced compared to the baseline prediction.

WASHINGTON — On January 12, former Federal Reserve chairpersons strongly condemned the ongoing U.S. criminal investigation into current Fed Chair Jerome Powell, describing it as an “unprecedented attempt” to undermine the central bank’s independence.

Two Republican senators also criticized the Trump administration and questioned the Justice Department’s credibility in pursuing charges against Powell, whom President Trump has long aimed to replace amid his push for lower interest rates.

On January 11, Powell disclosed that the Federal Reserve had received grand jury subpoenas and faced threats of a criminal indictment related to his Senate testimony from June.

The controversy centers on a $2.5 billion (S$3.2 billion) renovation project for the Federal Reserve’s headquarters. In 2025, President Donald Trump suggested he might dismiss Chair Jerome Powell due to cost overruns related to the historic building’s refurbishment.

On January 12, former Fed Chairs Ben Bernanke, Alan Greenspan, and Janet Yellen, along with other ex-economic leaders, publicly criticized the Department of Justice’s investigation.

In a joint statement, they condemned the probe as “an unprecedented attempt to use prosecutorial attacks” aimed at undermining the Fed’s independence.

The statement added, “This is typical of how monetary policy is conducted in emerging markets with fragile institutions, often resulting in severe inflation and broader economic dysfunction.”

“Such practices are unacceptable in the United States.”

In an unusual statement on January 11, Mr. Powell criticized the administration, calling the building renovation and his congressional testimony mere “pretexts.” “The possibility of criminal charges stems from the Federal Reserve’s commitment to set interest rates based on its best judgment of the public’s interest, rather than aligning with the president’s preferences,” Powell stated.

He pledged to perform his duties “without political fear or favor.”

Separately, New York Fed President John Williams noted that historically, political interference in monetary policy often results in “unfortunate” consequences such as inflation.

Stocks Reach New All-Time Highs

Despite concerns triggered by the investigation, U.S. stock indices closed at record highs.

Bernard Yaros, lead U.S. economist at Oxford Economics, noted, “The fact that market-based inflation expectations have stayed steady suggests that investors are largely dismissing the probe as having little or no effect on the Fed’s independence.”

The Federal Reserve operates independently with a dual mandate to maintain price stability and low unemployment. Its primary tool is adjusting the benchmark interest rate, which influences U.S. Treasury yields and borrowing costs.

President Trump has frequently criticized Powell, labeling him a “numbskull” and “moron” for the Fed’s policy choices and not cutting rates more aggressively.

On January 12, White House spokeswoman Karoline Leavitt told Fox News that Powell “has proven he’s not very good at his job.” Regarding whether Powell is a criminal, she added, “That’s a question the Department of Justice will have to answer.”

Republicans Push Back Against Investigation

The Justice Department’s investigation has faced backlash from across the political spectrum.

On January 11, Republican Senator Thom Tillis, a member of the Senate Banking Committee, pledged to block the confirmation of any Federal Reserve nominee—including the next Fed chair—until the legal issue is “fully resolved.”

He stated, “The independence and credibility of the Department of Justice are now at stake.”

Another Republican senator, Lisa Murkowski of Alaska, backed Thom Tillis’ stance, describing the investigation as “nothing more than an attempt at coercion.”

Earlier, Senate Majority Leader Chuck Schumer, a leading Democrat, criticized the probe as an assault on the Federal Reserve’s independence.

David Wessel, a senior fellow at the Brookings Institution, warned of serious risks if the Fed were to come under President Trump’s influence.

Politicians might be tempted to keep interest rates low to stimulate the economy before elections, while an independent Fed is expected to set policy focused on controlling inflation and maximizing employment.

Wessel told AFP that if Trump succeeds in swaying the Fed, the U.S. could face higher inflation and reduced willingness from global investors to finance the Treasury.

Powell was originally nominated as Fed chair by Trump during his first term. His chairmanship ends in May, but he may remain on the Fed board until 2028. In 2025, Trump also attempted to remove Fed Governor Lisa Cook over allegations of mortgage fraud.

The Australian Dollar ended its three-day slide on Monday.

ANZ reported a 0.5% decline in job advertisements for December, following a revised 1.5% drop in the previous month.

Meanwhile, the US Dollar weakened after federal prosecutors launched a criminal investigation into Federal Reserve Chair Jerome Powell.

The Australian Dollar (AUD) gained ground against the US Dollar (USD) on Monday, reversing a three-day losing streak. The AUD/USD pair rose as the Greenback weakened, partly due to growing concerns about the Federal Reserve.

Federal prosecutors have launched a criminal investigation into Fed Chair Jerome Powell, focusing on the central bank’s renovation of its Washington headquarters and allegations that Powell may have misled Congress about the project’s details, according to a New York Times report on Sunday.

ANZ Job Advertisements fell by 0.5% in December, following a revised 1.5% decline in November. Meanwhile, household spending rose 1.0% month-on-month in November 2025, slowing from a revised 1.4% increase in October, reflecting consumer caution amid high interest rates and ongoing inflation.

Australia’s mixed Consumer Price Index (CPI) report for November has left the Reserve Bank of Australia’s (RBA) policy direction uncertain. However, RBA Deputy Governor Andrew Hauser stated that the inflation data largely met expectations and indicated that interest rate cuts are unlikely in the near term. Attention now turns to the quarterly CPI report due later this month for clearer insight into the RBA’s upcoming policy decisions.

US Dollar Slides Amid Federal Reserve Uncertainty

The US Dollar Index (DXY), which tracks the Dollar against six major currencies, is weakening and trading near 98.90 amid expectations of a dovish Federal Reserve. Slower-than-anticipated US job growth in December suggests the Fed may keep interest rates steady at its upcoming January meeting.

US Nonfarm Payrolls increased by 50,000 in December, below November’s revised 56,000 and the expected 60,000. Meanwhile, the unemployment rate fell to 4.4% from 4.6%, and average hourly earnings rose to 3.8% year-over-year from 3.6%.

CME Group’s FedWatch tool shows about a 95% chance that the Fed will hold rates steady on January 27–28. Richmond Fed President Tom Barkin welcomed the unemployment drop, describing job growth as modest but steady. He noted hiring remains limited outside healthcare and AI sectors and expressed uncertainty about whether the labor market will see more hiring or layoffs going forward.

US Treasury Secretary Scott Bessent told CNBC on Thursday that the Federal Reserve should continue cutting interest rates, emphasizing that lower rates are the “only ingredient missing” for stronger economic growth and urging the Fed not to delay.

The US Department of Labor reported that Initial Jobless Claims rose slightly to 208,000 for the week ending January 3, just below expectations of 210,000 but above the previous week’s revised 200,000. Continuing claims increased to 1.914 million from 1.858 million, signaling a gradual rise in those receiving unemployment benefits.

The Institute for Supply Management (ISM) revealed that the US Services PMI climbed to 54.4 in December from 52.6 in November, surpassing expectations of 52.3.

ADP data showed a gain of 41,000 jobs in December, improving from a revised 29,000 job loss in November, though slightly below the expected 47,000. Meanwhile, JOLTS job openings dropped to 7.146 million in November from a revised 7.449 million in October, missing forecasts of 7.6 million.

China’s Consumer Price Index (CPI) increased by 0.8% year-over-year in December, up from 0.7% in November but slightly below the 0.9% forecast. On a monthly basis, CPI rose 0.2%, reversing November’s 0.1% decline. Meanwhile, China’s Producer Price Index (PPI) fell 1.9% year-over-year in December, improving from a 2.2% drop the previous month and slightly beating expectations of a 2.0% decline.

Australia’s trade surplus narrowed to 2.936 billion AUD in November, down from a revised 4.353 billion AUD in October. Exports declined 2.9% month-on-month in November, following a revised 2.8% increase the previous month. Imports edged up 0.2% in November, slowing from a revised 2.4% gain in October.

AUD rebounds, testing upper boundary of rising channel around 0.6700

On Monday, AUD/USD trades near 0.6700 as the pair attempts a rebound toward an ascending channel, indicating a renewed bullish outlook. The 14-day RSI at 58.33 remains above the neutral midpoint, supporting upward momentum.

A sustained move back into the channel would reinforce the bullish trend, potentially pushing the pair toward 0.6766—the highest level since October 2024. Further upside could target the channel’s upper resistance near 0.6860.

Immediate support is found at the nine-day EMA around 0.6700, followed by the 50-day EMA at 0.6631. A break below these levels could open the path to 0.6414, the lowest point since June 2025.

Ankur Banerjee provides a preview of the day ahead in European and global markets. Investors remain focused on the escalating conflict between U.S. President Donald Trump and Federal Reserve Chair Jerome Powell, who is pushing back against attempts to exert political control over the Fed and its interest rate decisions.

Meanwhile, growing turmoil in Iran—where over 500 people have reportedly been killed, according to human rights groups—adds to the geopolitical uncertainties shaping market sentiment at the start of 2026, supporting demand for safe-haven assets.

Markets opened Monday with shocking news that the Trump administration had threatened to indict Powell over his Congressional testimony last summer concerning a Fed building renovation. Powell described this as a “pretext” aimed at increasing political influence over monetary policy.

“This issue centers on whether the Fed can continue setting interest rates based on data and economic realities, or if monetary policy will instead be shaped by political pressure and intimidation,” Powell stated.

The initial market reaction saw the dollar weaken and stock futures decline, although the impact on interest rate policy remains unclear. Gold prices surged past $4,600 per ounce as investors sought refuge.

Despite the unsettling news, market responses were measured, with no signs of panic selling as investors await further clarity on the Fed’s independence and the future path of interest rates.

WASHINGTON, DC – DECEMBER 13: U.S. Federal Reserve Board Chairman Jerome Powell speaks during a news conference at the headquarters of the Federal Reserve on December 13, 2023 in Washington, DC. The Federal Reserve announced today that interest rates will remain unchanged. (Photo by Win McNamee/Getty Images)

Markets may now generally anticipate that the Federal Reserve will yield to Trump’s influence and ease interest rates freely once a new Fed chair takes over after Powell’s term ends in May. Futures pricing currently reflects expectations of two rate cuts this year.

With Japanese markets closed on Monday, no cash trading occurred in Treasuries during Asian hours. Attention will shift to the Treasury market when London trading begins.

Key events that could impact markets on Monday include: Germany’s November current account balance and the euro zone Sentix investor confidence index for January.

The ISM service index suggests potential positive revisions for fourth-quarter GDP growth. On Wednesday, the Institute for Supply Management (ISM) reported that its non-manufacturing service sector index increased to 54.4 in December from 52.6 in November, marking the third consecutive month of expansion and the fastest pace of growth in over a year.

The new orders sub-index rose sharply to 57.9 from 52.9, while business activity climbed to 56 from 54.5. Additionally, new export orders improved to 54.2, up from 48.7 in November. Out of 16 surveyed service industries, 11 showed expansion in December.

Conversely, the ISM manufacturing index fell to 47.9 in December from 48.2 the prior month, continuing its contractionary trend for the tenth straight month (a reading below 50 indicates contraction). Only 2 of 17 manufacturing industries—Electrical Equipment, Appliances & Components, and Computer & Electronic Products—reported growth, likely supported by strong data center demand.

ADP’s December report showed private payrolls increasing by 41,000, missing economists’ expectation of 48,000. This follows a loss of 29,000 private jobs in November, meaning just 12,000 private jobs were created over the last two months. Manufacturing shed 5,000 jobs in December, while education and health services added 39,000, and leisure and hospitality gained 24,000 jobs. Regionally, the West lost 61,000 private sector jobs, while the South led with a gain of 54,000.

Residential investment acted as a 5.1% drag on GDP growth during the second and third quarters. Strengthening GDP going forward will depend largely on stabilizing the residential real estate market, which remains sluggish due to high mortgage rates, rising insurance costs, and an oversupply in several key areas. According to the Intercontinental Exchange, prices for U.S. condominiums dropped 1.9% in September and October, with high homeowners association (HOA) fees and insurance expenses cited as major factors. In nine major metropolitan regions, over 25% of condominiums have fallen below their original sale prices. While multiple Federal Reserve rate cuts could help support home prices, the current weakness is fueling deflationary concerns that the Fed needs to address.

If deflation emerges from (1) weak housing and rental prices, (2) low crude oil prices, and (3) deflation imported from China and other struggling global economies, the Fed may need to implement rapid interest rate cuts totaling around 100 basis points. With President Trump expected to nominate a new Fed Chair soon, current Chair Jerome Powell is likely to become a lame duck. Minutes from the December Federal Open Market Committee (FOMC) meeting indicated at least one more 0.25% rate cut is probable, but any further deflationary signals could prompt the Fed to enact much larger reductions in key rates in the coming months.

President Trump is expected to nominate a new Federal Reserve Chair in January who will likely reverse the Fed’s current restrictive policies and adopt a more pro-business stance. Should Kevin Hassett, the current Chair of the Council of Economic Advisors, be appointed, the Fed would gain a strong economic advocate, a development that many find promising and exciting.